Vale and Sweden’s GreenIron have teamed up to reduce emissions in the mining and metals supply chain. The MOU focuses on key initiatives in Brazil and Sweden, including a feasibility study for a direct reduction facility in Brazil operated by GreenIron. Additionally, Vale will also supply iron ore to GreenIron’s commercial operations in Sandviken, Sweden.

Rogério Nogueira, EVP of Commercial and New Business at Vale noted,

“This agreement brings together Vale’s superior product portfolio, Brazil’s competitive advantage on green hydrogen and GreenIron’s expertise on sustainable iron production to provide low-carbon solutions for the mining and metals industry”, “We are focused on helping our clients achieve their decarbonization targets and also fostering Brazil’s new industrialization.

Vale and GreenIron’s Collaborative Vision for Metal Recycling

Moving on, their feasibility study will identify the best site and assess renewable energy and resource options for a direct reduction facility in Brazil. Most importantly, it will explore green hydrogen and innovative technologies to reduce the environmental impact of the industries.

GreenIron has conducted rigorous trials to commercialize its hydrogen-based, fossil-free, and energy-efficient technology. The press release revealed that in the last two years, Vale and GreenIron have tested Vale’s iron ore pellets at GreenIron’s Swedish facilities.

The new MoU includes plans to test Vale’s iron ore briquettes, which produce lower CO2 emissions than pellets.

Additionally, GreenIron’s technology offers exceptional adaptability. It can handle various feedstocks and customize capacity to meet specific client requirements. It is also cost-effective and compatible with green hydrogen use.

GreenIron’s Sandviken Facility

The company plans to bring the Sandviken Industrial Park, located 160 kilometers north of Stockholm into full-scale production by the end of this year. This is crucial for the company’s goal of becoming a leader in CO2-free metals and mining while advancing to a circular economy.

Each GreenIron furnace is expected to cut CO2 emissions by at least 56,000 tonnes annually, paving the way for a greener future.

Edward Murray, CEO of GreenIron said,

“This MOU with Vale marks a significant milestone for GreenIron. It represents a clear commitment to pursue collaborative opportunities that align with our vision for a sustainable mining and metals industry, and to drastically reduce the sector’s climate footprint. By pooling our expertise and resources, we aim to innovate and develop projects that not only benefit both companies but also positively impact the environment and the communities in which we operate.”

Vale is one of the largest iron ore producers in the world. Iron ore, the key raw material for steelmaking, is found in rocks mixed with other elements. It is refined through advanced industrial processes and then sold to the steel industry.

Vale’s iron ore from Carajás is among the best globally, with a 67% iron content. In Northern Brazil, the company’s mines occupy just 3% of the Carajás National Forest. The remaining 97% is protected in collaboration with environmental institutes. Vale operates in Brazil, China, and Oman to suffice global supply of this crucial resource.

Here’s Vale’s 3Q24 production and sales report for Iron ore, pellets, copper, and nickel.

Source: Vale

By 2025, the company plans to transition entirely to renewable energy in Brazil and 100% renewable energy by 2030 globally. Additionally, Vale aims to enhance its global energy efficiency by 5% by 2030, using 2017 levels as the baseline

DOE Partnership

In November, Vale completed negotiations with the U.S. Department of Energy’s Office of Clean Energy Demonstrations. The company will start Phase 1 of a project to develop an industrial-scale briquette plant in Louisiana. It will use over $3.8 million in DOE funds to support engineering studies and community engagement in 2025.

Vale’s sustainably sourced iron ore briquettes can reduce scope 3 emissions by 15% by 2035. These efforts align with Vale’s sustainability targets to cut absolute scope 1 and 2 emissions by 33% by 2030 and achieve net zero by 2050.

As per the latest media reports, Hussain Sajwani, chairman of Dubai-based DAMAC Properties, pledged a whopping $20 billion investment in the U.S. data center industry. He announced his plan in the presence of newly elected President Donald Trump at his Mar-a-Lago estate. This deal is immensely significant for Trump’s economic strategy and AI vision for America.

Sajwani and Trump: A New Era in AI Investment

Hussain Sajwani’s collaboration with Donald Trump started with the Trump International Golf Club in Dubai and expanded to other high-end developments. This eventually fortified their professional relationship. While DAMAC Properties is renowned for its luxurious real estate ventures, including Trump-branded projects in Dubai, this is Sajwani’s first investment in the U.S. data center sector.

Furthermore, Sajwani expressed his confidence in the U.S. market and said,

“We’re planning to invest $20 billion and even more than that, if the opportunity in the market allows us.”

This massive investment comes at a pivotal moment for the U.S., when the rapidly expanding AI sector needs robust infrastructure and cutting-edge technology. Sajwani’s investment highlights Trump’s commitment to boosting domestic industries and jobs. Moreover, Trump’s policies to attract foreign investment ensure that the U.S. remains competitive in the global AI landscape.

According to Newsweek, DAMAC will break ground on its U.S. data centers in early 2025, with full operations expected within two years. The initial rollout targets key states, including Texas, Arizona, Oklahoma, Louisiana, Ohio, Illinois, Michigan, and Indiana.

During his previous term, Trump launched the American AI Initiative which also aimed at bolstering America’s competitive edge in AI research and development. However, the initiative faced criticism for lacking sufficient funding and depth.

Now, with re-election Trump gas gained a golden opportunity to modify his AI strategy. And of course, with a stronger emphasis on national security, economic growth, and international competitiveness. He expects a significant shift in federal policy.

Bloomberg revealed that Trump plans to repeal President Biden’s October 2023 AI executive order. As he is known for favoring a hands-off regulatory approach, this decision can minimize regulatory constraints and create a more viable environment for innovation.

Trump’s approach stands in clear contrast to Biden’s, who focused on responsible innovation, ethical oversight, and global collaboration. But Trump’s ambition is clear and concise- make the U.S. a global leader in AI by focusing on industry growth rather than regulatory oversight.

AI in Defense and National Security

The Department of Defense (DOD) has identified AI as a transformative technology, with applications ranging from autonomous drones to cybersecurity. The Bloomberg report further explained that under Trump’s leadership, this sector expects to expand defense-related AI initiatives. It includes integrating AI into defense systems, developing tools to detect cyber threats, and ensuring critical infrastructure security.

Needless to say, Trump’s tough stance on China further highlights the strategic importance of AI. His administration is expected to tighten export controls and impose sanctions to limit China’s access to advanced AI technologies. He foresees investing heavily in AI research and collaborating with allies to counter China’s influence while maintaining America’s technological edge.

But are the AI Ethics at Risk?

However, there are always two sides of a coin.

Trump’s deregulation approach sparks debate—while it may accelerate innovation, it also raises concerns about proper oversight. The rapid development of AI technologies requires a high level of management to address ethical and safety issues. Critics argue that a “hands-off approach” could increase risks, including discriminatory outcomes, and misuse of AI in critical applications.

In this case, state governments will need to step in and might play a crucial role in addressing these challenges. California and New York, for instance, are expected to introduce regulations focused on safety, ethics, and accountability. Balancing federal policies with state-level initiatives could lead to responsible AI development.

In another scenario, international collaboration can also present some challenges. Trump’s polarizing leadership style might hinder efforts to establish global standards for AI governance.

However, if hurdles show up, there are ways to overcome them as well. And this time the Trump administration is expected to be more cautious while handling this crucial AI industry.

The Synergy Between Billionaires and Trump

Tech giants like Microsoft recently committing $80 billion to American AI infrastructure shows America’s continued dominance in the AI revolution.

Last year in December, SoftBank’s CEO Masayoshi Son bet big on an AI-driven future. The Japanese investment giant has committed $100 billion to support the U.S. AI, infrastructure, and technology projects.

The most hyped anticipation is the camaraderie between Musk and Trump this year could create a powerful synergy to accelerate AI development. Musk’s brilliant and innovative AI products and ideas like AV, EVs, and space exploration would certainly garner Trump’s support. Additionally, Sam Altman’s backing of Trump and pledging support to ensure the U.S. remains at the forefront of the AI age raises huge optimism for the domestic AI industry.

The $20 billion data center investment is just the beginning. However, Trump’s AI success for the U.S. will depend on balancing innovation with ethics and swiftly addressing the geopolitical challenges.

Companies and governments worldwide are transitioning to a low-carbon economy and corporations are under increasing pressure to reduce their carbon footprints. Tech giants, such as Meta, Apple, and Netflix, have committed to achieving net-zero emissions by 2030, while mining and energy giants like Barrick, Newmont, and ExxonMobil are following suit. For investors, this evolving trend presents a unique opportunity to invest in carbon stocks and support innovative companies focused on carbon reduction and capture.

Why Carbon Stocks Are Gaining Traction in 2025

Carbon stocks are becoming increasingly popular as people and organizations alike strive to meet climate goals. These stocks represent companies that focus on reducing or offsetting carbon emissions. They are drawing attention not only for their environmental benefits but also for their potential financial returns.

With governments and corporations prioritizing carbon reduction technologies and emissions offsets, the market for carbon-related solutions is poised for rapid growth.

In 2025, here are the top five carbon stocks worth keeping on your radar.

1. Brookfield Renewable Partners (BEP): A Leader in Clean Energy

Brookfield Renewable Partners (BEP) is one of the world’s largest publicly traded renewable energy companies. With a clear focus on clean, renewable energy, BEP distinguishes itself from many of its competitors by operating as a pure-play renewable energy company. This means that its portfolio consists exclusively of renewable sources of power generation, unlike other companies that often combine renewable energy with fossil fuel assets.

Energy Storage Facilities: 700 megawatts of capacity

This extensive array of assets spans multiple regions, including North America, South America, Europe, and Asia, underscoring BEP’s commitment to global renewable energy development.

Financial Performance, Growth, and Expansion Plans

In the third quarter of 2024, BEP reported Funds From Operations (FFO) of $278 million, equating to $0.42 per unit. This represents an 11% increase compared to the same period in the prior year, highlighting the company’s robust financial health and operational efficiency.

Over the past 5 years, BEP has maintained an average dividend yield of around 5%. Since its inception over two decades ago, it has reached over $109 billion in assets under management globally.

The company is actively pursuing an ambitious growth strategy, with a development pipeline poised to add 11,000 megawatts of capacity. This expansion represents a 46% increase over the current operating capacity, with plans to execute these developments over the next 3 years.

Successful realization of this pipeline could enable the renewable energy company to significantly scale its power generation capabilities. Here’s what BEP’s development and growth plans look like, highlighting its 10.5 GW partnership with Microsoft:

Source: Company presentation

Positioning in the Transition to Clean Energy

As corporations worldwide strive to achieve net-zero carbon emissions, the demand for renewable energy sources is escalating. BEP’s exclusive focus on carbon-free energy positions it as a preferred partner for companies seeking to reduce their carbon footprints.

For investors seeking exposure to the renewable energy sector with a preference for established companies demonstrating stable growth and reliable returns, Brookfield Renewable Partners represents a compelling option.

Aker Carbon Capture (AKCCF) is a Norwegian company specializing in carbon capture technology. Leveraging its expertise from the Aker Group, a global leader in offshore engineering, Aker Carbon Capture has developed modular carbon capture systems that are both cost-effective and scalable.

One of the company’s standout innovations is the “Just Catch” modular carbon capture plant. It is designed to meet the needs of mid-sized industries like cement, biomass, and waste-to-energy. This plant reduces the time and cost typically associated with custom-built carbon capture facilities.

Aker has also developed a proprietary amine solvent, a technology that efficiently captures CO₂ from industrial emissions. This solvent is highly stable, has low degradation rates, and minimizes energy consumption, making it a cost-effective solution for industries looking to reduce their carbon footprint.

The technology has been successfully deployed in real-world projects, such as the CO₂ capture pilot at the Norcem cement plant in Brevik, Norway.

Aker Carbon Capture is also undergoing a joint venture with SLB to form SLB Capturi, which will further accelerate the development of large-scale carbon capture technologies. The carbon capture company partnered with Microsoft last year to capture and store carbon at pulp and paper mills.

As of the third quarter of 2024, ACC ASA reported a net loss of NOK 47 million. The company maintained a robust financial position with NOK 4.5 billion in cash and an equity standing at NOK 5.5 billion.

Ørsted’s BECCS Project (Denmark): Deploying five Just Catch units to capture up to 500,000 tonnes of CO₂.

Twence Project (Netherlands): Captures 100,000 tonnes of CO₂ annually for use in local agriculture.

With a solid financial foundation and strategic partnerships, ACC ASA is well-positioned to expand its carbon capture solutions globally. The aim is to contribute significantly to the reduction of industrial CO₂ emissions and support the transition to a low-carbon economy.

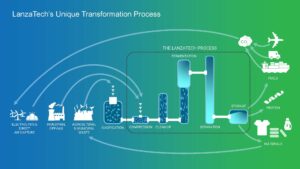

3. LanzaTech Global, Inc. (LNZA): Turning Emissions into Valuable Products

LanzaTech Global, Inc. (LNZA) is a pioneering carbon recycling company that transforms waste carbon emissions into sustainable fuels and chemicals through innovative biotechnology using gas fermentation. Through this process, industrial emissions—rich in carbon monoxide and carbon dioxide—are converted into ethanol and other chemicals.

Source: LanzaTech website

The company uses proprietary microbes engineered to thrive in industrial gas streams, such as those found in steel mills and refineries. These microbes consume waste gases, turning them into useful products.

The ethanol produced can serve as a building block for various products, including jet fuel, plastics, and synthetic fibers.

Financial Performance and Strategic Development

In the third quarter of 2024, LanzaTech reported revenue of $9.9 million, a decrease from $17.4 million in the second quarter and $19.6 million in the third quarter of 2023. This decline was primarily due to a timing delay in a LanzaJet sublicensing event, which was expected to generate about $8.0 million in licensing revenue.

LanzaTech has been actively expanding its technological capabilities and market reach:

CirculAir Initiative: In June 2024, LanzaTech and its subsidiary LanzaJet introduced CirculAir, a commercially viable solution designed to convert waste carbon and renewable power into sustainable aviation fuel (SAF).

Project Drake: LanzaTech advanced Project Drake, a 30-million-gallon sustainable aviation fuel project, furthering its commitment to large-scale SAF production.

Key Projects and Partnerships

The carbon recycling company has engaged in several significant projects and collaborations, including:

Eramet Partnership: Developing a Carbon Capture, Utilization, and Storage (CCUS) project in Norway.

LanzaJet Initiative: Introducing CirculAir, a technology to produce sustainable aviation fuel (SAF).

Additionally, LanzaTech is developing a novel biocatalyst to directly convert CO₂ to ethanol at 100% carbon efficiency, leveraging affordable, renewable hydrogen. This transformative technology aims to produce biofuels and feedstocks for valuable products using carbon-free renewable energy, water, and CO₂.

With a solid financial foundation bolstered by recent capital raises and strategic partnerships, LanzaTech is well-positioned to expand its carbon recycling solutions globally, creating sustainable products from waste carbon.

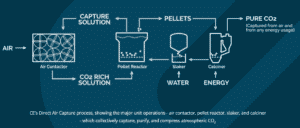

Occidental Petroleum (OXY) is a major player in the oil and gas industry. However, in recent years, the company has been transforming itself into a leader in carbon management solutions.

Occidental has embraced Direct Air Capture (DAC) technology, which removes CO₂ directly from the atmosphere. In partnership with Carbon Engineering, Occidental is constructing the world’s largest DAC facility in Texas, a groundbreaking project that will play a significant role in achieving global emission reduction targets.

Financial Performance

In the third quarter of 2024, Occidental reported net income attributable to common stockholders of $964 million, or $0.98 per diluted share. The company has scheduled the announcement of its fourth-quarter 2024 financial results for February 18, 2025.

Carbon Capture Initiatives

Occidental is actively investing in DAC technology through its subsidiary, 1PointFive. The company’s flagship DAC facility, named STRATOS, is under construction in the Permian Basin.

STRATOS is designed to extract 500,000 metric tons of atmospheric CO₂ annually, laying the foundation for commercial-scale DAC deployment. The facility will begin operations in the summer of 2025, with live power anticipated to come online in December 2024.

Occidental plans to integrate the captured CO₂ into enhanced oil recovery (EOR) processes, injecting the CO₂ into aging oil fields to extract additional oil while effectively sequestering the CO₂ underground.

This approach creates a closed-loop system that both boosts oil production and reduces atmospheric carbon.

Additionally, Occidental is developing a project to transport and store CO₂ captured from Velocys’ planned Bayou Fuels biomass-to-fuels project in Natchez, Mississippi, in secure geologic formations.

The Bayou Fuels project converts waste woody biomass into transportation fuels, and applying CO₂ capture and storage can make the facility a net-negative carbon dioxide emitter.

Occidental’s approach is an example of how traditional energy companies are evolving to embrace sustainability. By combining its existing expertise in oil extraction with innovative carbon capture methods, Occidental is paving the way for a future where fossil fuel extraction can coexist with carbon reduction technologies.

5. Equinor ASA (EQNR): Leading the Way in Carbon Storage and Capture

Equinor, formerly known as Statoil, is a Norwegian energy giant that has diversified its portfolio to include renewable energy sources like wind power. It has also been at the forefront of carbon capture, utilization, and storage (CCUS) technologies for over 25 years.

Their extensive experience includes operating the world’s first dedicated CO₂ storage site at the Sleipner field since 1996 and the Snøhvit field since 2008. The image from the company’s presentation below shows its overall performance in the latest report.

Moreover, Equinor is a key player in the Northern Lights project, a pioneering initiative in Norway aimed at developing a large-scale CCS infrastructure.

The Northern Lights project focuses on capturing CO₂ from industrial sources, transporting it via ships, and securely storing it beneath the North Sea seabed. This project is a crucial step in addressing the complexities of CCS, and Equinor is positioning itself as a facilitator of this transformative technology.

What makes the Northern Lights project particularly noteworthy is its open-source infrastructure. It allows other companies to use the storage facilities. This collaborative model could accelerate the widespread adoption of CCS technology across Europe and beyond.

Financial Performance

Equinor reported Q3 2024 operating income of $6.89 billion, down 13% from $7.93 billion in Q3 2023, missing forecasts. Adjusted net income after tax was $2.04 billion, with net income at $2.29 billion. Earnings per share reached $0.79. Lower oil prices and production declines drove the decrease in profit.

Other Key Projects and Developments

Bayou Bend CCS Project: Equinor has acquired a 25% interest in Bayou Bend CCS LLC, positioning it to be one of the largest carbon capture and storage projects in the United States.

UK Carbon Storage Initiatives: Equinor, in collaboration with BP and TotalEnergies, has secured investment into Britain’s carbon capture projects, directly supporting 2,000 jobs in the northeast of England.

Strategic Partnerships, Technological Innovations, and Outlook

Equinor has signed an agreement with French gas grid operator GRTgaz to develop a CO₂ transport system that will carry captured CO₂ from French industrial emitters to offshore storage sites in Norway.

The Norwegian energy giant operates the Technology Centre Mongstad, the world’s largest and most flexible plant for testing and improving CO₂ capture technologies. This facility plays a crucial role in advancing CCUS solutions to decarbonize industries and the energy system.

In December 2024, Equinor secured over $3 billion in financing for its Empire Wind 1 offshore project in the U.S. Scheduled to become fully operational by 2027, the project will deliver clean energy to 500,000 New York homes, advancing the company’s renewable energy ambitions.

Equinor has decades of experience in offshore oil and gas exploration. Its deep-rooted knowledge of energy infrastructure is key to its success in developing large-scale CCS solutions. With the potential to store the equivalent of 1,000 years of Norwegian CO₂ emissions beneath the seabed, Equinor’s initiatives are pivotal in supporting global climate goals.

Conclusion: The Future of Carbon Stocks

As more companies declare their commitment to net-zero goals and seek innovative solutions to reduce carbon emissions, carbon stocks are becoming attractive to investors. The top carbon stocks or companies mentioned in this article—Brookfield Renewable Partners, Aker Carbon Capture, LanzaTech, Occidental Petroleum, and Equinor—are leading the charge in decarbonizing industries and creating sustainable solutions for a carbon-constrained world.

By investing in these carbon stocks, investors support the transition to a cleaner, more sustainable future and also position themselves to benefit from the growth of the green economy.

As we move closer to 2030 and beyond, carbon stocks will become an increasingly important part of investment portfolios aiming to align financial returns with environmental impact.

SolarBank Corporation (NASDAQ: SUUN) has announced a significant deal with Qcells, a subsidiary of South Korea’s Hanwha Solutions. Qcells, through an affiliate, has entered into agreements to purchase four solar power projects in upstate New York.

These ground mount projects—Gainesville, Hardie, Rice Road, and Hwy 28 are under development and have a combined capacity of 25.577 MW. The total value of the sale and the engineering, procurement, and construction (EPC) agreements amounts to approximately $49.5 million.

SolarBank Brings Solar Access to Everyone

SolarBank developed the sites and has successfully passed the Coordinated Electric System Interconnection Review (CESIR). This confirms their feasibility for connection to the local electricity grid.

The projects will now progress as individual solar installations under engineering, procurement, and construction (EPC) agreements with Qcells, having manufacturing facilities in the U.S., Malaysia, and South Korea. The company serves customers in the utility, commercial, government, and residential markets with reliable clean energy solutions and long-term partnerships.

The company also plans to manage the projects through an operations and maintenance contract after completing construction. Once operational, the projects will serve as community solar systems, allowing multiple people to benefit from a shared solar energy system without installing panels on their homes.

Source: SolarBank

In an exclusive discussion with CarbonCredits, Dr.Richard Lu, CEO of SolarBank expressed his thoughts and the deal’s impact on the general community and the U.S. at large.

Read on…

CC: What inspired SolarBank to partner with Qcells for these community solar projects?

Dr. Richard: As the SUUN will always shine, we want to do our part to “Make America Great Again”. Solar energy is the power that we can deliver at a low cost in a timely manner, and we want to use “Made in the USA” solar panels to achieve our strategic goal.

CC: How will “Made in the USA” equipment for these projects impact both SolarBank and the broader clean energy sector?

Dr. Richard: For Solarbank, the Made in the USA panels demonstrate our commitment to supporting domestic production for the clean and renewable energy industry. For the sector, it will enable the industry to meet its demand with domestic supplies.

CC: Any challenges you foresee during the EPC phases of these four solar projects? If Yes, how SolarBank plans to address them?

Dr. Richard: We have every confidence to deliver these 4 solar projects as the EPC using domestic solar panels. We have completed initial designs with the “Made in the USA” solar panels andwe did not encounter any engineering issues. We have started site mobilization and will work with our long-term construction crews on these projects.

CC: What are SolarBank’s long-term goals in supporting the development of community solar projects and clean energy goals of America?

Dr. Richard: As demand for clean and renewable energy grows across general society, commercial, industrial, and especially digital economy—SolarBank is playing a key role in meeting this demand in the USA. Community solar enables more than 50% of Americans to enjoy clean and renewable energy at a lower cost, without having to install solar panels on the roof of their houses, if they live in a house.

Moving on, SolarBank further highlighted the many benefits of community solar projects.

These solar panels will feed clean energy into the local electricity grid.

Renters and homeowners who subscribe to the program can earn credits on their electricity bills based on the solar energy generated.

This setup will help save and bring environmental benefits to dozens or even hundreds of participants, depending on the size of the project.

These projects are expected to qualify for incentives under the New York State Energy Research and Development Authority (NYSERDA) NY-Sun Program. This initiative supports renewable energy adoption and helps make solar power more affordable to communities.

North American Growth Strategy: Development + EPC + O&M + IPPSource: SolarBank

Navigating the Potential Risks to Development

While the deal is promising certain risks remain. The press release revealed that developing these projects requires obtaining permits and securing financing for Qcells. Changes in government policies or reductions in solar incentives could also affect future project viability.

Qcells will make payments for the purchase and construction costs in stages. If Qcells cannot secure financing, SolarBank is obligated to reacquire the projects, retaining an initial payment as compensation. Essentially, SolarBank plans to retain an operations and maintenance contract for these projects after construction. This move will ensure continued involvement in their operation and enjoy long-term success.

Jin Han, Corporate Officer, Head of Distributed Energy at Qcells North America has affirmed this deal by noting,

“At Qcells, we are dedicated to delivering clean, affordable energy solutions to communities nationwide and around the globe. With a commitment of nearly $2.8 billion, we are working hard to onshore production of the solar supply chain from ingots and wafers to cells and finished panels. Each step we take strengthens domestic solar manufacturing, drives the clean energy transition, and brings us closer to a sustainable future for all.”

SolarBank Shares Surge 11% After $49.5M Qcells Deal

According to S&P Global SolarBank shares rose on Monday following the company’s announcement of selling its solar projects for $49.5 million. The stock gained 11%, reaching its highest at $2.66.

source: Yahoo Finance

Thus, this collaboration between SolarBank and Qcells is pivotal for advancing renewable energy in New York while supporting U.S.-based solar manufacturing. And we hope it Makes America Great Again!

The global carbon credit market in 2024 remained stagnant, valued at around US$1.4 billion, per MSCI report. Demand for carbon credits—measured by the number of credits “retired” or permanently used—did not grow significantly. Carbon prices, meanwhile, continued to fall.

However, the market is showing signs of potential growth. With more companies committing to ambitious climate goals and new policies emerging, experts believe the market could expand significantly.

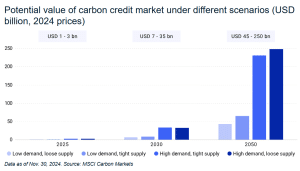

By 2030, the market is projected to reach between $7 billion and $35 billion, and by 2050, it could climb to $250 billion.

Carbon Credits in 2024: Key Numbers

Carbon credits allow businesses and governments to offset their greenhouse gas emissions. Each credit represents one ton of carbon dioxide either reduced or removed from the atmosphere. These credits come from a variety of projects, including:

Nature-Based Solutions: Reforestation, forest conservation, and soil carbon storage.

Renewable Energy: Projects like wind and solar farms that replace fossil fuel-based energy.

Carbon Capture Technologies: Direct air capture or storing carbon in the soil through biochar.

When companies buy and retire these credits, they use them to meet their climate targets, like achieving net-zero emissions.

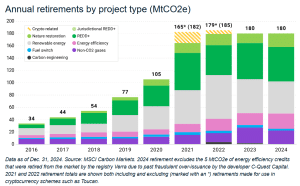

By the end of 2024, the carbon credit market had grown in some areas, even if overall demand remained flat. The MSCI report shows the following achievements last year:

Projects: Over 6,200 carbon credit projects were registered worldwide.

Issuance: These projects issued 305 million tons of credits (MtCO2e) in 2024 alone, bringing the total to over 2.1 billion credits since the 2016 Paris Agreement.

Retirements: Only 180 million credits were retired in 2024, roughly the same as in 2023.

Of the credits retired in 2024:

91% came from projects that reduce emissions (e.g., renewable energy or forest protection).

9% came from projects that remove carbon from the atmosphere, such as reforestation.

Falling Prices

Despite the growing number of carbon credits issued, their prices have dropped. In 2024, the average price of a carbon credit fell to just $4.8 per ton, a 20% decline compared to 2023.

Prices vary depending on the type of credit:

Nature-Based Projects: These often fetch higher prices because they are seen as more reliable and long-lasting.

Technology-Based Projects: Carbon capture and other engineered solutions command even higher premiums due to their permanence and innovation.

Why the Market Is Stuck But Shows Signs of Growth

Even with more companies announcing climate goals, the carbon credit market has struggled. Several factors have contributed to this stagnation.

One is the concern about quality. Questions about the reliability and impact of some projects have undermined trust. Another is the lack of urgency as many companies have climate targets set far into the future, reducing the immediate need to buy credits.

Lastly, negative publicity also impacted carbon credit markets heavily. Reports of fraud and overestimated project impacts have hurt the market’s credibility. As a result, demand (retired credits in the chart) has remained steady but unimpressive, and prices continue to drop.

Despite these challenges, there are promising signs that the carbon credit market could soon expand.

In 2024, more climate commitments were reported. Over 2,700 companies set science-based climate targets, a 65% increase from 2023. As deadlines approach, many companies will need to rely on carbon credits to meet their goals.

Additionally, policy improvements and new standards like the Core Carbon Principles (CCPs) aim to improve the quality and integrity of carbon projects. These alleviated trust in the market.

These factors could boost demand for high-quality credits and push the market out of its current stagnation. So, what does this year look like for carbon credits?

2025: A Year of Transition

The year 2025 and beyond hold immense potential for growth and impact. It marks a pivotal moment for the carbon market as it transitions toward greater maturity and alignment with global climate goals.

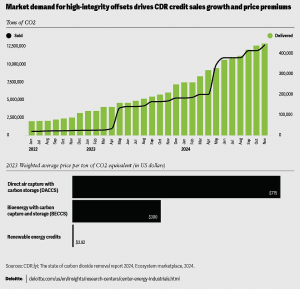

Demand for carbon credits could rise steadily, driven by companies ramping up efforts to meet their 2030 emissions reduction targets. As more organizations integrate carbon offsets into their climate strategies, the emphasis will shift toward high-quality carbon removal credits (CDR), which are increasingly considered essential for achieving net-zero emissions.

According to the Deloitte report, robust CDR credit sales and high prices highlight market confidence in carbon dioxide removal methods for achieving tangible removals. Elevated pricing offers a potential revenue stream. This enables emerging renewable energy providers to collaborate with CDR projects and secure a share of the generated credits.

This growing demand is likely to push prices higher, especially for credits that meet stringent integrity and additionality standards.

The aviation sector is anticipated to emerge as a significant player in the carbon market. The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) will enter its first mandatory phase in 2027, but airlines could begin preparing earlier by purchasing credits to offset their emissions. This development will further bolster demand and drive innovation within the voluntary carbon market.

Policy advancements will also play a crucial role in shaping the market in 2025. The continued implementation of Article 6 of the Paris Agreement, alongside national regulations like the EU’s Green Claims Directive and the U.S. transparency laws, will provide clearer guidelines for credit use and enhance market credibility.

However, challenges persist, including addressing fragmented market standards and ensuring robust monitoring and verification systems.

As the carbon market evolves, 2025 will serve as a year of progress and adjustment. This year will lay the groundwork for a more transparent, efficient, and impactful mechanism to combat climate change.

Beyond 2025: Projections for 2030 and 2050

By 2030, the carbon credit market could grow significantly, reaching between $7 billion and $35 billion, according to the MSCI analysis shown above. Several trends are driving this potential growth:

Rising Demand for Carbon Removal Credits: These tend to be more expensive but are considered more credible.

Corporate Climate Goals: Companies with ambitious targets for 2030 will likely rely more on carbon credits to bridge the gap between their emissions and goals.

Higher-Quality Credits: Buyers are increasingly choosing credits from projects with higher standards and transparency, which boosts trust in the market.

MSCI’s long-term outlook for carbon credits is even more optimistic. By 2050, the market could be worth between $45 billion and $250 billion, driven by:

Urgent Corporate Demand: Many companies will be nearing their net-zero deadlines by 2050, increasing the need for offsets.

Shift to Removal Credits: Around two-thirds of the market value by 2050 could come from credits that actively remove carbon.

Engineered Solutions: Technologies like direct air capture could become key players, with their market value potentially reaching $42 billion.

A Market Worth Watching

The carbon credit market may be stuck for now, but the outlook is promising. With stricter standards, growing corporate commitments, and innovative solutions, the market is poised for growth. As 2030 approaches, the demand for high-quality credits is likely to rise, thawing the frozen market and creating new opportunities for businesses and investors alike.

Nickel’s importance stems from its role in enhancing battery energy density, improving EV range, and enabling a shift away from fossil fuels. To support this energy transition there has been a meteoric rise of nickel as a key material, particularly for batteries. But Nickel’s high demand has consequently sparked a supply strain.

Let’s study the demand and supply dynamics of nickel and its impact on this metal’s future.

Why Nickel is Indispensable?

Nickel’s role in enhancing battery energy density makes it indispensable for long-range EVs and larger vehicles like trucks. For instance, in this nickel revolution, high-nickel cathodes, such as those in NMC 811 batteries are taking the lead. These batteries offer higher energy density, reduced weight, and extended driving ranges which are vital consumer needs.

Thus, as global EV adoption surges, the demand for nickel is set to increase, requiring simultaneous expansion in supply to prevent shortages that might stall the energy transition.

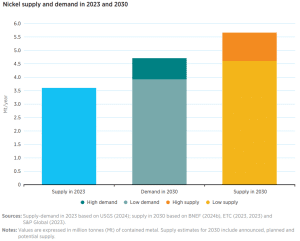

As you can see in the infographic, global nickel production has surged over the past two decades, increasing from 1.1 million tons in 2000 to 3.7 million tons in 2023. However, this growth may not be enough to meet future demand.

By 2030, nickel demand will reach 4.9 million tonnes, driven by the electric vehicle (EV) market and renewable energy storage needs.

Navigating the Nickel Supply Chain

IRENA projects a positive outlook for nickel supply, but challenges remain in meeting the rising demand. However, the demand surge is expected to face fewer supply shortages compared to other critical materials.

By 2030, nickel production is projected to range between 4.6 and 5.6 million tonnes, reflecting a relatively stable outlook for this essential resource.

Nonetheless, the potential for supply-demand imbalances persists due to the wide variation in production forecasts. For instance, the gap between the highest and lowest projections is nearly 60% of the current supply, underscoring uncertainties in meeting future needs.

Now achieving this supply level will require significant investments in sustainable nickel mining and refining infrastructure across various regions. This means nickel miners must ramp up exploration efforts to bridge the supply-demand gap.

Additionally, factors such as market dynamics, regulatory policies, mining advancements, and processing technology will be crucial for meeting supply targets.

Notably, Alaska Energy Metals Corp. is one of the nickel juniors playing a significant role in shaping nickel’s future by tapping into Alaska’s rich nickel resources. The company is putting serious efforts into bolstering the nickel supply and building a reliable, low-carbon supply chain essential for the growing EV and renewable energy markets.

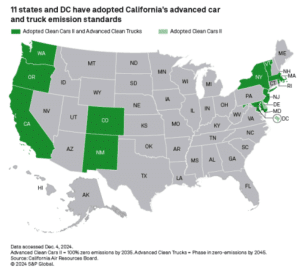

California Resources Corporation (CRC) and its carbon management arm, Carbon TerraVault (CTV), announced the launching of California’s first carbon capture and storage (CCS) project at CRC’s Elk Hills cryogenic gas plant in Kern County. This is a huge milestone for reducing carbon emissions in the state.

Francisco Leon, CRC’s President and Chief Executive Officer, said,

“We are pleased to advance California’s first CCS project to the next stage of its development highlighting our ability to deliver carbon management solutions while reducing our own emissions. This project strengthens Carbon TerraVault’s economic opportunities and positions us to create lasting value for our shareholders and partners. Carbon TerraVault remains at the forefront of providing innovative decarbonization solutions that support a cleaner, affordable, and reliable energy future for California.”Source: California Air Resources Board

CTV is focused on capturing, transporting, and permanently storing carbon dioxide (CO2) emissions. It’s working on several CCS projects to sequester CO2 from industrial sources deep underground, permanently.

Moving on, the Carbon TerraVault Joint Venture (CTV JV) is a partnership between CTV LLC and Brookfield Corporation. CRC holds a 51% stake in the joint venture, with Brookfield owning the remaining 49%. Together, they are advancing CCS solutions for both CRC and other emitters in California. One such project is the 26R reservoir, a depleted formation within CRC’s Elk Hills Field.

Natalie Adomait, Managing Partner at Brookfield said,

“This announcement underscores California’s leadership in carbon capture and sequestration in the United States and reaffirms our commitment to collaborating with the right partners on impactful and economically viable energy solutions that advance the transition to net zero. Together with CRC, we are deploying our clean energy expertise to accelerate decarbonization and drive capital deployment across California’s critical industries.”

The press release highlighted CRC’s plans to begin permanently storing CO2 emissions at the Elk Hills oilfield near Bakersfield by the end of this year. The EPA approved its request to drill four Class VI injection wells, each over a mile deep on December 31, 2024.

The storage site can hold approximately 38 million metric tons of CO2, with an annual capacity of 1.46 million metric tons.

The EPA also confirmed that the site meets safety standards and will not pose a risk to local drinking water supplies. This approval underscores the 26R reservoir’s importance in Kern County which is a prime hub for both agriculture and oil production.

Efficiency, Incentives, and Emissions Reduction in One Project

The project can capture and permanently sequester up to 100,000 metric tons (KMTPA) of CO2 annually. The captured carbon will be stored in the nearby 26R reservoir.

CRC anticipates several financial and environmental gains from this project:

The project qualifies for 45Q tax credits, offering $85 per metric ton of CO2 stored. It may also benefit from Low Carbon Fuel Standard (LCFS) credits and reduced Cap-and-Trade (C&T) liabilities, depending on California Air Resources Board (CARB) rule updates.

The proximity of the 26R reservoir minimizes transportation costs, ensuring cost-effective sequestration.

Decarbonized gas processing will boost propane recovery by up to 100 barrels of natural gas liquids per day.

The initiative can cut Scope 1 and 2 emissions from the Elk Hills Power Plant by up to 7%.

Investment and Profitability

Additionally, the capital investment for the capture infrastructure is estimated to be between $14–$18 million, ensuring cost-effective execution and long-term profitability.

The project is expected to deliver strong financial returns, with the joint venture anticipating sequestration revenue of $50–$60 per metric ton through fees paid by CRC. CRC forecasts a high internal rate of return, positioning it at the upper end of its 10%–30% range. This reflects the project’s economic viability.

CRC’s Net Zero Commitment Aligns with California’s Emission Reduction Goals

CRC believes climate change requires action from both government and the private sector. This is why it supports market-based solutions like CCS and direct air capture with storage (DAC+S), which benefit communities and society.

Its sustainability report reveals the commitment to the energy sector’s transition with a 2045 Full-Scope Net Zero goal, covering Scope 1, 2, and 3 emissions. The goal further aligns with California’s 2045 net zero ambition.

“This project represents another step forward in California’s world-leading pathway to combat climate change and achieve carbon neutrality over the next two decades. While slashing carbon pollution is the main thrust of our climate programs, capturing and removing carbon from our atmosphere is also essential to meeting our carbon targets. This project, which repurposes fossil fuel extraction infrastructure and expertise to sequester carbon, is a forward-looking way to remove emissions while creating jobs in an emerging sector. Simply put, getting projects like this operating in a safe and effective way is critical for our climate progress.”

source: CRC

Additionally, combating methane emissions is a vital element of its net zero strategy. It aims to reduce methane emissions by 30% from the 2020 baseline by 2030.

CRC also plans to reduce freshwater use by 30% by 2025 which exceeds California’s 15% target. Moreover, it supplies more treated water to California districts than it uses. This is one of the ways the company is helping address the state’s water challenges.

source: CRC

Carbon capture technologies safely capture carbon from industrial processes or the air, then transport and store it permanently underground. Thus, CRC’s role in decarbonizing California is huge with this project in their priority.

Prime Minister Justin Trudeau’s announcement to step down has created a vacuum that will shape the future of Canada’s leadership. This decision has ignited a fierce race for leadership within the Liberal Party, with former Bank of Canada Governor Mark Carney emerging as a key contender. On the other side, Conservative Party Leader Pierre Poilievre stands in stark opposition, ready to challenge the current climate policies.

With the ideological divide between Carney’s progressive climate agenda and Poilievre’s economic-focused stance, Canada’s climate future hangs in the balance. Let’s take a closer look at each of the potential replacements’ climate and net zero stance.

Mark Carney: A Champion of Climate Finance and Global Leadership

Mark Carney’s entry into the political race marks a significant moment for Canada and the global climate movement. Carney’s extensive experience as the Governor of the Bank of Canada, along with his tenure as the UN Special Envoy on Climate Action and Finance, positions him as a leading figure on the international stage.

For years, Carney has been a vocal proponent of transitioning to a net-zero economy. He has been emphasizing the potential for economic growth through climate action.

“…And what we have seen increasingly, spurred initially by the Sustainable Development Goals, accelerated by Paris, and then by social movements and governments, is societies putting tremendous value on achieving net zero. Companies, and those who invest in them and lend to them, and who are part of the solution, will be rewarded. Those who are lagging behind and are still part of the problem will be punished.”

He sees it as a way to unlock investment in renewable energy, clean technologies, and sustainable infrastructure.

A recent report by the International Renewable Energy Agency (IRENA) estimates that the global renewable energy market could generate up to $98 trillion in investment by 2050. This presents a significant economic opportunity for countries, like Canada, that choose to embrace green policies.

Carney’s vision for the country aligns with global trends, calling for a balanced approach to climate policy that integrates both environmental and economic goals. His leadership would likely usher in policies focused on scaling up investments in clean energy, carbon capture technologies, and creating more sustainable industries.

Under Carney, Canadians could see the implementation of mandatory carbon disclosure for corporations, helping drive transparency and accountability in the private sector. The UN climate envoy also advocates for leveraging private sector finance to accelerate the transition to a net-zero economy.

Pierre Poilievre: Opposing Carbon Taxes and Prioritizing Affordability

Pierre Poilievre, the current leader of Canada’s Conservative Party, has built his political identity on opposing carbon taxes. He is also questioning the effectiveness of environmental regulations.

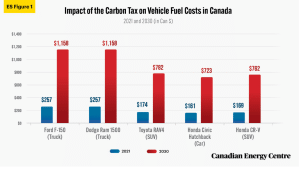

With his populist messaging and a strong emphasis on affordability, Poilievre has become a leading figure for those disillusioned by rising costs of living. His “Axe the Tax” campaign resonates with voters who view the carbon tax as an economic burden rather than a solution to climate change. The campaign aimed at eliminating Trudeau’s carbon pricing system.

Per the Canada Taxpayers Federation, the carbon tax under the current system costs an average family of four $1,200 annually. The chart below from the Canadian Energy Centre shows how much it will affect vehicle fuel costs by 2030.

Poilievre’s criticism of the carbon tax is largely driven by concerns over this financial impact. This becomes more paramount as inflationary pressures and cost-of-living concerns continue to grow.

Poilievre’s anti-carbon tax stance has been consistent. He argues that it disproportionately affects working Canadians, driving up the cost of goods and services, particularly in northern communities.

While Poilievre has voiced concern about the economic impact of such policies, he has yet to present a clear and actionable alternative to address climate change. His positions on climate policy, therefore, raise questions about Canada’s ability to meet its emissions reduction targets without strong regulatory frameworks.

Under Poilievre’s leadership, Canada might see a rollback of several key climate policies, including the following:

carbon tax,

emissions caps for oil and gas, and

investments in clean energy technologies.

Analysts think that this would likely distance Canada from international climate commitments, potentially putting the nation at odds with global efforts to mitigate climate change.

A Deepening Divide: What’s at Stake for The Future of Canada’s Climate Policy?

Trudeau’s resignation sets the stage for a new political era. The next leadership race will be pivotal in determining Canada’s climate future.

According to Environment and Climate Change Canada, the country must reduce emissions by at least 40-45% by 2030 compared to 2005 levels to meet its international commitments.

Carney’s policies would likely drive the investments and regulatory changes necessary to achieve these ambitious goals. On the other hand, Pierre Poilievre’s rise to power could shift Canada’s climate trajectory in a different direction. Prioritizing deregulation and affordability over bold climate action could lead to a retreat from critical environmental commitments.

Moreover, Carney’s proposed policies on climate finance, carbon pricing, and clean energy investments align with global efforts on sustainability. These measures reflect a commitment to both tackling climate change and positioning Canada as a leader in climate finance.

A report from Canada’s Clean Growth Hub reveals that Canada’s renewable energy sector has seen significant growth. It contributes nearly $4.5 billion to the national economy in 2020 alone. Carney’s platform would likely continue to build on this momentum as he noted in his speeches, further bolstering the sector.

In contrast, Poilievre’s carbon pricing opposition prioritizes short-term economic relief for Canadians. While Poilievre’s stance might appeal to those frustrated with rising costs, it lacks a clear strategy for long-term climate solutions.

As the leadership race heats up, Canadians will have to decide which path they want to take: Will the nation take the opportunity to lead in global climate action, or will it retreat from its environmental commitments? The outcome will not only shape Canada’s domestic climate policy but also its role in the global fight against climate change.

Donald Trump’s return to the White House in 2025 is already shaking up industries across the globe, particularly those reliant on stable trade and environmental policies. From sweeping tariffs to anticipated rollbacks of key climate initiatives, the impact of these changes could redefine global markets and state-led sustainability efforts.

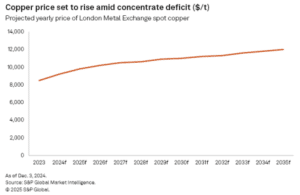

Copper, the backbone of global infrastructure and clean energy transitions, faces unprecedented challenges. Trump’s proposed tariffs, which could range from 10% to 100%, are poised to disrupt the market’s fundamentals.

Targeting major U.S. trading partners, including China, Canada, and Mexico, these tariffs are expected to inflate prices and dampen demand.

David Davidson, an analyst at Paradigm Capital, warns that these trade policies could lead to a tit-for-tat scenario, specifically noting:

“If we get a tit-for-tat trade war, then kiss global economic growth expectation goodbye.”

A strong U.S. dollar and sustained high interest rates, as the Federal Reserve grapples with likely inflation, could further compound these issues by making copper imports prohibitively expensive.

China, which consumes nearly half of the world’s copper, is especially critical in this equation. Economic slowdowns or retaliatory tariffs from China could reverberate across global markets, suppressing demand for the metal.

The country’s faltering property market, which has historically driven copper demand, remains a weak point. Analysts speculate that a substantial stimulus package from China might offset some of these challenges, but its timing and scale remain uncertain.

Tight Supply Chains

Adding to the turmoil is a looming deficit in copper concentrate supplies. S&P Global Commodity Insights projects a supply shortfall of 540,467 metric tons in 2025. This is exacerbated by delays in reopening First Quantum Minerals’ Cobre Panama mine.

The mine’s closure in 2023 following a dispute with Panama has left the market scrambling for alternatives, and analysts doubt it will resume operations before 2026.

Despite a projected surplus in refined copper, the concentrate deficit could severely impact smelters, particularly in Asia, which rely on steady supplies. Prices will reflect this tension, with the London Metal Exchange forecasting an average copper price of $9,734 per metric ton in 2025.

Last year, there was also a recorded deficit but with an anticipated electric vehicle (EV) boom, where copper is a key component, the demand for this metal will grow. BHP projects a 70% surge in global copper demand, exceeding 50 million tonnes annually by 2050. The traded metal is anticipated to grow at an average annual rate of 2%.

Blue States vs. Trump: The Battle for Climate Progress

While federal climate policy may see significant rollbacks under Trump, blue states (which lean Democratic) are gearing up for a fight. State leaders in progressive regions are determined to protect climate initiatives, even as federal support wanes.

California, a leader in climate action, faces the dual challenge of maintaining its ambitious emissions reduction targets while fending off federal interference.

A key battleground is the state’s waiver to set stricter vehicle emissions standards than those enforced federally. This waiver, which allows other states to adopt California’s rules, is critical to the state’s goal of reducing greenhouse gas emissions 40% below 1990 levels by 2030.

Revoking this waiver, as Trump is widely expected to attempt, could disrupt these efforts and ignite legal battles. Noel Perry, founder of the California think tank Next 10, emphasized the importance of the waiver. Perry noted that:

“California will fight tooth and nail if the Trump administration is going to again attempt to take that waiver away.”

Fiscal Challenges and Climate Goals

Complicating matters further are fiscal challenges in many blue states. California, New York, and Maryland, among others, face significant budget deficits that threaten to undermine their climate initiatives.

California has already reduced its climate-related spending by 21% for the next 8 years, though voters approved a $10 billion climate bond in November 2024 to fund drought mitigation and renewable energy infrastructure.

In New York, a $13.9 billion budget gap between 2025 and 2029 is putting pressure on the state’s ambitious climate goals. The state’s 2019 Climate Leadership and Community Protection Act mandates 70% renewable energy by 2030 and full decarbonization by 2050. However, achieving these targets amid fiscal constraints and uncertain federal policies will be a steep uphill battle.

2025: A Year of High Stakes for Sustainability and Global Markets

Despite the obstacles, blue states are not backing down. Washington Governor Jay Inslee, speaking at the COP29 climate summit, declared that state-led initiatives remain unstoppable. He remarked that Trump won’t be able to stop any of the states from moving forward, citing Washington’s cap-and-invest program and low-carbon fuel standards as examples.

California has allocated $25 million for litigation costs to defend its climate policies. Legal battles could intensify as the Trump administration targets state-level initiatives.

Trump’s trade and climate policies have far-reaching implications. For the copper market, they risk destabilizing supply chains and inflating prices, which could hinder the global clean energy transition.

Meanwhile, his administration’s deregulatory agenda poses challenges to state-led climate progress, even as blue states demonstrate resilience and determination.

With 2025 shaping up as a year of uncertainty, the stakes are higher than ever. Stakeholders, especially industries and governments, must balance economic growth with the urgent need to address climate change. How these competing priorities unfold will define the next chapter in the global effort to achieve sustainability.

In 2024, hydrogen emerged as a climate-friendly alternative to fuel as well as electricity. Promising projects sparked to life on both the production and consumption fronts. Despite Trump’s pro-oil stance, analysts are optimistic about hydrogen’s future in this new year- 2025.

According to BNEF, clean H2 supply is projected to increase 30X and could reach 16.4 million metric tons annually by 2030. This surge ismostly attributed to supportive policies and a flourishing project pipeline.

As we step into 2025, several crucial moments await the low-carbon, clean hydrogen sector. They could be a mix of challenges and opportunities. Analysts also predict an increase in the fructification of significant projects and financial investment decisions this year.

Wood Mackenzie recently released a report identifying some crucial developments in the hydrogen sector for 2025 that one needs to scrutinize. Let’s study it here.

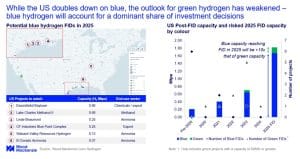

Blue Hydrogen to Dominate the U.S. Market in 2025

In 2025, the U.S. hydrogen market will focus heavily on blue hydrogen, with over 1.5 million tons per annum (Mtpa) of capacity reaching the final investment decision (FID).

This marks a 10X increase compared to green hydrogen. The report revealed that at least three large-scale blue hydrogen projects are expected to mature this year. With this output, theU.S. has all the potential to become the world’s leading blue hydrogen producer.

Green Hydrogen to Face Strong Headwinds in 2025?

Conversely, green hydrogen projects are likely to face major challenges in 2025. FIDs for these projects are expected to fall short of expectations. This could be due to reduced government focus on clean energy under the Trump administration.

Green hydrogen could also face stiff competition for electricity resources from data centers. On top of that, lengthy delays in connecting projects to the grid can slow down the progress.

While some demand will come from companies working toward sustainability goals, short-term growth opportunities are expected to shrink. Many green hydrogen projects, especially those targeting transportation, andheavy industries like steel, and e-fuels, may be delayed or canceled altogether.

If not in the U.S. green hydrogen will have its niche in emerging economies like South America, the Middle East, India, and China. Eventually, these economies can launch giga-scale projects in 2025. So how can these nations properly green hydrogen progress globally?

Well, these projects leverage cheap solar and wind power and government incentives that reduce costs and ensure financial viability. For instance, India’s Kakinada project utilizes existing ammonia infrastructure and enjoys government subsidies.

Meanwhile, Saudi Arabia’s Neom Helios project benefits from state-led support and a 30-year offtake agreement with Air Products. These factors add a bonus point to green hydrogen.

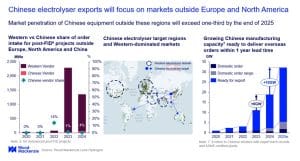

Emergence of Chinese Electrolyzers

Most importantly regions like Southeast Asia, the Middle East, and North Africa will benefit abundantly from low-cost renewable energy and affordable electrolyzers from Chinese manufacturers.

By 2025, China can supply at least one-third of orders outside North America and Europe. Competitive pricing, shorter delivery times, and strong manufacturing capacity give Chinese electrolyzers an edge. Moreover, China is also expanding its domestic manufacturing capacity and is most likely to add over 10 GW of capacity this year. This will further strengthen their global presence, especially in areas with fewer trade barriers.

However, entering Europe and North America is more challenging. Trade restrictions and regulatory hurdles, such as the European Union’s 25% content limit for Chinese-made electrolyzers, limit their opportunities. To overcome these challenges, some Chinese companies are localizing production through partnerships and technology licensing.

Green Hydrogen’s Stance in Europe and North America

While blue hydrogen dominates the U.S., green hydrogen is making headway in Europe and North America. The European Commission (EC) also launched a nearly €2 billion hydrogen auction as part of its broader €4.6 billion initiative to accelerate net-zero technologies. This marked a significant step in the EU’s push for renewable hydrogen.

In Germany, HydrogenPro partnered with J. Heinr. Kramer Group to develop green hydrogen projects ranging from 5 MW to 50 MW. They aim to advance green hydrogen projects in Germany, Austria, and the Benelux region. These projects will power industries and the grid, and fuel hydrogen-powered vehicles.

On October 30, 2024, Avina Clean Hydrogen announced its major green hydrogen project in Vernon, California, near the Port of Long Beach. The facility with a capacity of 4 metric tons of compressed green hydrogen daily can decarbonize heavy-duty transport and advance California’s clean energy goals.

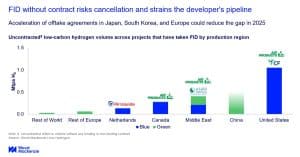

The Woodmack report emphasized another interesting scenario that would prevail in this year’s hydrogen economy. It says uncontracted low-carbon hydrogen capacity will remain a challenge due to difficulties in securing offtake agreements. This means out of the 5.5 Mtpa of low-carbon hydrogen projects that have reached FID, ~ 2.5 million tons of hydrogen remains without contracts.

This issue is most common in the U.S. blue hydrogen sector and, to a lesser extent, outside China, where securing agreements is tougher. The Chinese green hydrogen market lacks transparency in offtake contracts. So, the real value of uncontracted investment is not clear.

Moving on European policies like the Emission Trading Scheme (ETS) and the Carbon Border Adjustment Mechanism (CBAM), make it a key market for blue hydrogen and its derivatives. So, developers may keep production uncontracted to benefit from higher prices in Europe.

Overall, uncontracted hydrogen volumes may shrink for some projects, but overall, they are expected to grow as more blue hydrogen projects reach FID this year.

The U.S. Treasury Simplifies Clean Hydrogen Tax Credit Rules

The U.S. Department of the Treasury and IRS released final rules for the section 45V Clean Hydrogen Production Tax Credit under the Inflation Reduction Act on January 3. These rules encourage clean hydrogen production from some nuclear power plants that are nearing retirement. The hydrogen will be used in fuel cells.

The new rules included someimportant changes and added flexibility for the clean hydrogen industry. These updates will propel projects ahead and ensure they comply with the emissions requirement laws to qualify for clean hydrogen.

Notably, they will also provide much-needed clarity, investment stability, and adaptability, especially for participants in the Department of Energy’s Regional Clean Hydrogen Hubs program.

The final rules clarify how hydrogen producers,using electricity from diverse sources, natural gas with carbon capture, renewable natural gas (RNG), or coal mine methane, can qualify for the tax credit.

Nuclear for Clean Hydrogen

As the fresh rules enable at-risk nuclear to produce clean hydrogen, it will subsequently boost nuclear energy demand in sectors like AI. S&P Global reported market optimism surged following the announcement, and energy companies saw significant gains.

For instance, Constellation Energy’s shares rose by 3.8%, closing at $251.74, while Vistra experienced a 7% jump, reaching $160.33. NextEra Energy and its renewable energy unit also saw increases of 1.2% and 3%, respectively. Plug Power recorded a 2.6% rise, closing at $2.39. These positive market movements were witnessed after Constellation announced a $1 billion contract to supply nuclear energy to 13 government agencies.

John Podesta, Senior Advisor to President Biden for International Climate Policy mentioned something very significant that sums up all for the U.S. green hydrogen future. He said,

“The extensive revisions we’ve made in this final rule provide the certainty that hydrogen producers need to keep their projects moving forward and make the United States a global leader in truly green hydrogen.”

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy

Source: SolarBank

Source: SolarBank Source: SolarBank

Source: SolarBank

")

Source: California Air Resources Board

Source: California Air Resources Board source: CRC

source: CRC source: CRC

source: CRC