The carbon removal industry is expanding fast, with new projects moving from the pilot stage to the commercial scale. Companies are racing to build infrastructure that can permanently remove carbon dioxide from the atmosphere. One of them is a Canadian carbon management company, Svante Technologies, which announced that it acquired Carbon Alpha Corporation. This move brings together carbon capture technology with carbon dioxide removal (CDR) project development.

The acquisition strengthens Svante’s role in the carbon capture and storage (CCS) value chain. It also adds Carbon Alpha’s development portfolio to Svante’s operations.

Claude Letourneau, President & CEO of Svante, remarked:

“This project is a game-changer for Svante and a pivotal moment for scaling verifiable, durable engineered carbon removal solutions working in tandem with nature. By integrating Carbon Alpha’s team, we’re accelerating the delivery of high‑integrity CDR credits at commercial scale in partnership with the MLTC leadership, who is closely coordinating with us on the North Star Project.”

The North Star Project: A New Source of Carbon Removal Credits

The key asset in the deal is the North Star Bioenergy Carbon Capture and Storage (BECCS) project in Saskatchewan. The facility will capture carbon dioxide from the Meadow Lake Tribal Council Bioenergy Centre. This is how it works:

This plant produces renewable electricity and heat using forestry waste biomass from nearby sawmills.

Phase one of the project is designed to capture up to 140,000 tonnes of CO₂ per year from biomass combustion emissions.

The captured carbon dioxide will move through a dedicated pipeline to a deep saline aquifer. There, it will be stored permanently underground.

This process removes carbon from the natural cycle because biomass absorbs CO₂ while growing. Capturing and storing that carbon after combustion results in net negative emissions.

The project will generate durable carbon dioxide removal credits. Each credit represents one ton of CO₂ removed. These credits can be sold to companies seeking verified carbon removal to meet climate targets.

Carbon Alpha had already developed the project structure and storage system before the acquisition. Svante now takes over development and integration. The next step will be a front-end engineering design (FEED) study and test-well drilling program. A final investment decision is expected in early 2027.

Industry analysts say deals like this show how the carbon removal sector is shifting from research to deployment. Companies are now building full systems that include capture, transport, and long-term storage.

The acquisition expands Svante’s strategy to build an integrated carbon management company. It develops modular carbon capture systems that use nanoengineered solid sorbent filters to capture CO₂ from industrial emissions.

The technology is designed for industries that are difficult to decarbonize. These include cement, steel, hydrogen production, and power generation.

Before the acquisition, Svante already had expertise in capture technology. Carbon Alpha adds expertise in project development, geological storage, and carbon credit generation. This combination creates a full value chain for CCS in Canada:

Capture CO₂ from industrial sources or biomass energy

Transport the CO₂ through pipelines

Store the carbon permanently underground

Generate verified carbon removal credits

Industry experts say this type of integration is important. Carbon removal projects often fail because separate companies handle capture, storage, and financing.

The strategic acquisition includes Carbon Alpha’s development expertise, North Star Carbon Solutions LP’s ownership structure, and eligibility for Canada’s 50% CCUS investment tax credit, positioning Svante to scale multiple BECCS projects rapidly.

By combining these elements, Svante aims to scale projects faster.

First Nations Partnership Anchors the Project in Saskatchewan

The North Star project is being developed in partnership with the Meadow Lake Tribal Council (MLTC). The organization represents nine First Nations communities in northwest Saskatchewan.

Under the project structure, MLTC will be a co-owner of the BECCS facility alongside Svante. The partnership focuses on three main goals: local economic development, job creation, and long-term environmental leadership.

The bioenergy facility already produces renewable electricity and heat using forestry residues. The carbon capture system adds another layer of value. It turns the facility into a carbon removal hub that can produce verified CDR credits.

The project also includes the development of a regional CO₂ pipeline and storage hub. This infrastructure could support other emitters in the region.

Biogenic carbon sources from forestry, agriculture, or bioenergy plants could connect to the same storage network. This approach could turn the region into a carbon removal cluster.

Global Demand for Carbon Removal Is Rising Fast

The acquisition comes at a time when demand for carbon removal is increasing worldwide. Most countries now include carbon removal in long-term climate plans. Industry groups expect global carbon removal markets to reach hundreds of millions of tonnes of capacity by the 2030s.

Source: McKinsey & Company

Boston Consulting Group (BCG) outlines three demand scenarios for 2030–2040: low (40–80 MtCO₂/year), medium (70–230 MtCO₂/year), and high (200–870 MtCO₂/year). McKinsey also estimates durable CDR demand could hit 100 MtCO₂ by 2030, with announced supply at ~50 MtCO₂, creating a supply-demand gap.

The Intergovernmental Panel on Climate Change says that limiting global warming to 1.5°C will require removing billions of tonnes of CO₂ annually by mid-century. Many climate models further show that 5 to 10 billion tonnes of carbon removal per year may be needed by 2050. That translates to between $6 – $16 trillion of investment by mid-century.

Today, global carbon removal capacity is still very small. Most engineered projects remove only thousands or tens of thousands of tonnes annually.

However, investment is rising quickly. Major corporations such as Microsoft, Stripe, and Alphabet have signed large contracts for high-quality carbon removal credits.

Governments are also supporting the sector. In Canada, carbon capture projects can receive financial support through the CCUS investment tax credit. This covers up to 50% of eligible capture equipment costs, depending on project type. These incentives aim to help scale early infrastructure.

Source: Natural Resources Canada.

At 140,000 tCO₂/year, North Star Phase 1 represents about 35x the capacity of Climeworks‘ Orca plant. It also aligns with Microsoft‘s annual CDR purchasing scale, demonstrating commercial viability for durable removal credits.

Why BECCS Is a Key Carbon Removal Technology

Bioenergy with carbon capture and storage is one of the most widely studied carbon removal technologies. BECCS combines three steps:

Biomass absorbs CO₂ while growing.

The biomass is used to produce energy.

Carbon emissions are captured and stored underground.

This creates net negative emissions. The technology also produces electricity or heat, which can improve project economics. However, large-scale BECCS projects require several conditions, including:

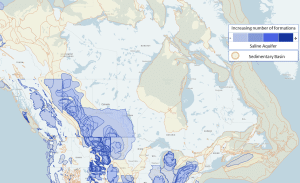

Canada has strong potential for BECCS development because of its forestry resources and suitable geological formations. Western Canada already hosts major CCS infrastructure. For example, large carbon storage reservoirs exist in Alberta and Saskatchewan.

Map of Canada showing saline formations and sedimentary basins

Data source: North American Carbon Storage Atlas. Image from Natural Resources Canada.

This geological capacity could store billions of tonnes of CO₂ over time. Developers say regional storage hubs will be essential for scaling carbon removal.

The Next Phase for Carbon Removal Infrastructure

The acquisition of Carbon Alpha marks an important step in the industrialization of carbon removal. Instead of isolated pilot projects, companies are now building complete carbon management systems.

For Svante, the deal strengthens its ability to build and operate large carbon removal projects. For the broader market, it shows how carbon removal is moving from concept to infrastructure.

As governments and companies push toward net-zero targets, the demand for durable carbon removal credits is expected to keep rising. Projects like North Star may become an important part of the global climate strategy.

A war in the Middle East may increase demand for carbon credits if it continues for a long time. Analysts say energy supply disruptions from the conflict could push some industries back to higher‑emission fuels like coal. This, in turn, could raise emissions and force companies in regulated markets to buy more carbon credits.

The Middle East conflict has already disrupted liquefied natural gas (LNG) supplies. Qatar, a top LNG producer, has halted output at its largest LNG plant. This is due to disruptions in transport routes through the Strait of Hormuz. Qatar supplies about 20% of global LNG output.

LNG provides cleaner fuel for power generation than coal. When gas costs rise sharply or supply is limited, utilities sometimes increase coal use to meet electricity demand. Higher coal use increases carbon emissions. This can lead to higher demand for carbon credits in compliance markets.

Carbon Credits 101: How the Market Responds

A carbon credit represents one tonne of greenhouse gas emissions reduced, avoided, or removed from the atmosphere. Companies must hold carbon credits to meet emissions limits in regulated markets. These markets are part of government climate policy.

Compliance carbon markets, like emissions trading systems (ETS), require companies to lower their emissions. If they can’t, they must buy credits to stay within a limit.

Over 113 carbon pricing systems are in use worldwide. This includes ETS and carbon taxes, which cover about 28% of global greenhouse gas emissions.

In compliance markets, rising emissions usually increase demand for allowances or carbon credits. If companies cannot reduce emissions fast enough, they buy credits to stay compliant. Strong or rising demand can also influence credit prices.

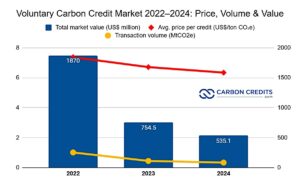

Voluntary carbon markets exist separately from compliance markets. In voluntary markets, companies buy credits to meet internal climate goals, not legal limits.

The voluntary market is smaller but growing. The global voluntary carbon credit market is expected to rise from $1.88 billion in 2025 to $2.29 billion in 2026. It could reach $4.92 billion by 2030.

From Gas to Coal: When Utilities Flip the Switch

The Middle East conflict has pushed energy prices higher. Global natural gas and oil prices climbed because of risks to supply routes such as the Strait of Hormuz, a key passage for crude oil and LNG.

Source: TradingView

When gas prices rise, utilities may switch from gas‑fired generation to coal, which is cheaper but emits more CO₂. Analysts observed that fuel switching happened in 2022 after Russia invaded Ukraine. European gas supply was disrupted, so utilities turned to burning more coal.

Coal prices have also risen in response to supply pressures. Some markets saw thermal coal prices climb about 26%, reaching highs not seen in more than two years.

Source: Trading Economics

Such shifts can put pressure on emissions limits in regulated markets. Higher emissions would require companies to buy more compliance credits to avoid penalties. This dynamic is central to why analysts say carbon credit demand could rise if disruptions persist.

Compliance Markets Under Pressure, So Who Pays the Price?

Compliance carbon markets form the largest portion of carbon credit demand. These include emissions trading systems in Europe, China, and the U.S., and expanding carbon pricing schemes globally. The Middle East conflict could affect these markets, which shows how energy security and climate policy are connected.

Demand for carbon credits depends on how countries and companies aim to meet climate goals, like those in the Paris Agreement. This agreement aims to limit global warming to below 2°C. Compliance markets set legal limits, and voluntary markets support corporate climate goals.

If more companies switch to coal, emissions per unit of energy could go up, and compliance markets might see a higher demand for allowances or credits. This happens as companies try to stay within legal limits. This could result in higher carbon prices and tighter markets, depending on how regulators respond.

Source: GECF

Here is a sample scenario for better understanding:

Coal’s higher emissions factor (~0.35 tCO2/MWh vs. gas’s ~0.20 tCO2/MWh, per IPCC data) means switching boosts shortfalls against free allocations (often benchmarked low, e.g., 0.3 tCO2/MWh). Using this estimation, a firm generating 1 million MWh yearly will have this result:

This scenario creates ~46,000 extra allowances demanded firm-wide, scaling market-wide with multiple switchers.

In the European Union Emissions Trading System (EU ETS), companies must hold allowances equal to their emissions, or face fines. The EU is considering reforms to improve market stability and balance supply and demand for allowances. This scheme has been a key tool for reducing emissions in Europe since 2005.

In addition, more sectors are entering compliance markets. For example, China’s national ETS covers key industrial sources. It accounts for a big part of emissions from the world’s largest emitter.

Any rise in emissions from fuel switching could increase demand in these established markets. However, the exact impact will depend on how long energy disruptions continue and whether regulators adjust compliance caps or other rules.

Voluntary Market Volatility: Green Goals on Hold?

Global carbon pricing revenues topped over $100 billion in 2023 and in 2024. The World Bank reports that around $69 billion came from emissions trading systems and $33 billion from carbon taxes. This amount covers nearly 24% of global greenhouse gas emissions, which reflects the growing scale of these markets.

While compliance demand may rise if emissions increase, the outlook for the voluntary market could differ.

According to analysts, an energy crisis may temporarily constrain corporate spending on voluntary credits. High energy prices raise operating costs. This may lead companies to delay voluntary purchases as they will focus more on their core operations instead.

High-integrity voluntary markets have grown recently. This growth is driven by corporate net-zero commitments and new standards. Companies increasingly seek credits that meet quality criteria such as compliance eligibility, durability, and third‑party verification.

Sudden economic strains or changes in energy costs could quickly change how companies buy.

The Ripple Effect: Energy Security Meets Climate Action

A prolonged Middle East conflict could have ripple effects beyond energy prices. Disruptions to LNG supply may push some utilities toward higher‑emission fuels, raising emissions levels. That could drive demand for carbon credits in regulated markets where companies must meet emissions limits.

At the same time, short‑term pressures from high energy costs could slow voluntary demand as companies focus on operational priorities. The overall direction of carbon credit demand will depend on the duration of energy supply disruptions, policy responses by regulators, and the pace of the global energy transition.

Carbon markets are an evolving part of climate policy, linking energy markets and climate goals. As energy security concerns grow, the role of carbon credits in balancing compliance and emissions reductions may attract more attention from policymakers, investors, and companies in the coming years.

Disseminated on behalf of Alaska Energy Metals Corporation.

Nickel prices remained flat today (May 25, 2026), with global benchmarks holding at $18,859.97 per ton and Chinese markets at ¥127,951 per ton. This 0.00% change reflects a market tug-of-war. While tight Indonesian mining quotas and dropping LME inventories provide a strong price floor, an elevated global visible surplus and weak Chinese stainless steel demand cap upward momentum. These structural supply constraints are perfectly balanced by sluggish consumption, resulting in stagnant sideways trading.

The global nickel market enters 2026 after a bruising and uneven year. In 2025, macroeconomic stress, trade disruptions, and deep supply imbalances reshaped pricing and sentiment. Although short-term rallies have returned, the underlying structure of the market remains fragile. As a result, 2026 is shaping up to be a year defined by volatility rather than a sustained recovery.

A Challenging Backdrop from 2025

To understand where nickel is headed, it helps to revisit the environment it emerged from. In 2025, global trade flows came under pressure after the US implemented new tariff policies. These measures disrupted supply chains and dampened confidence across industrial commodities. At the same time, global manufacturing growth slowed, weighing heavily on the broader nonferrous metals complex.

SMM reported highlighted some significant points. Adding to the uncertainty, the US Federal Reserve sent mixed signals throughout the year. Expectations around interest rate cuts shifted repeatedly. Each change altered risk appetite and triggered sharp moves across commodity markets. Nickel, already vulnerable due to oversupply, struggled to attract sustained buying interest.

China attempted to offset some of these pressures. Policymakers rolled out proactive fiscal measures and maintained a moderately accommodative monetary policy. They also focused on boosting domestic demand and diversifying export routes to reduce exposure to trade frictions. In July, China introduced its “anti-involution” policy, aimed at curbing destructive price competition across industries.

Even so, nickel underperformed. While other nonferrous metals showed mixed results, nickel remained constrained by a clear mismatch between supply and demand. Prices trended lower for most of the year. LME nickel opened near $15,365 per tonne and slid to lows around $13,865 per tonne, marking a sharp reset in the price center.

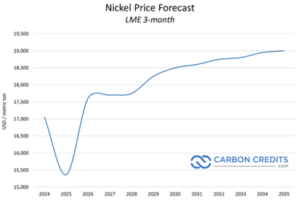

2026 Nickel Price Outlook: A Volatile Start to the New Cycle

Momentum shifted suddenly toward the end of the year. From mid-December, nickel prices began climbing rapidly.

By early January, LME prices had surged past $18,000 per tonne, the first time in more than a year. In just 12 trading sessions, prices jumped nearly 20%, catching many traders off guard.

Several factors fueled this rebound. Demand signals from China improved modestly, particularly from stainless steel mills and EV battery producers. At the same time, speculative positioning adjusted as supply risks from Indonesia returned to the spotlight.

Trading Economics analysis stated that Indonesia, the world’s largest nickel producer, hinted at a potential 34% reduction in output for this year. Meanwhile, Vale temporarily halted operations at its Pomalaa and Bahodopi mines while waiting for regulatory approvals. Although its flagship Sorowako mine continued operating, these pauses added to market caution.

Still, the rally faced clear limits. Inventory levels remained elevated. Combined LME registered and off-warrant stocks jumped nearly 58% last year, reaching more than 367,000 tonnes. In addition, large shadow inventories in Singapore and Kaohsiung continued to hang over the market. As a result, every price spike met resistance.

Price Expectations Remain Capped

Most analysts expect nickel prices to settle into a narrow band rather than trend sharply higher. Forecasts largely cluster between $15,000 and $16,000 per tonne. Several major institutions attribute the restrained outlook to ongoing surpluses.

Trading Economics data indicated that nickel futures moved back up to nearly $17,800 per tonne, reversing last week’s steep decline as buyers stepped back into the market.

Analysts consider that the differences in price forecasts primarily reflect contrasting views on how strictly Indonesia will enforce production limits and how quickly global manufacturing activity is expected to recover.

Stainless steel: remains the dominant driver, accounting for about 70% of total demand. Consumption may rise to roughly 2.45 to 2.5 million tonnes. China’s production recovery offers support, while infrastructure projects in emerging markets add incremental demand. Still, no major surge is expected.

Battery and EV application: They make up roughly 13% to 15% of demand. Nickel use in this segment could reach up to 500,000 tonnes. High-nickel cathodes continue to support premium EV models.

According to Benchmark Mineral Intelligence, demand for battery-grade nickel is expected to surge, tripling by 2030. This growth will largely be due to mid- and high-performance EVs in Western markets.

Other uses, including alloying, plating, aerospace, and electronics, provide steady but smaller contributions. A broader manufacturing recovery and net-zero investments could lift demand slightly, while faster EV adoption remains the main upside risk.

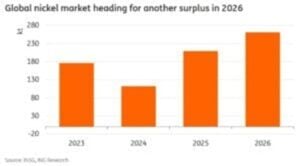

According to SMM, the nickel market will remain oversupplied through the year, remaining between 120,000 and 275,000 tonnes. While short-term rallies may continue, oversupply will remain the dominant force.

On the supply side, Indonesia’s refined nickel output stays high, supported by sunk investments and low operating costs. On the demand side, growth remains steady but unspectacular.

Source: AEMC

Ewa Manthey, a commodities strategist at London-Based ING Group, explained that the global nickel market is still set to remain oversupplied, with a projected surplus of about 261,000 metric tonnes. As a result, any production cuts would need to be deep and sustained to meaningfully shift market fundamentals.

China’s real estate support policies may provide limited relief for stainless steel consumption. However, a strong housing rebound appears unlikely, and any improvement is expected to be gradual. Similarly, demand from ternary batteries faces structural headwinds. Solid-state batteries remain years away from large-scale commercial use, and near-term battery chemistry trends do not favor a sharp jump in nickel intensity.

As a result, the average price level may drift lower over time. Tightening ore supply could briefly push prices above $16,000 per tonne. However, high inventories and excess capacity will take longer to absorb.

Why Nickel Matters for US Critical Mineral Independence?

Nickel plays a critical role in military-grade alloys, advanced weapons systems, electric vehicle batteries, grid-scale energy storage, and broader clean energy infrastructure. Despite its importance, the United States remains almost entirely dependent on imports for nickel, while China controls much of the global processing and supply chain. This reliance has become a clear strategic risk, one that domestic resources need more exploration.

And this is the reason America’s push to secure its critical mineral supply is gaining real momentum.

Spotlight: Alaska Energy Metals – America’s Nickel Backbone

At the center of this shift is Alaska Energy Metals Corporation (TSX-V: AEMC, OTCQB: AKEMF) and its Eureka deposit, the largest documented nickel resource in the United States. As Washington intensifies efforts to reshore critical supply chains for national security and clean energy goals, AEMC’s Nikolai Project in Alaska is steadily gaining recognition as a strategic domestic asset.

At the same time, the project aligns closely with the Trump administration’s executive orders focused on critical minerals and Alaska resource development. Those directives sought to speed up domestic production, curb reliance on foreign suppliers, and reinforce US security interests.

Against this backdrop, Nikolai stands out as a fully US-based “Sulphide nickel and battery metal project” to meet the country’s metal needs for the energy transition. Significantly, it has two claim blocks: Eureka and Canwell.

Source: AEMC

Eureka: The Largest Known Nickel Resource in the US

The Eureka deposit is not just large—it is nationally strategic. It hosts nickel alongside copper, cobalt, chromium, iron, and platinum group metals, including platinum and palladium. This metal mix makes Eureka highly relevant for both defense systems and the expanding clean energy economy.

According to the 2025 Mineral Resource Estimate, Eureka contains:

Indicated Resource of 814 million tonnes grading 0.42% nickel equivalent, representing 5.62 billion pounds of nickel in situ.

Inferred Resource of 896 million tonnes grading 0.39% nickel equivalent, totaling 9.38 billion pounds of nickel in situ.

Combined, the deposit contains more than 15 billion pounds of nickel, enough to support American demand for decades.

FAST-41 Listing Accelerates the Nikolai Project

A major step forward came when the Nikolai Project was accepted onto the FAST-41 Transparency Dashboard by the Federal Permitting Improvement Steering Council.

The initial phase focuses on infrastructure upgrades, including rehabilitation and extension of the Rainy Creek Mining Trail, installation of temporary bridges, and development of an on-site camp.

These improvements will lower exploration costs, improve safety, enable better site access, and speed up the transition to advanced exploration and development at Eureka. Just as important, FAST-41 provides transparency, inter-agency coordination, and defined permitting milestones.

Source: AEMC

Live Nickel Spot Price

Unit: USD/Tonne

---

---

Loading Chart...

Key catalysts ahead

AEMC is entering a phase with several near- and mid-term value drivers. These include a first-pass metallurgical study to assess metal recovery, the potential for a major US Department of Defense grant, completion of a Preliminary Economic Assessment, and continued drilling at the Angliers target. Each step strengthens the investment and strategic case for Eureka.

Nickel Oversupply Overseas, Opportunity in the US

In summary, the nickel market faces another complex year. Structural oversupply, elevated inventories, and cautious demand growth define the landscape. Although policy shifts in Indonesia and short-term demand improvements can trigger sharp rallies, fundamentals continue to cap sustained upside. For now, nickel remains a market driven more by volatility than by balance.

As the US rebuilds its domestic critical mineral supply chain, assets like Eureka are becoming indispensable. With its scale, multi-metal profile, federal permitting support, and alignment with national policy priorities, Alaska Energy Metals Corporation is positioning itself as a key player in America’s push for resource security. In a world increasingly defined by competition for critical metals, Eureka has the potential to become the backbone of the US nickel supply for generations.

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Alaska Energy Metals. (“Company”) made a one-time payment of $90,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: .

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Nickel prices remained flat today (May 25, 2026), with global benchmarks holding at $18,859.97 per ton and Chinese markets at ¥127,951 per ton. This 0.00% change reflects a market tug-of-war. While tight Indonesian mining quotas and dropping LME inventories provide a strong price floor, an elevated global visible surplus and weak Chinese stainless steel demand cap upward momentum. These structural supply constraints are perfectly balanced by sluggish consumption, resulting in stagnant sideways trading.

Nickel has moved from being a niche industrial metal to a critical pillar of the global energy transition, along with copper, lithium, and uranium.

Once primarily used in stainless steel, nickel is now critical for high-energy-density batteries, electric vehicles (EVs), grid storage, aerospace alloys, and emerging hydrogen infrastructure.

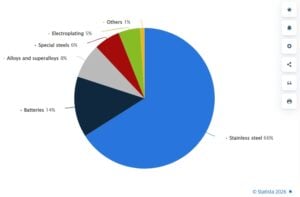

Essentially, it’s now another mineral on that list, albeit one that seems to have largely flown under most investors’ radars thus far. However, it’s understandable why that’s been the case – after all, the primary use for mined nickel has long been industrial, with over three-quarters of global nickel demand being for things like alloy production or electroplating.

Distribution of primary nickel consumption worldwide in 2024, by industry

Nickel Basics: Types, Grades, and Industrial Uses

Nickel is a silvery-white transition metal with high corrosion resistance, ductility, and thermal stability. Its unique properties make it indispensable in alloys and electrochemical applications.

Nickel is generally classified into two main categories:

Class 1 nickel: High-purity nickel metal, powders, briquettes, and salts such as nickel sulfate. These are essential for battery cathodes, advanced alloys, and aerospace applications.

Class 2 nickel: Ferronickel and nickel pig iron (NPI), primarily used in stainless steel production.

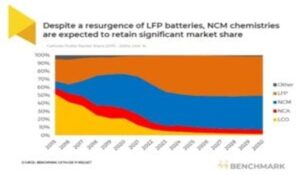

Historically, stainless steel accounted for roughly two-thirds of nickel consumption, providing a stable demand base. However, batteries have emerged as the fastest-growing segment, particularly for nickel-rich cathode chemistries such as NMC (nickel-manganese-cobalt) and NCA (nickel-cobalt-aluminum).

Aerospace, defense, and superalloys also rely heavily on nickel for high-temperature and corrosion-resistant applications.

This dual-market nature—spanning bulk industrial use and high-tech energy transition applications—makes nickel one of the most structurally complex metals in the critical minerals ecosystem.

Nickel Processing Technologies: The Backbone of the EV and Steel Boom

Not all nickel is equal, and processing technology determines where it ends up. Nickel processing is the set of industrial methods used to extract nickel from its ores and turn it into usable forms for various industries, including stainless steel, batteries, and alloys. Essentially, it’s how raw nickel in rocks becomes the high-purity metal or chemical compounds needed for manufacturing.

Nickel is mined mainly from two types of ores:

Sulfide ores – Found deep underground, easier to process, high purity.

Laterite ores – Found near the surface, lower nickel content, more challenging to process.

The Case Of Battery Grade Nickel

In order to be used in an electric vehicle, nickel must first be refined to extremely high purities, creating what’s known as “battery grade” nickel. Following this, it then needs to be dissolved in sulphuric acid to create nickel sulphate, which can then be used to produce battery cathodes.

Nickel’s high energy density, which allows it to hold more charge for less weight, makes high-nickel battery chemistries more desirable in EV batteries. While the first iterations of the lithium-ion battery used equal proportions of nickel, manganese, and cobalt, modern ones use as much nickel as manganese and cobalt combined.

And as technology continues to progress, it’s expected that the ratio will rise to as much as 80% nickel, or even more.

Now here’s a simple breakdown of the processing technologies:

Pyrometallurgy Still Dominates Stainless Steel

High-temperature smelting remains the most common route for nickel extraction. Rotary kiln–electric furnace (RKEF) and flash smelting convert sulfide and laterite ores into ferronickel or nickel pig iron (NPI). These products suit stainless steel, but they consume large amounts of energy and emit significant CO₂.

Notably, NPI and ferronickel continue to anchor global supply.

Hydrometallurgy Powers Battery-Grade Nickel

Hydrometallurgical routes, especially high-pressure acid leaching (HPAL), are becoming critical for EV batteries. HPAL converts laterite ores into mixed hydroxide precipitate (MHP) and then into nickel sulfate for cathodes.

Refining and Recycling Gain Momentum

Electrorefining and solvent extraction deliver high-purity Class 1 nickel. Refined products made up around 60% of the nickel market in 2024. Recycling is also rising as a low-carbon supply source.

In short, nickel processing is splitting into two markets: low-cost NPI for steel and high-purity nickel for batteries. This divide is reshaping supply chains, investment flows, and decarbonization strategies across the metals industry.

The Volatile Nickel Price Cycle

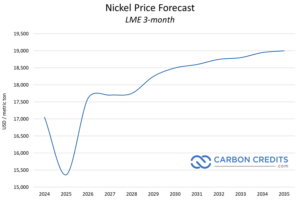

Unlike lithium, the nickel market is much more complex. The metal sits at the crossroads of geopolitics, industrial demand, and changing battery technology. Over the past five years, nickel prices have been highly volatile.

For example, during the 2022 LME squeeze, prices spiked above $100,000 per tonne. Then they dropped sharply to around $13,900 per tonne in early 2025.

Since then, they have started to recover, reaching about $17,200 per tonne by February 2026.

This volatility shows how sensitive nickel is to supply, demand, and global events. As EV demand grows, the nickel market will continue to face swings.

This volatility reflects a structural mismatch between supply expansion and shifting demand patterns. Massive Indonesian production growth has flooded the market, while battery chemistry trends toward lithium iron phosphate (LFP) have reduced nickel intensity in mass-market EVs. At the same time, premium EVs and aerospace applications continue to rely heavily on Class 1 nickel, creating a bifurcated market structure.

For investors, policymakers, and corporates, nickel represents a critical test case for the energy transition economy. Understanding its supply chain, macro drivers, and long-term price scenarios is essential for navigating the next decade of critical minerals markets.

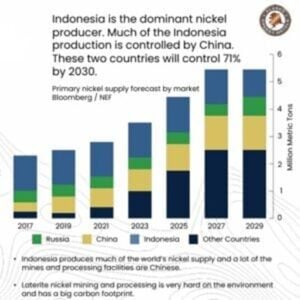

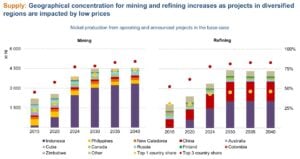

Global Nickel Supply: Indonesia’s Dominance and Market Impact

Source: IEA

Indonesia has reshaped the global nickel market more than any other country. In 2024, its nickel in mine production was 2.2 million tonnes (mt), an increase of 158% over the previous five years. Its rise was fueled by a combination of raw-ore export bans, massive Chinese-backed investments in downstream processing, and the rapid deployment of high-pressure acid leach (HPAL) facilities for battery-grade nickel.

By consolidating both mining and smelting, Indonesia has established a vertically integrated nickel ecosystem capable of supplying both stainless steel and battery markets at low cost.

Policy Controls and Quota Management

Despite its dominance, Indonesia’s nickel supply faces tightening government controls in 2026. The government sharply reduced the nickel ore production quota (RKAB) to 250–260 million wet metric tonnes (wmt), down from 379 million wmt in 2025 and 298 million wmt initially approved for 2025—a cut of roughly 34%.

The move aims to align ore output with domestic smelter capacity, curb oversupply, and support prices. Following the announcement, LME nickel prices surged past $18,000/t before stabilizing near $17,200/t in February 2026.

Delays in RKAB approvals have already halted operations at mines such as PT Vale Indonesia, signaling enforcement risks for the policy. Meanwhile, demand growth is tempered by slower stainless steel uptake and the structural shift toward LFP batteries, which has helped sustain a global surplus forecast of 261–288 kt in 2026 despite production cuts.

Indonesia’s strategic approach—resource nationalism, controlled expansion, and downstream integration—has fundamentally altered global nickel pricing. Low production costs and government-backed industrial policy allow Indonesian producers to remain profitable even during periods of weak prices.

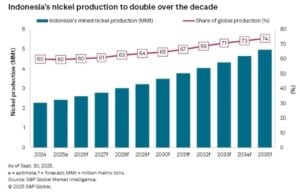

However, S&P Global noted that, “Indonesia is still projected to more than double its production over the next decade to an estimated 4.97 MMt by 2035.”

Source: S&P Global

China’s Role in the Nickel Supply Chain

China continues to dominate the processing of nickel intermediates and battery materials. Chinese firms have financed and built much of Indonesia’s upstream infrastructure, including HPAL plants and mixed hydroxide precipitate (MHP) facilities.

It is also the single largest consumer of nickel, driven by domestic stainless steel production and battery manufacturing. Policy shifts, stimulus measures, and industrial planning decisions in China have an outsized impact on global nickel markets, influencing both price and supply chain dynamics.

Other Global Producers

Beyond Indonesia and China, major nickel-producing countries include Russia, the Philippines, Canada, Australia, and New Caledonia. However, many high-cost producers have struggled to compete with Indonesia’s integrated, low-cost production model. For example, BHP suspended operations at its Nickel West facility in Western Australia amid persistent low prices, highlighting the competitive pressures faced by high-cost producers.

This dynamic has accelerated consolidation in the global nickel industry, with strategic repositioning focused on securing downstream processing and high-grade nickel for energy transition applications.

Nickel Demand Dynamics: Stainless Steel vs. Batteries

Stainless Steel: The Legacy Anchor

Stainless steel remains the primary driver of nickel demand, accounting for roughly two-thirds of consumption. Demand is closely tied to construction, infrastructure, and manufacturing activity. China, the world’s largest stainless steel producer, remains a key macro driver for nickel demand globally.

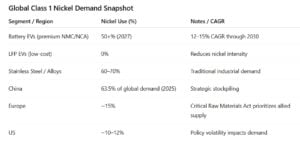

Class 1 Nickel: Powering the EV Boom

Nickel demand for batteries has grown fast over the past decade. Class 1 nickel, with purity above 99.8%, is key for high-energy NMC and NCA batteries. These batteries power premium EVs, giving longer driving ranges and lighter, more efficient vehicles. Advanced cathodes now contain 60–80% nickel, with some designs targeting 90%+ nickel content.

By 2030, nickel-heavy batteries could reach 1,320 MWh globally, covering about 80% of all EV lithium-ion batteries. Battery demand is expected to use over 50% of Class 1 nickel by 2027, growing at 12–15% per year. The average EV battery now contains 28–30 kg of nickel.

But there are risks:

LFP batteries, which contain no nickel, are growing in lower-cost EVs, especially in China. Nickel intensity per vehicle has fallen nearly one-third since 2020.

Policy differences affect supply: China held 63.5% of global nickel demand in 2025, Europe prioritizes allied supply, and US policies are less stable.

Source: Crux Investor

The Lights Are Green for Nickel

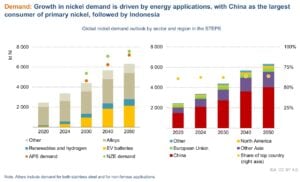

Forecasts from the International Energy Agency (IEA) project nickel demand more than doubling by 2035 under current pledges, potentially tripling in net-zero scenarios driven by EVs and storage.

Source: IEA

IEA also projects that nickel use in EV batteries, renewables, and stainless steel is projected to push nickel demand above 5.5 Mt by 2035. As Indonesia tightens output and China dominates downstream processing, Western economies face rising exposure to supply disruptions and geopolitical leverage. Even conservative outlooks show 8-9x EV battery demand growth by 2050, despite late-decade plateaus from chemistry shifts.

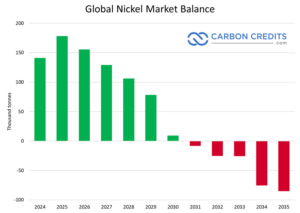

Long-Term Supply Outlook: From Oversupply to Potential Deficit

As per INSG last year, supply vastly outpaced demand, hitting 209-212 kt global surplus. Recently, S&P Global projected a 156,000-tonne surplus in 2026. However, the same analysis also says that today’s surplus will not last forever.

The report projects that global nickel stocks will peak around 2028. After that, inventories will begin to fall as demand improves and supply growth slows. By the early 2030s, the market balance will flip.

By 2031, S&P Global expects the primary nickel balance to turn negative. EV battery demand will grow as electrification expands. Stainless steel consumption will recover alongside global manufacturing. Significantly, Indonesian supply growth will slow as easy expansions may run out, and regulatory risks can increase.

Once inventories drop below comfortable weeks-of-consumption levels, prices respond quickly. S&P Global points to nickel prices rising toward $25,000 per tonne or higher, especially for Class 1 material.

Data source: S&P Global

Policy and Geopolitics: Resource Nationalism and Market Fragmentation

Indonesia exemplifies modern resource nationalism. The government’s export bans, production quotas, and mine suspensions aim to capture downstream value and stabilize prices.

Western governments are responding with critical minerals strategies, including subsidies, domestic mining support, and restrictions on Chinese supply chains. This could fragment the global nickel market into competing blocs, heightening geopolitical risk for downstream industries.

Most importantly, the Trump administration sees developing U.S. nickel supply chains as key to reducing dependence on foreign sources and boosting the domestic industry. Efforts include promoting new mining projects, speeding up permits for critical mineral operations, and exploring tariffs or other trade measures to support local production. One major example is a copper-nickel project in Minnesota, led by a joint venture between Glencore and Teck Resources.

Macro Drivers: Energy Transition, Industrial Demand, and Monetary Policy

Nickel is highly sensitive to macroeconomic and policy conditions. Industrial demand tracks global manufacturing cycles, while battery demand depends on EV adoption rates, subsidies, and consumer behavior.

Interest rates, inflation, and currency fluctuations affect nickel through speculative flows and production financing costs. Meanwhile, energy transition policies, carbon pricing, and ESG mandates are reshaping supply chains, pushing automakers and battery manufacturers to secure long-term nickel supply agreements.

Nickel’s Role in Carbon Markets and Net-Zero Strategies

Nickel’s importance extends beyond industrial use. Battery supply chains are central to decarbonization, embedding nickel demand in national net-zero strategies. Companies increasingly link nickel sourcing to ESG frameworks, carbon disclosure requirements, and sustainability-linked financing.

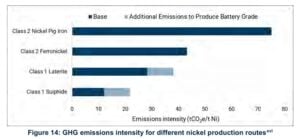

At the same time, nickel production drives greenhouse gas (GHG) emissions. According to a disclosure from the International Finance Corporation (World Bank Group), under a scenario accounting for declining ore grades and cleaner grids, emissions could rise 90% from 2020 to 2050. Additionally, a lack of decarbonization could push emissions to 164%.

Source: IFC

Most emissions come from processing rather than mining. Pyrometallurgical routes for Class 2 nickel (used in stainless steel) are coal-intensive, while Class 1 battery-grade nickel has lower emissions. Shifting to EV-focused, Class 1 production can help limit emissions growth.

Thus, cleaner processing, low-carbon production, and recycling could give automakers and battery makers a competitive edge, while decarbonized electricity is key to controlling nickel emissions as production rises.

Top 3 Nickel Producers Signal Tight Supply Heading into 2026

The global nickel market entered 2026 with cautious signals from its largest producers. Industry analysts revealed that mining output stayed broadly flat, disruptions persisted, and companies focused more on battery-grade processing than expanding supply. This reinforced expectations of a structurally tight nickel market.

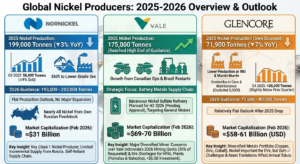

Nornickel

Norilsk Nickel, or Nornickel, reported stable but slightly lower production in 2025. The company produced 199,000 tonnes of nickel, down 3% year-on-year, mainly due to a shift toward lower-grade disseminated ore. Production recovered in the fourth quarter, rising 9% quarter-on-quarter to 58,000 tonnes after scheduled maintenance in Q3. Nearly all nickel came from the company’s own Russian feedstock, highlighting its self-reliant supply chain.

For 2026, Nornickel guided nickel output between 193,000 and 203,000 tonnes, signaling flat production with no major expansion plans. Nornickel’s market capitalization stood at about $31 billion as of February 2026, underscoring its role as a major global supplier despite geopolitical constraints.

The lack of growth from one of the world’s key Class 1 nickel producers suggests limited incremental supply from Russia.

Vale

Brazil’s Vale continued to position itself as a strategic player in the battery metals supply chain. The company plans a nickel sulfate refinery in Bécancour, Québec, with deliveries to General Motors targeted for the second half of 2026, pending regulatory approvals. This move highlighted Vale’s push toward high-purity battery materials rather than bulk nickel mining.

Vale’s market capitalization was around $69–70 billion in early 2026, making it one of the largest diversified miners with significant nickel exposure. It produced 175,000 tonnes of nickel in 2025, reaching the high end of its guidance. Growth came from Canadian operations in Sudbury and Long Harbour and restarts in Brazil.

Looking ahead, Vale Indonesia warned its 2026 mining quota won’t meet demand for new nickel smelters. The approved quota is only about 30% of what the company requested, raising concerns that upcoming processing plants could face ore shortages.

Vale and partners are building three HPAL plants for EV battery nickel. The Pomalaa plant, starting in August 2026, will need 21 million tonnes of limonite ore per year, while Bahodopi will require 10.4 million tonnes annually. These projects represent over $6.5 billion in investment and highlight the growing pressure on Indonesia’s nickel supply.

Glencore

Glencore’s 2025 Full‑Year Production Report showed nickel output from its own sources at 71,900 tonnes, down about 7% from 82,300 tonnes in 2024. This decline was driven by lower production at both Integrated Nickel Operations (INO) and the Murrin Murrin operations. The reported figure excludes 5,000 tonnes from the Koniambo project, which is in care and maintenance.

In the fourth quarter of 2025, nickel production (including third‑party feed) was around 35,300 tonnes, slightly below the prior quarter. Glencore also gave 2026 nickel guidance of 70,000–80,000 tonnes, reflecting a relatively flat outlook after the 2025 drop.

Its nickel business is part of a broader diversified metals portfolio, with the company also producing copper, zinc, cobalt, coal, and other commodities. Nickel remains important to its strategy, especially given rising EV battery demand, but output challenges and asset transitions affected annual totals.

As of February 2026, Glencore’s market capitalization is widely reported to be around $58–61 billion (USD) based on its London Stock Exchange listing and share price.

This positions Glencore as a major diversified mining and commodity trading company, though smaller in market value than some of its peers like Rio Tinto or BHP. The company’s valuation reflects its breadth across metals, energy, and marketing operations, and its prospects are often shaped by commodity price swings and operational performance.

Source: Company reports

Risks and Opportunities for Investors and Policymakers

The top nickel producers showed limited growth in mining output while accelerating investments in battery-grade processing. Ore quality challenges, regulatory delays, and operational disruptions continued to constrain supply. At the same time, electric vehicle demand and energy transition needs kept rising.

The lack of aggressive supply expansion from major producers suggests the nickel market could remain structurally tight through the late 2020s, especially for high-purity Class 1 nickel required in batteries.

This is why nickel stocks present a unique combination of risks and opportunities. Supply concentration, policy interventions, and technological disruption create price volatility. Conversely, long-term demand from electrification, aviation, and hydrogen infrastructure provides structural upside.

Investors must navigate cyclical price swings, while policymakers balance industrial policy with market stability. Strategic supply agreements, diversification, and technology adoption will be crucial for managing risk.

Conclusion: Nickel’s Strategic Decade Ahead

Nickel is entering a decisive decade. The metal is so vital for the global energy transition, but faces structural uncertainty from supply expansion and evolving battery technology.

The next ten years will determine whether nickel becomes a stable metal of clean energy supply chains or a cautionary case study in commodity oversupply and industrial policy missteps. For institutions, understanding nickel’s macro dynamics, supply chains, and policy risks is essential. The metal’s trajectory will shape not only battery markets but also the geopolitics of the global energy transition.

Europe’s carbon market is facing new political pressure. Europe’s largest business lobby group has called for reforms. At the same time, Italy has asked for a temporary suspension of the system. These calls focus on the European Union Emissions Trading System (EU ETS).

The EU ETS is the world’s largest carbon market. It covers around 40% of the EU’s total greenhouse gas emissions. It sets a cap on emissions from power plants, heavy industry, and aviation within Europe.

Under this scheme, companies must hold allowances for each ton of carbon dioxide (CO₂) they emit. They can buy and sell these allowances on the market. Recent carbon price swings and concerns about industrial competitiveness have triggered a new debate.

Inside the System: How Europe’s Carbon Market Operates

The EU ETS started in 2005. It now operates in its fourth phase, which runs from 2021 to 2030. The cap on emissions declines each year. This ensures that total emissions fall over time.

Under the reforms agreed in 2023, the annual cap will decline faster. The linear reduction factor increased to 4.3% per year from 2024 to 2027 and to 4.4% per year from 2028 to 2030.

The EU also decided to cut the total cap by 90 million allowances in 2024 and 27 million allowances in 2026.

In 2023, emissions from sectors covered by the EU ETS fell by about 15.5% compared to 2022, according to the European Commission. Power sector emissions dropped sharply due to higher renewable energy use and lower gas demand. Since 2005, emissions from ETS sectors have fallen by around 47%.

The EU aims to cut net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. This target is part of the European Climate Law. The EU ETS is a key tool to meet that goal.

Source: European Commission

From €10 to €100: The Price Swings Shaping the Debate

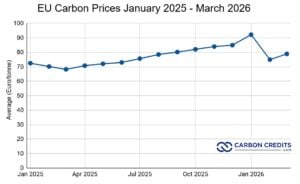

Carbon prices in the EU ETS have risen strongly in recent years. In 2018, prices were below €10 per ton. By early 2023, prices reached record highs of around €100 per ton.

However, prices fell in 2024. By early 2025, EU carbon prices were trading closer to €60–€70 per ton. Slower industrial activity, lower energy demand, and market expectations about future supply influenced this drop.

Most recently, EU prices have fluctuated, trading around €70–€75 per tonne of CO₂ in early March 2026, after rising from their lows in late 2025. On March 3, 2026, EU carbon allowances were around €74.20 per tonne. This is a slight rise from recent lows, but still below the peaks above €90 from earlier in the year.

Data source: TradingEconomics

The Market Stability Reserve (MSR) adjusts the supply of allowances. It removes surplus allowances from the market when supply is high. In 2023, the MSR continued to absorb allowances to support market balance.

Despite these controls, industry groups say price volatility creates uncertainty. Energy-intensive sectors such as steel, cement, chemicals, and aluminum face higher costs when carbon prices rise.

BusinessEurope represents national business federations across the EU. In early 2026, it called for reforms to the EU carbon market.

The group warned that high energy and carbon costs are hurting European industry. It said the EU risks “deindustrialization” if companies move production outside Europe. This could lead to carbon leakage, where emissions shift to countries with weaker climate rules.

BusinessEurope asked EU policymakers to review the Market Stability Reserve. It also called for measures to reduce excessive price swings. The group stressed the need to align climate policy with industrial competitiveness and reduce energy prices in the short term.

Source: BusinessEurope

The lobby group noted in its paper:

“The enabling conditions and incentives to create a viable business case for decarbonisation are still largely missing. The EU has yet to put in place effective short-term measures to lower energy costs and close the related cost competitiveness gap faced by European companies compared to their global competitors… Moreover, EU climate and energy policies continue to lack a genuinely technology-neutral approach. For example, state aid thresholds still differentiate between technologies, making it harder for industries to invest in the technologies needed to achieve Europe’s climate neutrality targets.”

At the same time, the EU has introduced the Carbon Border Adjustment Mechanism (CBAM). CBAM will apply a carbon price on imports of cement, steel, aluminum, fertilizers, electricity, and hydrogen.

The goal is to level the playing field between EU and non-EU producers. The system is in its transitional phase from 2023 to 2025. Full financial obligations begin in 2026.

Italy’s Bold Proposal: Hit Pause on Carbon Pricing?

Italy has taken a stronger position. Italian officials have called for a temporary suspension of the EU ETS. They argue that high carbon prices increase electricity costs and hurt households and businesses.

“The ETS, as currently conceived, represents an additional tax on European companies, affecting costs and limiting their competitiveness.”

Italy relies on gas for a large share of its power generation. When gas prices rise, electricity prices also increase. Adding a carbon price can raise costs further. Italian leaders say this creates pressure on industry and families.

However, suspending the EU ETS would require agreement at EU level. The carbon market is governed by EU law. A single member state cannot stop it alone.

The European Commission has defended the system. It argues that the EU ETS reduces emissions in a cost-effective way. It also generates revenue for member states. In 2023, EU ETS auction revenues reached tens of billions of euros across the bloc. These funds support climate action, energy transition, and social measures.

Billions at Stake: Where Carbon Market Revenues Go

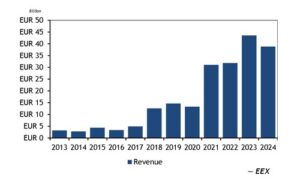

EU member states receive most revenue from auctioning carbon allowances. From 2013 to late 2025, total auction revenues have exceeded €245 billion, per official EU sources.

In 2024 alone, revenues totaled around €39 billion (down from €44 billion in 2023), with €24.4-25 billion going directly to member states despite lower average prices of €64.76/tCO2.

Source: Argus Media

At least 50% of auction revenues must be used for climate and energy-related purposes. Many countries report using much more than this minimum share.

The EU ETS also funds innovation. The Innovation Fund supports low-carbon technologies in industry and energy. It is financed by the sale of 450 million allowances from 2020 to 2030. The Modernisation Fund supports lower-income EU countries in upgrading their energy systems.

These funds aim to help the industry reduce emissions rather than relocate.

What Could Reform Look Like?

The European Commission has signaled a review of the ETS later in 2026. This review comes as part of the broader European Green Deal, the EU’s plan to reach net-zero emissions by 2050.

Reform proposals could include:

Adjusting the pace at which free allowances are phased out.

Modifying how carbon prices are calculated or allocated.

Changing how new sectors like transport and buildings are integrated into the system.

Some industry representatives also want changes to the CBAM. CBAM is a carbon tariff on certain imported goods, such as steel, cement, and fertilisers, starting in 2026. It aims to prevent carbon leakage by making non-EU products pay a carbon cost similar to EU goods.

However, the European Commission recently rejected calls to suspend carbon levies on fertilisers, saying the CBAM must remain stable to protect EU producers.

Reform could seek a balance between climate goals and business competitiveness. How to achieve this balance remains a key question for EU policymakers.

The Road Ahead: Reform, Resistance, or Reinforcement?

The debate reflects a broader tension. The EU wants to cut emissions quickly. At the same time, it wants to protect industrial jobs and economic growth.

The European Commission will continue monitoring the carbon market. It publishes regular reports on supply, demand, and price trends. Any major reform would require agreement from the European Parliament and EU member states.

For now, the EU ETS remains central to Europe’s climate policy. It has helped drive a nearly 50% cut in emissions from covered sectors since 2005. But political pressure is rising. The outcome will shape Europe’s path toward its 2030 target and its longer-term aim of climate neutrality by 2050.

Vistra Corp. (NYSE: VST) closed 2025 with strong operational and financial momentum. Headquartered in Irving, Texas, the Fortune 500 power producer operates one of the largest competitive electricity portfolios in the United States.

Last year, the company expanded its fleet, strengthened long-term partnerships, and delivered record operational performance. At the same time, it positioned itself to benefit from rising electricity demand driven by data centers, electrification, and AI growth.

It now owns and operates roughly 44,000 megawatts (MW) of generation capacity across natural gas, nuclear, coal, solar, and battery storage assets. That capacity can power about 22 million homes.

Financial Performance Shows Underlying Strength

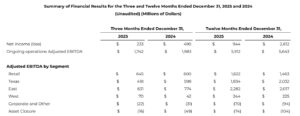

For the year ended December 31, 2025, Vistra reported GAAP net income of $944 million. This figure included an $808 million unrealized pre-tax loss from commodity hedges expected to settle in future years.

Source: Vistra

Although net income declined compared to 2024, the drop mainly reflected accounting impacts from rising forward power prices. Higher forward prices typically increase the long-term value of Vistra’s generation portfolio. As a result, the underlying business remains strong.

Ongoing Operations Adjusted EBITDA reached $5.9 billion, up $269 million year over year. Stronger retail margins and contributions from newly acquired assets supported the increase. Cash flow from operations totaled $4.07 billion, reinforcing liquidity and balance sheet strength.

2026 Expectations

For 2026, Vistra expects its adjusted EBITDA to range between $6.8 billion and $7.6 billion, while its adjusted free cash flow before growth is projected between $3.93 billion and $4.73 billion.

Importantly, these projections exclude potential impacts from the pending Cogentrix acquisition and recently signed nuclear agreements.

Meta and Amazon Anchor Vistra’s Nuclear Growth Strategy

The company operates the second-largest competitive nuclear fleet in the United States, providing steady, carbon-free baseload electricity that supports both grid reliability and corporate decarbonization goals.

In early 2026, the company signed 20-year power purchase agreements with Meta, covering more than 2,600 megawatts of nuclear energy across its PJM facilities. As Meta expands its AI capabilities and data center footprint, it needs dependable, around-the-clock power. These agreements secure long-term access to emissions-free electricity while giving Vistra predictable revenue streams.

Importantly, the structure of the contracts goes beyond traditional energy sales. They include capacity payments and plant uprates, allowing higher output from existing nuclear units. This approach improves asset efficiency for Vistra while ensuring price stability and supply certainty for Meta.

Vistra also strengthened its clean energy partnerships in Texas. Last year, it signed a separate 20-year agreement with Amazon Web Services for up to 1,200 megawatts of nuclear power from the Comanche Peak Nuclear Power Plant. The deal supports Amazon’s growing data operations with firm, carbon-free electricity and locks in long-term value for the company.

Together, these agreements reinforce the long-term viability of Vistra’s nuclear fleet. Long-term license renewals for the PJM units extend the life of critical zero-carbon infrastructure and strengthen grid reliability. At the same time, they position Vistra to meet rising corporate demand for clean, dependable power in the AI-driven economy.

Source: IEA

Expanding Solar and Natural Gas

Vistra also commissioned the 200-MW Oak Hill Solar Facility on a reclaimed coal mine site. The project includes a PPA with AWS, expanding the clean energy collaboration.

In November 2025, it closed a 2,600-MW acquisition from Lotus Infrastructure Partners. Shortly after, it announced plans to acquire Cogentrix Energy, adding approximately 5,500 MW of gas-fired capacity. The transaction is expected to close in mid-to-late 2026.

Additionally, it has also begun construction on two new gas units totaling 860 MW at its Permian Basin plant, effectively tripling that site’s capacity. In addition, it executed uprates across its Texas gas fleet to increase efficiency and output.

These investments reflect a balanced approach. As renewable penetration increases, flexible gas generation helps stabilize the grid and manage peak demand.

Advancing Emissions Reduction Goals

Vistra’s Scope 1 greenhouse gas emissions declined for the third consecutive year in 2024, primarily due to reduced coal generation. Scope 1 includes carbon dioxide, methane, and nitrous oxide, with carbon dioxide representing the largest share.

The company targets a 60% reduction in Scope 1 and 2 emissions by 2030 compared to 2010 levels. It also aims to achieve net-zero emissions by 2050.

Corporate sustainability efforts extend beyond generation. The company’s headquarters operates on 100% Green-e Wind renewable energy certificates. Nuclear-based emissions-free energy certificates also support fleet electricity usage. Together, these certificates covered more than 30% of corporate electricity consumption in 2024.

Source: Vistra

Positioned for Long-Term Value Creation

Vistra enters 2026 with strong momentum. Long-term nuclear PPAs with Meta and Amazon, expanded gas capacity, disciplined hedging, and growing renewable assets provide earnings visibility.

As electricity demand rises from AI, electrification, and digital infrastructure, companies with scale and reliability will benefit. Vistra’s integrated model of combining retail operations, nuclear baseload, flexible gas assets, and renewables positions it to capture that growth.

With projected EBITDA exceeding $7 billion in 2026 and potential upside from acquisitions, Vistra is not only adapting to the evolving energy market. It is actively shaping its future.

Spanish energy company Moeve approved more than €1 billion ($1.2 billion) for the first phase of its Andalusian Green Hydrogen Valley. The final investment decision cleared the way for construction to begin in the coming weeks. Significantly, Moeve will hold a 51% majority stake. The remaining share will be owned by Masdar and Enalter.

Enalter is majority controlled by Enagás Renovable, a pioneer in renewable gas development. Meanwhile, Masdar brings global clean energy expertise from Abu Dhabi.

This first phase, called Onuba, will install 300 megawatts (MW) of electrolyser capacity in southern Spain. Moreover, the company kept the option to expand the project by another 100 MW, subject to grid access and board approval.

Onuba: A Strategic Project With European Backing

The Onuba project will be the largest green hydrogen facility in southern Europe once operational. It carries a total investment of over €1 billion. That includes related infrastructure and a dedicated solar power plant for self-consumption.

Importantly, the project secured strong public support. The European Commission classified it as a Project of Common European Interest (PCI). In addition, the Spanish government awarded €304 million in funding under its Recovery, Transformation and Resilience Plan. This support came through the EU’s NextGenerationEU program under the Hydrogen Valleys scheme.

Such backing places the project at the center of Europe’s industrial decarbonization strategy. Brussels aims to reduce dependence on imported fossil fuels while scaling domestic clean energy production.

Ownership Mix Boosts Financing

This ownership mix reflects a wider shift in global capital. Gulf and European investors are increasingly channeling funds into hydrogen infrastructure. Notably, Moeve itself is owned by Mubadala, Abu Dhabi’s sovereign fund, and U.S. private equity firm Carlyle. As a result, the project benefits from deep financial backing and international reach.

Production Capacity and Climate Impact

At 300 MW, Onuba will produce about 45,000 tonnes of green hydrogen per year. This output will help avoid around 250,000 tonnes of CO₂ annually.

Simply put, the emissions reduction equals more than the total emissions generated by passenger vehicles with internal combustion engines in the Spanish cities of Huelva, Cádiz, and Jaén.

The hydrogen produced will serve multiple sectors. It will support aviation fuels, road transport, and marine fuels. In addition, it will help decarbonize chemical and fertilizer industries. Therefore, the project directly targets hard-to-abate sectors.

Solving the Grid Bottleneck

Grid access has slowed many hydrogen projects across Europe. However, Moeve recently secured a connection to the Spanish electricity grid. This approval came at a crucial time.

Besides grid power, the project will use a dedicated solar plant. This hybrid model will stabilize the electricity supply and improve the plant’s carbon intensity profile.

Access to renewable electricity remains essential. Green hydrogen only delivers climate benefits when powered by clean energy. Therefore, Andalusia’s strong solar resources give the region a clear advantage.

Furthermore, the region’s port infrastructure could support exports of hydrogen derivatives such as ammonia to northern European markets. This strengthens Spain’s ambition to become a renewable energy exporter.

Moeve’s Broader €8 Billion Transition Plan

The hydrogen valley forms part of Moeve’s broader €8 billion transition strategy. Formerly known as Cepsa, the company rebranded in 2024 to signal its shift toward low-carbon businesses.

Since 2022, Moeve sold most of its oil production assets, including operations in Abu Dhabi and South America. It redirected that capital into renewables, biofuels, and hydrogen.

This capital reallocation marks a clear pivot. Instead of expanding oil production, the company invested in long-term clean infrastructure.

Financially, the company strengthened its position before making this move. Net profit rose to €341 million last year, compared to €92 million in 2024. This improved profitability provided internal funding capacity for large-scale energy transition projects.

At the same time, Moeve entered non-binding talks with Portuguese energy firm Galp. The companies are exploring a combination of refining, chemicals, and fuel retail businesses. They aim to complete due diligence and possibly reach an agreement by mid-2026.

If successful, consolidation could free up more capital. It could also stabilize legacy businesses during the transition period.

Low-carbon hydrogen plays a critical role in cutting emissions from industry and transport. The European Union set ambitious goals under its hydrogen strategy and REPowerEU plan. The bloc aims to produce 10 million tonnes of renewable hydrogen and import another 10 million tonnes by 2030.

However, the path remains complex.

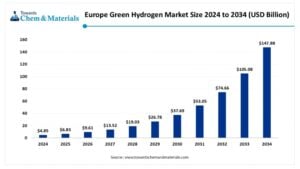

Analysts say that by 2030, Europe would need at least 100 gigawatts (GW) of installed electrolyser capacity to meet REPowerEU targets. That implies annual capacity growth of roughly 150% between 2025 and 2030. By comparison, growth between 2020 and 2024 averaged around 45%.

European renewable hydrogen production capacity announced

Source: EY

In addition, regulatory rules for renewable hydrogen, such as strict temporal and geographical correlation requirements, increase development costs. Projects often require extra storage and grid adjustments.

Funding remains another bottleneck. Although the EU structured many subsidies and incentives, approval processes can take 12 to 24 months. These delays risk slowing deployment.

As of December 2024, about 60% of Europe’s renewable hydrogen production ambition was covered by national targets. Member states must better align policies and accelerate ramp-up if the EU hopes to meet 2030 goals.

A Fast-Growing Market

Despite challenges, market growth remains strong. The European green hydrogen market was valued at around $4.85 billion in 2024. Analysts expect it to reach nearly $147.88 billion by 2034. This implies a compound annual growth rate (CAGR) of about 40.7% between 2025 and 2034.

Several factors drive this expansion:

Rising demand for net-zero solutions

Decarbonization pressure on heavy industry

Expanding renewable energy capacity

Policy incentives and carbon pricing

By technology, alkaline electrolysers dominated the market in 2024, holding about 45% share. These systems remain cost-competitive and proven at scale.

Why This Project Matters

Moeve’s Andalusian Green Hydrogen Valley signals more than a single investment. It highlights three broader trends. First, capital is shifting from oil to clean infrastructure. Second, Europe is backing hydrogen with serious public funding. Third, Spain is emerging as a strategic clean energy exporter.

If executed successfully, Onuba could become a cornerstone of Europe’s hydrogen economy. More importantly, it shows that large-scale projects are moving from ambition to action. Thus, in a decade defined by energy transition, this €1 billion decision may mark a turning point for southern Europe’s clean industrial future.

Disseminated on behalf of Surge Battery Metals Inc.

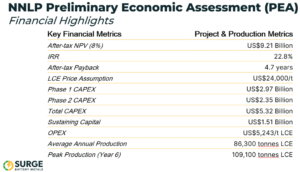

Grade matters because it affects how much lithium a project can produce and how costly it is to operate. Higher grades generally mean more lithium can be recovered with lower costs. This matters for projects that want to compete in the fast‑growing electric vehicle (EV) and energy storage markets.

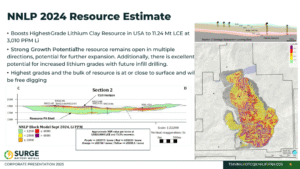

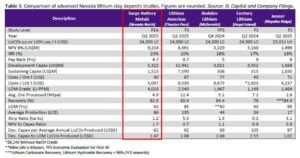

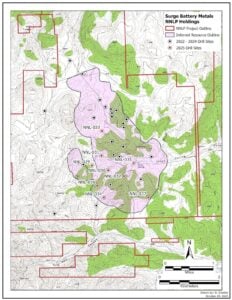

Let’s explore why grade is essential for lithium clay projects and learn how it affects economics, operations, and investor interest. More notably, we highlight how Surge Battery Metals’ Nevada North Lithium Project (NNLP) stands out in this context.

What “Grade” Means in Lithium Projects

In mining, “grade” refers to how much lithium is present in a deposit. It is usually reported in parts per million (ppm) or as lithium carbonate equivalent (LCE). A higher grade means there is more lithium per tonne of rock.

For lithium clay, grades can vary widely. Some clay deposits have grades below 1,000 ppm. Others reach several thousand ppm. The higher the grade, the more lithium metal is available to extract.

U.S. lithium clay peers usually range from 800 to 2,540 ppm Li. Some areas are lower, at 120 to 766 ppm, like American Lithium’s Tonopah claims. Others can reach 1,690 to 2,900 ppm in drilling. Common cutoffs start at 1,000–1,250 ppm for economic viability, far above the <500 ppm in some global clays like Australia’s Kaolin resources.

Grade affects several key project factors:

Revenue potential – Higher grade means more lithium output per tonne of material moved.

Cost efficiency – Projects with a higher grade may spend less on mining and processing per unit of lithium produced.

Product quality – Higher-grade feedstock can result in higher‑purity lithium products, which are valuable in battery markets.

Investors and developers pay close attention to grade because it is a strong indicator of future project performance.

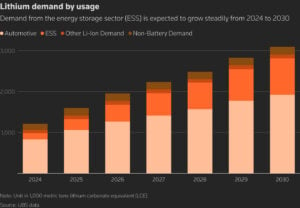

The global lithium market is changing fast. EV production is growing quickly. Energy storage systems are expanding. Demand for lithium is outpacing supply in many markets. This puts pressure on producers and developers to find the most competitive resources.

In this environment, grade has become a key differentiator among lithium clay projects. Several market trends explain why grade now matters more than ever:

Rising Demand for Battery‑Grade Lithium