Disseminated on behalf of Alaska Energy Metals Corporation

Alaska Energy Metals Corporation (AEMC) is starting to draw serious attention from investors. The reason is simple: it offers exposure to nickel, a key metal for electric vehicles (EVs) and clean energy, at a very early stage and a low valuation. At the center of this story is the company’s Nikolai project in Alaska, which combines large-scale resources, improving economics, and a steady flow of upcoming catalysts.

Put together, these factors are building a strong case for a potential re-rating.

Nikolai’s Massive Nickel Resource Stands Out

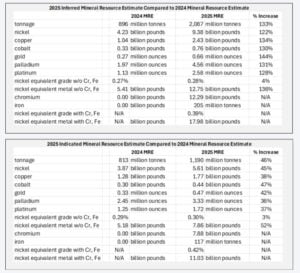

The Nikolai project is one of the largest undeveloped nickel resources in North America. As of March 2025, it hosts:

- 5.6 billion pounds of indicated nickel

- 9.4 billion pounds of inferred nickel

- Plus copper, cobalt, platinum, palladium, gold, chromium, and iron

This mix of metals matters. Nickel and cobalt are essential for EV batteries, while platinum and palladium add extra value. As a result, the project is not dependent on just one commodity.

Even more important, the deposit sits within a pit shell. This suggests it could be mined using open-pit methods, which are generally cheaper and easier to scale than underground mining.

Grades also support early development. The indicated resource averages about 0.30% nickel equivalent, with a higher-grade core extending over 2.5 kilometers near the surface. This could allow for faster production and earlier cash flow.

Recent drilling has already significantly expanded the resource. Between 2023 and 2024, indicated resources grew by 45%, while inferred resources jumped by 122%. This shows the system is still open and has room to grow.

From Explorer to Value Creator: A Shift the Market Is Missing

As of May 2026, AEMC is consolidating with a market cap of CAD 15 million. While the stock currently trades at a speculative CAD 0.07–0.10, the outlook is bolstered by the upcoming Preliminary Economic Assessment (PEA) for the Nikolai Nickel Project and a tightening global nickel market driven by Indonesian supply constraints.

As the company advances through federal permitting and metallurgical studies, its valuation remains sensitive to news flow; however, its positioning as a large-scale domestic source for critical minerals provides a strategic foundation for potential long-term growth as the project de-risks.

However, the company is moving beyond early exploration. It is now entering a stage where studies will start to show real economic potential. This shift is critical, yet the market has not fully priced it in.

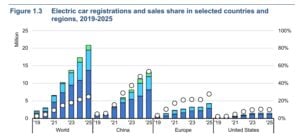

At the same time, the broader nickel market is changing. After a period of oversupply, conditions are tightening. Nickel price have already risen 37.5% from $14,241 on December 14, 2025 to $19,587 per tonne on May 6, 2026, and demand continues to grow with EV adoption.

Nickel Price

FAST-41 Could Accelerate Development

A major turning point came in late 2025 when the Nikolai project was added to the U.S. FAST-41 program. This initiative is designed to speed up approvals for critical infrastructure and mineral projects.

In practical terms, FAST-41 does three things:

- Coordinates multiple government agencies

- Sets clear timelines for approvals

- Reduces delays in permitting

This can cut years off the development timeline. For mining projects, that is a huge advantage.

The program also reflects a bigger policy shift. The U.S. wants to reduce reliance on foreign sources of critical minerals, especially from countries like China and Russia. As a result, domestic projects like Nikolai are gaining priority.

For AEMC, this means faster progress on infrastructure, including road access and site development.

A Low-Carbon Advantage Adds Appeal

Another key strength is the project’s location in Alaska. The region offers access to cleaner energy compared to many global mining hubs.

This creates a lower carbon footprint for nickel production. As ESG standards become stricter, this matters more to automakers and investors.

In addition, the project is scalable. Drilling has confirmed thick mineralized zones, including intersections like 356 meters at 0.34% nickel equivalent. These wide zones support large-scale, long-life operations.

Together, low emissions and scalability make Nikolai more attractive in a market that increasingly values sustainable supply.

Processing Partnerships Could Unlock More Value

AEMC is not just focused on mining. It is also exploring ways to process its ore into battery-ready materials.

The company signed a memorandum of understanding with RecycLiCo to test hydrometallurgical processing. This technology aims to recover nearly 100% of nickel, cobalt, and other metals more cleanly.

At the same time, a partnership with Lucid Motors points to potential direct supply into the EV value chain.

If successful, these efforts could transform Nikolai into more than just a mine. It could become a processing hub, generating additional revenue through refined products or toll processing.

Metallurgical testing is currently underway, and results will be critical. Strong recovery rates would significantly improve project economics.

A Strong Pipeline of Catalysts Ahead

One of the biggest reasons investors are watching AEMC is its upcoming news flow. The company has several important milestones lined up.

The most important is the Preliminary Economic Assessment (PEA), expected this year. This study will outline:

- Project costs

- Expected profits

- Production scale

Before that, investors will see results from metallurgy tests and development studies. These will help confirm whether the project is technically and economically viable.

On the financial side, AEMC recently raised about $3 million to support ongoing work. Future funding updates will also be closely watched. Meanwhile, permitting activities under FAST-41 and new drilling campaigns in 2026 could further expand the resource.

Each of these catalysts has the potential to move the stock. If results are positive, the company could shift from being seen as an explorer to a developer. That transition often drives significant valuation gains.

Strong Alignment With U.S. EV and Policy Trends

The timing also works in AEMC’s favor. The U.S. government is pushing hard to secure domestic supplies of critical minerals.

Nickel is a key part of this strategy. EV batteries require large amounts of nickel sulfate, and sulfide deposits like Nikolai are well-suited for producing it.

Globally, supply risks are rising. While countries like Indonesia continue to expand output, the U.S. wants more secure and local sources.

AEMC fits directly into this trend. Its project offers scale, location, and the right type of mineralization.

The company’s leadership also adds confidence. CEO Greg Beischer has deep experience in Alaska and has raised significant capital in the past. The project itself spans over 10,000 hectares and is located near existing infrastructure.

Risks Remain, But So Does the Upside

Like all junior mining companies, AEMC faces risks. These include:

- Metal recovery uncertainty

- Permitting delays

- Commodity price volatility

- Future funding needs

However, some of these risks are now lower than before. FAST-41 improves permitting visibility, while the project’s polymetallic nature provides some protection against nickel price swings.

At the same time, the low market valuation creates a strong risk-reward balance. If key milestones are achieved, the upside could be significant.

The Bottom Line

AEMC is building a clear and compelling story. It has already proven the scale of its resources. Now, it is moving toward studies, partnerships, and permits that could unlock real value.

Step by step, the company is creating a pipeline of catalysts:

- Large resource base established

- Permitting process accelerated

- Metallurgy and processing are advancing

- Economic studies approaching

For investors who believe in the long-term demand for nickel and the push for U.S. supply security, AEMC stands out as a high-upside opportunity.

Right now, it is still priced like an early-stage explorer. However, if upcoming milestones deliver, that may not last long.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Alaska Energy Metals. (“Company”) made a one-time payment of $90,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.