The newly appointed President of the World Bank, Ajay Banga, unveiled plans to launch a mechanism for certifying forest carbon credits in the coming months. His mission is to revolutionize the bank’s operations while enhancing the credibility and transparency of voluntary carbon markets.

Banga emphasized the urgent need to redirect resources from affluent nations to less prosperous regions to address climate-related challenges.

In his address to a substantial audience at the Singapore FinTech Festival, he stressed that achieving this goal cannot solely rely on taxation or calls for financial contributions from wealthier countries due to political barriers. Instead, Banga proposed that reinforcing the trustworthiness of voluntary carbon markets holds the key.

Revamping Forest Carbon Credits for Credibility

The World Bank’s imminent certification mechanism for the forestry sector aims to establish reliable carbon credits. It also seeks to ensure proper pricing and direct resources appropriately.

Banga highlighted the significance of incorporating safeguards against deforestation and misleading reforestation practices to enhance the credibility of these markets.

During a conversation with Ravi Menon, the head of Singapore’s central bank, Banga emphasized that endorsing certified green credits could potentially streamline the carbon pricing process.

This strategy is meant to facilitate the flow of funds from companies and investors in developed nations to developing countries. The latter often provide the forest carbon credits that rich nations are buying.

Carbon credits have been a mechanism for companies and governments to mitigate greenhouse gas emissions. However, recent incidents such as the case with South Pole, a major carbon offsets player, have tainted the industry’s reputation.

Renat Heuberger’s exit as South Pole’s CEO followed accusations that the company exaggerated the climate impact of its products. Ajay Banga’s initiatives aim to address such credibility issues and instill trust in the carbon credit markets.

It’s important to note that major companies are also trying to rebuild confidence in these markets. Large asset managers and investors such as Manulife and Stafford Capital have raised millions of dollars in closing their forest carbon credit funds. Also, the likes of Oak Hill Advisors are also spending billions to reduce logging and boost forest carbon deals.

Redefining World Bank’s Focus

Ajay Banga’s leadership at the World Bank has introduced innovative proposals. The major one is expanding the institution’s focus on poverty alleviation to address urgent global issues like climate change.

During his address at the FinTech Festival, Banga advocated for the repurposing of subsidies that contribute to environmental harm. He highlighted the necessity to redirect subsidies, which presently support fossil fuels, towards initiatives that combat climate change.

Emphasizing the significance of allocating resources more thoughtfully, he expressed the need to reconsider how public funds are utilized, saying that:

“Repurposing these subsidies can be enormously helpful in the fight on climate…We must find a better way to spread the peanut butter.”

According to a World Bank report, the global expenditure on sectors like agriculture, fishing, and fossil fuels amounts to a staggering $1.25 trillion annually—equivalent to the size of a major economy such as Mexico.

Banga also stressed the role of multilateral development banks (MDBs), including the World Bank, in mitigating risks associated with climate-related projects. He proposed the idea of absorbing initial losses from projects like wind and solar, making them more appealing to investors.

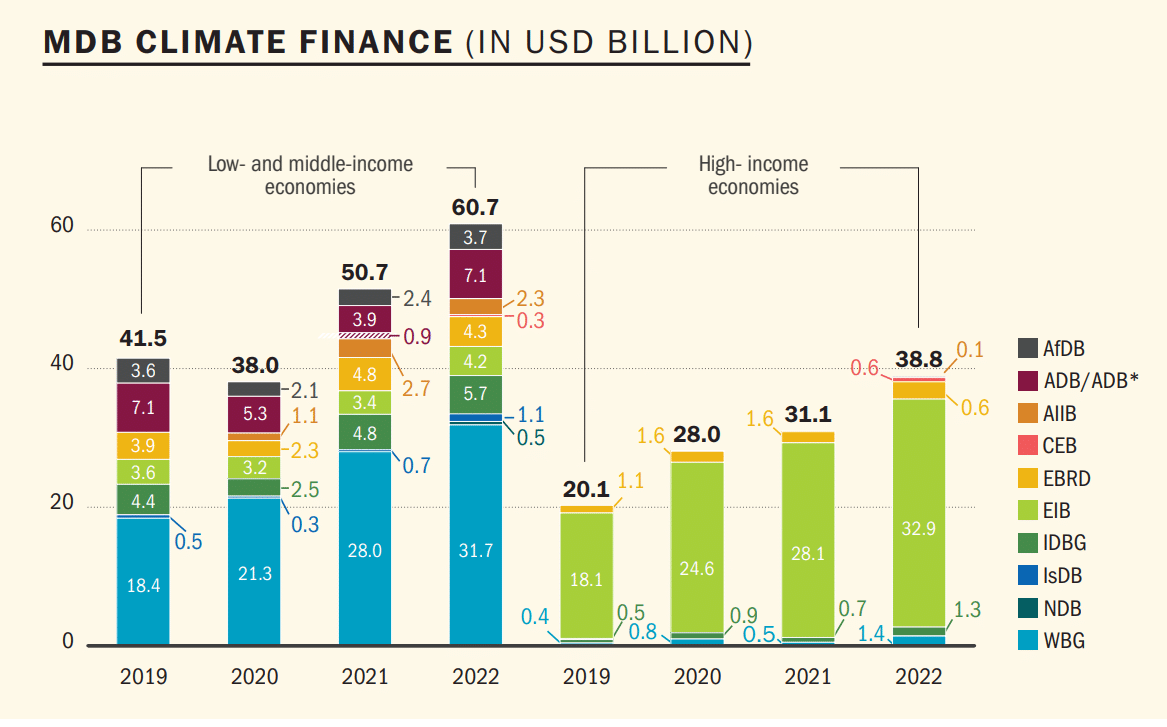

In 2022, about $61 billion of MDB climate finance was given to low-income and middle-income economies. 63% ($38 billion) of this total was for climate change mitigation finance and 37% ($22.7 billion) for adaptation finance.

Source: 2022 Joint Report on Multilateral Development Banks’ Climate Finance

Mitigating Risks in Carbon Markets

However, Ravi Menon, Singapore’s central bank chief, cautioned that using public capital to reduce project risks has practical challenges and lacks universal acceptance. Concerns about political and foreign exchange risks could deter Western funds from investing in emerging market climate projects.

But Banga countered by underscoring the importance of MDBs in addressing regulatory risks. These financial institutions could offer risk guarantees and insurance to incentivize private investment.

The World Bank’s insurance arm protects investments from non-commercial risks, enhancing access to funding with better financial terms. The new president believes that the bank’s expertise is crucial in this space. Their backing will bolster private sector investments.

Recently, companies like Kita Earth are also introducing insurance products to protect carbon credit purchases. This safeguard has never been more crucial in building trust to scale this essential market that helps combat climate change.

Backing carbon markets underscores a strategic shift in the World Bank’s role. It positions the institution as a key player in steering financial resources towards sustainable and climate-resilient initiatives while navigating the challenges associated with global investment in climate-related projects.

California enacted a law in 2022 to phase out gas-powered vehicles by 2035, and now it’s planning to do the same for millions of lawn mowers, taking effect in 2024.

The state will ban the sale of gas-powered lawn care equipment according to a new law phasing out small, off-road engines.

Small But More Terrible in Polluting Than Cars

The world’s 4th-biggest economy will be the first to phase out fossil fuel-powered landscaping tools. This decision marks a significant move in environmental policy.

The ban isn’t just about eliminating the noise the equipment causes but primarily focuses on curbing emissions from small engines. These small, off-road engines (SOREs) are known to be more polluting than all cars combined in the state.

California’s ambitious goal of achieving carbon neutrality by 2045 requires addressing emissions from various sources, including SOREs. The comparison drawn by the California Air Resources Board (CARB), a state agency that regulates air quality, between the emissions from these SOREs and a 2016 Toyota Camry’s output is quite striking:

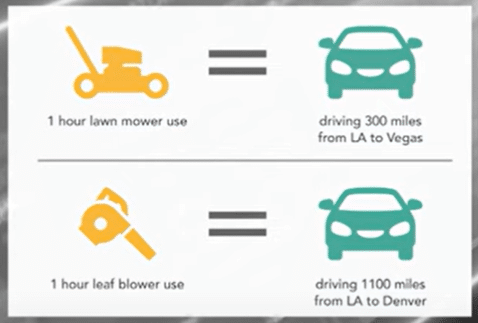

1 hour use of a gas-powered lawn mower releases as much pollution as a Toyota Camry does over 300 miles.

The ban has sparked a debate similar to the controversy surrounding the ban on gas stoves. Opposition from certain groups, including some Republicans and gas companies, argues that these restrictions impede consumer choice.

A policy analyst at the environmental think tank Frontier Group highlighted the growing awareness of the impact of gas stoves and gasoline-powered lawn equipment on public health. This move will be closely observed by policymakers across the country to assess its effectiveness in driving environmental change.

The ban also serves as a test of Americans’ acceptance of cleaner technologies in their daily lives amid increasing restrictions on gas-powered appliances, traditional vehicles, and the fervent push toward electric alternatives by companies.

The ban on gasoline-powered lawn equipment in California could signify a transformative shift in the landscape of suburban America, where manicured lawns symbolize status and pride. The cultural significance of lawns in the post-war era was associated with the acquisition of homes by returning veterans. Their well-manicured grassy yards became a hallmark.

Back in the 1950s, having a lawn was not a choice but an inherent aspect of owning a house. However, this American dream came at an environmental cost.

Gas-powered lawn equipment, as per the CARB, emits pollutants comparable to driving a car 300 miles in just an hour. The emissions from these tools, especially lawn mowers and leaf blowers, significantly contribute to air pollution while generating excessive noise.

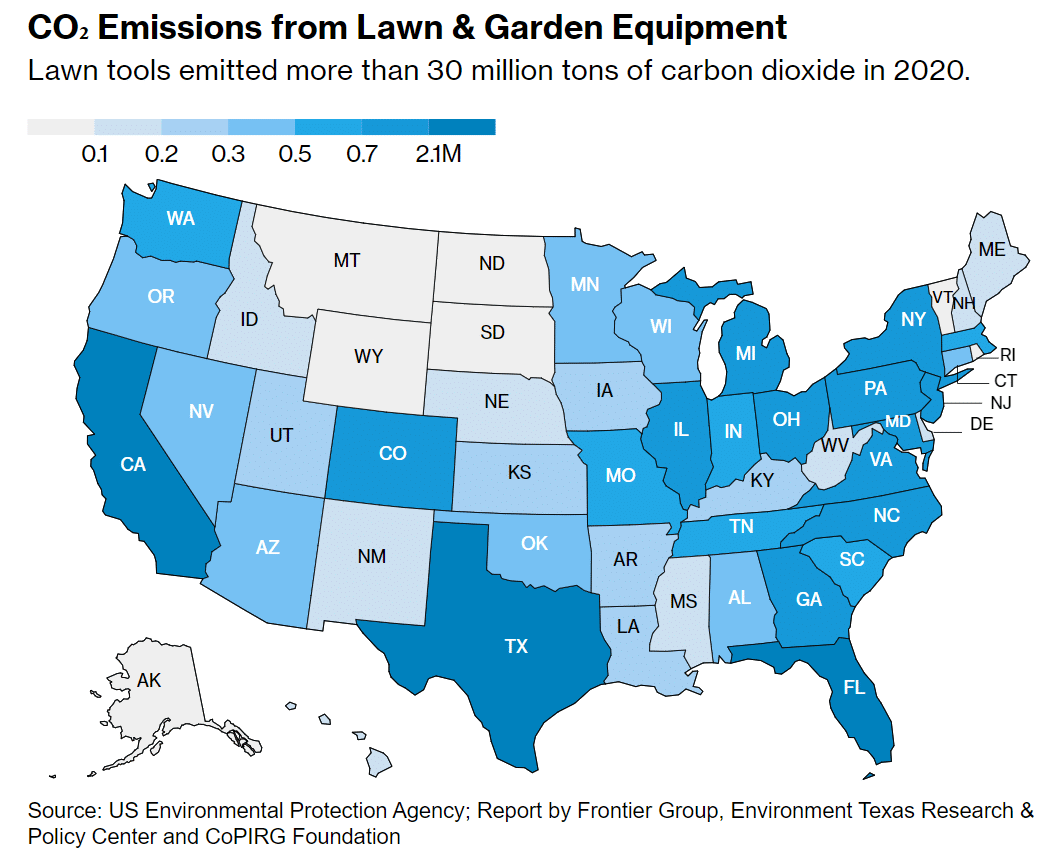

In 2020, lawn tools emitted over 30 million tons of CO2, geographically illustrated below per state.

The emitted gas can negatively impact both human health and wildlife; in contrast, electric alternatives offer quieter and cleaner operation.

The need to maintain lawns has evolved into a substantial industry. The North American market accounts for a considerable portion of the global power lawn and garden equipment market.

Today, manufacturers are investing heavily in encouraging consumers to adopt battery-powered options, particularly as regulations become more stringent. In fact, many individuals and businesses have already transitioned to electric alternatives voluntarily or due to local regulations.

Moreover, various cities and towns nationwide have implemented bans or restrictions on gas-powered equipment, including those in Naples, Florida and Washington, DC. Their decisions emphasize growing awareness and action toward cleaner and quieter lawn maintenance practices.

The Big Push for Electrifying Appliances

The movement towards electric lawn equipment is gaining momentum, driven by incentives provided by local governments and evidenced by an uptick in sales of electric tools. This shift reflects an acknowledged reality among lawn equipment manufacturers: the future lies in battery power.

While companies like Stanley Black & Decker Inc. aren’t entirely eliminating gas-powered equipment, they are prioritizing electrified devices.

Other manufacturers, like Husqvarna and Honda, are focusing on innovations like robotic mowers and autonomous, battery-powered equipment, designed to navigate and maintain lawns efficiently.

Image from Honda website

However, not everyone is readily embracing this transition to electrification, particularly because of the costs. Electric tools can come with a price premium of up to 25% for hand-held grass cutters and 50% for push mowers compared to their gas-powered counterparts.

Concerns also revolve around the performance, durability, battery life, and charging limitations of electric models, especially for extensive landscaping tasks.

The California rule banning the sale of new gasoline-powered lawn equipment in 2024 aims to drive this transition without prohibiting the use of existing gas-powered tools. The new policy also allocates $30 million for rebates and programs to aid landscapers in shifting to zero-emission equipment.

Just last month, the state enacted the nation’s first-of-its-kind climate disclosure law that requires companies to report on their carbon emissions and climate-related financial risks.

The lawmaker behind the new legislation, Marc Berman, envisions a broader implication beyond landscaping. He hopes it will pave the way for more aggressive policies targeting gas-powered appliances like heaters and pumps. The ultimate goal is to achieve significant reductions in air pollutants and greenhouse gas emissions.

The Supervisory Body overseeing Article 6.4 of the Paris Agreement has recently released a preliminary draft document outlining proposed methodologies for carbon reduction projects. This is important as the most anticipated climate conference, COP28, will take place starting this November 30 in Dubai.

The methodologies are integral for projects aiming to claim Article 6.4 emission reduction credits, also called 6.4 ERs. The focus of the draft recommendation centers on the requirements set for projects aimed at curbing greenhouse gas (GHG) emissions.

Supervising “The Mechanism”

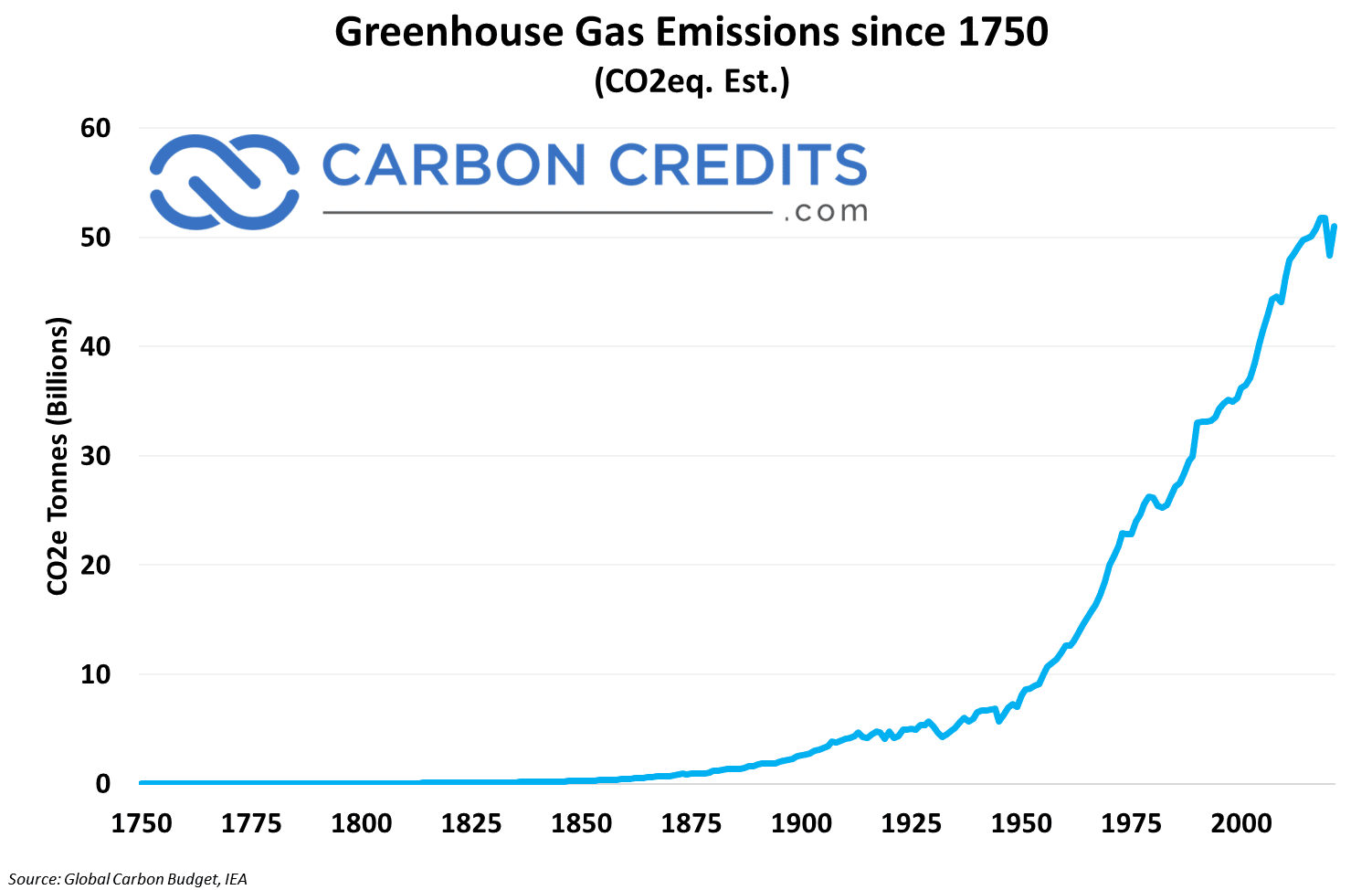

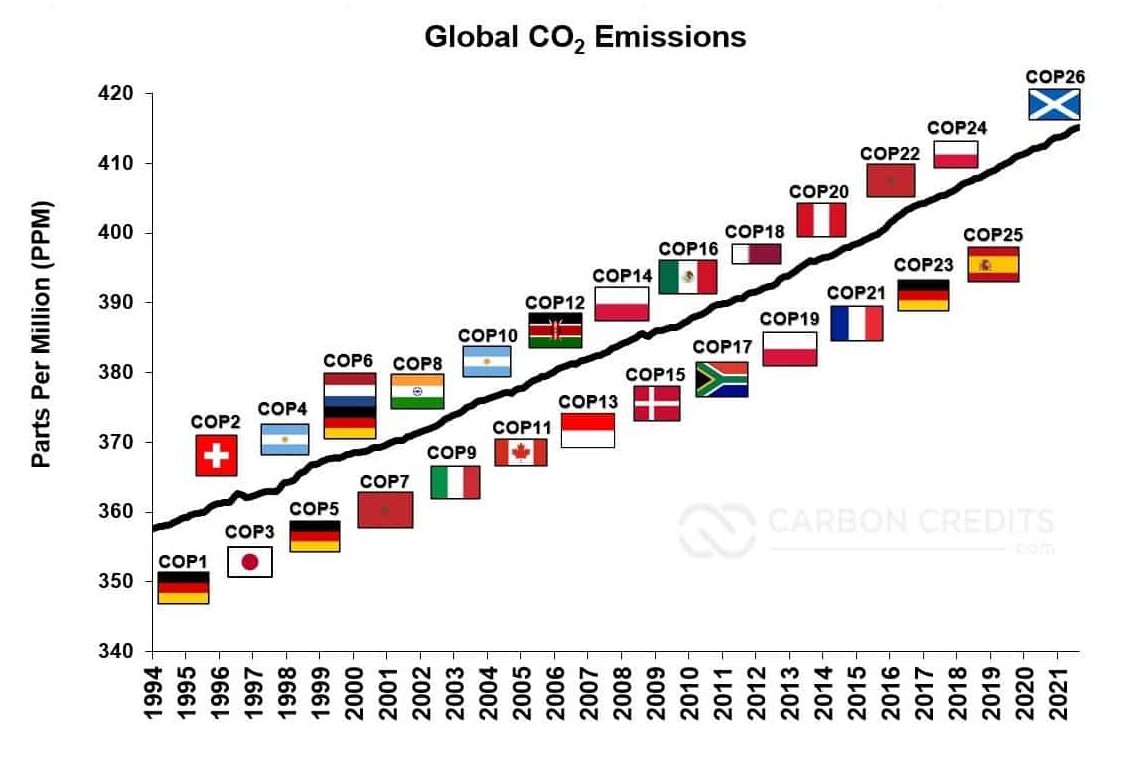

The Conference of the Parties (COP), serving as the meeting of the Parties to the Paris Agreement (CMA), during its 3rd session held in Glasgow, made a significant decision by adopting Decision 3/CMA.3. The COP timeline is shown below, alongside the rising global carbon emissions.

The decision captures the rules, procedures, and operational framework for the mechanism established by Article 6, paragraph 4, of the Paris Agreement, commonly referred to as “the mechanism.”

In line with this decision, the CMA has appointed a Supervisory Body responsible for overseeing and administering the mechanism. It operates under the authority and guidance of the CMA.

The Supervisory Body also works with full accountability to the COP.

Comprising 12 members from Parties to the Paris Agreement, the Supervisory Body ensures a wide and fair geographical representation. Its members aim for a balanced representation, with this composition: 2 members from each of the 5 United Nations regional groups, 1 member representing the least developed countries, and 1 member representing small island developing States.

The term of service for the newly appointed members begins from the first meeting of the Supervisory Body this year.

Key Principles for Emissions Reductions & Accountability

Central to the Body’s proposed methodologies are several key principles and features of carbon projects.

For instance, the methodologies advocate for a cautious approach in estimating a project’s emission reductions or removals. This is to ensure the credibility of the credits and to promote greater ambition in emissions reduction efforts.

It involves establishing emission baselines below the scenario of business-as-usual GHG emissions that would have occurred without the carbon project.

Moreover, to uphold increasing environmental ambition, the draft suggests that the baseline should “evolve or lead to a downward adjustment of creditable emission reductions over time”.

Additionally, stakeholder involvement throughout the methodology development process and accounting for potential uncertainties associated with the underlying data are crucial aspects emphasized in the draft.

Demonstrating a project’s additionality is another pivotal requirement within each methodology. It requires an assessment showing that the project activity would not have taken place without the incentives from the mechanism. But this should consider all relevant national policies, including legislation.

Mechanism methodologies will also need to address project leakage. This refers to a change in GHG emissions outside the project boundary linked with the project’s activities.

Finally, the document touches upon non-performance and reversal aspects. These pertain to the potential reversal of emission removals or the risk that the carbon avoided or removed might not remain so for the duration of the project. An example would be a wildfire, which has been reversing the carbon removals of the trees under a carbon project.

The draft mentions the ongoing need for the supervisory body to further develop guidance in these areas.

What Comes Next?

Some market players have commented on the draft prior to its release. An accredited observer organization highlighted the need to come up with an agreed definition of “removals”. They refer to clearly identifying exact removal of greenhouse gasses (GHG) versus carbon dioxide (CO2).

The Supervisory Body responded accordingly, adopting this final definition on its recently published draft:

“Removals are the outcomes of processes to remove greenhouse gasses from the atmosphere through anthropogenic activities and durably store them…”

Given the timelines associated with investments in project activities and the preparatory period for project implementation, the VCM is expected to remain the predominant platform for investment. This is likely to persist until 2025, if not longer, as frameworks and methodologies for the mechanism are established.

Therefore, the VCM will continue to attract investments until the Art 6.4 mechanism drafted becomes fully operational.

Nonetheless, the Supervisory Body’s focus on key principles such as cautious estimation of emission reductions, stakeholder involvement, and addressing uncertainties reflects a commitment to credibility and accountability. The preliminary draft outlining methodologies for carbon reduction projects signifies a pivotal step in establishing frameworks for emission reduction credits.

Xpansiv’s CBL provided an update on its latest carbon markets results. The report provides an overview of recent activities in emissions, renewable energy credits, and compliance markets. It further details trading volumes, prices, and specific market movements across different regions and instruments.

In the space of renewable energy credits (RECs) trading, Maryland and New Jersey dominate.

Trading Carbon Credits On The Rise

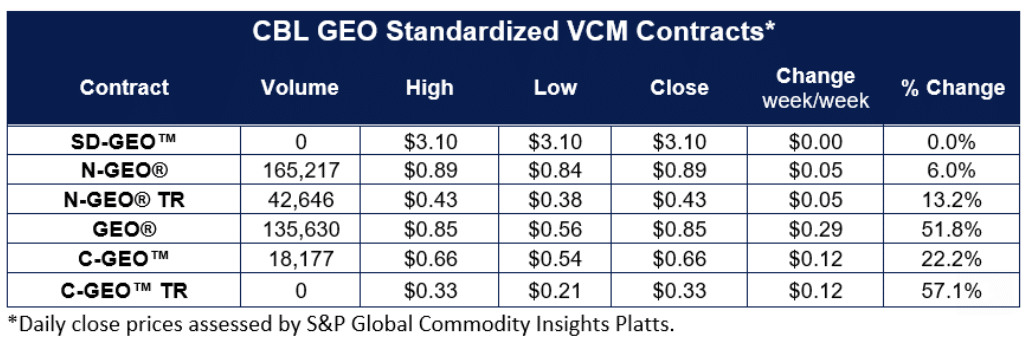

Last week witnessed a notable surge in spot and front-month CBL GEO futures contracts at 52%, surpassing the rise of the resurfacing CBL N-GEO at 40%. Both have experienced significant increases in trading volume and prices, with N-GEO poised to bounce back in pricing the broader nature-based sector.

However, the spot contract’s volume was traded OTC (over-the-counter) at higher prices. A substantial portion of CBL VCM’s volume was traded through its GEO benchmark contracts.

In particular, about 80% of CBL VCM 456,239-ton volume was traded. This included 207,863 tons via the N-GEO current and trailing vintage instruments.

For other important results, here are the key takeaways:

Project-Specific Transactions:

There are various project-specific transactions that occurred. Indonesian AFOLU credits closed at $6.95 while 2018 Brazilian nature credits at $3.00. Older vintage Brazilian nature and vintage 2001 Indian fuel-switching credits settled much lower at $0.35.

Gold Standard’s Announcement:

Gold Standard highlighted Rwanda’s issuance of a Letter of Authorization for a cookstove project. This achievement is historical, marking the first recognition of credits issued by an independent standard with an Article 6 authorization.

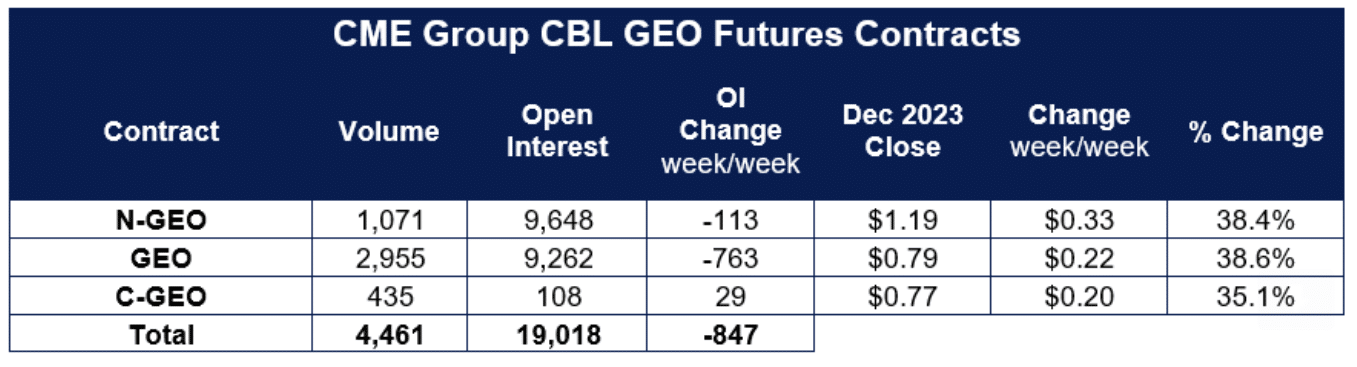

CME Group’s CBL GEO Emissions Futures:

December GEO and N-GEO, under the CME Group’s CBL GEO emissions futures complex, both saw a 38% rally. The total trading volume across CBL GEO futures was nearly 3 million tons, significantly higher than CBL N-GEO futures’ over 1 million tons.

Overall, 4,461,000 tons were traded across futures, much lower than the previous week (9,897,000).

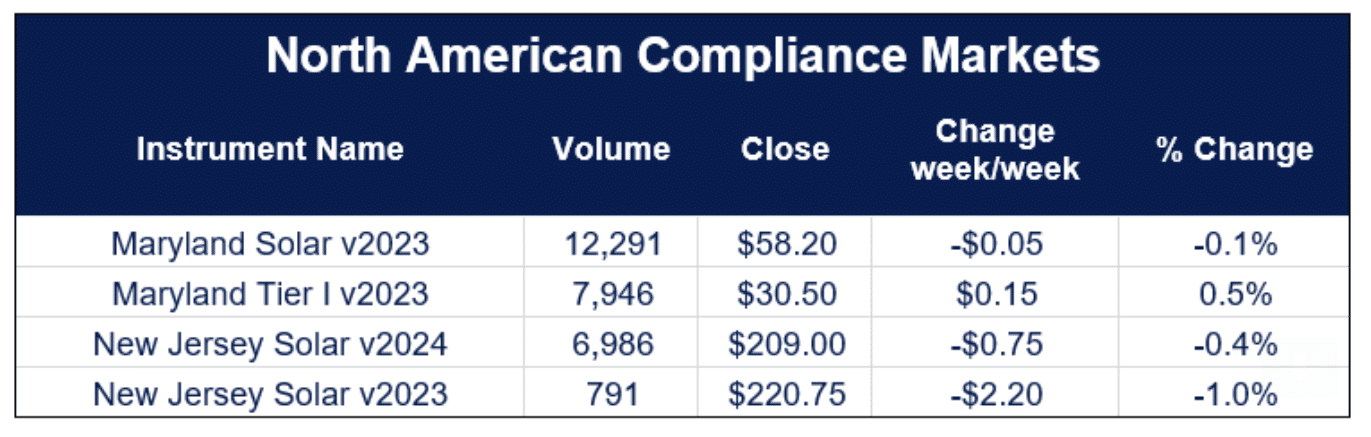

North American Compliance Carbon Markets

CBL works with environmental registries to facilitate the trading of both voluntary and compliance Renewable Energy Certificate (REC) contracts. It’s a type of carbon credits generated by choosing cleaner renewable sources over fossil fuels.

Xpansiv report’s highlighted the compliance REC market performance with the following results.

Maryland: Around 12,000 2023 Maryland solar credits were exchanged, with a closing price of $58.20 after multiple trades at $58.10.

New Jersey: Active trading occurred for both 2023 and 2024 vintage solar credits, with trades surpassing 1,000 credits at $209 and $222, respectively, before closing at $220.75 due to falling offers.

Xpansiv’s recent report on environmental markets outlines a notable surge in spot and front-month CBL GEO futures and CBL N-GEO. Trading volumes and prices for both have increased, signaling potential growth in the broader nature-based sector. Despite some fluctuations, CME Group’s CBL GEO Emissions Futures witnessed a significant rally, indicating a continued interest in emissions trading.

The dominance of Maryland and New Jersey in renewable energy credits trading, along with other transactions, underscores the diverse landscape within carbon credit markets.

A US-based Direct Air Capture (DAC) company, Heirloom, launches a novel climate solution that sucks in carbon dioxide from the air using limestone and locking it away in concrete. It is the first commercial DAC plant that opened in the U.S.

Capturing carbon from the air was once seen as unlikely. But today, it’s gaining traction as an important tool to fight the climate crisis. Funds from various sources are pouring into carbon removal initiatives and projects.

In the U.S., the current administration has committed nearly $4 billion towards promoting DAC and other carbon removal initiatives.

How Does Heirloom DAC System Work?

Located in Tracy, California, Heirloom facility aims to capture up to 1,000 tons of CO2 per year using limestone.

The DAC process involves heating the limestone to high temperatures, breaking it down into CO2 and calcium oxide using industrial kilns.

The captured carbon dioxide is then stored in concrete for construction purposes. The remaining calcium oxide is spread on trays, exposed to air, and sucks in carbon naturally. After 3 days, the powder is saturated with CO2 and is returned to the kiln, where the process begins again.

Heirloom claims their system uses fewer energy-intensive fans, leveraging limestone’s natural carbon-attracting properties. Other DAC systems use giant fans to pull CO2 from the atmosphere. Heirloom’s modular facilities enable easy expansion by employing larger trays for limestone and adding more trays to the setup.

The DAC company worked with another climate tech innovatorCarbonCure which stores the extracted CO2 in their concrete plants near Heirloom’s facility.

The company’s CEO, Shashank Samala, shared that his motivation in developing the technology is the worsening effects of climate change he experiences in his home country, India. Emphasizing the need for impactful climate solutions, he noted that:

“For me, it’s really important to work on a solution that actually has a meaningful, scaled impact on climate change, to actually make a dent on this.”

However, the DAC facility’s capacity to absorb carbon is limited, capturing only 1,000 metric tons of CO2 annually. That’s only a small fraction of what a gas-fired power plant emits yearly.

But the company has an ambitious goal of removing 1 billion tons by 2035, subject to considerable scale up challenge. The company plans to triple this capture capacity each year over the next 12 years to reach that goal.

The Hurdles and The Hope in Carbon Capture

That level of scale up needs a lot of money and the good news is that tech companies are significantly supporting DAC.

For instance,Microsoft has inked a long-term carbon removal agreement with Heirloom. Their deal is to capture up to 315,000 metric tons of CO2, offsetting its own emissions towards its net zero targets. Moreover,Frontier, a carbon removal fund, has pledged massive support to Heirloom and similar carbon capture ventures.

Heirloom expresses its commitment to using renewable energy from local providers and refrains from accepting investments from oil majors. They asserted that the carbon captured from DAC won’t be used to enhance oil extraction, aligning with their principles of responsible environmental stewardship.

The DAC firm’s latest achievement involves securing a substantial$600 million award from the Department of Energy to establish a processing hub in Louisiana capable of handling up to a million tons of carbon per year. The agency is also supporting the other DAC plant in Texas developed byOccidental Petroleum.

However, despite such advancements, there are still obstacles in significantly reducing carbon dioxide levels.

A mechanical engineer highlights thatdirect air capture technology remains costly and demands substantial energy. A scientist also underscores the economic challenges in relation to the scale of the atmosphere. He pointed out the uncertainty of entirely resolving the climate crisis, even with the application of all available solutions.

Despite these challenges, Samala remains hopeful that the world increasingly recognizes the important role of DAC in tackling climate change. Comparingcarbon capture with waste collection, he said that people should consider paying for removing carbon they generate.

“We need to pay for the CO2 we are putting out there,” he asserts, highlighting the necessity for greater accountability regarding carbon emissions.

Capturing Carbon and Generating Credits

Notably, climate-tech startups focusing oncarbon emissions technology received $7.6 billion in venture capital funding in Q3 this year. This VC funding result is defying the downturn trend in fundraising.

Heirloom offerscarbon credits that companies and government entities can purchase to offset their emissions. These credits represent an exchange where an individual or company pays for CO2 emissions removed by an entity specializing in carbon capture.

Prominent companies likeStripe,Shopify,Klarna, and Microsoft are among Heirloom’s initial buyers of these credits. The advanced purchasing model allows organizations to offset their emissions by investing in carbon removal initiatives.

Positioned as the first commercial DAC plant in the U.S., Heirloom’s system leverages natural properties of limestone that require fewer energy-intensive mechanisms compared to conventional DAC systems. Despite challenges, Heirloom has set ambitious goals, aiming to scale up itscarbon capture capacity significantly by collaborating with tech giants and securing substantial funding. The company emphasizes the critical role of DAC in mitigating emissions and fostering a sustainable future.

In the realm of long-haul trucking, a technological crossroads has emerged: the divide between hydrogen-powered and battery-electric trucks. As the industry grapples with stringent emissions regulations, particularly in California, truckers are starting to embrace hydrogen for zero-emission technology.

Companies like Nikola and traditional manufacturers are investing in hydrogen technology, aiming to overcome infrastructure challenges and meet growing demand.

The Shift to Hydrogen-Powered Trucks

Many truckers are shifting focus towards electric technology adapted for 18-wheelers. But there’s a clear divide between those favoring battery-cell rigs commonly used in electric cars and those considering hydrogen as the best solution for zero-emission technology, particularly for long-haul trips.

Supporters of hydrogen believe it offers advantages for long trips and quicker refueling compared to battery technology. Hydrogen trucks can carry heavier loads since they don’t require large batteries.

However, hydrogen fuel cell vehicle, also called FCEV, and infrastructure are not as developed as battery-electric trucks, and strict regulations are pressuring truck operators.

Starting January 1, California will mandate that trucks visiting the state’s seaports be zero-emission vehicles. The state also plans to increase the use of clean fuels, aiming to phase out diesel over the next decades.

These stringent rules on diesel trucks are among the toughest in the country, and other states might adopt similar regulations based on California’s lead.

The upcoming regulations have caused a surge in diesel truck purchases as carriers seek to expand their fleets before the restrictions come into effect. Truckers are also investing in zero-emission vehicles, although they come at a high cost, almost triple a diesel truck’s price.

These purchases are supported by grants from California and local agencies but hinge on the promise of future infrastructure development.

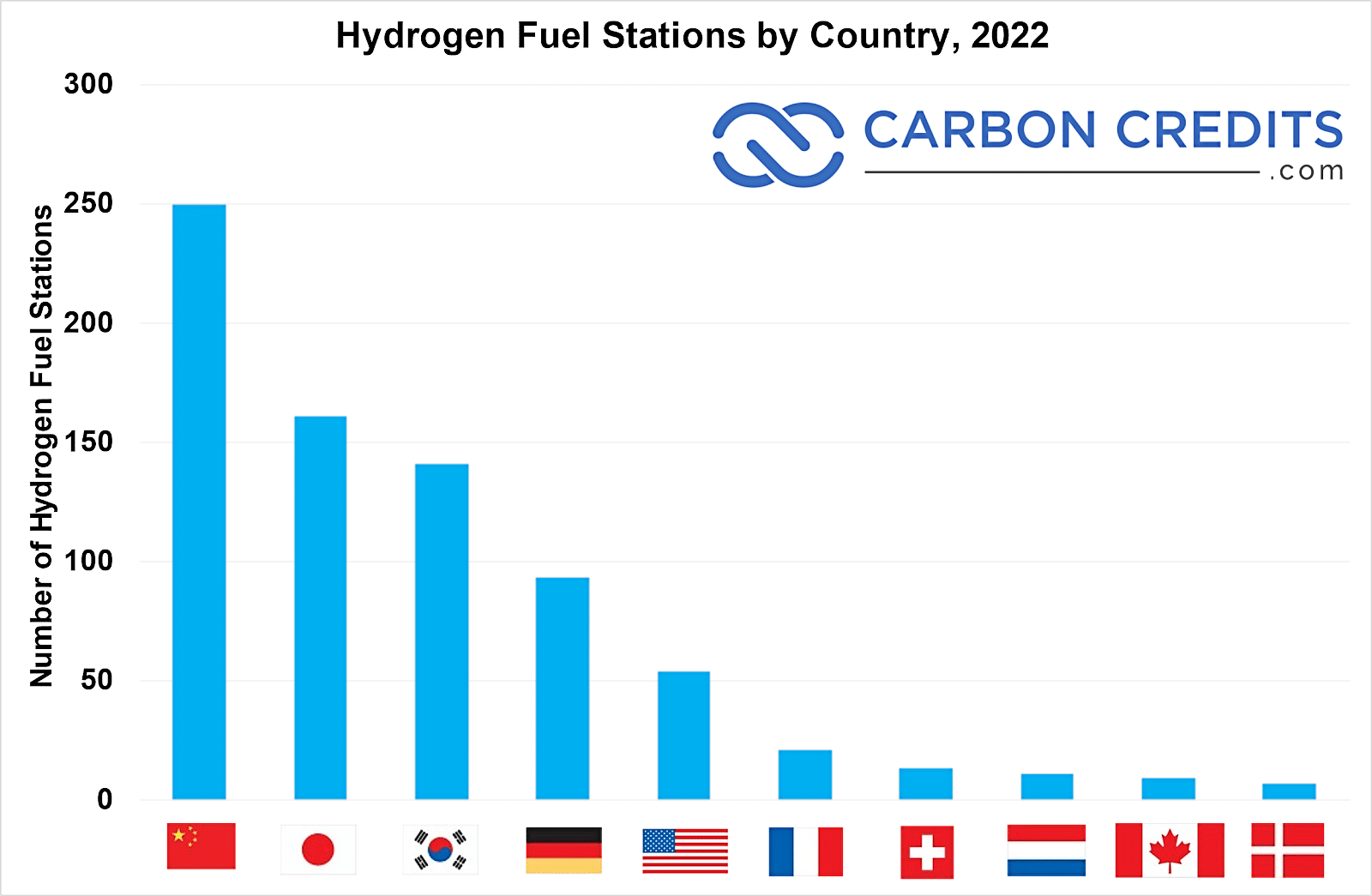

Battery-electric trucks are already in operation in California, with over a dozen companies transporting freight using these vehicles. However, hydrogen-powered trucks are just starting to enter the market in the state, and hydrogen-fueling stations are lagging behind battery-electric infrastructure.

Globally, China has the most hydrogen fuel network at around 250 while the U.S. only has a little over 50 stations, mostly in California.

Truckers find battery-electric trucks suitable for short trips between ports, rail yards, and warehouses. Yet, for longer journeys of 100 miles or more, they consider these trucks less practical due to limited battery range and lengthy recharging times.

Currently, battery-electric heavy-duty trucks can travel around 300 miles and take hours to recharge. Some truckers report getting just over 150 miles between charges.

In contrast, hydrogen trucks boast a range of up to 500 miles and refuel in about 30 minutes. They are also lighter than battery-electric rigs, enabling heavier loads.

While Nikola leads in hydrogen-truck technology, traditional manufacturers like Kenworth, Hyundai Motor, and Volvo Trucks are also working on developing hydrogen fuel-cell big rigs.

In July, Nikola received a $41.9 million grant under the Trade Corridor Enhancement Program (TCEP) to build 6 heavy-duty hydrogen refueling stations across Southern California through its HYLA brand.

Each hydrogen refueling station is designed to support and scale up the growth of heavy-duty commercial hydrogen refueling needs. Nikola also reached a milestone of sales orders for its hydrogen fuel cell electric trucks, reflecting a growing industry trend.

Hydrogen Holds The Promise of a Sustainable Energy

Napa-based trucking firm Biagi Bros recently trialed a hydrogen-powered Nikola truck for two months. Gregg Stumbaugh, their corporate equipment director, noted that due to the truck’s extended range and rapid refueling, their drivers accomplished twice the work compared to battery-electric trucks.

California’s regulations mandate that 10% of Biagi Bros’ 230-truck fleet must be emission-free by 2027. Stumbaugh expects most of their zero-emission trucks bought before then, including the upcoming 10 Nikola trucks to be run by hydrogen fuel.

He emphasized the quick refueling time as a significant advantage over battery-electric options.

Nikola’s CEO, Steve Girsky, aims to establish nine public fueling sites in California by mid-2024, a combination of the company’s HYLA brand and third-party providers.

They’re collaborating with Voltera to set up 50 Hyla hydrogen-fueling stations across key trucking routes in the next five years. Their goal is to “make sure there’s a supply of hydrogen everywhere there’s customers”, said Nikola’s CEO Steve Girsky.

While hydrogen refueling is faster, it remains expensive due to the limited fuel market.

Hyzon Motors‘ CEO, Parker Meeks, mentioned hydrogen’s cost being 2-4x higher per gallon than diesel. But as hydrogen becomes more prevalent, its price would decline in the next 3 years.

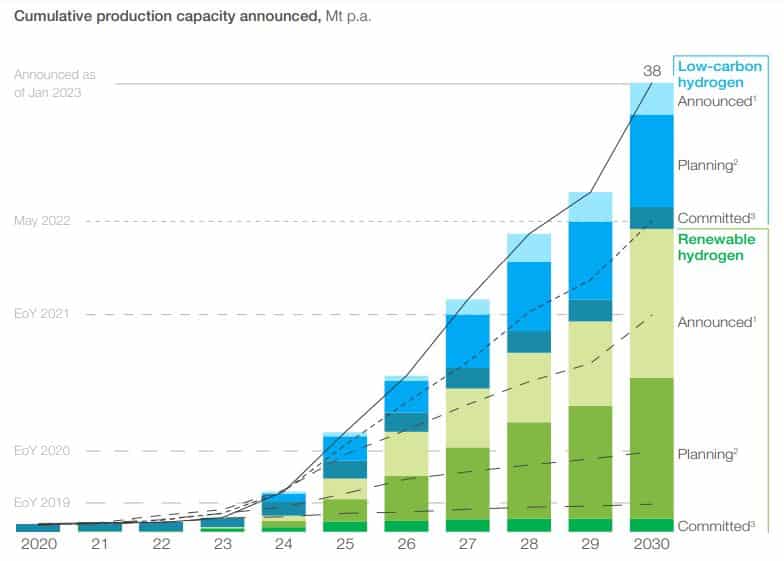

Meanwhile, McKinsey & Company estimated that the total hydrogen production capacity announced by companies by 2030 rose by 40% as shown below.

For Tennessee-based IMC, investing in hydrogen trucks is a necessity. The company operates regular round trips of about 300 miles between ports and warehouses. These are areas where battery-electric vehicles fall short due to range limitations.

The adoption of hydrogen-powered trucks in California is still in its initial stages. And hydrogen-fueling stations lag significantly behind those supporting battery-electric vehicles.

However, as the recent developments in the hydrogen market show, a revolution is unfolding where hydrogen seems to hold the promise of a sustainable energy transition.

The Attorney General’s office in New Hampshire is examining a plan proposed by Bluesource Sustainable Forest Company regarding the reduction of logging activities on a significant portion of the state’s forests as policymakers are working on bills associated with the use of carbon credits.

The area, covering 146,000 acres, was initially safeguarded for logging and recreational purposes through a conservation easement. The plan did not anticipate revenue generation through carbon credit markets, a recent development in the industry.

Bluesource, the new owner, aims to curtail logging by around 50% on this massive tract of land in 2024. That area represents about 3% of the state’s landmass.

Though the plan’s intent is to increase forest carbon sequestration, it affects local mills, loggers, the region’s economy, and potentially taxpayers.

The Value of Keeping Trees Standing

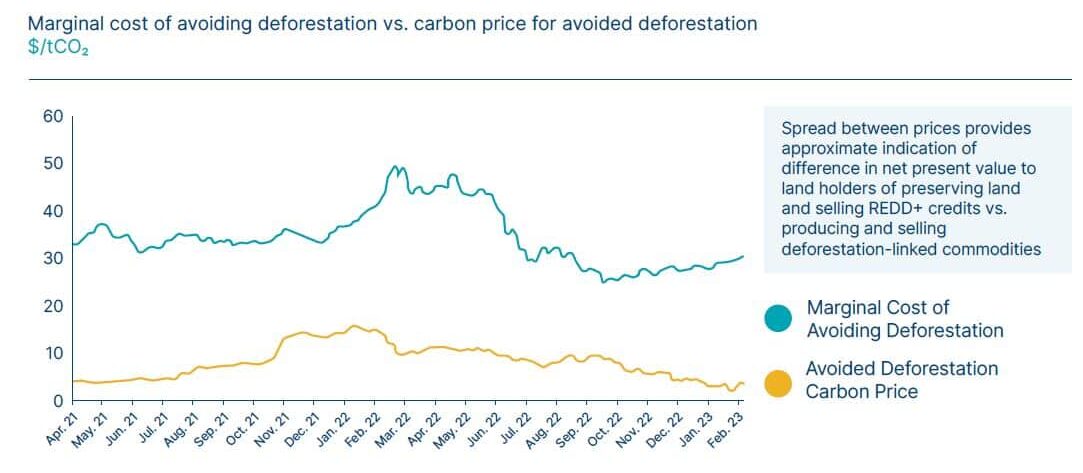

The shift towards less logging is due to the increasing value of preserving trees for carbon credits. It is a market-driven initiative aimed at reducing carbon emissions.

According to Energy Transitions Commission (ETC)’s report, the current price of carbon credits for avoiding deforestation isn’t enough to cover the marginal cost of avoiding commodity-driven deforestation.

The Attorney General’s office is assessing whether Bluesource’ planned reduction aligns with the original agreement established to protect the land.

The plan outlines the company’s goals, which are subject to the easement.

The easement acts as a safeguard, ensuring that the land remains protected from development. It also dictates how it should be utilized while outlining the responsibilities of both the state and the landowner.

From the original 171,500 acres, 25,100 acres were allocated to the state. Out of this, 25,000 acres were set aside for wildlife habitat management, while an additional 100 acres were allocated to expand the Deer Mountain Campground.

The easement guarantees public access for various traditional recreational activities such as hiking, hunting, fishing, trapping, snowmobiling along designated trails. However, it limits “non-forest activities” to a maximum of 10% of the property.

In addition to preserving open spaces, protecting natural resources, and nurturing wildlife habitats, the primary objective of the easement is to maintain the property as a financially sustainable land area for timber, plywood, and other forest product production. It explicitly permits “forest management activities,” including various methods of cultivating, harvesting, and removing forest products.

Bluesource’s move to participate in the carbon credit market wasn’t foreseen when the conservation easement was formulated two decades ago.

Promoting Forest Carbon Credits in the US

For ages, forests have been valued mainly for the timber they provide. However, efforts to combat climate change have given them an additional value by recognizing their ability to absorb and hold carbon.

Forests can trap nearly double the amount of carbon they release, acting as significant carbon storage.

In 2020, the U.S. Forest Service calculated that per acre in New Hampshire, forests held around 87 tons of carbon by 2018. Approximately 42% of this was in above-ground growth, with 38% stored in the forest soils.

When trees are cut down, processed, and used to create solid wood products like furniture or building materials such as plywood, their carbon remains stored within these products for potentially hundreds of years.

In 2003, there was no established carbon market in the US. Hence, the easement related to the Connecticut Lakes forest didn’t address managing the forest for carbon sequestration, storage, or carbon credit trading.

In 2022, Bluesource Sustainable Forest Company (BFSC) acquired the Connecticut Lakes Headwaters Working Forest, totaling a million acres managed. Thus, BFSC positions itself as “the largest private forestland owner entirely focused on addressing climate change.”

In 2021, Bluesource partnered with Oak Hill Advisors, a subsidiary of T.Rowe Price managing $500 billion in assets, to acquire forest lands, including those in New Hampshire.

BFSC’s president, Roger Williams, said that the collaboration would transition the company from developing projects generating carbon credits to becoming a forest land asset manager.

Additionally, last year, BFSC merged with Element Markets, a majority-owned entity of TPG Inc., an alternative investment manager. Element Markets describes itself as the primary creator and promoter of carbon and environmental credits across North America.

Companies that want to reduce their carbon emissions can buy the credits to offset their footprint. Each credit corresponds to one tonne of reduced or removed carbon from the air.

The Debate Goes On

Bluesource intends to reduce timber harvests by over half of what has been cut in recent years, particularly between 12,000 and 14,000 cords for the year ending April 2024.

Meetings, discussions, and proposed legislative actions are underway to address the broader consequences of the plan on the local economy. The potential outcomes could have a profound impact on the logging industry, the local community, and the area’s fiscal landscape.

In response to concerns, Bluesource is engaging with legislators and stakeholders, offering expertise and collaboration to deal with the situation.

According to Patrick D. Hackley, director of the state Division of Forests & Lands, Bluesource had submitted its revised Annual Operating Plan, noting that:

“We are now in the review process… to ensure the new harvesting plan, based on the company’s participation in California’s Air Resource Board Compliance (Carbon) Offset Program, complies with the purpose and all provisions of the conservation easement.”

Bluesource’s initiative to reduce logging for carbon credit generation within a preserved land area is raising debate in New Hampshire. The company’s move intersects with the long-standing conservation easement, provoking discussions on economic impact and forest carbon credit strategies.

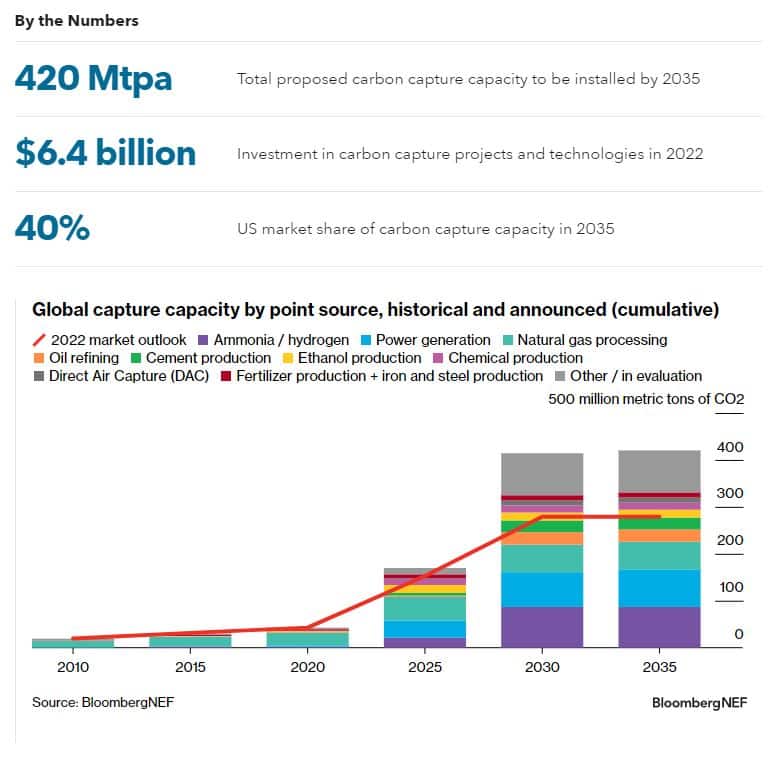

This year has seen the rapid growth of the carbon capture, utilization, and storage (CCUS) industry, owing to strong global policy support for projects and initiatives increasing capture capacity.

According to research company BloombergNEF (BNEF), the industry will see a 50% increase by 2025. It will reach 420 million metric tons a year by 2035.

Investments in CCUS infrastructure amounted to $6.4 billion in 2022, while funding this year will reach $5 billion.

CCUS Growth and Expansion

The CCUS market has initially focused on natural gas processing. But as decarbonization efforts intensify, it is expanding into carbon-intensive sectors, including power, cement, iron and steel.

BNEF reported that the industry captured over 140 million metric tons per annum (mtpa) from 2022. It is forecasted to grow at a 18% compound annual growth rate and capture 420 mtpa by 2035. This represents 1.1% of current global annual emissions.

The major sectors that will drive CCUS expansion include ammonia or hydrogen production and power generation. Together, they will account for 33% of announced carbon capture capacity.

It is interesting to note that the cement sector has experienced a massive increase in proposed carbon capture capacity – 175%.

Startups are also developing innovative technologies that can capture CO2 from the atmosphere and lock it away for good by injecting it into the cement.

The BNEF market outlook further noted that the US will remain the leader in deploying carbon capture. It will keep 40% in market share in 2035, followed by the UK at 16% share.

Canada ranks third at 12% while other large country emitters, including Australia, the Netherlands, and China will take 3-4% share.

The Setbacks

While the future of CCUS looks promising, some challenges are just around the corner.

The major hurdle is the lack of transport and storage capacity in deploying carbon capture projects. One solution to this challenge is commercialization as what some national governments and companies are promoting.

Yet, the high costs in constructing storage are not acknowledged by policies such as the EU’s Net Zero Industry Act.

In the US, permits for transport and storage were denied. Recently, the Environmental Protection Agency (EPA) called on states to have their own regulatory frameworks for CCUS. This followed when policymakers questioned the agency’s limited permit issuances.

In the private sector, oil majors aiming to be first movers in advancing carbon capture and storage turn to mergers and acquisitions. For instance, ExxonMobil acquired Denbury, a small-scale oil business running an extensive CO2 pipeline transport network across the Gulf Coast.

Remarkably, the BNEF highlights that DAC is far more costly than previously thought. This carbon capture technology costs up to $1,100 per ton but can potentially drop to $400/ton by 2030. This decrease would be possible if the industry can develop enough supply chains to scale the technology.

The cost of capturing carbon differs across industries. In facilities where CO2 concentration is high, the cost ranges from $20-$28 per ton while for industrial sources, it can go up to $80 a ton of CO2.

Total costs for CCUS can increase to $92-$130 per ton of CO2, and it can swell 2-4x more for transporting liquid CO2.

Industries like cement, iron and steel, and power, which emit a lot of CO2, are using carbon capture methods more. This is driven by the incentives provided by the government in the US and EU, making CCUS more practical.

For instance, building new gas power plants with carbon capture may be less expensive than making power without capturing carbon in Germany by 2024, especially when factoring in carbon price.

The CCUS industry is experiencing rapid growth and diversification across sectors due to strong global policy support. Although promising, challenges such as transport and storage capacity constraints, high construction costs, and regulatory hurdles pose significant barriers. Addressing these challenges will be crucial for CCUS to play a substantial role in global emissions reduction.

With the worsening impacts of climate change, countries around the world are up to their heels to find solutions that can significantly reduce carbon emissions.

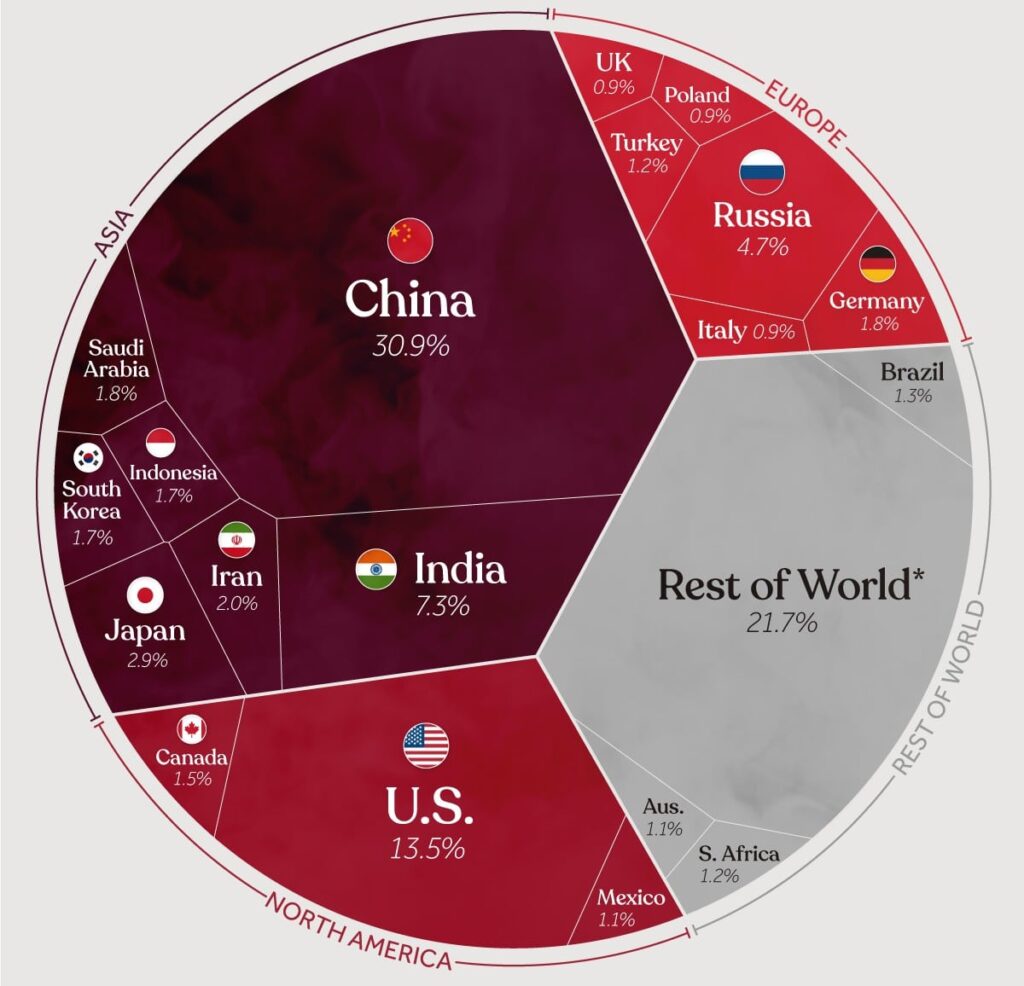

The top three major emitters – China, United States, and India – are responsible for emitting over 50% of global carbon emissions.

How Much CO2 Does Each Country Emit?

Burning too much fossil fuels intensifies the greenhouse effect, which is essential for keeping the Earth’s temperature suitable for life. This change is causing major shifts in the planet’s climate system that also led to worsening natural disasters.

As this year’s UN climate summit, COP28, is approaching, it’s important to know how much each country contributes to global carbon footprint. The COP28 in Dubai also represents a great opportunity to assess the progress of countries toward achieving their climate goals.

As per the Global Carbon Atlas data, interpreted by Visual Capitalist, 52% of the world’s carbon dioxide emissions in 2021 was caused only by three countries: China, U.S. and India. Apart from contributing the most to global emissions, they also have the highest number of population.

Source: Visual Capitalist

As shown above, China is the top carbon polluter (almost 31%) compared to the rest of the world (around 22%).

When it comes to carbon emissions per capita, the US tops the rank with around 15 (metric tons). China comes second with 7 Mt CO2 per capita while India has only around 2 Mt CO2.

All these three top carbon emitters have pledged to cut their footprint and reach net zero emissions. But they don’t share the same net zero target.

China targets to achieve net zero by 2060 while India plans to reach it ten years later, by 2070. Only the US’ net zero target is in line with the Paris Agreement objective of hitting net zero by 2050.

According to a World Bank Group Report, China needs as much as $17 trillion in investments to meet its net zero targets and transition to a low-carbon economy. This particularly involves investments in the power and transport sectors for green technologies and infrastructure.

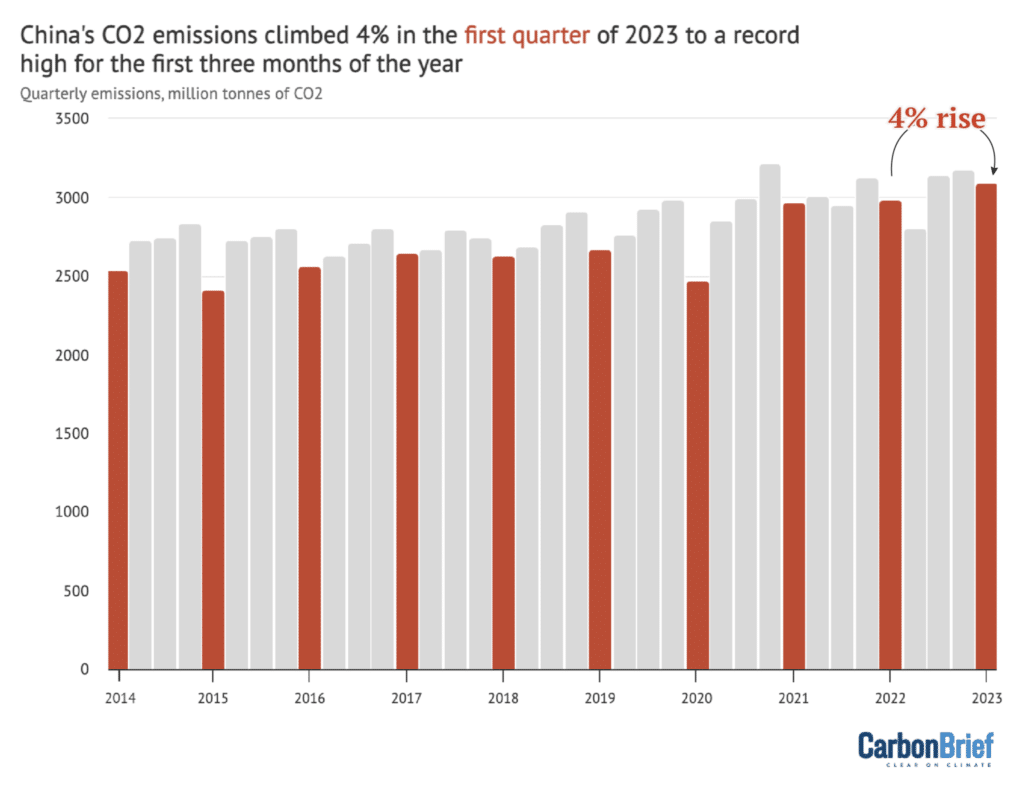

As the biggest emitter focuses on economic growth, its carbon footprint will most likely hit an all-time high in 2023. Its CO2 emissions increased 4% in the Q1 this year, hitting a record high, according to the Carbon Brief report.

Meanwhile, the US has seen a significant increase in clean energy investments, showing its commitment to decarbonization. The country has been pouring billions of dollars into clean technologies and infrastructure to lower its carbon footprint.

According to the Clean Investment Monitor database, clean energy is becoming one of the biggest industries in the U.S. In 2022, investments made in the sector reached a total of $213 billion.

Unlike China, India aims to hit net zero by 2070. To reach this, the third emitter will focus on the use of electric vehicles and achieve 3x more nuclear capacity by 2032.

However, as India becomes more developed, its carbon emissions may also continue to grow more. According to the International Energy Agency (IEA), its share of global emissions would go up to 10% by 2030.

How Much Renewables Must Be Achieved by 2030?

The IEA also projected that to reach global net zero target, renewable energy capacity installed must be 3x more the current level by the decade’s end.

As per the agency’s updated Net Zero Roadmap, renewables capacity should be at 11,000 GW by 2030. Reaching that capacity will achieve the largest emissions reductions.

The major polluters have also set ambitious targets for increasing their renewables by 2030, focusing on solar and wind power generation. The UK and the EU also have done the same.

Unfortunately, reports show that most of the countries are facing major hurdles to achieve their annual capacity targets.

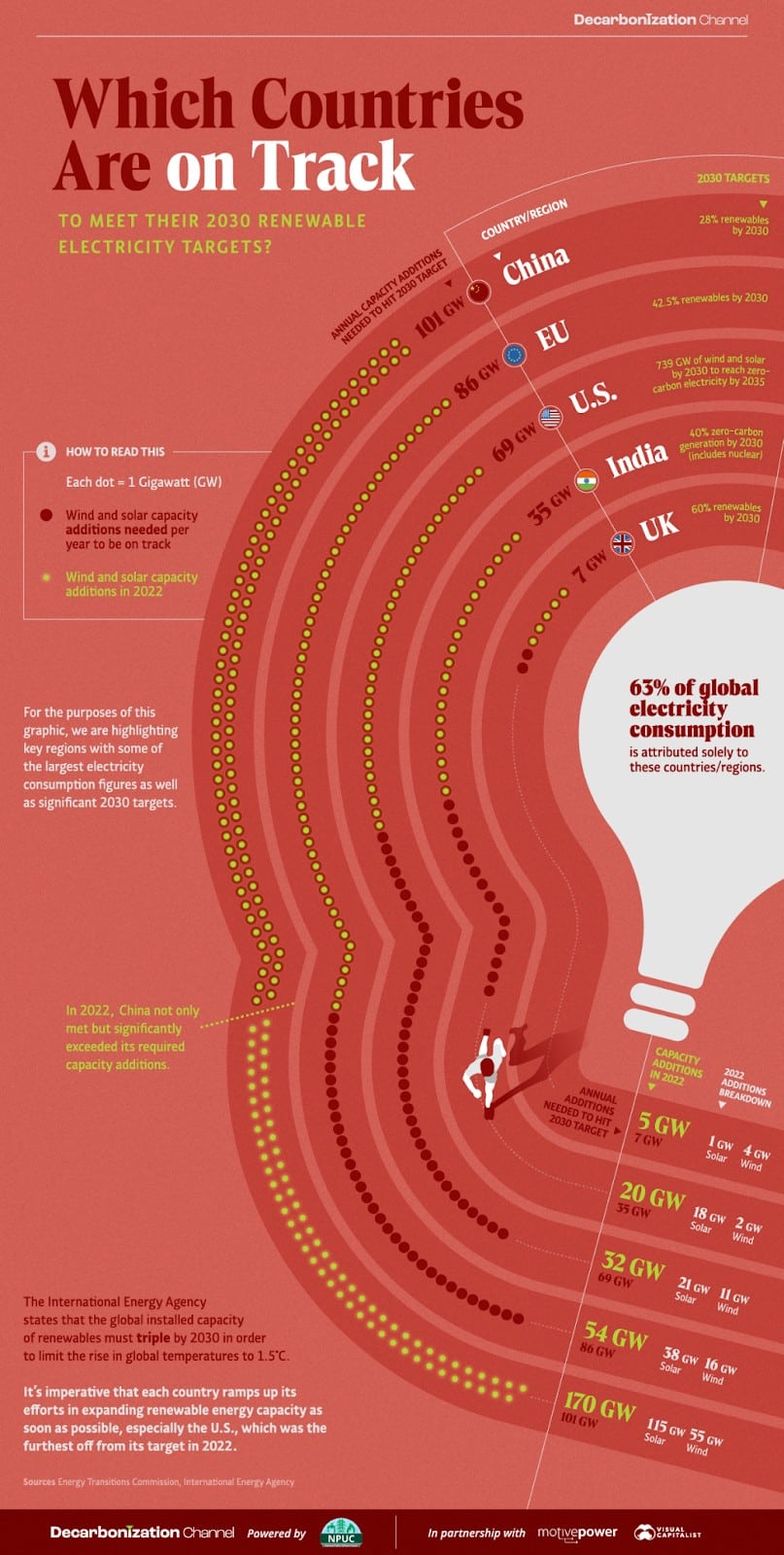

Data from Visual Capitalist illustrates how each of the nations are progressing towards their 2030 renewables targets. The chart also shows how much they performed in 2022.

Of the major carbon emission contributors, China is the only country on track to achieving its 2030 renewables goal. In fact, the top CO2 polluter exceeded its required renewable capacity for new installations, adding 168% more (101 GW).

In contrast, the US and India were the furthest off the track from reaching their 2022 targets. They were able to add only 46% and 57% of what is required, respectively. Other countries in Europe successfully made some progress but still have to add more installations to hit their 2030 goals.

Together, China, US, India, EU, and the UK accounted for >60% of the world’s total electricity consumption. This underlines their big responsibility in decarbonizing the power sector.

As the global community grapples with the escalating impacts of climate change, attention turns to the top carbon emitters. The challenge extends beyond emissions, with hurdles evident in meeting renewable energy goals by 2030, emphasizing the critical role these major emitters play in the urgent shift toward greener and more sustainable practices.

After a record-breaking year of devastating effects of climate change, from record wildfires in Greece and Canada to floods in Libya, the United Nations COP28 conference comes at a decisive moment for international climate action to put us on a safer path.

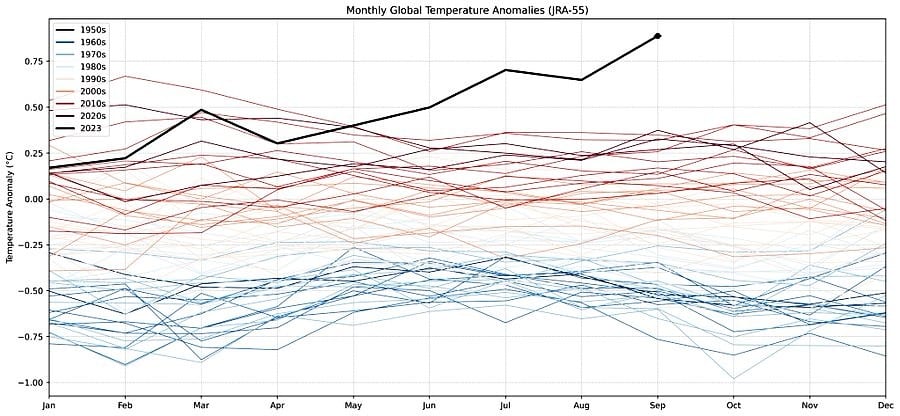

Temperature records are being beaten and climate effects are felt worldwide. As climate scientist Zeke Hausfather described global temperature data for September, it’s “absolutely gobsmackingly bananas”.

Source: Zeke Hausfather

As seen in Hausfather’s chart, last month’s temperature beat the prior monthly record by over 0.5°C, and was around 1.8°C warmer than pre-industrial levels.

So, what is the world doing about it? How do national governments tackle the climate crisis? The UN COP28 summit will show humanity’s progress in meeting the climate goals first set at the landmark Paris Agreement. Representatives from around 200 countries will come together to talk about it and agree on crucial climate actions.

In case you’ve never heard of COP28 or you most likely have if you’re following the climate change conversation but need a fresher, this comprehensive article will tell you the things you need to know about this defining climate summit.

First, let’s talk about the COP.

What is COP?

The Conference of the Parties to the Convention or COP is the product of the Rio Summit and the launch of the United Nations Framework Convention on Climate Change (UNFCCC).

Every year since the creation of the COP, member countries meet to agree how to deal with climate change. Tens of thousands of delegates from around the world gather together at the climate conference. Head of states, government officials, and representatives from international organizations, private sector, civil society, nonprofits, and the media are attending.

The COP’s 21st session led to the birth of the Paris Agreement, a global consensus to collectively achieve three important goals:

Limit global temperature rise to 1.5°C above pre-industrial levels by 2100,

Act upon climate change, adapt to its impact, and develop resilience, and

Align financing with a “pathway towards low greenhouse gas emissions and climate-resilient development”.

Here’s the COP in a timeline, alongside global carbon emissions record.

This year’s UN climate convention is the 28th session of the parties or simply COP28.

How Important is COP28?

So what makes this COP session significant and different from the previous climate talks? The Global Stocktake.

The GST is the first ever report card on the world’s climate progress. It shows exactly how far we are in achieving the Paris Agreement goals set in 2015. Are we on or off track?

Though the details won’t be in until COP28 takes place in November 30 – December 12 in Dubai, United Arab Emirates (UAE), there’s a hunch that we need rapid climate actions and have to act now. COP28 is our chance to do that.

Plus the fact that UAE is a major oil producing country makes COP28 quite different and controversial. Many are raising concerns that the agenda doesn’t match well with the host country’s plan to increase oil production.

Some environmental groups noted that it could result in weak results leading to a point where curbing fossil fuels has to be ratcheted up rapidly to make the 1.5°C achievable. Their point is valid. About 100+ years ago, there was far less carbon released into the atmosphere than there is today.

The designation of Sultan al-Jaber as COP28 president-designate incited a furious backlash from climate activists and civil society groups. They warned that there could be a conflict of interest and that protesters would be restricted.

Dr. Sultan al-Jaber is a managing director and CEO of the Abu Dhabi National Oil Company (ADNOC). As appointed president, he would lead the talks, consult with stakeholders, provide leadership roles, and broker any agreements produced.

Given his position within the fossil fuel industry, it raised concerns about impartiality in the climate talks.

But putting aside these controversies, it’s more important to know what would be the specific talking points for this year’s climate summit.

What Are the Focus Issues to Watch at COP28?

Similar to previous sessions, the host nation sets the tone and direction of discussion for the conference. For this year’s COP28, here are the major areas to be deliberated.

Money Matters

As the case with the rest of the COPs, climate finance is one of the key issues. More so, if the money involved is worth $100 billion annually which was pledged by developed nations to developing countries.

Climate finance is critical because developing nations need resources, financial and technological, to enable them to adapt to climate change.

It was back in 2009 when rich countries promised to provide $100 billion from 2020 onwards to help poor nations in dealing with the impacts of climate change. However, until now that pledge has never been met, stirring frustrations for many developing countries.

The potential consequences of failing to meet the promised target in a timely manner could extend to the broader negotiations. It heavily affects the trustworthiness of governments to fulfill their commitments.

At COP28, governments will persist in their discussions on a fresh climate finance objective, aiming to supplant the existing $100 billion commitment. Though the deadline for reaching an agreement is 2024, substantial progress in Dubai remains pivotal to establishing a foundation for next year’s COP.

Moreover, financial matters will prominently feature in talks on the Green Climate Fund and on loss and damage.

Ultimately, deliberations and pledges related to the amplification and execution of climate finance may impact various other areas of negotiation. It may also help propel more climate actions or impede progress.

Where’s the ‘Loss and Damage’ Fund?

The concept of ‘loss and damage’ compensation isn’t new; it has been around for some time. It’s an arrangement wherein rich nations should pay the poorer ones that have suffered the brunt of climate change.

It differs from the funds to help poor nations adapt to the effects of climate change. While it gives hope for low-income countries heavily impacted by the climate-related disasters, it left several unanswered questions.

Unsurprisingly, one big question is:

Who’s going to pay into the fund and who deserves to get it?

This issue has been unresolved for some time and was also discussed in COP27 at Egypt last year. Different organizations have different suggestions as to how much the fund needed to pay for the loss and damage.

For one study, the funding can be as high as $580 billion each year by 2030, going up to $1.7 trillion by 2050.

Matter experts noted that the fund has been the “underlying climate finance discussions for a long time”. But after years of stalemate, the question hasn’t been resolved still.

Governments decided and agreed to form a ‘transitional committee’ at COP27. At COP28, they expect to come up with the recommendations on how to operationalize the fund.

Leading up to COP28, there’s been growing attention on food systems and agriculture in global discussions.

The current food systems are failing us; over 800 million people face hunger right now. Climate-related droughts and floods are destroying farmers’ crops and livelihoods. At COP28, world leaders must devise a plan that changes the ways the world produces and consumes food.

The COP28 presidency and the UN Food Systems Coordination Hub launched the COP28 Food Systems and Agriculture Agenda in July. It urges nations to align their national food systems and agricultural policies with their climate plans.

The agenda emphasizes the inclusion of targets for food system decarbonization in national biodiversity strategies and action plans.

Like the other issues above, food systems were also part of the COP27 summit. But there was also still some resistance to fully adopting a holistic approach to them.

Sultan al-Jaber is encouraging both private and public sectors to contribute funds and technology to transform food systems and agriculture. He also emphasized that food systems contribute to a significant portion of human-generated emissions. In line with this, the UAE and the US team up to promote their Agriculture Innovation Mission for Climate (AIM4C).

The increased focus on food at COP28 has been well-received. The GST synthesis report even stresses the need to address interconnected challenges, including demand-side measures, land use changes, and deforestation.

It’s important that actions to change food systems work together with efforts to speed up the transition to cleaner energy. Transformations in both sectors are crucial to meeting climate goals.

Moving Cities At the Front

For many years, UN climate summits have historically concentrated solely on national-level climate action, overlooking a crucial aspect.

Urban centers, responsible for around 70% of global CO2 emissions, face heightened vulnerability to climate change impacts, too. To restrict warming to 1.5C, all cities must achieve net zero emissions by 2050.

Research indicates that existing technologies and policies can cut urban emissions by 90% by 2050. But cities alone can realize only 28% of this potential.

Full decarbonization requires robust partnerships between local and national governments, along with engagement in international climate initiatives.

At COP28, it’s crucial for national, regional, and local governments to intensify partnerships, accelerating progress toward climate goals.

Moreover, national governments should also integrate urban areas more effectively into their climate plans. This includes reinforcing city-centric targets in their NDCs and National Adaptation Plans, expanding public transit, enhancing building energy efficiency, and ensuring that subnational actors have easy access to climate finance.

COP28: The Deciding Moment for Climate Action

Leaders at the national, corporate, and municipal levels must not only showcase progress in fulfilling previous commitments but also unveil new, ambitious plans. These plans are vital to curbing the worsening impacts of climate change, safeguarding both people and the environment.

The Global Stocktake was established to reach the objectives of the Paris Agreement. It also particularly highlighted the need to phase out unabated fossil fuels, which are the major culprit in releasing carbon. It will face its inaugural evaluation at COP28, presenting a crucial assessment of decision-makers’ commitment to its goal.

The report card of the world’s collective climate action was out. And the data isn’t good. COP28 is our best chance to make a critical course correction. It isn’t just a conference; it’s a decisive moment for leaders to demonstrate commitment to curbing harmful emissions.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy

New Jersey: Active trading occurred for both 2023 and 2024 vintage solar credits, with trades surpassing 1,000 credits at $209 and $222, respectively, before closing at $220.75 due to falling offers.

New Jersey: Active trading occurred for both 2023 and 2024 vintage solar credits, with trades surpassing 1,000 credits at $209 and $222, respectively, before closing at $220.75 due to falling offers.

Meanwhile, the US has seen a significant increase in

Meanwhile, the US has seen a significant increase in