Apple had doubled its investment up to $200 million to expand its Restore Fund, also doubling the tech giant’s commitment to promoting carbon removal.

The project, which is between Apple and partners including Conservation International, is funding nature-based carbon removal projects.

What is Apple’s Restore Fund?

Apple’s Restore Fund was launched in 2021 with an initial commitment worth $200 million from the company and its partners, Conservation International and Goldman Sachs.

It was part of Apple’s roadmap to be net zero for its entire supply chain and life cycle of every product by 2030. To achieve that, the company aims to lower all emissions by 75% by the same period and offset any remaining emissions with high-quality carbon removal credits.

The world’s largest tech company created the Fund to encourage investments into protecting and restoring critical ecosystems and scale nature-based carbon removal solutions. Through high-quality carbon credits the projects generate, help businesses deal with their residual emissions that they can’t yet reduce or avoid.

In addition to the initial $200 million, Apple will invest another $200 million in the Fund to expand it. Climate Asset Management, a joint venture of Pollination and HSBC Asset Management, will manage the new investment portfolio.

The new portfolio is also looking to remove 1 million metric tons of CO2 per year while aiming to generate a financial return for investors.

For company suppliers-turned-partners in the fund, the portfolio will give them the means to decarbonize through high-impact carbon removal projects.

Commenting on the announcement, VP of Environment, Policy, and Social Initiatives, Lisa Jackson noted that:

“The Restore Fund is an innovative investment approach that generates real, measurable benefits for the planet, while aiming to generate a financial return… The path to a carbon neutral economy requires deep decarbonization paired with responsible carbon removal, and innovation like this can help accelerate the pace of progress.”

Apple and its partners are partnering with forestry managers for sustainable forest management for optimal carbon and timber production. Their work creates not just revenue from the timber but also from high-quality carbon credits.

With the additional $200 million, the Restore Fund is set to grow with a new portfolio of carbon removal projects.

Advancing a New and Unique Model for Carbon Removal

Carbon removal is vital to mitigating climate change and reaching global climate goals, as highlighted by the scientific body, IPCC.

Apple and Climate Asset Management are taking a unique approach to prospect projects, pooling two different types of investments:

nature-forward agricultural projects that yield revenue from sustainably managed farming practices, and

projects that restore critical ecosystems that remove and store CO2.

The goal of this unique blended fund structure is to achieve both financial and climate benefits for investors. All the while promoting a new model for carbon removal that addresses the potential for nature-based solutions.

All investments in the Restore Fund are subject to stringent social and environmental standards.

Carbon Removal Investments for Apple’s Climate Goal

Apple has already achieved carbon neutrality for its corporate operations last year. But the leading tech also called on its suppliers to do the same across its operations by 2030. And that includes both their Scope 1 (direct emissions) and Scope 2 (electricity-related) emissions.

Achieving its ambitious climate goal is possible by offsetting Apple’s unavoidable emissions with high-quality carbon removal credits.

Suppliers can cut their emissions by abating direct carbon footprint, improving energy efficiency, and shifting to using renewable energy. As progress of this advocacy, Apple revealed that 250+ of its manufacturing partners also pledged to use 100% renewable energy to power their production by 2030.

The previous investments that the tech firm committed along with Conservation International and Goldman Sachs were in Brazil and Paraguay. Example of a Restore Fund project in Paraguay shown below involves a sustainably managed timber farm on one side of the road, and a preserved natural forest on the other side.

Source: Apple website

These carbon reduction projects will restore 150,000 acres of sustainably certified forests and protect another 100,000 acres of native forests, grasslands, and wetlands. They aim to remove 1 million Mt of CO2 from the atmosphere each year by 2025.

Monitoring Investments Impact

For accurate measurements and monitoring of the Restore Fund projects’ impact, Apple is using advanced remote sensing technologies. These include the Upstream Tech’s Lens platform, Maxar’s satellite imagery, and Space Intelligence’s Carbon and Habitat Mapper. Together, they help the company create forest carbon maps of the project areas.

Apple also explores using LiDAR Scanner on iPhone to further improve monitoring capabilities on the ground.

The detailed maps those tech produce will help ensure that projects meet Apple’s high standards before investments are made. They’re also important to quantify and verify the carbon removal impact of the projects over time.

Amsterdam-based STX Group raises 150 million Euros from environmental commodities, marking the first time the banking sector backs this innovative credit facility vital for the energy transition.

Who’s The STX Group?

The STX Group is a leading global environmental commodity trader and climate solutions provider. The group is based in Amsterdam, Netherlands, with ten offices globally. It has an annual trading volume of over €4 billion.

The global trading company offers a wide range of innovative solutions to help businesses and organizations in their transition. It has a track record in pricing carbon emissions, creating trust in providing market-based carbon reduction solutions.

After acquiring Vertis and Strive in December 2021, the trader now has a diverse team of about 500 employees from 50+ countries.

STX ensures that money flows to thousands of projects that help the world transition to a low-carbon economy with its trading and Corporate Climate Solutions offerings. It provides access to a wide range of products and solutions to reduce carbon emissions such as:

The firm also gives corporations certificates as proof of their efforts in making the planet greener. Customers can choose verified emission reductions (VERs) or voluntary carbon credits from thousands of projects worldwide, with these technologies:

Afforestation

Reforestation

Cookstove

Biomass Cogeneration

Wind Power

Hydro Power

Energy Efficiency

Solar Power

Recycling

Biogas

Biodigesters

The company provides carbon offset solutions with labels from the VCS (Verified Carbon Standard), the CDM (Clean Development Mechanism), Gold Standard, the Climate, Community & Biodiversity (CCB), and the REDD+ Business Initiative.

STX €150 Million Credit Facility

STX credit facility is considered oversubscribed, featuring the unique quality of having a partial security from a diverse portfolio of environmental commodities.

Remarking on the announcement, STX’s Chief Financial & Risk Officer, Bart Wesselink said that:

“With the energy transition in the heart of STX, we have been in the business of decarbonization for a long time, and are therefore pleased to see a group of mainstream global banks finally recognizing the underlying value of the wider range of environmental commodities.”

The group expects that this facility will fuel the rapid expansion of its business operations, particularly its borrowing power. Half of the €150 million funding (€75m) is a committed portion while the other half has an uncommitted accordion feature.

The facility is supported by a syndicate of globally renowned banks, leaders in the field of commodities trade financing. The company, however, didn’t name them.

Historical Support from the Banking Sector

The fundraising by STX marks the first time that the banking system supports this kind of financing facility.

Wesselink added that the banks’ willingness to take part in their credit facility is a pivotal step for the industry. It provides more “access to financing and promotes a level playing field” for those who wish to contribute to the energy transition.

Just last year, major banks were criticized for neglecting shareholders’ plea to put an end to fossil fuel financing. They prefer to continue supporting “dirty” projects that burn fossils than advance their climate goals.

But there are a few that made a braver move to stop direct funding of fossil fuels like Lloyds Bank. They set the trend towards sustainable banking.

By the end of 2022, climate commitment from four major banks reached a total of $5.5 trillion. They include HSBC, Barclays, JPMorgan Chase, and Citigroup.

According to STX CFO, the financiers used to accept biofuels and financial instruments such as the EU carbon credits (EU Emission Allowances, a.k.a. EUA) as collateral for borrowed funds.

But under STX new credit facility, it’s the first time that the banking sector accepts other environmental commodities like Guarantees of Origin and Renewable Gas Certificates as collateral. It seems that the banking community is also picking up the pace of the global phenomenon of energy transition.

Investors were used to looking for companies to cut only their operational emissions and indirect emissions from energy purchases. But now they’re focusing on the entire business supply chain, meaning Scope 3 emissions are becoming more significant.

This trend puts emissions from the value chain at the spotlight. But why is it important to account for this type of carbon emissions and why its disclosure is a must?

This article will explain everything you need to know about Scope 3 emissions and the importance of disclosing and accounting for them.

The Importance of Evaluating Scope 3 Emissions

Scope 3 emissions, which include indirect emissions from a company’s value chain, often represent the largest portion of corporate-related emissions. But companies often neglect to disclose these emissions or simply mention them without enough details.

The lack of transparency leaves investors in the dark when assessing the real climate risk exposure of their portfolios.

Good news for investors in the US, the EU, and New Zealand. Regulators in these countries proposed a mandatory Scope 3 emissions reporting for listed companies.

Even the central banks are feeling the weight of this matter as they’re starting to take climate exposure into consideration.

This growing awareness and increasing regulatory interest will likely lead to more Scope 3-related policies in the coming years.

Accounting for Scope 3 emissions is very flexible as they tend to be self-imposed. Yet, it’s still difficult to compare data across companies because of the varying emissions profiles even within sectors.

Unfortunately for investors, companies often omit significant Scope 3 categories without providing transparent reasons for doing so. This is why stricter rules on disclosure are coming up, prompting large companies to start accounting for value chain emissions.

Investors can use value chain emissions as an indicator of transition risk and gauge a company’s true climate ambition.

After all, assessing exposure to carbon-intensive activities in value chains and products is critical for investors. It can help them expect any potential impacts on asset values and operating costs.

So, it’s just reasonable for investors to demand more comprehensive and transparent Scope 3 disclosures and scrutinize them more closely. Doing so will help them better understand overall climate risk and identify potential greenwashing.

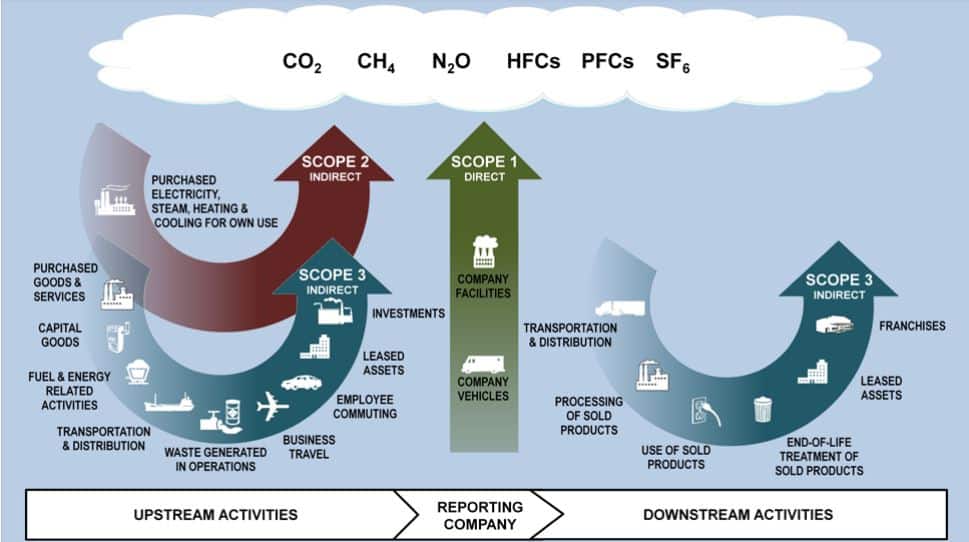

Scope 3 Emissions and the Greenhouse Gas Protocol

Scope 3 emissions, as defined by the Greenhouse Gas Protocol (GHG Protocol), cover all indirect emissions from a company’s value chain that are not owned or controlled by the company itself. These emissions extend beyond the direct operations (Scope 1) and purchased energy (Scope 2) emissions of a company.

The GHG Protocol is a collaboration between the World Resources Institute and the World Business Council for Sustainable Development. It sets global greenhouse gas accounting and reporting standards, such as The GHG Protocol Corporate Accounting and Reporting Standard and The Corporate Value Chain (Scope 3) Standard. These standards are widely adopted by corporations and regulators.

In 2016, 92% of Fortune 500 companies responding to the CDP climate questionnaire used GHG Protocol standards either directly or indirectly.

The GHG Protocol breaks down Scope 3 emissions into 15 distinct categories, covering both upstream and downstream activities.

Source: GHG Protocol

Companies determine their own Scope 3 boundaries and report based on the categories’ relevance and materiality to their business. This can result in varying emissions profiles even among companies in the same sector.

The differences in emissions profiles present a significant challenge in addressing this type of emissions. For instance, Alphabet considers emissions from downstream leased assets as “not relevant,” while Microsoft includes them in its emissions disclosure, despite their similar business nature.

In essence, it still depends on a company how it would regard a specific category. It’s up to them if the emission is material or not and relevant or irrelevant. In this case, providing enough disclosure details on emissions sources becomes even more important.

The Need for Improved Disclosure

Scope 3 emissions often represent the majority of corporate GHG emissions.

For example, oil companies’ Scope 1 and 2 emissions are a small fraction of their total emissions, while the consumption and combustion of their products account for most emissions.

In fact, CDP estimates that Scope 3 emissions make up 75% of related GHG emissions across all sectors. In the financial sector, financed emissions can be over 700 times greater than operational emissions.

Undeniably, emissions from the value chains have substantial impact but they are underreported or ignored most of the time. Large polluters simply claim that they have “no influence or control” over them. It is, thus, not surprising that Scope 3 emissions have lower disclosure rates than the other two emissions types.

Big companies like those included in the S&P Global 1200 index face more pressure to disclose their sustainability performance. Despite this, the overall Scope 3 disclosure rate across the wider market is likely much lower.

Add to that the fact that many businesses don’t provide a detailed breakdown of their value chain emissions, preventing investors from understanding the full extent of climate risk exposure along value chains.

The number of reported categories may offer some insight into the completeness of corporate disclosure. But there is still significant room for improvement in both the quantity and quality of Scope 3 disclosures.

Improved reporting will enable investors to better identify sources of emissions and potential solutions, ultimately contributing to a more accurate assessment of climate risks.

Why Net Zero Targets must Include, not Ignore Scope 3

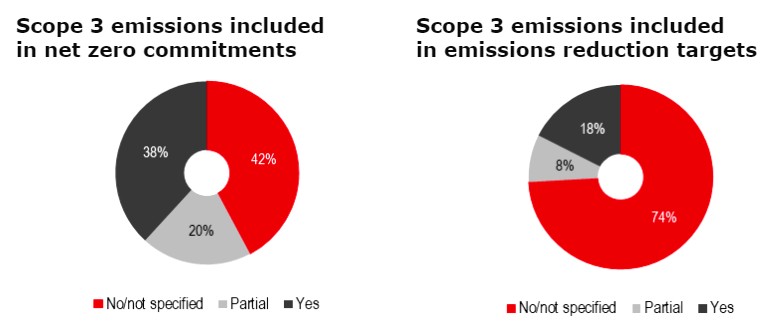

As the momentum for net zero commitments grows at both the national and corporate levels, many companies still fail to address Scope 3 emissions in their climate pledges.

Over 40% of corporate net zero targets do not cover Scope 3 emissions, even if they often represent the largest share of GHG emissions. Only 18% of companies in Net Zero Tracker’s survey of 2000 large, publicly-traded companies have set Scope 3 reduction targets.

Source: Net Zero Tracker 2022, HSBC

The Science Based Target Initiative requires a Scope 3 target if a company’s relevant Scope 3 emissions are 40% or more of related GHG emissions. This is to ensure that corporate emission reduction targets are in line with the latest climate science.

Neglecting Scope 3 emissions in climate commitments not only weakens the overall climate strategy but also raises concerns about greenwashing.

For instance, Exxon Mobil faced criticism for its net zero announcement in January 2022, which included Scope 1 and 2 emissions while excluding Scope 3 emissions.

Similarly, Brazilian meatpacker JBS reported flat emissions over 5 years. But the Institute for Agriculture and Trade Policy disagreed, saying that JBS’ emissions actually increased by 51% during that period. The NGO claimed that JBS ignored its supply chain emissions in its disclosures and commitments, thereby guilty of greenwashing.

Considering the huge impact of these emissions, it is crucial for companies to include them in their net zero targets to effectively address climate risks and avoid greenwashing.

Not to mention the potential legal consequences they may face considering climate policies’ growing focus on value chain emissions.

Including Scope 3 Emissions in Climate Policies

Regulators are increasingly focusing on Scope 3 emissions, with some markets already implementing mandatory disclosure requirements:

US: The SEC requires publicly listed companies to disclose Scope 3 emissions if material or included in their GHG reduction goals. US funds will have to report the GHG footprint of their portfolios.

EU: The EBA plans to require banks to disclose financed Scope 3 emissions starting July 2024. The European Commission proposes all large and listed companies to report in compliance with the European Sustainability Reporting Standards (ESRS), which require Scope 3 emissions disclosure.

New Zealand: The External Reporting Board proposed mandatory Scope 3 disclosure, emphasizing the need to cover the entire value chain.

Singapore: Singapore Exchange requires listed companies to report Scope 1, 2, and 3 emissions when appropriate.

The Disclosure Club and Climate Litigation

More jurisdictions will join the “mandatory disclosure club,” especially as the International Sustainability Standards Board (ISSB) includes Scope 3 emissions in its draft climate-related disclosure requirements. The official standards, expected by the end of 2022, could catalyze wider adoption of reporting standards and policy requirements for Scope 3 emissions.

Moreover, climate stress tests by central banks now include value chain emissions as a climate risk metric. Examples are the European Central Bank (ECB) and the People’s Bank of China (PBoC). Banks with high exposure to climate risks may face higher capital reserve requirements.

Climate change-related litigation is also on the rise, with some cases focusing on Scope 3 emissions. They have been brought into the courts, such as the case with Royal Dutch Shell. The court obliged Shell to reduce emissions relating to its entire energy portfolio, including value chain emissions.

The case makes it even more important for investors to be aware of the legal risks associated with value chain emissions and their significance in climate risk assessments.

Carbon pricing mechanisms rarely apply to Scope 3 emissions; but they can impact the costs of companies with high value chain emissions, such as those in the real estate sector.

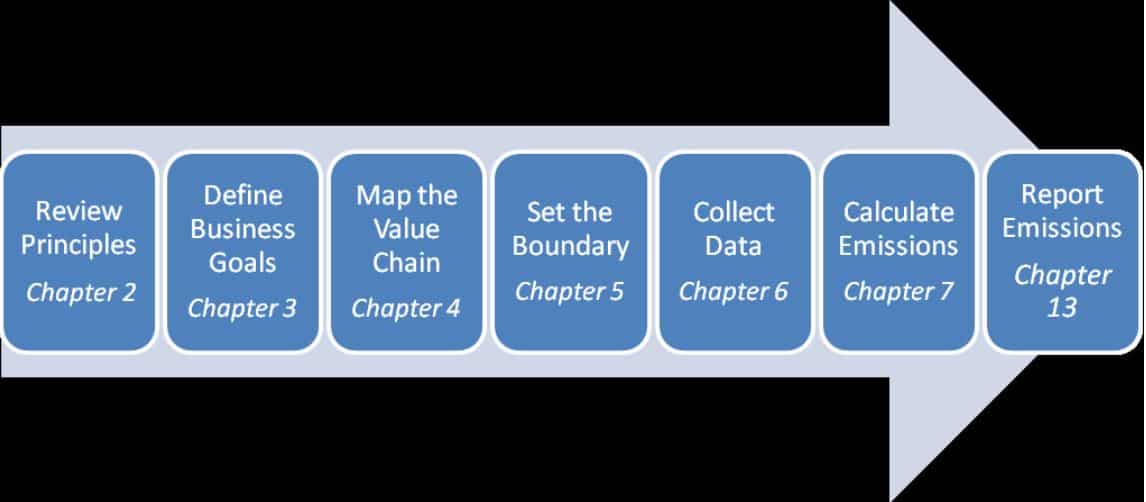

Accounting for Scope 3 Emissions

Accounting for Scope 3 emissions becomes even more challenging due to the discretion allowed in selecting relevant categories, data availability, and sector applicability. But understanding of Scope 3 emissions is growing, and a more nuanced approach to disclosures will soon evolve.

Despite the more challenging accounting for value chain emissions, it shares the same principles as Scope 1 and 2 emissions. The major difference is the identification of relevant activities and boundary setting.

In general, here’s the overview of the steps involved according to GHG Protocol:

Overview of Steps in Scope 3 Accounting & Reporting

Key points when accounting for emissions from value chain:

Flexibility in selecting relevant categories can make calculations, analysis, and comparisons challenging. Companies may exclude categories that are actually material to their business.

Timing of emissions adds complexity to Scope 3 accounting, as some emissions occur in the current year, while others may have occurred in the past or are yet to occur.

Double counting may occur as Scope 1 and 2 emissions for one company can be Scope 3 emissions for another. Aggregating Scope 3 emissions across companies or subsidiaries should be avoided.

Scope 3 emissions are more relevant to some sectors than others, and disclosure rates can provide an indication of relevance.

Overall, instead of aggregating across several companies, investors and companies should focus on analyzing Scope 3 emissions at an individual company level to determine exposure. This approach will offer a more complete picture of a business’s overall exposure to potential climate risks and impacts.

A London-based carbon procurement and market intelligence tech firm, Abatable, secured $13.5 million in funding from Azora Capital and fully acquired a nature-based carbon credits provider, Ecosphere+.

Founded in 2016, Ecosphere+ seeks to create and build demand for high-impact voluntary carbon credits. The company’s portfolio strategies enable other businesses to take action and integrate carbon credits into their net zero plans.

Operating since 2003, Azora Capital is an investment management and private equity firm based in Spain. It has over €6.5 billion in assets under management (AUM). Azora’s European Climate Solutions private equity strategy supports and provides growth capital to companies that bring decarbonization solutions.

Remarking on the fundraising, Abatable CEO and Co-founder Valerio Magliulo said:

“We are thrilled to have the support of Azora as we accelerate our growth plans to support an increasing number of businesses taking climate action for their hard-to-abate emissions.”

Creating the Largest Tech-enabled Carbon Procurement Platform

Abatable’s carbon procurement platform allows entities to connect and transact with carbon project developers to deliver their ambitious climate goals. The firm’s mission is to help companies deal with their hard-to-abate carbon emissions in two ways:

Deliver long-lasting and measurable environmental and social impact beyond value chains

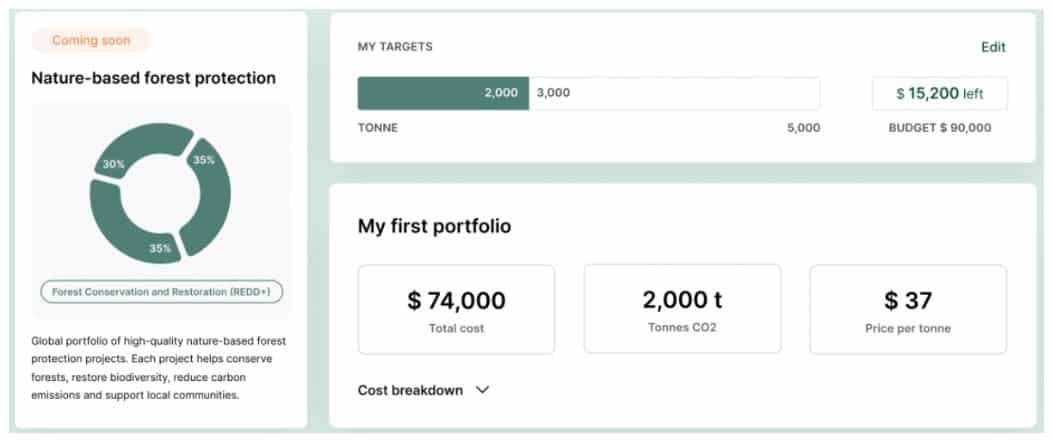

Carbon credit buyers can pick from a selection of pre-built thematic portfolios or create their own to align with climate goals. Here’s an example of a thematic portfolio in Abatable carbon credit marketplace:

Its tech platform helps bring transparency and efficiency to the voluntary carbon market (VCM). It also gives entities access to 2,000+ project developers across different project types and geographies while providing them effective ways to buy carbon credits.

By acquiring Ecosphere+, Abatable will be expanding its services to a wider reach of corporate clients. The company will also benefit from Ecosphere+’s proven track record and data, transacting over 45 million carbon credits.

Ecosphere+ is a provider of nature-based carbon credits with projects focusing on reforestation and reducing deforestation while supporting local communities. The company offers solutions that turn carbon markets into effective financing tools needed in the race to net zero.

Abatable said that they’re “excited to combine their [Ecosphere+] access and expertise with our digital solutions to establish the largest tech-enabled carbon procurement platform.”

For Ecosphere+, the new team up will further propel their joint reach and impact in scaling action for climate, nature and people.

Driving Climate Solutions at Critical Times

The $13.5 million investment from Azora is the second deployment coming from its European Climate Solutions private equity strategy. It specifically targets companies that provide decarbonization solutions for the European economy.

The deal comes at a critical time for the VCM that can help speed up its development through a trusted mechanism for climate solutions.

Here’s how Abatable platform works for corporates with complex carbon procurement needs in 7 steps.

Define procurement requirements

Identify matching carbon projects

Submit a Request for Proposal

Leverage Abatable’s quality insights

Construct the optimal portfolio

Use standardized procurement contracts

Communicate and monitor your impact

Boom and Busts

The VCM is at a critical point. There has been a boom in market size and interest from various organizations across industries. Projections show that the market will grow to reach $50 billion by 2030 and a 100% increase by 2050.

But the VCM also received serious busts about its integrity. There are valid concerns on the quality of nature-based carbon credits verified by major standards.

Meanwhile, the carbon markets need to scale to ensure that net zero is possible and the window of opportunity is closing. Abatable is working with businesses around the world across industries, supporting high-impact projects that produce high-quality carbon credits.

The company helps businesses source, vet, and structure their long-term carbon procurement programs. The goal is to help deliver measurable carbon reductions along with environmental and social impacts.

Apart from the Ecosphere+ acquisition, the funding from Azora will let Abatable reach out and support more entities achieve their net zero plans.

A capital transition company, Martello, launches first UK carbon credits with 32,000 hemp carbon credits, expecting them to trade at $40 per unit (£32.50).

What Does Martello do?

Martello enters the carbon credits market because it believes the market is broken and to challenge the US dominated $7.4 billion carbon market.

The founder of Martello, Jonny Mulligan, noted that:

“The carbon credits market has massive economic and climate potential, but today they are largely broken. This is why Martello is entering the market to challenge the status quo, bring transparency and assurance for Net Zero companies.”

The UK-based transition capital firm advises companies on the structure and fiduciary risks in the carbon credits market. Doing so is critical so that they know how those risks can impact their net zero strategy.

Martello is also developing and selling high-quality carbon credits that enables companies to offset their carbon emissions. The advisory firm also helps businesses know the trends that shape the global carbon market and the future carbon pricing.

More importantly, they help companies understand the limits of net zero and how they can develop credible plans and strategies.

Martello is working with the voluntary UK carbon code, the UKCCC, which validates the credits they issue. The firm focuses on triple returns:

Reducing carbon

Investing in biodiversity

Incentivizing farmers to adopt regenerative farming practices

Their goal is to achieve the targets of net zero, UN sustainable development goals, and the IPCC mitigation.

Addressing Opaque and Junk Credits

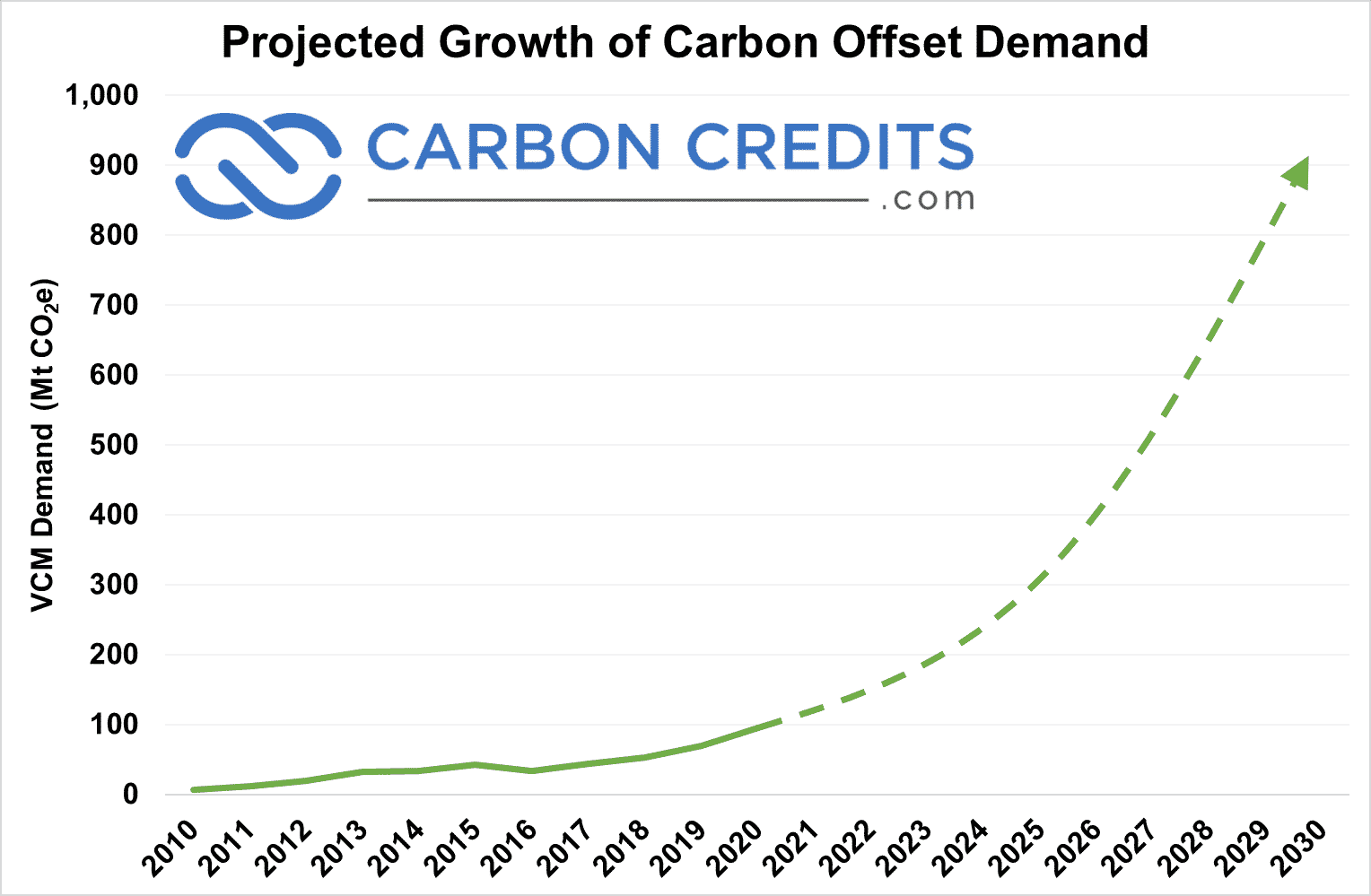

Since 2021 the voluntary carbon markets (VCMs), have increased in size by 74% with a value of $7.4 billion. Estimates further show the market would be worth over $50 billion in 2030, with a 100% increase by 2050. Demand for carbon offset credits continue to soar as seen in the chart.

According to Mulligan, carbon credits are an important tool to cut carbon and meet net zero at speed. Emitters rely on them for up to 80% of their carbon reduction by the end of this decade.

But Martello believes that the VCM is opaque, lacking innovation and transparency. Hence, the company decided to create its own carbon credits to address those concerns, particularly the junk credits that are poorly validated. These credits create problems for the companies with net zero pledges and investors avoiding greenwashing and climate or ESG litigation.

Recent issues in the market, especially with forest carbon credits, spur major concern in the sector. They affected the major non-profit carbon offsetting standards which are responsible for verifying over 70% of the credits.

Studies also show that as much as 85% of carbon reduction projects validated junk credits, causing huge concern for investors.

Mulligan noted that “with little warning, a carbon project promising millions could be worthless, leaving investors with no returns”. And so Martello joined the market and searched the global carbon markets to find the team to create the first global standard for hemp and validate the credits they create.

The company picked the Re-generation Earth because of the robust science and their insistence on data transparency across projects.

Hemp Carbon Credits

There has been a growing number of growers producing industrial hemp in Europe and in Canada.

Hemp grows very fast like a weed and was a cash crop for centuries. Its versatility and hardiness make it useful in making various biomaterials and resources. It can deliver products such as CBD oil, hempcrete for low-carbon building material, and protein powder for a vegan diet.

Compared to forests that can take years to root, industrial hemp has a much faster growing cycle. This prolific growth allows the plant to sequester a significant amount of CO2.

According to research, a hectare of hemp can absorb about 8 to 15 tonnes of CO2. In comparison, forests capture 2 to 6 tonnes only depending on the type of trees, region, etc.

In Canada, hemp also acts as an essential habitat in the country’s vast plains; it gives many birds and insects food and shelter.

Martello’s project focused on soil carbon sequestration by growing hemp in a regenerative agricultural system. This crop’s annual carbon sequestration into soils is the main reason to cultivate it.

Growing hemp crops also promotes sustainable land management, circular economy principles, and local food systems while reducing waste.

32,179 Regenerative Agriculture Hemp Carbon Credits available for bulk or smaller issuance

15,000tCo2 equivalent, validation UKCCC in the UK

Supports sustainable farming practices that enhance soil health, reduce emissions, and promote biodiversity in Canada

Hemp carbon credits increase land absorption of CO2

Pre-project estimate +60,0000 Actual project issuance

Verified carbon offset certificates

Focus on high assurance, meeting net zero fiduciary duty requirements, and transparency via blockchain smart contracts

Martello will host The Peripatetic Series on the global carbon credits markets in April and May 2023 to boost buying good credits and raise more awareness of greenwashing.

2022 has seen significant progress in the fight against climate change with the greening of the global economy intensifying and expanding, along with the search for renewable and sustainable materials like lignin.

The growing concerns of environmental pollution and the need to do away with fossil fuel resources have prompted more research on bio-based raw materials. And among the various options available, lignin stands out for some reasons, four reasons actually.

Lignin-based biomaterial is of high carbon content, low-cost, highly renewable, and sustainable. So, what is lignin exactly? What are its industrial applications or uses and what are the processes to make it?

Understanding and knowing its role in the world’s transition to a low-carbon economy is important. More so if you are running a business and are looking for a potential raw material that emits low carbon. Or perhaps you’re brainstorming a project that requires the use of lignin.

Either way, we’ll help you know better about this planet-saving material and why it will be the flagship for the low-carbon transition.

What is Lignin?

Deep within the cell walls of every tree lies a powerful substance called lignin.

Lignin is the second most abundant organic polymer on Earth and it’s also the largest natural source of aromatic monomers. It is what makes the plant’s structure firm and resistant to rotting.

This biomaterial makes up approximately 30% of the total composition of a wood. It also has a high carbon content of up to 60% and is present in all vascular plants.

Kraft lignin was discovered back in the 1940s but it has never been a hotter topic in the biomaterial industry than today. As governments and companies around the world focus their investments in reducing carbon emissions and supporting low-carbon economies, efficient production and use of lignin grab their attention.

Industry estimates forecast that the global lignin market will reach $1 billion by 2025.

Primarily, lignin has been produced as a by-product in pulp and paper factories like the case of the Kraft process. Of the millions of tons of lignin made each year, most of it is used as a low-cost fuel for generating power and heat.

And as the demand for renewable materials continues to increase, new commercial applications and technological improvements for lignin are underway.

In particular, wood pulping and other biorefinery industries extract about 50 – 70 million tonnes of lignin each year; still, only about 2% is used for industrial applications, which is pretty small.

But with the growing interests and funding pumped into biorefinery and extraction innovations, lignin application will only multiply. In fact, this biomaterial is now useful in a variety of industrial applications.

What are the Industrial Applications of Lignin?

Lignin, which basically has the same chemical components as their petroleum-based counterparts and is renewable, has various practical uses. That is because of the various advantages it provides, primarily that it reduces the carbon footprint of a product.

The biomaterial can even make a product better in some applications.

In general, here are the major applications for bio-based lignin:

Adhesives

Foam insulation

Dispersant (textile, pesticide, concrete admixture, and drywall industries)

Replacement of fossil-based polymers in making plastics

Asphalt binder

Bio-based carbon fiber

Now let’s consider some key examples of lignin applications by companies that have commercialized the use of this material.

Bio-based furniture board and plywood

Reducing the carbon footprint of plywood products is possible without compromising their technical performance.

For instance, Latvijas Finieris, a global producer of birch plywood that’s using the bio-based lignin as binder in making plywood was able to cut emissions by up to 49%. It uses lignin Lineo® by Stora Enso as plywood resins instead of phenol.

Another product manufacturer, Koskinen, started using lignin-based glue in producing furniture boards, calling its product Zero Furniture Board. The company is also using Stora Enso’s lignin-based binder NeoLigno®.

Bioplastics

Lignin is also very beneficial in making plastics, turning these not-so-eco-friendly materials into a more biodegradable product.

One company, Lignin Industries, converts lignin into a biodegradable polymer that can replace fossil-based plastics. They call it RENOL, which can be used as raw material together with the existing thermoplastics.

In particular, it is the top biomaterial option in three applications for bioplastics – films, infill, and injection-molded products.

The huge benefit of using a lignin-based polymer is that each kilogram (kg) of fossil-based plastic replaced saves 5 to 6 kg of carbon emissions.

So, if the world is producing over 380 million tons of plastic every year, applying lignin as the base polymer results in a whopping 1.9 to 2.3 billion tons of CO2 prevented from getting released. Or it can only be half of that figure, which is still an impressive progress for the plastic industry.

Bio-asphalt

With over 1 trillion metric tonnes of asphalt produced each year, greening this industry is a huge task. Asphalt is usually a mixture of 95% aggregates and 5% binder, which is bitumen.

Bitumen, which does occur naturally, is a very thick liquid form of crude oil. Used as a binder in asphalt, it’s a by-product of oil refining.

Replacing it with lignin-based bio-bitumen reduces the planet-warming emissions of asphalt. Lignin has been studied, tested, and showed positive results in this industrial application.

Stora Enso’s Lineo™ has been successfully used in several asphalt projects in Europe, including bike lanes and heavy load transportation roads. In these applications, the lignin-based binder replaces half of the bitumen.

Apart from the above uses of Lignin, the chemical industries also offer many possible uses for lignin. These include adhesives, coating, emulsifier, and polyols.

In addition, Stora Enso built a facility for €10 million to create bio-based carbon by turning lignin in trees into batteries.

As the global lignin culture is in the making, it will lead to making safer, carbon-neutral and cost-effective products that we use daily. So, what makes this biomaterial important and beneficial.

What are the Key Benefits of Lignin?

Most of the benefits of using lignin are mentioned in the applications above. In gist, here are the key advantages of using this biomaterial instead of its fossil-based counterpart:

Renewable material of natural origin

It doesn’t need any additional tree-cutting and it doesn’t generate waste as it is from the kraft pulp process

Can replace fossil-based materials across a wide range of applications, reducing significant emissions

Traceable origin, usually from sustainably managed forests

These benefits make lignin a desirable raw material for countless applications. And recent developments qualify lignin as a carbon additive in making batteries out of wood.

This and other uses as a carbon fiber material is due to the growing demand for eco-friendly and renewable energy storage.

So, how is lignin-based biomaterial produced? Same as its uses, the processes of producing lignin also vary, depending on the end-use application.

What are the Main Processes to Produce Lignin?

In Canada, the leaders in lignin recovery have led scientific research that resulted in the patenting of both lignin-recovery methods in use in this country — LignoForce System™ and the up-and-coming TMP-Bio™.

The LignoForce Method:

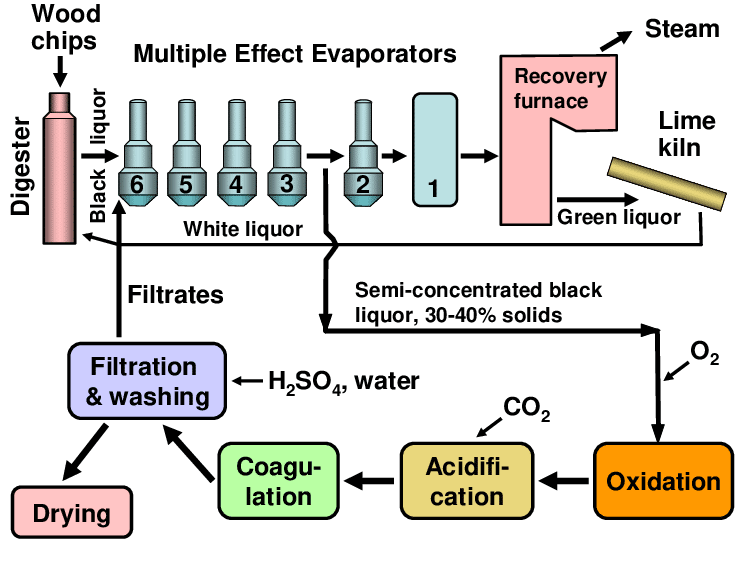

FPInnovations and NORAM Engineering together developed the LignoForce method, a patented technology for recovering high-purity lignin from softwood, hardwood or eucalyptus kraft black liquors (BL).

This process uses an oxidation step to extract and convert harmful compounds present in kraft BL to non-volatile compounds.

LignoForce was implemented in 2016 in the West Fraser’s Hinton pulp mill, Canada’s first commercial-scale lignin recovery plant. This process is often ideal at kraft pulp mills to produce:

more pulp in mills that are recovery-boiler limited

high-quality lignin (acid form) for use as a carbon-neutral fuel in the lime kiln

high-quality lignin for use in industrial applications such as wood adhesives, dispersants, and as a bitumen substitute in asphalt.

The following diagram shows how the LignoForce process works as discussed in Hubbe et al. (2019) study.

Source: Hubbe et al., 2019

In this process, the black liquor is oxidized with oxygen before being acidified with carbon dioxide, which has several advantages including:

Reduced sulfur odor

Reduction of CO2 use by 20 to 40 per cent

Heat from the oxidation step gets recovered and reused at the mill

The lignin is purer (less than 0.5 per cent ash content compared to 3 per cent ash)

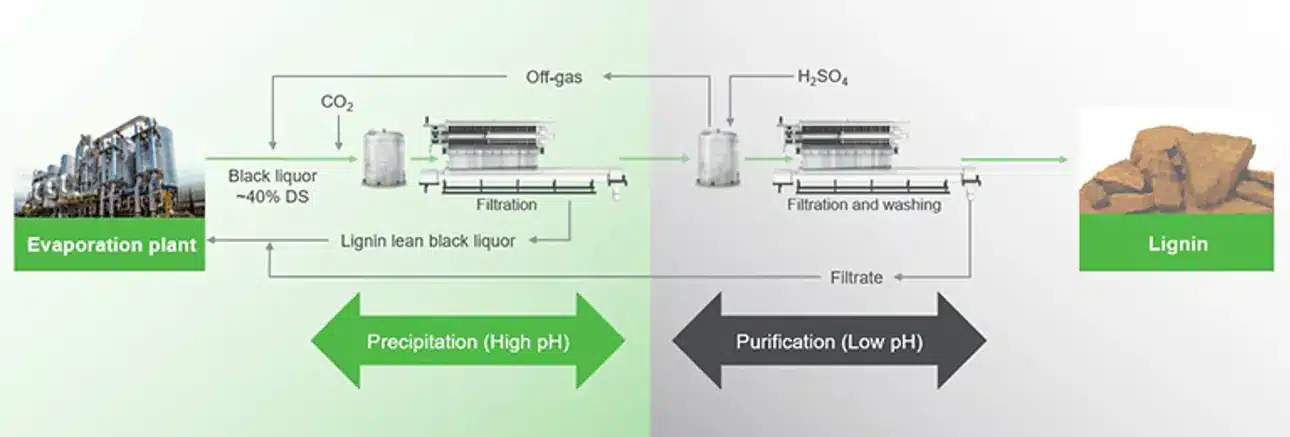

The LignoBoost Process:

LignoBoost is a patented extraction process that was initially developed by universities but commercialized and further improved by Valmet. This process involves two major steps – (1) separation and (2) washing.

Source: Valmet website

By separating the process into two steps, a high-quality lignin is produced. The method also offers great options to adjust the characteristics of the final lignin material.

Step 1: Separation

The first step is to separate the material from the mill’s black liquor. BL is from the evaporation process, and the pH gets lower with carbon dioxide and gas from the second step of the process.

Once the pH drops, lignin precipitates, gets separated from the liquor, and produces the LignoBoost crude lignin.

Step 2: Washing

This is where the lignin gets purified. A low pH solution is used to wash the crude material and then it’s dewatered in another filter press. The conditions during this washing step significantly impact material’s purity and LignoBoost ensures it is very pure.

Lignosulfonates vs kraft lignin:

Lignosulfonates are sulfonated lignins produced via the sulfite pulping process of the paper and pulp mills. This source has been the most abundant type of lignin that’s available on a commercial scale.

The process involves the use of sulfurous acid as the pulping solution to extract raw liquor to cook the biomass. The extracted lignin becomes water soluble and gets separated from its lignocellulosic biomass. It is this sulphonation process that is critical in giving lignosulfonates its key qualities.

Lignosulfonates were the first dispersants added as water-reducing admixtures to concrete.

In fact, they account for about 90% of the total market of commercial lignin, with global annual production of 1.8 million tons.

But most pulp mills are employing kraft technology for their production. Thus, kraft lignin becomes more readily available for many value-added applications.

In this sense, the sulfonation of kraft lignin has also become more common practice.

Kraft lignin is separated from wood using sodium hydroxide (NaOH) and sodium sulfide (Na2S). The kraft pulping process involves digesting wood chips at high temperatures and pressure in “white liquor” – a water solution of NaOH and Na2S.

The white liquor dissolves the lignin that binds the cellulose fibers together.

Lignin’s Role in Sustainable, Low-carbon Economy

The growing concerns of environmental pollution and shortage of fossil fuel resources have prompted substantial research on bio-based materials. And lignin becomes one of the top choices.

Its industrial uses have attracted immense attention because of its advantages of high carbon content, low cost, renewability, and sustainability. The bio-based material becomes the environmentalists and climate activists best option for making low-carbon polymers, chemicals, and other materials.

Lignin can replace or augment its petroleum-based counterparts. And with the current trend for sustainable industries, both from the public and private sectors, lignin has the potential to be a building block of a low-carbon economy.

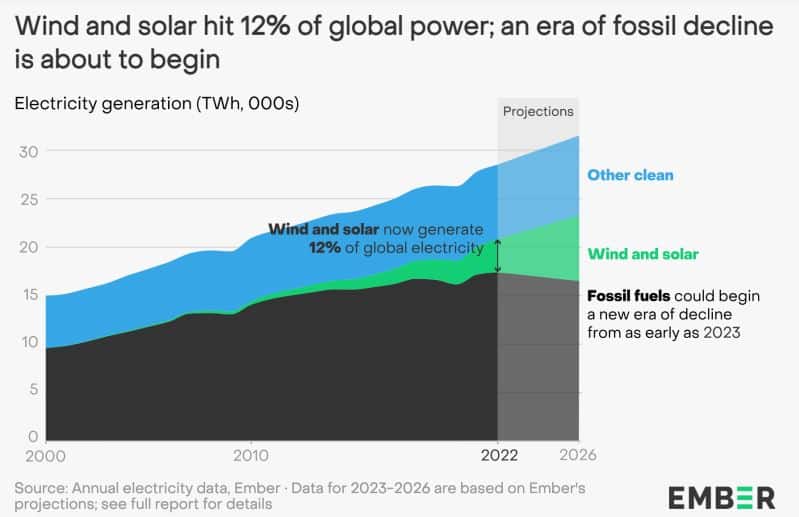

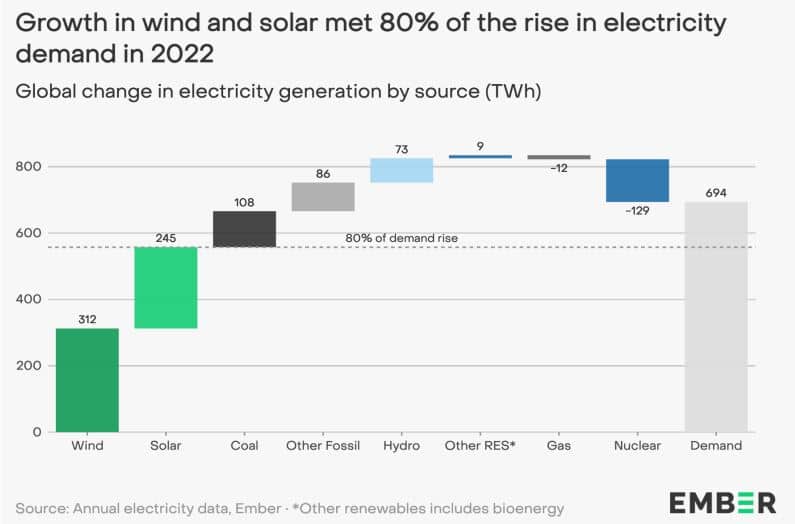

Clean power sources reached a new record 12% of global electricity generation in 2022 while experts say that the power sector’s emissions may have peaked.

Electricity emissions went up by 1.3% in 2022, hitting a record high as per Ember’s report. This is due to a small increase in coal consumption to meet the rising demand for power following the end of the pandemic lockdowns.

Meanwhile, coal generation grew by 1.1% only in the same year. 2022 was also the year for things electric, e.g. electric vehicles, electrolyzers, and heat pumps and this trend will continue.

But to deliver on the required carbon emissions reductions, it should be coupled with enough investments in clean electricity transition.

The Era of Clean Power

According to the energy think tank Ember, the global electricity sector’s carbon footprint may have peaked last year and it will begin to fall in the coming years. This prediction sends a signal that the sector was at its tipping point to shifting to clean power.

In its recent report, Ember found that deployments of renewable energy in 2022 drove wind and solar to reach a new record of 12% share in the electricity mix. It went up from 10% in the previous year.

Together, all clean electricity sources – renewables and nuclear – reached 39% of global electricity, a new record high.

All these caused the carbon intensity of global power to hit a record low of 436 gCO2/kWh, the cleanest-ever.

The report covered 2022 data gathered from 78 countries, comprising 93% of the world’s electricity generation. 80% of the increase in demand for electricity after the lockdowns was met by clean power, particularly wind and solar.

The report’s lead author, Małgorzata Wiatros-Motyka said that:

“In this decisive decade for the climate, it is the beginning of the end of the fossil age. We are entering the clean power era…Clean electricity will reshape the global economy, from transport to industry and beyond.”

The rapid growth in clean power use will sustain in 2023 and the following years, the report says. And that would be enough to see that the sector’s carbon emissions will plateau or decline next year.

That happens if clean energy developers and governments continue to support generation of cheap green power.

However, the author also noted that it still depends on how businesses and individuals “put the world on a pathway to clean power by 2040.”

The global electricity sector is the largest emitter. And it’s the first sector that has to decarbonize for the world to achieve net zero because it helps unlock electrification in other sectors.

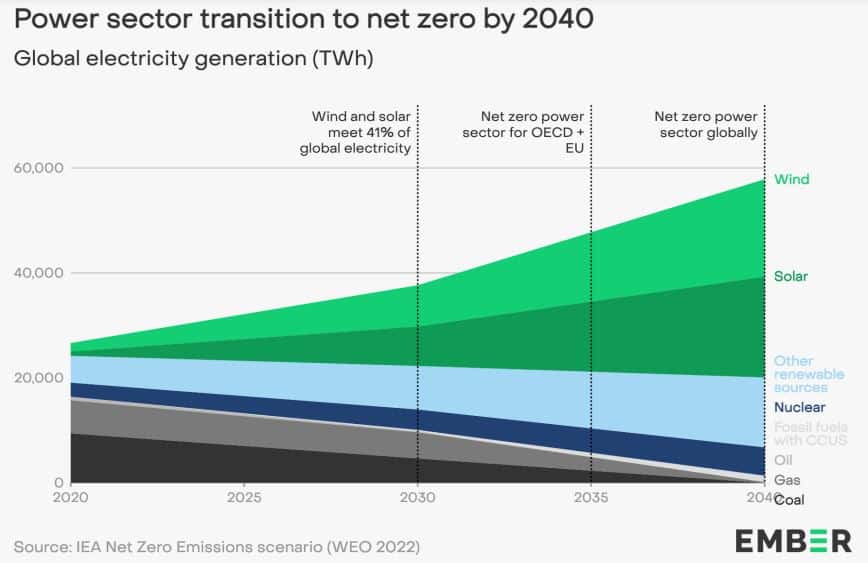

Net Zero Power by 2040

According to the International Energy Agency (IEA), the power sector must be net zero by 2040 to bring the world to net zero economy-wide by 2050.

In the IEA Net Zero Emissions (NZE) modelling, wind and solar are the key drivers, providing 75% of the growth in clean power from now to 2050.

By 2030, wind and solar have to increase to 41% of global electricity generation. By the same year, coal generation has to decrease by 54% while gas by 24%.

Electricity demand, however, will continue to rise significantly by about 3.7% annually until 2030 as electrification intensifies.

Here’s how Ember forecasts the power sector’s transition to its 2040 net zero emissions.

Investment in clean power is critical, not only in the sector but the whole energy generation to ensure that the path to net zero is taken.

Remarkably, investment in clean energy technologies in 2022 is the same as that of fossil fuels for the first time. This is a good sign but investments must triple by the end of this decade to be on track for 1.5C.

Developing countries received financial support from large emitters such as the EU, UK, and US. The funds help them displace the dirty coal with clean renewable sources.

Yet overall, fossil fuel generation still increased in 2022 by 183 TWh. This led to the power sector’s CO2 emissions to grow by 160 million tonnes.

While the global electricity’ emissions intensity is heading towards the right direction, its absolute emissions are yet to fall. This shows that the power sector hasn’t reached yet the point where emissions reductions are at the net zero level.

As per the IEA NZE scenario, the sector’s emissions should decline by about 7.6% each year until 2030.

Some industry experts agreed that Ember’s forecast might be attainable. But others said that it will take more years to become a reality, not this year or the next.

Whoever holds the right prediction depends on how commercial and political forces play in the transition to a low-carbon power.

A collaboration among four organizations created the first carbon credit accounting methodology in Europe for protecting seagrass beds that have a key role in mitigating the climate, and thus, allowing French companies to use the credits to offset emissions.

EcoAct, Digital Realty France, Schneider Electric France and the Calanques National Park work together in developing the said methodology.

EcoAct is an international climate consultancy and project developer, supporting companies in setting net zero strategies and achieving climate targets.

The Calanques National Park is Europe’s only national park that sprawls on land, sea and suburbs. It is one of the world’s biodiversity hotspots and is home to 200+ protected species both on land and at sea.

First Carbon Accounting for Seagrass Bed

The first low-carbon methodology for the seagrass bed protection in Europe is a result of a research project called the “Prométhée-Med”. Implementing the project can sequester about 24,000 tCO2e per year.

The crediting methodology in place will help ensure that the project can indeed reduce carbon emissions backed by science. It will also play an important role in preserving a key natural habitat of the Mediterranean, which is a critical carbon stock – the Posidonia meadows.

The seagrass carbon credits system gained the approval of the French Directorate General for Energy and Climate (DGEC).

Moreover, the project can help preserve the coastline because seagrass beds may prevent or slow down coastal erosion. Plus, the marine ecosystem where seagrass beds are a key habitat in the Mediterranean.

Commenting on the project, Director of EcoAct, Emilie Alberola said that:

“This project is the concrete proof that public-private partnerships can leverage technical expertise, such as that carried out by EcoAct’s teams, and help advance the protection of marine biodiversity through innovative financing mechanisms.”

Apart from the support of the four major players, the seagrass carbon credit project is based on the results of various academic and scientific institutions. These include the University of Corsica Pasquale Paoli, the GIS Posidonie – Corsica Centre, and the Mediterranean Institute of Oceanography (MIO) – Aix-Marseille University.

Seagrass’ Role in Regulating the Climate

So, why protect the seagrass beds?

Primarily because they play a vital role in regulating the climate and preserving global biodiversity. They are also very productive and diverse, providing important ecological functions.

Seagrass beds take less than 2% of the total surface area of the seas, providing home to as much as 18% of marine species.

More notably, the Posidonia meadow, is known for its carbon sequestration qualities. It can store as much as 700 tonnes of carbon per hectare.

That means the meadow has 5x more carbon storage capacity than tropical forests. Not to mention that seagrass beds can also support coastal fisheries and act as a water filter.

However, many factors led to the loss of seagrass beds such as pollution and climate change. A decaying underwater meadow also means a destroyed carbon stock.

This is why the new methodology for seagrass carbon credits is crucial to avoid further loss and destruction. These credits are also known in general as the blue carbon credits.

The Benefits and Challenges of the New Methodology

The Prométhée-Med project identifies some potential benefits and hurdles to help France reach its climate goals. These include the following:

Surface area – 80,000+ hectares

Regression rate – 0.29% a year

Carbon stocks – 327 tonnes of CO2 per hectare

Carbon reduction potential – 24,000 tCO2e a year or 700,000 tCO2e over 30 years for 80,000 ha.

In comparison, other low-carbon projects can reduce about 465,000 tCO2e.

More remarkably, the project touches on some social and economic benefits. The new carbon crediting system for seagrass can create more jobs, raise more awareness about meadow protection, and set up rules for anchorage (ship anchors destroy seagrass beds).

The Posidonia meadows is a key Mediterranean habitat and is a marine protected area but it hasn’t been the case. The Mediterranean Maritime Prefecture has implemented regulations on protecting the ecosystem, which they are further strengthening now.

With the approved methodology, the National Park is working on a project that will enable the developer to make the carbon market as a beneficiary.

The seagrass carbon accounting aligns with the industry need to provide high-integrity carbon credits as outlined in ICVCM’s Core Carbon Principles.

By putting in place strong standards, it will drive enough investments highlighting the important role of carbon markets in providing net zero solutions.

The Sustainable Aviation Buyers Alliance (SABA) members will buy sustainable aviation fuel (SAF) certificates or credits, allowing entities to buy scope 3 emissions credits.

For the first time, major companies such as JPMorgan Chase, Bank of America, Meta, Boston Consulting Group, Boom Supersonic, and non-profit RMI join together to buy credits for about 850,000 gallons or 2,576 tons of SAF.

The biofuel will power JetBlue flights this year.

This first joint procurement is a leap forward from SAF credits purchases by companies in the past. Industry experts believe this will dramatically boost the demand signal that customers send to the SAF credits market.

Commenting on the historic purchase, head of Net Zero Strategy at Meta, Devon Lake said:

“SAF certificates enable corporate aviation customers like Meta to credibly and transparently contribute to decarbonizing the aviation sector. Buying SAF through SABA‘s collective procurement process allows us to go one step further and send a strong and coordinated demand signal to the market.”

What’s the Sustainable Aviation Buyers Alliance?

The Sustainable Aviation Buyers Alliance or SABA is a joint initiative of clean energy non-profit MRI and the Environmental Defense Fund aimed at speeding up the path to net zero aviation by attracting investment in SAF.

According to MRI, they started working on the concept of SAF credits and market demand signals in 2019. The first procurement is a culmination of that effort.

The alliance’s founding members are large companies, including JetBlue, Boston Consulting Group, Boeing, JPMorgan Chase, Bank of America, Microsoft, Netflix, Deloitte, and Salesforce.

SABA’s work involves this three major areas:

Education and policy support: by helping members explore the technical attributes of SAF and its market, policy landscape and aviation emissions accounting

Technology innovation: by evaluating novel SAF technologies and working with like-minded organizations to manage barriers to entry

Investment opportunity: by establishing a transparent SAF crediting system that enables not just operators but also flyers to invest in high-quality SAF to achieve their climate goals

Net Zero Aviation with SAF

The SAF that the SABA members will buy is produced by World Energy, working to make net zero real. World Energy is currently producing 144,000 tons per year of SAF in Paramount, California.

The organization has a refinery that will go online at the same site with a capacity of 576,000 tons a year. It has a bigger plant that will start operating in 2025 in Houston, Texas, capable of producing over 700,000 t/yr.

Why SAF?

SAF is a drop-in fuel made with renewable or waste materials that can significantly reduce the carbon emissions of air travel. It has the potential to cut down the carbon intensity of flights by around 84% or 8,500 tons.

However, SAF makes up only 0.1% of the global aviation fuel supply and has a premium price compared with conventional fossil jet fuel. That is because of insufficient, disaggregated demand and cost barriers to SAF production.

Each SAF certificate or credit is equal to one ton of biofuel produced.

In the U.S., about 1 billion tons of biomass can be collected each year to produce 50 to 60 billion gallons of biofuels like SAF. The biomass sources vary, including:

Corn grains

Oil seeds

Algae

Agricultural and forestry residues

Municipal solid waste streams

Wood mill waste

Wet wastes and other fats, oil, and grease

Companies buying SAF credits will pay some or all of the premiums associated with SAF. And their purchases will help pursue decarbonization efforts that directly slash CO2 emissions in the aviation sector.

Also, SAF credits will deliver the following functions:

Promote the production of high-integrity SAF, making the biofuel more competitive relative to conventional fuel

SABA will launch its 2nd competitive process where it plans to buy SAF credits across a 5-year period. The organization expects to grow its annual demand by over 10x this second time compared to the first procurement.

The second process will be open to all fuel providers and airline operators.

SABA members will also pilot a new digital registry to bring more transparency, consistency, and integrity for SAF credits. This is crucial to build trust in the system and convince more companies to buy the certificates.

The estimates by the International Air Transport Association (IATA) show that SAF will account for 65% of mitigation needed by aviation. And the industry expects this to grow even more as the world economy races to net zero.

Galvanize Climate Solutions, an investment arm of a company owned by billionaire Tom Steyer, plans to buy apartments and buildings across the U.S. and upgrade them to be net zero in three years.

The philanthropist and climate activist’s plan will start this summer, with the goal to reduce the portfolio’s carbon emissions and bring it to net zero by improving energy efficiency.

A New Model for Climate Investing

Joseph Sumberg heads Galvanize Real Estate and is from Goldman Sachs. He commented on the firm’s plan saying:

“This is a real estate strategy with a decarbonization goal… Capitalism will look at this successful strategy, and replicate it, creating ripples through the built environment.”

Sumberg and Galvanize, a company co-founded by two stalwarts of Bay Area finance, Steyer and Katie Hall, will invest billions of dollars into the plan. But they didn’t disclose how much exactly their investment would be.

Sumberg, however, noted that it will be sizable and focus on markets in the Pacific Northwest, Colorado, California, Arizona, and Texas.

Steyer said that their plan of upgrading properties in line with Net Zero is not only good for the planet. It is also a good investment from a financial perspective. He also added that:

“The impact and the returns are linked; it’s not a trade-off. We are trying to create a new model for climate investing.”

Their goal is to employ a strategic asset acquisition and will follow proprietary ways to retrofit buildings. They will also add solar panels as a renewable source of energy for buildings. Doing so allows the investment arm to have a portfolio of energy-efficient buildings that will pay off in the long run.

The team that makes up the investing unit will have incentives and compensation that are linked to the plan’s sustainability targets.

Galvanize seeks to focus on acquiring these real estate properties:

Student Housing

Self-storage

Industrial properties

1 to 3-story, low-density multifamily residential properties with parking

The team will perform significant upgrades to the properties and will install solar panels for reduced energy and carbon footprint.

The investment arm will do that with the help of the company’s in-house tech experts and scientists. The team includes an energy expert and scientist Howard Branz.

Their approach provides a way to invest where investors will enjoy risk-adjusted returns as well as climate benefits, says Sumberg. If both aspects – financial return and environmental impact – are not met, they will stop the deal. In his words, “if we don’t get to net zero in three years, we forfeit those incentives.”

Greening Real Estate and Bringing it to Net Zero

Buildings consume 40% of energy and 70% of electricity produced in the U.S.

They also account for about 40% of annual global greenhouse gas (GHG) emissions and 12% of direct GHG emissions in the U.S.

So, making real estate greener is a must for achieving climate goals. In fact, it has been a huge criterion in making big investment decisions.

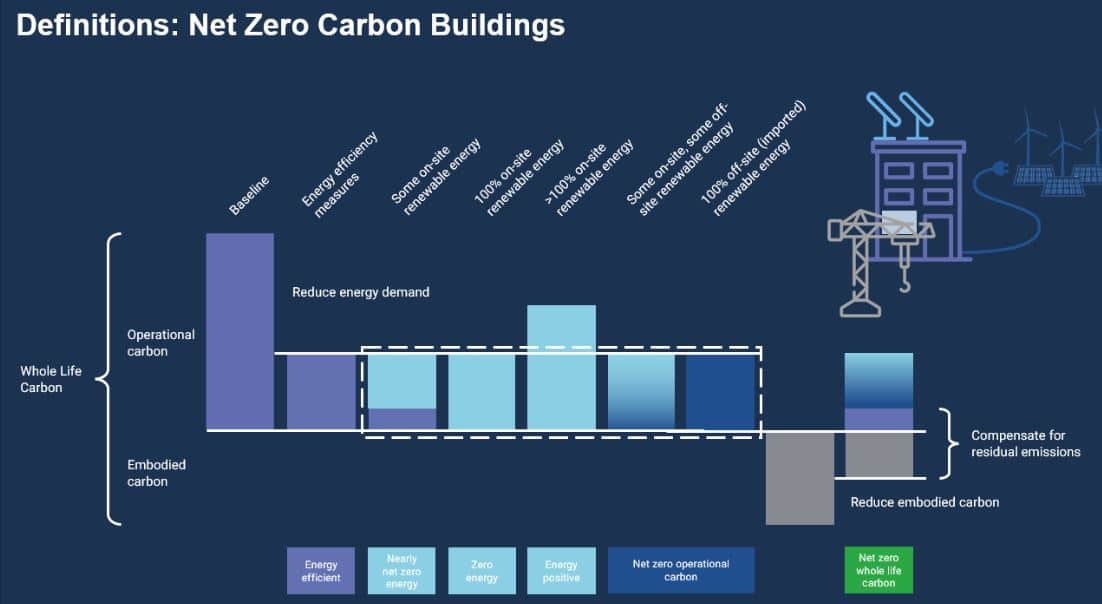

There are different terms used to describe buildings that are on a path to Net Zero. According to the World Green Building Council, here’s what a net zero carbon or net zero energy building looks like:

Source: World Green Building Council

Recently, states’ climate programs are putting a limit on how much carbon buildings are allowed to emit. Add to that the growing investors’ interest in ESG investing.

Take for instance the case of BlocPower, a New York-based company backed by Microsoft’s Climate Innovation Fund and Goldman Sachs. The firm secured a $155 million investment to expand green building retrofits. The tech startup has started its energy retrofitting model to 5,000+ apartments and buildings.

Another firm, RENU Communities also has a portfolio of over 2,800 housing units. It’s a subsidiary of Taurus Investment Holdings, which seeks to also green the real estate industry by reviewing properties. They check out designs, energy audits, and existing infrastructure to determine if they need some retrofits.

Galvanize joins these companies looking to green and decarbonize American buildings at scale.

More than 50% of apartments across the country were built before the 1990s. It means they most likely need some upgrades to boost energy efficiency.

From an investor’s point of view, energy-efficient retrofits are a must-have and become one of the real estate valuation criteria.

For Galvanize, it would be a first-mover advantage amid rising property rates and uncertainties. That means the firm would be in a better position to invest in assets that are worth upgrading and hence, avoiding non-performing properties.

Parking companies are also joining the retrofits and the race to net zero within the built environment. Installing chargers for electric vehicles in parking lots is one strategy for greening buildings.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.