Lithium prices are entering a new phase. China is strengthening its role in price discovery, sodium-ion batteries are gaining ground, and EnergyX is investing heavily in future supply. Together, these trends are reshaping the global lithium market.

China Tightens Its Grip on the Global Lithium Market

China has opened its lithium carbonate futures market on the Guangzhou Futures Exchange (GFEX) to qualified foreign investors. The move gives overseas traders direct access to one of the world’s most important lithium pricing markets.

Until now, most global lithium contracts have relied on price assessments from private agencies. By opening its futures market, China is taking another step toward making domestic prices an international benchmark.

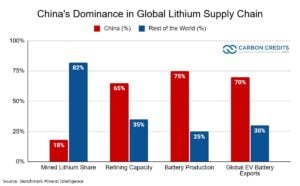

The timing is significant. China already dominates much of the global lithium supply chain. According to the International Energy Agency (IEA), the country refines about 70% of the world’s lithium and produces around 80% of lithium-ion battery cells.

China also leads electric vehicle (EV) production and battery manufacturing. Expanding access to its futures market boosts its control over global lithium price discovery.

For producers, battery makers, and investors, the new market offers another tool to manage price risk. For China, it reinforces its growing role as the center of the global battery economy.

Lithium Prices Remain Far Below Their Peak

The futures market opens during a very different price environment than it did just a few years ago.

Lithium prices surged to record highs in late 2022 as EV demand outpaced supply. Since then, a wave of new production from Australia, China, South America, and Africa has pushed prices sharply lower.

According to CarbonCredits.com, battery-grade lithium carbonate in China traded around 165,250 yuan per metric ton, down from a peak above 590,000 yuan in November 2022.

The sharp decline has squeezed profit margins across the industry. Several producers have delayed expansions or reduced output while waiting for market conditions to improve.

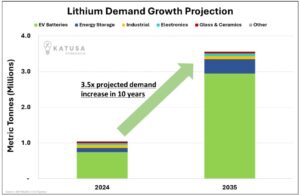

Still, demand continues to grow. The IEA estimates that global demand for lithium reached roughly 240,000 metric tons in 2024—more than triple the level recorded in 2020. Long-term forecasts still point to strong growth as EV adoption and battery storage expand worldwide.

Can Sodium Batteries Slow Lithium Demand?

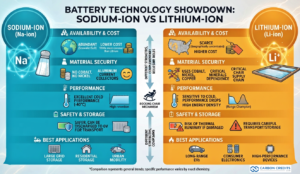

Another factor shaping the market is the rapid development of sodium-ion batteries. China recently approved wider commercial use of sodium-ion batteries, which replace lithium with sodium, an element that is far more abundant and lower in cost.

Several Chinese companies are already scaling production. Sodium batteries are attracting interest because they perform well in cold weather and reduce dependence on critical minerals.

However, most experts do not expect sodium to replace lithium in the near future.

Lithium-ion batteries still provide higher energy density, making them the preferred choice for long-range electric vehicles. Sodium batteries are likely to be used in lower-cost EVs, stationary energy storage, and other applications. In these cases, energy density is not as crucial.

The IEA expects lithium to remain the dominant battery material through at least the next decade, even as alternative chemistries gain market share.

For investors, sodium batteries might slow future demand growth. However, they probably won’t remove the need for a lot of lithium.

Investment Keeps Flowing Into New Lithium Supply

Despite lower lithium prices, companies are still investing in new supply.

U.S.-based EnergyX recently secured a $225 million investment from Italian energy major Eni to advance its Black Giant Lithium Project in Chile’s Atacama region. The funding will support project development and expand EnergyX’s direct lithium extraction (DLE) technology.

The investment shows that major energy companies still expect strong long-term demand for lithium.

The Black Giant project is one of the largest undeveloped lithium brine resources in the world. EnergyX says the project could become an important new source of lithium as global EV production continues to grow.

The project could produce 52,500 metric tons of lithium carbonate equivalent (LCE) per year when fully operational. It will be built in two phases.

The first phase includes Train 1, which will produce 7,500 metric tons of LCE per year and could begin operating in 2028. The second phase will add more processing trains, increasing total annual capacity by another 45,000 metric tons, with operations expected to start in 2030.

The company also believes DLE technology can recover more lithium while using less land and water than traditional evaporation ponds. Although the technology is still being scaled, many producers see it as a way to improve both efficiency and sustainability.

The investment comes at a time when many developers are slowing projects because of weak prices. That makes Eni’s decision a strong vote of confidence in the long-term outlook for lithium.

Demand Still Points Higher

While prices have fallen, the long-term demand outlook remains strong.

The International Energy Agency (IEA) reports that global electric vehicle sales topped 20 million in 2025. This means one in four new cars sold worldwide was electric. Battery storage is also growing rapidly as countries add more solar and wind power.

Both trends require large amounts of lithium.

The IEA projects that demand for critical minerals used in clean energy technologies will continue rising through 2035. Lithium will likely remain one of the fastest-growing minerals because of its central role in rechargeable batteries.

Meanwhile, the U.S. Geological Survey (USGS) estimates global lithium reserves at about 30 million metric tons, with major resources located in Chile, Australia, Argentina, and China. As demand rises, countries are also trying to diversify supply chains by developing new projects in North America and other regions.

These investments aim to reduce reliance on a single region while improving long-term supply security.

What Comes Next for Lithium Prices?

The lithium market is entering a new stage.

China is expanding its influence over global pricing through its futures market. At the same time, sodium-ion batteries are adding more competition in some battery segments, while companies like EnergyX continue investing in future supply.

In the short term, lithium prices may remain under pressure as new production continues to enter the market. However, many analysts expect supply and demand to become more balanced later this decade as EV sales, battery storage, and electricity demand continue to grow.

The market is also becoming more mature. Prices will not just be driven by shortages. They will also respond to new technologies, financial markets, government policies, and shifts in global supply chains.

The latest developments show that the lithium industry is changing, not slowing down. These trends are reshaping how the market operates.

Although lithium prices remain far below their 2022 record highs, demand fundamentals remain strong. The next chapter for the lithium industry will likely be defined not only by higher production but also by better pricing tools, new technologies, and more diversified sources of supply.