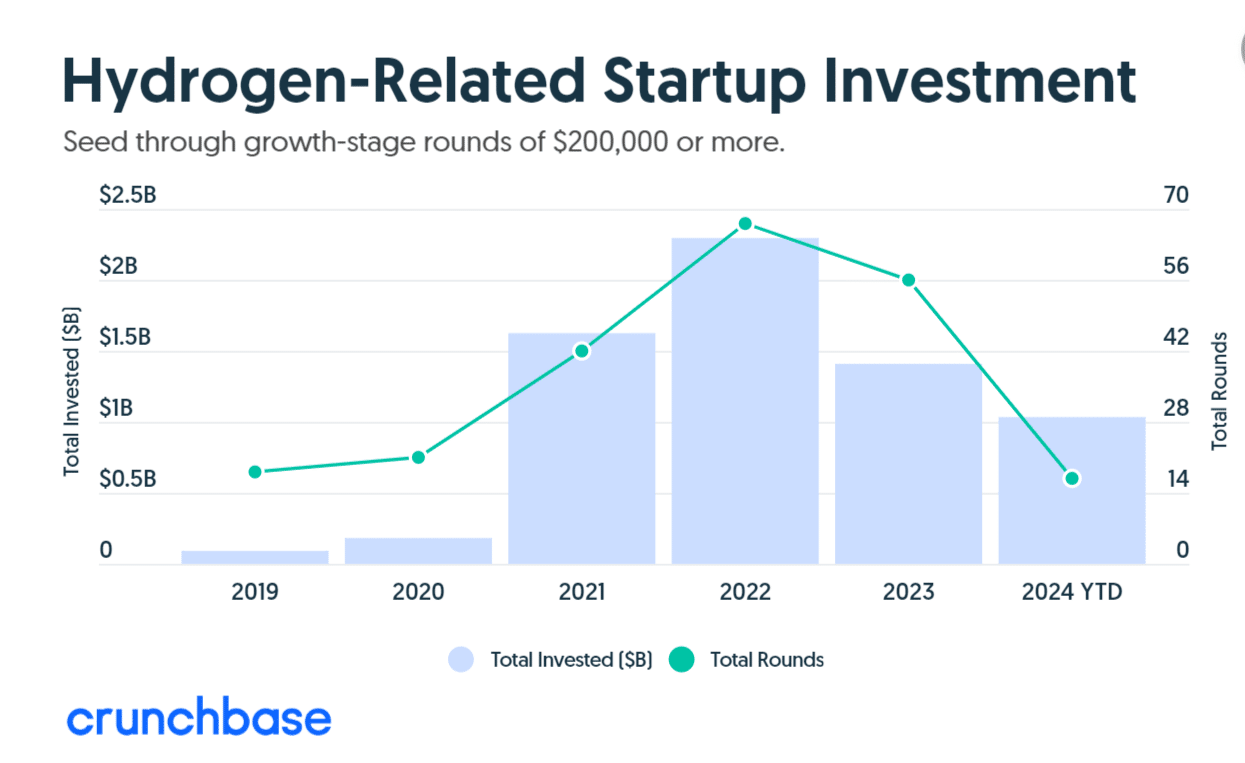

Hydrogen technology startups have secured over $1 billion in venture investment in the past four months, according to Crunchbase data. This already surpasses two-thirds of last year’s total, and the surge includes several significant early-stage rounds, including:

- Hysata: Last week, the Australian electrolyzer developer raised $110 million in a Series B co-led by BP Ventures and Templewater.

- Koloma: Denver-based Koloma, focused on geologic hydrogen resources, secured $246 million in a Series B led by Khosla Ventures earlier this year.

READ MORE: Bill Gates Backs Stealth Startup with $91M for Hydrogen Revolution

Hydrogen energy startup investment didn’t peak in 2021. Instead, funding reached its highest in 2022 and is on track to surpass that this year.

Notable Hydrogen Startups and Funding

Crunchbase data lists 13 well-funded hydrogen startups that raised significant capital recently. Collectively, they have secured $3.66 billion in equity funding, plus additional grant and debt financing.

Key examples include:

- HysetCo: Based in France, HysetCo operates hydrogen distribution stations and mobility services. It raised $216 million in April, managing a fleet of over 500 hydrogen vehicles and distributing nearly 30 tons of hydrogen monthly.

- Ohmium: The Nevada-based company is manufacturing proton exchange membrane systems to produce pressurized, high-purity hydrogen. It secured $295 million in Series C in April last year.

- Tree Energy Solutions: This Brussels-based company closed a $150 million Series C in April to use renewable energy for generating green hydrogen, which it combines with recycled CO₂ to create e-NG.

- ZeroAvia: The California-based developer of hydrogen-electric engines for zero-emission flight raised $116 million in a Series C in September. Airbus is the lead investor, along with United Airlines and Alaska Air Group.

- Electric Hydrogen: This Massachusetts company raised $380 million in a Series C last October. It manufactures electrolyzers to produce hydrogen at the lowest cost and is the green hydrogen industry’s first unicorn.

A week ago, the US Department of Energy revealed its R&D priorities to cut clean hydrogen cost production, potentially at $1 per kilo by 2031.

READ MORE: DOE Sets Eyes on Cutting Clean Hydrogen Cost, $1/Kilo by 2031

Global Initiatives Driving Green Hydrogen Growth

Investors’ increasing interest in green hydrogen is driven by government incentives, technological advancements reducing costs, and favorable market conditions. This combination of factors suggests a promising future for low-emission hydrogen technologies, potentially marking a pivotal moment for the industry.

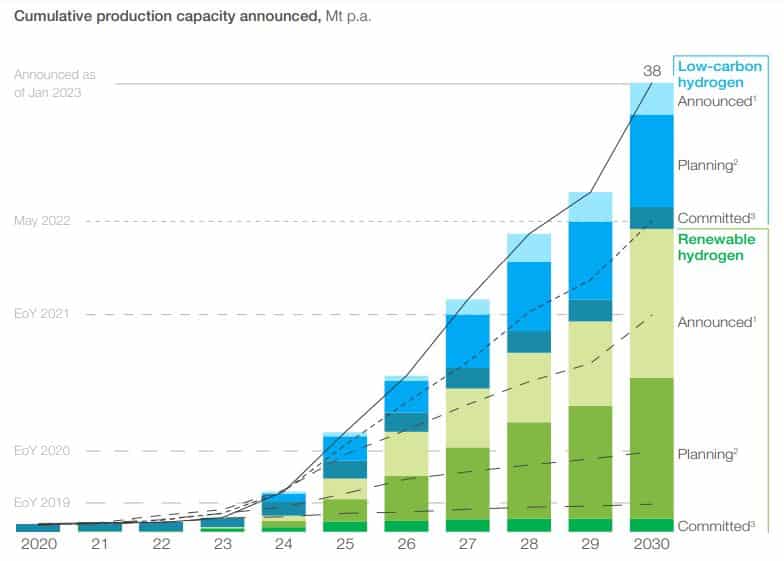

Data from Mckinsey & Company below shows that the hydrogen production capacity announced increased by 2030 (over 40%). This capacity is about 50% the volume necessary to be on track to net zero emissions.

In April, the EU Commission approved a $380 million German scheme to enhance renewable hydrogen production. This groundbreaking initiative will be administered exclusively through the European Hydrogen Bank’s “Auctions-as-a-Service” tool.

The scheme supports the objectives of REPowerEU and The European Green Deal. It outlines a comprehensive strategy to reduce reliance on fossil fuels and transition to a net zero economy.

By fostering renewable hydrogen production, the scheme aims to decrease dependence on Russian fossil fuels and contribute to the EU’s green energy future.

India, the world’s 3rd largest polluter plans to be the largest producer and exporter of green hydrogen by setting ambitious milestones. According to the Indian Ministry of New and Renewable Energy, the key goals include:

- Production Capacity: Establishing a capacity to produce at least 5 Million Metric Tonnes (MMT) of green hydrogen annually by 2030.

- Global Demand: Aiming to drive global demand for green hydrogen and its derivatives, such as green ammonia, to nearly 100 MMT by 2030. India targets capturing 10% of the global market, with an annual export demand of about 10 MMT of green hydrogen/green ammonia.

- Decarbonization: Mitigating 50 MMT of CO2 emissions annually through the implementation of green hydrogen initiatives.

In the Gulf region, Oman Energy Development’s subsidiary, Hydrom, hosted a second-round public auction for green hydrogen development in the Dhofar Governorate. Hydrom offers three prime blocks ranging from 340km² to 400km² in the Dhofar Governorate for green hydrogen production. The auction will leverage the region’s abundant renewable energy resources to build a robust green hydrogen industry in the sultanate.

The surge in venture investments in hydrogen technology startups highlights the sector’s growing momentum. With significant early-stage funding rounds and robust global initiatives, the future of green hydrogen looks promising.

Subsequently

Subsequently

Sources:

Sources:

source: Stockholm Exergi

source: Stockholm Exergi