Australia’s reformed Safeguard Mechanism is reshaping how large industrial emitters manage carbon. The policy, updated in 2023, sets declining emissions limits for the country’s biggest facilities, including mining and energy operations. Companies that exceed their baselines must either cut emissions or purchase carbon credits.

This has triggered a sharp rise in demand for Australian Carbon Credit Units (ACCUs). According to the Australian government, the Safeguard Mechanism covers about 215 facilities, responsible for roughly 28% of Australia’s total greenhouse gas emissions. These sites must collectively reduce emissions by 4.9% per year through 2030.

Instead of cutting emissions immediately, many companies are turning to carbon credits to stay compliant. This includes major players like Rio Tinto and Woodside Energy, which are among the largest emitters in the system.

Mining Giants are the Biggest Buyers of Australia’s Carbon Credits

The mining and energy sectors dominate Australia’s emissions profile. Together, they account for a large share of industrial output and carbon intensity.

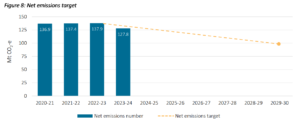

Under the Safeguard Mechanism, companies can use ACCUs or Safeguard Mechanism Credits (SMCs) to offset emissions above their limits. This flexibility has led to a surge in credit purchases. Moreover, entities covered by this scheme must cut net emissions to 100 MtCO2-e by 2029–30.

The ACCU Scheme supports projects that either reduce emissions or remove carbon from the atmosphere. These projects aim to:

- Enhance vegetation for better carbon storage.

- Adjust land practices to reduce emissions.

- Upgrade equipment to lower energy use and methane output.

Project developers earn one ACCU for every tonne of CO₂-equivalent emissions avoided or stored. These credits can then be sold to companies or governments, creating a financial incentive for emissions reduction.

The scheme continues to expand. In November 2024, a new reforestation method was introduced. This new approach builds on past models. It supports projects that boost carbon storage through environmental or mallee plantings.

Activity in the market has been strong. In 2024–25, over 380 new project applications came in, and 1,183 crediting applications were processed.

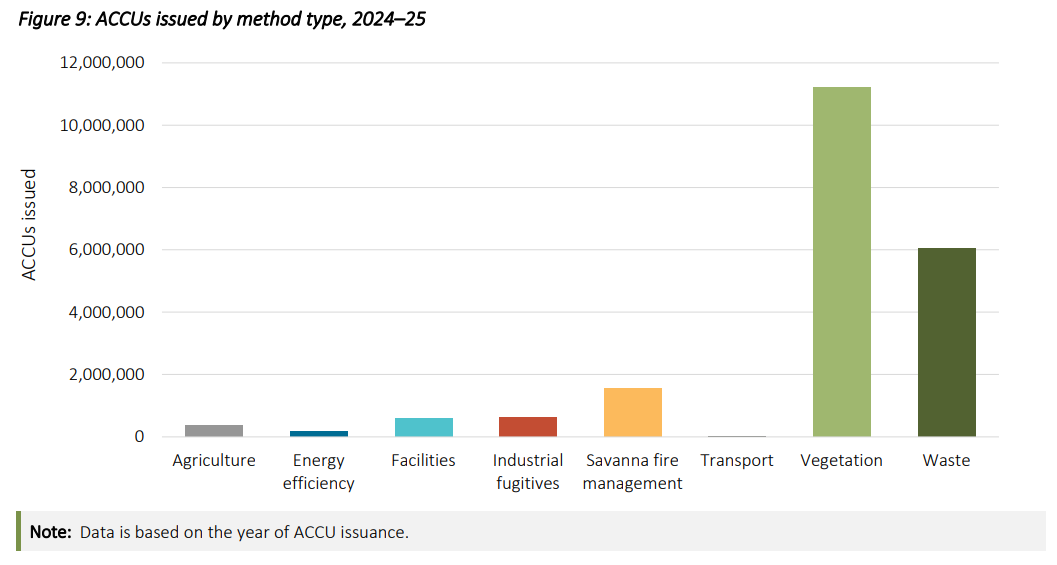

Credit supply has also reached new highs. A record 20.6 million ACCUs were issued in 2024–25, up from 18.7 million the year before. Over half of these credits—about 54%—came from vegetation projects. Meanwhile, 29% were from waste-related projects.

At the same time, spot prices are currently around AUD $30 to $35 per ton and are expected to stay relatively stable through 2028. However, the government’s cost containment price, used for companies facing higher emissions obligations, is much higher, set at $82.68 for 2025–26.

This imbalance reflects a broader trend. Companies are using credits as a short-term solution while longer-term decarbonization projects take time to develop.

Rio Tinto’s Tightrope: Balancing Cuts and Offsets

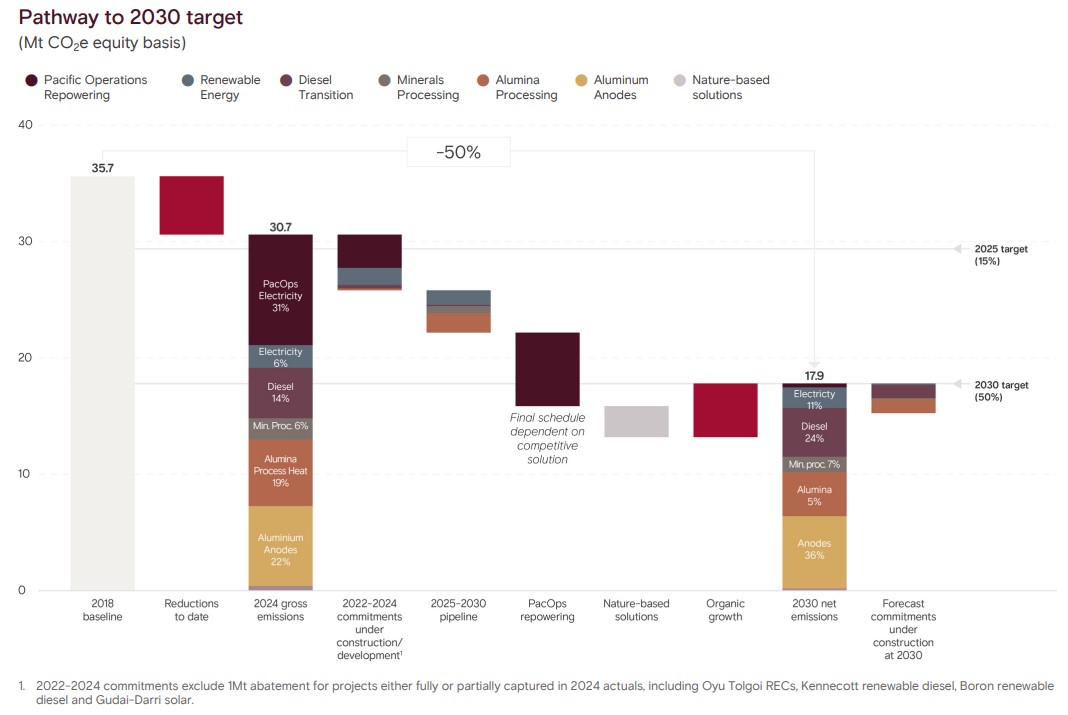

Rio Tinto is one of the world’s largest mining companies and a major emitter in Australia. The company has set a target to cut Scope 1 and 2 emissions by 50% by 2030, using a 2018 baseline. It also aims for net-zero emissions by 2050.

To reach these goals, Rio Tinto is investing in renewable energy, electrification, and low-carbon technologies. For example, it is developing large-scale solar and battery projects to power its iron ore operations in Western Australia.

However, emissions reductions in mining are complex. Heavy equipment, remote locations, and energy-intensive processes limit how fast emissions can fall. As a result, Rio Tinto has also used carbon credits to manage near-term compliance under the Safeguard Mechanism.

- The mining giant retired 1.1 million ACCUs in 2024 and plans to scale it to 3.5 million credits annually by 2030.

The use of credits reflects a broader strategy. The company combines direct emissions cuts with offset purchases to stay within regulatory limits while transitioning operations over time.

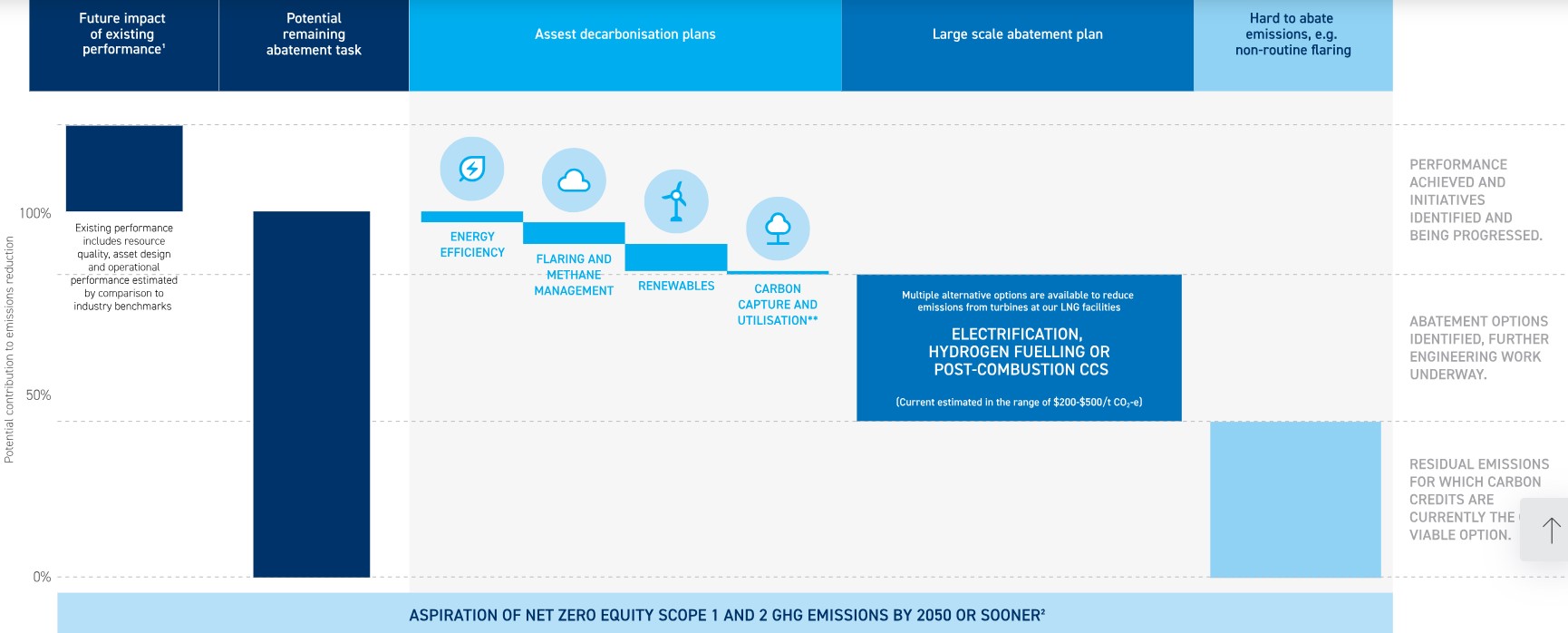

Woodside’s Climate Dilemma: Oil, Gas, and the Offset Dependence

Woodside Energy faces similar challenges. As Australia’s largest independent oil and gas company, it operates in a high-emission sector with limited short-term alternatives.

Woodside has set a target to reduce net equity Scope 1 and 2 emissions by 30% by 2030, based on a 2020 baseline. It also aims for net zero by 2050.

The company plans to invest in carbon capture and storage (CCS), hydrogen, and renewable energy. However, these technologies are still scaling.

In the meantime, Woodside has relied on carbon credits to offset emissions. This includes purchasing ACCUs to meet compliance requirements and support its climate targets. This approach highlights a key issue. For sectors like oil and gas, offsets remain a major tool in the transition.

Carbon Markets Are Growing—But Trust Issues Are Growing Too

Australia’s carbon market is growing, but it faces ongoing scrutiny. The Clean Energy Regulator oversees ACCU issuance and compliance, aiming to ensure credit quality and transparency.

At the same time, independent reviews have raised concerns about the integrity of some nature-based credits. This has led to tighter rules and increased oversight.

Globally, similar trends are emerging. According to the World Bank, carbon pricing mechanisms now cover about 24% of global emissions, with carbon prices ranging widely across regions.

In voluntary markets, demand is shifting toward higher-quality credits. Buyers are prioritizing projects with clear, verified emissions reductions and long-term impact. However, supply remains limited. This creates price pressure and increases competition for high-integrity credits.

Offsets vs Real Cuts: The Debate Behind Net Zero Strategies

Offsets play a growing role in corporate climate strategies, especially for hard-to-abate sectors. But they are not a complete solution.

Most net-zero frameworks require companies to reduce emissions first, then use carbon offsets only for residual emissions. This principle is reflected in global standards such as the Science Based Targets initiative (SBTi).

Still, the reality is more complex. Large industrial companies often face technical and economic limits on how fast they can decarbonize. As a result, many firms use a mix of strategies:

- Direct emissions reductions through efficiency and clean energy,

- Investment in new technologies like CCS and hydrogen, and

- Carbon credits to manage remaining emissions.

This blended approach is now common across the mining and energy sectors.

A Climate Transition Under Pressure: Progress or Delay?

The surge in carbon credit use under Australia’s Safeguard Mechanism highlights both progress and tension in climate policy. On one hand, the system is driving emissions accountability and creating a market for carbon reductions. On the other hand, heavy reliance on credits raises questions about how quickly real emissions cuts are happening.

For companies like Rio Tinto and Woodside, the path to net zero is complex. It requires balancing operational realities, regulatory pressure, and long-term investment.

The next phase will depend on several factors. These include the availability of low-carbon technologies, the integrity of carbon markets, and the pace of policy tightening.

For now, carbon credits remain a key tool. But their role is likely to evolve as the transition to lower emissions accelerates.

- READ MORE: Top Carbon Credit Companies to Watch in 2026