Chevron is adjusting its clean energy strategy at a time when global attention on emissions continues to rise. At the WSJ CEO Council, CEO Mike Wirth shared how the company plans to grow its traditional oil-and-gas business while steadily expanding into biofuels, geothermal power, and a few select emerging technologies. His message was clear: Chevron wants to stay practical, invest in what works now, and keep improving its carbon profile without making unrealistic leaps.

Chevron Bets on Biofuels to Boost Profits and Cut Carbon

Even though Chevron exited a U.S. biomass diesel trade group last year, it maintains that strong financial returns remain possible through smarter feedstocks and better use of existing refinery assets.

Wirth put biofuels at the center of Chevron’s renewable plans. He said these fuels offer a real-world, ready-to-use solution for cutting emissions, especially because they work in today’s engines, pipelines, and fueling systems. Unlike early-stage technologies that still need major breakthroughs, biofuels can scale faster and support industries that cannot switch to electricity overnight.

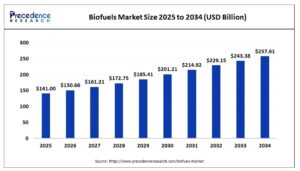

- The global biofuels market size is estimated at USD 141 billion in 2025 and can reach around USD 257.61 billion by 2034, at a CAGR of 6.9%.

Expanding Refineries to Meet Growing Demand

The oil major already runs nine biorefineries around the world, and it recently boosted capacity at its Geismar, Louisiana, site. The company expanded renewable diesel output there from about 90 million gallons to 340 million gallons a year. Wirth explained that this growth helps Chevron serve transportation and maritime sectors, where demand for drop-in fuels remains high.

Additionally, partnerships also play a key role. Chevron works with Bunge and Corteva to produce canola-based feedstocks and teams up with Optimus Power to integrate B100 biodiesel into municipal fleets. Its Renewable Energy Group supplies lower-carbon fuels made from used cooking oil and animal fats, and Chevron has become Singapore’s second-largest marine biofuels supplier.

With ISCC certification in key U.S. ports, Chevron has a strong hold to serve global shipping customers who want cleaner fuels.

Geismar Expansion Stands Out

In this context, more than 40 major biofuel projects worldwide aim to deliver around 260,000 barrels per day by 2030. Chevron’s own Geismar expansion stands out as one of the largest of the 31 new projects tracked. The company is also converting units at traditional refineries, such as El Segundo, to produce about 10,000 barrels per day of renewable fuel.

Research and development efforts continue behind the scenes. At the Ames Technology Centre, Chevron is advancing catalytic technologies for multiple fuels—renewable diesel, biodiesel, SAF, and renewable natural gas—to improve efficiency and cut emissions even further. Its RNG projects are also growing through partnerships with CalBio in California and dairy farms in Michigan.

- READ MORE: Chevron (CVX Stock) Powers Through Q2 With $5.5B Payout, Permian Growth, and Net-Zero Push

Geothermal Steps Alongside Biofuels

Along with biofuels, Wirth highlighted geothermal energy as a promising and reliable clean power source. He described geothermal as a natural fit for Chevron because the company already has decades of subsurface experience from oil-and-gas operations.

Chevron is exploring enhanced geothermal systems that could significantly boost output from traditional geothermal wells. He also said partnerships will play an important role as the company works to scale these technologies and support utility-scale power generation. Because geothermal power does not depend on weather, it can help balance grids as more intermittent energy enters the system.

This interest reflects a broader industry shift. Many energy analysts now see next-generation geothermal as a strong candidate for 24/7 clean electricity, especially for data centers and industrial facilities. Chevron believes it can use its drilling and reservoir expertise to help bring this technology forward.

Connecting the Strategy to Chevron’s Emissions Profile

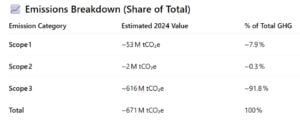

Chevron’s emissions numbers show why the company wants practical solutions.

In 2024, Chevron reported total greenhouse gas (GHG) emissions of approximately 671 million tonnes of CO₂‑equivalent (tCO₂e). This figure includes emissions from direct operations as well as the broader value chain, with Scope 3 emissions — mainly from the use of sold products — accounting for roughly 92% of the total.

- Scope 1 — Direct Operational Emissions: It comes from company-controlled operations such as fuel combustion and flaring, totaled around 53 million tCO₂e in 2024.

- Scope 2 — Indirect Emissions: arising from purchased electricity, steam, and heat, were approximately 2 million tCO₂e in 2024, calculated using both market‑based and location‑based approaches.

- Scope 3 — Value Chain Emissions: reached about 616 million tCO₂e in 2024. The bulk of these emissions comes from Category 11: Use of Sold Products, which includes the CO₂ released when customers consume Chevron’s fuels.

- See details of Chevron’s emissions here: 2024 Corporate Sustainability Highlights — Chevron

Chevron has still made progress in areas it directly controls. Flaring intensity has dropped 22% since 2013, and methane intensity has fallen between 20% and 25%. The company aims to cut upstream emissions intensity to 3 kg CO2e per barrel by 2028, representing a 66% reduction from 2016. Independent assessments show Chevron outperforming about 71% of its oil-and-gas peers on emissions management.

Biofuels help reduce lifecycle emissions in the products Chevron sells, which supports these intensity goals. Geothermal also contributes by lowering operational footprints, especially when combined with carbon capture or renewable power procurement.

Taps Carbon Credits to Offset Emissions

Biofuels and RNG connect directly to the carbon credit market. Both can generate certified greenhouse gas reductions under systems like ISCC. These credits help Chevron and its customers offset certain emissions and meet regulatory and voluntary climate requirements. They also support compliance markets under Article 6, especially for SAF and RNG.

Chevron continues to invest in carbon capture and storage. The Gorgon CCS project in Australia has stored more than 10 million tonnes of CO2 since 2019. While CCS alone cannot solve Chevron’s Scope 3 challenge, it remains an important part of the company’s long-term net-zero plan.

Wirth stressed that Chevron does not expect one single solution to dominate. Instead, the company is building a portfolio that lets it adapt to changing policies, especially as energy rules shift under the current U.S. administration.

Investors following Chevron’s commitment to spend $10 billion on low-carbon investments by 2028 see biofuels and geothermal as the clearest opportunities for near-term commercial value. These technologies lower emissions while supporting Chevron’s core business model.

A Practical Path Through the Energy Transition

The company’s updated strategy shows a company trying to move forward without losing sight of real-world constraints. It plans to keep growing its oil-and-gas business while lowering carbon intensity and expanding into renewable fuels, geothermal, carbon capture, hydrogen, and other emerging technologies. Significantly, Wirth also noted growing interest in nuclear energy and the company’s venture investments in fusion companies.

In simple terms, Chevron is choosing a practical, step-by-step transition. Biofuels offer quick wins. Geothermal adds stable, clean power. Nuclear and fusion represent longer-term bets. Together, they form a balanced path that blends its strengths with rising pressure to cut emissions.