,And,Ccs")

India is making its largest public commitment yet to carbon capture technology. Finance Minister Nirmala Sitharaman announced an allocation of ₹20,000 crore over the next five years for Carbon Capture, Utilization and Storage (CCUS) technologies in the Union Budget 2026–27.

The funding, equivalent to about US$2.12 billion, aims to speed up CCUS deployment in hard-to-abate industrial sectors. These sectors are difficult to decarbonize using renewable energy alone.

The investment focuses on five major carbon-intensive industries: steel, cement, power, refineries, and chemicals. These sectors are central to India’s economic growth, but also among the largest sources of emissions.

The announcement comes from Budget documents and media like Business Standard. It matches India’s national CCUS roadmap released in December 2025.

Breaking Down India’s CCUS Strategy

CCUS refers to technologies that capture carbon dioxide (CO₂) from industrial sources. The CO₂ can either be used in products such as chemicals or stored permanently underground.

The International Energy Agency (IEA) states that CCUS is vital for sectors with hard-to-avoid emissions. This includes cement, steel, and chemicals.

India’s roadmap targets large-scale deployment in exactly these industries. According to Down to Earth, the goal is to move from pilot projects to commercial-scale systems. The timeline has three phases:

- 2025–2030: Focuses on research and pilot projects.

- 2030–2035: Centers on industrial integration and regulation.

- 2035–2045: Aims for full commercial scale-up.

Over the next five years, experts estimate CCUS capacity could reach 10–15 million tonnes (MT), and possibly up to 20 MT if execution is efficient. Even 10 MT would mark a strong early stage, according to energy consultancy M N Dastur, cited in Business Standard.

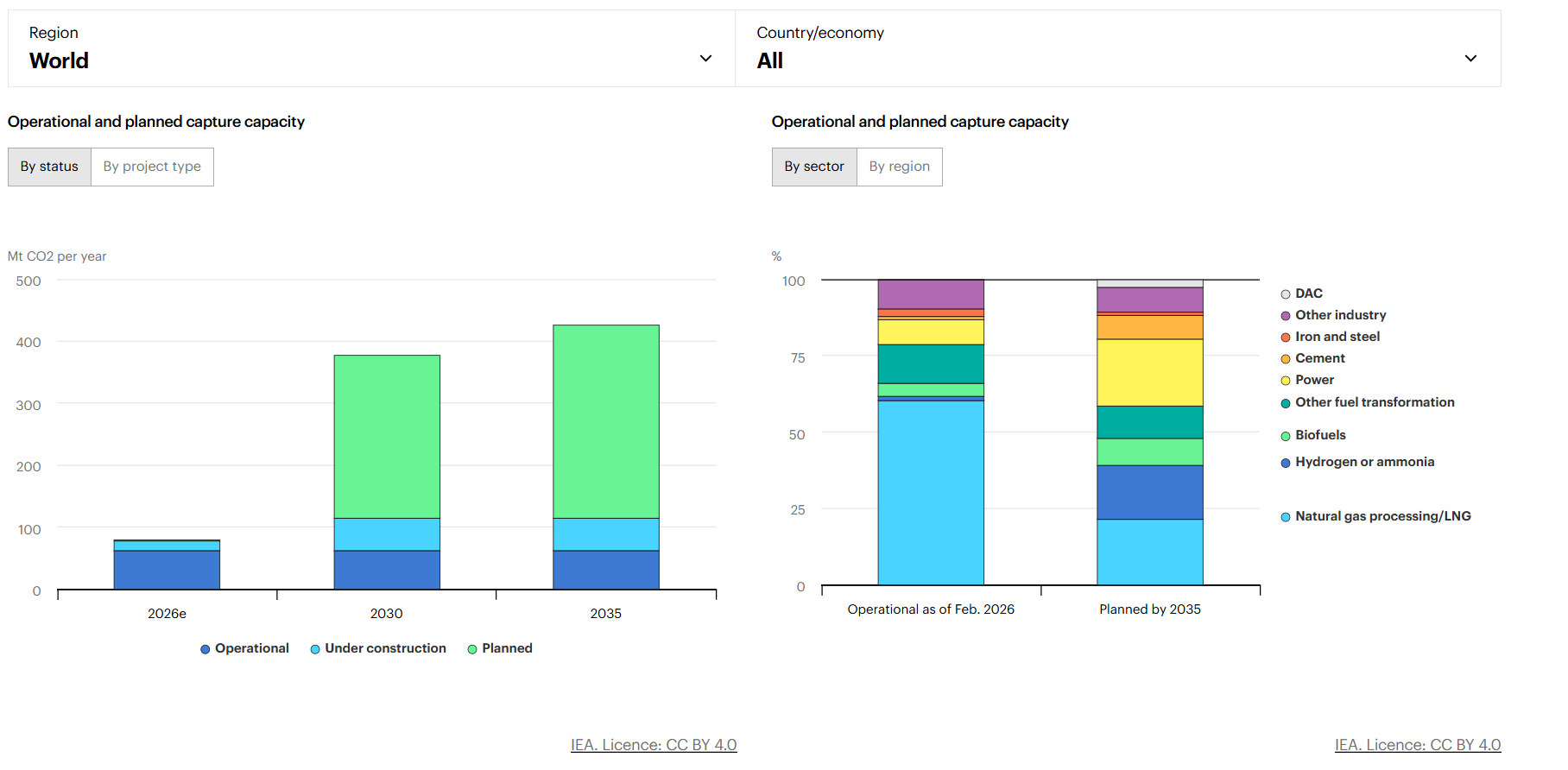

The IEA estimates that global CCUS capacity is about 50 MT each year. This means India’s planned expansion would be a significant but early step forward. The chart below shows global carbon capture capacity by status and by sector.

Why India Needs CCUS for Industrial Sectors

India’s steel and cement industries are central to its development goals, but are also major emission sources. The Council on Energy, Environment and Water (CEEW) reports that these two sectors make up 19% of India’s total emissions and 53% of industrial emissions. Within this, steel contributes about 300 MT CO₂ (33%), while cement contributes around 230 MT CO₂ (25%).

Demand is also expected to rise sharply. Research from The Energy and Resources Institute (TERI) and the World Business Council for Sustainable Development (WBCSD) shows that steel and cement demand may rise 3–4 times by 2050. If no action is taken, emissions in these sectors could nearly triple.

Both industries rely on fossil fuels. Over 90% of their energy comes from coal, petroleum coke, and other fossil sources.

In cement production, emissions come mainly from two sources. About 50–55% comes from calcination of limestone, while 30–35% comes from fuel combustion, according to Chemistry World. This makes cement especially difficult to decarbonize using renewable energy alone.

Studies show that CCUS could cut emissions in steel and cement by up to 56%. This makes it one of the few scalable solutions for process emissions.

Global CCUS Boom Adds Pressure and Momentum

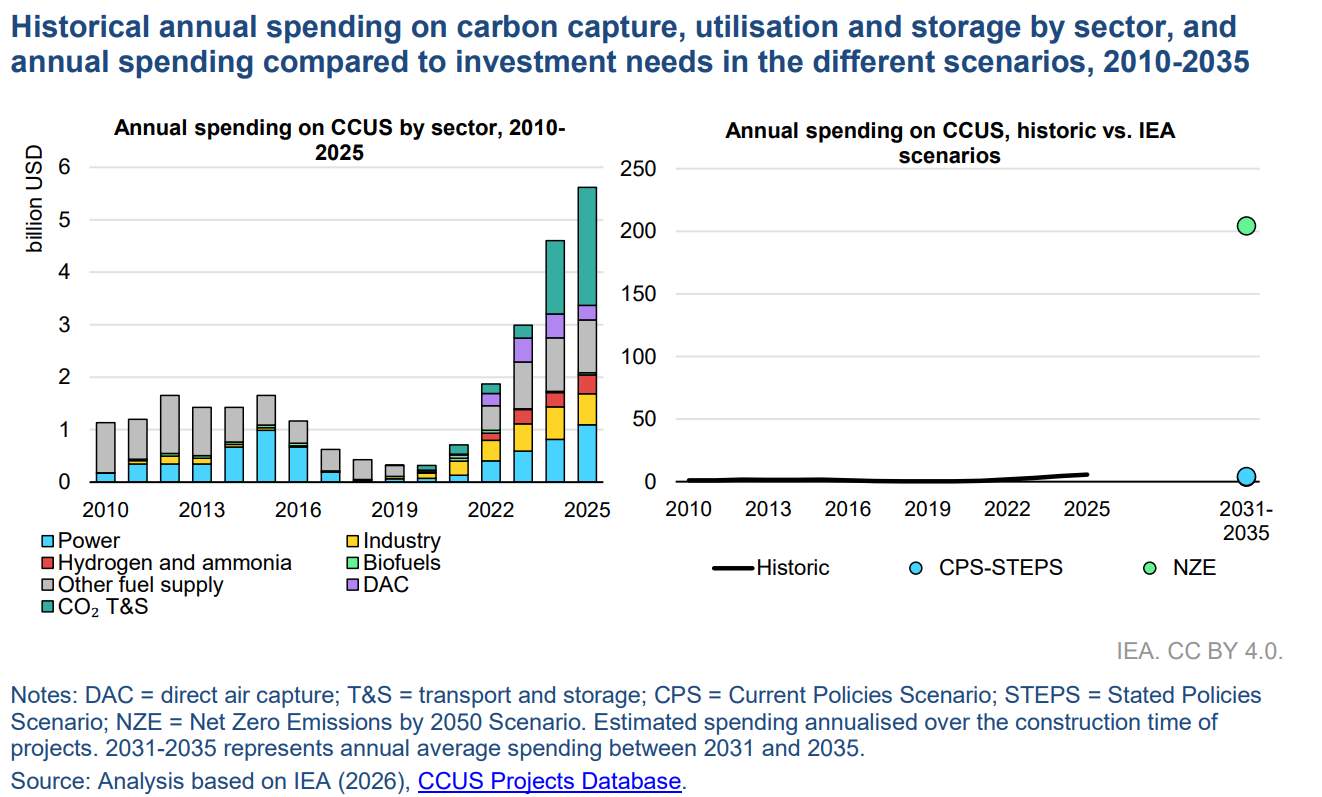

India’s push comes as global investment in CCUS accelerates. According to the IEA, global CCUS investment has increased more than 15 times since 2020 and reached over $5 billion in 2025. Operational capacity is expected to nearly double by 2030.

Over $27 billion in projects are in advanced planning stages. That’s almost double the investment in all CCUS projects since 2010. The IEA reports that more than 30 final investment decisions (FIDs) were made in just the last two years. This shows that private sector confidence is growing.

However, CCUS remains expensive. In India, capturing 1 MT of CO₂ per year is estimated to cost ₹900 crore–₹1,000 crore. ₹1 crore is equivalent to almost US$106,000 as of this writing.

Based on this, scaling to 10 MT could require around ₹15,000 crore (around US$1.6 million) in investment, which is close to the government’s planned allocation.

The IEA highlights that CCUS growth needs strong policy support, tax incentives, and carbon pricing. Without these, the economy will remain challenging.

Policy Push Meets Market Reality: Costs and Carbon Border Taxes

India’s CCUS push is also shaped by global trade pressure. One major factor is the European Union’s Carbon Border Adjustment Mechanism (CBAM), which places tariffs on imports based on their carbon content. This includes steel, cement, and chemicals.

For Indian exporters, this creates pressure to reduce emissions or risk losing competitiveness in European markets. CCUS is one of the few technologies that can directly reduce embedded carbon in heavy industry exports.

The CCUS roadmap also connects to India’s wider innovation goals. This includes the ₹1 lakh crore Research, Development, and Innovation (RDI) scheme, which aims to draw in private sector investment in clean technologies.

However, major challenges remain. India is still in the pilot stage of CCUS deployment. There is limited commercial infrastructure, unclear storage site identification, and slow regulatory processes.

Experts argue that a clear national strategy is needed. This includes identifying CO₂ storage basins, simplifying licensing, and offering viability gap funding for early projects. Without this, scaling could remain slow.

Cost Debate and Competing Priorities

Despite strong policy support, CCUS remains debated among experts.

One concern is cost efficiency. Analysis from Telangana Today suggests that the ₹20,000 crore (US$2.1 million) allocation could alternatively fund 10–15 GW of solar power capacity, along with large-scale energy efficiency upgrades.

Solar energy costs in India have fallen significantly in recent years, with utility-scale projects often below ₹40 crore per MW. This makes renewables a cheaper way to cut emissions in the power sector.

There are also concerns about long-term risks. Many CCUS projects globally are still experimental. Key issues include high costs, uncertainty around long-term carbon storage, and limited proof of large-scale viability.

Some analysts also warn about carbon lock-in. This refers to continued dependence on fossil fuel industries that rely on CCUS instead of shifting fully to cleaner alternatives like electrification and renewables. Critics argue this could slow the transition to cleaner energy systems if not carefully managed.

What Success Would Mean for India’s Net Zero 2070

India’s ₹20,000 crore CCUS commitment marks a major shift in its industrial decarbonization strategy.

Unlike renewable energy, which mainly targets electricity generation, CCUS focuses on process emissions from heavy industries like steel and cement. These emissions are harder to eliminate and represent a major challenge for India’s net-zero target by 2070.

If implemented well, the investment could help build early CCUS infrastructure, support export competitiveness, and reduce emissions in key industrial sectors. It could also position India more strongly in global markets that are increasingly shaped by carbon rules like CBAM.

Globally, CCUS is gaining momentum but remains in an early scaling phase. India’s approach will test whether large public investment can turn it into a commercially viable climate solution.