Singapore and Ghana signed a carbon credit agreement on May 27, 2024, in a significant step towards global environmental sustainability. This deal enables businesses in Singapore to offset a part of their carbon tax by investing in certified carbon reduction projects in Ghana.

Unlocking the Details of the Singapore-Ghana Carbon Credits Agreement

The carbon credit agreement, officially known as the “Implementation Agreement” promotes cooperation under Article 6 of the Paris Agreement. Singapore’s Minister for Sustainability and the Environment and Minister-in-charge of Trade Relations, Grace Fu, and Ghana’s Minister of Environment, Science, Technology and Innovation, Ophelia Hayford, officiated the signing.

The important attributes of this agreement are:

Project developers must contribute 5% of proceeds from authorized carbon credits to climate adaptation efforts in Ghana. It would assist the country in preparing for climate change impacts.

Developers will have to cancel 2% of authorized carbon credits upon initial issuance to contribute further to global emissions reduction. These carbon credits cannot be sold, traded, or counted towards any country’s emission targets. They will contribute only to a net decrease in global emissions.

Under Singapore’s International Carbon Credit (ICC) framework, eligible ICCs from this Implementation Agreement can be used by Singapore-based companies to offset up to 5% of their carbon tax liabilities.

The Agreement can meet binding mandates like Nationally Determined Contributions (NDCs) and international mitigation requirements such as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

Singapore’s Minister Grace Fu said,

“Singapore and Ghana share many mutual interests in the sustainability sphere. The conclusion of the Implementation Agreement is a testament to our shared commitment to advance global climate action through high-integrity carbon markets.”

She further assured that carbon credit projects under this Agreement will deliver climate and economic benefits. Subsequently, Singapore will keep collaborating with partners like Ghana to create opportunities for a sustainable future.

Media reports state that the bilateral agreement follows Temasek-backed investment platform GenZero’s ongoing investments in a forest restoration project in Ghana’s Kwahu region.

The project, in collaboration with Singapore-based AJA Climate Solutions, aims to replant degraded forest reserves. It includes sustainably growing cocoa trees in shaded farms to protect them from climate impacts like floods, heat stress, and pests.

The project area within the Kwahu region, once a lush forest 40 to 50 years ago, has been heavily exploited for timber in recent decades. This deforestation has resulted in Ghana losing more cocoa hectares each year, leading to economic downfall. Consequently, this Agreement under Article 6 and the project came as a blessing for Ghana.

The forest project will eventually focus on regenerating native tree species across degraded forests. It plants to grow 20 million seedlings within seven years to balance the impact of heavy deforestation.

Talking about economic benefits, Ghana will experience increased investment in its green projects.

These initiatives, which range from reforestation to renewable energy, will not only reduce carbon emissions but also promote sustainable development and create job opportunities within Ghana.

Supporting Singapore’s Climate Goals

For Singapore, this partnership is a strategic move to meet its ambitious climate goals. The city-state has committed to cut down its GHG emissions by 50% by 2030. The country aims to help businesses by allowing them to offset their carbon taxes through overseas credits.

Notably, the Kwahu project extends Singapore’s intergovernmental partnerships regarding Article 6. In November 2022, Singapore and Ghana finalized substantive negotiations on the Implementation Agreement on Cooperative Approaches. This agreement allows for the bilateral transfer of carbon credits aligning with Article 6.

Singapore is most likely to witness the following impacts on its carbon credit economy:

Carbon credits traded under this Implementation Agreement, upon completion, might offset a portion of corporate carbon tax liabilities in Singapore.

This would be the first project in the country to generate carbon credits with corresponding adjustments under this Implementation Agreement.

We may infer that the carbon credit agreement offers a win-win scenario economically and environmentally. Singaporean companies gain flexibility in managing their carbon tax liabilities, potentially lowering their operational costs. Simultaneously, Ghana benefits from the inflow of funds into its green economy, bolstering its efforts to combat climate change and fostering economic growth.

However, both nations must establish a robust monitoring and verification mechanism to maintain the integrity of the carbon credits.

All said and done, The Singapore-Ghana carbon credit agreement can leverage international cooperation to combat global climate change. No wonder it provides a scalable model for other nations to follow and paves the way for a more sustainable future.

Enbridge Inc. has received a permit from Wyoming’s Industrial Siting Council to proceed with a major solar-plus-storage project in Laramie County, Wyoming. The $1.24 billion Cowboy Solar I & II Project, paired with the Cowboy Battery Project, will be one of the largest in the U.S., featuring up to 771 MW of solar power and 269 MW of battery storage.

Solar power, using the sun’s energy to produce electricity, is fundamental to the global move toward sustainable energy. As a clean and renewable resource, it plays a crucial role in reducing greenhouse gas emissions and addressing climate change.

Enbridge’s Solar Ambitions Take Root

In the United States, solar energy has grown tremendously due to technological improvements, falling costs, and greater environmental consciousness. This rapid expansion has also propelled the rising demand for battery storage, positioning Enbridge in this burgeoning industry.

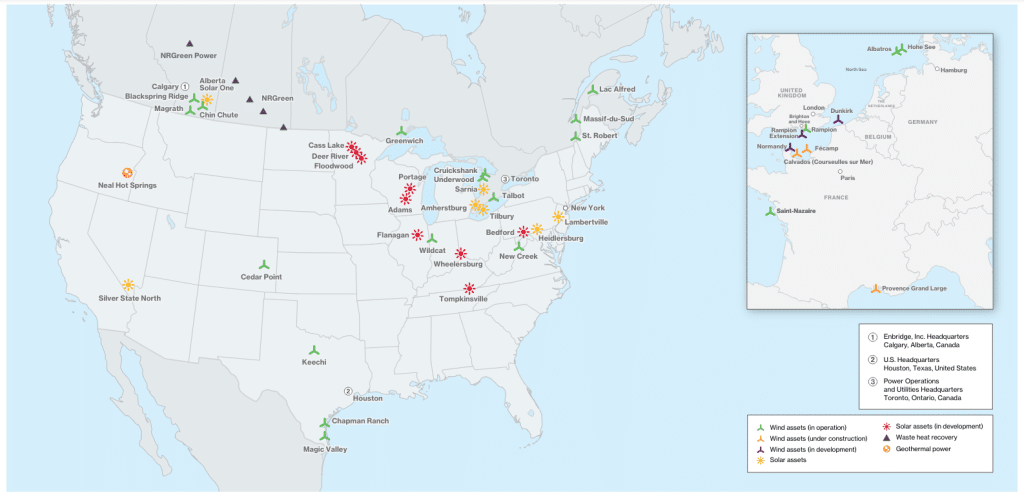

Enbridge, headquartered in Calgary, Alberta, operates natural gas, oil, and renewable energy projects across North America. It is the region’s largest natural gas utility by volume and owns the world’s longest crude oil and liquids pipeline system.

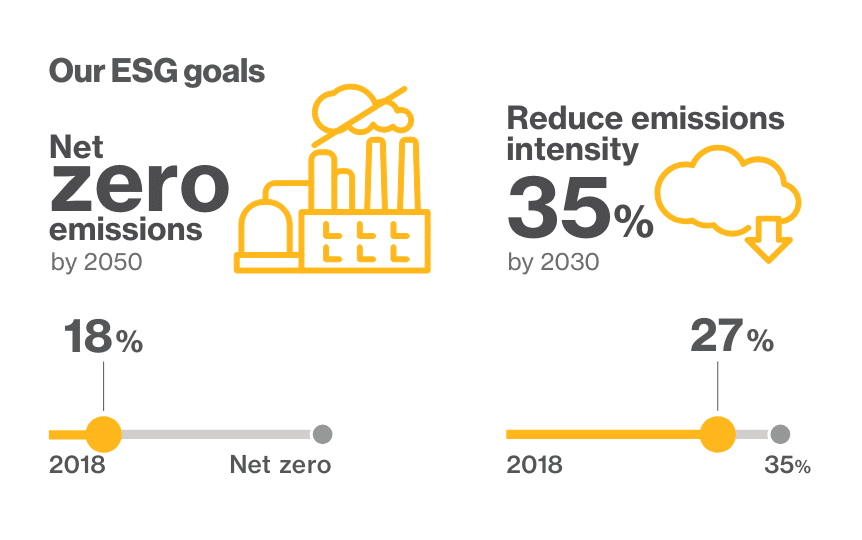

As pressure for companies to help in decarbonization efforts continues to intensify, energy companies must step up in slashing their carbon footprint. Enbridge is employing various means to decarbonize its operations and reach net zero by 2050.

In 2020, Enbridge set new ESG targets, including a goal to reduce GHG emissions intensity by 35% by 2030. Since 2018, the energy company has achieved a 27% reduction in emissions intensity.

Enbridge Net Zero

In 2022, despite increased energy consumption, Enbridge saw a slight decrease in emissions intensity, mainly due to enhanced system efficiency and the use of lower-intensity power.

The company is reducing the emissions intensity of the electricity it buys with solar self-power projects and advocating for policies that decarbonize the power grid. Below are the company’s renewable projects, operational and under development.

Source: Enbridge net zero report 2023

A Landmark Solar-Plus-Battery Storage Initiative

The $1.24-billion Wyoming solar-plus-storage project is one of the initiatives Enbridge pursues as part of its net zero efforts. Construction will start in March 2025, with the first phase expected to be operational by January 2027 and the second by August 2027.

The first phase includes a 400-MW photovoltaic (PV) system and 136 MW of battery storage, while the second phase will add 371 MW of PV and 133 MW of storage.

Fluence Energy Inc. will supply the battery system, and American Hyperion Solar LLC, a subsidiary of China’s Jiangsu Runergy New Energy Technology Co. Ltd., will provide the solar panels.

The project will connect to the local grid operated by Cheyenne Light Fuel and Power Co., an affiliate of Black Hill. Enbridge’s application mentions planned data centers in Laramie County, including one by Microsoft Corp., which will require substantial electrical power.

Enbridge’s gas utilities in Canada are receiving requests from data centers, according to Cynthia Hansen, president of gas transmission and midstream. She noted that they’re supplying the utilities that are getting such requests. While their main lines haven’t received direct requests from data centers yet, they would support those markets through their utilities.

The Wyoming project faced some opposition from local mining and ranching interests but received support from the Cheyenne-Laramie County Corporation for Economic Development and local labor groups. Enbridge estimates a peak workforce of around 375 workers during construction.

John Fulk, business manager of Construction and General Laborers’ Local 1271, remarked on the project approval, saying that:

“The development of solar, wind power and battery storage creates an opportunity for the state’s legacy coal workers to expand their skills so they may fully participate in new job opportunities created by the energy transition.”

Enbridge’s Pathway to Reducing Carbon Footprint

In addition to its renewable energy initiatives, the energy company is also balancing residual emissions by purchasing carbon offset credits. These credits are from nature-based solutions and renewable energy credits, with a primary focus on areas near their operations. According to its recent net zero report, the company invested a total of $350,000 in carbon credit projects.

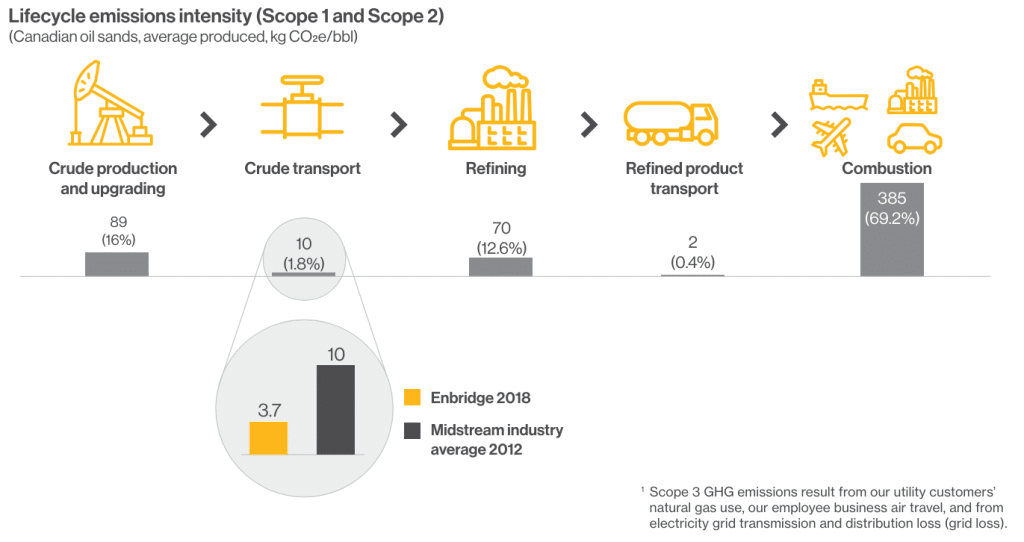

Enbridge’s GHG emissions reduction targets focus specifically on Scope 1 and Scope 2 emissions. However, carbon emissions from the midstream constitute only a small part of its total GHG emission on a lifecycle basis.

Oil sands transportation accounts for less than 2% of lifecycle emissions, with most emissions from combustion, production, and upgrading. Enbridge leads in tracking, reporting, and reducing Scope 3 emissions, doing so since 2009 despite limited sector guidance.

The company reports on utility customer natural gas use, employee air travel, and electricity grid loss. In 2021, Enbridge added metrics for emissions intensity of delivered energy and emissions avoided through renewables, lower-carbon fuels, and conservation programs. They’re also committed to collaborating with suppliers to further reduce Scope 3 emissions.

Through innovative projects and comprehensive emission reduction strategies, Enbridge continues to lead in the global shift towards renewable energy.

Lithium, a critical element in modern technology, has become a focal point in discussions about renewable energy and electric vehicles (EVs) due to its importance in batteries. The fluctuating prices of lithium have significant implications for industries and economies worldwide. This article explores the dynamics of lithium pricing, offering insights into historical trends, current market conditions, future predictions, and the key factors that drive its valuation.

Background Information

Lithium is a soft, silvery-white metal belonging to the alkali metal group. It is highly reactive and flammable, making it essential in various industrial applications. Most notably, lithium-ion batteries power everything from smartphones to electric vehicles.

The demand for lithium has surged with the rise of renewable energy technologies and the global push towards reducing carbon emissions. Lithium’s unique properties make it irreplaceable in high-performance batteries, which are pivotal in energy storage solutions and portable electronics.

Lithium is also on several countries’ Critical Minerals lists, such as the U.S., Canada, and Australia.

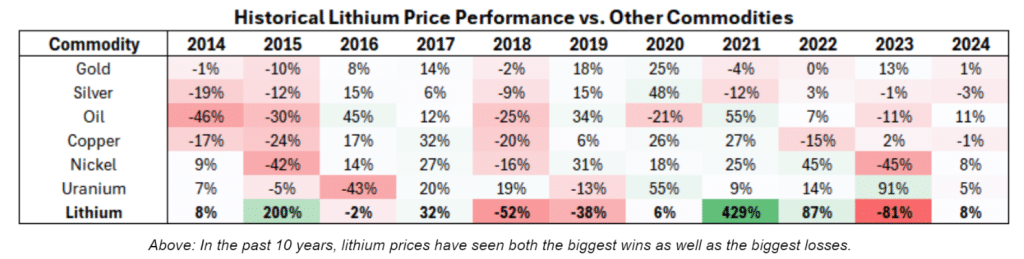

Historical Lithium Price Trends

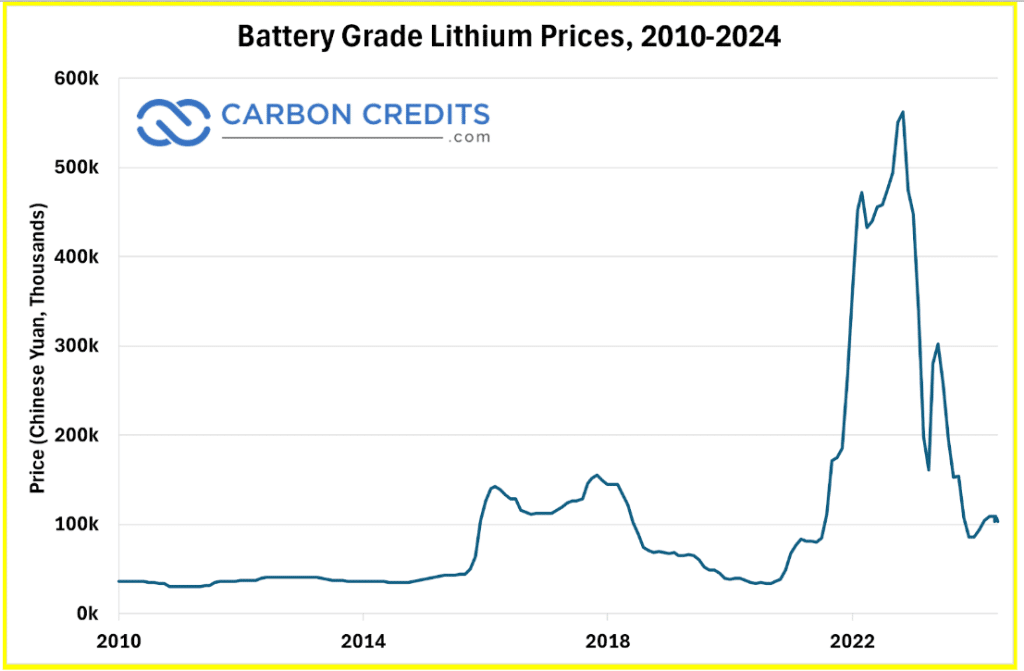

Lithium prices have seen dramatic changes over the past decade. From 2010 to 2015, prices remained relatively stable, with minor fluctuations due to steady demand and supply conditions. However, from 2015 onwards, prices began to soar, driven by the booming EV market and increased demand for renewable energy storage solutions.

By 2017, lithium prices had tripled compared to their 2015 levels. This spike was primarily due to the rapid expansion of China’s EV market and increased lithium mining and production investments.

The year 2018 saw prices peaking, but by 2019, an oversupply in the market led to a sharp decline. From 2019 to 2021, prices remained subdued, reflecting a period of market correction and stabilization.

In 2022, however, a record-breaking price rally occurred due to a large supply deficit. Lithium’s largely agreement-based supply model also contributed to this squeeze, sending lithium prices skyrocketing over 5x. This push would continue until midway through the year as China re-implemented full lockdowns nationwide due to rising COVID-19 case numbers, leading to a brief economic slowdown.

While the end of lockdowns coincided with another surge in demand, sending lithium prices to their all-time high of 575,000 CNY (USD 80,000) per tonne, this rally was short-lived. With inflation rates on the rise and EV supply finally overtaking demand, lithium prices plummeted back down in 2023 before stabilizing around the 100,000 CNY (USD 14,000) level, where it continues to trade today.

The past few years have been marked by significant market adjustments. Producers ramped up supply, anticipating continuous high demand, but the market did not grow as quickly as expected.

Consequently, this led to a surplus, driving prices down. Moreover, technological improvements in mining and processing lithium contributed to cost reductions, which also played a role in lowering market prices during this period.

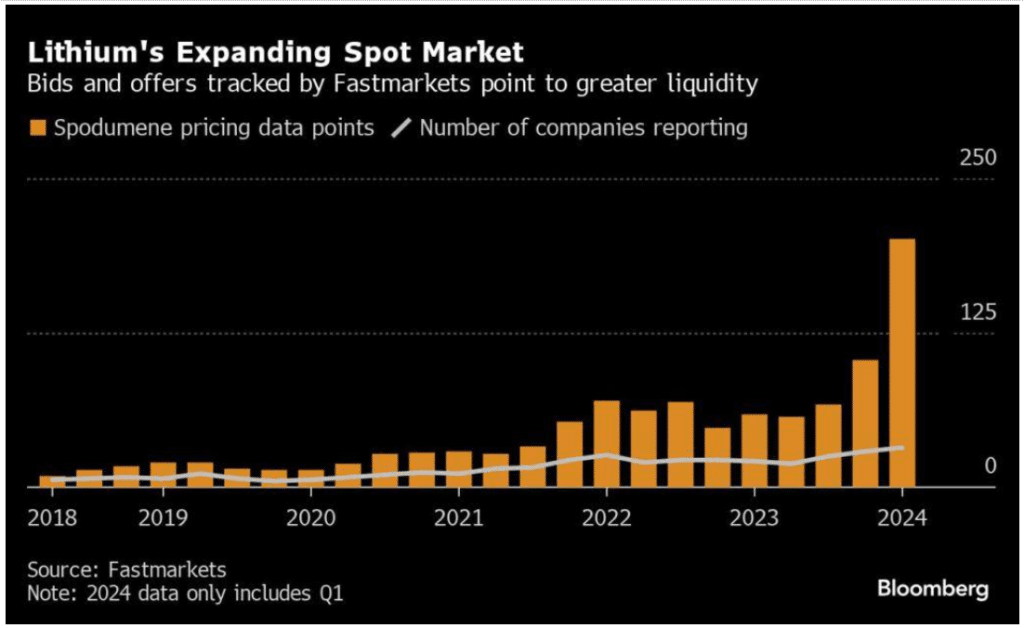

Lithium Price Volatility

One of the main factors contributing to the volatility of lithium prices is that unlike other minerals like gold or copper, the lithium markets are still fairly young and hence the spot market is not very well established. With the recent explosive growth in lithium demand added on top of that, the result is a market sector that’s very much still going through growing pains.

Right now, instead of purchasing contracts for delivery on a spot market most lithium consumers choose to directly sign long-term offtake agreements with lithium miners, securing a guaranteed supply at a fixed price. The current state of the lithium markets has drawn parallels to the iron ore market prior to the 2010s, where pricing would follow an annual benchmark negotiated between miners and steelmakers each year.

In the early 2000s, explosive growth in iron ore demand from China was the catalyst that finally led to change in the iron ore markets. It would take a concerted effort from BHP and other top miners for the iron ore markets to shift towards the spot pricing model it follows today.

Something similar is happening in the lithium markets, with top producer Albemarle having begun holding auctions for its mined lithium since March 2024. These auctions allow buyers to secure pricing that’s more truly reflective of the present supply-demand dynamic, as opposed to being forced to lock in fixed long-term pricing to avoid not having enough supply.

Albemarle plans on holding auctions every two weeks in order to provide more timely and consistent data on lithium pricing.

The lithium spot market has been seeing increasing activity as well, as shown in the chart above. In conclusion, while lithium prices will likely continue to be volatile for the foreseeable future, there are changes under way that will help stabilize the market as it matures and develops.

Current Market Analysis

As of 2024, lithium prices have stabilized from their major plunge of 2022-2023. The current price is attributed to several factors:

Increased Demand: The global shift towards electrification and decarbonization has accelerated the demand for lithium-ion batteries. EVs, energy storage systems, and consumer electronics continue to drive this demand. The Paris Agreement and other international efforts to curb carbon emissions have further intensified the focus on lithium as a key resource for achieving climate goals.

Supply Chain Dynamics: While demand is rising, supply chain disruptions have hindered the steady flow of lithium. These disruptions are caused by geopolitical tensions, logistical challenges, and regulatory hurdles in major lithium-producing countries. For instance, political instability in regions like South America, where a significant portion of lithium is mined, has led to production slowdowns and export restrictions. However, there is still a significant surplus of lithium supply to work through.

Technological Advancements: Innovations in battery technology, such as solid-state batteries, promise higher efficiency and longer life cycles. These advancements have spurred further investment in lithium production, contributing to the current price dynamics. Additionally, advancements in extraction technologies, such as direct lithium extraction (DLE), are expected to enhance the efficiency and environmental sustainability of lithium production.

The increased focus on domestic production in countries like the United States and Australia is also reshaping the market landscape. Efforts to reduce dependence on imported lithium are driving investments in local mining projects, which, in turn, affect global supply and pricing dynamics.

Future Price Predictions

Looking ahead, the future of lithium prices is shaped by a combination of technological, economic, and geopolitical factors.

Analysts predict that demand for lithium will continue to grow, driven by several key trends:

Expansion of the EV Market: With governments worldwide setting ambitious targets for EV adoption, the demand for lithium is expected to skyrocket. For instance, the European Union aims to phase out internal combustion engine vehicles by 2035, significantly boosting lithium demand. Major automakers are also announcing aggressive plans to electrify their fleets, further driving demand.

Advancements in Energy Storage: Beyond EVs, the need for efficient energy storage solutions in renewable energy systems will drive lithium demand. Solar and wind energy projects increasingly rely on lithium-ion batteries for energy storage, ensuring a steady demand. The development of grid-scale storage solutions is particularly significant, as it addresses the intermittency issues associated with renewable energy sources.

Sustainable Mining Practices: The push for sustainable and ethical mining practices may impact the supply side. While this could constrain supply in the short term, it is expected to ensure a stable and environmentally friendly lithium supply in the long run. Innovations in recycling technologies and the development of closed-loop systems are also expected to play a crucial role in meeting future demand sustainably.

Factors Affecting Lithium Prices

Several factors influence lithium prices, creating a complex and dynamic market landscape:

Supply and Demand Dynamics: The fundamental economics of supply and demand play a crucial role. Any imbalance, such as oversupply or undersupply, directly affects prices. For example, the rapid development of new mining projects can lead to temporary oversupply, depressing prices until demand catches up.

Geopolitical Factors: Lithium-rich countries, such as Australia, Chile, and Argentina, play a significant role in the global supply chain. Political stability and regulatory policies in these regions can impact lithium prices. Trade policies, tariffs, and international agreements also influence the global flow of lithium and its pricing.

Technological Developments: Breakthroughs in battery technology can influence lithium demand. For example, the development of alternative battery chemistries could reduce reliance on lithium, affecting its price. Conversely, improvements in lithium extraction and processing technologies can increase supply efficiency and reduce production costs, impacting prices favorably.

Environmental Regulations: Stricter environmental regulations on mining practices can limit supply and drive up prices. Conversely, advancements in sustainable mining techniques can stabilize prices. The growing emphasis on reducing the environmental footprint of lithium extraction is prompting the industry to adopt greener practices, which may initially increase costs but lead to long-term sustainability.

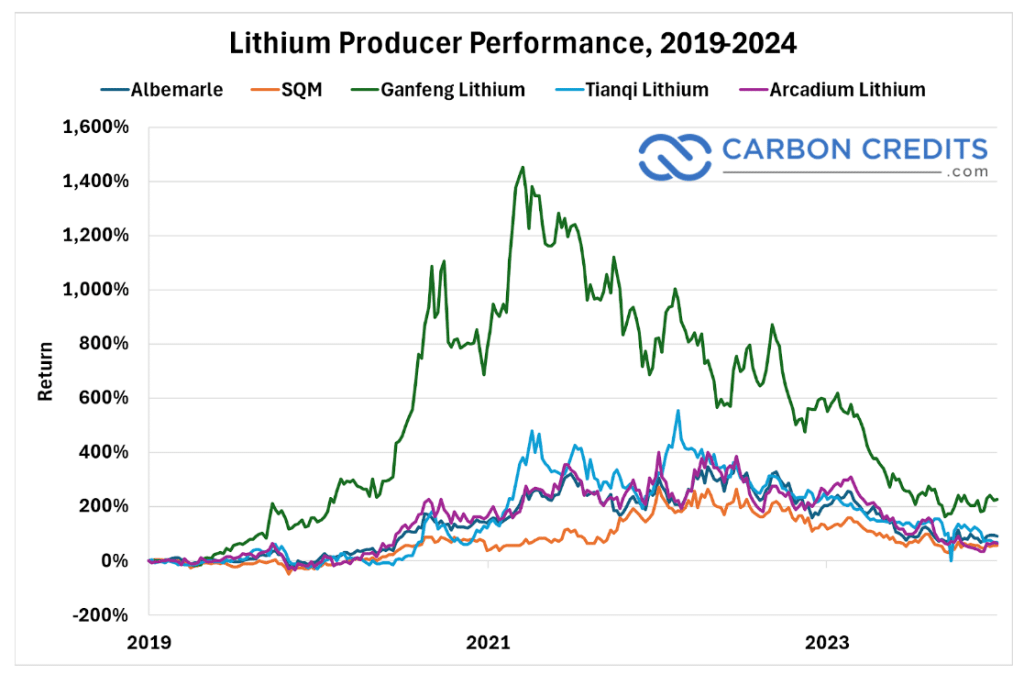

Key Players in the Lithium Market

The global lithium market is dominated by a few key players who control a significant share of the mined supply. Here are five of the top producers from 2023, who combined for roughly half of total global production:

Albemarle Corporation: Currently the world’s largest lithium producer, Albemarle operates major lithium mining projects in Australia and the United States. The company has invested heavily in expanding its production capacity to meet rising demand.

SQM (Sociedad Química y Minera de Chile): Based in Chile, SQM, the world’s second largest producer, is known for its extensive lithium brine operations in the Atacama Desert. The company has leveraged its strategic location and technological expertise to become a dominant player in the market.

Ganfeng Lithium: A Chinese company, Ganfeng is a major player in the lithium market, with operations spanning from mining to battery production. The company’s vertically integrated business model allows it to control the entire supply chain, ensuring stable supply and competitive pricing.

Tianqi Lithium: Another Chinese giant, Tianqi, has significant stakes in lithium mining operations globally, including the Greenbushes mine in Australia. The company’s strategic investments and partnerships have positioned it as a key supplier in the global market.

Arcadium Lithium: A vertically integrated lithium company formed from a merger between American refiner Livent and Australian miner Allkem, Arcadium focuses on high-quality lithium compounds used in batteries and other applications. The company’s commitment to innovation and sustainability has made it a preferred supplier for many high-tech industries.

Environmental Impact: Lithium mining has significant environmental repercussions, including water usage and habitat destruction. Addressing these concerns is crucial for sustainable growth. The industry is under increasing scrutiny to minimize its environmental footprint and adopt greener practices. Expect to see a more pronounced price premium for “green” sustainable lithium once the market matures further.

Market Volatility: Fluctuations in supply and demand combined with the infancy of the lithium markets can lead to volatile prices, making it challenging for investors and producers to plan long-term strategies. The cyclical nature of commodity markets adds to the unpredictability, requiring robust risk management practices.

Technological Risks: Dependence on lithium-ion technology poses a risk if alternative battery technologies emerge, potentially reducing lithium demand. The rapid pace of technological innovation necessitates continuous adaptation and investment in research and development.

Opportunities:

Technological Innovation: Advancements in mining and processing technologies can enhance efficiency and reduce environmental impact. Innovations such as direct lithium extraction (DLE) and improved recycling techniques are expected to revolutionize the industry.

Strategic Investments: Investing in lithium recycling and alternative sources can diversify supply and stabilize the market. Developing secondary sources of lithium, such as extracting lithium from geothermal brines or recycling used batteries, offers promising avenues for ensuring supply security.

Global Collaboration: International cooperation on sustainable mining practices and environmental regulations can ensure a stable and ethical lithium supply chain. Collaborative efforts among governments, industry players, and environmental organizations can drive the adoption of best practices and foster a resilient market.

Types of Lithium Companies: Technology, Exploration, Production, Extraction, Refining

The lithium industry comprises various types of companies, each playing a crucial role in the supply chain. These companies can be broadly categorized into technology, exploration, production, extraction, and refining. Understanding the distinct roles and contributions of each type is essential for grasping the complexity of the lithium market.

Technology Companies

Role and Contribution: Technology companies are pivotal in the development and advancement of lithium battery technologies. These firms focus on enhancing the performance, efficiency, and safety of lithium-ion batteries. Innovations by technology companies drive the demand for lithium by creating new applications and improving existing ones.

Examples:

Tesla: Known for its electric vehicles (EVs), Tesla also invests heavily in battery technology through its Gigafactories, which produce lithium-ion batteries for both EVs and energy storage systems.

Panasonic: Partnering with Tesla, Panasonic manufactures lithium-ion batteries, focusing on improving energy density and reducing costs.

Impact: Technology companies push the boundaries of battery capabilities, influencing the overall demand for high-quality lithium and driving advancements that make renewable energy solutions more viable and efficient.

Exploration Companies

Role and Contribution: Exploration companies are responsible for discovering new lithium deposits. These firms conduct geological surveys, drilling, and sampling to identify potential lithium reserves. Exploration is the first step in the lithium supply chain, determining future supply availability.

Examples:

LiFT Power Corp: An exploration company focused on developing its lithium project in Northwest Territories, Canada, aiming to establish a domestic North American supply of lithium.

Impact: Successful exploration leads to the development of new lithium mines, increasing the global supply of lithium and potentially stabilizing prices. These companies are crucial for ensuring a steady pipeline of lithium resources to meet future demand.

Production Companies

Role and Contribution: Production companies are involved in the extraction of lithium from mines and brine sources. They manage the operations of lithium mines and are responsible for bringing raw lithium materials to the market.

Examples:

Albemarle Corporation: The world’s largest lithium producer in 2023 with operations in Australia and the USA, Albemarle is a key supplier of lithium compounds to various industries.

SQM (Sociedad Química y Minera de Chile): Operating extensive lithium brine extraction facilities in the Atacama Desert, SQM is a leading global producer of lithium.

Impact: Production companies are the backbone of the lithium supply chain, ensuring that sufficient quantities of lithium are available to meet industrial and consumer needs. Their production capacities and efficiencies directly influence lithium prices and availability.

Extraction Companies

Role and Contribution: Extraction companies specialize in the technologies and processes used to extract lithium from raw materials. These firms develop and implement methods for efficiently and sustainably extracting lithium from both hard rock (spodumene) and brine sources.

Examples:

Standard Lithium: Known for its proprietary extraction technology that aims to streamline the lithium extraction process and increase efficiency.

Impact: Advancements in extraction technology by these companies can significantly lower production costs and environmental impact, making lithium more accessible and sustainable. Efficient extraction processes are essential for meeting growing demand while minimizing ecological footprints.

Refining Companies

Role and Contribution: Refining companies are responsible for processing raw lithium materials into high-purity lithium compounds that are suitable for use in batteries and other applications. These companies ensure that the lithium meets stringent quality standards required by technology and battery manufacturers.

Examples:

Ganfeng Lithium: A vertically integrated company that not only mines lithium but also refines it into battery-grade compounds.

Tianqi Lithium: Engages in refining lithium to produce battery-grade lithium hydroxide and carbonate, supplying major battery manufacturers.

Impact: Refining companies add value by transforming raw lithium into a usable form, ensuring a consistent supply of high-quality lithium to downstream industries. Their operations are critical for maintaining the supply chain’s integrity and meeting the specifications required for advanced lithium-ion batteries.

Conclusion

Lithium prices are influenced by a myriad of factors, from technological advancements and supply chain dynamics to geopolitical and environmental considerations. The future of lithium pricing looks promising, with growing demand driven by the global shift towards electrification and renewable energy.

However, addressing the challenges of sustainable production and market volatility will be crucial for long-term stability. As the world continues to embrace green technologies, lithium remains a critical component in the journey towards a sustainable future.

References and Further Reading

Lithium Market Overview and Trends. (2023). International Energy Agency. https://www.iea.org/reports/critical-minerals-market-review-2023/key-market-trends#abstract.

The Future of Lithium: Supply, Demand, and Prices. (2023). BloombergNEF (https://about.bnef.com/blog/the-future-of-lithium-supply-demand-and-pr)

The Biden administration announced the release of the “Voluntary Carbon Markets Joint Policy Statement and Principles”, aiming to enhance and advance the market for carbon credits by establishing the US government’s guidelines to ensuring the high integrity of voluntary carbon markets (VCMs).

This policy statement arrives as demand for carbon offset projects and related credits will surge. It’s primarily due to companies pursuing net zero goals and using offsets to complement their emissions reduction efforts or to balance unavoidable emissions. Notably, the Science Based Targets initiative (SBTi) recently indicated that carbon credits may be allowed in net zero targets to address Scope 3 emissions.

Despite the growth, the market faces significant integrity challenges. Participants struggle to differentiate between high and low-quality projects due to insufficient or inconsistent data on project effectiveness.

Announcing the new carbon credits guidelines, US Treasury Secretary Janet Yellen stated:

“Voluntary carbon markets can help unlock the power of private markets to reduce emissions, but that can only happen if we address significant existing challenges. The principles released today are an important step toward building high-integrity voluntary carbon markets. This is part of the Biden administration’s ambitious efforts to tackle the climate crisis and accelerate a clean energy transition that benefits all Americans.”

Here Are the Key Points of the Policy Guidelines:

Certified Carbon Credits

Carbon credits and the activities that generate them must meet credible atmospheric integrity standards, representing real decarbonization. They should be certified to robust standards for design and MMRV (Measurement, Monitoring, Reporting, and Verification).

Core principles include additionality (activities wouldn’t occur without the crediting mechanism), uniqueness (one credit corresponds to one tonne of CO2 reduced or removed without double-issuance), and real, quantifiable emission reductions. Activities must prevent leakage and be validated and verified by an independent third party.

Permanence is essential, ensuring emissions stay out of the atmosphere for a specified period. More remarkably, robust baselines should avoid over-crediting and reflect advancements in climate policy and technology.

Climate and Environmental Justice

Credit-generating activities should avoid environmental and social harm, supporting co-benefits and transparent, inclusive benefits-sharing. Understanding climate and environmental justice impacts is crucial, and developers should avoid negative externalities for local communities.

Safeguards must prevent adverse impacts on people and the environment, including land use, tenure rights, food security, and biodiversity. Continuous monitoring and mitigation of adverse impacts are necessary, with efforts to enhance positive impacts where possible.

Verified co-benefits, such as sustainable economic development and increased biodiversity, are encouraged. Projects should be designed and implemented in consultation with relevant stakeholders, respecting Free, Prior, and Informed Consent where applicable.

Emissions Reductions Within Value Chains

Corporate buyers of credits should prioritize measurable emissions reductions within their own value chains. The use of credits involves purchasing and canceling or retiring them, and making public claims based on their climate impact. To achieve long-term climate goals, businesses must transform their models across economies.

Credit users should use VCMs to complement measurable within-value-chain emissions reductions as part of their net zero strategies. This includes taking inventory of Scope 1, 2, and 3 emissions, regularly reporting them, setting near-term emissions reduction targets, and adopting transition plans. Where feasible, companies should collaborate with their stakeholders to achieve these goals.

Disclosure of Purchased and Retired Credits

Credit users should disclose purchased, canceled, or retired credits annually, providing details to assess their integrity and environmental and social impacts. This disclosure may exceed legal requirements and should be in a standardized, easily accessible format for comparability.

Users should consider reporting to aggregating resources that disseminate this information publicly, ensuring stakeholders can evaluate the credibility and impacts of the credits.

Public claims by credit users must reflect the true climate impact of retired credits, using only high-integrity carbon credits. Claims should support ongoing incentives for within-value-chain emissions reductions and align with developing frameworks.

Credits should meet high integrity standards, avoiding claims based on reversed or failed credits unless remediated. Corporate climate strategies should prioritize within-value-chain reductions, using credible credits to complement efforts.

Improving Market Integrity

Market participants should enhance market integrity by creating incentives for high-integrity carbon credits, improving transparency, and ensuring fair treatment of suppliers. Measures include preventing fraud, promoting global standards interoperability, and supporting equitable market participation.

Enhancing market functionality involves collaboration among private, public, and civil sectors, focusing on robust data, fair revenue distribution, and clear accounting practices to support the health of VCMs.

Facilitating Efficient Market Participation

Policymakers and market participants should lower transaction costs and support credit providers, especially those in developing countries. Addressing barriers for suppliers can enhance VCMs’ ability to produce high-integrity credits.

Efforts should include using robust models to reduce MMRV costs and providing market certainty for long-term decarbonization investments. Supporting credible credit providers is crucial for advancing decarbonization and generating economic opportunities as part of the climate strategy.

The new US’ voluntary carbon credit guidelines was co-signed by senior administration officials, including Treasury Secretary Janet Yellen, Agriculture Secretary Tom Vilsack, Energy Secretary Jennifer Granholm, Senior Advisor for International Climate Policy John Podesta, National Economic Advisor Lael Brainard, and National Climate Advisor Ali Zaidi.

Xpansiv, a leading provider of market infrastructure for the global energy transition, has finalized a new capital raise led by Aramco Ventures, a major investor in low-carbon energy and sustainability, along with existing investors. This investment will help further develop Xpansiv’s global energy and environmental markets infrastructure solutions and support the company’s investment and acquisition strategy.

Strengthening Market Infrastructure for Sustainable Growth

Xpansiv runs the largest spot exchange for environmental commodities, including carbon credits and renewable energy certificates. As the premier provider of registry infrastructure for energy, power, and environmental markets, Xpansiv also operates the largest independent platform for managing and selling solar renewable energy credits in North America.

Aramco Ventures is the corporate venturing subsidiary of Aramco, the world’s leading fully integrated energy and chemical enterprise. Headquartered in Dhahran, Aramco’s investments primarily support Aramco’s operational decarbonization, new lower-carbon fuels businesses, and digital transformation initiatives.

The investment from Aramco Ventures is part of its Sustainability Fund, which focuses on companies that can support Aramco’s goal of achieving net zero Scope 1 and Scope 2 greenhouse gas emissions across its wholly owned and operated assets by 2050. This aligns with Aramco’s broader sustainability objectives and commitment to reducing its carbon footprint.

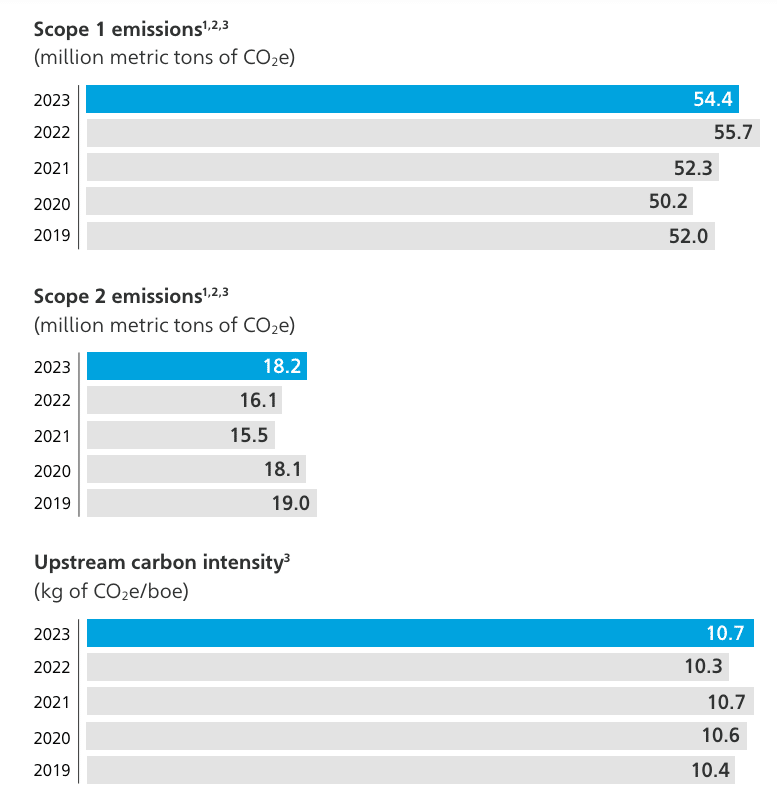

In 2023, the oil major’s Scope 1 emissions decreased by 2.4% compared to 2022, primarily due to lower hydrocarbon production and a revised CO2 venting emissions methodology for gas processing operations, leading to more accurate accounting.

Conversely, Scope 2 emissions increased by 13.0% compared to the previous year. The company said it’s mainly due to the inclusion of the Jazan Refinery in the 2023 greenhouse gas emissions inventory.

As part of its decarbonizing efforts, the oil giant recently invested in a US-based direct air capture (DAC) company, CarbonCapture. Moreover, in line with Saudi Arabia’s Vision 2030 plan, Aramco partnered with ADNOC to launch ambitious lithium extraction projects.

Aramco Ventures also operates Prosperity7, the company’s disruptive technologies investment program. Daniel Carter, Managing Director at Aramco Ventures, emphasized the significance of robust market infrastructure in driving the global energy transition. He noted,

“We recognize the importance of markets to drive the global energy transition at pace, and further recognize Xpansiv’s core position as the innovator of new trading products, marketplaces, and institutional-grade market infrastructure to enable these vital markets to flourish and scale.”

Leading the Charge in Environmental Commodities and Market Integration

John Melby, Chief Executive Officer of Xpansiv, expressed his satisfaction with Aramco’s investment, stating:

“We are pleased to receive this investment from Aramco Ventures and existing investors, which not only represents significant support for our organic and acquisition-driven strategy, but also our shared belief in the pivotal role of market infrastructure in accelerating investment in the global energy transition.”

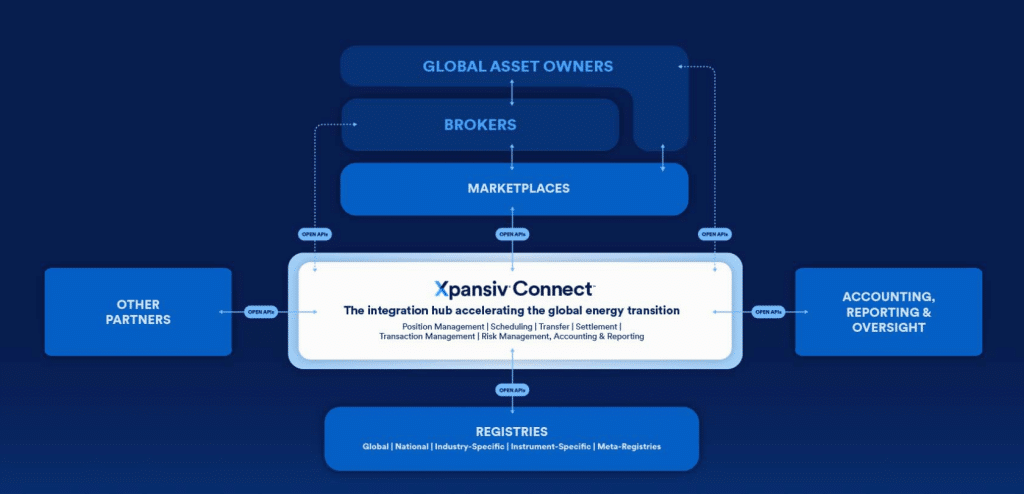

Xpansiv continues to expand its suite of solutions for the global energy transition markets. The company recently launched its Xpansiv Connect™, an open-access market infrastructure which facilitates efficient trading and market operations. This strategic investment will enable Xpansiv to further enhance its capabilities and support the broader push towards sustainable energy solutions.

Xpansiv manages over 1 billion asset transfers annually through its SaaS meta registry and portfolio management system at the core of Xpansiv Connect. This system is integrated with 13 leading carbon and renewable energy registries worldwide.

Xpansiv’s registry software supports more than 80% of global carbon credits and 60% of North American renewable energy certificates (RECs). This along with new environmental commodities such as digital fuels. Its CBL spot exchange holds over 90% global market share of exchange-traded and settled carbon credits.

In 2023, nearly 2 billion metric tons of carbon and over 36 million megawatt hours of renewable energy were transacted by Xpansiv market intermediaries. For live carbon prices, it’s available here.

The company has completed 11 acquisitions and strategic investments recently, including a notable investment in Evident, a leading clean economy registry provider and certification body. This investment highlights Xpansiv’s support for the growing international renewable energy certificate (I-REC) market and emerging instruments. These include sustainable aviation fuel (SAF), green hydrogen, biomethane, and carbon removals.

Xpansiv’s investors include prominent names such as Aramco Ventures, Blackstone Group, Bank of America, Goldman Sachs, Macquarie Group Ltd., S&P Global Ventures, Aware Super, BP Ventures, Commonwealth Bank of Australia, and the Australian Clean Energy Finance Corporation.

By leveraging the new capital raise, Xpansiv will continue to lead in the environmental commodities sector, fostering innovation and efficiency in carbon credits and renewable energy market solutions, crucial for achieving sustainable energy goals and reducing global carbon emissions.

Following Nvidia’s first-quarter earnings report, the company’s CEO Jensen Huang emphasized that it is facing overwhelming demand rather than a lull. This happens as the company transitions from its Hopper AI platform to the more advanced Blackwell system. Huang dismissed concerns about a potential slowdown in demand, stating,

“People want to deploy these data centers right now. They want to put our [graphics processing units] to work right now and start making money and start saving money. And so that demand is just so strong.”

Surpassing Expectations with Stellar Q1 Results

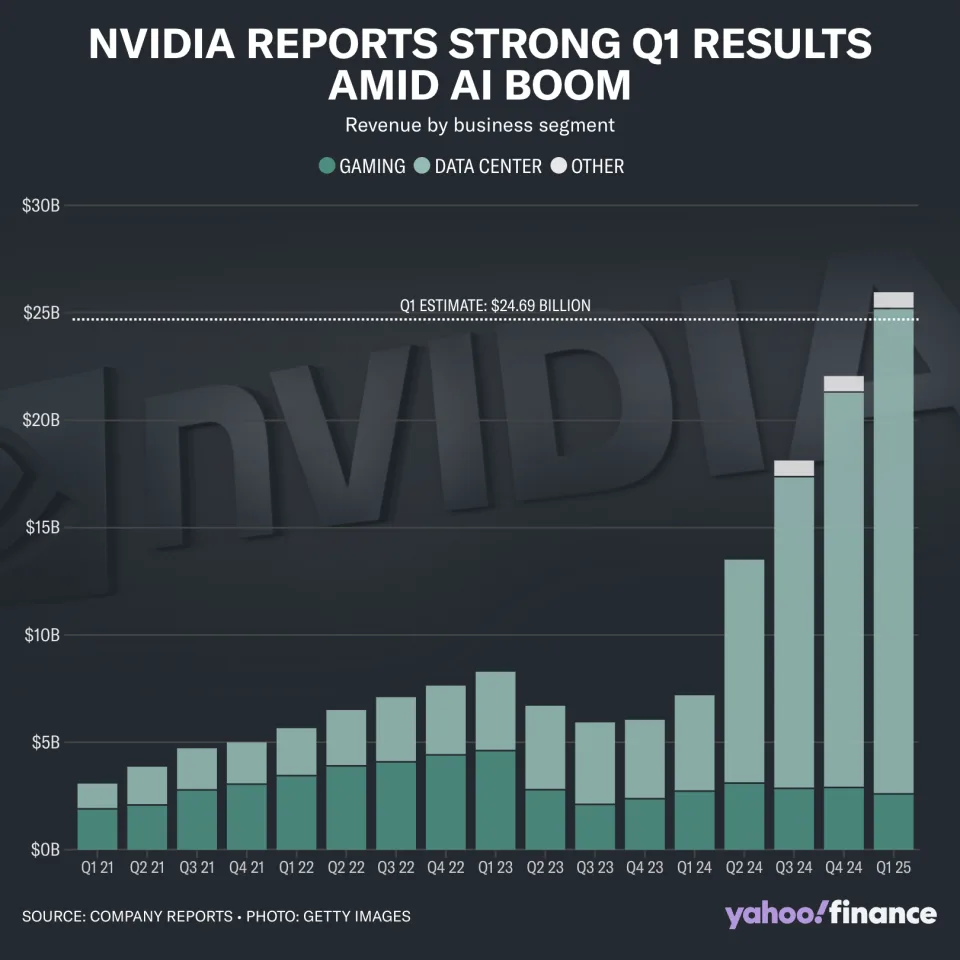

For the first quarter, Nvidia reported stellar results. Adjusted earnings per share reached $6.12 on revenue of $26 billion, representing year-over-year increases of 461% and 262%, respectively. Non-GAAP operating income was $18.1 billion for the quarter.

Nvidia expects its revenue for the current quarter to be around $28 billion, plus or minus 2%, surpassing analysts’ expectations of $26.6 billion.

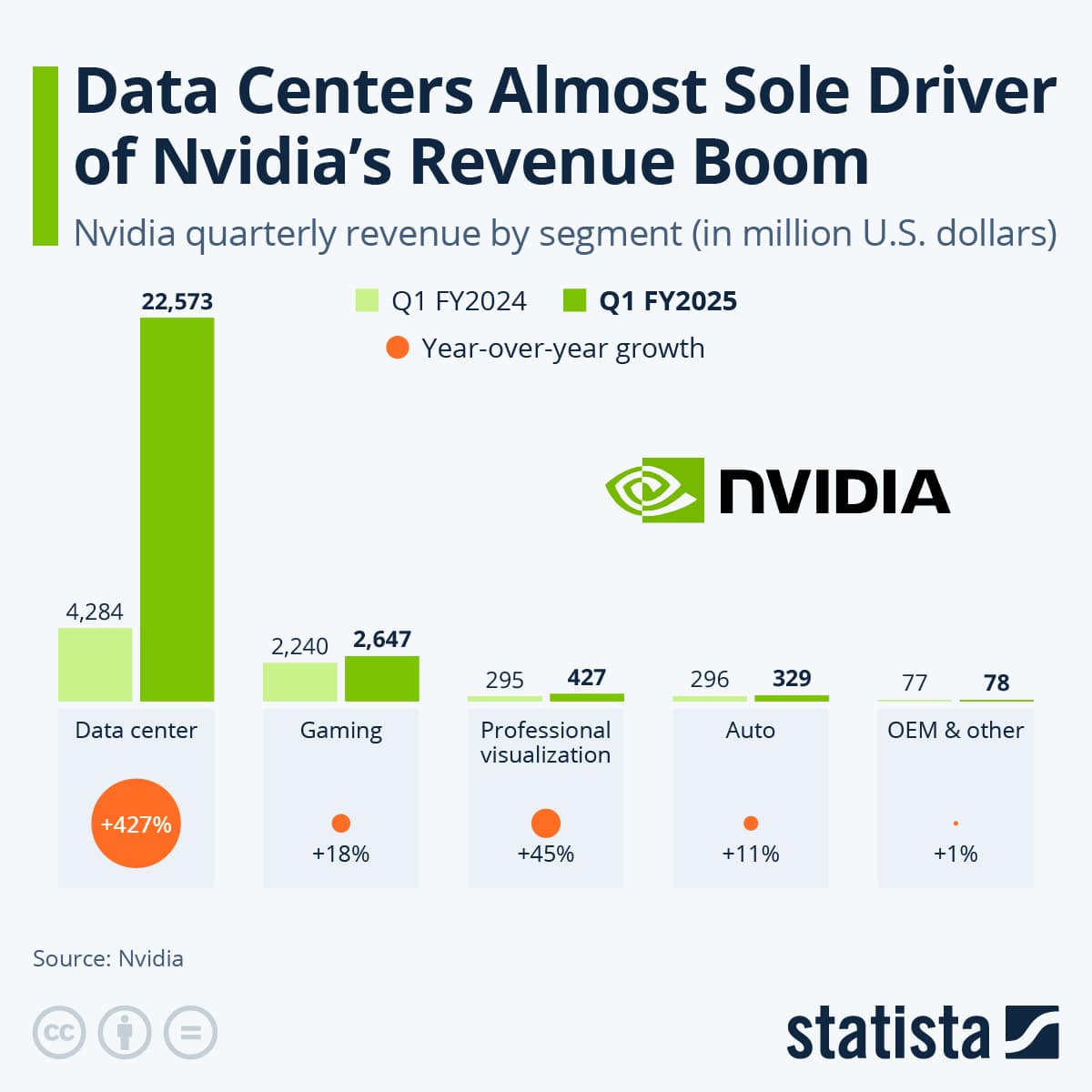

Nvidia’s data center segment, crucial for AI and reliant on high-powered server farms, generated $22.6 billion or 87% of its revenue between February and April 2024. Other segments also saw growth, with gaming and visualization solutions increasing by 18% and 45%, respectively, compared to fiscal Q1 2024. However, the data center segment’s growth was extraordinary, surging 427% year-over-year, as seen below.

In addition, Nvidia announced a 10-to-1 stock split, effective June 10 for shareholders as of June 7, and increased its quarterly dividend to $0.10 per share, up from $0.04. Following the earnings report, Nvidia’s stock rose by as much as 6% in extended trading.

Moreover, Huang highlighted the growing customer base for Nvidia chips beyond the major cloud service providers, mentioning companies like Meta, Tesla, and various pharmaceutical firms. He specifically pointed out the automotive industry as a significant user of Nvidia’s data-center chips.

Setting New Standards in Energy Efficiency

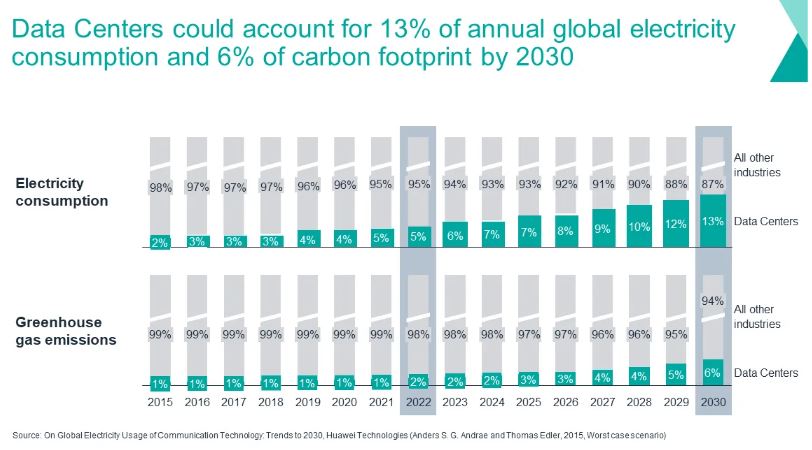

Nearly 75% of global carbon emissions stem from the production and consumption of energy, primarily due to the burning of fossil fuels for electricity. Data centers, which currently consume 460 terawatt-hours of electricity annually, contribute about 2% to this total. However, this share is expected to nearly triple to 6% by 2030 as data centers continue to expand.

Improving energy efficiency in data centers is crucial for reducing their carbon footprint and mitigating their environmental impact. By adopting more efficient technologies and practices, data centers can play a significant role in lowering overall carbon emissions.

Nvidia aims to address growing concerns about AI’s monetary cost and carbon footprint by highlighting Blackwell’s energy efficiency.

One expert at Microsoft has suggested that the Nvidia H100s currently in deployment will consume as much power as the entire city of Phoenix by the end of this year. What’s noteworthy about the new Blackwell GPU is its power efficiency, which Nvidia is now highlighting as a key selling point.

Traditionally, more powerful chips have also required more energy, and Nvidia focused primarily on raw performance rather than energy efficiency. However, when unveiling the Blackwell, CEO Jensen Huang emphasized its superior processing speed, which significantly reduces power consumption during training compared to the H100 and earlier A100 chips.

Huang noted that training ultra-large AI models with 2,000 Blackwell GPUs would consume 4 megawatts of power over 90 days, whereas using 8,000 older GPUs for the same task would consume 15 megawatts. This reduction translates to the power consumption of 8,000 homes compared to 30,000 homes.

Undeniably, Nvidia stands at the forefront of the exploding demand for AI applications, driven by major tech giants like Tesla, Meta, Microsoft, and Alphabet. These companies’ recent management commentary underscores the significant potential for Nvidia’s business expansion in the AI sector.

Tesla’s ambitious plans to increase its Nvidia chip use by 140% highlight the critical role of Nvidia’s GPUs in training AI models for its full self-driving capabilities and upcoming robotaxi launch. This substantial investment represents a major endorsement of Nvidia’s technology by Tesla CEO Elon Musk.

Similarly, Meta’s aggressive spending to bolster its AI infrastructure aligns with CEO Mark Zuckerberg’s vision of establishing Meta as a leading AI company globally. As Meta continues to develop its large language model (LLaMA) and Meta AI chatbot, Nvidia’s chips remain integral to its AI training efforts.

Microsoft is also experiencing surging demand for AI, outstripping its available capacity. The tech giant is investing in its own AI development using OpenAI’s GPT model. However, it plans to ramp up spending to meet the growing demand, with Nvidia’s chips playing a crucial role in its cloud service offerings.

Finally, Alphabet’s substantial capital expenditures in the first quarter, primarily directed towards Google Cloud and advanced AI models, further validate the importance of Nvidia’s technology in powering AI-driven initiatives. While Alphabet uses its chip designs for certain AI tasks, it continues to rely on Nvidia chips to meet its cloud customers’ needs.

While most AI runs on renewable energy, concerns persist about water consumption for data center cooling. As AI adoption grows, renewable energy demand could outpace supply, prompting interest in expediting nuclear plant approvals, notably by Microsoft.

Overall, the overwhelming demand for AI compute presents a significant opportunity for Nvidia, reflected in its robust financial performance and soaring gross margins. And with the company’s discussion of the Blackwell GPU’s energy efficiency, it signals that the company is starting to consider AI’s sustainability.

Lithium, a crucial element in energy storage, holds immense significance in powering various industries. With metal prices soaring, the demand for lithium has surged over recent years.

This article delves into the intricate world of lithium dynamics, exploring the factors influencing lithium prices, recent trends, and future projections.

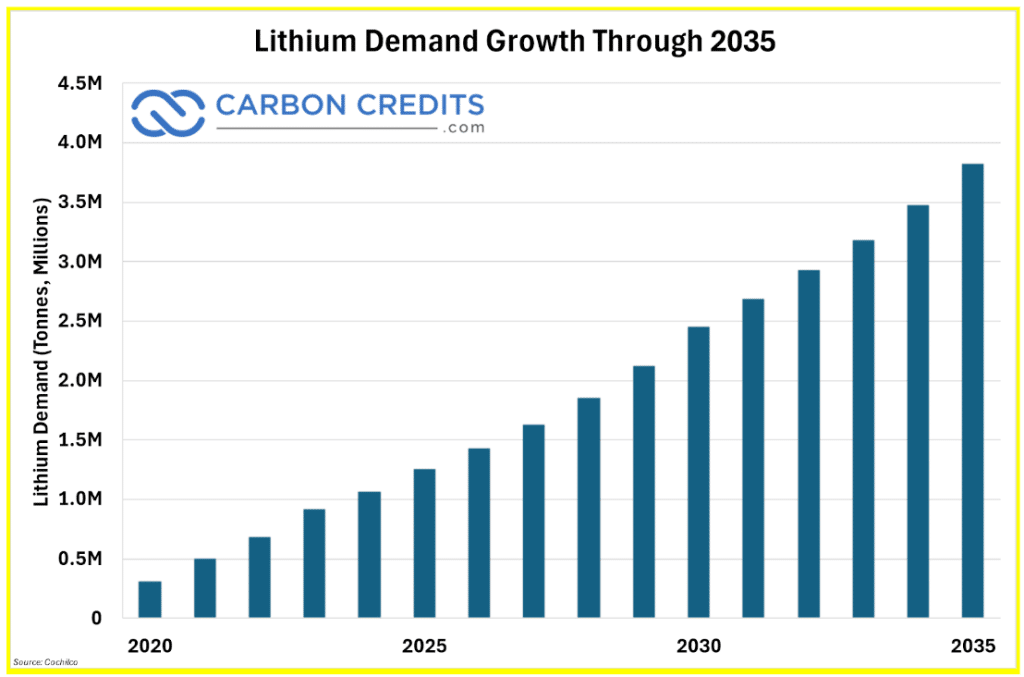

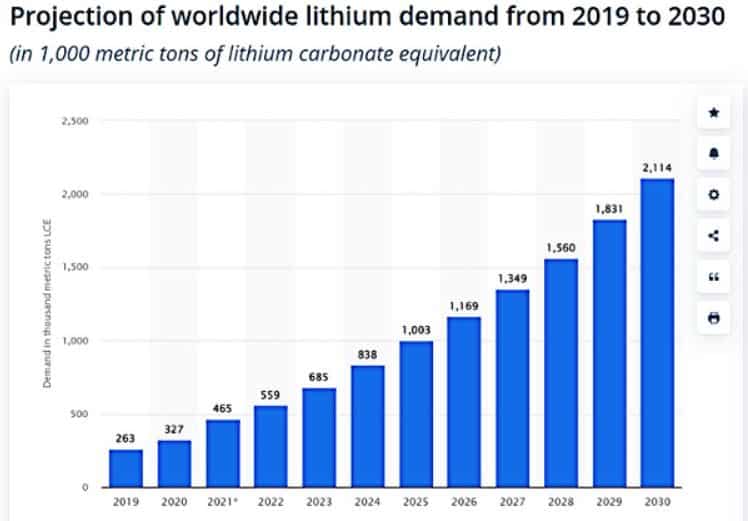

Global production of lithium has seen a remarkable increase. In 2020, the total demand for lithium worldwide was 292 thousand metric tons of lithium carbonate equivalent.

Forecasts indicate a substantial rise to over 2.1 million metric tons by 2030, highlighting the industry’s exponential growth. This surge is primarily due to the rising battery demand for electric vehicles, which is expected to reach 3.8 million tons by 2035.

Source: The World Economic Forum

Data from the US Geological Survey shows that global lithium production reached 180,000 metric tons in 2021, with about 90% coming from just three countries.

Market Demand

Despite robust demand for lithium, growth experienced a decline year-on-year in 2023 due to economic slowdowns, particularly affecting the electric vehicle market in China. Additionally, accelerated capacity expansions led to an oversupply situation. These fluctuations underscore the delicate balance between supply and demand that significantly impacts lithium prices globally.

Economic Factors

Economic factors such as inflation rates and currency fluctuations also influence lithium prices considerably. These macroeconomic indicators directly impact production costs and subsequently affect pricing strategies within the lithium market.

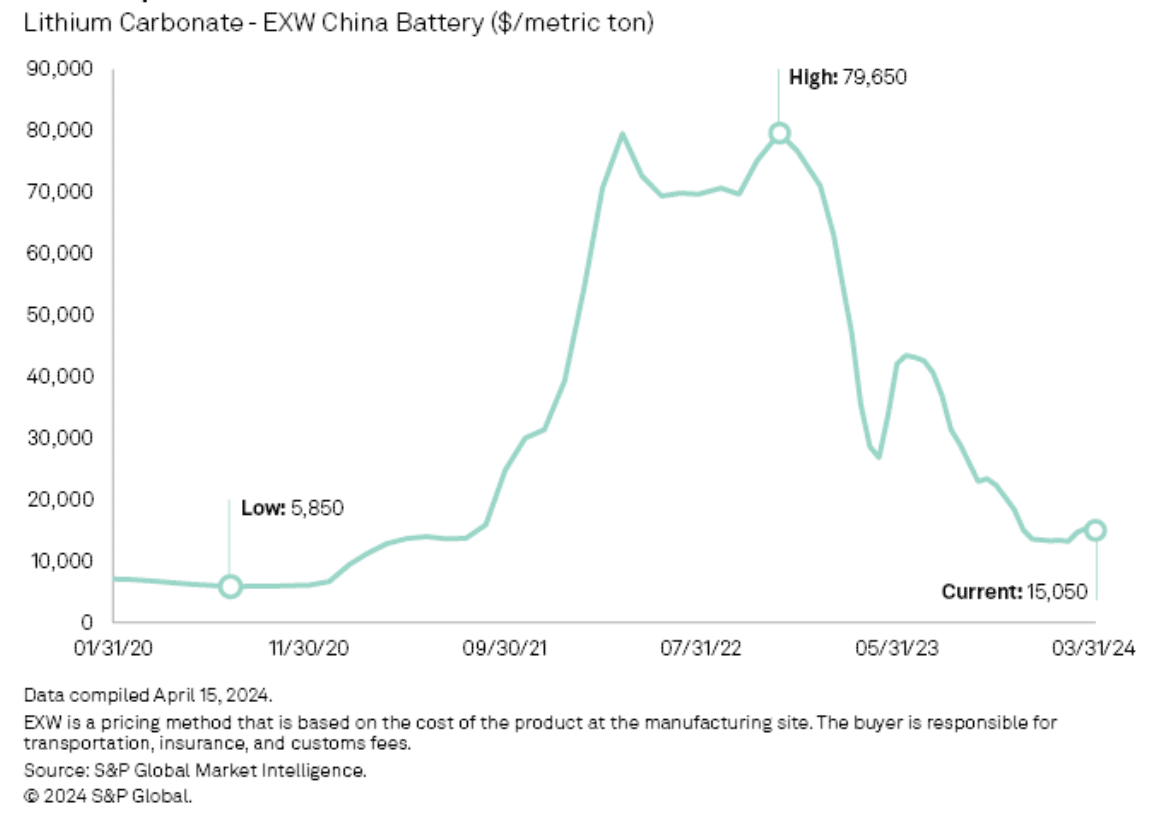

Lithium prices have recently experienced a notable downward trajectory. As of December 18, prices plummeted by 80% within a year, and as of May 7, CIF North Asia price at $14,600/t. This decline has sparked discussions about the sustainability of this trend.

Expert insights suggest that low prices may lead to reduced supply and hesitant new investments amidst strong demand and cautious predictions.

Effect on the EV Sector

The lithium price drop has a significant impact on the EV sector. Reduced input costs present opportunities for manufacturers to recalibrate pricing strategies, potentially driving down EV costs and increasing consumer adoption rates. This shift highlights the interconnected nature of commodity pricing and its far-reaching consequences on diverse industries.

What’s the Future of Lithium Prices?

As the lithium market navigates significant fluctuations, industry experts provide valuable insights into future price trajectories. By examining expert predictions and analyzing market opportunities and challenges, stakeholders can comprehensively understand the dynamic landscape ahead.

In a recent interview, industry analyst Joe Lowry predicts that the lithium chemical supply is nearing equilibrium, with prices expected to rise by mid-2024 as inventories rebuild in key markets like China. Similarly, Andy Leyland emphasizes that the lithium market’s balance is delicate and that a projected surplus of 24,000 tonnes LCE in 2024 could quickly change due to market dynamics.

Staying informed about lithium carbonate and hydroxide prices is crucial for industry participants to capitalize on opportunities and navigate challenges. Monitoring real-time lithium prices and commodity trends provides invaluable insights for strategic positioning amidst market uncertainty.

On May 17th, Japan’s House of Councillors passed a new law to bolster the business environment for carbon capture and storage (CCS) technology which is crucial for achieving a decarbonized society. The legislation received majority support in the plenary session.

Key Provisions of Japan’s New CCS Law

The law mandates that the government introduce a permit system for businesses to facilitate CO2 capture from industries operating at variable scales and their underground storage. This measure is part of Japan’s broader strategy to achieve net-zero carbon emissions by 2050.

Role of Japan’s Ministry of Economy, Trade, and Industry (METI)

To foster a conducive business environment for CCS projects, theMinistry of Economy, Trade, and Industry (METI) of Japan will establish a licensing system. It will cover storage and exploration drilling rights, and develop business and safety regulations for storage companies and CO2 pipeline transportation businesses. Test drilling permits at potential CCS sites will initially be valid for four years. METI will designate suitable geological storage areas as “specified areas” and solicit operators, granting licensed operators prospecting and storage rights.

Notably, this is the first time the CCS bill defines operators’ rights and regulatory requirements. The main highlights of the newly introduced bill are:

CCS Sites and Business permits

Designate Suitable Areas: Identify specific regions where carbon dioxide (CO2) can be safely stored underground.

Grant CCS Business Permits: Select businesses through a public offering process and grant them permits to operate CCS projects.

Licensed operators will be given

Exploratory Drilling Rights: These rights allow businesses to drill and confirm if geological formations are suitable for CO2 storage.

Storage Rights: These rights permit the actual storage of captured CO2 underground.

Obligations and Liabilities

The law imposes several obligations on businesses:

Monitoring: Businesses must continuously monitor for any CO2 leaks.

Liability for Accidents: Businesses are liable for compensation regardless the leak was due to negligence or an intentional act.

CCS project operators must have their implementation plans approved by the Minister for Economy, Trade, and Industry. Once the stored CO2 is stabilized, theJapan Organization for Metals and Energy Security (JOGMEC) will take over the management. Operators will be liable for compensation during accidents, regardless of intent or negligence.

Subsidy System for Hydrogen

In addition to the CCS law, the House of Councillors also passed a law to establish a subsidy system. This system aims to narrow the price gap between hydrogen and natural gas, promoting hydrogen as a viable next-generation energy source.

This comprehensive approach strengthens Japan’s efforts to reduce carbon emissions through CCS and supports the broader adoption of hydrogen energy, aligning with the country’s long-term environmental goals.

Japan Advances Carbon Capture under Green Transformation (GX) Policy

Japan’s newly approved law is crucial to achieving a decarbonized economy. It’s an extension of the Green Transformation (GX) Policy that existed since last year.

Unveiled in February 2023 and approved in July 2023, Japan’s GX policy integrates fiscal and policy measures, potentially amounting to a $1 trillion (150 trillion yen) budget. This policy provides a roadmap for the next decade, balancing economic growth with environmental sustainability.

Japan’s Prime Minister Fumio Kishida said,

“First of all, green transformation, or GX in short, does not just mean the departure from fossil energy. It involves the implementation of major reforms of energy, all industries, and our economy and society, toward achieving the goal of carbon neutrality by 2050. To this end, Japan has made a highly challenging international pledge of a 46 percent reduction in greenhouse gas emissions by fiscal 2030.”

Image: The Tomakomai CCS Demonstration Project- Japan’s first full-chain CCS project, captured and stored CO2 from a coastal oil refinery on Hokkaido Island in Japan from 2016 to 2019.

source: IEA

Based on International Energy Agency (IEA) calculations,

Japan’s estimated annual storage capacity for CCS could range from 120 to 240 MTs by 2050. The goal is to have the first commercial CCS project operational by 2030.

By advancing these legislative measures, Japan aims to create a robust framework for CCS and low-carbon hydrogen, supporting its long-term decarbonization and economic growth objectives.

By enacting these laws, Japan is taking significant steps toward a sustainable and decarbonized future, leveraging both CCS technology and hydrogen energy to mitigate climate change.

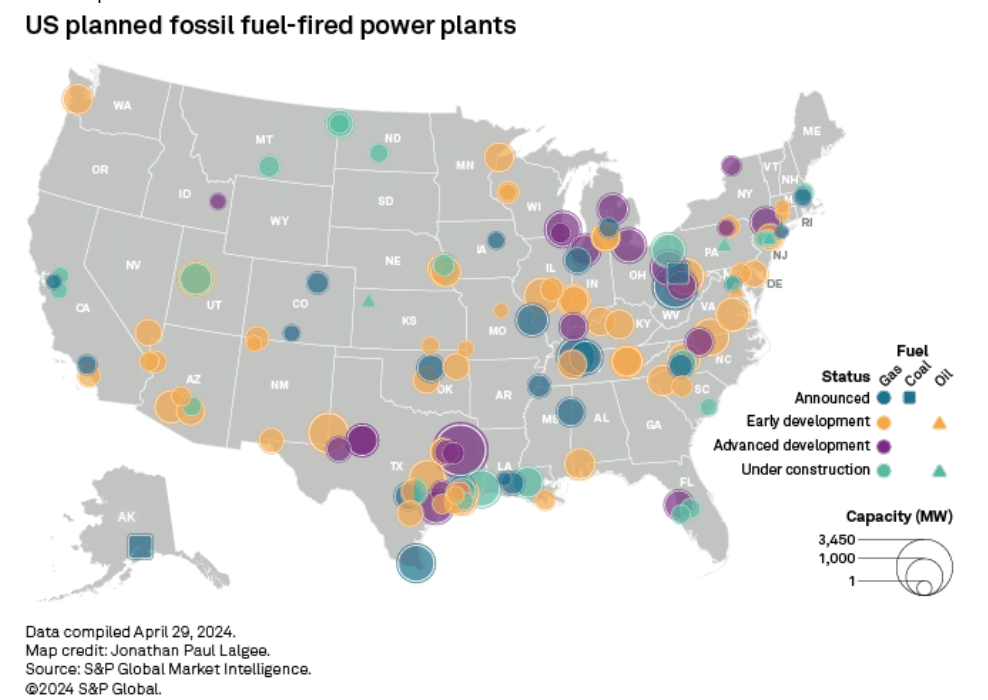

Nearly halfway through a decade critical for mitigating climate change, US utilities and investors plan to add 133 new natural gas-fired power plants to the nation’s grid, as reported by S&P Global Market Intelligence. Additionally, 4 oil-fired plants and two coal-fired plants are either under construction or in early development.

These plans for new fossil fuel-based power generation emerge amidst growing concerns over increasing power demand driven by electrification and industrial growth.

Surging Power Demand in the U.S.

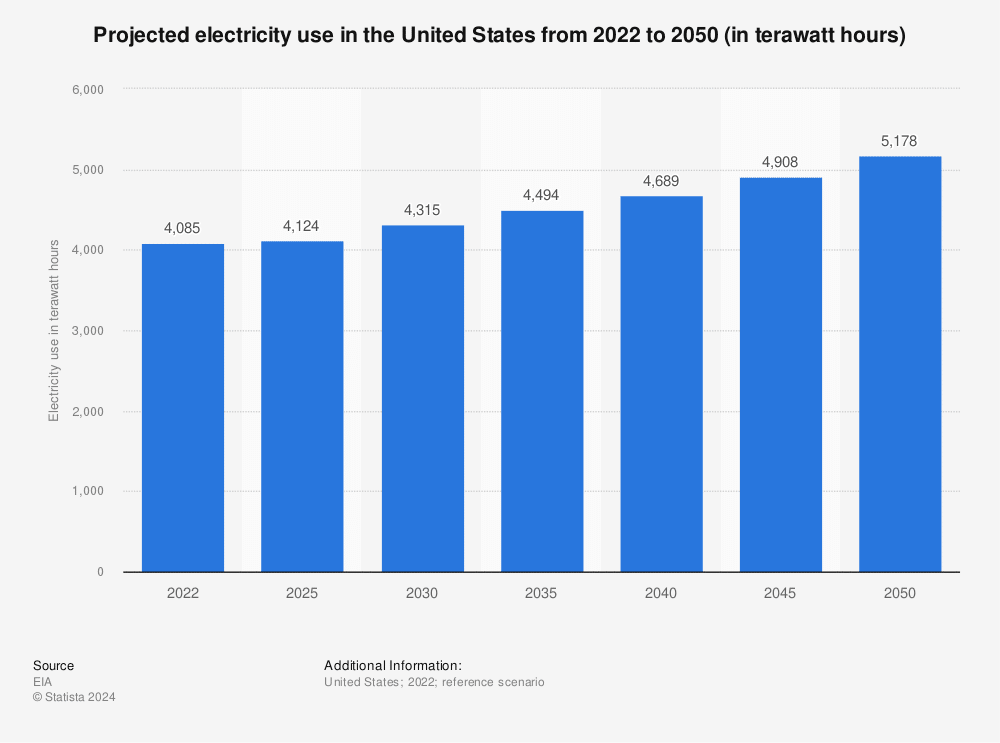

Electricity use in the United States was around 4,085 terawatt hours in 2022, per Statista data. Projections indicate that U.S. electricity consumption will rise to 5,178 terawatt hours by 2050. That’s an increase of about 27% from 2022 levels.

In December 2023, grid regulators warned of potential power demand surpassing supply in the coming decade. Notably, consulting firm Grid Strategies noted that the “era of flat power demand is over.”

According to some experts, long-term investments in natural gas infrastructure pose a threat to the nation’s commitment to halving economy-wide greenhouse gas emissions by 2030, which could result in stranded assets.

For instance, Lauren Shwisberg, a principal in the carbon-free electricity practice at RMI, emphasized the need for a significant reduction in gas generation and emissions in the power sector by 2035. However, current utility plans suggest otherwise.

RMI’s latest forecast, based on data from 121 utility resource plans, projects an 18% increase in US natural gas-fueled power generation between 2024 and 2035.

This trend raises concerns about aligning energy development with climate goals, highlighting the challenges of transitioning to a cleaner grid.

Balancing Climate Goals with Gas Infrastructure

Limiting global warming to 1.5°C above preindustrial levels calls for states to cut emissions across sectors by nearly 50% by 2030. However, US CO2 emissions from gas plants were 39% higher in 2023 than in 2017, as per the US Energy Information Administration. Notably, 2023 saw CO2 emissions from gas plants surpass those from coal for the first time.

More remarkably, the surge in energy use by data centers, driven by the rise of AI, has placed the energy industry in a challenging position.

Estimates show that power demand from data centers will explode. The International Energy Agency forecasts that energy use in data centers will rise to around 1,050 TWh in 2026, from 200 terawatt-hours (TWh) in 2022. Putting this in context, this is equivalent to the energy demand of Germany.

Ernest Moniz, head of the nonprofit energy research group EFI Foundation, addressed this power concern during a recent interview.

“There’s some battery storage, there’s some renewables, but the inability to [quickly] build electricity transmission infrastructure is a huge impediment. So we need the gas capacity.”

Monitz emphasized that natural gas still has a role in a decarbonized world. Despite this, US utilities continue to advance new natural gas projects. And while ratepayer advocates, environmental groups and climate-conscious corporate customers closely scrutinize their plans.

Regional Developments and Controversies

Wisconsin Electric Power Co., part of WEC Energy Group, seeks state approval for $2.1 billion in rate increases to fund 2 new natural gas-fired plants, an LNG storage facility, and 33 miles of pipelines. This infrastructure will replace 4 coal units shutting down by 2025.

In Arizona, the Salt River Project (SRP) plans to add 2 GW of gas-fired generation by 2035 to integrate 9.5 GW of renewables and storage and replace over 1.3 GW of retiring coal capacity. SRP cites a 40% rise in demand over the next decade.

Critics, including the Sierra Club, argue this plan will exacerbate water issues, raise costs, and worsen the climate crisis. SRP’s analysis showed no-gas options would not be reliable or affordable.

In Texas and the Southeast, utilities are pushing for more natural gas generation. Duke Energy’s updated plans for the Carolinas include 10 new gas-fired units, adding nearly 9 GW by 2033. These “hydrogen-capable” plants aim to help Duke reach carbon neutrality by 2050, despite public concerns over rising renewables costs.

Georgia Power Co.’s proposal for over 1.4 GW of new gas and oil-fired power by 2027 was approved, despite Microsoft’s claims of over-forecasting demand. The Southern Environmental Law Center estimates these investments will cost customers about $3 billion.

Critics argue that regulators in states without emissions reduction laws focus solely on costs, ignoring climate benefits. For a watchdog utility group’s leader, David Pomerantz, utilities’ attempts to balance decarbonization goals with building new gas plants are contradictory.

As the US faces growing power demands and strives to meet climate goals, new fossil fuel plants raise significant concerns. The projected increase in natural gas infrastructure may conflict with the nation’s emissions reduction commitments, highlighting the challenges of balancing energy needs with environmental responsibilities.

With almost every nation endorsing the Paris Agreement, the goal is to limit global warming to below 2°C by reducing greenhouse gas (GHG) emissions. However, a significant amount of carbon dioxide has already been accumulated in the atmosphere since the Industrial Revolution. Merely halting emissions would not be enough to reverse climate change.

Climate scientists suggest to remove 10 gigatons of CO2 annually by 2050 and 20 gigatons thereafter to meet the climate target.

In response, professionals and researchers worldwide are actively exploring carbon removal technologies to mitigate the impact of accelerating climate change. Research institutions, in particular, are focusing on curbing their GHG emissions and developing technologies for carbon capture and storage (CCS).

Negative emissions solutions like CCS or carbon capture utilization and storage (CCUS) are gaining importance. Top universities worldwide are actively contributing to this effort, each with specialized research groups focusing on various aspects of carbon capture and utilization. These ranges from capturing CO2 from smokestacks to developing innovative products that use atmospheric CO2 in beneficial ways.

Other top universities are implementing ways on how to directly curb their own carbon emissions and footprint to reach Net Zero goals. Here are the top six universities in the United States and what they’re doing to help in this fight.

Harvard University and Its Zero Goal

Faculty and students from across the Harvard community are working on ways to address climate change and its effects. The university has implemented various sustainability and climate initiatives. Here are some of them:

Salata Institute for Climate and Sustainability: Established in fall 2022 with a generous $200 million gift from Melanie and Jean Salata, the institute serves as a hub for interdisciplinary collaboration, research, and engagement aimed at addressing the climate crisis.

Sustainability Management Council (SMC): Senior leaders in operations, facilities, and administration convene regularly to facilitate the sharing of best practices and achieve the University’s sustainability and energy management objectives.

Council of Student Sustainability Leaders (CSSL): Comprising graduate and undergraduate students involved in sustainability-related groups, the CSSL fosters collaboration, networking, and feedback on Harvard’s sustainability initiatives.

Climate Solutions Living Lab: This initiative combines pedagogy and applied research to advance climate goals through interdisciplinary student projects focused on solutions for the building and energy sectors.

Harvard Green Office Program: This program guides staff in creating sustainable workspaces, promoting environmental stewardship across the University.

Resource Efficiency Program (REPs): Founded in 2002, REPs promotes sustainability within undergraduate housing through peer-driven educational initiatives.

Harvard’s Sustainability Action Plan underscored the university’s unwavering commitment to environmental stewardship and its relentless pursuit of sustainability initiatives both on campus and in broader contexts.

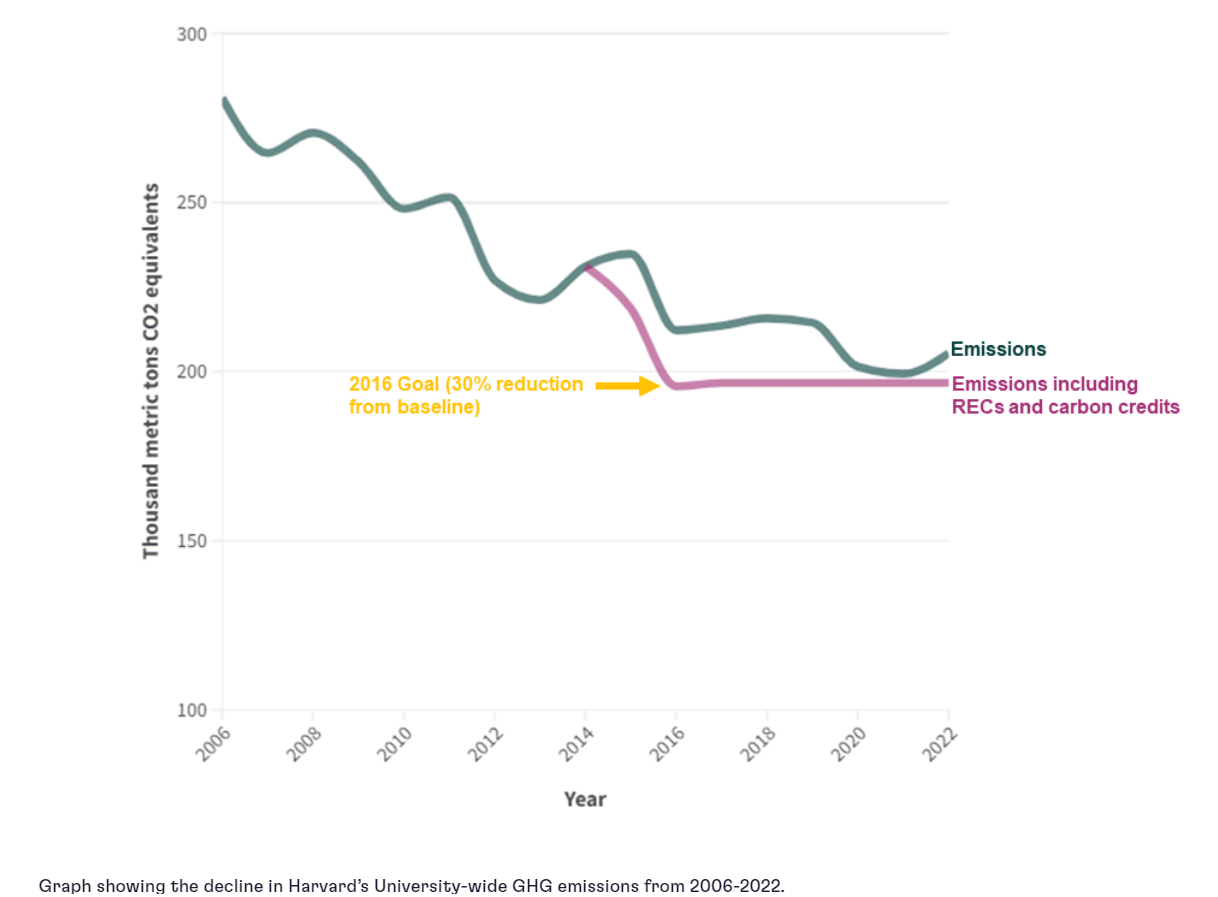

Central to Harvard’s agenda is the acceleration of clean energy adoption and the complete transition away from fossil fuels. Through these efforts, Harvard aims to establish a blueprint for a decarbonized world as shown by its decreasing carbon footprint.

Harvard University Carbon Emissions, 2006-2022

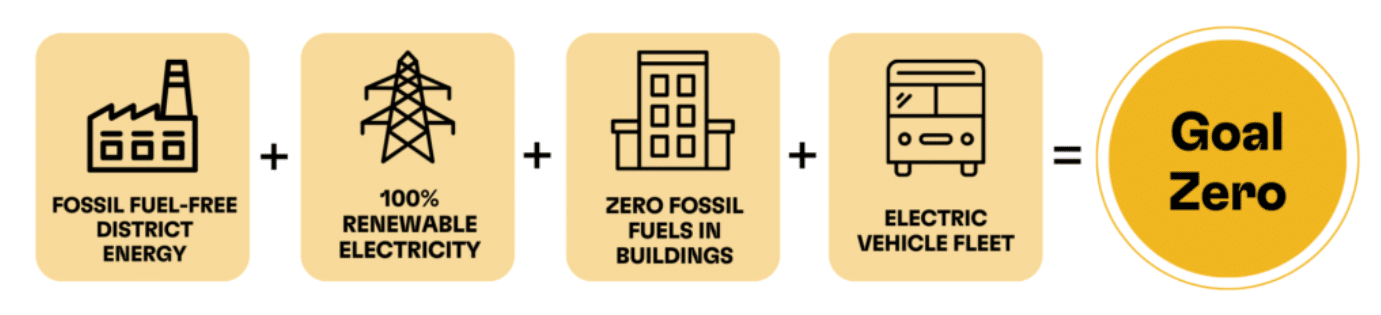

Goal Zero: A Fossil Fuel-Free Harvard

Harvard has set a bold objective to achieve fossil fuel-free status by 2050, surpassing the benchmark of merely attaining “carbon neutrality.”

While carbon neutrality typically involves offsetting emissions through initiatives like renewable energy procurement and tree planting, Goal Zero, as embraced by Harvard, aims for the complete elimination of fossil fuel usage. This approach acknowledges the comprehensive spectrum of harms stemming from fossil fuel consumption, going beyond carbon emissions alone.

Recognizing the manifold negative impacts of fossil fuels, which extend to their role as key components in plastics and toxic chemicals, Harvard also endeavors to curb these dependencies. This multifaceted approach aligns with the university’s broader mission to mitigate waste and foster a healthier, more sustainable value chain.

As an interim measure to progress towards Goal Zero, Harvard has established a short-term target to achieve fossil fuel neutrality by 2026. This entails eliminating campus emissions (both Scope 1 and Scope 2) and investing in initiatives that not only neutralize GHG emissions but also mitigate the adverse health effects of fossil fuel usage, such as air pollution.

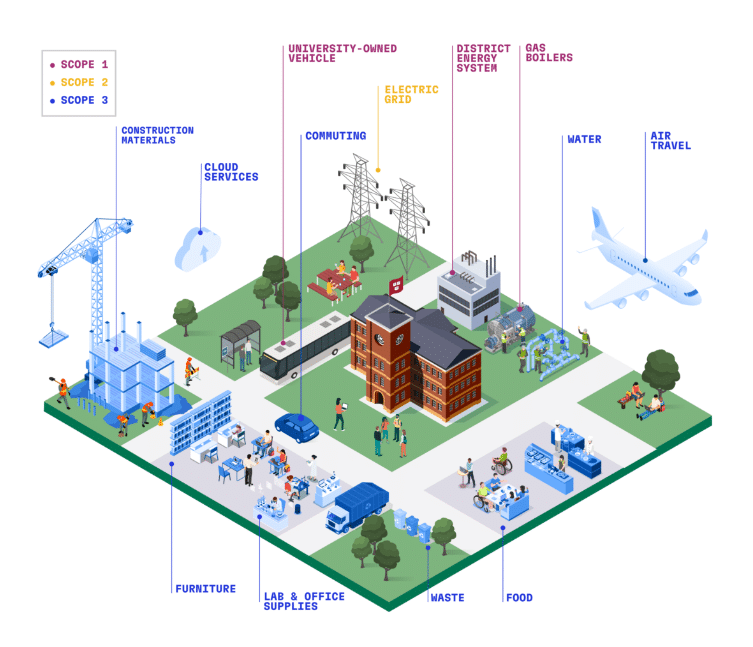

The university is intensifying efforts to reduce Scope 3 emissions, focusing on emissions generated throughout its value chain. This includes various areas such as construction, food production, air travel, commuting, and procurement of goods and services.

Its value chain (Scope 3) emissions goals and priorities are as follows:

25% reduction in food-related emissions by 2030

20% lower embodied carbon in new construction

In 2023, the Harvard Kennedy School took a significant step toward mitigating its environmental impact by purchasing its inaugural portfolio of high-quality carbon offsets. These offsets were to compensate for the climate and health-related damages stemming from Harvard Kennedy School (HKS) travel activities throughout the year, as well as to offset the institution’s broader global emissions footprint.

Harvard carbon footprint ecosystem

By prioritizing human health, social equity, and slashing carbon footprint, Harvard aims to generate positive impacts through its transition to fossil fuel neutrality.

MIT’s Plan for Action on Climate Change

Since the announcement of Massachusetts Institute of Technology’s Plan for Action on Climate Change in October 2015, MIT Energy Initiative (MITEI) has made significant strides in research, education, outreach, and engagement efforts aimed at combating climate change and advancing clean energy solutions.

MITEI established its Carbon Capture, Utilization, and Storage (CCUS) Center in 2006 as part of its commitment to addressing climate change through innovative energy solutions. The center brings together faculty members focused on research in 3 key areas: capture, utilization, and geologic storage of CO2.

Within the CCUS Center, researchers explore a range of technologies and methods, including molecular simulation, materials design, catalytic processes, fluid mechanics, and advanced imaging techniques. They are developing emerging technologies for gas storage and separation.

Geologic storage research investigates the behavior of CO2 in underground reservoirs, including its interactions with pore fluids, and employs advanced imaging techniques to better understand the opportunities and risks associated with storing carbon dioxide underground.

Through these efforts, MIT is contributing to the development of innovative solutions for carbon capture and storage, essential for mitigating climate change. Here are the other key achievements of the university in various aspects of its efforts in cutting carbon emissions:

Research:

MITEI’s research portfolio focuses on deep decarbonization across four major energy sectors—power, transportation, industry, and buildings—to address climate change and expand access to clean energy.

The establishment of Low-Carbon Energy Centers has facilitated collaborative research efforts with industry partners to tackle pressing energy challenges. These centers help in advancing projects related to mobility systems, energy storage, carbon capture, and more.

Major studies and reports, such as “Insights into Future Mobility” and “The Future of Nuclear Energy in a Carbon-Constrained World,” have provided comprehensive analyses of key technologies and sectors, informing policy and business decisions.

Education and Outreach:

MITEI has been actively involved in educating students and the public about climate change and clean energy solutions through various initiatives, including workshops, seminars, and educational programs.

The Mobility Systems Center, established as part of MITEI’s research efforts, has contributed to the understanding of individual travel decisions and the importance of sustainable mobility.

Engagement and Collaboration:

Collaboration with industry partners, including global engineering and energy companies like IHI, Iberdrola, Eni S.p.A., and ExxonMobil, has led to significant advancements in clean energy technologies and policies.

A new study [by Joel Jean, a former MIT postdoc, MITEI Energy Fellow, and CEO of startup company Swift Solar; Vladimir Bulović (Electrical Engineering and Computer Science; MIT.nano); and Michael Woodhouse (NREL)] shows that replacing new solar panels after just 10 or 15 years, using the existing mountings and control systems, can make economic sense, contrary to industry expectations that a 25-year lifetime is necessary. Credit: MIT

Membership agreements and collaborations with companies have resulted in substantial financial support for research projects, professorships, and technology development initiatives.

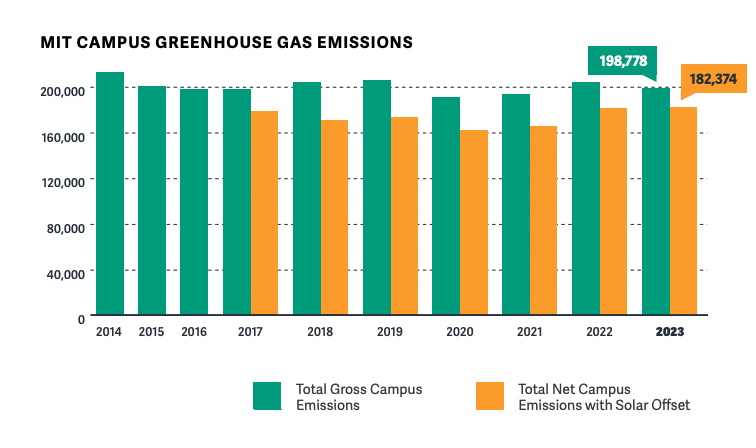

MIT is also joining the race to zero by aiming to eliminate direct emissions by 2050, with a near term milestone of net zero carbon campus emissions by 2026.

The university takes a multifaceted approach to achieve such climate goal. In general, the school will focus on:

Decarbonizing its on-campus energy systems,

Enabling large-scale clean energy generation on- and off-campus, and

Embracing new decarbonization solutions.

These efforts underscore MIT’s commitment to addressing climate change and accelerating the transition to a sustainable energy future.

Yale University’s Center for Natural CO2 Capture

Founded with a transformative donation from FedEx and as a part of Yale’s Planetary Solutions Project, the Yale Center for Natural Carbon Capture is dedicated to exploring the science of natural carbon capture. Its mission is to develop solutions that contribute to addressing some of the most pressing challenges of our time.

The Center introduces fresh and innovative research and researchers to the Yale community, forging connections with relevant research laboratories both on and off-campus. Through funding research projects, workshops, and fellowships, the Center supports initiatives at the University and invests in training the next generation of scientists and practitioners. These efforts revolve around three primary Focus Areas:

Over the past year, the Center has achieved several notable milestones. Among these, two standout initiatives have emerged: the Yale Applied Science Synthesis Program (YASSP) and significant advancements in enhanced rock weathering (ERW).

YASSP connects academic researchers, policymakers, and those managing lands to answer applied questions about how land management decisions affect the services provided by forests, croplands, wetlands, rangelands, and grasslands.

Yale’s Net Zero Goal

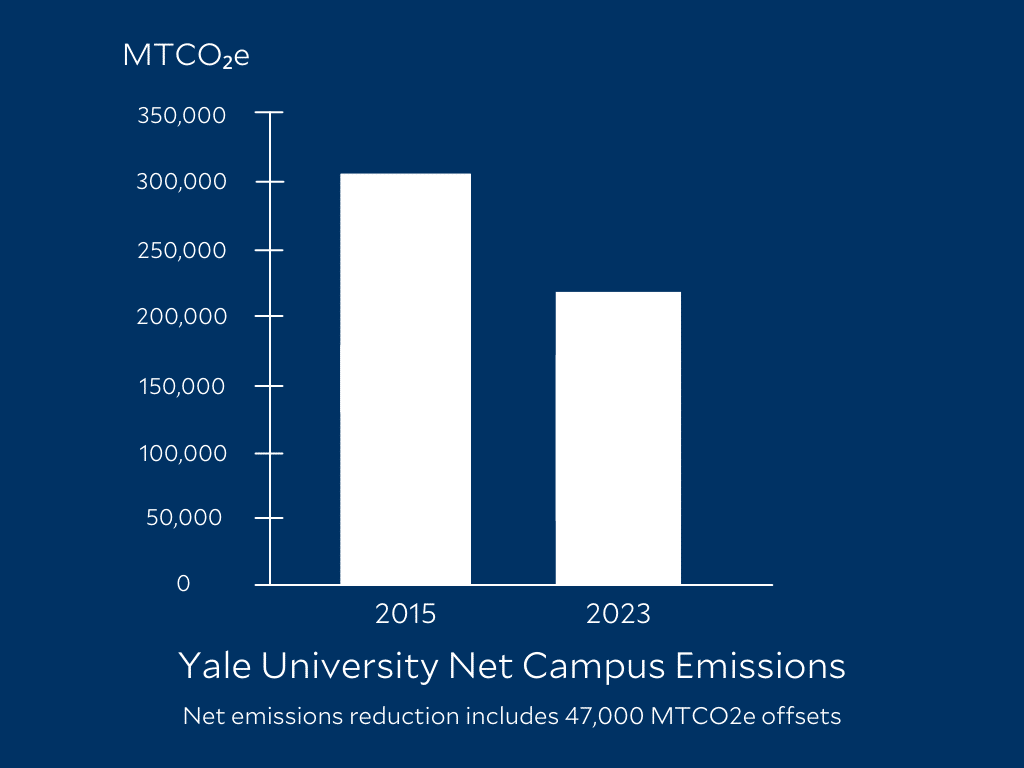

Yale University is dedicated to achieving zero actual carbon emissions by 2050, with an interim objective of reaching net zero emissions by 2035. This goal will primarily be accomplished by reducing campus emissions by 65% below 2015 levels and, if needed, utilizing high-quality, verifiable carbon offsets.

The ultimate aim of zero actual carbon emissions will involve minimizing campus emissions entirely and implementing clean energy technology. The university managed to cut emissions by 28% since 2015, as seen below, despite a huge increase in campus size.

The university’s approach to climate action is comprehensive and encompasses all aspects of its operations. Yale is expanding its educational offerings to address the complexity and magnitude of global climate challenges.

Additionally, investments are being made in campus infrastructure and emerging technologies to mitigate the university’s environmental impact. Yale has also adopted fossil fuel investment principles to facilitate a transition towards a decarbonized energy future.

Responsible energy use through conservation, efficiency upgrades, and innovative approaches to campus operations.

Ensuring that energy generation on campus is efficient and environmentally friendly.

Implementing a greenhouse gas emissions reduction strategy to steadily progress towards zero emissions targets.

Purchasing and retiring high-quality, verified carbon offsets when necessary to meet emissions goals.

Stanford University Center For Carbon Storage

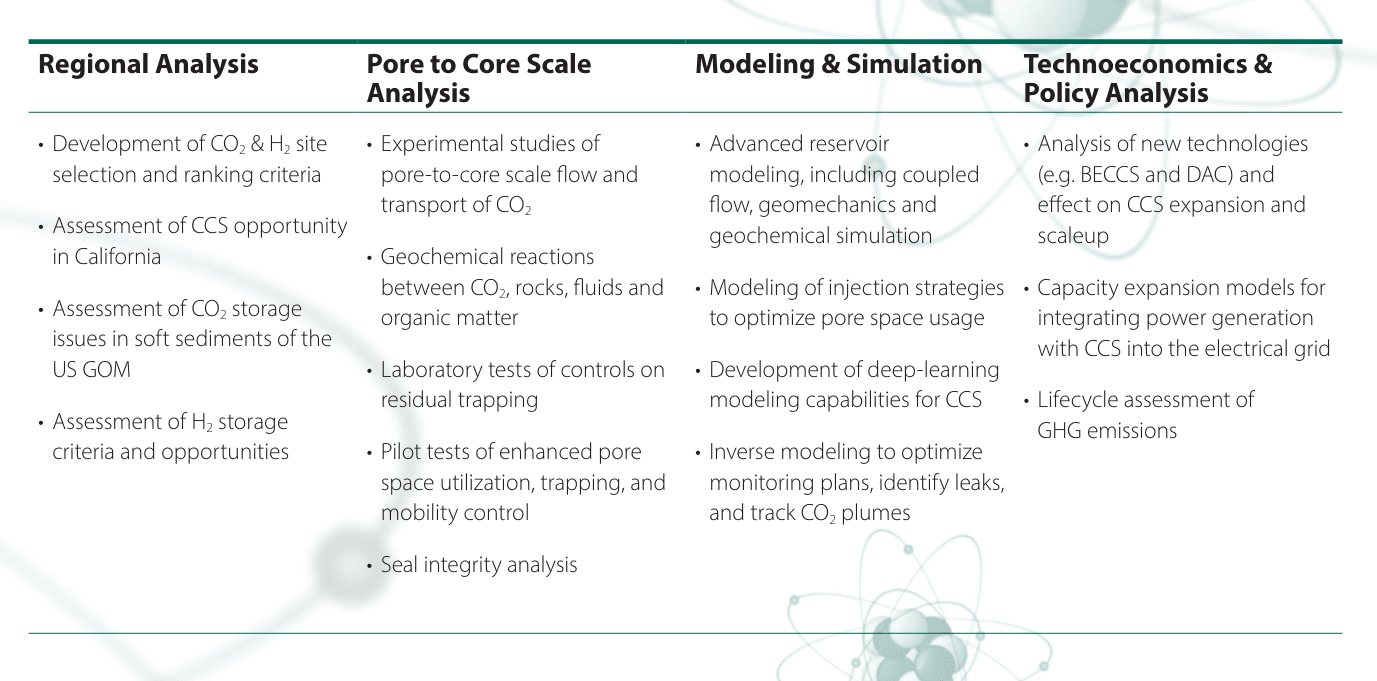

Stanford University leads global research on carbon sequestration, tackling critical questions on flow physics, monitoring, geochemistry, and more. They study CO2 storage in depleted oil and gas fields, saline reservoirs, and explore policies and techno-economics.

Stanford also focuses on capturing CO2 with engineered and natural applications, and combines bioenergy production with carbon capture to achieve net-negative emissions. Additionally, they research the impact of carbon taxes and cap-and-trade systems on CO2 capture and storage implementation.

The Stanford Center for Carbon Storage (SCCS)

The Stanford Center for Carbon Storage is focused on advancing crucial Carbon Capture and Storage (CCS) technologies aimed at capturing greenhouse gas emissions from smokestacks and securely storing them. Their research efforts are directed towards developing cost-effective methods for permanent storage on an industrial scale.

Visit this link to get to know more about the university’s CCS research highlights.

The center is actively addressing fundamental questions related to flow physics, monitoring techniques, geochemistry, and simulation of CO2 transport and behavior once stored underground. Their storage research encompasses a variety of geological formations, including fully-depleted oil fields, saline aquifers, and other unconventional reservoirs.

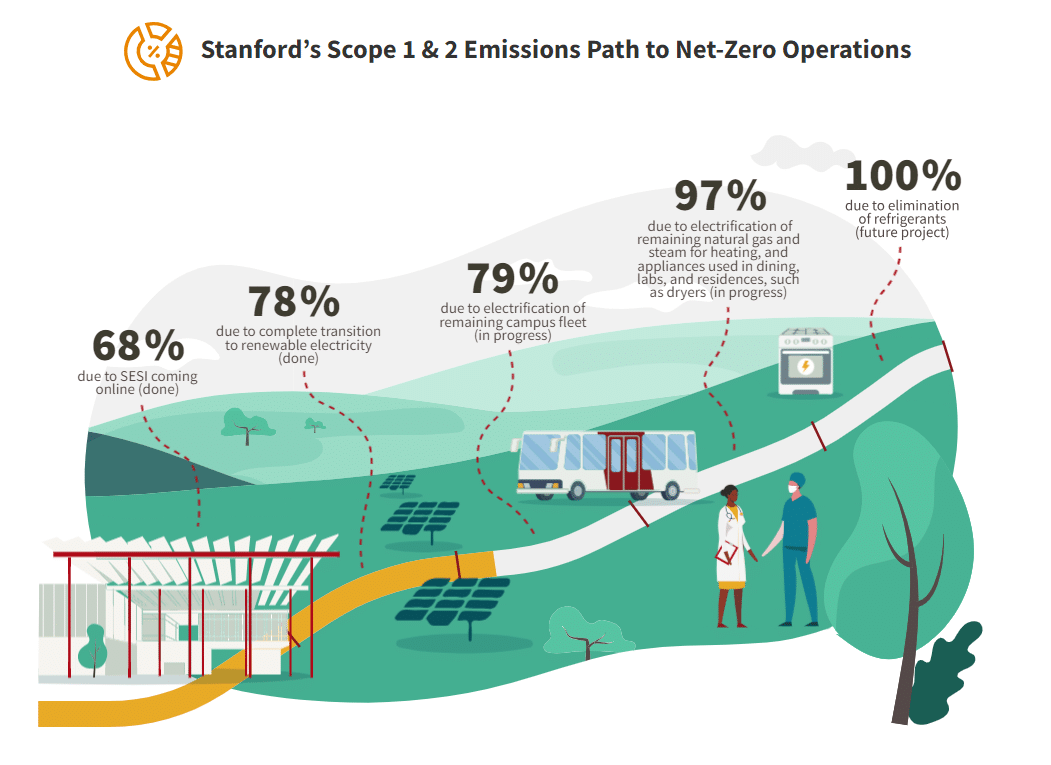

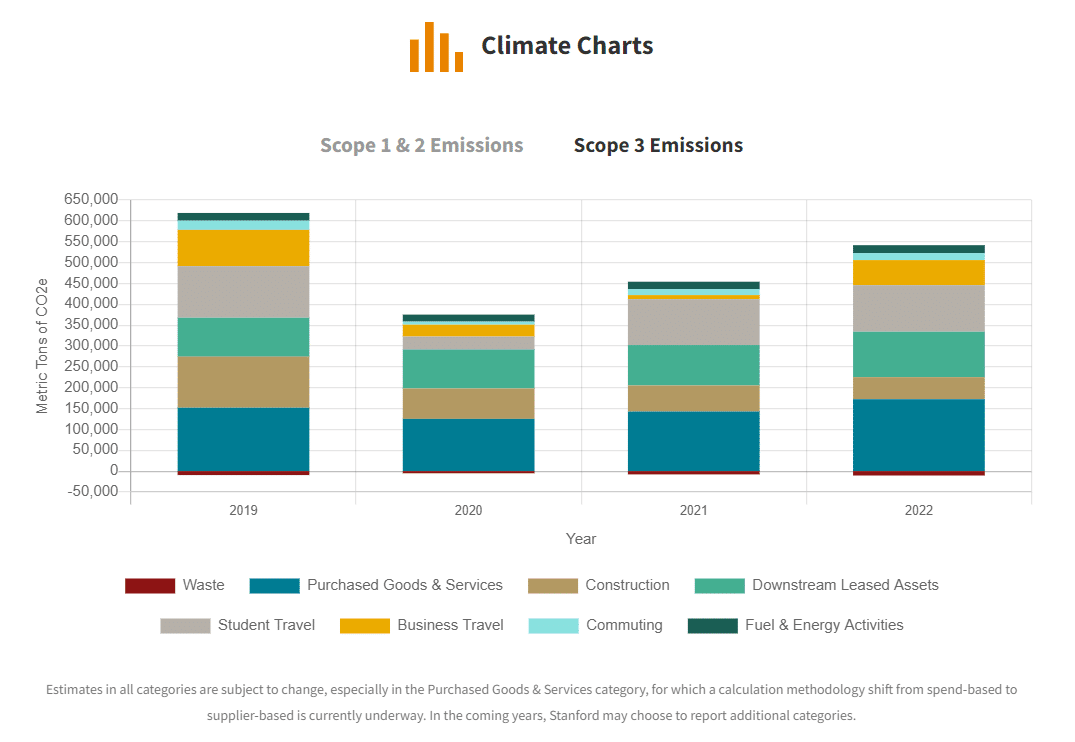

After completing the full year of 100% renewable electricity, Stanford University revealed new goals to get rid of construction and food-related emissions by 2030.

The university is currently monitoring Scope 3 emissions across eight categories, including business and student travel, fuel and energy activities, waste, employee commute, construction, purchased goods and services, leases, and food purchases.

There’s still much work to be done to decrease Stanford’s scope 3 emissions. But with the two emission reduction goals revealed last year, they represent significant progress in the university’s understanding of and ability to reduce these emissions.

These goals underscore climate action as a fundamental value for the departments involved and showcase close collaboration on sustainability initiatives across the university.

Arizona State University: The Center For Negative Carbon Emissions

Their goal is to demonstrate a system that enhances the efficiency and scalability of DAC while reducing costs. Currently, they are testing a prototype technology utilizing “mechanical trees” to extract CO2 from the air. These 10-meter-high structures employ a sorbent, an anionic exchange resin, which absorbs CO2 when dry and releases it when exposed to moisture.

ASU “mechanical tree”

Within just 20 minutes, these “mechanical trees” can capture greenhouse gases brought by the wind. The collected CO2 is then converted into a liquid that can be used to produce carbon-neutral fuel, other products, or sequestered for permanent disposal.

The research on mechanical trees has been ongoing for two decades and was pioneered by Dr. Klaus Lackner, the director of the Center for Negative Carbon Emissions. These trees are remarkably efficient, being a thousand times more effective than natural trees at removing CO2 from the atmosphere.

In addition to technological advancements, the center also examines the economic, political, and social implications of widespread implementation of affordable DAC technology, aiming to lead the way in the field of direct air capture.

ASU Climate Positive Pledge

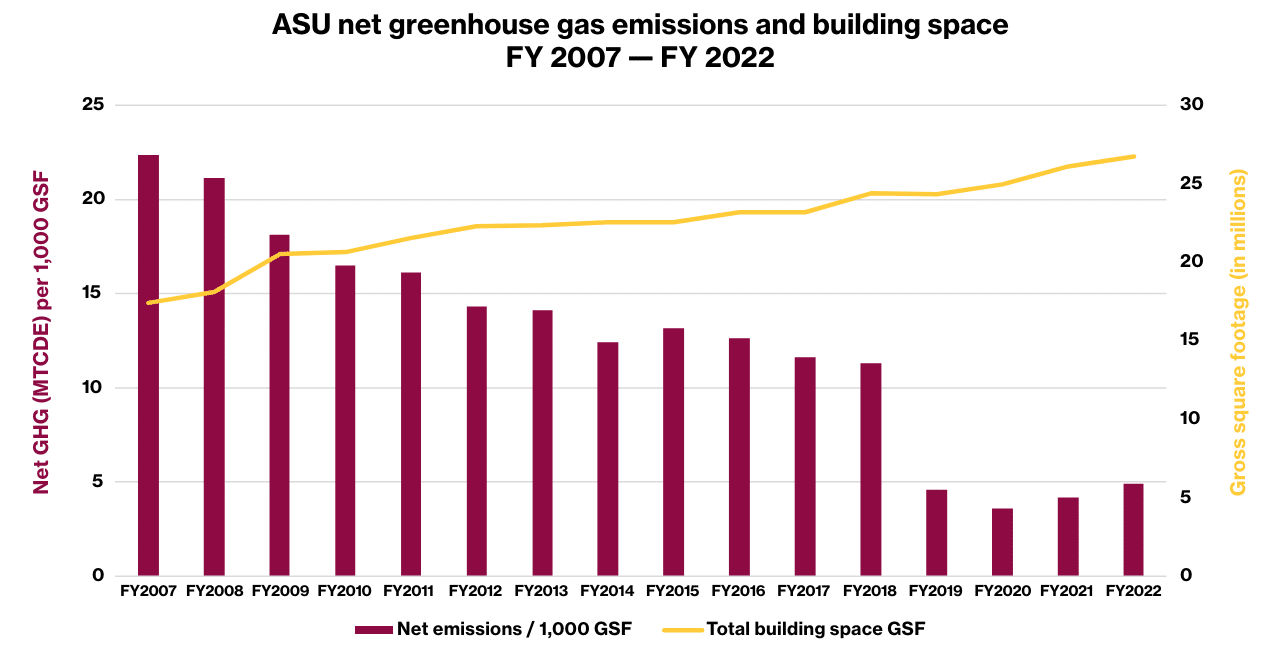

Since fiscal year 2019, the university has been carbon neutral for scope 1 and 2 emissions through energy efficiency measures, green construction, offsetting, and renewable energy acquisition. The university is working toward achieving the same for its Scope 3 emissions by 2035.

ASU emphasizes energy efficiency and conservation through various initiatives. The university also promotes low-carbon energy sources, with 43% of energy in 2022 coming from such sources.

The school further aims for carbon-neutral transportation by 2035, achieving a milestone with single-occupancy vehicle travel reduced to 59% in 2022. Initiatives include bike parking expansion, ride-sharing incentives, electrification of fleet vehicles, and free intercampus shuttles. ASU also imposes a carbon price on air travel to mitigate emissions.