DevvStream Holdings Inc., a publicly traded carbon management and technology company, has taken a bold step into the world of digital assets. The company announced it will use $10 million from its first financing round to buy digital currencies like Bitcoin and Solana. This strategy helps DevvStream’s long-term goal. It aims to use blockchain tech to digitize and grow the global carbon credit market.

The funds come from the first tranche of a much larger $300 million convertible note facility, provided by Helena Partners. DevvStream plans to speed up the growth of tokenized carbon credit systems. They will do this while keeping share dilution low for existing investors. This latest development positions DevvStream at the intersection of sustainability, finance, and technology.

Building a Blockchain Treasury: Why Bitcoin and Solana?

DevvStream’s newly launched crypto treasury will include Bitcoin (BTC), Solana (SOL), and the company’s own DevvE token. Each digital asset plays a different role in the company’s overall strategy.

- Bitcoin

Bitcoin is being used as a reserve asset. This cryptocurrency is known for its limited supply and wide use. This gives DevvStream a stable and liquid foundation. Its role in the treasury is to provide long-term value. It also acts as a financial cushion, separate from traditional markets.

- Solana

Solana, on the other hand, is being used for its technical utility. Known for fast transaction speeds and low fees, Solana’s blockchain provides the flexibility DevvStream needs to power smart contracts and digital token systems. It will play a central role in enabling the real-time creation, exchange, and settlement of tokenized carbon credits.

- DevvE

Finally, DevvE—the company’s native utility token—will serve as the bridge between environmental assets and blockchain infrastructure. DevvStream plans to use DevvE to create financial tools. These tools will help trade, monitor, and verify carbon credits and other sustainability assets on the blockchain.

These digital assets give DevvStream a varied crypto base. In turn, this base helps ensure financial security and supports platform functionality. The company noted:

“This $300 million facility allows us to improve capital efficiency, reduce dilution, and bring global investors into the carbon ecosystem through a digital gateway. The combination of crypto reserves and real-world asset tokenization represents the next evolution of our capital strategy.”

Tokenizing Carbon Credits and Real-World Environmental Assets

At the core of DevvStream’s strategy is the tokenization of carbon credits and related environmental assets. Tokenization turns real-world assets, like a certified carbon offset or a clean energy project, into digital tokens. These tokens can be issued, traded, and tracked on a blockchain.

This move is designed to bring transparency, liquidity, and speed to carbon markets, which are criticized for being slow, opaque, and fragmented. DevvStream thinks that by tokenizing these credits, it can help investors. This will improve access, ensure quality and traceability, and lower transaction costs.

The company is not only focused on carbon credits. It is also looking into tokenizing renewable energy infrastructure. This includes solar farms and battery storage systems.

These real-world assets could turn into digital investment products. This change could create new ways to finance clean energy development.

With this, DevvStream is not just making digital currencies; it is also building a new model for sustainable finance. This model links environmental impact with digital market infrastructure.

Trust and Tech: Safeguarding the Digital Green Future

DevvStream has chosen a regulated digital asset custodian. This helps them manage their crypto treasury safely and professionally. It has also partnered with a digital asset adviser to oversee treasury operations and ensure compliance with financial and regulatory standards.

DevvStream’s approach shows it is dedicated to building a strong and secure base for its digital finance strategy. It also helps build trust with investors and partners who may still be cautious about cryptocurrency exposure.

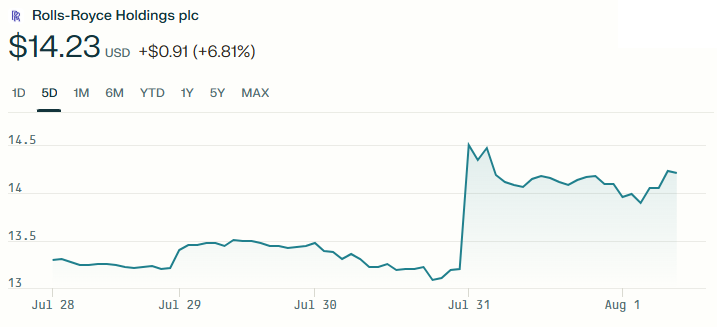

The company’s stock responded positively to the announcement. Shares jumped after the news. This shows that investors trust DevvStream’s plan to mix sustainability with blockchain innovation.

The treasury allocation is just the beginning. DevvStream will use more funds from the $300 million facility. They plan to boost their blockchain capabilities, support new sustainability projects, and launch their full token platform worldwide.

A Glimpse Into the Future Where Climate Goals Meet Crypto Gains

DevvStream’s decision to combine carbon management with digital assets reflects a growing trend in climate finance. More companies see how blockchain can fix old problems in the carbon market. These issues include double counting, poor transparency, and limited access.

As a result, the voluntary carbon market, though valued at around $4 billion in 2024, still operates far below its potential.

The issue of double counting alone may affect up to 30–40% of reported GHG reductions, undermining trust in climate claims. Also, carbon markets are often broken up, unclear, and depend on many brokers and registries.

Blockchain solves these issues with features like:

-

Tamper-proof tracking

-

Real-time updates

-

Automated credit retirement

-

Tokenizing real-world assets, such as carbon offsets

These systems make it easier to trace the origin and ownership of each credit, reduce fraud, and lower transaction costs. They expand access by allowing fractional ownership. This allows more people and companies to take part.

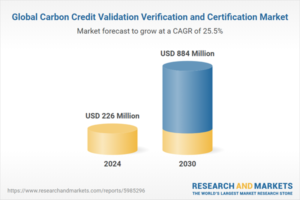

The market for blockchain carbon credit certification is growing fast. It could jump from about $884 million–$1.06 billion by 2030.

By combining carbon management with digital assets, DevvStream is tapping into this momentum—helping build a more open, liquid, and trustworthy carbon credit market.

A Digital Pathway to Real Climate Impact

With blockchain, each token can carry data about the origin, verification, and impact of a carbon credit. Investors can see where their money goes and what environmental results it supports. This level of clarity is difficult to achieve in traditional markets but becomes possible with digital tools.

In the long run, this approach could allow sustainability projects—from reforestation efforts to clean transportation systems—to raise capital faster, more efficiently, and with full transparency. It also helps align financial returns with climate goals, providing a win-win for investors and the planet.

DevvStream’s $10 million investment in Bitcoin, Solana, and its own token isn’t just about treasury management. It shows the future direction of sustainable finance.

The company is using digital assets and blockchain. This creates a platform for carbon credits and environmental projects, where they can work quickly, reliably, and openly. With this strategic move, DevvStream is not just participating in the future of clean finance. It is helping to define it.

Stock Dips Despite Q2 2025 Beat: Cloud Growth Slows, Net-Zero Push Expands")

to Get Fusion Power as Helion Energy Kicks Off Orion Plant Construction")

Rings Up $94B Q3 Win Fueled by iPhones, AI Push, and Climate Smarts")

Securing U.S. Battery Independence with $4.3 B LG Energy Solution Deal?")

Tops Q2 2025 Record-Breaking Surge in Durable Carbon Removal Credit Purchases")