Stellantis and Samsung SDI’s joint venture, StarPlus Energy LLC, has received a U.S. government commitment of up to $7.54 billion to build two electric vehicle (EV) battery plants in Kokomo, Indiana. If finalized, the project will significantly expand North America’s EV battery manufacturing capacity while creating thousands of jobs.

Massive EV Battery Plant to Power North America

Stellantis‘ proposed plants will produce battery cells and modules for North American EVs. Their combined capacity will support around 670,000 vehicles annually. This joint initiative aligns with efforts to bolster domestic production and reduce reliance on foreign suppliers, especially from adversarial nations like China.

In addition to the manufacturing facilities, the project could generate at least 2,800 direct jobs and hundreds more through a nearby supplier park.

Loan Details and Conditions

The U.S. Department of Energy’s (DOE) commitment includes $6.85 billion in principal and $688 million in interest. However, finalization is subject to several conditions, including:

- Developing a plan for meaningful engagement with community and labor leaders to ensure good-paying jobs.

- Meeting technical, legal, environmental, and financial requirements.

The DOE emphasized the importance of continuing support for projects like this, despite potential policy shifts under the incoming administration. President-elect Donald Trump has previously criticized such initiatives, labeling them part of the “green new scam.”

It remains uncertain, however, if the loan will be finalized before Trump’s inauguration on January 20. The DOE refrained from confirming a timeline but stressed the economic and environmental benefits of funding such projects.

A Broader Context in EV Manufacturing

The loan commitment follows a similar $6.6 billion loan granted to Rivian Automotive for a stalled EV factory in Georgia. These investments reflect the Biden administration’s push to strengthen domestic EV supply chains.

The announcement comes amid a leadership shakeup at Stellantis. CEO Carlos Tavares resigned abruptly, with the company announcing an interim executive committee led by Chairman John Elkann until a permanent successor is appointed.

If the loan is finalized, the Kokomo project will mark a significant milestone in North America’s transition to clean energy. It will provide a vital boost to EV infrastructure while fostering job creation and reducing reliance on foreign suppliers.

For Stellantis, it means a highly significant boost for its Net Zero ambitions.

A Roadmap to Net Zero: Stellantis’ Electrification Revolution

Stellantis is taking bold steps to lead the global transition toward a sustainable future through its Dare Forward 2030 plan, a pathway aligned with science-based recommendations to combat climate change. Recognizing transportation’s heavy reliance on fossil fuels—responsible for over 90% of the sector’s energy needs and more than 7 gigatonnes of CO₂ emissions in 2020—the automaker aims to make transformative changes.

The EV giant aims to achieve the following goals and targets:

- 50% CO₂ Reduction by 2030: Benchmarking against 2021 levels, Stellantis is targeting a 50% cut in greenhouse gas emissions.

- Net Zero by 2038: Committed to achieving carbon neutrality, with less than 10% of emissions offset through compensation.

These goals align with the Paris Agreement’s mission to limit global temperature rise to 1.5°C above pre-industrial levels.

A Holistic, ‘Daring for Zero’ Approach

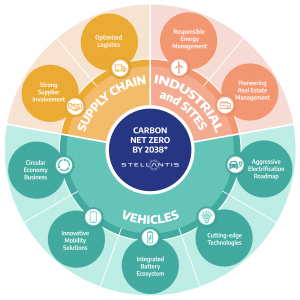

To achieve carbon net zero by 2038, Stellantis has adopted a threefold strategy addressing emissions across its value chain.

For vehicles, it has set an aggressive electrification roadmap, integrating advanced technologies and batteries, offering innovative mobility solutions, and emphasizing circular economy practices to reduce waste.

Stellantis is aggressively advancing its electrification strategy, aiming for a 100% battery electric vehicle (BEV) sales mix in Europe and a 50% BEV sales mix for passenger cars and light-duty trucks in the U.S. by the end of 2030.

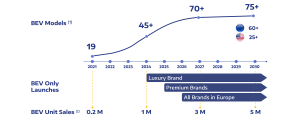

Across its 14 iconic brands, Stellantis plans to introduce 75 BEV models by 2030, targeting sales of 5 million units annually by then. Starting in 2025, all new luxury and premium segment launches will exclusively feature BEVs, with this approach extending to all segments in Europe by 2026.

Stellantis Roll Out of Battery Electric Vehicles (BEVs)

To achieve these ambitious goals, Stellantis is investing €30 billion by 2025 in electrification and software development. This will ensure its EV portfolio aligns with evolving market demands and solidifies its leadership in sustainable mobility.

In the supply chain, the company is optimizing logistics and collaborating with suppliers to ensure sustainability. Lastly, in industrial operations and sites, Stellantis employs responsible energy management and innovative real estate solutions to minimize its carbon footprint.

This holistic strategy tackles Scopes 1, 2, and 3 emissions, including direct emissions from its operations, indirect emissions from purchased energy, and emissions from upstream and downstream activities. in doing so, Stellantis focuses on real reductions, minimizing reliance on carbon offsets.

However, achieving these goals depends on external enablers like a decarbonized energy supply and supportive public policies for BEV infrastructure, including charging stations and purchasing incentives.

Stellantis’ initiatives, part of its Daring for Zero series, highlight its commitment to achieving sustainability milestones. The automaker is driving innovation and collaboration across the industry, reaffirming its crucial role in tackling climate change. And the committed loan from the U.S. government can rev up the automaker’s drive toward net zero.