The Canadian Bank of Montreal or BMO recently released its report on the voluntary carbon market (VCM), providing an in-depth overview of market growth potential and complexity.

BMO Capital Markets believes that the VCM is slated for impressive growth. But that will be predicated on VCM’s ability to deliver high-integrity carbon credits.

Here are the four key takeaways from the report.

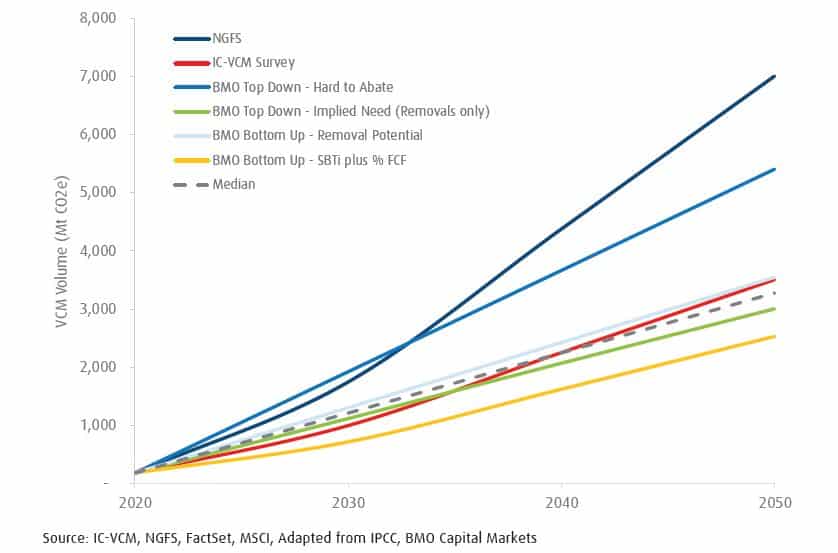

BMO Voluntary Carbon Market Projections

As per BMO’s projections, the banking giant sees the potential growth of the VCM to reach 6.5x by 2030 and 17.4x by 2050, relative to 2020 VCM total traded volumes.

- That also means the VCM can hit an annual volume of ~1.2 GT CO2e by 2030 and 3.3 GT CO2e by 2050.

This projection is based on the median of BMO’s four scenario analyses described below.

BMO VCM Growth Projections

Top-Down Growth Scenarios

Hard to Abate Emissions: This scenario was from “hard-to-abate” global emissions where offsetting is strictly reserved for.

BMO considers emissions hard to abate if the abatement cost is above US$200/T of CO2e or ~18 GT of CO2e per year. Three major sectoral emitters fall under this scenario:

- Energy,

- Industry, and

- Transport.

Implied Need, Removals Only: This BMO top-down scenario reflects how much CO2 must be removed to meet climate goals.

To stay within the 2°C carbon budget, BMO estimates that collective efforts must remove more than 110 GT CO2. This is under an assumption that VCM will get 30% carbon market share.

Bottom-up Growth Scenarios

SBTi limits: This scenario is based on a corporate offsetting limit of 10% to hit emissions targets.

The assumption under this scenario is that public firms have net zero targets for scope 1 but excluding scope 2 emissions.

Also, BMO assumes that offset price will rise over time, so the implied growth is ~4x by 2030 and ~14x by 2050.

Removal Potential: Under this bottom-up growth situation, BMO assumes that each carbon removal reaches the lower bound of their potential.

Applying 30% penetration rate, BMO projects voluntary carbon market growth of ~7x by 2030 and ~19x by 2050.

Overall, market volatility will have a negative effect on price and trade volumes of carbon credits or offsets.

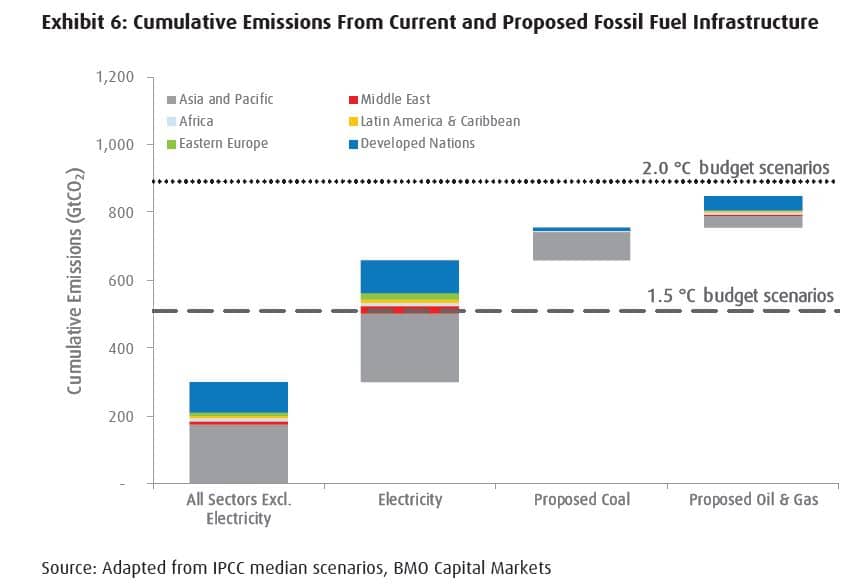

Carbon Removal Offsets Are Necessary

Market based solutions, particularly the ones that promote carbon removals, become increasingly necessary.

As governments are slow to enact climate policies, total emissions continue to increase. And current projections say that they will go beyond the budget needed to limit warming to 2°C.

Hence, it’s clear that climate finance is crucial to combine fossil fuel infrastructure with abatement technologies.

Carbon offsetting solutions are efficient even for projects that represent near-term reductions.

In particular, carbon removal technologies must be deployed to meet global climate goals. This also calls for investment in these technologies in the near-term.

As per BMO’s analysis, the highest quality carbon offset credits come from removal projects. Direct air capture scores best when it comes to meeting a set of criteria including:

- Additionality,

- Permanence,

- Net negativity, and

- Tradeoffs

Correlation Between Pricing and Credit Quality

Right now, the VCM is opaque with most credits trading over-the-counter. As such, price discovery and transparency are a challenge.

- Credit quality and price should be directly correlated according to BMO.

The firm also believes that credits not listed on one of the top carbon registries such as Verra, Gold Standard, Climate Action Reserve, and American Carbon Registry are challenged from a quality perspective.

That’s because investors likely don’t have the level of information or sophistication to evaluate a project absent from a top registry.

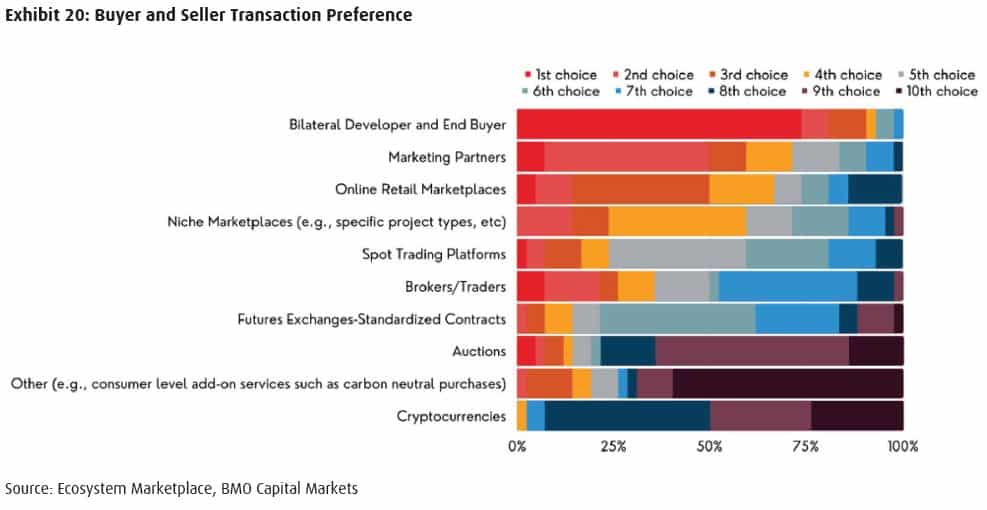

Quality projects are sought after and their credits mostly trade through bilateral agreements. They’re the ones that get premium pricing.

Evidently, direct, bilateral transactions for offsets remained the top choice for buyers and sellers.

As carbon exchanges provide the most transparent pricing data, transaction preference impacts market transparency.

Prices from exchanges don’t represent the market as a whole. But their movements may offer context on price momentum in the VCM.

With all these, investors must consider pricing transparency alongside the quality of carbon credits.

Corporate Offsetting Guidelines Shape the VCM

Offsetting in corporate decarbonization plans will be a key driver of demand growth in the VCM. But there are very few offsetting standards that guide net zero pursuit.

BMO examined offsetting strategies among the 2,000 largest public firms. They found little consistency across their decarbonization plans.

Due to inconsistency in net zero definitions, there are various categories for emissions reduction commitments from companies. In fact, the Net Zero Tracker identifies 14 different categories.

- By industry, apparel took the #1 spot with 100% of companies having emissions reduction pledges.

When it comes to disclosed detailed decarbonization plans, BMO said that firms with no targets have a low level of reduction planning, as expected.

Microsoft has one of the more detailed disclosures on its offsetting strategy and portfolio. The tech giant discloses carbon credit quality criteria and its offset purchases.

The company further documents offsets by:

- supplier,

- project name,

- location,

- type,

- certifier,

- contracted durability, and

- contracted volume.

BMO finds Microsoft’s example as a sophisticated and transparent offset disclosure. And more firms will have the same detailed reporting as education enhances and disclosure guidelines improve.

Overall, there are only a few official offsetting guidelines. These include the VCMI, SBTi, and the Oxford Principles.

While that’s the case, BMO thinks that there’s a growing agreement on ways of best practice that will affect offsets demand and shape the voluntary carbon market.

Entities that are not using carbon offsets properly may be at risk of reputational damage.