Disseminated on behalf of Surge Battery Metals.

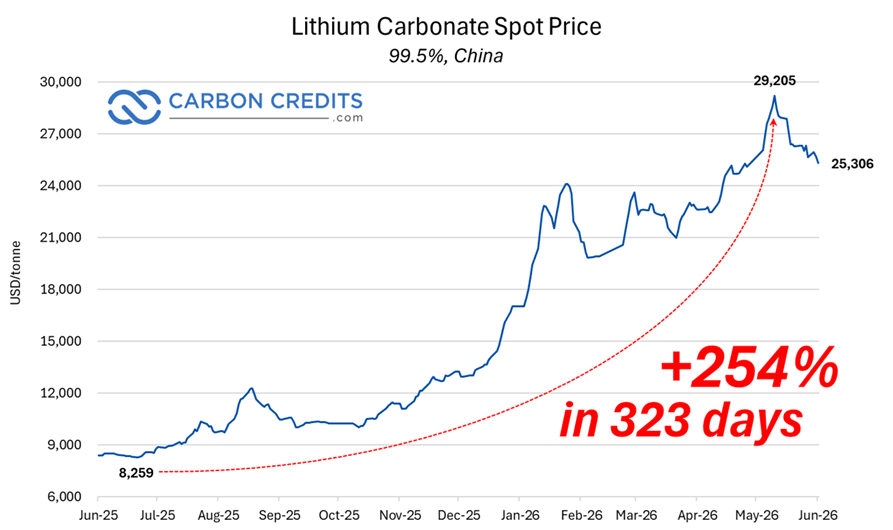

Lithium carbonate prices in China have risen close to their highest levels in years, officially passing the 200,000 CNY mark on May 12. While prices have since dropped to around 170,000 CNY per tonne or about $25,306 USD, this sharp bounce keeps lithium in a high-price bracket. This fast-moving market shows a major shift in how people view global battery metals. It proves that the industry has entered a new era of unpredictable price swings.

But this time, unlike past cycles marked by steady demand or supply shocks, the current shift is happening in a more complex setting. Pricing is getting more volatile. It reacts quickly to changes in inventory signals, procurement timing, and benchmark shifts in China — the main reference point for lithium carbonate value.

The result is a market that is no longer behaving like a traditional commodity cycle. Instead, it behaves like a high-volatility pricing system adjusting to evolving long-term supply expectations.

Lithium’s New Bull Market Is Driven by Volatility, Not Stability

Lithium remains supported by strong structural demand from electric vehicles and energy storage systems. However, price behavior has shifted significantly compared to earlier cycles.

The market has shifted from slow trends based on consumption growth to quick ups and downs. Now, it moves within a tighter trading range.

Two dynamics are particularly important to note here:

- China’s lithium benchmark prices are now a real-time sentiment gauge. They amplify short-term market reactions in global supply chains.

- Supply responses vary by region, causing sporadic tightness. This only increases volatility instead of solving it.

This environment has created a market where prices depend more on expectations than just physical supply and demand. In this case, lithium is acting less like a typical industrial commodity. Instead, it resembles a strategic material that quickly adjusts its prices.

China’s Lithium Benchmarks Are Once Again Steering Global Markets

China is key to global lithium carbonate prices. It is a big consumer and the main processing hub for battery-grade materials at the same time.

Recent lithium carbonate price changes reaching $29,205 per tonne on May 12, 2026, multi-year highs, show this trend. Global sentiment often shifts quickly with changes in Chinese benchmark pricing.

Demand for electric vehicles and grid storage is strong. However, the main factor is how quickly prices respond to changes in sentiment in Chinese markets rather than to slow shifts in consumption.

This creates a feedback loop. Expectations, procurement strategies, and inventory positioning all add to short-term volatility.

Lithium Is Moving Beyond Boom-and-Bust Cycles

One of the most important developments in the lithium market is the transition away from traditional boom-and-bust cycles toward a structural pricing band with persistent volatility inside it.

Earlier cycles had clear phases of growth and correction. This usually happened because supply couldn’t keep up with rising demand. That structure is becoming less predictable.

Today, lithium prices seem to be stabilizing in a higher range. However, they still show frequent and sometimes sharp movements within that range. This suggests that the market is now shaped by a combination of:

- shifting expectations about future supply,

- liquidity-driven price adjustments,

- regional benchmark sensitivity, and

- contract timing dynamics across Asia.

The result is a market where volatility is no longer an anomaly — it is a defining feature.

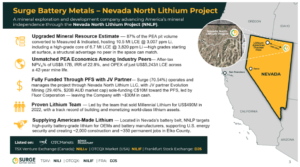

NNLP Project: How Surge Battery Metals (NILI) Fits Into the Next Supply Cycle

Within this evolving pricing environment, Surge Battery Metals (TSX-V: NILI | OTCQX: NILIF) is increasingly positioned around its flagship Nevada North Lithium Project (NNLP). It represents the company’s core asset in the United States’ lithium development landscape.

The NNLP project is in northeastern Nevada, an area that is crucial for critical mineral development. Its mining-friendly rules and closeness to new battery supply chains make it strategically important in North America.

With lithium prices steady at high levels, projects like NNLP are becoming crucial. They are not just exploration assets; they are future supply options in a tighter global market.

The broader market shift toward sustained higher lithium pricing is also changing how early-stage projects are evaluated. Investors are increasingly focused on:

- the long-term scalability of resource bases

- jurisdictional stability and permitting visibility

- alignment with North American supply chain security priorities

In this context, NNLP becomes more than a standalone development project. It shows future supply potential in a market that values flexibility more than quick production timelines.

That strategic importance has grown even more following the continued development of major Nevada lithium projects like Thacker Pass. Lithium Americas recently confirmed construction progress at Thacker Pass, with first production targeted for 2028.

Moreover, General Motors supported the project with $625 million. This investment is part of a larger joint venture and a long-term strategy for lithium supply.

For many investors, this was a major validation moment for Nevada clay lithium. For years, sedimentary clay deposits were doubted. This was mainly because only a few projects reached commercial-scale production. Thacker Pass moving into construction helped reduce that uncertainty and increased attention on nearby and similar lithium clay assets across Nevada.

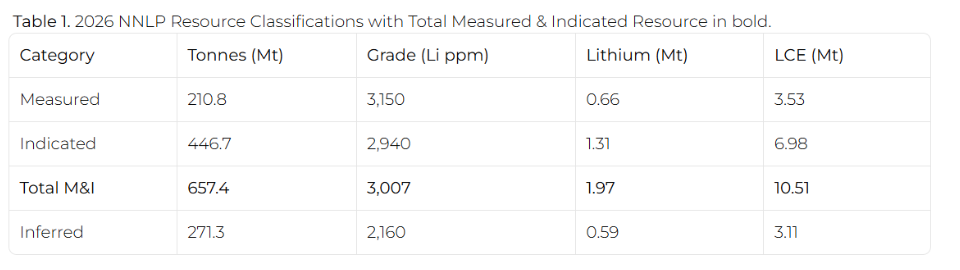

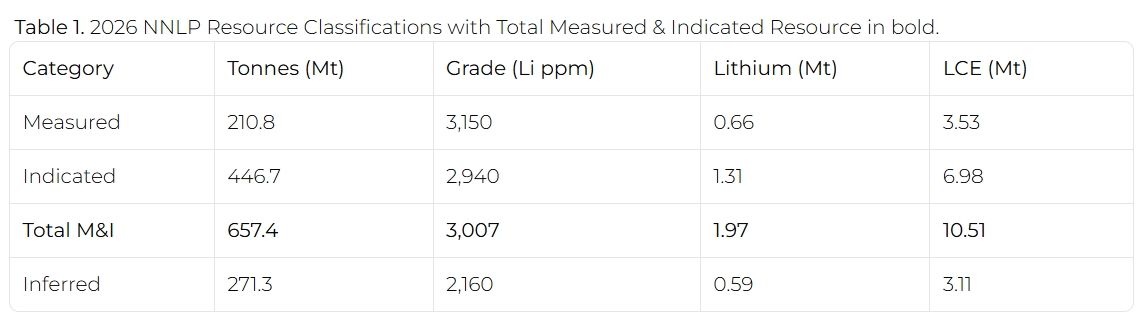

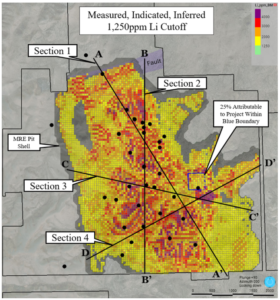

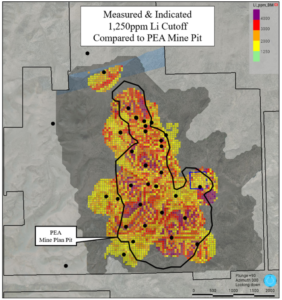

This broader shift has helped bring more focus to Surge Battery Metals’ Nevada North Lithium Project. The company reported an updated resource of 10.5 million tonnes of lithium carbonate equivalent (Measured & Indicated), grading 3,007 ppm lithium, including a high-grade subset of 6.7 million tonnes LCE at 3,820 ppm lithium.

The project benefits from Nevada’s mining infrastructure. Its location is in one of America’s fastest-growing battery material areas. And with prices high and volatility ongoing, undeveloped domestic lithium assets are becoming more strategically important.

Rising Lithium Demand Is Shifting Attention Toward Future Supply Assets

For Surge Battery Metals (NILI), the current lithium market is not just about short-term price moves. It reflects a longer shift in how the market values future supply.

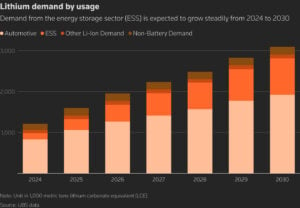

Lithium demand continues to grow strongly. The International Energy Agency (IEA) expects lithium demand to rise several times over by 2030, mainly driven by electric vehicles and battery storage.

At the same time, supply is still highly concentrated. China remains a major hub for lithium processing and battery-grade material production. This makes global pricing more sensitive to Chinese benchmark movements.

Because of this, investors are looking beyond current production. They are focusing more on future supply sources that can support long-term demand growth.

This is where NNLP becomes important. The project is located in one of the key lithium regions in the United States. The U.S. government is also pushing to secure more domestic critical mineral supply for the energy and battery industries.

As lithium prices stay high compared to long-term averages, early-stage projects like NNLP gain more attention. They represent future supply in a market where demand is expected to keep rising for years.

Lithium Enters a High-Volatility Structural Phase

The latest move in China’s lithium carbonate price, about $29,500 per tonne, shows more than a simple price increase. It reflects a deeper change in the market.

Lithium is no longer moving in simple boom-and-bust cycles. Instead, it is now trading in a higher and more unstable price range.

For Surge Battery Metals (NILI), this shift is important. The NNLP project becomes more relevant as the market looks for new long-term lithium supply sources.

Overall, lithium is now in a phase where future supply matters as much as current production. This supports long-term interest in early-stage developers as the market adjusts to a tighter and more volatile pricing environment.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Upgrades Nevada North to 10.5 Mt LCE M&I Resource as U.S. Lithium Development Gains Momentum")

and SpaceX Pull It Off?")