Copper prices hit new multi-year highs in 2026. This rise is due to supply disruptions, increased industrial demand, and structural shortages in global mining markets.

On the London Metal Exchange (LME), copper rose to $14,153 per metric ton on May 13, 2026. This marks its first time over $14,000 since January. It’s now approaching its all-time high, which is above $14,500 per ton.

In the United States, COMEX copper futures also hit a record near $6.64 per pound on May 13, 2026, marking one of the strongest rallies in recent years.

Copper Price

The metal is now up roughly 40% over the past year and about 75% since late 2023, showing a sustained upward trend rather than a short-term spike.

Peru Energy Crisis Raises New Supply Risks

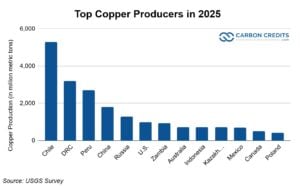

One of the biggest recent drivers of copper’s rally is growing supply uncertainty in Peru, the world’s third-largest copper producer in 2025. This is according to data from the latest U.S. Geological Survey.

On May 11, Peru issued an emergency decree (Decreto de Urgencia 003-2026) to manage a worsening energy crisis. The government said it would prioritize electricity for households and essential services. This raises concerns that industrial users, including copper mines, could face power restrictions.

- LME copper jumped as much as 1.2% in a single session to $14,106.50 per ton following the announcement.

The timing is critical because the global copper supply is already under pressure. Analysts say Peru’s disruption worsens production issues in other areas. This tightens the global supply of refined copper.

- SEE OUR LIVE COPPER PRICES HERE

Global Mine Disruptions Push Market Into Deficit Risk

Supply challenges are not limited to Peru. One of the world’s largest copper mines, Freeport-McMoRan’s Grasberg operation in Indonesia, has also faced delays after a major incident last year. Full recovery has now been pushed to 2027–2028, with current output running at only 40–50% capacity.

These disruptions are now feeding into global supply forecasts. The International Copper Study Group estimates a deficit of 150,000 tonnes in 2026. In contrast, J.P. Morgan predicts a shortfall of up to 330,000 tonnes. This gap is due to supply cuts and increased demand.

CITIC Securities has also flagged that global copper production forecasts for 2026 are now trending downward due to ongoing mine disruptions.

At the same time, China’s refined copper imports reached 452,000 tonnes in April 2026, showing that demand remains strong even as supply tightens.

AI, Clean Tech, and Electrification Turn Copper Into a Strategic Metal

While supply tightens, demand is accelerating from multiple long-term growth sectors. Copper is a critical material for electricity grids, electric vehicles, renewable energy systems, and now artificial intelligence infrastructure.

AI data centers, in particular, are emerging as a major new source of demand. JPMorgan estimates that AI-related data centers could add around 110,000 tonnes of additional copper demand by 2026. BloombergNEF predicts that data center infrastructure could hold over 4.3 million tonnes of copper by 2035.

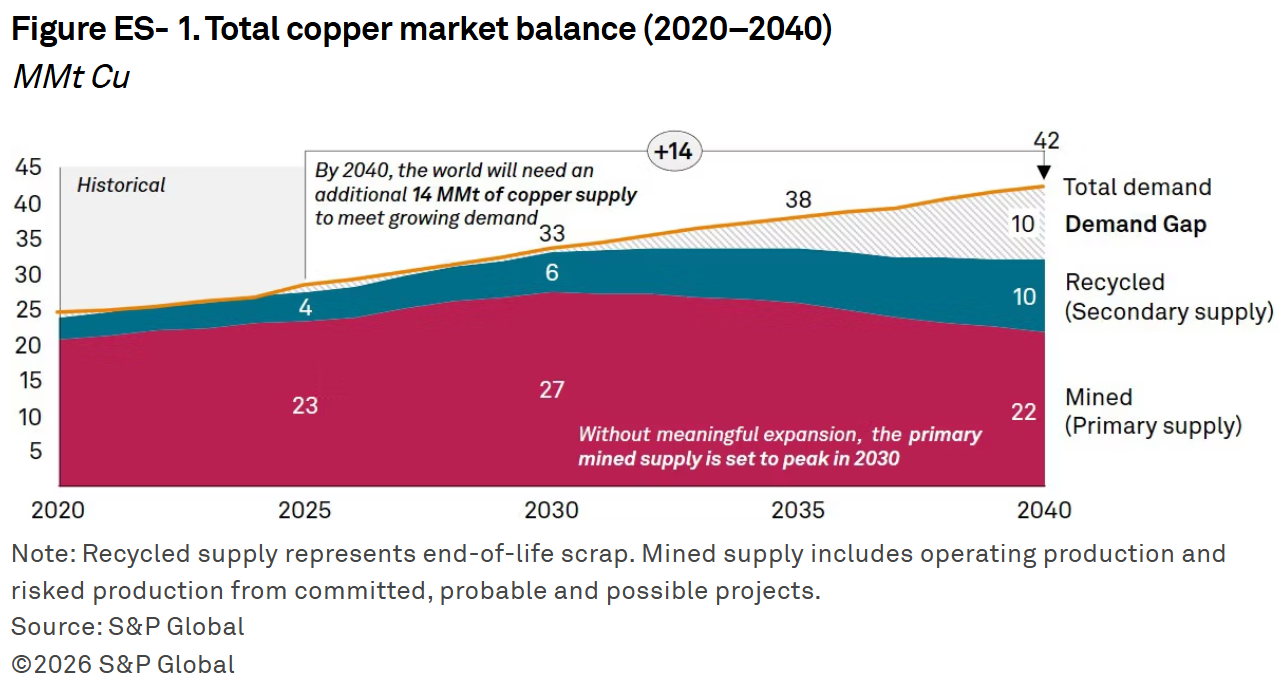

S&P Global predicts that global copper demand will grow by 50% by 2040, meaning it will hit around 42 million tonnes each year. Electrification and advanced technologies will drive this increase.

China is also reinforcing demand momentum. Export data revealed a 14.1% increase in April 2026 compared to last year. This rise exceeded expectations, driven by strong demand for copper-intensive goods. Key items included electric vehicles, lithium batteries, and solar panels.

- EV exports rose 53% year-on-year

- Solar exports increased 80% year-on-year

- Battery exports climbed 34% year-on-year

These trends reinforce copper’s role as a core input in the global energy transition.

RELATED: Rio Tinto’s FY25 Profit Falls 14%, but Copper Projects and Sustainability Efforts Stand Out

Hidden Bottleneck: The Sulfuric Acid Crunch No One Is Pricing In

Beyond mining disruptions, copper is facing a less visible but critical constraint: input shortages.

A key issue is the global shortage of sulfuric acid, which is essential for copper extraction. Export restrictions from China, Russia, and other countries have tightened supply. Spot prices have doubled since February in some markets.

Chile, which relies heavily on imported sulfuric acid for copper production, has been particularly affected. The country produces roughly 20% of global copper output, meaning input shortages there have global consequences.

Energy markets are also playing a role. Copper production uses a lot of energy. Higher costs for electricity and fuel are adding pressure on production in key mining areas. These combined bottlenecks are limiting the industry’s ability to respond quickly to rising demand.

Tariffs and Geopolitics Add Fuel to an Already Heated Market

Trade policy is also tightening global copper flows. The United States has set a 50% tariff on copper-heavy products under Section 232. This has changed how refined copper flows into the U.S. market. It has also tightened availability in other regions and added volatility to global pricing.

Geopolitical tensions, including risks around key shipping routes like the Strait of Hormuz, have also contributed to market uncertainty. While the direct impact has been limited so far, traders continue to price in potential disruptions to energy and industrial supply chains.

Market Outlook: Structural Tightness Likely to Continue

Despite short-term volatility, most market analysts expect copper prices to remain elevated. Major banks forecast prices to stay between $13,000 and $15,000 per ton, depending on supply conditions and global demand trends.

J.P. Morgan’s estimated 330,000-tonne global deficit for 2026 highlights how tight the market could become if disruptions continue. Even modest demand growth from AI and electrification could deepen the imbalance.

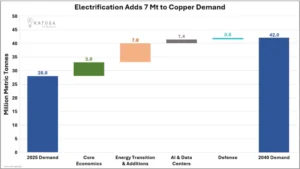

- Electrification in various sectors will require 7 million tonnes of copper by 2040.

Some analysts say copper is acting less like a cyclical commodity. Instead, it seems more like a strategic metal linked to long-term infrastructure growth.

Overall, copper’s surge above $14,000 reflects more than a traditional commodity rally. Three overlapping forces are driving it:

- Supply shocks in key producers like Peru and Indonesia.

- Rapid demand growth from AI, electrification, and clean energy.

- Rising input constraints and geopolitical pressure.

With global deficits emerging and demand accelerating, copper is entering a structurally tight phase. If current trends continue, the metal will remain central not only to industrial growth but also to the global energy transition and digital infrastructure expansion.