The United States announced it would leave several major international climate agreements and scientific organizations. This includes pulling out of the United Nations Framework Convention on Climate Change (UNFCCC), reducing involvement with the Intergovernmental Panel on Climate Change (IPCC), and ending participation in dozens of other international groups. This is one of the biggest changes in U.S. climate diplomacy in recent years.

The decision has drawn strong reactions from governments, scientists, and environmental groups worldwide. Leaders and experts are discussing how this decision will impact global climate cooperation, scientific research, and long-term climate action.

What Was Announced: The Scope of the U.S. Withdrawal

On January 7, 2026, the Trump administration released a memo. It ordered the country to pull out of 66 international organizations. This includes key climate bodies like the UNFCCC and the IPCC.

The UNFCCC is a treaty adopted in 1992 to help countries work together on climate change. Almost every country in the world is part of it. The treaty supports frameworks such as the Paris Agreement.

The IPCC is not a treaty but a UN scientific group that reviews climate research. Countries participate by sending scientists, attending meetings, and helping fund their work. U.S. withdrawal means Washington will no longer take a full part in these activities. The memo reads:

“I (Pres. Trump) have considered the Secretary of State’s report and, after deliberating with my Cabinet, have determined that it is contrary to the interests of the United States to remain a member of, participate in, or otherwise provide support to the organizations listed in section 2 of this memorandum.”

The White House said these organizations “no longer serve American interests.” Officials said the move is part of a plan to focus on national priorities over international agreements.

Treaties, Science, and Authority: Legal and Procedural Questions

The UNFCCC became effective in 1994 after ratification by countries, including the United States. Under its rules, a country can leave, but the process can take time and may face legal challenges.

The U.S. has already left the Paris Agreement twice in the past decade. Under Executive Order 14162, President Trump’s administration started the withdrawal from the Paris Agreement, effective in January 2026.

Because the Paris Agreement is part of the UNFCCC, leaving the UNFCCC also ends U.S. obligations under the Paris Agreement framework.

Some legal experts note that the U.S. Constitution sets rules for international agreements. Critics of the withdrawal say the president may not have full authority to leave a treaty without Congress. This could lead to court cases.

The Roles of the UNFCCC and IPCC

The UNFCCC helps countries work together to reduce emissions and adapt to climate change. Countries report greenhouse gas emissions each year. They also meet yearly at the Conference of the Parties (COP) to set climate goals.

The Paris Agreement sets targets to limit global warming. It aims to keep the temperature rise “well below 2°C” above pre-industrial levels and to try to limit it to 1.5°C.

The IPCC produces reports that summarize global climate research. Governments and international organizations use these reports to make policy decisions.

Without formal participation, the U.S. government won’t negotiate climate rules as a full member. It also won’t help shape scientific reports.

Global Response and Reactions

Many governments and climate leaders reacted quickly.

The UN climate chief called the decision a “colossal own goal” that could hurt U.S. economic opportunities and climate preparedness. Further, Jake Schmidt of the Natural Resources Defense Council said in an interview:

“It’s critical the United States is a participant in and is actively trying to reduce climate change — it’s the world’s largest economy, the world’s biggest historical emitter.”

European Union officials said the move is “regrettable” and emphasized that they will continue international climate work, per the European Commissioner for Climate Action Wopke Hoekstra. Meanwhile, Vice-President Teresa Ribera stated:

“The White House does not care about the environment, health, or human suffering.”

Environmental and science groups warned that leaving climate institutions could hurt global cooperation. It may also cut funding for poorer countries.

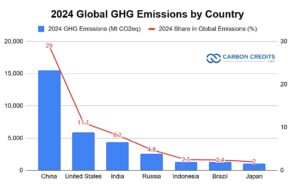

Critics also note that the U.S. is one of the world’s largest greenhouse gas emitters. It is, in fact, the second-biggest emitter in 2024. It produced over 11% of global CO2 emissions, as shown below.

What This Means for Global Climate Action

The U.S. has played an important role in global climate work. As a major economy and emitter, it has helped set global goals, reporting rules, and funding for developing countries.

With the U.S. withdrawing, climate negotiations will continue but without American influence in formal treaty processes. Other countries, like the EU and China, are expected to take leading roles.

For science, the IPCC will continue producing reports, but U.S. government scientists may be less involved. Private researchers and universities can still take part independently.

Money and Markets: Climate Finance at a Crossroads

International climate finance helps countries reduce emissions and adapt to climate change. Funds such as the Green Climate Fund and the Global Environment Facility receive some money from rich countries, like the U.S.

Leaving these bodies could make funding less predictable, at least temporarily. This may affect projects in developing countries, such as clean energy development and climate resilience programs.

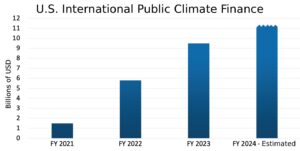

In 2024, the United States gave about $11 billion each year in international public climate finance under the former Biden administration. This funding helped developing countries reduce emissions and adapt to climate impacts. It made up around 8% of global climate finance that year. This figure shows a big jump from past years. It grew from about $1.5 billion in 2021 to over $9.5 billion in 2023. By 2024, it reached $11 billion.

However, recent policy changes canceled the U.S. International Climate Finance Plan. The U.S. contributed to both bilateral and multilateral programs. It also pledged $3 billion to the Green Climate Fund. However, future payments may be uncertain due to recent policy changes.

Market analysts also note that climate policies, standards, and carbon markets guide clean energy investments. Without the U.S., these frameworks might change. This could impact global energy markets and corporate strategies.

What Happens Next?

Withdrawal from treaties like the UNFCCC takes time and may face legal challenges in U.S. courts or Congress. Some experts expect court cases over whether the president can leave treaties ratified by the Senate alone.

Meanwhile, countries will continue climate talks and prepare for future COP meetings. U.S. states, cities, and private businesses may also increase climate cooperation outside the treaty system. However, the U.S. government’s role in guiding global science and policy through the IPCC and UNFCCC will be smaller during the withdrawal.

Trump’s decision to leave the UNFCCC, reduce engagement with the IPCC, and exit other international bodies is a major change in global climate policy. Even though the U.S. remains a major economy and emitter, its role in shaping global climate agreements and scientific reports has been greatly reduced.

The full effects of these moves will unfold over the coming years as climate negotiations continue and countries adjust to a new international landscape.