The European Union (EU) has unveiled a funding package of €545 million (around US $638 million) to speed up Africa’s clean energy transition. The funds will help develop renewable energy, upgrade electricity grids, and support rural electrification in nine African countries. This move is part of the EU’s Global Gateway strategy. It aims to boost sustainable infrastructure and strengthen economic ties with partner regions.

The package highlights the EU’s focus on both climate action and energy security. It also comes at a time when Africa faces urgent energy challenges. About 600 million people in Africa still don’t have electricity. Meanwhile, the need for reliable and affordable power is rising quickly.

Power to the People: Where the Money Goes

The EU funding will be spread across several African nations, each with projects tailored to local needs:

Côte d’Ivoire will get the biggest share, around €359.4 million. This funding will help build a high-voltage energy line. It will improve transmission and make the grid more reliable.

Cameroon will receive €59.1 million to boost rural electrification. This will help about 687 communities.

Somalia will have €45.5 million to increase access to renewable energy and enhance resilience to climate shocks.

Mozambique will receive €13 million. This funding aims to support a low-emission transition and draw in private investment.

Other countries in the program are the Central African Republic, the Republic of Congo, Ghana, Lesotho, and Madagascar. Their projects focus on renewable generation, grid integration, and improving access in underserved regions.

This funding could attract more investment from global partners and private firms. The EU believes its support will lower risks for investors. This, in turn, should encourage long-term investments in Africa’s energy sector.

Africa is home to vast renewable energy resources, but its power sector faces deep challenges. The continent boasts some of the highest solar irradiation levels globally. It also has strong wind potential in coastal and desert regions.

Source: Ember

Additionally, there are significant untapped hydro resources and geothermal opportunities in East Africa. Yet, these remain underdeveloped. Here are some facts about the continent’s energy landscape:

As of 2024, around 43% of Africa’s population has no access to electricity, mostly in rural areas.

The International Energy Agency (IEA) says Africa needs $25 billion each year for energy access. This investment is crucial to ensure that everyone has electricity by 2030.

Africa has 60% of the world’s best solar resource potential. But only about 2-3% of global clean energy investment currently flows to Africa, despite its vast potential.

Electricity is central to Africa’s clean energy future, with renewables driving growth. Renewables, led by solar, wind, hydro, and geothermal, will make up over 80% of new power capacity by 2030. Redirecting funds from canceled coal projects could finance half of Africa’s solar additions to 2025.

Source: IEA

The clean energy transition is not only about climate. Reliable electricity is essential for health services, schools, businesses, and job creation. According to estimates, Africa’s renewable sector could create 38 million green jobs by 2030. This will happen if there is enough funding and infrastructure.

The EU’s $638 million clean energy funding could deliver a range of benefits for African communities and economies.

It can stabilize electricity grids. This makes power more reliable and cuts down on blackouts for homes and businesses. Stronger transmission systems will also make it easier to integrate renewable power sources.

Second, rural electrification projects will deliver power to communities that have long lacked it. Electricity access in rural areas boosts education by letting schools stay open after dark. It also supports local health clinics and creates opportunities for small businesses.

Third, the investment will support Africa’s climate goals. Countries can reduce their reliance on fossil fuels by expanding solar, wind, hydro, and other renewable projects. This shift also helps to cut greenhouse gas emissions.

Finally, EU involvement is expected to encourage co-financing and private sector participation. Investors often see African energy projects as risky. However, public funding from the EU and other groups can lower barriers. This makes projects more appealing.

Roadblocks on the Green Highway

While the funding is significant, there are still challenges that could affect the success of these projects.

Many African electricity grids are weak or fragmented. This makes it hard to add new renewable sources on a large scale. Large infrastructure projects need good governance, transparency, and technical skill. Some areas may not have these.

Financing remains another hurdle. The $638 million package, while important, is only a fraction of Africa’s total energy investment needs. Africa needs hundreds of billions of dollars in extra funding over the next decade. This is essential for universal access and a shift to clean energy.

Source: IEA

Political instability, regulatory barriers, and limited local capacity may also slow down progress. To tackle these problems, the EU and African governments must work together. They need strong project oversight and to improve local technical skills.

More Than Money: Why This Partnership Matters

The EU’s support is part of its larger vision for sustainable growth and climate action. Under the Global Gateway initiative, the EU has pledged €150 billion in investment for Africa by 2030, with clean energy as a central focus. This funding aims to support Africa’s development. It also strengthens Europe’s ties with the continent in a competitive world.

By supporting Africa’s energy transition, the EU is also advancing its own climate commitments. Expanding renewable capacity in Africa contributes to global emissions reduction while also reducing reliance on fossil fuel imports.

The projects announced will help lay the foundation for deeper EU-Africa cooperation in the years ahead. If successful, they could serve as models for scaling up investment and technology transfer in clean energy.

Funding alone won’t close Africa’s big investment gap. However, it shows that people are starting to recognize the continent’s role in the global clean energy shift. Success will depend on strong governance, effective implementation, and mobilization of additional financing from both public and private sources.

If delivered well, the initiative could improve millions of lives, create jobs, and bring Africa closer to universal energy access while also contributing to the global fight against climate change.

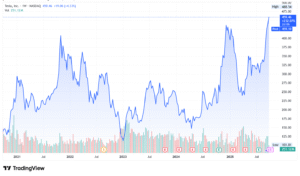

Tesla has once again made headlines after its stock climbed above $450 per share, lifting its market value past $1.5 trillion. This milestone places Tesla among the most valuable companies in the world, alongside tech giants.

The market jump reflects strong investor belief in Tesla’s role as a leader in electric vehicles (EVs) and clean energy. It also shows rising expectations ahead of the company’s upcoming third-quarter delivery results.

While the stock’s performance has impressed many, Tesla now faces new challenges that could affect future demand. One of those challenges has already started to take shape in the U.S. market: leasing costs.

Leasing Gets Pricier as Tax Credit Expires

At the beginning of October, Tesla raised lease prices across most of its American lineup. This change came after a $7,500 federal EV tax credit for leased vehicles expired. The EV giant had previously used the credit to lower monthly lease payments for customers. With the incentive gone, leasing now costs more.

For example, the Model Y saw its monthly lease rate climb by about $50 to $70. The Model 3 also rose by around $80 on some versions. Purchase prices, however, did not change.

This means that buying a Tesla outright still costs the same, but leasing has become less affordable. Leasing has been a popular way for many first-time EV owners to enter the market, so higher rates may slow demand in that segment.

Still, Tesla benefits from the adjustment because it helps protect profit margins at a time when incentives are shifting. This change also ties closely to Tesla’s delivery expectations for the third quarter.

All Eyes on Q3: Can Tesla Deliver Half a Million Cars?

Tesla will soon report how many cars it delivered in the third quarter. Analysts are watching closely, and estimates have been rising. Projections range from 442,000 to more than 500,000 vehicles.

Some firms expect Tesla to deliver around 480,000 units, which would be stronger than expected earlier in the year. Others even believe Tesla could pass the half-million mark, thanks to a last-minute rush of buyers who wanted to take advantage of cheaper leasing before the credit expired.

This boost in sales, however, may create uneven demand. If customers rushed to buy in Q3, the following quarters might see weaker numbers. That possibility has some analysts cautious, even as they raise their short-term forecasts.

Regardless of the exact total, the delivery report will act as a test of Tesla’s ability to keep growing at scale while facing new market pressures.

Investors Fuel Tesla’s $1.5 Trillion Market Cap Surge

The recent stock surge to $459 highlights how much investors believe Tesla can continue to deliver. Moving into the $1.5 trillion market cap club has made Tesla one of the most closely watched companies worldwide.

The optimism is clear: if Tesla reports strong Q3 deliveries, the stock could climb even higher. But expectations are also very high. Any sign of weakness, either in deliveries or future guidance, could push the stock lower.

This tension between confidence and caution explains why Tesla’s stock is so volatile. Every update on sales, pricing, or government policy has the potential to shift the company’s market value by billions in a single day.

Moreover, Tesla’s latest surge is fueled by a proposed $1 trillion compensation plan for Elon Musk, linking his pay to bold targets. These include lifting Tesla’s value from $1 trillion to $8.5 trillion by 2035.

The company is betting big on AI, with robotaxi services using Model Y cars set for Austin in mid-2025. This is followed by Cybercab production in 2026. Tesla also plans to launch Full Self-Driving software version 14 and deploy thousands of Optimus humanoid robots in factories by year-end.

Still, critics caution that Tesla’s high valuation—around 180 times forward earnings—rests heavily on unproven AI ambitions.

Amid all these, one thing remains: the EV leader’s sustainability and emission reduction drive.

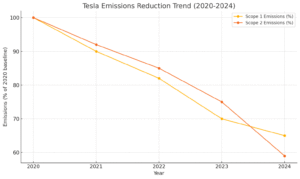

Tesla Balances Emissions Cuts with Supply Chain Challenges

Tesla emphasizes reducing emissions across its operations and product life cycle. In 2024, the company reported a total carbon footprint of about 56 million metric tons CO₂e, combining its own operations and supply chain emissions.

Source: The Sustainable Innovation

Tesla also notes that in 2023, its customers avoided over 20 million metric tons of CO₂e by driving electric vehicles instead of fossil-fuel cars.

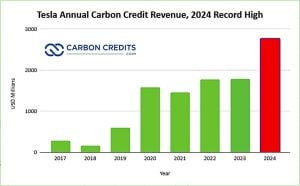

Regulatory credits are another pillar. In 2024, Tesla generated $2.76 billion from selling regulatory carbon credits. This is a 54% increase compared to $1.79 billion in 2023. This revenue comes from providing greenhouse gas (GHG) credits to other automakers that need to meet emissions regulations in the U.S., Europe, and China.

Tesla’s carbon credit sales in 2024 accounted for nearly 39% of its net income for the year, making it a dominant player in the emissions credit market.

To support its goals, Tesla operates its Supercharger network with 100% renewable energy, and its Berlin Gigafactory has run on fully renewable power for the past two years. However, the company still faces its biggest challenge in Scope 3 emissions—those tied to its supply chain and the use of its vehicles.

Opportunities and Obstacles on Tesla’s Road Ahead

Tesla’s path forward is full of both opportunities and risks. The company continues to expand globally, invest in new technologies, and explore new business areas such as energy storage and software. At the same time, it must handle challenges like shifting policies, rising competition, and customer affordability.

On the opportunity side, strong U.S. demand could carry Tesla through short-term changes in subsidies. Growth in markets like China and Europe also offers new revenue streams. Tesla’s work in batteries, charging infrastructure, and AI features may help it build a broader ecosystem beyond cars.

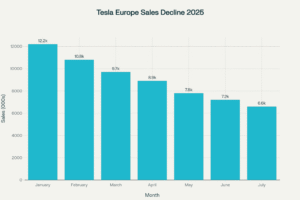

But risks are just as clear. Without the leasing credit, some U.S. customers may wait longer or choose competitors. Supply chain costs could rise, cutting into margins. And with global EV competition heating up, especially from Chinese automakers, Tesla’s share of the market may come under pressure. This has been the case in its European sales.

Source: Tesla Europe Sales, Jan-July 2025 (Data: European Automobile Manufacturers’ Association; sources: PBS, Yahoo Finance, JATO Dynamics).

Managing these factors will decide whether Tesla’s $1.5 trillion valuation remains justified. Investors are already reacting based on how Tesla balances growth with these headwinds.

Tesla’s Future: Growth Under Pressure

Tesla enters the last part of the year in a strong but demanding position. The company has reached a market value that few automakers in history could have imagined. Yet with that success comes more pressure to deliver not just cars, but also consistent growth and profits.

The rise in leasing costs shows how quickly policies can change the market. The Q3 delivery report will test whether Tesla can handle those changes while keeping demand strong. If results meet or beat forecasts, Tesla may strengthen its image as the EV leader. If results fall short, the stock could face new doubts.

Either way, Tesla’s next moves will be closely watched not only by investors but also by the wider auto industry. As the world transitions to electric transport, Tesla’s performance will continue to serve as a signal of how fast and how strong that shift can be.

Normod Carbon has announced plans to build a $294 million carbon dioxide (CO₂) hub at the Port of Grenaa, Denmark. This large-scale project will serve as a central facility for the collection, handling, and shipping of captured CO₂ from industries across Northern Europe.

Once completed, the hub could play a critical role in helping Denmark and the wider European Union (EU) reach their climate targets. Europe is shifting from planning to constructing key carbon capture and storage (CCS) infrastructure.

Normod Carbon is a Danish company that offers a transport and export hub. This helps industries store captured emissions underground or send them to offshore sites in the North Sea. The company’s projects also link to carbon markets, creating new opportunities for businesses to meet net-zero targets.

Why the Port of Grenaa?

The Port of Grenaa, located on Denmark’s east coast, is one of the country’s largest commercial ports. Its location on the Kattegat Strait is great for shipping routes in Northern Europe. It also connects easily to offshore CO₂ storage areas.

Normod Carbon chose Grenaa for several reasons:

It already has a strong shipping and logistics infrastructure.

It provides easy access to industrial regions in Denmark, Sweden, and Northern Germany.

It can be a crucial link to offshore storage projects in the Danish North Sea. There, depleted oil and gas reservoirs are being readied for permanent CO₂ storage.

With these advantages, the Port of Grenaa could become one of the first major CO₂ export hubs in the Nordic region.

The total investment of $294 million (about DKK 2 billion) will cover the design, construction, and operation of the hub. The facility will be able to handle several million tonnes of CO₂ per year, with potential for expansion as demand grows.

Phase 1 (mid-2020s): Construction of storage tanks, loading equipment, and initial pipeline connections.

Phase 2 (late 2020s): Expansion to handle larger volumes and connect with more industrial emitters in Denmark and nearby countries.

Phase 3 (2030 and beyond): Integration into a broader European CO₂ transport and storage network.

Normod Carbon aims for the hub to be fully operational by 2030. This aligns with Denmark’s goal to reduce greenhouse gas emissions by 70% from 1990 levels by that year.

Source: EPRS

Denmark’s Role in the European CCS Market

Denmark is positioning itself as a leader in carbon capture and storage. The country has committed to storing up to 13 million tonnes of CO₂ annually by 2030. Much of this will take place in the North Sea, where geological formations left by oil and gas production provide secure storage.

Several projects are already underway, including the Greensand project, which aims to inject CO₂ into a depleted oil field. The new Grenaa hub will complement these efforts by acting as a collection and export center.

The EU sees CCS as an essential tool for reaching net-zero emissions by 2050. The International Energy Agency (IEA) states that global CCS capacity needs to grow from 50 million tonnes a year to over 1.2 billion tonnes by 2030.

The IEA further says the world will need to capture about 7.6 billion tons of CO₂ each year by 2050 to reach net zero. This means the use of CCS must grow more than 100 times by 2050 to meet the IEA’s net-zero goals. Facilities like Grenaa are part of that scaling effort.

Why Heavy Industry Needs This Hub

The Grenaa hub is expected to bring economic benefits to the region. Construction and operation will create hundreds of jobs in engineering, logistics, and maintenance. Local industries will benefit from easier access to CO₂ handling services. This can help them stay competitive under Europe’s strict climate rules.

The EU Emissions Trading System (ETS), which sets a price on carbon emissions, has made it more expensive for companies to emit CO₂. In 2024, carbon prices averaged around €70–90 per tonne. By using CCS and hubs like Grenaa, industries can reduce their ETS costs and meet compliance targets.

Sectors such as cement, steel, and chemicals — known as hard-to-abate industries — stand to gain the most. These sectors face limited options for deep decarbonization, making CCS a critical pathway.

CCS and Carbon Credits: A Growing Connection

The Grenaa hub also connects directly to the fast-growing carbon credit market. When industries capture and store CO₂, they can generate credits that represent verified emissions reductions. These credits can then be sold or used to offset other emissions within the same company.

The global voluntary carbon market was valued at over $2 billion in 2024 and is expected to expand as more companies adopt net-zero targets. By linking CCS with carbon credits, projects like Grenaa can create new revenue streams while driving climate action.

For emitters, using CCS and trading credits provides both a compliance tool under the EU ETS and a way to show progress to investors and customers.

Climate Math: Can CCS Deliver?

From an environmental perspective, the hub could help reduce emissions that are otherwise difficult to eliminate. By 2030, it may handle millions of tonnes of CO₂ annually, equal to the emissions of hundreds of thousands of cars.

Denmark’s broader climate strategy also relies on balancing renewable energy growth with CCS. The country is already a leader in offshore wind power, generating more than 59.3% of its electricity from wind in 2024. However, wind and solar cannot fully eliminate emissions from heavy industries. This is where CCS infrastructure like Grenaa becomes essential.

Challenges Ahead

Despite its potential, the project faces challenges. CCS remains expensive, with capture and storage costs often exceeding €50–100 per tonne of CO₂. Securing long-term contracts with emitters will be key to making the hub financially viable.

Public perception is another factor. Some environmental groups argue that CCS could delay the phase-out of fossil fuels by offering a “license to pollute.” Normod Carbon and Danish authorities must demonstrate that the hub supports a shift to a low-carbon economy. It should not replace renewable energy.

Finally, technical hurdles such as ensuring safe transport, storage integrity, and large-scale infrastructure build-out must be addressed. Eventually, the success of Grenaa could serve as a model for other ports across Europe.

Grenaa as Europe’s Net-Zero Gateway

The Grenaa CO₂ hub represents a major investment in Europe’s climate future. Normod Carbon is investing $294 million to create the infrastructure for safe and efficient carbon transport.

As industries across Northern Europe face rising climate regulations and carbon costs, the hub offers a practical solution. It will connect emission sources to storage sites. This will boost Denmark’s CCS leadership and help the EU reach its 2050 net-zero goal.

If completed on schedule, the hub could become a central node in Europe’s emerging carbon management network. It reflects a broader trend of turning ports and industrial hubs into climate infrastructure, ensuring that heavy industries can transition while keeping economic activity alive.

Nike released its earnings for the period ending August 31, 2025. The report showed stronger results than expected, giving investors insight into both its business recovery and its ongoing environmental commitments.

The sportswear company is making financial gains while focusing on its long-term goal: reaching net zero emissions. It aims to cut greenhouse gases (GHG) as part of this effort. Let’s look at Nike’s latest earnings, its climate goals, and its most recent progress on emissions.

Profits Under Pressure, but Revenue Holds Strong

Nike reported revenue of $11.72 billion in its fiscal first quarter of 2025. This represented a small increase of about 1% from the previous year and was stronger than analysts had expected.

Net income for the quarter was $727 million, down roughly 31% compared with the same period last year. While profit margins declined, mainly due to tariffs, higher discounts, and shifts in sales channels, the company still beat Wall Street forecasts.

Gross margin fell to just over 42%, showing that Nike continues to face cost pressures across its operations. Still, the earnings results reflected resilience in consumer demand and Nike’s ability to manage challenges in the global retail market.

After the earnings release, Nike’s stock responded positively. Shares rose 1.5%, reflecting investor confidence in the company’s results. The stronger-than-expected revenue, improved profit margins, and lower inventories reassured markets about Nike’s recovery strategy.

This performance marked one of Nike’s best single-day jumps in 2025, showing how financial momentum and clear progress on operations can quickly influence investor sentiment.

Nike’s “Move to Zero” Playbook

Nike’s sustainability strategy is known as “Move to Zero”, which represents its long-term vision of achieving both net-zero carbon emissions and zero waste. The company has set several science-based targets to guide its environmental goals.

Source: Nike

It has also set a 2030 target to cut absolute Scope 1 and 2 emissions by 65% and Scope 3 emissions by 30% compared to 2015 levels.

Scope 1 emissions are from Nike’s own operations. Scope 2 comes from purchased energy, and Scope 3 includes the larger supply chain, like materials, manufacturing, and shipping. Since most of Nike’s carbon footprint comes from its supply chain, Scope 3 reduction is one of the company’s biggest challenges.

Nike also aligns its goals with the Science Based Targets initiative (SBTi), which ensures climate targets match global pathways to limit warming to 1.5°C.

Cutting Carbon: Wins and Stumbles

Nike’s most recent sustainability report shows mixed progress on its emissions. Here are the major ones:

Scope 1 and 2 emissions:

Nike has cut its Scope 1 and 2 greenhouse gas emissions by 69-73% as of 2023-2024. This is compared to the 2015 baseline. They surpassed their goal of a 65% reduction by 2030. These reductions come from energy efficiency efforts and switching to 100% renewable electricity. This shift is happening in owned and operated facilities in places like North America and Europe.

Source: Nike

Scope 3 emissions:

Nike’s value chain emissions remain the largest part of its carbon footprint, accounting for over 90% of total emissions. Total Scope 3 emissions for 2024 were about 8.2 million metric tons of CO₂e. This marks a 29% reduction since 2020. However, it shows only a small drop from the 2022 and 2023 levels. The company emphasizes material innovation and the use of renewable energy in its supply chain. This is especially true for its Supplier Climate Action Program (SCAP).

Renewable energy use:

The company uses 100% renewable electricity in its North American and European facilities. Globally, it aims for about 78-80% renewable electricity by 2023-2024. This is achieved through power purchase agreements, onsite solar and wind, and green energy options.

Transportation:

Nike has reduced air freight by 80% since 2020. This aligns production with shipping schedules. They are increasing ocean freight usage and aim to ship 50% of products by ocean freight by 2025. This change could cut shipping emissions by around 40%. Pilot projects in Europe are testing hydrogen-fueled barges to support this effort.

These figures show that while Nike is reducing emissions from its direct operations, tackling supply chain emissions remains difficult.

Sneakers Go Green: From Waste to Wear

Beyond emissions, Nike is also working on materials and product design. The company has pledged to cut the environmental impact of its shoes and apparel through innovation.

Nike now uses recycled polyester and organic cotton in many products through its “Move to Zero” program, which includes a focus on zero carbon and zero waste. In 2023, almost 40% of Nike’s polyester came from recycled sources, helping reduce reliance on fossil fuels.

The company also reuses waste from manufacturing. More than 90% of Nike’s footwear manufacturing waste is either recycled or reused. The popular “Nike Grind” program turns scrap materials into new products, like shoe soles or sports surfaces.

Nike has also tested circular design models, such as recycling old shoes into new ones. Its refurbishment program extends the life of products by repairing and reselling lightly worn footwear.

Nike has made real progress, but challenges remain. Scope 3 emissions are still the largest part of its footprint, and reducing them will require deeper changes in supply chain practices. This includes encouraging suppliers to use renewable energy and improving manufacturing efficiency.

Nike also faces growing consumer and regulatory pressure. Governments in Europe and North America are pushing for stricter climate reporting and accountability. Meeting these standards will test Nike’s ability to deliver on its promises.

Still, Nike has shown commitment by tying executive pay to sustainability goals. The company has also joined global climate coalitions, such as RE100, which aims for 100% renewable electricity.

Bridging the Gap: Offsets for Shipping and Beyond

The company offsets 100% of emissions from U.S. and European e-commerce orders, covering shipping from warehouses to customers. In Oregon, it partners with Ecotrust Forest Management on 28,000 acres of forests that capture about 30% more carbon than standard practices. In Europe, it supports reforestation projects that remove carbon through tree planting.

Nike stresses that carbon credit offsets are only a “bridge” and focuses on using projects verified by independent standards to ensure real and lasting results.

Looking ahead, Nike’s financial growth and climate commitments will remain closely linked. Investors are now paying attention to both quarterly earnings and ESG performance. The company’s ability to reduce emissions while maintaining strong revenue will be key to its long-term success.

Where Performance Meets Purpose

Nike’s latest earnings report shows solid financial momentum, with rising revenue, higher profit, and lower inventory levels. At the same time, the company continues to advance its net-zero journey, with major progress on Scope 1 and 2 emissions and renewable energy adoption.

However, its large Scope 3 footprint remains a challenge, making supply chain transformation essential. With strong climate targets, sustainable material use, and innovation in circular design, Nike is positioning itself as both a sportswear leader and a company working toward climate responsibility.

Carbon capture and storage (CCS) is moving from niche pilot projects to a global climate strategy worth billions. Once seen as a backup plan, it’s now racing to the forefront — from massive U.S. industrial hubs to China’s fast-expanding carbon pipelines. Supporters call it essential for tackling the world’s toughest emissions in steel, cement, and energy. Critics warn it could be a costly detour.

As governments, investors, and big tech pour money into CCS, one question looms: can it deliver the deep carbon cuts needed to hit net zero by 2050?

This guide walks you through everything you need to know: how CCS works, the latest technologies, the biggest projects and market leaders, and where the fastest growth is happening.

We’ll also explore market trends, policy drivers, corporate demand, and the risks investors should watch. Whether you’re new to CCS or tracking it as a climate tech opportunity, this resource covers the science, the strategy, and the business potential shaping the future of carbon removal.

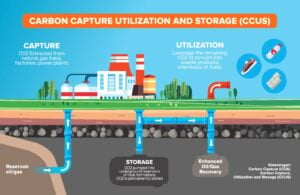

What is Carbon Capture and Storage (CCS)?

Carbon Capture and Storage is a climate technology designed to prevent carbon dioxide (CO₂) from entering the atmosphere. It captures CO₂ emissions from places like power plants, cement factories, and steel mills. This happens before the emissions can add to global warming.

A related term is Carbon Capture, Utilization, and Storage (CCUS). It takes things further by using captured CO₂ in products like synthetic fuels, building materials, or plastics.

The key difference between CCS and CCUS lies in the “U” — utilization. In CCS, the captured CO₂ is permanently stored underground, while in CCUS, part or all of that CO₂ is repurposed for industrial use before storage.

This technology helps fight climate change. It can reduce emissions from hard-to-decarbonize industries. The Intergovernmental Panel on Climate Change (IPCC) and the International Energy Agency (IEA) both recognize CCS as a critical tool for achieving net-zero targets.

Global climate agreements, like those at the annual UN Climate Change Conferences (COP), stress that CCS is key to limiting global temperature rise to below 1.5°C.

CCS works in three main stages — capture, transport, and storage — with an optional fourth step for utilization. Let’s break down each one of them.

Source: Shutterstock

Capture: The process starts by separating CO₂ from other gases produced during industrial processes or electricity generation. This can be done at power plants, cement kilns, oil refineries, and other facilities. Special chemical solvents, membranes, or advanced filters are used to remove CO₂ from flue gas or fuel before combustion.

Transport: Once captured, CO₂ must be moved to a storage or utilization site. The most common method is through high-pressure pipelines. In some cases, ships or even trucks carry CO₂ over long distances, especially if storage sites are far from industrial hubs.

Storage: For permanent storage, CO₂ is injected deep underground into geological formations such as saline aquifers or depleted oil and gas fields. These sites are chosen for their ability to trap CO₂ securely for thousands of years, with monitoring systems in place to detect any leaks.

Utilization: In CCUS projects, some or all of the captured CO₂ is reused instead of being stored immediately. It can be converted into synthetic fuels, used in making cement and plastics, or even injected into greenhouses to boost plant growth. While utilization does not always result in permanent storage, it can reduce the need for fossil-based raw materials.

Tech Toolbox: The Many Ways of Capturing Carbon

CCS is not a single technology. Different methods are used depending on the type of facility, the fuel being used, and the stage at which CO₂ is removed. The main types are:

Post-combustion capture: This is the most common method today. CO₂ is removed from the exhaust gases after fuel has been burned. Chemical solvents or filters separate the CO₂ from other gases before it is compressed for transport.

Pre-combustion capture: Here, the fuel is treated before it is burned. The process converts the fuel into a mixture of hydrogen and CO₂. The CO₂ is separated and stored, while the hydrogen can be used to produce energy without direct emissions.

Oxy-fuel combustion: In this method, fuel is burned in pure oxygen instead of air. This creates a stream of exhaust that is mostly CO₂ and water vapor, making it easier to capture the CO₂.

Direct Air Capture (DAC): DAC removes CO₂ from the air instead of just one source. It uses big fans and chemical filters to do this. It can be used anywhere but requires more energy because CO₂ in the air is less concentrated.

As of end-2024, around 53 DAC plants were expected to be operational globally, rising to 93 by 2030 with a capacity of 6.4–11.4 MtCO₂/year.

Bioenergy with CCS (BECCS): This approach combines biomass energy production with carbon capture. Plants absorb CO₂ while growing, and when the biomass is burned for energy, the emissions are captured and stored. This can result in “negative emissions,” removing CO₂ from the atmosphere.

Global Race: Which Countries Are Winning CCS Leadership

Carbon capture and storage is now a reality. It’s in operation in many countries, with numerous projects either planned or being built. CCS technology is still new compared to global emissions. But momentum is growing.

Governments, industries, and investors are now committing to large-scale deployment. CCS capacity differs between regions:

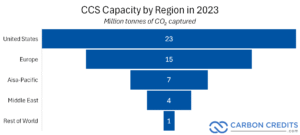

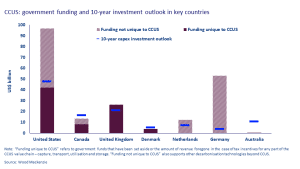

United States

The U.S. leads CCS deployment, holding about 40% of global operational capacity. By mid-2024, facilities captured roughly 22–23 Mt CO₂ annually. Growth is driven by the expanded 45Q tax credit under the Inflation Reduction Act, rewarding storage and utilization. Flagship projects include Petra Nova in Texas and Midwest CCS hubs serving ethanol, fertilizer, and industrial sites.

Canada

Canada hosts pioneering projects like Boundary Dam (the world’s first commercial coal CCS) and Quest in Alberta, capturing CO₂ from hydrogen linked to oil sands. National capacity is ~4 Mt per year, supported by a federal CCS investment tax credit targeting heavy industry and clean hydrogen.

Norway

Norway has led offshore CO₂ storage since the Sleipner project began in 1996, injecting ~1 Mt annually into a saline aquifer. The Northern Lights project, part of Longship, will create a shared CO₂ transport and storage network for European industries.

China

China’s CCS capacity grew from ~1 Mt/year in 2022 to over 3.5 Mt in 2024, mainly in coal-to-chemicals, gas processing, and EOR. CCS is now part of national climate strategies, signaling rapid expansion.

United Kingdom

The UK’s cluster model links industries via shared pipelines and offshore storage. The East Coast Cluster and HyNet, due late 2020s, could together capture over 20 Mt CO₂ annually.

Australia

Australia’s ~4 Mt/year capacity includes the massive Gorgon gas-linked CCS facility in Western Australia, despite operational setbacks. With vast geological storage potential, the country aims to be a CO₂ storage hub for Asia’s export industries.

Total Operational Capacity and Growth

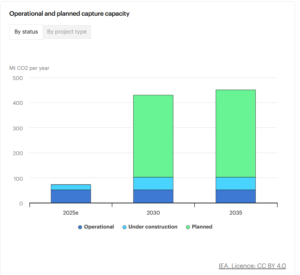

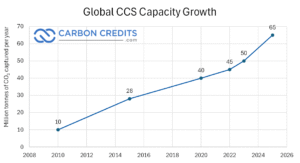

As of 2024, global CCS facilities in operation had a combined capture capacity of just over 50 million tonnes of CO₂ per year. This shows steady growth, up from about 40 Mt a few years ago. However, it still accounts for just a small part of the over 40 billion tonnes of CO₂ emitted worldwide each year.

However, the project pipeline is expanding quickly. The facilities being built will double the current capacity. Early development projects might raise global capacity to over 400 million tonnes per year by the early 2030s if they stay on track.

The Rise of CCS Hubs and Clusters

A key trend in the industry is the creation of CCS hubs—shared infrastructure networks where multiple companies use the same transport and storage systems. This model lowers costs and speeds up deployment by avoiding the need for every facility to build its own pipeline or storage site.

The U.S. Midwest ethanol corridor, Norway’s Northern Lights, and the UK’s industrial clusters are among the most advanced examples. These hubs usually form close to industrial areas. Here, emissions are high, and the current infrastructure, like pipelines and ports, can be adjusted for CO₂ transport.

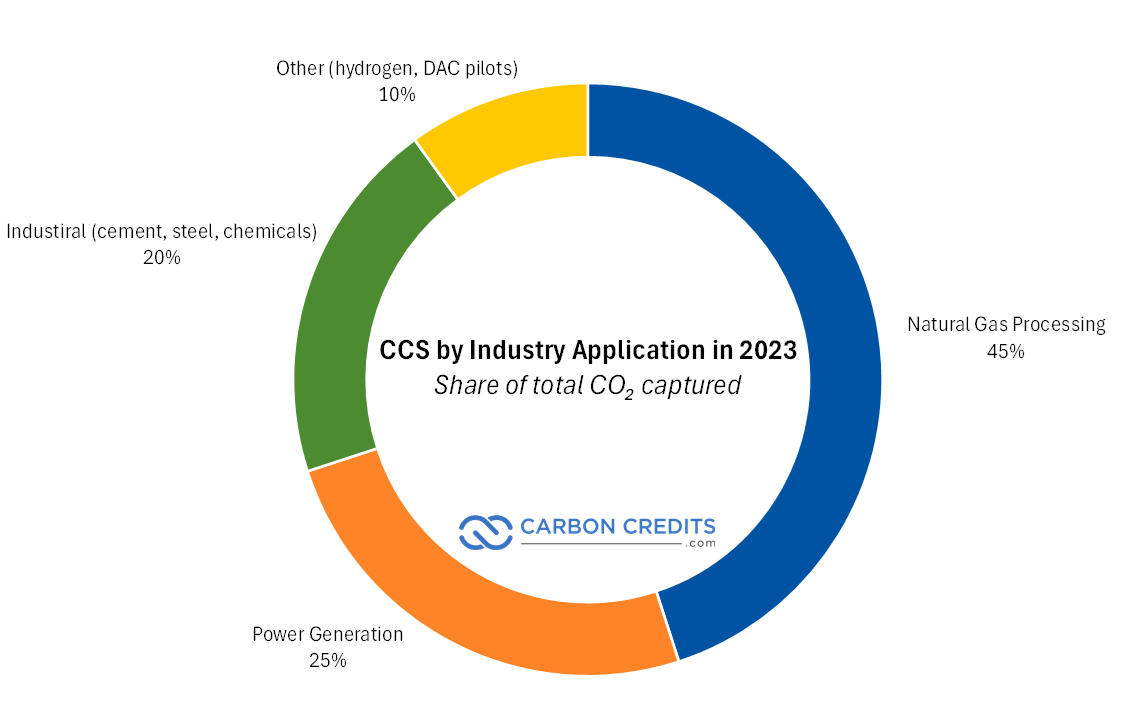

Carbon capture and storage is not meant to replace renewable energy or other climate solutions. Instead, it focuses on the toughest parts of the emissions problem—places where cutting CO₂ is especially hard or expensive. Experts call these hard-to-abate sectors.

Hard-to-Abate Sectors

Some industries can’t simply switch to clean electricity. For example, making steel requires very high heat and chemical reactions that release CO₂. Cement production also releases CO₂ as a byproduct of making clinker, the key ingredient in concrete.

Chemical plants and refineries have complex processes that generate large amounts of CO₂. Even aviation faces limits, since planes can’t yet fly long distances on batteries alone. CCS can capture emissions from these sources. This helps reduce climate impact while keeping production running.

Here is the technology’s application in various industries:

Role in Meeting the 1.5°C Target and Net-Zero by 2050

To avoid the worst effects of climate change, scientists say global warming must be kept to 1.5°C above pre-industrial levels. That means reaching net-zero emissions by around 2050.

The Intergovernmental Panel on Climate Change (IPCC) has run hundreds of models to see how this can be done. In most scenarios, CCS plays a key role. Without it, the cost of meeting climate targets could rise by 70% or more, because other solutions would have to carry the full load.

Synergies with Clean Hydrogen, Carbon Markets, and Industrial Strategy

CCS also works well with other low-carbon solutions. CCS captures CO₂ that would escape when producing clean hydrogen, especially “blue hydrogen” from natural gas. This creates a cleaner fuel for use in transport, heating, and industry.

In carbon markets, CCS can generate credits for each tonne of CO₂ captured and stored. These credits can be sold to companies looking to offset their emissions. Governments are also linking CCS to industrial strategy by building shared hubs and pipelines. These will serve multiple factories, power plants, and fuel producers. This makes CCS cheaper and faster to deploy.

Endorsements from the IEA and UN

The International Energy Agency (IEA) calls CCS “critical” for reaching net zero, especially in heavy industry. It estimates the world will need to store 1.2 billion tonnes of CO₂ each year by 2050.

The United Nations also recognizes CCS in its climate plans. It has been featured in multiple COP agreements as a key technology for both reducing emissions and removing CO₂ from the atmosphere. These endorsements matter because they help drive policy support, funding, and international cooperation.

CCS Investment and Financing: How Much Does It Cost?

Carbon capture and storage can make a big impact on emissions. But it comes with a high price tag. Most projects cost between $50 and $150 for every tonne of CO₂ (and even over $400 for some technologies) captured and stored.

The lower end usually applies to large industrial sites near storage locations. The higher end often applies to smaller or more complex projects, or those that require long transport pipelines.

Government Support

Governments play a key role in making CCS affordable. In the U.S., the 45Q tax credit offers up to $85 per tonne for CO₂ stored underground and $60 per tonne for CO₂ used in other industrial processes.

Canada provides an Investment Tax Credit (ITC) covering up to 50% of eligible CCS costs. In Europe, the Innovation Fund supports early-stage CCS and other low-carbon projects, offering billions in grants.

Blended Finance and Partnerships

Because CCS is expensive, many projects rely on blended finance—a mix of public and private funding. Oil and gas companies invest in cutting carbon emissions. Meanwhile, governments help by offering grants and tax breaks.

Public-private partnerships are common, especially for shared CCS hubs where multiple companies use the same pipelines and storage sites. International lenders, such as the World Bank and the Asian Development Bank, are funding CCS in emerging economies.

Voluntary Carbon Market (VCM)

CCS can also generate carbon removal credits for sale in the voluntary carbon market. These credits are purchased by companies aiming to offset their emissions.

While VCM prices vary, high-quality removal credits often sell for $100 per tonne or more, making them a potential revenue stream for CCS operators. Market demand for CCS-based credits is still growing. It relies on trust in the technology’s monitoring and verification.

Interest in carbon capture and storage is rising among ESG, climate tech, and energy transition investors. The global CCS market was valued at about $4.5 billion in 2023 and could grow to more than $20 billion by 2033, according to industry forecasts. This growth is being driven by stricter climate policies, corporate net-zero pledges, and rising carbon prices.

Public Stocks

Investors can buy shares in companies directly involved in CCS. Examples include Aker Carbon Capture (Norway), Occidental Petroleum (U.S.), Air Liquide (France), and ExxonMobil.

Many oil and gas majors now see CCS as essential to keeping their assets viable in a low-carbon future. These firms are investing billions in CCS hubs and carbon removal partnerships.

Private Startups

Private markets offer exposure to emerging technologies like DAC. Leading firms include Climeworks (Switzerland), CarbonCapture (U.S.), and Heirloom (U.S.).

DAC projects are smaller today but attract premium interest from tech backers and climate-focused venture capital. In 2022 alone, DAC startups raised over $1 billion in funding.

ETFs and Funds

There are also climate-focused ETFs and funds that include carbon removal technologies as part of their portfolios. These funds reduce risk by investing in various companies. They focus on CCS, renewable energy, hydrogen, and other low-carbon solutions.

Carbon Credit Markets

Some investors buy into CCS through the carbon credit market. This can be done by funding CCS or DAC projects that issue carbon removal credits.

Platforms like Puro.earth and CIX (Climate Impact X) connect investors with verified carbon removal projects. Credits from high-quality CCS projects can fetch $100–$200 per tonne depending on location and verification standards.

Due Diligence

Before investing, it is important to check policy risk, technology readiness, cost curves, and scalability. CCS works best in large industrial hubs with access to geological storage. Finally, watch these key sectors because they will likely drive demand and scale for CCS:

The oil & gas sector uses CCS for enhanced oil recovery and to lower its emissions.

Cement firms need CCS because their production process emits CO₂ that can’t be avoided easily.

Hydrogen—especially blue hydrogen—depends on CCS to cut its carbon footprint.

DAC startups aim to remove CO₂ directly from the air and may sell high-value removal credits.

And carbon marketplaces and registries will shape how removal credits are priced and trusted.

These areas have the most potential to scale quickly as policies tighten and carbon prices rise.

Risks, Challenges, and Criticism of CCS

While CCS has strong potential as a climate solution, it faces several challenges that investors, policymakers, and project developers must consider.

High Capital Costs and Slow ROI: Large CCS projects cost hundreds of millions to billions of dollars. At $50–$150 per tonne captured, returns depend on strong policy support, carbon pricing, or premium credits, with payback periods often spanning years.

Energy Requirements and Lifecycle Emissions: CCS uses significant energy, sometimes from fossil fuels. Without low-carbon power, net emissions savings shrink, making efficiency improvements essential.

Storage Risks: Leakage, Permanence, and Monitoring: Geological storage is generally safe, but leakage is possible. Continuous monitoring ensures CO₂ remains underground for centuries.

Debate Over Fossil Fuel Dependency vs. Genuine Decarbonization: Critics say CCS can prolong fossil fuel use. Supporters argue it’s vital for industries like cement and steel.

Policy Uncertainty and Lack of Global Standards: Policy changes can undermine project economics. The absence of global CO₂ measurement standards adds risk to cross-border investments.

Market Outlook (2024–2030): What’s Next for CCS?

The world is gearing up for a big expansion in carbon capture and storage. But just how fast will CCS grow—and what could power that growth?

Growing CCS Pipeline and Capacity

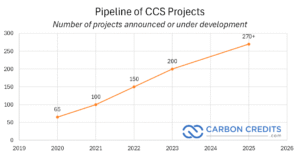

Momentum is clearly building. The Global CCS Institute reports a record 628 projects in the pipeline—an increase of over 200 from the previous year.

The expected annual capture capacity from these projects is 416 million tonnes of CO₂. This amount has been growing at a 32% rate each year since 2017. Once the current construction is completed, operational capacity is set to double to more than 100 Mt per year.

Similarly, the IEA sees global capture capacity rising from roughly 50 Mt/year today to about 430 Mt/year by 2030, with storage capability reaching 670 Mt/year.

Still, this is only a start. To meet global climate goals, CCS will need to scale much more, lasting into the billions of tonnes annually.

Policies Fueling Momentum

Governments are shoring up policy support to accelerate CCS rollout. Here are the regional trends so far:

In the U.S., the Inflation Reduction Act (IRA) expanded the 45Q tax credit—making CCS more financially appealing for project developers.

The EU’s Net-Zero Industry Act and updated Industrial Carbon Management Strategy aim to help the region capture at least 50 Mt by 2030, rising to 280 Mt by 2040.

Across the Asia-Pacific, countries like Australia are positioning themselves as carbon storage hubs. With strong geology and policy backing, Australia could generate over US$500 billion in regional carbon storage revenue by 2050.

Corporate Buyers Powering Demand

Major companies are not just talking—they’re signing deals:

Microsoft stands out as a leading buyer of carbon removal credits. It has contracted close to 30 million tonnes. This includes 3.7 million tonnes over 12 years with startup CO280 and 1.1 million tonnes in a 10-year deal with Norway’s Hafslund Celsio project.

Shopify co-founded Frontier—a $925 million advance market commitment—with other big names like Stripe and Alphabet. It has also purchased over $80 million in carbon removal from startups using DAC, enhanced weathering, and other technologies.

These corporate purchases show a strong demand for CCS-backed removal credits. They also help build a stable market for project developers.

CCS is also benefiting from broader climate market trends:

Carbon pricing and trading systems globally are starting to include CCS credits. As prices rise, CCS projects can improve their economics.

ESG reporting and net-zero commitments are increasing transparency and accountability. Firms are expected to show real results—CCS helps deliver that.

The rise of international carbon markets and registries is creating standardized ways to value and certify carbon removals. This makes CCS credits more trustworthy and investable.

Quick Take

By 2030, CCS capacity could rise eightfold—from 50 million to over 400 million tonnes. This growth is being driven by government policy, big corporate offtake deals, and a maturing carbon credit market. While still far from what’s needed to fully tackle climate change, the CCS sector is clearly moving from pilot stage to commercial reality

The Role of CCS in a Net-Zero Future

CCS isn’t a silver bullet. It’s a vital tool that works with renewables, electrification, and nature-based solutions like reforestation.

Renewables stop future emissions. CCS tackles the emissions that still exist, especially from old infrastructure in steel, cement, and chemicals. These are costly and slow to replace.

CCS captures emissions at the source. This helps extend facility lifespans and supports climate goals. It’s especially important for economies with new industrial assets.

Beyond reduction, CCS can enable permanent carbon removal through direct air capture and bioenergy with CCS, storing CO₂ underground for centuries. These methods can offset hard-to-abate sectors such as aviation and agriculture.

Responsible deployment is key. It needs strong MRV standards, community engagement, and alignment with sustainability goals. This helps avoid delays in phasing out fossil fuels.

CCS, when used wisely, connects our current fossil fuel economy to a low-carbon future. It helps reduce emissions we can’t fully eliminate yet and gives us time to develop cleaner technologies.

CCS is Not a Silver Bullet—But a Vital Tool

Carbon capture and storage is not a cure-all for the climate crisis. No single technology can deliver net zero on its own, and CCS should be viewed as one tool in a broader decarbonization toolkit.

A balanced approach requires acknowledging both the potential and the limitations of CCS. The technology can cut emissions and even remove carbon permanently when it’s based on solid science, strong policies, and clear reporting.

However, overreliance or misuse—particularly if it delays the shift away from fossil fuels—risks undermining climate goals.

The pathway to net zero will demand a combination of innovation, investment, and urgency. Carbon capture and storage is part of that solution set, and with careful governance, sustained funding, and clear standards, it can help bridge the gap between today’s emissions reality and the low-carbon future we urgently need.

A new community-led carbon initiative has launched in Zambia. Its goal is ambitious: to remove up to 2 million tonnes of CO₂ each year by 2030. This project, called The Ecopreneur Movement – Miombo Woodland Restoration Project, is led by Community Climate Solutions (CCS) and backed by Climate Impact Partners.

The initiative empowers 240,000 Zambians to create sustainable livelihoods while restoring degraded ecosystems. Farmers, trained as “Ecopreneurs,” play a crucial role. They are revitalizing Zambia’s Miombo Woodlands, vital carbon sinks, through tree planting, sustainable farming, and fire prevention.

Located in the Kazungula District, this 185,000-hectare initiative restores wildlife corridors between Kafue and Mosi-oa-Tunya National Parks.

The 40-year project aims to deliver 2.9–6 million verified carbon credits while supporting 23 communities.

Long-Term Community and Ecological Benefits

The project uses various restoration methods, including:

Assisted natural regeneration of degraded woodlands

Indigenous tree nurseries for planting

Fire breaks and buffer zones

Watershed rehabilitation for water security

Communities benefit from programs like climate-smart farming, sustainable beekeeping, and eco-friendly businesses. This ensures carbon revenues are not the only source of resilience.

Source: Eden People + Planet

A Model That Puts Communities First

The project prioritizes community benefits. Farmers receive upfront payments for eco-services through CCS seed funding. Once carbon revenues arrive, 60% of the proceeds, after fees, return to the farmers and their communities.

Currently, 25,000 farmers have joined, and this number is expected to double by 2025. This growth supports one of Sub-Saharan Africa’s most ambitious restoration efforts.

By the decade’s end, the program aims to plant 30 million native trees and reach the 2-million-tonne CO₂ target.

Source: Eden People+Planet

Two Pillars of Restoration

Farmers use two key strategies:

Introducing Native Trees to Farmlands: Adding trees to cropland improves soil, boosts food production, and captures carbon.

Restoring Miombo Woodlands: Farmers encourage natural regrowth, plant native species, and apply fire-prevention techniques to enhance biodiversity.

This dual approach increases productivity and resilience, linking environmental gains to livelihoods.

Transparency and Integrity at Scale

To ensure credibility, the project employs satellite monitoring alongside local field checks. Key indicators include fire reduction, woody biomass growth, and soil carbon accumulation.

Digital payments are tracked, and project revenues will be publicly reported and audited. The program will register under Verra’s reforestation methodology (VM0047), aligning with the Core Carbon Principles. It also aims for the ABACUS quality label at initial verification.

Carbon credits are expected to start in 2027, with verified removals over a 40-year lifespan.

The Musokotwane-Nyawa project uses blended finance, combining philanthropy with carbon market mechanisms. It expects to channel about $90.8 million into restoration efforts.

Preparations are underway. By Q1 2026, the program will be fully implemented, planting 800,000 native trees and establishing fire prevention measures.

Tackling Drivers of Deforestation

Zambia’s Miombo ecosystems face pressure from slash-and-burn farming, unsustainable logging, and charcoal production. These practices harm landscapes, reduce biodiversity, and increase greenhouse gas emissions.

Both projects aim to reverse this. By restoring Miombo woodlands and protecting natural growth, they offer communities sustainable alternatives that lessen forest pressure.

Zambia’s Roadmap for Carbon Markets and Forest Conservation

These initiatives align with Zambia’s Eighth National Development Plan and the Green Economy and Climate Change Act of 2024. This framework regulates carbon markets, protects ecosystems, and directs funds toward climate resilience.

Zambia is also a pilot for the REDD+ mechanism, benefiting from international funding to protect forests. With 49 million hectares of forest, the country is poised to lead in high-integrity carbon projects.

Investment Potential: A Green Goldmine

Zambia contributes about 6% of Africa’s carbon credit output and 0.7% globally. The potential is vast: Africa’s carbon markets could generate $6 billion annually by 2030, creating 30 million green jobs, according to the Africa Carbon Markets Initiative.

The global voluntary carbon market, valued at $331.8 billion in 2022, is projected to grow 31% annually from 2024 to 2028. Major companies like TotalEnergies and ENI are showing interest in Zambia’s market, attracting significant investment.

Both initiatives aim for more than just carbon removal. They seek to:

Restore biodiversity by reviving habitats

Enhance food security through climate-smart farming

Minimize wildfire risk and protect watersheds

Boost household incomes through carbon revenues and new ventures

Safeguard wildlife corridors vital for conservation across Southern Africa

This holistic approach makes Zambia’s Miombo woodland projects unique in the voluntary carbon market.

With carbon credits set to issue from 2027, Zambia’s community-led restoration projects are unlocking grassroots climate solutions. By combining community leadership, scientific methods, and innovative funding, they remove millions of tonnes of CO₂ while also promoting sustainable economic growth in rural Zambia.

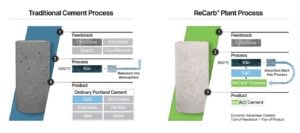

Microsoft (NASDAQ: MSFT) is stepping deeper into climate action by targeting two of the world’s most emissions-intensive industries: cement and steel. The company invested in Fortera, a U.S. startup making low-carbon cement, and signed new agreements with Stegra, a European producer of green steel.

These efforts support Microsoft’s 2030 goal to become carbon negative and its plan to cut supply chain emissions. Since cement and steel are core to buildings and technology, new solutions in these materials are key to global decarbonization.

Microsoft Backs Green Cement with Fortera

Cement production causes 7–8% of global CO₂ emissions, mainly from heating limestone and powering kilns. Fortera uses a new process that locks carbon into the cement itself. This can cut emissions by up to 60% compared to traditional methods.

Source: Fortera

Microsoft’s funding supports this innovation and signals corporate demand for cleaner building materials. The company can use green cement for offices, data centers, and infrastructure.

The global green cement market was worth about $28 billion in 2024. It is forecast to nearly double to $60 billion by 2032, growing at a rate of over 9% per year. Demand is rising due to stricter climate rules, more construction, and corporate sustainability targets. Microsoft’s move shows how tech giants can shape this market.

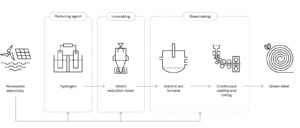

Microsoft and Stegra: Green Steel for Data Centers

Steelmaking is another hard-to-abate sector, responsible for around 7% of global energy-related CO₂ emissions. Traditional steel production uses coal. However, new methods are emerging. Hydrogen-based direct reduction and electric arc furnaces powered by renewable energy offer cleaner alternatives.

Microsoft’s new deals with Stegra aim to secure green steel for its data centers, hardware production, and corporate facilities. Stegra makes steel with renewable electricity and low-emission methods. This cuts emissions by up to 90% compared to regular steel. For Microsoft, this partnership helps reduce Scope 3 emissions, which come from the materials and products in its supply chain.

Source: Stegra

The global green steel market is just starting out. It’s expected to hit over $760 billion by 2030. This growth is driven by rising demand from construction, automotive, and tech companies. Europe leads in green steel production thanks to strong government policies and carbon pricing. However, the U.S. and Asia are gaining momentum, too.

Source: Grand View Research

Corporate Demand and Industry Shifts

Microsoft’s actions reflect a broader shift among global companies. Many are now pushing suppliers to provide low-carbon materials. Science-based climate targets cover not only direct emissions but also entire supply chains.

Key industry shifts include:

Corporate procurement power: Companies like Microsoft, Apple, and Amazon are committing to buying greener materials, creating demand for innovation.

Policy drivers: The EU’s Carbon Border Adjustment Mechanism and U.S. Inflation Reduction Act incentives are accelerating clean material adoption.

Investment flows: Global investment in clean industrial technologies reached over US$150 billion in 2024, according to the International Energy Agency, with strong growth expected through 2030.

This combination of corporate demand, public policy, and capital flows is reshaping industries once seen as difficult to decarbonize.

Microsoft has set some of the most ambitious climate goals among global technology companies. In 2020, it announced plans to become carbon negative by 2030, meaning it will remove more carbon from the atmosphere than it emits.

Source: Microsoft

By 2050, it aims to erase all of its historical emissions since its founding in 1975. To achieve this, the company is cutting direct emissions. It is also investing in renewable energy, carbon removal technologies, and low-carbon supply chains.

A major part of Microsoft’s plan involves reshaping the materials it uses across its global operations. Steel and cement account for nearly 15% of global carbon emissions. They are essential for data centers, offices, and product supply chains.

By supporting low-carbon producers like Fortera and Stegra, Microsoft is addressing these hard-to-abate sectors. If successful, these partnerships will lower Microsoft’s footprint. They will also create scalable solutions for other companies to adopt.

Microsoft is also driving progress in its broader ecosystem. Its Cloud for Sustainability platform gives businesses tools to track and cut emissions. This creates a vital connection between climate promises and real results. This shows how Microsoft is working on both sides of the challenge: cutting its own emissions while helping other organizations do the same.

The company’s climate strategy is also closely tied to investor expectations. ESG-focused funds now manage more than $600 billion worldwide. Companies with solid net-zero plans are gaining favor among institutional investors.

Microsoft’s ability to show progress gives it an advantage in attracting long-term capital while strengthening its reputation as a leader in climate action.

Outlook: Why Microsoft’s Bets Could Reshape Industries

The global clean materials market is entering rapid growth. The International Energy Agency (IEA) reports that annual clean energy investment hit US$1.8 trillion in 2023. It could reach more than US$4.5 trillion by 2030 if countries meet climate targets.

Cement and steel will be vital. By 2050, they could account for more than 20% of all carbon cuts needed. This makes them top targets for innovation and new business models.

Over 6,000 companies worldwide have now set science-based targets. Many are pressuring their suppliers to deliver cleaner products. This could push demand for green cement and steel far faster than the current supply. Microsoft’s early partnerships put it ahead of the curve.

For Microsoft, the benefits are twofold: lower emissions and reduced risk from future carbon rules. Using cleaner materials in data centers, AI facilities, and logistics will also make its operations more resilient.

The tech giant’s deals with Fortera and Stegra show that green materials are moving beyond small pilots into real, large-scale use. This momentum could reshape whole industries in the years ahead.

Amazon (NASDAQ: AMZN) has announced a major renewable energy deal in the United States, partnering with Avangrid on a $100 million solar project. The development will add clean electricity to the U.S. grid and further support Amazon’s climate goals.

The agreement highlights the growing role of large corporations in driving clean energy demand. Amazon is one of the biggest buyers of renewable energy in the world. It is quickly growing its solar and wind portfolio.

Amazon signs long-term power purchase agreements (PPAs) to secure renewable electricity. This also helps developers like Avangrid get the funds they need to build large projects.

Net-Zero by 2040: Amazon’s Big Climate Goals, and Bigger Challenges

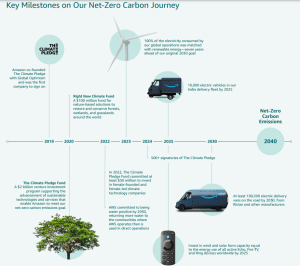

Amazon aims to reach net-zero carbon emissions by 2040. It also plans to run all operations on 100% renewable energy by 2025, a target it says it is close to achieving.

Source: Amazon

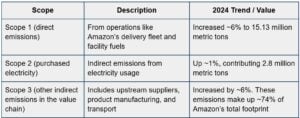

But Amazon’s emissions profile shows how hard this goal is. In 2024, the company’s total greenhouse gas emissions rose by 6%, reaching 68.25 million metric tons of CO₂ equivalent. That marked a reversal after years of reductions. All scopes saw increases.

Source: Amazon

Here is how the emissions break down: Despite the growth in absolute emissions, Amazon says it improved its carbon intensity (emissions per unit of business) by 4% in 2024.

Source: Amazon

Amazon explains its carbon footprint calculation using the GHG Protocol. It includes direct operations, energy use, and activities in the value chain. This covers product manufacturing, logistics, packaging, and more.

To reduce its impact, Amazon has taken multiple steps:

Matching electricity use with renewable energy: In 2024, Amazon used 100% renewable energy for all its data centers and facilities.

Investing in renewable capacity: As of early 2025, Amazon had invested in 621 renewable projects, amounting to 34 GW of carbon-free energy capacity.

Storage and grid support: Amazon pairs solar projects with battery energy storage systems, enabling more stable renewable energy integration.

Efficiency in data centers: Amazon’s AWS data centers reported a Power Usage Effectiveness (PUE) of 1.15, better than many industry averages.

Innovation in cooling and design: New data center components launched in 2024 provided 12% more compute power. They also reduced peak cooling energy use by 46% without increasing water usage.

These actions show the e-commerce giant is not just buying clean power, but trying to redesign how it uses energy.

Avangrid, part of the Iberdrola Group, is one of the largest renewable energy companies in the United States. Its $100 million investment in the new solar project underlines the scale of capital required to expand America’s clean power supply.

The company currently operates more than 8.6 gigawatts (GW) of renewable capacity in the U.S., including wind and solar. By partnering with Amazon, Avangrid gets a steady buyer for its electricity. This deal also speeds up the growth of renewable infrastructure. This helps meet both state and national clean energy goals.

This project also illustrates how large tech and energy firms can work together. Amazon’s demand provides a stable revenue stream, and Avangrid gains the capital certainty to build more solar capacity. Over time, similar deals can help accelerate the transition of the U.S. power grid to cleaner sources.

Scaling renewable energy helps Amazon in two ways:

It reduces operational emissions (Scope 2) in regions where Amazon operates.

It supports grid decarbonization, which benefits all electricity users—including Amazon’s neighbors and future expansions.

How Corporate Demand Supercharges Renewable Growth

The deal comes at a time when renewable energy investment in the U.S. is accelerating. The International Energy Agency (IEA) reports that global clean energy investment hit $3.3 trillion in 2025. This amount surpassed spending on fossil fuels.

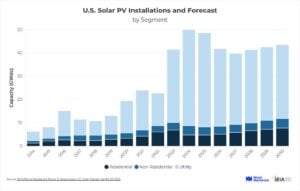

The U.S. remains a key market, with solar power installations alone expected to grow by more than 40 GW annually through 2030.

Source: SEIA

Corporations are an important driver of this trend. Companies now hold a larger share of renewable PPAs. This shift comes as investors, regulators, and consumers demand stronger climate commitments. Amazon has been the biggest buyer of renewable electricity worldwide since 2020.

Amazon’s deal with Avangrid sends a strong signal to the renewable sector. Corporate demand for clean power gives developers and financiers long-term certainty. This certainty helps make scaling projects easier. As more companies set science-based climate targets, the renewable PPA market is expected to keep expanding.

Industry forecasts say that corporate PPAs might make up 20–25% of new renewable capacity by 2030. Amazon’s scale gives it an outsized role in shaping this market. The company partners with developers like Avangrid. This helps unlock capital and speeds up the clean energy transition.

Amazon’s Hardest Climate Challenge

Amazon leads in renewable procurement, but it faces big challenges in hitting its 2040 net-zero target. The majority of its emissions come from Scope 3 sources, including suppliers, logistics, and product use by customers.

While renewable energy agreements cover operational electricity, tackling emissions across Amazon’s vast value chain will need deeper collaboration with partners and new technologies.

Analysts point out that Amazon’s total emissions haven’t dropped consistently. This shows the struggle between fast business growth and climate goals. For instance, even with renewable progress, Amazon’s overall footprint grew steadily during its years of fastest e-commerce expansion.

Balancing E-Commerce Expansion with Carbon Cuts

Amazon’s renewable energy strategy, like solar, is both a business and environmental decision. Access to low-cost clean power reduces long-term energy risks, while also positioning the company as a leader in climate action.

Partnerships with Avangrid and other developers boost the U.S. renewable energy market. They show that when companies demand clean energy, it can quicken the shift to clean electricity.

The U.S. renewable sector is set for strong growth in 2025, led by wind and storage, per S&P Global analysis. Wind power additions are projected at 15.7 GW, up 73% from 2024’s 9.1 GW. Energy storage is expected to triple, surging from 14.5 GW in 2024 to nearly 44 GW in 2025.

However, S&P Global cautions that some large wind and solar projects may face delays, with in-service dates potentially shifting beyond 2025. Overall, broad-based gains highlight accelerating momentum in the U.S. clean energy transition.

For Amazon, the challenge ahead lies in balancing growth with deeper emissions cuts. The Avangrid solar project represents progress, but a broader supply chain transformation will be needed to meet the 2040 net-zero target.

As more corporations follow Amazon’s lead, the renewable energy landscape in the U.S. is set for continued expansion. The success of these partnerships will help determine whether the country can meet its clean power goals and maintain momentum in the global shift away from fossil fuels.

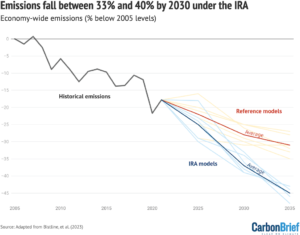

The U.S. government, through the Department of Energy, intends to cancel $13 billion in federal funds that were originally set aside for clean or green energy projects. This decision marks one of the largest reversals in clean energy financing since the passage of the Inflation Reduction Act (IRA) in 2022.

The IRA is seen as the biggest climate law in U.S. history. It offers nearly $370 billion in tax credits, grants, and loans for clean energy. With the $13 billion withdrawal, questions are popping up about the U.S. energy transition. Many are wondering if the nation can still meet its climate goals.

The move comes at a critical time. U.S. renewable energy deployment has accelerated in recent years, with solar, wind, and battery storage all expanding.

The U.S. Energy Information Administration (EIA) reports that renewables made up about 24.2% of electricity in 2024. This number could rise to 26% by 2025. However, this progress relies heavily on federal support. The cancellation of billions in funding could slow growth in some areas and introduce uncertainty for investors.

The Inflation Reduction Act and Its Role

The IRA created a powerful framework to support the clean energy economy. It provided tax credits for wind and solar projects. It also gave incentives for making renewable components in the United States. Plus, there was funding for hydrogen, carbon capture, and nuclear innovation.

Analysts estimate that the IRA could cut U.S. greenhouse gas emissions by 40% from 2005 levels by 2030. This would help the country move closer to its net-zero goal for 2050.

The $13 billion cut, however, alters this pathway. Much of the funding was expected to go toward loan guarantees, manufacturing incentives, and rural energy support programs. Without this, developers could face higher costs and financing risks. The cancellation also signals political challenges to sustaining long-term climate policies.

The U.S. DOE stated:

“By returning these funds to the American taxpayer, the Trump administration is affirming its commitment to advancing more affordable, reliable and secure American energy and being more responsible stewards of taxpayer dollars.”

Impact on Renewable Energy Development

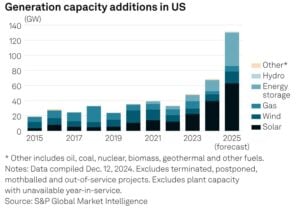

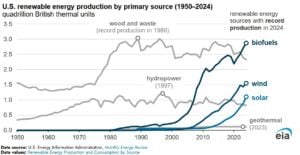

The U.S. renewable sector has been scaling rapidly. In 2024, the country added around 33 GW of solar and wind capacity, one of the highest yearly totals on record, per EIA. Battery storage is also growing fast, with capacity expected to triple from 14.5 GW in 2024 to 44 GW in 2025, according to S&P Global.

Source: EIA

Pulling $13 billion from the funding pool could have several impacts:

Wind and solar projects may see slower financing approvals, particularly in rural and utility-scale developments.

Manufacturers of solar panels, wind turbines, and batteries could lose incentives that made U.S. production competitive with China and Europe.

Grid modernization and transmission upgrades may face delays, even as demand for electricity rises with the growth of data centers and electric vehicles.

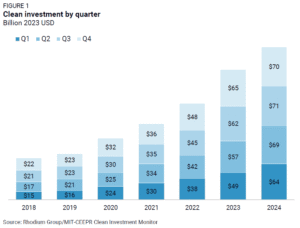

Industry groups warn that this reduction could affect project timelines. The American Clean Power Association says that long-term certainty is key to keeping private investment strong. In 2024, investments or funding in U.S. clean energy and storage projects topped $272 billion.

Source: Clean Investment Monitor’s Q4 2024 Report

Climate Targets and Emissions Outlook

The U.S. has committed under the Paris Agreement to cut emissions by 50–52% below 2005 levels by 2030. Progress has been steady but uneven.

The EIA reports that total U.S. energy-related carbon dioxide emissions stood at 4.77 billion metric tons in 2024, about 17% below 2005 levels. This shows a slight decline from 2023 emissions of around 4.79 billion metric tons. Reductions are largely driven by fuel switching in power generation and increased use of renewables.

The IRA aims to speed up reductions, especially in the power sector. This sector makes up about one-quarter of national emissions. By withdrawing $13 billion in support, the government may put more pressure on states and private companies to deliver reductions.

At the same time, fossil fuel use is proving stubborn. Natural gas remains the largest source of U.S. electricity, providing about 38% of generation in 2024, while coal contributed around 14%. Without aggressive investment in clean energy, these shares could decline more slowly than expected.

The clean energy sector has become a major driver of U.S. job creation and investment. According to the U.S. Department of Energy, clean energy jobs reached approximately 3.56 million in 2024, with solar employment alone rising about 4% year over year. The IRA boosted the building of new factories for solar panels, batteries, and EV parts in several states.

Canceling $13 billion in funding raises questions for investors who rely on policy certainty. Market analysts say companies might cut back or delay expansion plans if financing is harder to get. However, private capital could still play a strong role, especially since renewable energy is increasingly competitive in cost.

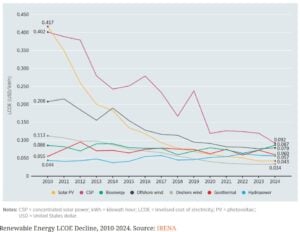

The International Renewable Energy Agency (IRENA) says global solar power costs are down 89% since 2010. Wind costs have also dropped by about 70%. These declines mean renewables often outcompete fossil fuels even without subsidies. Still, the lack of government support may slow adoption in costly areas. This is especially true in rural and low-income regions.

Broader Policy and Political Context

The decision to cancel funds also reflects a larger debate over federal spending and the future of U.S. climate policy. While some policymakers argue that scaling back funds is necessary to reduce fiscal pressures, others see it as a retreat from climate commitments.

Globally, the U.S. is under pressure to maintain leadership in clean energy investment. China and the European Union continue to pour resources into renewables and green manufacturing. If the U.S. reduces support, it could risk falling behind in the race for clean energy innovation and exports.

Environmental groups worry that this step hurts the U.S. credibility before COP30 in Belém, Brazil. At this event, nations will share updates on their climate goals.

Can Momentum Continue?

Despite the intended cuts in clean energy funding, the long-term outlook for U.S. renewables remains positive. Private sector investment is strong. Technology costs are falling. And corporations want more carbon-free electricity. These factors keep the momentum going.

Companies such as Amazon, Google, and Microsoft have pledged to power their operations with 100% renewable energy within the next decade, creating strong demand signals.

Still, the $13 billion reduction highlights the fragility of policy-driven growth. To keep momentum, states may need to expand their programs. Moreover, utilities should speed up grid upgrades. Companies also need to increase investments beyond federal incentives.

While the clean energy transition is not stopping, it may face more turbulence ahead. The U.S. still has the opportunity to lead, but maintaining progress will depend on balancing fiscal priorities with climate commitments.

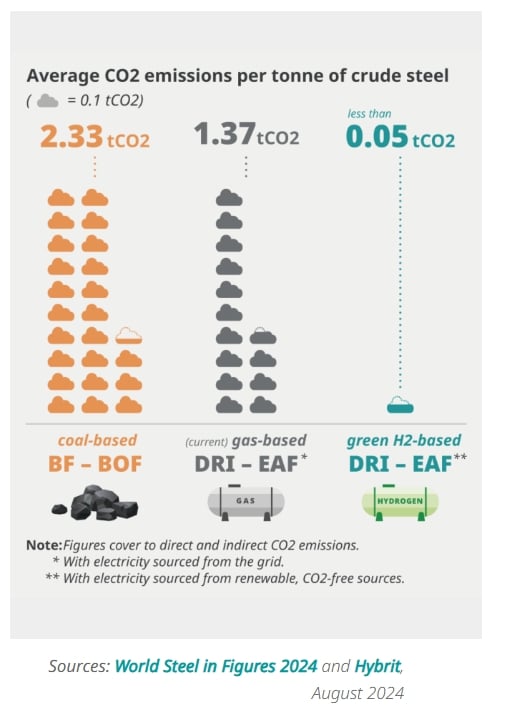

Steel is one of the most carbon-intensive materials on Earth, responsible for around 7% to 9% of global greenhouse gas emissions. The industry produces nearly two billion tonnes of crude steel annually, with average emissions ranging from 1.85 to 2.33 tonnes of CO2 for every tonne of steel. Despite being the backbone of infrastructure, renewable energy, and modern manufacturing, steel remains one of the hardest sectors to decarbonize.