Battery technology is now one of the most important pillars of the global clean energy transition. It sits at the center of electric vehicles, renewable energy storage, and grid decarbonization.

Global investment in battery materials has jumped in recent years. This sector has drawn tens of billions in venture and infrastructure funding. Meanwhile, the demand for EVs and clean power keeps rising. These private companies are now competing to solve three major challenges: energy density, cost, and circular supply chains.

The four companies below are among the most influential private players shaping the next phase of battery innovation. But before we dive into each of them, let us examine the current market trends and growth forecast first to have a full picture of the sector.

Battery Market Growth Accelerates as Net-Zero Targets Expand

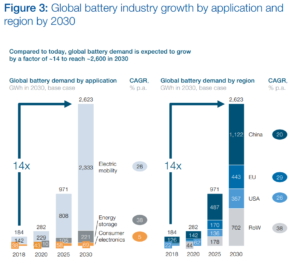

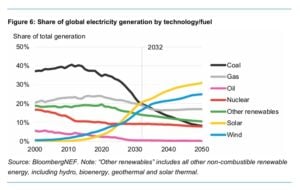

The global battery industry is entering a period of rapid growth as countries, automakers, and utilities invest in electrification. According to the International Energy Agency (IEA), global electric vehicle sales exceeded 20 million units in 2025, up from about 17 million in 2024.

EVs accounted for 25% of all new car sales worldwide. Global battery demand exceeded 1 terawatt-hour (TWh) for the first time. This surge was mainly due to transport and energy storage needs.

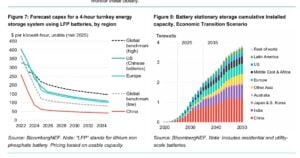

Growth is expected to continue through the decade. The IEA projects battery demand could increase more than fourfold by 2030 under current policy settings. Meanwhile, global energy storage deployment is also accelerating as countries add more solar and wind power to their grids.

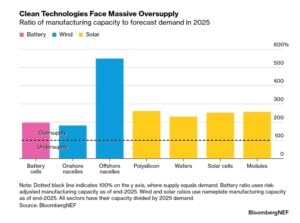

BloombergNEF predicts that stationary battery storage will grow quickly until 2035. This growth will make batteries essential for energy security and decarbonization.

As a result, investors are increasingly focusing on private companies developing next-generation battery materials, chemistries, and recycling solutions. Here are the top private tech companies that are making a great impact in the sector.

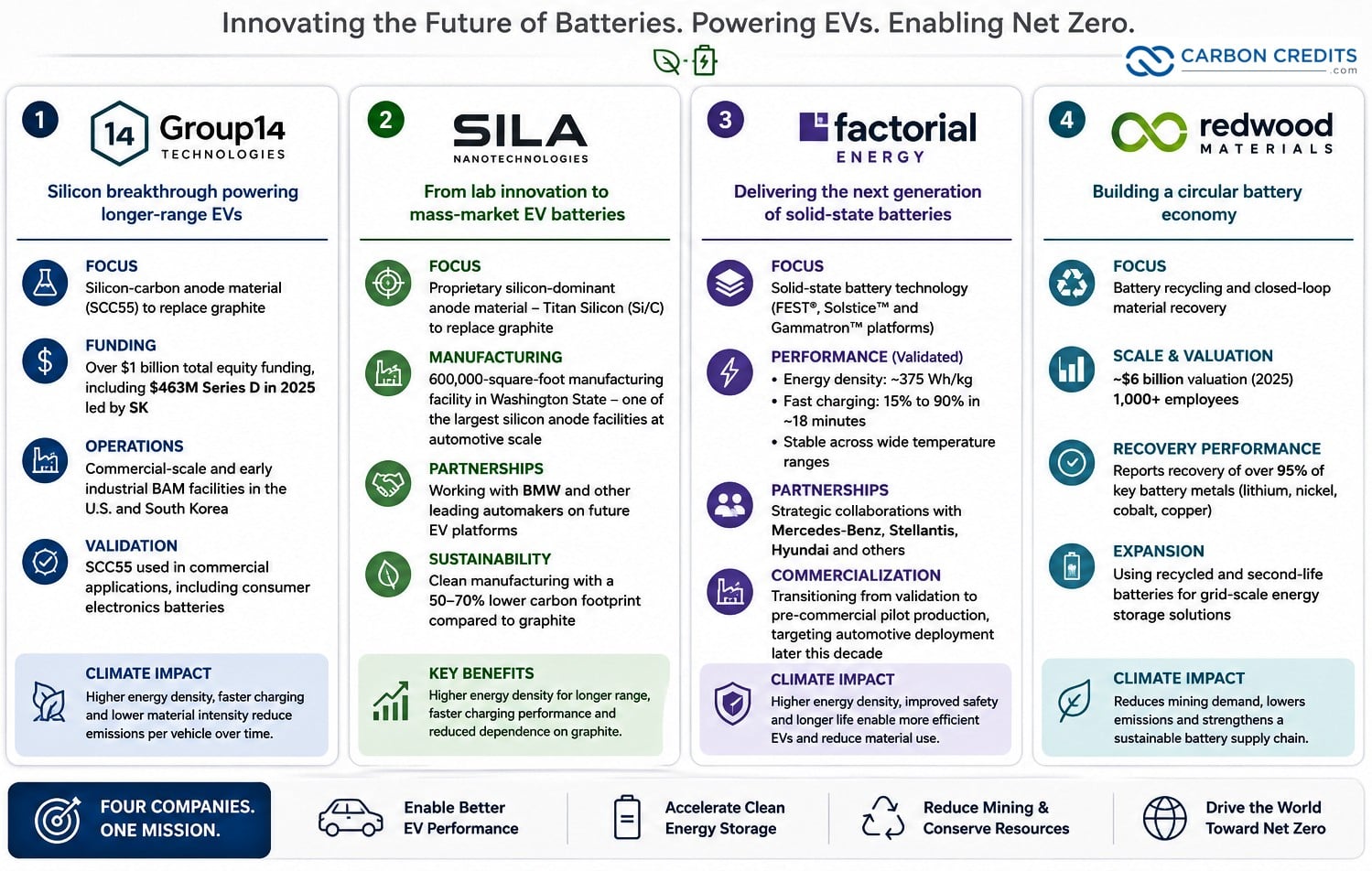

Group14 Technologies: The Silicon Breakthrough Powering Longer-Range EVs

Group14 Technologies is one of the most advanced silicon-carbon battery material companies in the world. It develops SCC55, a silicon-based anode material designed to replace graphite in lithium-ion batteries.

This matters because graphite is one of the limiting factors in current EV battery performance. Silicon can store significantly more lithium, enabling higher energy density and faster charging.

The company has raised over $1 billion in total equity funding. This includes a $463 million Series D round in 2025. SK led this round, marking one of the largest battery material investments in the sector. It also includes backing from major strategic investors such as Porsche and Microsoft’s climate-focused investment arm.

Group14 runs commercial-scale and early industrial production Battery Active Material (BAM) facilities in the U.S. and South Korea. These facilities have the production capacity for EV-scale deployment. Its SCC55 material is already used in commercial applications, including consumer electronics batteries, showing early real-world validation.

From a climate perspective, silicon anode technology is important because it can:

- Increase EV driving range without larger battery packs.

- Reduce material intensity per kilowatt-hour.

- Improve battery lifecycle efficiency.

These improvements lower emissions per vehicle over time. They do this by boosting EV adoption rates and cutting battery manufacturing inputs for each unit of performance.

Group14 is now scaling toward multi-GWh production capacity, positioning itself as a key materials supplier in the global EV supply chain.

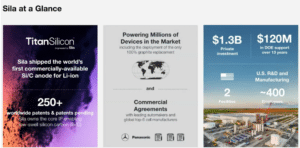

Sila Nanotechnologies: From Lab Innovation to Mass-Market EV Batteries

Sila Nanotechnologies is a top U.S. company developing silicon-based battery materials. Their goal is to enhance EV battery performance.

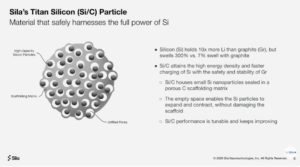

Founded in 2011, Sila has built a proprietary silicon-dominant anode material, known as Titan Silicon (Si/C), designed to replace graphite in lithium-ion batteries. This means higher energy density. So, EVs can go farther on one charge without adding battery size or weight.

A key milestone is the new 600,000-square-foot manufacturing facility in Washington State. This is one of the largest facilities for silicon anode production at an automotive scale. This facility represents a key step in moving silicon battery technology from lab-scale innovation to industrial production.

Sila has also partnered with leading automakers, including BMW, to support the integration of its materials into future EV platforms. The company’s technology targets three core improvements in EV batteries:

- Higher energy density for longer driving range

- Faster charging performance

- Reduced dependence on graphite supply chains

The company also claims that its clean manufacturing has a 50-70% lower carbon footprint than graphite. These changes are significant for decarbonization. Transportation makes up about a quarter of global CO₂ emissions. Also, battery performance is a key barrier to quicker EV adoption.

By improving range, boosting charging time, and lowering emissions, silicon anode technology directly supports broader net-zero transport goals.

- RELATED: How BESS and Lithium Demand Are Shaping Energy Storage: Global Shipments to Surge 50% in 2025

Factorial Energy: Delivering the Next Generation of Solid-State Batteries

Factorial Energy is one of the most advanced private companies working on solid-state battery technology. It is revolutionizing batteries through its next-generation high-performance battery platforms, including Factorial Electrolyte System Technology (FEST®), SolsticeTM, and GammatronTM.

Unlike conventional lithium-ion batteries, solid-state batteries replace liquid electrolytes with solid materials. This improves safety, increases energy density, and reduces overheating risk.

Factorial has achieved key validation milestones with major automakers. Stellantis has confirmed that Factorial’s solid-state cells reach:

- Around 375 Wh/kg energy density,

- Charging from 15% to 90% in about 18 minutes, and

- Stable performance under automotive testing conditions.

These results place Factorial among the leading solid-state developers globally, alongside a small group of competitors working toward commercialization.

The company has also secured strategic automotive partnerships, including with Stellantis, Hyundai, and Mercedes-Benz. These partnerships are critical because they provide a pathway from prototype cells to real-world vehicle deployment.

Solid-state batteries could significantly impact emissions reduction by:

- Extending EV range and reducing range anxiety,

- Improving safety and battery lifespan, and

- Reducing reliance on critical raw materials per unit of energy.

If scaled successfully, this technology could accelerate EV adoption across passenger vehicles and commercial fleets.

Factorial is now transitioning from validation to pre-commercial pilot production, targeting automotive deployment later in the decade.

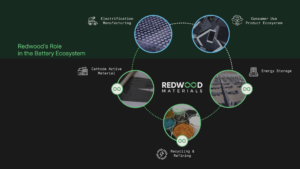

Redwood Materials: Building a Circular Battery Supply Chain

Redwood Materials is focused on one of the most overlooked parts of the battery ecosystem: recycling and materials recovery.

The company, started by ex-Tesla CTO JB Straubel, aims to create a closed-loop system that will recover essential battery metals like lithium, nickel, cobalt, and copper. They focus on recycling from old batteries and manufacturing waste.

The company has grown rapidly and was valued at around $6 billion as of 2025. It employs more than 1,000 people and operates large-scale recycling and materials processing facilities in the United States.

Redwood reports recovery rates of over 95% for key battery metals in its processing systems. This makes it one of the most efficient recycling platforms in the industry.

The company has recently ventured into grid-scale energy storage. They use second-life EV batteries to create stationary storage systems for utilities and data centers.

This expansion is important for net-zero goals because it:

- Reduces dependence on newly mined critical minerals.

- Lowers lifecycle emissions from battery production.

- Supports renewable energy integration through storage systems.

Battery recycling is expected to become a major industry as millions of EV batteries reach end-of-life over the next decade. Redwood is positioning itself as a key player in this emerging circular economy.

Four Different Paths, One Climate Goal: Why These Companies Matter for Net Zero

These four companies each cover a different part of the battery value chain, and together they support the shift toward net-zero emissions.

Group14 Technologies and Sila Nanotechnologies focus on better battery materials. Their silicon-based anodes help EVs store more energy and charge faster. This improves driving range and reduces the amount of raw material needed per battery. Over time, this helps lower emissions per kilometer.

Factorial Energy works on solid-state batteries, which use a solid material instead of a liquid one. They can be safer, last longer, and store more energy. If widely used, they could make EVs and energy storage systems more efficient and less material-intensive.

Redwood Materials focuses on recycling. It recovers key metals from used batteries instead of relying only on new mining. This reduces environmental damage and helps secure supply chains.

Together, these companies improve both sides of the climate challenge. They help scale clean technologies while also cutting emissions across the full battery lifecycle.

Final Takeaway

Battery innovation is moving from research to industrial scale. The top four private battery tech companies driving this change are boosting performance. They are also changing how the global energy system handles emissions.

As EV adoption accelerates and renewable energy expands, battery technology will remain one of the most important enablers of the net-zero transition.

Private innovators like Group14, Sila Nanotechnologies, Factorial Energy, and Redwood Materials are now central to that shift—each addressing a different but essential part of the future energy system.

in Focus: Record EV Exports, Solid-State Batteries Advances, and Smart Driving Push")