The Mercedes-AMG PETRONAS F1 Team has stepped up its climate action strategy with a major expansion of its global carbon dioxide removal (CDR) portfolio. The team has added seven new projects across multiple carbon removal pathways, making it one of the most diverse portfolios in global sport.

This move is a long-term, multi-year investment designed to support high-integrity, science-backed climate solutions. While emissions reduction remains the top priority, the team recognizes that some emissions cannot be eliminated. That is where durable carbon removals come in.

The expansion marks another milestone in Mercedes’ broader Net Zero journey — one built on practical solutions, data transparency, and industry collaboration.

A Clear Net Zero Roadmap

Mercedes tracks its carbon footprint in two ways. First, it measures Race Team Control emissions (RTCe). These include Scope 1, Scope 2, and selected Scope 3 emissions that the team can influence directly. Second, it reports its total emissions across Scopes 1, 2, and 3.

Unlike many companies that only focus on direct emissions, Mercedes extends its control boundary to include upstream transport, waste, fuel-related activities, business travel, employee commuting, and energy use. This broader approach aligns with Formula 1’s 2030 Net Zero commitment.

The team has set two major targets:

- Achieve Race Team Control Net Zero by 2030

- Reach Full Net Zero across all scopes by 2040

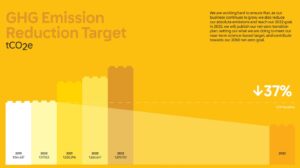

For its 2030 goal, Mercedes plans to cut 75% of RTC emissions compared to its 2022 baseline. The remaining 25% will be addressed through high-quality carbon removals, following the Oxford Offsetting Principles.

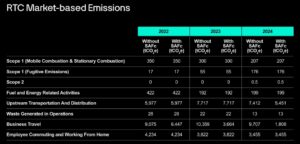

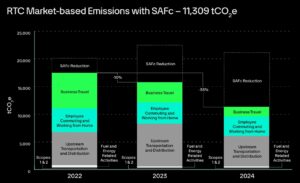

Progress so far is significant. By 2024, the team had already reduced its Race Team Control emissions by 35% compared to 2022.

Where the Emissions Cuts Came From

The 35% reduction came from targeted operational changes. During the European race season, 98% of logistics used HVO100 biofuel. This low-carbon fuel helped slash transport emissions. Meanwhile, 68% of aviation emissions were addressed through Sustainable Aviation Fuel certificates (SAFc).

At its Brackley factory in the UK, Mercedes reduced gas consumption and improved energy efficiency. The team also continued electrifying its company vehicle fleet.

However, not everything went smoothly. In 2024, an F-gas leak at the factory temporarily increased Scope 1 emissions. F-gases have high global warming potential, so even small leaks can have an outsized impact. While the team has already transitioned to lower-impact refrigerants where possible, some cooling systems still rely on high-impact gases. Mercedes has tightened monitoring systems and plans to shift to better alternatives as soon as viable options become available.

Despite this setback, the overall emissions trend remains downward. The team now aims to fully eliminate Scope 1 and 2 emissions by 2026, with any small residual amounts neutralized through removals.

Building a Long-Term Carbon Removal Strategy

Even with aggressive cuts, some emissions remain hard to eliminate — especially across global supply chains. Purchased goods and services represent a large share of Scope 3 emissions. These are complex and often outside direct control.

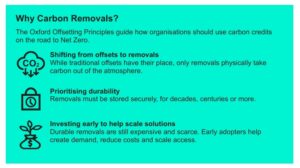

That is why Mercedes is investing in durable, verifiable, and scalable carbon removals.

In total, the team is investing in roughly 18,900 tonnes of CO2 equivalent across nature-based, hybrid, and engineered removal projects. These investments support the 2030 Race Team Control Net Zero goal.

Importantly, the strategy follows the Oxford Offsetting Principles. This means prioritizing permanent removals and gradually shifting from short-term nature-based offsets toward long-term engineered solutions.

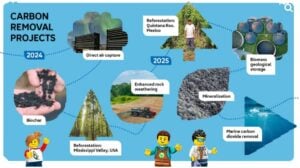

A Diverse Portfolio Across Technologies

To reduce risk and build resilience, Mercedes has spread its investments across several technologies and geographies. The portfolio now spans:

- Direct Air Capture

- Biochar, Biomass Storage

- Bioenergy with Carbon Capture and Storage (BECCS)

- Ocean Alkalinity Enhancement

- Enhanced Rock Weathering

Frontier: One key partner is Frontier, supporting durable removal technologies. Through this agreement, Mercedes backs solutions such as direct air capture and enhanced weathering. These technologies aim to store carbon for more than 1,000 years and eventually reduce costs below $100 per tonne. The team expects to begin receiving credits from Frontier-backed projects as early as 2027.

Blaston Farm: In the UK, Mercedes works with Blaston Farm near Silverstone to support regenerative agriculture. This project removes carbon while restoring soil health and boosting biodiversity. The team signed a three-year agreement and used 2,000 tonnes of removals from the project against its 2024 footprint. Advanced soil monitoring combines direct sampling with AI-driven image analysis, improving both accuracy and scalability.

Chestnut Carbon: In the US, Mercedes partnered with Chestnut Carbon to restore degraded agricultural land in the southeastern region. The first project will convert 200 hectares into biodiverse forests by planting more than 260,000 native trees. Since 2022, Chestnut Carbon has planted over 17 million trees across 30,000 acres. The collaboration is expected to deliver 1,000 to 1,500 tonnes of carbon removals annually starting in 2027.

The broader portfolio also includes projects in Brazil, Canada, Denmark, and India. This geographic spread reflects the team’s goal to create impact in regions connected to the Formula One race calendar.

All projects are curated and verified by CUR8, a carbon removal marketplace that assesses durability, transparency, and methodology. This adds an extra layer of credibility to the portfolio.

- FURTHER READING: Frontier’s $31.3M Offtake with Planetary Signals a New Era for Ocean Carbon Removal

Collaboration Beyond the Track

Mercedes understands it cannot solve climate challenges alone. The team actively collaborates within and beyond motorsport.

It participates in the F1 ESG Working Group, sharing best practices across the grid. Internally, its Sustainability Working Group connects team partners to exchange ideas and tackle shared challenges.

Notably, Mercedes was the first motorsport team to sign The Climate Pledge, committing to Net Zero across total emissions by 2040.

Team partners such as Signify, UBS, and Nasdaq support high-integrity climate solutions as well. Meanwhile, companies like Meta and Microsoft have played a major role in scaling the carbon removals industry, helping create demand for early-stage technologies.

Speaking at Economist Impact’s Sustainability Week, Head of Sustainability Alice Ashpitel emphasized that emissions reduction remains the priority. However, she stressed that high-quality removals are essential for dealing with residual emissions. By investing early across different technologies and regions, the team aims to help scale durable climate solutions while delivering benefits to communities and ecosystems.

Engineering Change On and Off the Track

Formula One has committed to Net Zero by 2030. As one of the sport’s most prominent teams, Mercedes is positioning itself at the forefront of that transition.

The team’s approach combines aggressive emission reductions, early investment in permanent carbon removal technologies, and strong governance. Instead of relying on short-term offsets, it is helping build a long-term carbon removal market capable of delivering climate impact at scale.

This strategy reflects the same engineering mindset that drives success on the track: test, refine, optimize, and scale.

By cutting emissions where it has control and investing in durable removals where it does not, Mercedes is shaping a credible path toward Net Zero. The goal is not just to meet targets but to help raise standards across motorsport and beyond.

In a sport defined by speed and precision, Mercedes is proving that climate leadership also requires bold action and long-term thinking.