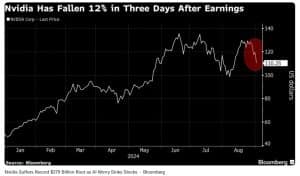

On September 3, NVIDIA faced a shocking $279 billion market cap loss in a single trading day. As concerns over artificial intelligence growth mounted and fears of a U.S. antitrust probe emerged, the chip maker’s stock plummeted by 9.5%. This marked the biggest single-day value loss for a U.S. company in history. While Nvidia’s position as a market leader remains intact, the massive sell-off has prompted deeper questions about AI’s future and stock market volatility.

Inside the Shocking Drop in Nvidia’s Stock Value

NVIDIA’s fall wasn’t just a random market fluctuation, rather it was driven by several key events. Analysts issued warnings that the AI boom might be overstated, sparking fears that its recent stock surge was unsustainable.

Additionally, Bloomberg highlighted the U.S. Department of Justice’s antitrust investigation fueled further concern, leading investors to sell off shares. It also explained that the DOJ probe is still in its early stages, and no formal complaint has been filed yet. The agency is investigating whether Nvidia creates barriers that make it more difficult for customers to switch to other AI chip suppliers.

Bloomberg has thrown light on another reason. Well, the broader market sentiment also played a role in the massive share plummet. Economic uncertainty in China, sluggish U.S. manufacturing data, and inflation worries contributed to a risk-averse environment. Investors, already cautious, were quick to react to the company’s potential regulatory challenges.

AI Rise and Returns, What Investors Are Talking About?

This dramatic decline has sparked considerable skepticism around AI. We discovered from media reports that leading financial analysts like JPMorgan and BlackRock suggest that the AI hype may have reached its peak. It’s a paradox because even though the tech giants survive on AI, they fear real returns from AI investment could take years.

This reality check has forced investors to reevaluate the lofty valuations that have driven tech stocks to near-record levels. Nvidia’s recent earnings report, which failed to meet sky-high expectations, only added to the sense that AI may not deliver quick profits.

However, the stock market is a fickle place, and this record-breaking fall has left a lasting impact. As AI develops, it’s clear that companies like Nvidia will face growing scrutiny, both from investors and regulators.

Despite Dwindling Shares, AI and Data Centers are the Silver Lining

Despite the massive sell-off, Nvidia’s leadership remains optimistic about the company’s future. CEO Jensen Huang reassured investors that Nvidia’s core strengths in AI and GPU technology will continue to drive growth. Huang pointed to Nvidia’s strategic partnerships and product innovations as evidence that the company is well-prepared to bounce back.

Betting on energy efficiency

From an NVIDIA blog, we discovered its newly introduced CUDA-powered accelerated computing is transforming industries by drastically reducing energy use while boosting performance. By migrating from traditional CPUs to energy-efficient GPUs, companies are seeing up to 66x faster processing speeds and massive energy savings. This shift is particularly important for data-heavy tasks like AI, 6G research, and scientific computing.

The benefits extend beyond speed. NVIDIA estimates that if all AI, high-performance computing (HPC), and data analytics workloads switched to GPUs, data centers could save up to 40 terawatt-hours of energy annually. That’s equivalent to the energy used by 5 million U.S. homes each year.

Source: NVIDIA

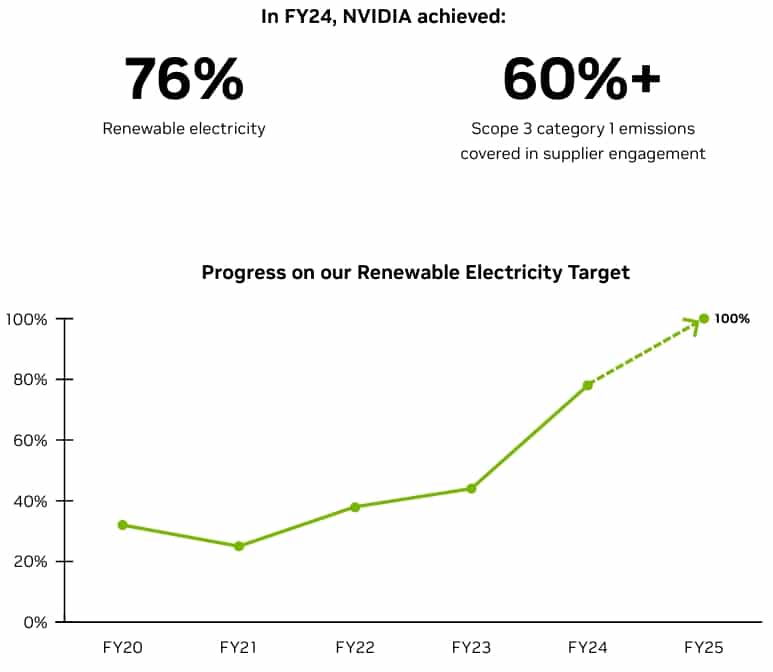

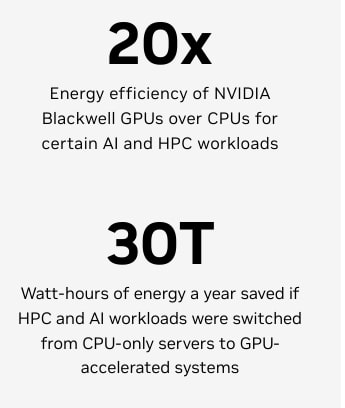

The blog has given utmost significance to the sustainability factor that these GPUs are promising. They explain GPU acceleration offers around 20x more energy efficiency than CPUs. It achieves this by finishing tasks faster and entering a low-power state, thereby cutting total energy use while maintaining top performance.

Source: NVIDIA

For instance,

“The NVIDIA GB200 Grace Blackwell Superchip is estimated to offer 25X better energy efficiency over the prior Hopper generation for massive LLMs, while CPUs have not demonstrated an ability to effectively run larger or massive LLMs.”

Over the past decade, NVIDIA’s AI computing has seen a 100,000x improvement in energy efficiency, helping businesses meet sustainability goals. Moreover, companies running workloads on NVIDIA’s platform experience 10-180x speed improvements across tasks like data processing and computer vision. This has fueled a 154% increase in NVIDIA’s data center revenue year-over-year, driven by strong demand for its Hopper architecture and upcoming Blackwell platform.

As AI models evolve and demand grows, NVIDIA’s energy-efficient solutions will continue to play a key role in reducing the carbon footprint of data centers, supporting a more sustainable future for tech.

Direct Air Capture (DAC) is crucial in the fight against climate change and is identified as a key solution to remove up to 310 billion tons of CO₂ by 2100. However, this demands significant investment in this field. With this motive, two Irish companies, NEG8 Carbon and Carbon Collect have unlocked their innovative DAC technology to combat carbon emissions.

Unleashing NEG8 Carbon’s Advanced DAC Technology to Tackle Carbon Emissions

NEG8 Carbon, a leading carbon capture company in Waterford, Ireland, has introduced major upgrades to its Direct Air Capture (DAC) system. As the company believes that simply cutting emissions will not fully address the problem, their innovative enhancements are making CO₂ capture from the atmosphere more efficient and effective.

How Does It Work?

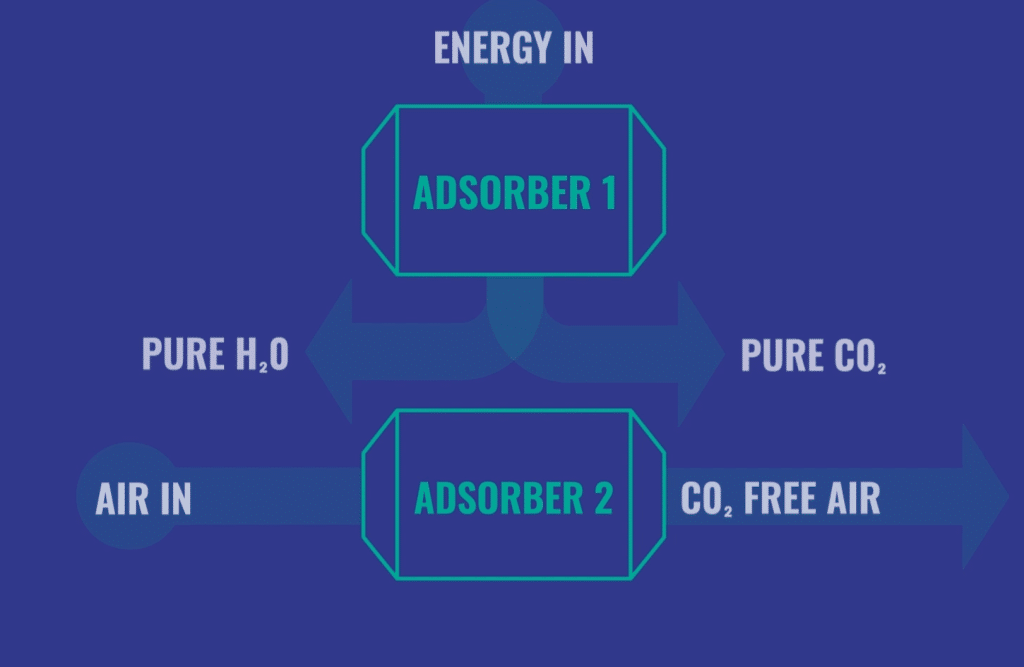

The advanced DAC system operates by pulling in large volumes of air and passing it over specially designed sorbent materials that attract and hold CO₂ molecules. Once captured, the CO₂ can be safely stored underground or transformed into climate-neutral products, like sustainable aviation fuel. This innovative DAC method reduces sorbent by 80%.

Furthermore, their blueprint DAC system speeds up the CO₂ capture process and cuts regeneration time by 90%. Additionally, an improved heat exchange process boosts CO₂ uptake by 50% and lowers energy use by more than 20%. All these upgrades make the system more efficient and eco-friendlier.

“Plug and play” CO2 capture units.

We discovered something interesting from NEG8’s official website. They have made DAC widely accessible through modular, ‘plug and play’ carbon capture units. These units can be deployed almost anywhere. They are an integral part of the company’s vision to roll out millions of devices globally, capturing billions of tons of CO₂ ten years down the line.

The existing NEG8 Carbon system is a compact and modular solution for capturing CO2. Each module captures up to 400 tons of CO2 annually. Additionally, multiple modules can be stacked together at a site to enhance capacity.

Notably, the company focuses on reducing the cost per ton of CO₂ captured with these groundbreaking modular systems.

Dr. John Breen, CTO of NEG8 Carbon, said,

“These innovations are making significant improvements to our Direct Air Capture technology. They enhance both efficiency and sustainability, reinforcing our dedication to providing effective solutions in the fight against climate change.”

How the NEG8 Carbon Technology Works

Moving on, NEG8 Carbon has a robust plan for its global climate targets. By the end of this year, the company plans to test its latest innovations in a demo unit, with full deployment set for 2026. By 2035 it aims to install 25,000 DAC units across Ireland, aiming to capture 10 mtCO₂ annually. These efforts will further push the company to capture 100 mtCO₂ annually by 2050, at a global scale.

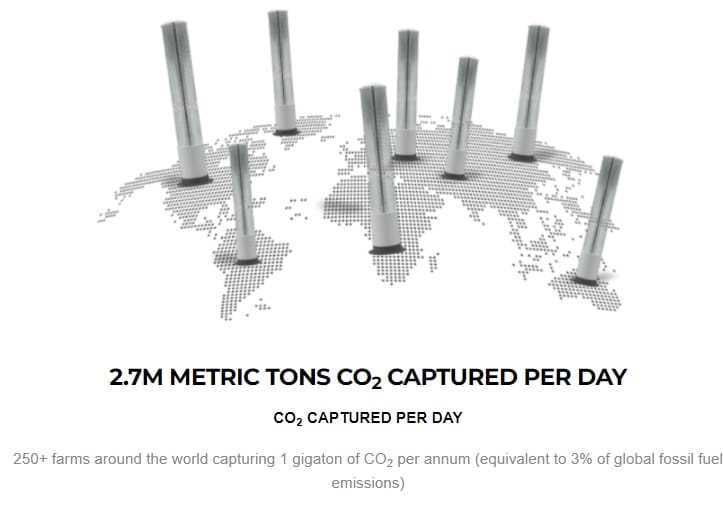

Carbon Collect Unveils Next-Gen Direct Air Capture Technology to Slash Costs

Carbon Collect, a leader in direct air capture (DAC) technology, has introduced its second-generation MechanicalTree, designed to capture CO2 directly from the atmosphere. This new system enhances the original design by increasing the amount of CO2 captured per unit of energy, thanks to advancements in sorbent materials and regeneration technology.

“The MechanicalTree™ is a thousand times more efficient than natural trees at removing CO2 from the atmosphere” – Carbon Collect

The MechanicalTree operates by simulating photosynthesis, but with engineered materials that absorb CO2 from the air more efficiently. The modular design allows clusters of these systems, known as “carbon farms,” to scale up “vertically” and capture significant amounts of CO2.

A milestone for the DAC industry

The MechanicalTree stands 10m tall and captures CO2 as it is exposed to natural wind. Once saturated, the column is lowered into a regeneration chamber where the CO2 is released and processed. This design is a significant advancement in reducing the high costs associated with conventional DAC, which can range from $250 to $600 per metric ton of CO2.

The company aims to bring this cost below $200 per ton by 2030, with the first installation of the Gen-II MechanicalTree expected by 2024 year-end. They expect commercial deployments beginning in 2025.

Pól Ó Móráin, CEO of Carbon Collect, emphasized that this innovation is a response to market demands and expert collaboration. He added that they are offering a solution that is more efficient, scalable, and cost-effective than anything before.

Early deployments are planned across the US, Europe, and other regions and will play a key role in the Southwest Regional Direct Air Capture Hub. Notably, their first industrial-scale MechanicalTree™ is already operational in Tempe, Arizona. All these scaling efforts are supported by the U.S. Department of Energy.

source: Carbon Collect

In conclusion, both NEG8 Carbon and Carbon Collect have set ambitious goals with their innovative direct air capture technology. Additionally, governments are playing a significant role in supporting this effort, as financial feasibility would otherwise be challenging. The US DOE and the EU have integrated DAC into their climate strategies, aiming for carbon neutrality by 2050.

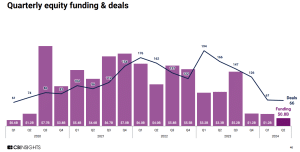

The growing electric vehicle (EV) market has flourished, largely due to strong government support aimed at meeting climate objectives, which has in turn captured the attention of Wall Street investors. This alignment between policy and market interest has driven substantial investment and innovation in the EV sector. However, it’s not that easy to test the waters of the EV technology industry, and several startups have closed down.

This trend is echoed in the CB Insights’ recent Climate Tech Report. The data showed that equity funding and deals for EV tech in Q2 2024 were at the lowest since 2020.

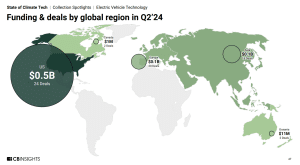

When it comes to the region, U.S. startups got the largest funding and number of deals as seen below. Europe and Asia follow with the same funding amount but the latter comes second for the number of deals.

For the startups that stand out during this quarterly funding, we handpicked the top four per the CB Insights report. Here is what they’re doing, what they’ve accomplished, and what they have to do to help in the clean energy transition.

1. Sila Nanotechnologies: Powering the Future of EVs

Based in the US, Sila Nanotechnologiesbagged almost 50% of the total funding in the sector for the reported quarter. It received a $375 million Series G round from various investors including Sutter Hill Ventures, Bessemer Venture Partners, Coatue, and Perry Creek Capital.

Sila is revolutionizing the electric vehicle (EV) industry with its innovative battery materials that significantly enhance performance and sustainability. Founded in 2011 by former Tesla engineer Gene Berdichevsky, alongside Alex Jacobs and Gleb Yushin, Sila Nano focuses on replacing traditional graphite anodes with silicon-based materials to increase battery efficiency.

Sila Nano’s silicon anode material can increase the energy density of lithium-ion batteries by up to 20%. The innovative material allows for a 15-20% longer driving range or smaller, lighter batteries. This breakthrough directly addresses the range anxiety that many EV users face. Plus, the material releases 50-70% less carbon dioxide per kWh than graphite during production.

From company material

Sila’s technology is scalable and designed to be a drop-in solution for existing battery manufacturing processes, making it easier for automakers to adopt.

In 2021, Sila Nano announced a partnership with BMW to integrate its advanced battery technology into the automaker’s next-generation EVs by 2025. This collaboration is expected to result in vehicles with significantly improved range and charging times.

From company website

The company has raised over $930 million in funding, reaching a valuation of about $3.3 billion, underscoring its potential to reshape the battery industry.

Sila Nano’s silicon-based anode material is a key component of cleaner, more efficient energy storage solutions. By enhancing battery performance, Sila Nano supports the broader adoption of EVs, which are critical to reducing global carbon emissions. The company’s technology also contributes to lowering the overall carbon footprint of battery production by improving energy density and reducing material usage.

Through its cutting-edge innovations, Sila Nanotechnologies is playing a pivotal role in advancing clean energy and accelerating the transition to a sustainable, electrified future.

2. EnviroSpark: Electrifying the Energy Transition with EV Charging Solutions

Another US-based climate tech startup, EnviroSpark received $50 million in EV tech equity funding from Basalt Infrastructure Partners. EnviroSpark is a leading provider of EV charging solutions, dedicated to expanding the accessibility and convenience of EV charging infrastructure.

Image from company website

Founded in 2014 by Aaron Luque, the company focuses on designing, installing, and managing EV charging stations across residential, commercial, and public spaces.

Since its inception, EnviroSpark has installed over 8,800 EV charging stations across the United States and beyond, significantly contributing to the growth of the EV ecosystem. The company has forged partnerships with major utilities, municipalities, and property developers to integrate EV charging solutions into new and existing developments.

EnviroSpark EV charging stations footprint

EnviroSpark’s commitment to quality and innovation has earned them recognition as one of the fastest-growing companies in the EV infrastructure space.

One of the company’s key milestones was securing a contract with Georgia Power, the largest utility in the state of Georgia, to install and maintain EV charging stations across the region. This partnership has expanded EV charging accessibility for thousands of drivers and supports the state’s goal of reducing transportation-related emissions.

EnviroSpark’s charging stations are designed to be energy-efficient and compatible with various renewable energy sources, such as solar power. The company also offers advanced software solutions that enable real-time monitoring, smart energy management, and demand response capabilities, further enhancing the sustainability of its charging infrastructure. By promoting the widespread adoption of EVs, EnviroSpark is helping to reduce GHG emissions and accelerate the transition to clean transportation.

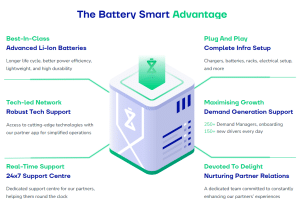

3. Battery Smart: Innovating Battery Swapping for a Greener Future

Hailing from India, Battery Smart got about 6% of the total equity funding for EV tech startups or $45 million. The company attracted a lot of investors during this Series B round, including Acacia Inclusion, Blume Ventures, British International Investment, Ecosystem Integrity Fund, and Panasonic Living Visionary Fund.

Battery Smart is a leading provider of battery-swapping solutions for electric vehicles, dedicated to transforming the EV ecosystem with efficient and scalable energy storage solutions. Founded in 2018, the India-based company focuses on solving the challenges of battery charging and range anxiety through its innovative swapping technology.

Battery Smart has rapidly established itself as a key player in the EV infrastructure space. The company has successfully deployed over 1,000 battery-swapping stations across major Indian cities, including Delhi, Bangalore, and Hyderabad. This extensive network supports a range of two-wheelers and three-wheelers, providing quick and convenient battery swaps to enhance operational efficiency.

One of Battery Smart swapping stations

A significant milestone for Battery Smart was securing a strategic partnership with the Indian government’s National Electric Mobility Mission Plan (NEMMP). This collaboration aims to expand the company’s battery-swapping infrastructure and accelerate the adoption of electric vehicles in the country. Additionally, Battery Smart has raised over $50 million in funding from notable investors, further bolstering its growth and expansion plans.

Battery Smart’s battery-swapping technology offers a sustainable alternative to traditional charging methods. Their stations allow for rapid replacement of depleted batteries with fully charged ones, significantly reducing downtime and increasing the efficiency of EV operations. The company’s approach also supports the integration of renewable energy sources into the charging process, enhancing the overall sustainability of their solutions.

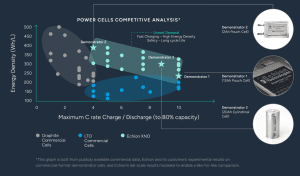

Snatching the fourth rank in total EV tech funding, Echion Technologies received $35 million in Series B from Volta Energy Technologies, BGF, CBMM, and Cambridge Enterprise Ventures. The EV tech startup is at the cutting edge of battery innovation, specializing in the development of advanced materials for lithium-ion batteries.

Founded in 2017, the company is headquartered in the UK and focuses on enhancing battery performance to meet the growing demands of the EV and energy storage markets.

Echion Technologies has made significant strides in improving battery technology with its proprietary niobium-based anode materials. Their innovative materials offer up to 50% higher energy density compared to traditional graphite anodes, translating into longer battery life and extended driving ranges for electric vehicles. This advancement addresses one of the key limitations of current battery technology and supports the broader adoption of EVs.

A key milestone for Echion Technologies was securing a £4.5 million funding round in 2021, led by investors such as Future Planet Capital and Innospark. This funding will accelerate the development and commercialization of their advanced anode materials. The company has also established strategic collaborations with major automotive and energy storage companies to integrate their materials into next-generation batteries.

Echion’s niobium-based anode materials contribute to cleaner energy solutions by increasing battery efficiency and reducing reliance on fossil fuels. Their technology enhances the performance of EV batteries, which supports the transition to electric transportation and reduces GHG emissions. The company’s focus on sustainable materials and energy storage solutions aligns with global efforts to mitigate climate change and promote environmental sustainability.

Charging Ahead to Drive Clean Energy and Green Transportation

Each of the four startups contributes uniquely to the advancement of the EV industry, though they operate in different niches.

Sila Nanotechnologies and Echion Technologies both focus on battery innovation, but they approach it from different angles. Sila is enhancing energy density through silicon anode materials that can integrate seamlessly into existing manufacturing processes. In contrast, Echion’s work on niobium-based anode materials offers even higher energy density, promising longer battery life and extended driving ranges.

EnviroSpark and Battery Smart tackle the EV infrastructure from opposite perspectives. EnviroSpark is building out the EV charging network, making it easier for drivers to access reliable, energy-efficient charging stations. Battery Smart, on the other hand, addresses the issue of charging time with its innovative battery-swapping technology, particularly in India, where fast and efficient solutions are needed to overcome infrastructural constraints.

As the EV market continues to evolve, these top four EV tech startups—Sila Nanotechnologies, EnviroSpark, Battery Smart, and Echion Technologies—are pushing the boundaries of innovation despite the recent slowdown in funding. Their groundbreaking technologies are not only enhancing the performance and accessibility of electric vehicles but also contributing to the broader goal of reducing global carbon emissions.

The path forward may be difficult, but these startups are proving that with the right vision and commitment, the future of clean energy is bright. Together, their efforts are paving the way for a more sustainable and electrified future, each contributing a vital piece to the EV ecosystem puzzle.

TotalEnergies made a historic announcement of partnering with Adani Green Energy Limited (AGEL) to the next level with a new joint venture to develop over 1GW of solar energy in Gujarat, India. This collaboration is part of a broader strategy to boost renewable energy production in India and support global decarbonization efforts.

Unlocking TotalEnergies-Adani JV

This partnership will push Adani Green to develop t a new solar portfolio of 1,150 megawatt alternating current (MWac) in Khavda, Gujarat. Consequently, this initiative will strengthen their existing collaboration and support India’s renewable energy goals.

Notably, the electricity generated will be sold through Power Purchase Agreements (PPAs) with the Solar Energy Corporation of India (SECI) and on the open market. The project aligns with TotalEnergies’ strategy to capitalize on India’s evolving renewable electricity and natural gas market.

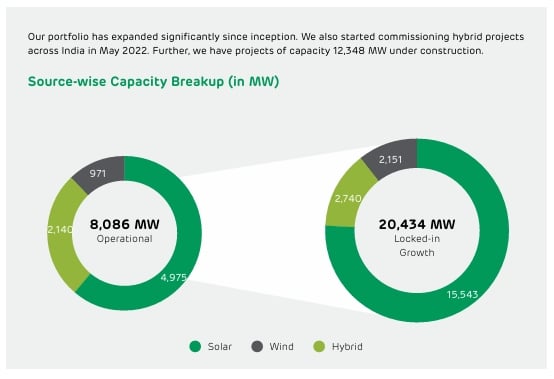

Speaking about the investment, TotalEnergies will invest $444 million with a 19.7% stake in the JV, while Adani Green will contribute assets. Currently, AGEL has 11 GW of solar and wind capacity across India and aims to reach 50 GW by 2030.

Adani’s energy portfolio as per 2023 sustainability report

TotalEnergies is investing significantly in renewable energy and low-carbon solutions. This investment is a testament to this ambitious goal of expanding its electricity generation from renewable sources like wind, solar, bioenergy, and hydropower. In addition, it is also investing in low-carbon mobility infrastructure, including EV charging stations and hydrogen filling stations. It’s current energy portfolio looks like this:

Gross installed capacity of 22 GW for renewable electricity by the end of 2023.

Aims to exceed 100 TWh of net electricity production by 2030 and expand its renewable electricity capacity to 35 GW by 2025.

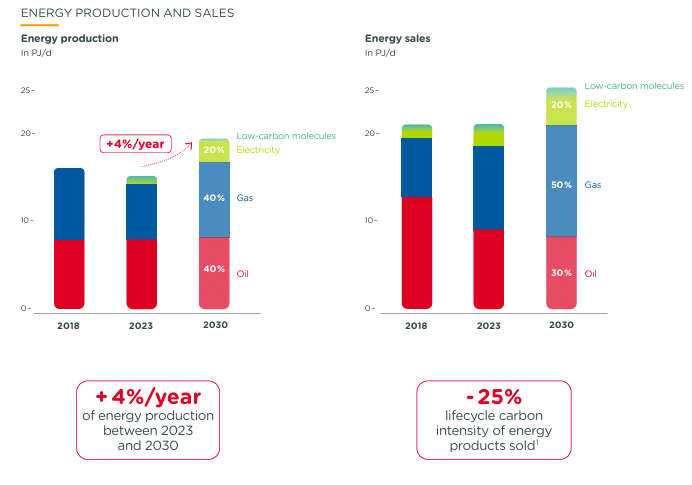

In 2023, the company invested $16.8 billion, allocating 35% of that amount to low-carbon energy. By the end of this year, it aims to invest $17-18 billion, including $5 billion for its growing Integrated Power segment. This commitment highlights the company’s shift to sustainable energy and its efforts to cut carbon emissions while staying profitable.

source: TotalEnergies

TotalEnergies Emissions Reduction Strategy

TotalEnergies is committed to the Paris Agreement’s goal of keeping global temperature rise “well below 2°C.” Thus, the company evaluates every new project for profitability and most importantly its impact on scope 1 and 2 emissions.

Scope 1+2 emissions for new oil and gas projects:

Compared to the average emissions intensity of upstream production or downstream units (like LNG plants or refineries).

As of 2024, the threshold has been lowered to 18 kg CO2e/boe (from 19 kg CO2e/boe), showcasing the company’s progress in reducing emissions.

Concisely, its net zero road map entails making 3x renewable energy, 2x energy efficiency and cutting methane emissions by 2030.

source: TotalEnergies

Adani’s Vision for a Net Zero Future

Their partnership dates back to September 2023, when both companies signed a binding agreement for the joint venture.

The portfolio included 1,050 MW, with 300 MW already operational, 500 MW under construction, and 250 MW in development. At that time, TotalEnergies invested $300 million in Adani Green, acquiring a 50% stake in the solar and wind projects.

The press release further reveals that this project in Khavda is part of Adani’s larger ambition to develop the world’s largest renewable energy site, which will span 538 km² and generate 30 GW of power once fully operational. With robust efforts and investments, the energy giant will turn Khavda into a key landmark on India’s net zero path.

source: Adani

Thus, we can see that Adani’s every move aligns with the country’s decarbonization efforts. With this goal intact, they mitigated 36.7 MT of CO2 and generated 3.9 million carbon credits in the previous financial year. Overall, TotalEnergies, recognizing India as a key market for its renewable and natural gas ventures, will play a significant role in Adani’s mammoth energy expansion plan.

On August 20, PETRONAS, ADNOC, and Storegga signed the Joint Study and Development Agreement (JSDA) to assess the CO2 storage potential of saline aquifers and develop carbon capture and storage (CCS) facilities in the Penyu basin of Malaysia.

Unlocking the PETRONAS, ADNOC, and Storegga CCS Project

The initiative aims to achieve a CCS capacity of at least 5 million tons annually by 2030. The agreement outlines the following plans:

Conduct CO2 shipping and logistics study, along with geophysical and geomechanical modeling, reservoir simulation, and containment research.

The partners will explore the scope of CCS using advanced technologies like AI to optimize storage capacity.

“This agreement with ADNOC and Storegga will potentially allow us to build our capability to develop and de-risk saline aquifers as carbon dioxide storage sites by leveraging on our partners’ expertise and experience in other regions. This strategic partnership aligns with PETRONAS’ overarching goal of establishing Malaysia as a regional CCS hub to serve Asia Pacific where it may build up the storage capacity through saline aquifers. This also demonstrates our earnestness in establishing the right pace to deliver CCS hubs here while also contributing to the national climate target.”

Bolstering Ties for a Low-Carbon Future

The Penyu basin is located offshore Peninsular of Malaysia. The country’s rich geological resources, particularly its deep saline aquifer reservoirs, provide an excellent opportunity for large-scale, permanent CO2 storage solutions. Consequently, this agreement is set to boost CCS facilities in the region, helping to create a hub that will support both local and international efforts to reduce emissions.

Nora’in Md Salleh further emphasized Malaysia’s interest in enhancing economic partnerships with the UAE. The collaboration will focus on various sectors, including renewable energy, innovation, and infrastructure. She further noted that the JSDA aligns with the Malaysia-UAE Joint Committee for Cooperation (JCC) framework, thereby building a strong relationship between PETRONAS and ADNOC.

Milestones of the MOU Between Storegga and PETRONAS

Storegga Limited is a UK-based company, focused on developing decarbonization projects like CCS, CCUs, DACs, and hydrogen projects both in the UK and internationally. As a private company, Storegga is backed by investors such as GIC, Mitsui & Co., Ltd., M&G Investments, Macquarie Group, and Snam. Notably, Storegga is the lead developer of the Acorn Carbon Capture and Storage and Hydrogen project in Aberdeen, Scotland.

Moving on, The MOU between Storegga and PETRONAS outlines a two-phase collaboration:

Phase 1: The companies will jointly develop a commercial strategy for CCS. They aim to identify key enablers and drivers for launching CCS hub and cluster projects in Malaysia or the region, with potential international expansion. This phase also includes:

Sharing knowledge on the global CCS landscape

Evaluating CCS economics and business models

Creating integrated solutions for emitters

Phase 2: Jointly they will explore partnerships on CCS and related projects both in Malaysia and internationally. This phase may also involve developing projects connected to CCS, such as Direct Air Capture (DAC).

Dr Nick Cooper, CEO at Storegga, said:

“CCS is a vital tool. A reverse carbon cycle at scale is urgently needed to reduce and remove CO₂ from the atmosphere. We are looking forward to working with PETRONAS in Malaysia and beyond to catalyze CCS hubs and clusters. These hubs will accelerate the development of important carbon reversal technologies such as direct air capture. We have one atmosphere – it is vital that countries around the world work together to reduce and remove CO₂. We are excited that this relationship also expands Storegga’s global presence and utilizes our capabilities to support Asia’s progress towards decarbonization.”

Thus, Storegga’s involvement is crucial due to its pioneering role in advancing CCS globally.

PETRONAS Leads the Way for Malaysia’s Net Zero with CCS Innovation

PETRONAS, a key player in Malaysia’s National Energy Transition Roadmap (NETR), has identified CCS as vital to achieving the nation’s sustainability goals. The Malaysian Government plans to introduce a standalone CCUS bill by year-end to support these efforts.

Aiming for net zero carbon emissions by 2050, PETRONAS is capping Malaysia’s operational emissions at 49.5 mtCO2e by 2024 and reducing Groupwide emissions by 25% by 2030. Guided by its Energy Transition Strategy, PETRONAS balances current energy needs with climate goals, investing in new technologies and sustainable practices to drive the transition to a low-carbon future.

Source: Petronas

Emry Hisham Yusoff, Head of Carbon Management at PETRONAS, shared his thoughts on the MOU, stating that the partnership will explore the commercial aspects and surrounding factors needed to develop the CCS value chain in Malaysia and the region. This move will bring PETRONAS closer to establishing Malaysia as a leading regional hub for CCS solutions.

He emphasized that this partnership supports PETRONAS’ goal of building a sustainable portfolio and advancing the shift to lower-carbon energy.

ADNOC’s World-Class CCS Technology Powers the Partnership

ADNOC is ramping up its decarbonization efforts by doubling its CCS capacity to 10 million tons annually by 2030. Additionally, it aims to achieve net zero in scope 1 and 2 emissions by 2045. Last year in September, ADNOC approved the Habshan CCS project, one of the largest in the Middle East and North Africa, which will store 1.4 million tonnes of CO2 each year in deep underground formations.

Following this, ADNOC greenlit the Hail and Ghasha project, targeting net zero CO2 emissions with a capacity to capture 1.5 million tons of CO2 annually. Over 60% of the investment in this project will boost the UAE’s economy through ADNOC’s In-Country Value program.

Additionally, ADNOC partnered with Carbon Clean, a UK-based company, to deploy the world’s first modular CycloneCC unit in Abu Dhabi, designed to save time, capital, and energy compared to traditional carbon capture methods.

In this context, Hanan Balalaa, ADNOC Senior Vice President for New Energies, said

“Carbon capture is an important tool to responsibly reduce carbon emissions and ADNOC will continue to develop this technology as we work towards our Net Zero by 2045 goal. We are committed to working with trusted global partners like PETRONAS and Storegga to develop and utilize global carbon management hubs, enabling our customers to reduce their emissions and supporting their decarbonization goals.”

source: ADNOC

The project, set to begin by the end of the year, holds great promise for Malaysia. It marks a significant step forward in the country’s mission to become a leader in CCS and other decarbonization efforts.

TotalEnergies announced a significant $100 million investment in sustainable forestry projects in the United States. This strategic initiative is a collaboration with Anew Climate, a leader in climate solutions, and Aurora Sustainable Lands, a company specializing in carbon stewardship and forest management.

The partnership aims to protect productive forests from extensive timber harvesting, promote sustainable management practices, and enhance the forests’ capacity to sequester carbon from the atmosphere.

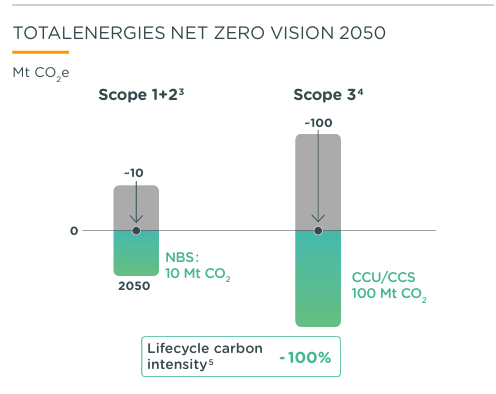

Beyond Emissions: TotalEnergies’ Bold Move Towards Net Zero

The $100 million investment will support Improved Forest Management (IFM) practices across 300,000 hectares of forested land in 10 U.S. states. These include Arkansas, Florida, Kentucky, Louisiana, Michigan, Minnesota, New York, Virginia, West Virginia, and Wisconsin.

The projects will focus on reducing timber harvesting to preserve natural carbon sinks, improving water and soil quality, protecting biodiversity, and conserving natural habitats. The carbon credits generated from these activities will be acquired by TotalEnergies and retired after 2030.

The investment is part of TotalEnergies’ commitment to spend $100 million annually on nature-based solutions capable of generating at least 5 million metric tons of CO2e in carbon credits each year by 2030. The forest carbon credits will help the oil major offset a portion of its direct Scope 1 and 2 emissions as part of its broader climate strategy.

Scope 1+2 Emissions Reduction by 2030

From TotalEnergies Climate 2024 Progress Report

TotalEnergies has committed to a vision of becoming a net-zero energy company by 2050, a goal that aligns with the International Energy Agency’s net-zero pathway. As part of this strategy, the company aims for a 40% reduction in net Scope 1 and 2 emissions by 2030 compared to 2015 levels.

To achieve these ambitious goals, TotalEnergies plans to spend the next decade developing the necessary projects and capabilities.

In addition to nature-based solutions, the energy company is also focusing on a combination of carbon capture and storage (CCS) technologies and e-fuels to potentially avoid up to 100 million tons of CO2 per year.

One of the key initiatives supporting this vision is the CO2 Fighters Squad, a dedicated team established in late 2018. This team is responsible for monitoring GHG emissions across the company and promoting a low-carbon mindset. Their work includes initiating energy efficiency projects, accelerating the electrification of facilities, and introducing greener energy consumption methods.

By 2025, the CO2 Fighters Squad is expected to oversee 160 upstream and more than 200 downstream projects, resulting in significant reductions in Scope 1 and 2 emissions. These efforts are part of TotalEnergies’ broader commitment to sustainability and its strategic pivot towards cleaner energy sources.

Advancing Climate Action Through Nature

TotalEnergies’ investment is closely aligned with the U.S. government’s Voluntary Carbon Markets Principles, which emphasize integrity, transparency, and environmental protection in carbon trading. These principles were outlined in a joint policy statement issued in May 2024. TotalEnergies committed to adhering to these guidelines to ensure that its investments in carbon projects contribute meaningfully to climate action.

Last month, the oil major made headlines by announcing its decision to halt its gas exploration activities in South Africa. This move highlights the growing global awareness of the harmful environmental impacts of fossil fuels and supports the broader movement towards sustainable energy solutions.

Under the Anew Climate and Aurora Sustainable Lands partnership, the latter two will provide operational oversight to the projects. This is to ensure that the carbon projects meet the highest standards of additionality and durability.

Their collaboration highlights a shared commitment to advancing climate action through nature-based solutions that offer tangible environmental and social benefits.

Anew Climate’s CEO, Angela Schwarz, emphasized the alignment between TotalEnergies’ comprehensive climate action strategy and Anew’s mission to create meaningful climate impact through diverse solutions. She noted that:

“…it was clear that their [TotalEnergies] commitment to avoiding and reducing emissions as a first principle while recognizing the co-benefits of investing in meaningful carbon projects as part of a comprehensive climate action strategy aligned perfectly with Anew’s mission.”

How Green Giants are Revolutionizing Carbon Stewardship

Anew Climate is a global leader in climate solutions, focusing on transparency and accountability. They offer innovative products and services to reduce or offset carbon footprints, restore the environment, and create economic value. With operations across five continents, Anew leverages technology and nature-based solutions for environmental credit markets.

Jamie Houston, CEO of Aurora Sustainable Lands, highlighted the importance of maintaining the delicate balance between forest health, soil quality, watersheds, and wildlife habitats through this partnership.

Aurora Sustainable Lands is a leading platform for carbon removal and climate-focused asset management. Managing over 1.7 million acres of U.S. forestland previously used for industrial logging, Aurora employs a carbon stewardship strategy that maximizes carbon removal and storage.

Utilizing advanced technologies, Aurora offers high-quality, durable nature-based carbon credits at scale. This venture is a joint effort between Anew Climate and key equity investors, including Oak Hill Advisors, EIG, and GenZero.

The collaboration with TotalEnergies will enable Aurora to enhance climate resilience across its forestlands, contributing to a substantial and lasting impact on a massive scale.

This partnership between TotalEnergies, Anew Climate, and Aurora Sustainable Lands represents a significant step forward in the global effort to combat climate change. By investing in sustainable forestry and carbon stewardship, TotalEnergies is fueling its net zero ambition while contributing to the preservation of vital ecosystems and the protection of natural carbon sinks.

On October 2, 2024, Taiwan will take a significant step toward addressing climate change by launching its domestic carbon credit exchange platform, the Taiwan Carbon Solution Exchange (TCX). This development follows detailed discussions between TCX and Taiwan’s Ministry of Environment regarding the trading of domestic carbon credits. It began after the relevant regulations were enacted on August 15, 2024.

The trading platform is set to play a crucial role in the nation’s carbon reduction efforts, aiming to align Taiwan with global carbon trading mechanisms while fostering a more sustainable industrial structure. Its initial focus will be on those planning to establish new factories, as the carbon fee scheme—targeting entities emitting more than 25,000 metric tons of carbon dioxide equivalent annually—is yet to be implemented.

A New Dawn in Taiwan’s Carbon Trading

Current regulations require new large-scale factories and high-rise construction projects to offset their emissions by purchasing carbon credits from voluntary projects or implementing other offsetting measures, such as adopting high-efficiency equipment and energy-saving technologies.

Voluntary carbon emission reduction projects can be initiated by entities with annual emissions below 25,000 metric tons. These projects must adhere to internationally accepted standards for being measurable, reportable, and verifiable (MRV).

Carbon credits generated from these offsetting measures will be available for sale on the TCX platform. It will be primarily catering to buyers needing to meet environmental assessment requirements for construction and development projects.

Additionally, these domestic carbon credits may be used to partially offset carbon fees once the collection begins, projected for 2026, with 2025 serving as a preparation period.

How TCX Will Transform Taiwan’s Carbon Market and Helps in Net Zero Goal

The TCX, operational since December 2023, is Taiwan’s only certified platform for trading international and domestic carbon credits. It serves as a marketplace where enterprises can trade, transfer, and auction carbon credits in a transparent manner.

The platform’s core mission is to establish a robust carbon trading market that complements the international carbon trading framework. This initiative is particularly important given Taiwan’s ambitious goals to achieve net zero by 2050.

Taiwan’s net-zero goal by 2050 is a comprehensive roadmap aimed at transforming the country’s energy, industrial, and economic landscape. The plan includes a focus on four key transition strategies:

energy transformation,

industrial innovation,

lifestyle changes, and

social inclusion.

Taiwan intends to reduce its reliance on fossil fuels, increase renewable energy use, and invest in green technologies. The roadmap also emphasizes the importance of public and private sector collaboration to achieve these ambitious targets, positioning Taiwan as a leader in global sustainability efforts.

The TCX encourages businesses to adopt more sustainable practices, contributing to the broader national and global objectives of reducing greenhouse gas emissions.

Key Features of the Carbon Trading Platform

Taiwan’s carbon credit exchange will initially focus on purchasing high-quality carbon credits from the international market to offset the shortfall in domestic emission reductions. This approach is to meet the immediate needs of Taiwanese enterprises while the country ramps up its domestic emission reduction capabilities.

Over time, the platform is expected to foster a more self-sufficient carbon credit market within Taiwan, reducing reliance on international credits.

The platform also includes strict regulations to ensure transparency and prevent greenwashing—a practice where companies falsely claim environmental benefits for their actions. Only sellers with government-overseen emission reduction projects can auction or sell domestic carbon credits.

Additionally, buyers cannot resell traded or auctioned domestic carbon credits, a measure designed to stabilize the market and maintain its integrity.

The Environment Minister, Peng Chi-ming, indicated that the carbon fee rate is expected to be finalized by the end of 2024, with fee collection slated to start in 2026. During the interim period, businesses will still be required to report their emissions for 2024.

From Regulation to Innovation: TCX’s Role in Taiwan’s Carbon Neutrality Journey

The introduction of the TCX is expected to have a profound economic impact. The platform could attract significant private investment, potentially bringing in over NT$4 trillion (about US$131 billion) by 2030. This influx of capital can create more than 550,000 jobs in sectors related to carbon reduction and sustainability.

Furthermore, the TCX will contribute to Taiwan’s broader environmental goals by encouraging companies to invest in emission reduction technologies and projects, thus driving innovation in green technologies.

Challenges and Future Outlook

Despite its potential, the success of the TCX will depend on several factors, including:

the active participation of businesses,

the effectiveness of government policies, and

the platform’s ability to integrate with international carbon markets.

Taiwan’s industrial sector, which is a significant contributor to the nation’s carbon emissions, will play a critical role in this transition. Companies will need to adapt to the new regulations and market dynamics, which may involve significant operational changes and investments in sustainable practices.

Moreover, the TCX’s success will also hinge on its ability to evolve alongside global carbon trading systems. As international carbon markets become more interconnected, the platform must ensure that Taiwan remains competitive and compliant with global standards. This includes adhering to international carbon neutrality standards and ensuring that domestic carbon credits are recognized and valued in the global marketplace.

The launch of Taiwan’s domestic carbon credit exchange platform in October marks a pivotal moment in the country’s climate strategy. By creating a structured and transparent market for carbon credits, the TCX aims to accelerate Taiwan’s transition to a low-carbon economy while fostering innovation and economic growth.

With Direct Air Capture (DAC) technology gaining momentum, some companies involved are facing the significant challenge of securing enough clean power to sustain their energy-intensive operations in the US. S&P Global has scrutinized the situation and has reported the challenges and potential solutions to overcome the massive clean energy demand of DACs.

As DACs Expand, So Does the Quest for Clean Energy

Earlier this year, Climeworks launched the world’s largest DAC plant in Hellisheiði, Iceland. The location was ideal, offering abundant geothermal heat and power. But as Climeworks shifted its focus to the U.S., drawn by federal subsidies and opportunities for expansion, the company faced a new hurdle: energy procurement.

Well, Douglas Chan, Chief Operating Officer of Climeworks, emphasized the importance of understanding the U.S. grid, which the company has studied for nearly three years. They pioneer in absorbing CO2 from the atmosphere and sell the carbon offsets to major corporations such as Microsoft. However, without a reliable source of clean power, the entire purpose of this technology i.e. reducing carbon emissions could be compromised.

In another instance, Max Scholten, Head of Commercialization at Heirloom Carbon Technologies, explained the critical need for low-carbon electricity sources. He stressed that what DAC companies sell must be a net removal of CO2, meaning they cannot emit more CO2 than they capture. This need for clean energy has placed added pressure on DAC plants to prove that their electricity sources are zero-emission, new, and “additional” to the grid.

Is Funding Enough to Navigate the U.S. Energy Landscape?

Last year, in August, the DOE announced a whopping $1.2 billion in funding to develop two major DAC facilities led by Climeworks and Occidental (Oxy). The funding was part of President Biden’s Investing in America agenda, marking the beginning of the Bipartisan Infrastructure Law’s Regional DAC Hubs program, designed to create a nationwide network of large-scale carbon removal sites.

Secretary of Energy Jennifer M. Granholm emphasized the importance of these investments by remarking,

“Addressing climate change requires not just reducing emissions but also removing existing CO2 from the atmosphere. This historic investment will help build a crucial industry for combating climate change while supporting local economies.”

For example, the landmark project is led by 1PointFive, a subsidiary of Occidental. This project will initiate the installation of the South Texas Direct Air Capture (DAC) Hub. The hub on King Ranch in Kleberg County aims to become the world’s first DAC plant capable of removing up to 1 million metric tons of CO2 annually.

Clean Power Solutions for DAC Expansion

As the U.S. power consumption continues to rise, DAC companies face long grid connection queues, some stretching over the years. Thus, many DAC companies are choosing to follow strict carbon accounting standards to meet the expectations of buyers and carbon credit exchanges.

Thus, funding is not a problem for DAC plants, but energy procurement is. S&P Global reported that Puro.earth, the carbon removal certifier requires detailed energy emissions analysis for DAC projects listed on its exchange. Such projects must use renewable energy certificates or similar instruments to offset grid emissions, ensuring that the electricity is generated and consumed within the same physical grid and calendar year.

DAC Projects in the U.S.

source: Reuters

The good news is the challenge of securing sufficient clean power has not deterred the sector’s growth. Consequently, Climeworks’ upcoming facility, part of the Battelle-led Project Cypress hub in Louisiana, is set to capture about 1 MMTCO2 annually. This is much more than its current Iceland plant, Mammoth. This project also comes under DOE’s 1.2 billion funding program. Notably, Climeworks is working with renewable energy developers to secure virtual power purchase agreements to achieve this target.

Meanwhile, Heirloom’s initial projects, also part of Project Cypress, will rely on additional wind, solar, and storage facilities. This approach is crucial as DOE has committed around $600 million each to support large-scale DAC hubs on the Gulf Coast.

Furthermore, this level of scrutiny highlights the importance of “additionality”—a concept ensuring that the clean power used by DAC plants is genuinely new and not merely diverted from other uses.

In conclusion, DAC offers great potential in combating climate change. However, as it expands in the U.S., securing clean energy to power operations is a major challenge. S&P Global has scooped this paramount factor and analyzed it focusing on innovative energy solutions and sustainability. With these viable solutions, major carbon capture companies like Climeworks and Heirloom are bound to succeed.

Lego is taking significant steps to replace fossil fuels in its iconic bricks with renewable and recycled plastic. Despite the higher costs, the Danish toymaker is determined to phase out oil-based materials by 2032. On top, the company delivered outstanding double-digit top-and-bottom-line growth in H1 2024, which would accelerate its swift transition into 100% sustainable bricks.

CEO Neils Christiansen revealed that,

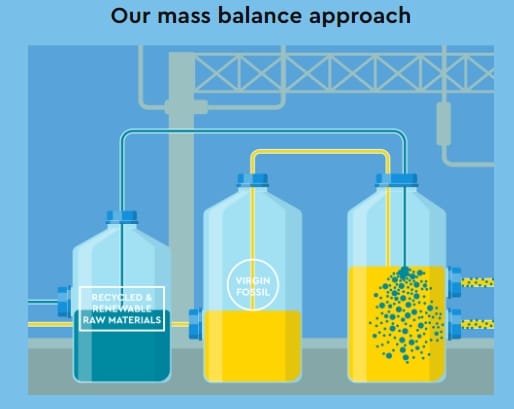

“The company is on track to ensure that more than half of the resin it needs in 2026 is certified according to the mass balance method, an auditable way to trace sustainable materials through the supply chain, up from 30% in the first half of 2024.”

Lego’s Massive Revenue Jump

LEGO has achieved impressive financial growth in the first half of 2024, setting new records across the board. The company’s growth was driven by strong demand for its diverse product range, particularly in the U.S. and Europe.

Key Financial Highlights

Revenue: Increased by 13% to DKK 31.0 billion (from DKK 27.4 billion in H1 2023)

Consumer Sales: Grew by 14%, outpacing the overall toy industry

Operating Profit: Up by 26% to a record DKK 8.1 billion

Net Profit: Up 16% to DKK 6.0 billion (from DKK 5.1 billion in H1 2023)

Cash Flow from Operations: Jumped 60% to DKK 7.5 billion (from DKK 4.7 billion in H1 2023)

Investments: DKK 4.5 billion spent on new factories, facilities, and offices (up from DKK 3.6 billion in H1 2023)

Free Cash Flow: Increased to DKK 3.0 billion (from DKK 1.1 billion in H1 2023)

The company also increased its spending on sustainability, retail, and digital initiatives, ensuring it remains a leader in the toy industry.

Building Each Brick with Sustainable Materials

From media reports, we discovered that Lego has already tested over 600 materials in its quest for sustainable alternatives to plastic. The company plans to reduce the oil content in its bricks by spending 70% more on certified renewable resin. CEO Neils Christiansen has also stated figuratively that this would certainly increase the cost of production.

Sugarcane Based Bio-PE

Since 2018, LEGO has been using bio-polyethylene (bio-PE) for flexible parts like flowers, botanical elements, and minifigure accessories. Made from sugarcane sourced in Brazil, this material is produced in a way that aligns with WWF guidelines, ensuring sustainability without compromising food security. Today, over 200 different LEGO elements are crafted from bio-PE, and nearly half of all LEGO sets include at least one of these eco-friendly pieces.

ArMABS: Recycled Artificial Marble

LEGO’s transparent elements, such as lightsabers, windscreens, and windows, now contain 20% recycled materials from artificial marble kitchen countertops. With more than 500 different arMABS elements available, these sustainable components appear in over 60% of LEGO sets, proving that recycling can lead to crystal-clear results.

Highly Durable ePOM

For robust, rigid components like axles, LEGO is developing a new plastic called ePOM. This innovative material blends renewable energy and CO2 from bio-waste, making it the futuristic choice for LEGO’s most durable parts. Notably, the company plans to start using ePOM by 2025, marking another step forward in sustainability.

A Thing of the Past: Recycled Prototype Brick

In 2021, LEGO created a prototype brick using PET plastic from recycled bottles. However, after two years of development, it became clear that this material did not achieve the carbon reduction goals LEGO aimed for. Despite this, the project provided valuable insights that will guide LEGO as it continues to explore new materials and improve the sustainability of its bricks.

Interestingly, these bricks are permanent. Whether you bought them years ago or will buy them in the future, they all fit together perfectly. The company calls this reliable connection- ‘clutch power’. This means that every brick stacks securely, no matter when it was made.

No wonder these materials meet high standards for safety, quality, durability and now sustainability. Furthermore, the shift to greener plastic comes at a time when global toy sales are sluggish, with major competitors like Hasbro cutting jobs due to declining demand.

However, with high sales volume and strong brand value, LEGO can easily afford the production cost.

Responsible Sourcing and Strategic Partnerships

Lego wants to achieve net-zero greenhouse gas emissions by 2050 and cut emissions by 37% by 2032 based on 2019 levels. Notably, it aims to remove more than 139,000 tons of CO2e this year. One key strategy for reaching this goal is incorporating sustainable and circular materials into all products by 2032.

This involves using responsibly sourced recycled materials to minimize waste while ensuring high safety and quality standards. For instance, it sourced 18% of its resin under mass balance principles in 2023.

Mass balance is a strategy designed to boost the use of renewable and recycled materials in all LEGO products. This model involves blending virgin fossil sources with certified renewable and recycled inputs to create their raw materials.

Source: LEGO

By doing so, LEGO reduces its dependence on virgin fossil fuels, stimulates the market, and encourages the industry to increase the production of sustainable materials. LEGO aims to achieve International Sustainability and Carbon Certification (ISCC) Plus Certification in the first half of 2024. This global certification system covers all types of sustainable feedstocks, including agricultural and forestry biomass, chemicals, plastics, packaging, bio-based materials, and renewables.

Furthermore, the company is working closely with suppliers, research institutions, and industry partners to innovate new materials. Additionally, LEGO is exploring e-Methanol with partners like European Energy and Novo Nordisk, with prototypes expected soon, which could lead to future commercial use.

By investing in renewable materials, LEGO hopes to lead the toy industry toward a greener future. All in all, it is a smart move as Christiansen confidently says,

“We used our solid financial foundation to further increase spending on strategic initiatives which will support growth now and in the future to enable us to bring learning through play to even more children.”

Verra, the leading nonprofit organization in the voluntary carbon credit market, has taken a significant and unprecedented step by rejecting 37 rice cultivation projects in China. Alongside this rejection, Verra has imposed substantial sanctions on the project proponents and the validation/verification bodies (VVBs) involved.

These actions are a result of an extensive quality control review, showing Verra’s commitment to improving transparency, integrity, and quality within voluntary carbon markets.

Cracking Down on Compliance

The projects in question employed the AMS-III.AU methodology, part of the UNFCCC Clean Development Mechanism. It was permanently inactivated by Verra in March 2023. This methodology was designed to reduce methane emissions through adjusted water management practices in rice cultivation.

However, the quality control review revealed serious issues, namely:

insufficient demonstration of additionality,

overstated project areas, and

a lack of credible evidence to support baseline and project scenario implementation.

The review was bolstered by an analysis of remote sensing data, further validating the concerns raised.

Verra’s decision to impose sanctions on these projects marks a watershed moment in the voluntary carbon market. As part of the sanctions, Verra has issued non-conformity reports to four VVBs:

China Classification Society Certification Company,

China Quality Certification Center,

Shenzhen CTI International Certification Co., Ltd, and

TÜV Nord Cert GmbH.

These VVBs are required to present strong corrective action plans within 15 days to prevent similar issues from happening again. Failure to do so could result in their temporary suspension from doing audits of other projects under Verra’s Agriculture, Forestry, and Other Land Use (AFOLU) sector.

Verra’s Sanctions Send Shockwaves Through Carbon Markets

One of the most critical aspects of Verra’s action is the decision to seek compensation from the project proponents for the over issued Verified Carbon Units (VCUs). This move reinforces the importance of accountability in the carbon market, ensuring that projects adhere to the rigorous standards set by Verra. By holding project proponents accountable, Verra aims to maintain the integrity of the market and ensure that carbon credits represent genuine emission reductions.

About a year ago, Verra was criticized for the quality of carbon offset credits the certifier approves. The standard setter has been accused of approving “worthless” carbon offsets that could harm corporate climate goals.

Verra’s response to these issues reflects its broader mission to tackle global environmental and social challenges. The organization works with both the private and public sectors to support climate action and sustainable development, providing standards, tools, and programs that credibly assess environmental and social impacts.

As a mission-driven nonprofit, Verra is committed to reducing greenhouse gas emissions, improving livelihoods, and protecting natural resources.

In line with its commitment to continuous improvement, Verra is also developing a new rice cultivation methodology under the Verified Carbon Standard (VCS) Program. This new methodology will incorporate more robust provisions, including:

guidance for field stratification,

consideration of nitrous oxide emissions, and

soil organic carbon stocks, and standardized protocols for methane measurements.

The goal is to enable project proponents to achieve credible emission reductions and generate high-quality VCUs. The consultation for this new methodology recently closed, and its official launch is anticipated later this year.

Reimagining Carbon Credits: A New Era for Rice Cultivation Projects Begins

The suspension and sanctions against the 37 rice cultivation projects conclude a process that began in March 2023. At that time, Verra inactivated the AMS-III.AU methodology following a thorough review.

The new methodology aims to address the shortcomings identified in the previous approach. This includes providing clearer guidance and more efficient processes for:

determining additionality,

quantifying emission reductions, and

ensuring transparent data measurement, reporting, and verification (MRV) procedures.

As of now, Verra has registered 37 projects applying the AMS-III.AU methodology, with 25 of these projects having issued VCUs totaling 4.56 million units, which represents 0.43% of all VCUs.

Verra’s decisive action in this matter serves as a strong signal to the market that inclusion in the Verra Registry is a mark of quality and integrity of carbon credits. It also highlights the organization’s commitment to ensuring that all projects meet the high standards necessary to deliver meaningful environmental and social benefits.

Janice O’Brien, Director, Auditing and Accreditation, Verra, noted on this announcement saying that:

“Our quality control review identified serious failures that required a serious response. What we have learned in this process will also support the development of a more effective and credible rice cultivation methodology for future projects.”

By taking these unprecedented steps, Verra not only addresses the immediate issues with the rejected projects but also sets a precedent for how similar issues will be handled in the future. The organization’s actions are expected to contribute to a more robust and credible voluntary carbon market. This is particularly important in supporting global efforts to combat climate change and promote sustainable development.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy

Source: NVIDIA

Source: NVIDIA

Source: Adani

Source: Adani

Source: LEGO

Source: LEGO