")

Disseminated on behalf of Surge Battery Metals.

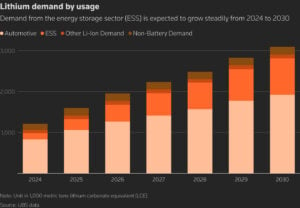

The story of lithium demand is changing. For many years, electric vehicles (EVs) were the main driver of demand for lithium. Today, that is no longer the full picture.

Battery storage is growing quickly. In 2025, global battery energy storage system (BESS) installations exceeded about 315 gigawatt‑hours (GWh), nearly 50% more than in 2024, according to Benchmark Mineral Intelligence. Grid‑scale storage and behind‑the‑meter projects for industry and data centers are major contributors to that growth.

This shift matters. According to industry analysis cited by Lithium Americas CEO John Evans, every one GWh of grid storage capacity requires about 900 tonnes of lithium. That is a large amount of material, and it adds a new layer to how lithium demand is understood.

As a result, lithium demand is now coming from three main forces in parallel: EVs, grid storage, and data center power resilience. This expanded demand picture is changing market forecasts and investment strategies.

EVs, Grid Storage, and Data Centers: The Three Forces Driving Demand

Electric vehicles are still an important part of lithium demand. EV sales and battery build‑outs continue to grow worldwide. However, they are not the only force driving lithium consumption.

Battery storage for the grid and for industrial power systems is becoming a major demand driver. Utilities around the world are installing lithium‑ion batteries to balance renewable energy, improve reliability, and cut peak power costs.

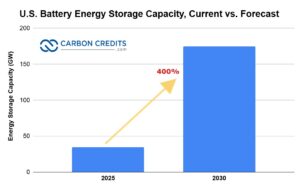

In the United States, the battery energy storage capacity is projected to grow 400% from 2025 to 2030. Data from Benchmark Mineral Intelligence and the SEIA project this rapid growth in five years.

At the same time, technology companies are deploying large lithium battery systems behind the meter to support reliable power for AI and cloud computing.

This broadening of lithium demand reflects developments in energy and technology infrastructure planning. For many regions, battery storage is no longer a side project; it is part of the core energy strategy.

Lithium-Ion Batteries Powering the Grid and Industry

Lithium‑ion technology is now the dominant choice for BESS. It accounted for a large majority of storage systems installed in 2024, and that share remained high into 2025.

Industry reports project that the global BESS market could be worth tens of billions of U.S. dollars by 2030, with steady growth as storage systems scale up to support renewables and grid flexibility.

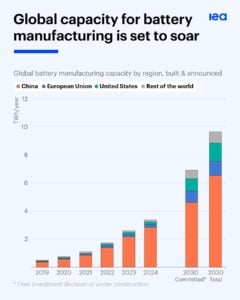

Meanwhile, battery manufacturing capacity is expanding rapidly. The International Energy Agency reported that global battery production exceeded 3 terawatt‑hours (TWh) per year in 2024, nearly three times what was needed for EV and storage demand that year. And it could soar to almost 10 TWh a year.

These developments show that demand for lithium in storage applications is becoming structural, not temporary.

From Transport to Infrastructure: Lithium’s Expanding Role

The rapid growth of grid storage affects how lithium demand is forecasted. In the past, most forecasts focused on EV batteries. Today, models are being adjusted to include storage applications that are tied to national energy planning and corporate resilience strategies.

As BESS installations grow, demand becomes more predictable and less tied to consumer EV purchase cycles. This stability matters for investors, suppliers, and policymakers alike. It means that supply projects need to plan for longer-term demand horizons, with stable output for multiple industry uses.

Nevada North Lithium Project: Built for the Multi-Driver Lithium Market

This expanded demand picture highlights the importance of long‑lived lithium resources. Projects that can supply lithium steadily, for many years, are becoming more important as demand widens beyond EVs.

One example that aligns with this shift is the Nevada North Lithium Project (NNLP) by Surge Battery Metals (TSX-V: NILI | OTCQX: NILIF), a high‑grade, domestic resource with characteristics that match the evolving market needs.

Here are key attributes of NNLP that align with expanding lithium demand:

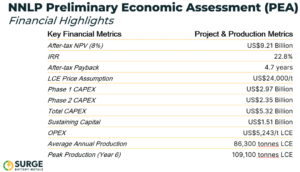

- Long Duration Supply: NNLP has a projected 42‑year mine life, according to the 2025 Preliminary Economic Assessment (PEA). This long horizon supports the extended demand profiles needed for grid storage build‑outs and infrastructure projects, not just EV batteries.

- High Annual Output: The project’s average production of approximately 86,300 tonnes per year of lithium carbonate equivalent (LCE) places it in the range needed for large‑scale storage supply frameworks.

- Domestic Resource Position: Located in Nevada, NNLP contributes to U.S. goals for domestic critical mineral supply. This is increasingly important for utilities, policy makers, and corporate partners who want secure, high‑quality sources closer to end markets.

- Development Framework: NNLP’s planning and partnerships position it to meet commercial expectations tied to long‑term supply, offtake, and investment strategies.

These features are meaningful as the market looks for lithium that can serve EVs, grid‑scale storage, and data center power resilience together, not in isolation.

Why Grid Storage Becomes a Strategic Priority

Battery storage is becoming a focus of public policy and business planning. In regions where grid reliability is a concern, storage systems help prevent blackouts and manage peak demand. For utilities, storage offers a way to integrate more renewable energy without compromising stability.

At the same time, commercial and industrial users, especially data centers supporting AI workloads, are investing in battery systems that protect operations from interruptions. This is especially true for data centers that support AI workloads.

Companies like Amazon Web Services, Microsoft, and Google are deploying large-scale battery storage at their data centers to prevent outages. These systems provide instant backup power, helping avoid costly downtime. They also reduce the need for diesel generators, which are expensive and produce emissions. As AI demand grows, more companies are expected to follow this approach.

As a result, storage applications are increasingly planned alongside utility infrastructure and technology investments. This trend has elevated battery storage from a supporting data point to a lead story in lithium demand.

Numbers Speak: BESS Installations and Market Growth

To put the storage boom in perspective:

- Global BESS installations exceeded 315 GWh in 2025, up about 50 percent from 2024.

- Lithium‑ion batteries remain the dominant technology in utility and industrial storage systems.

- Global battery manufacturing capacity surpassed 3 TWh per year in 2024, expanding supply frameworks for EVs and storage alike.

- The global BESS market is projected to grow strongly through 2030, supported by energy policy and grid modernization plans.

These figures show that lithium demand is no longer defined by a single industry application, but by multiple, overlapping infrastructure and technology drivers.

Lithium Demand Reimagined: Multi-Decade Opportunities

As battery storage continues to grow alongside EV adoption, the narrative around lithium demand will continue to evolve. Lithium’s role is expanding from a material tied mainly to transportation to a foundational input in energy systems and technology infrastructure.

In this new landscape, projects with deep resources, stable mine lives, and strong production profiles like NNLP are positioned to meet diversified demand over decades. Their potential to supply lithium for multiple demand drivers reflects how the market is reshaping itself.

The battery storage boom is more than a trend; it is redefining how lithium is used and valued in the global economy.

DISCLAIMER

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.