Andurand Capital Management, led by renowned oil trader Pierre Andurand, has set its sights on the UK carbon market as a major growth opportunity. The fund is betting on a significant rise in UK carbon prices, with expectations that the market will outperform other cooling commodities markets in the coming months.

The UK government’s push toward stricter climate policies, combined with the country’s post-Brexit carbon market developments, is setting the stage for what could be a major price surge in carbon allowances.

The UK Carbon Pricing System: An Overview

Following Brexit in 2021, the UK has developed its own Emissions Trading System (ETS) to replace the EU’s carbon market. The UK ETS requires power plants, industrial facilities, and airlines to buy permits for each tonne of carbon they emit.

The UK carbon permits, also called carbon allowances (UKAs) or carbon credits, can be traded in the market, with prices fluctuating based on demand and policy changes. By capping the total amount of emissions allowed, the system effectively forces businesses to either cut emissions or buy allowances. As such, it becomes a key tool for reaching the country’s climate goals.

Currently, the UK carbon price trades at a discount of more than 20% compared to its EU counterpart, a gap that investors like Andurand see as a potential opportunity. The EU ETS has benefited from a series of reforms that have driven carbon prices higher. However, the UK’s system has been slower to align with these moves.

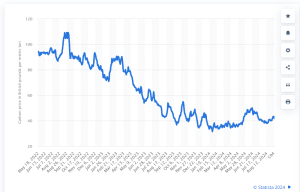

UK Allowance (UKA) Futures Pricing from May 2022 to September 2024 (in GBP per metric ton of carbon dioxide)

Remarkably, with the Labour government looking to close a £22 billion ($28.8 billion) fiscal gap and accelerate decarbonization efforts, a rise in carbon prices could benefit both the environment and government revenues.

Andurand’s Bullish Bet on UK Carbon

Mark Lewis, Andurand’s head of research and portfolio manager, believes the UK carbon price could rise by 50% in the near term. It could reach over £60 per ton, up from its current level of £42 per ton.

The price forecast is driven by several potential policy changes, which could align the UK market more closely with the EU’s, where prices have surged following moves to tighten emissions caps.

Lewis argues that the UK market presents a unique opportunity for growth, particularly as policies could potentially drive prices higher. He said in an interview that:

“This is a significant-policy driven catalyst. Those catalysts don’t exist in other markets.”

Investors are increasingly focusing on UK carbon credits as one of the most interesting opportunities in the compliance carbon market.

Major Catalysts for UK Carbon Price Surge

Interestingly, several upcoming developments could drive UK carbon prices higher and closer to EU levels.

A key factor is a potential linkage between the UK and EU ETS, allowing businesses to trade permits across both regions. This could significantly reduce the price gap.

The UK government is also considering raising the floor price for the allowances, creating a minimum price to prevent sharp declines and offer stability for businesses. Additionally, the introduction of a mechanism to remove excess permits from the market could help raise prices by limiting supply.

Another measure includes reducing the number of free allowances given to industries, which would increase demand and drive prices up. These changes, if implemented, would create a more competitive and stable carbon market. It can then encourage businesses to invest in reduction efforts and help the UK transition to a low-carbon economy more effectively.

Risks and Uncertainty

Though Andurand’s outlook on UK carbon prices is bullish, there are risks. For one, it’s unclear when these changes will be implemented, and some of the specifics remain undecided.

Key policy changes, like linking the UK and EU carbon markets, raising the floor price, and reducing free permits, lack a confirmed timeline. Additionally, demand for carbon permits has weakened due to the growth of renewable energy like wind and solar.

As more clean energy is added to the grid, fossil-fuel plants need fewer carbon permits, potentially limiting price increases. Analyst Henry Lush from Veyt highlights that while the long-term outlook is positive, short-term uncertainty could lead to price volatility before details are finalized.

Hedge Funds Betting on UK Carbon

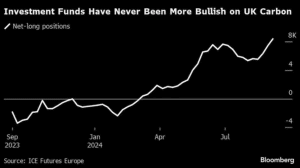

Despite the risks, hedge funds are increasingly turning their attention to the UK carbon market. At the end of last week, investment funds placed a record number of bets that the UK carbon price would increase, according to data from ICE Futures Europe. This trend highlights growing confidence that policy-driven catalysts will push prices higher, making the market an attractive opportunity for speculative investors.

The UK carbon market has the potential to mirror the EU’s success. In 2021, reforms to the EU ETS pushed the carbon price up by nearly 150%, creating lucrative opportunities for investors who had positioned themselves early. Andurand and other hedge funds are hoping to replicate that success in the UK.

The UK ETS stands at a pivotal moment, with a combination of policy changes and market dynamics likely to drive prices higher in the coming months. For investors like Andurand, the market presents a rare opportunity to profit from the energy transition while supporting the fight against climate change.

Source: McKinsey and Company

Source: McKinsey and Company

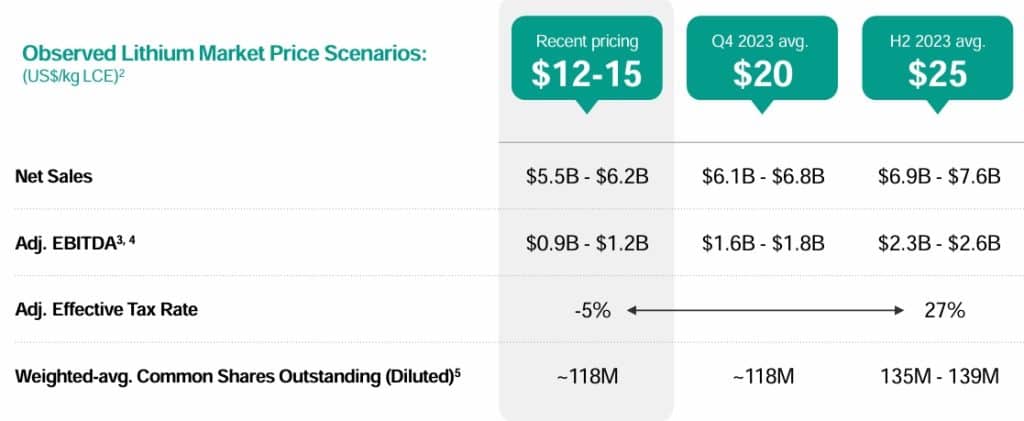

Source: Albemarle

Source: Albemarle

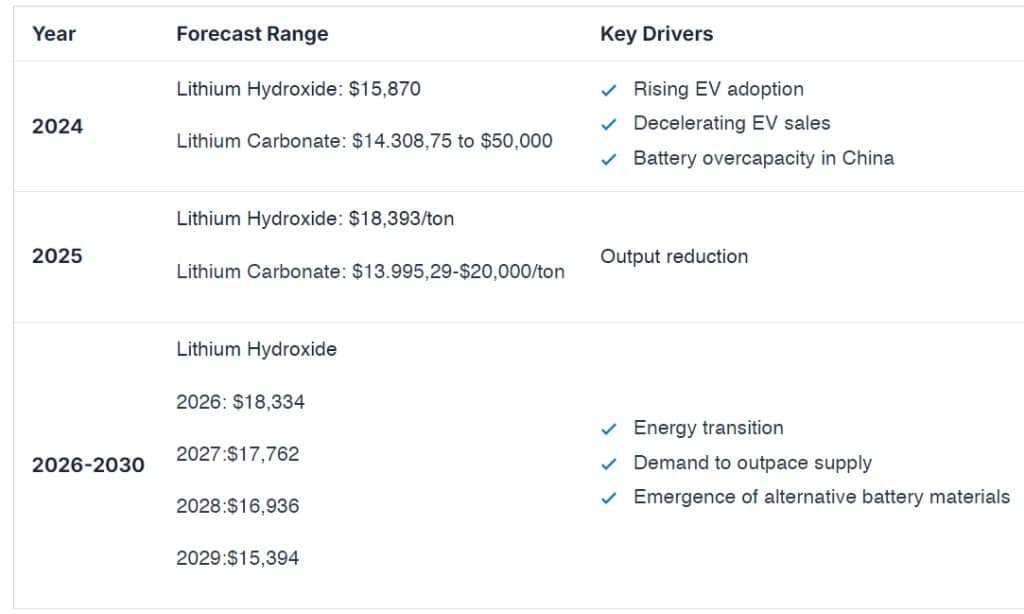

Source: Techopedia

Source: Techopedia