According to industry experts, the cobalt market is currently under pressure due to an oversupply and slow demand. The heat is palpable more on cobalt sulfate prices, which are gradually declining, indicating weaker demand. One reason is China’s passenger electric vehicle (PEV) sector, which strongly prefers lithium-iron-phosphate (LFP) batteries that do not rely on cobalt.

However, as revealed by S&P Global Commodity Insights, the Platts-assessed European cobalt price has held steady at approximately $11.00/lb since October 11, but with suppressed trading activity.

Let’s see what the report reveals further about the current and future cobalt market.

China’s Move to LFP Batteries Weakens Cobalt Market

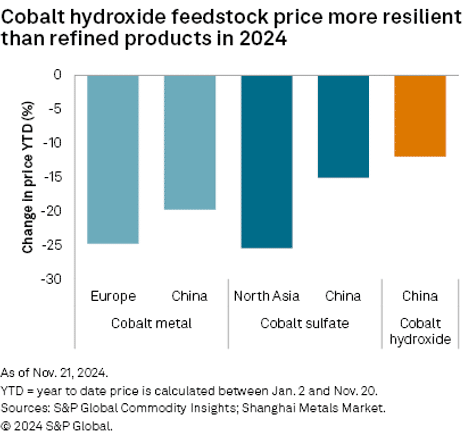

The report revolved around the cobalt market in China. It highlighted that China’s cobalt metal price stabilized after hitting a low in late September. From September 25 to November 21, the price rose by 5.6% and increased another 2.0% month to November 21, despite some fluctuations.

This recovery was driven by stronger feedstock costs, as cobalt hydroxide prices remained more stable compared to refined cobalt products.

However, according to Shanghai Metals Market, margins for cobalt sulfate production using imported cobalt hydroxide turned negative in Q3 2023. This strained margin significantly impacted China’s cobalt sulfate output.

From January to October 2023, combined production dropped by 28.1% compared to the same period last year.

The reason for the decline remains the same- a slowdown in the PEV sector. The other significant reason is automakers shifting to lithium-iron-phosphate (LFP) batteries as they are cost-effective and avoid using critical minerals like cobalt and nickel. This transition has reduced the demand for cobalt-containing batteries in China.

Additionally, S&P Global noted, that in October 2024, cobalt-containing batteries accounted for only 20.6% of vehicle installations in China. This figure is a steep drop from nearly 50% in 2021.

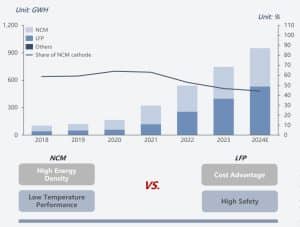

Cobalt remains a vital component in many battery chemistries, offering stability and safety benefits. In 2023, demand for cobalt-containing chemistries grew by 15% year-over-year (y/y) to approximately 500 GWh, accounting for 55% of total battery demand.

While this represents a decline from 63% in 2022, cobalt chemistries are expected to maintain a significant market share in the medium to long term as demand continues to grow. Let’s study how experts explain this evolving landscape…

A Shifting Landscape

Cobalt Institute’s latest report revealed that demand for cobalt was mainly driven by high and mid-nickel chemistries driving this growth in 2023. High-nickel chemistries saw a 32% increase, while mid-nickel grew by 15%. Meanwhile, low-nickel and lithium cobalt oxide (LCO) chemistries experienced declines of 11% and 13% y/y, respectively.

It further highlighted,

Demand for cobalt-containing chemistries rose 15% y/y in 2023, to ~ 500

GWh. This equated to around 55% of battery demand in 2023, down from 63% in 2022.

High-nickel chemistries also increased their market share to 11%, while low-nickel chemistries fell behind nickel-cobalt aluminum oxide (NCA) chemistries for the first time.

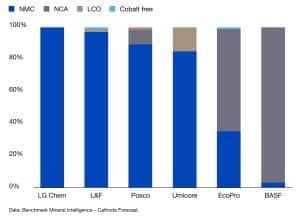

These cobalt-free chemistries now make up 45% of global cathode demand, driven largely by lithium iron phosphate (LFP) batteries. For the first time, LFP overtook nickel cobalt manganese (NCM) cathodes, claiming a 45% market share compared to NCM’s 43%. While manganese-based chemistries also contributed, their impact was minor.

Beyond batteries, cobalt is needed in aviation, energy storage, and electronics and its recyclability makes it sustainable.

Image: LFP vs. NCM: the share of NCM battery cells declines

Source: Cobalt Institute report

Pressures Facing Cobalt

Cobalt, despite its critical role in batteries, faces significant challenges in the supply chain related to cost, composition, and sourcing. Cobalt is costly, but falling prices have improved battery cell cost competitiveness.

The report highlighted that in 2023, NCM and LFP chemistries dominated the global lithium-ion battery market, making up 88% of cathode demand. Automakers in North America and Europe preferred NCM batteries for their higher energy density and longer range and they were mainly used in high-performance EVs.

On the other hand, LFP batteries have gained market share globally, particularly in China, where their lower cost and reduced reliance on critical minerals like cobalt make them a popular choice. This also means that although NCM chemistries have high energy density they are globally less widely adopted.

Image: 2023 Cathode active materials (CAM) product mix from the major ex. China CAM suppliers, %

Additionally, ethical and environmental concerns regarding cobalt sourcing, particularly from the DRC and Indonesia are extensively scrutinized over its sustainability and responsible extraction practices.

Cobalt Forecast 2024: Price and Production

As cobalt demand continues to face challenges with automakers favoring lithium-iron-phosphate (LFP) batteries, cobalt-containing batteries are considerably losing market share. CMOC expects cobalt-containing batteries to eventually make up less than 10% of the total battery mix.

This declining demand is further reflected in price forecasts as rolled out by S&P Global Commodity Insights noted below:

Analysts now estimate the cobalt market surplus will widen significantly in 2024, reaching 53,000 metric tons, which is more than 2X of its earlier predictions.

The growing surplus has also led to a downward revision of cobalt price estimates, with prices now expected to fall to $12.72/lb by 2028.

Batteries now drive three-quarters of global cobalt demand, making the market highly sensitive to changes in cathode chemistries and technologies. As demand for EVs grows, cobalt’s role remains crucial, but the rise of alternatives like LFP will reshape the landscape.

The EV sector’s trajectory in key regions, including the US, China, and the EU, will play a critical role in shaping cobalt’s future. However, with battery technology shifting rapidly and economic policies uncertain, the path ahead remains unpredictable.

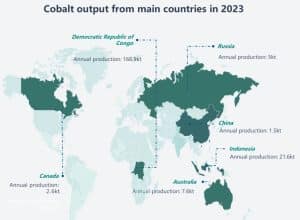

Supply Surge from CMOC, DRC, Australia, and Indonesia

The Democratic Republic of the Congo (DRC), Australia, and Indonesia are the three major countries that control about 73% of the world’s cobalt reserves. Last year, DRC topped the list, accounting for more than 70% of global production.

Source: Cobalt Institute

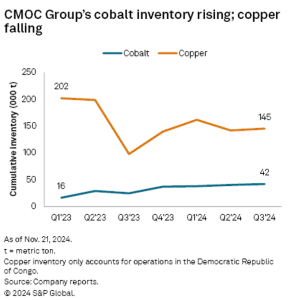

S&P Global forecasts that cobalt production is expected to soar in 2024. It will be significantly driven by Indonesia’s high-pressure acid leaching (HPAL) projects and surge in output from the DRC. Additionally, China’s CMOC, a major producer, has already surpassed its 2023 full-year cobalt production guidance by 21% within the first nine months.

In H1 2024, the company secured the position of the world’s largest cobalt producer with an impressive output of 54,024 tons, marking a staggering 178.22% year-over-year (YoY) growth. This surge not only reflects the company’s pivotal role in the global cobalt supply chain but also signifies a contribution to meet rising demand for battery-grade cobalt.

Notably, CMOC’s production surge is primarily linked to its copper-focused strategy that resulted in increased cobalt inventories.

From this report, we can fairly infer that cobalt can still hold its ground as a key material in high-performance batteries, particularly in Western markets. However, its future will depend on balancing cost, sustainability, and evolving technology trends.

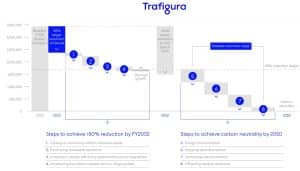

Trafigura Group, a global leader in commodities trading, is making a bold bet on the recovery of the carbon credits market. Despite its recent struggles, the company views emerging regulatory frameworks and international agreements as pivotal for mainstreaming carbon credits in emissions accounting.

With new policies creating clearer pathways for businesses to meet climate targets, Trafigura expects a surge in demand for record growth.

The Carbon Market Makeover: Regulations Reshape Voluntary Credits

The voluntary carbon market (VCM) allows companies and individuals to buy carbon credits to offset emissions voluntarily, rather than as part of regulatory compliance. These credits fund projects that reduce or avoid greenhouse gas emissions, such as renewable energy, reforestation, or community-based initiatives.

Unlike mandatory carbon markets governed by laws, VCM operates through independent standards and registries, providing flexibility for participants. As the VCM evolves, efforts to enhance quality and credibility are shaping its role in global climate action.

Hannah Hauman, Trafigura’s global head of carbon trading, highlighted the impact of increased regulations in Europe, the US, and Asia. These frameworks are designed to help companies achieve net-zero emissions, reinforcing the importance of a robust carbon credits market.

At the recent COP29 summit in Baku, negotiators finalized rules under Articles 6.2 and 6.4 of the Paris Agreement, laying the groundwork for a global carbon trading system.

Article 6.4 introduces a UN-backed mechanism with standardized guidelines for carbon credit quality. It offers a more transparent and structured approach. In contrast, Article 6.2 allows countries to set their own criteria for carbon credit exchanges, which some critics fear could weaken the market.

Danny Cullenward, senior fellow at the Kleinman Center for Energy Policy, warned that Article 6.2 could create an “anything goes” market. This can potentially undermine both Article 6.4 and broader climate efforts.

Industry Challenges and Corporate Retreats

The voluntary carbon market has faced criticism over greenwashing and the issuance of low-quality credits. In 2023, the market’s value dropped by 23% as shown in the graph below. This declining trend started in 2021 when critics began to shake the market. Moreover, key players like HSBC Holdings, Shell Plc, Delta Air Lines, Google, and EasyJet have scaled back their involvement.

Despite these challenges, regulatory advancements have led to optimism. Hauman remarked that countries now have a “regulatory line of sight” to guide them through 2030, providing clarity for companies on expectations, investment strategies, and emissions reductions.

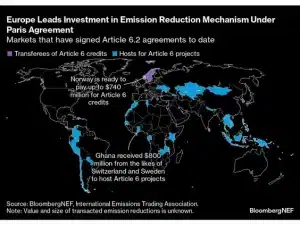

According to BloombergNEF’s data, Europe is leading the UN-backed carbon credit investment while Ghana gets the most funding for Article 6 projects.

Trafigura is capitalizing on this evolving landscape. As the world’s largest trader of carbon-removal credits, the company is expanding its portfolio to meet rising demand.

In November 2024, Trafigura announced a $500 million investment in a carbon credits project to restore Africa’s Miombo woodlands. The project aligns with Article 6.4 guidelines, emphasizing quality and environmental impact.

In the same month, the giant commodity trader, alongside Temasek-owned GenZero, has pledged $100 million to Colombia’s largest nature-based carbon removal project. The project seeks to restore degraded land in the South American nation while generating carbon credits.

Hauman noted that carbon credits are evolving from experimental tools to investment-grade assets, thanks to regulatory shifts. This transformation is expected to enable companies to incorporate credits into their long-term sustainability strategies confidently.

The company itself is pursuing ambitious carbon reduction goals, aiming to:

cut Scope 1 and 2 emissions by 50% by 2032, and

achieve net zero by 2050.

In addition to reducing its direct emissions, Trafigura is focused on lowering Scope 3 emissions intensity. This includes the impact of its traded products. To accelerate its energy transition, the company does these measures:

Invest heavily in renewable energy, including solar and wind projects.

Develop low-carbon fuels like green hydrogen and ammonia.

Launched a $2 billion fund in 2023 to support energy transition projects.

The fund is also for advancing its emissions trading activities, helping clients offset their carbon footprints with high-quality carbon credits.

A New Era of Investment-Grade Carbon Assets

While the carbon market faces hurdles such as inconsistent legal definitions and price volatility, companies like Trafigura, Cummins, Bosch, Daimler, Toyota, and Volvo see potential for growth. Regulators across regions recognize the role of carbon credits, especially removal-based units, in helping businesses achieve net-zero emissions by mid-century.

COP29 also marked a turning point for reforestation and afforestation projects under the UN’s Clean Development Mechanism (CDM). These projects, previously stalled, have been transferred to the revamped Article 6.4 framework, benefiting countries like India and Colombia, which host 27 eligible projects.

The carbon market is moving away from being policy-driven to becoming a dynamic investment arena. Trafigura’s strategic partnerships and investments position it to lead this transition. The company aims to drive both market growth and meaningful climate action, by addressing regulatory requirements and maintaining high-quality standards.

As the industry adapts to new rules, Trafigura’s efforts show the shift toward a more structured and credible carbon credits market. It underscores the company’s readiness to thrive in the evolving carbon market landscape.

Westinghouse Electric Company and CORE POWER have collaborated together to design and develop a floating nuclear power plant (FNPP) using the former’s blueprint eVinci™ microreactor and its heat pipe technology Both the companies have formalized a cooperative agreement to advance the design of the FNPP. This innovation is ideal for maritime and coastal applications where traditional energy sources may have less potential.

Jon Ball, President of eVinci Technologies at Westinghouse commented,

“With this groundbreaking agreement, we will demonstrate the viability of the eVinci technology for innovative use cases where power is needed in remote locations or in areas with land limitations. We look forward to our partnership with CORE POWER, bringing the unique advantages of eVinci microreactors to maritime and coastal applications, potentially even paving the way for future disaster relief efforts.”

Mikal Bøe, CEO of CORE POWER noted,

“There’s no net-zero without nuclear. A long series of identical turnkey power plants using multiple installations of the Westinghouse eVinci microreactor delivered by sea, creates a real opportunity to scale nuclear as the perfect solution to meet the rapidly growing demand for clean, flexible and reliable electricity delivered on time and on budget. Our unique partnership with Westinghouse is a game changer for how customers buy nuclear energy.”

Unlocking the Power of Floating Nuclear Power Plants

Floating nuclear power plants (FNPPs) are an innovative solution for delivering energy to remote coastal areas, islands, and offshore locations. Their compact size and mobility make them ideal for providing electricity at the need of an hour. They can be moved or towed to remote regions, where they dock with coastal facilities to supply power and heat to the local grid.

Floating nuclear power plants are gaining attention as a versatile clean energy option. They use small modular reactors (SMRs) to generate electricity and heat. These reactors, which are compact and efficient, can serve various applications:

Electricity for remote regions like islands and coastal communities.

Decarbonizing industries such as offshore oil, gas, and mining.

Supporting hydrogen production, desalination, and district heating.

The International Symposium on the Deployment of Floating Nuclear Power Plants (FNPPs) held in Vienna last November explored the potential of FNPPs. Delegates weighed if FNPPs could be a reliable energy solution for remote locations. They highlighted that these innovative power stations could replace fossil-fueled generators, advancing global decarbonization efforts.

IAEA Director General Rafael Mariano Grossi highlighted the growing interest in FNPPs during the symposium. He noted that many countries are actively considering these plants but emphasized the importance of addressing safeguards, andlegal, and regulatory frameworks before large-scale deployment.

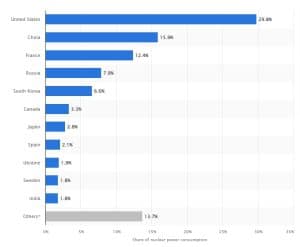

The same IAEA report revealed that several countries, including Canada, China, Denmark, South Korea, Russia, and the USA, are developing marine SMR designs. Russia leads with the Akademik Lomonosov, the world’s first operational FNPP. Since 2020, it has supplied electricity and district heating in Russia’s far east.

However, floating nuclear power plants do not compete with land-based SMRs. They rather expand the potential of nuclear technology to achieve net zero goals.

Distribution of nuclear power consumption worldwide in 2023, by leading countrySource: Statista

Moving on we will explore the companies and the kind of nuclear technologies they are deploying.

Westinghouse is pioneering the next generation of nuclear technology with its eVinci™ Microreactor. It is typically designed for decentralized and remote applications. The micro-modular reactor is a product of 60 years of nuclear expertise and technical knowledge. They successfully created this unique microreactor to deliver a resilient, cost-effective energy solution.

The key attributes of this reactor are:

Heat Pipe Technology

The eVinci™ Microreactor has an inbuilt heat pipe technology that enables passive heat transfer without the need for complex coolant systems. Heat pipes efficiently transfer heat at high temperatures without relying on high-pressure systems or moving parts. Recently, the company successfully manufactured the first-ever 12-foot nuclear-grade heat pipe. See the pic below:

Source: Westinghouse

The inbuilt design ensures reliability, reduces maintenance needs, and eliminates risks associated with coolant loss or high system pressures.

Compact Design for Rapid Deployment

Unlike traditional nuclear plants that require extensive construction, the eVinci reactor is fully factory-built, assembled, and shipped in a container for easy deployment. It operates just like a battery with minimal moving parts.

eVinci can produce 5MWe with a 15MWth core design. The reactor core can run for eight or more full-power years 24/7 before refueling.

Source: Westinghouse

Beyond Maritime Applications

The reactor’s compact design and minimal maintenance requirements make it ideal for maritime and coastal use. Significantly, it offers efficient, reliable power for ports, coastal communities, and offshore operations where traditional energy sources fall short.

However, its versatility extends to the following areas:

Reliable power to remote communities.

Mining operations and industrial facilities.

District heating and hydrogen production for cleaner energy solutions.

Research reactors, critical infrastructure, and military installations.

Data centers seeking uninterrupted power.

The eVinci microreactor integrates easily with wind, solar, and hydro. It stabilizes grids by quickly adjusting to demand, ensuring reliable power in any condition.

Net Zero Goals and Safety Standards

The eVinci microreactor delivers carbon-free energy without requiring water cooling, making it an eco-friendly power solution. This partnership shows how the companies are helping countries meet their net-zero targets.

Each reactor prevents up to 55,000 tons of CO2 emissions annually, significantly reducing carbon footprints.

After its operational life, spent fuel is either returned to the manufacturer or stored in deep geological repositories (DGR) for long-term safety. Additionally, Westinghouse ensures high safety standards even in unexpected scenarios. This is because of the advanced features that minimize failure risks and make it a reliable and environmentally responsible energy source.

Check out the more details of the eVinci Microreactor

According to the press release, CORE POWER is advancing a Maritime Civil Nuclear Program across the OECD (Organisation for Economic Co-operation and Development), providing scalable nuclear solutions for maritime and heavy industries. The company has offices in London, Washington, D.C., and Tokyo.

At present, they are aiming to enhance energy efficiency and local energy security by delivering reliable floating nuclear energy systems built in shipyards, on time and within budget.

Some notable achievements of CORE POWER in this field are:

Its next-generation reactors or advanced nuclear technologies, like molten salt reactors (MSRs), offer improved safety and efficiency compared to earlier models. These floating plants deliver dependable and sustainable electricity while addressing modern energy needs.

CORE POWER’s FNPPSource: CORE POWER

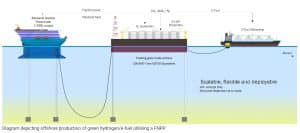

Fueling Offshore Green Industry

Floating nuclear power plants (FNPPs) are more than electricity generators; they enable sustainable industrial processes. One key application is green hydrogen production, which uses seawater and provides an eco-friendly alternative to fossil fuels.

These FNPPs offer efficient cooling and unlimited water access, making them ideal for scalable hydrogen production. This green hydrogen can power zero-emission transport and support green steel manufacturing, transforming industries with clean energy and industrial heat.Source: CORE POWER

Sustainable Water Solutions

Floating nuclear desalination plants provide a continuous supply of fresh water without relying on fossil fuels. Operating 24/7, these plants are mobile, allowing relocation along coastlines to address water scarcity in different regions.

Significantly desalination plants are safe from tsunamis and earthquakes as they are harbored offshore. This makes them a reliable and sustainable solution to growing water challenges.

Source: CORE POWER

This groundbreaking partnership of Westinghouse and CORE POWER can potentially revolutionize the energy landscape energy with their floating nuclear power plants (FNPPs) and innovative eVinci microreactor. All in all, these innovations mitigate carbon emissions and support countries in their net zero goals.

The hydrogen sector is seeing transformative developments from two key players. Nikola Corporation is advancing hydrogen fuel cell technology for zero-emission transportation, setting a new standard in sustainable mobility. Meanwhile, PureWave is revolutionizing hydrogen production with innovative, cost-efficient solutions to meet the growing demand for clean energy.

Nikola and FEF: Setting A New Standard for Hydrogen Transportation

The world’s first hydrogen fuel station for commercial trucks has opened near the Port of Oakland. Built by FirstElement Fuel (FEF), a California-based company, this station boasts a fueling capacity over 10x greater than any existing hydrogen station.

In December 2023, Nikola Corporation formalized its partnership with FEF, naming the latter an authorized Nikola Fueling Solutions Partner. The collaboration ensures Nikola customers have access to FEF’s cutting-edge hydrogen refueling services, including the new multi-use heavy-duty truck station strategically located near Oakland’s port.

FEF hydrogen station at Oakland Port

The station is equipped with the world’s first H70 fast-fill lane for heavy-duty trucks. It enables rapid hydrogen refueling in just 10 minutes. This technology allows the station to serve up to 200 trucks daily, supporting the growing fleet of hydrogen-powered vehicles.

The project also received funding from the California Energy Commission under the NorCal Zero Project.

FEF’s founder and executive chairman, Joel Ewanick, highlighted the significance of the partnership, stating:

“This collaboration is a testament to our commitment to transform the transportation industry and we are proud to play a role in powering Nikola’s innovative hydrogen fuel cell electric trucks.”

Nikola’s Role in the Hydrogen Transition

Nikola’s hydrogen fuel cell electric trucks represent a pivotal step in decarbonizing the trucking industry. With access to FEF’s advanced refueling infrastructure, these trucks can efficiently refuel and support long-haul operations, making hydrogen a practical alternative to diesel.

Hydrogen technology has gained interest from other industry leaders, including Hyundai, Daimler, and Volvo. But Nikola’s agreement with FEF positions it as a front-runner in the U.S. hydrogen economy.

The Oakland station is part of a broader push to establish a robust hydrogen infrastructure in the U.S. Tyson Eckerle, clean transportation advisor for California’s Governor, noted that federal funding of $8 billion aims to jump-start the hydrogen economy, with plans for up to 60 more truck stations statewide.

However, industry critics said that the shift remains slow, as most hydrogen today is still produced from natural gas without carbon capture as shown below. This underscores the challenges in transitioning to sustainable hydrogen sources quickly.

This is where an innovative hydrogen solution of an emerging player comes in – PureWave Hydrogen.

PureWave and the University of Wyoming: Redefining Hydrogen Production

PureWave Hydrogen Corporation has signed a letter of commitment with the University of Wyoming’s Hydrogen Energy Research Center (H2ERC) to advance groundbreaking geologic hydrogen containment technology. This collaboration marks a pivotal step in developing innovative solutions for safely and efficiently storing naturally occurring hydrogen.

PureWave Hydrogen is a pioneering company in the green energy transition, dedicated to discovering and developing naturally occurring hydrogen resources. The company focuses on unlocking the potential of ‘white’ hydrogen to revolutionize the global hydrogen economy.

White hydrogen is a clean form of hydrogen that eliminates energy-intensive processes to produce.

The company’s partnership with the University of Wyoming provides PureWave access to the institution’s patent-pending synthetic clay suspension technology. This innovative solution, developed by Dr. Saman Aryana’s research group, aims to enhance hydrogen containment by reducing hydrogen diffusivity.

The agreement is part of a proposal submitted to the U.S. Department of Energy’s Advanced Research Projects Agency – Energy (ARPA-E) and is subject to the project’s approval.

This development underscores PureWave’s commitment to leveraging advanced research to lead the natural hydrogen sector. As global demand for sustainable energy grows, the company is focused on solutions that make hydrogen a secure and viable energy option.

The collaboration with the University of Wyoming’s School of Energy Resources and Chemical and Biomedical Engineering Department highlights a shared mission to advance hydrogen technology and contribute to the green energy transition.

Hydrogen, especially naturally occurring ‘white’ hydrogen, is gaining attention as a clean energy source. With Wyoming’s abundant natural resources and established energy infrastructure, the state could become a hub for hydrogen production.

The Hydrogen Energy Research Center aims to support this transition by exploring innovative hydrogen production methods, including geologic storage, and collaborating with industry leaders like PureWave.

Breakthrough in Hydrogen Containment Technology

At the heart of this collaboration is the synthetic smectite clay, Laponite, a material engineered to significantly improve hydrogen containment. This technology creates a suspension designed to reduce H₂ diffusivity, enabling better storage in geological formations.

Key features of the technology include:

Synthetic Smectite Clay (Laponite): Reduces the rate at which hydrogen molecules escape, ensuring higher containment efficiency.

Enhanced Containment: Provides a stable environment for hydrogen production and storage by forming a soft solid upon injection.

Flexible Application: Suitable for use in vertical and horizontal wells, making it adaptable to various geological conditions.

Environmental Safety: Minimizes environmental impact while ensuring the secure containment of hydrogen.

Cat Campbell, Head of Geoscience at PureWave, highlighted the importance of this agreement, noting that:

“This agreement represents a significant leap forward in PureWave’s commitment to developing safe and sustainable methods for capturing and storing naturally occurring hydrogen. By partnering with H2ERC, we are now equipped with groundbreaking technology that enhances containment and minimizes the environmental impact of our operations.”

Ultimately, hydrogen’s potential as a clean energy solution is coming to life through advancements by Nikola and PureWave. Nikola’s fuel cell innovations promise zero-emission transportation, while PureWave’s efficient production methods drive accessible, scalable hydrogen energy. Together, these efforts highlight hydrogen’s growing role in global decarbonization and the transition to a sustainable future.

KlimaDAO (Decentralized Autonomous Organization), a global leader in blockchain-powered climate finance, is transforming the carbon credit market. Established in 2021, KlimaDAO leverages blockchain technology to enhance transparency, liquidity, and efficiency in carbon credits trading. With over 25 million tons of Verified Carbon Standard (VCS) credits migrated onto its blockchain platform and 600,000 tonnes retired on-chain, KlimaDAO is accelerating climate action worldwide.

Now, its Japan-based subsidiary, KlimaDAO JAPAN Co., Ltd., is pioneering an innovative project named KlimaDAO JAPAN MARKET. This platform aims to tokenize Japan’s J-Credits on the blockchain, enhancing accessibility and trust in the carbon credit ecosystem.

Blockchain Meets Carbon Credits: A Game-Changing Demonstration

According to the latest news, KlimaDAO JAPAN has initiated a beta test for its blockchain-based carbon credit marketplace. The KlimaDAO JAPAN MARKET is set to revolutionize the market by addressing key challenges such as low liquidity, opaque transactions, and complex processes.

KlimaDAO will use a globally recognized Carbonmark API smart contract to demonstrate how blockchain technology can enhance the transparency, reliability, and efficiency of carbon credit markets.

Moving on, the beta phase will focus on Japan’s J-Credit system which is a government-certified program for promoting carbon reduction initiatives.

KlimaDAO JAPAN Co., Ltd. Representative noted,

“We are very pleased to be collaborating with Mizuho Financial Group, Optage, and other advanced partner companies to launch the world’s first demonstration experiment of J-Credit blockchain transactions. The current carbon credit market faces a variety of challenges, including transaction opacity and complex procedures. KlimaDAO JAPAN MARKET aims to solve these issues and realize a more transparent and efficient market by utilizing blockchain technology.

Through this platform, we hope to create an environment where more people, from companies to individuals, can participate in carbon credit transactions and contribute to the decarbonization of Japan. Furthermore, by collaborating with the global KlimaDAO network, we will promote the globalization of Japan’s carbon credit market.

Toward the realization of a sustainable society, we will open up new possibilities through the power of technology. That is the mission of KlimaDAO JAPAN. We look forward to your participation and support.”

Now let’s understand how the demonstration will work:

First, the trial involves tokenizing J-Credits, making them tradeable as ERC-20 standard tokens called “J-Credit Tokens” on the Polygon blockchain. Each token will represent one metric ton of CO2 (1 t-CO2).

Trading will initially be limited to participating companies and local governments in a controlled environment. Eventually, they plan to open the platform to the public by spring 2025.

KlimaDAO JAPAN is partnering with the following organizations to ensure the project is successful:

Mizuho Financial Group offers practical project support.

PBADAO oversees project management and development.

These collaborations bring expertise and credibility to the platform and foster trust among participants. Some notable companies that have agreed to participate include Blue Lab, Electric Power Development, ENERES, SoftBank, Uhuru, JPYC, Decarbonization Support, etc. Get the complete list here: press release.

Source: KlimaDAO JAPAN Co., Ltd.

Steps to Follow for the Demonstration

For Sellers:

Convert J-Credits into tokens called J-Kure Tokens using smart contracts.

List these tokens for sale on the KlimaDAO JAPAN MARKET.

For Buyers:

Buy J-Kure Tokens and carry out these actions:

Store the tokens in a digital wallet.

Use a smart contract to make the tokens invalid.

Receive and save the invalidation certificate in the wallet.

Transfer the tokens to the J-Credit Management Account.

Resell the tokens in a secondary market.

Notably, the demonstration period will last until the end of February 2025.

source: Medium.com

Innovative Use of Blockchain for Carbon Credits

The integration of blockchain technology with J-Credits introduces several advanced features. These carbon credits bring new possibilities through programmability and enable innovative services that may have been unattainable previously in traditional markets. Some attributes are:

Tokenization of Credits: Converts traditional carbon credits into secure, tradeable digital tokens.

Blockchain-Based MRV System: Links with a measurement, reporting, and verification (MRV) system for greater accountability.

Programmable Functionality: Automates transactions, supports credit splitting, and integrates with stablecoins and financial products.

These features promise to revitalize the carbon credit market while promoting and supporting more adaptable climate change solutions.

KlimaDAO aims to solve major problems in the carbon credit market, such as low trading options, ambiguous transactions, and complicated processes. These issues limit participation, reduce trust, and make the system difficult to navigate.

Using blockchain technology, KlimaDAO is simplifying the entire process and offering viable solutions. From this perspective, it will ensure real-time verification, cut out middlemen, and make credit issuance and trading faster and more reliable.

Looking ahead, the broader goal is to democratize carbon credit trading by creating a platform where both individuals and companies can easily buy and sell credits. This approach not only fosters broader involvement but also enhances Japan’s contribution to the global decarbonization goal.

Additionally, KlimaDAO will connect its global marketplace, Carbonmark, to this service. This will allow trading of international credits certified by EcoRegistry and the International Carbon Registry (ICR)

All in all, KlimaDAO’s innovative approach is paving the way for sustainable carbon markets in Japan as well as internationally. And by combining blockchain with carbon credits the market looks more transparent and efficient.

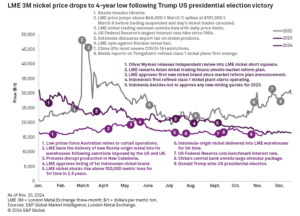

Demand for battery-grade nickel is projected to grow significantly by the end of the decade due to rising electric vehicle (EV) adoption. However, the nickel market faced more volatility and uncertainty in November 2024, according to S&P Commodity Insights data. It is largely due to macroeconomic and political developments following Donald Trump’s U.S. presidential election victory.

Trump’s Victory Fuels Nickel Market Volatility

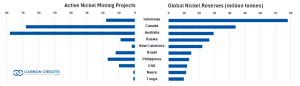

Nickel is vital for producing stainless steel and alloys used in equipment, transport, buildings, and power generation. Major nickel producers include Indonesia, the Philippines, Russia, and Australia, with Indonesia having the highest nickel reserves while Australia has the most active mining projects.

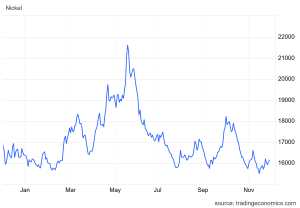

Nickel futures are traded on the London Metal Exchange (LME), reflecting its global industrial importance. The LME three-month nickel price dropped to a four-year low of $15,540 per metric ton on November 15.

Concerns over Trump’s potential economic policies, particularly their implications for China, the industrial metals’ top consumer, have fueled investor caution. A stronger U.S. dollar and increased LME nickel inventories further worsen the downward pressure on prices as shown above. This highlights a risk-off sentiment across metals markets.

Nickel prices initially saw an uptick after Trump’s election win, rising from $16,007 per metric ton on November 4 to $16,587 per metric ton on November 7.

This temporary boost mirrored gains in U.S. equity markets. However, optimism quickly faded as the trade-weighted U.S. dollar index climbed to a one-year high, fueled by market expectations that Trump’s policies—such as higher tariffs on Chinese imports—could revive U.S. inflation.

The prospect of prolonged high interest rates from the Federal Reserve further strengthened the dollar. This makes nickel and other commodities more expensive for non-dollar investors.

Investor sentiment in the nickel market took another hit following China’s unveiling of a 10 trillion yuan fiscal stimulus package on November 8. The measures failed to meet market expectations for more aggressive economic support. This disappointment, coupled with rising nickel inventories and a nearly 4x increase in net short positions on LME nickel, accelerated the price decline.

By mid-November, the LME three-month nickel price had plunged to levels not seen since November 2020, underscoring the market’s vulnerability to both economic and geopolitical developments.

In late November, nickel rebounded to $16,040 per tonne amid Indonesia’s tighter mining policies. Approved quotas could drop 27% by 2026, while license fees for low-grade ore may be reduced.

According to the Indonesian mining minister, nickel ore imports surged 50-fold, as officials prioritized domestic reserves and warned of dwindling stocks to stabilize prices.

IRA Under Threat: What Trump’s Plans Mean for Nickel and EVs

The implications of Trump’s election for the U.S. Inflation Reduction Act (IRA) add another layer of uncertainty to the global nickel market.

Signed into law by President Joe Biden in 2022, the IRA has been a key driver of clean energy initiatives. This includes a $7,500 consumer tax credit for electric vehicles.

However, Trump’s transition team is reportedly considering repealing this tax credit as part of broader tax reform efforts. Such a move could slow the adoption of EVs in the U.S. This could undermine a major driver of global primary nickel demand over the next five years.

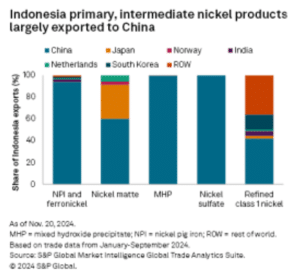

Additionally, Trump’s administration may tighten the IRA’s foreign entity of concern (FEOC) guidelines, which currently disqualify companies with significant Chinese ownership from benefiting from the EV tax credit. For instance, Indonesia—a leading producer of nickel—has been working to reduce China’s influence to qualify for IRA incentives.

In a recent deal between PT Vale Indonesia and China’s GEM Co., GEM’s stake in a $1.42 billion nickel plant was capped at 25% to comply with the guidelines. However, stricter FEOC rules could make it even harder for such projects to qualify for U.S. tax incentives. This can potentially limit Indonesia’s ability to expand its nickel exports to the U.S.

China remains a dominant player in Indonesia’s nickel sector. Between January and September 2024, Indonesia exported 129,860 metric tons of nickel sulfate exclusively to China.

If Indonesia faces challenges in accessing U.S. markets due to stricter IRA policies, its reliance on China is likely to deepen. This dynamic could reshape global nickel supply chains, with potential long-term implications for battery manufacturing and EV production.

Short-Term Pain, Long-Term Gain? Nickel’s Future Outlook

Beyond U.S. policy developments, other global factors are contributing to nickel market uncertainty. Escalations in the Russia-Ukraine war have dampened investor confidence, while concerns about slowing economic growth in China continue to weigh on demand projections.

The interplay of these factors has led to reduced risk appetite among investors, as evidenced by the sharp rise in short positions on LME nickel.

Despite these challenges, S&P Global’s fundamental outlook for primary nickel supply and demand remains broadly unchanged from previous forecasts. However, the near-term trading environment is expected to remain difficult.

Amid all these challenging market conditions, an emerging player is targeting U.S. nickel independence. Alaska Energy Metals Corporation (AEMC) is leading efforts to support the U.S. energy transition through its flagship Nikolai project in Alaska. The site holds a significant resource of nickel, copper, cobalt, and platinum group metals essential for renewable energy and electric vehicles.

The Canadian nickel junior’s dual focus on sustainability and critical mineral supply underscores its commitment to reducing U.S. reliance on imports.

With the nickel prices already at a multi-year low, the market’s recovery will depend on clearer policy signals and stronger demand drivers, particularly from the EV and clean energy sectors.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: AEMC.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Cryptocurrency has revolutionized the financial world, offering decentralized, secure, and borderless transactions. However, its rise has come with a significant downside—high energy consumption. The world’s most popular cryptocurrency, Bitcoin relies on energy-intensive mining processes to secure its network, emitting lots of carbon dioxide. Meanwhile, other blockchain applications also contribute to this growing energy demand.

As the crypto industry expands, so do concerns about its environmental impact. This article explores how cryptocurrency and blockchain technology affect global energy consumption and carbon emissions. It explores how Green AI enables sustainable blockchain solutions. It also explains how blockchain can help carbon markets address some of its most pressing issues.

But first, let’s unveil how energy-intensive cryptocurrency mining is and whether Bitcoin can be truly green.

Can Bitcoin Be Truly Green? The Carbon Footprint of Cryptocurrency Mining

High energy consumption in cryptocurrency mining directly translates to significant carbon emissions, especially when powered by fossil fuels.

Bitcoin mining is notorious for its immense energy consumption. Here are the facts about crypto mining’s environmental impact:

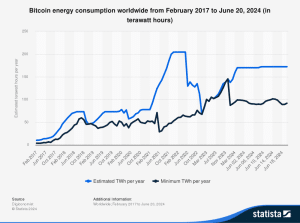

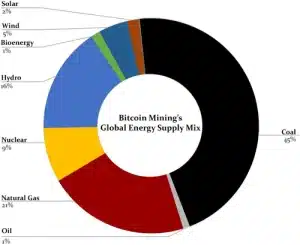

According to recent data, the Bitcoin network consumes around 127 terawatt-hours (TWh) of electricity annually—more than entire countries like Argentina and the Netherlands. This energy usage stems from the Proof-of-Work (PoW) mechanism, where miners compete to solve complex mathematical puzzles, requiring powerful hardware and vast amounts of electricity.

To put this into perspective, Bitcoin mining accounts for 0.55% of global electricity consumption, equivalent to the energy use of some large industrial sectors. As a result, the environmental cost of mining continues to spark debate, urging the industry to explore more sustainable practices.

Higher energy use translates into more carbon emissions…

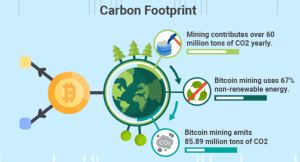

On average, a single Bitcoin transaction is responsible for emitting 300 to 400 kilograms of CO₂, equivalent to the carbon footprint of over 800,000 Visa transactions or 50,000 hours of YouTube streaming.

Globally, Bitcoin mining emits an estimated 69 million metric tons of CO₂ annually, comparable to the emissions of countries like Greece.

Image from GREENMATCH

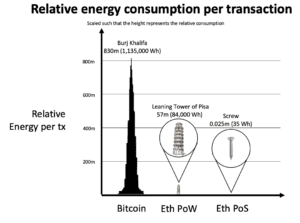

Moreover, cryptocurrency transactions, particularly those on the Bitcoin network, consume far more energy than traditional payment systems. As mentioned above, Bitcoin transactions use a lot more power than Visa processes.

A single Bitcoin transaction = 100,000 Visa transactions.

PayPal, another widely used platform, also operates with significantly lower energy consumption, processing thousands of transactions with minimal electricity use. This stark difference underscores the inefficiency of current cryptosystems compared to traditional financial networks.

The substantial environmental cost underscores the urgent need for cleaner energy sources and innovative solutions to reduce the crypto industry’s carbon footprint.

The Growing Role of Renewable Energy in Bitcoin Mining

Recent data suggests that over 50% of Bitcoin’s mining network now uses renewable energy sources such as hydroelectric, wind, and solar power. For instance, regions like Iceland and Quebec, known for abundant renewable energy, have become hotspots for mining operations.

This transition is driven by economic and environmental incentives. Renewable energy is often cheaper than fossil fuels, reducing operational costs for miners. Furthermore, as governments introduce stricter regulations on carbon emissions, miners are motivated to adopt greener practices to avoid penalties and maintain their social license to operate.

Proof-of-Stake and Other Energy-Efficient Consensus Mechanisms

Bitcoin operates on a Proof-of-Work consensus mechanism, which is energy-intensive by design. Miners compete to solve complex mathematical problems, consuming significant electricity in the process.

In contrast, Proof-of-Stake (PoS) systems, like Ethereum’s, the second-largest blockchain, recent transition, eliminate the need for energy-hungry computations.

Instead of miners, validators are chosen based on the number of tokens they hold and are willing to “stake.” This drastically reduces energy consumption—Ethereum’s shift to PoS has cut its energy use by 99.95%, setting a benchmark for other cryptocurrencies.

Before its transition to Proof-of-Stake in 2022, Ethereum consumed around 78 TWh of electricity annually, comparable to Chile’s total energy use. Even smaller blockchains, such as Litecoin and Dogecoin, utilize PoW, albeit with lower energy requirements.

Source: Ethereum

On the other hand, many altcoins, including Cardano and Solana, have adopted PoS or other less energy-intensive models. These networks drastically reduce energy consumption, making them more sustainable.

However, the cumulative impact of various blockchains still adds to the global energy demand, highlighting the need for widespread adoption of greener technologies.

Apart from changing consensus mechanisms, innovative solutions like KlimaDAO offer a new way to address crypto’s carbon footprint.

KlimaDAO allows users, including Bitcoin miners, to purchase tokenized carbon credits, effectively offsetting their emissions. These credits represent verified reductions in greenhouse gases and are retired after purchase to ensure accountability.

One carbon credit equals one metric ton of CO₂ reduced or removed from the atmosphere.

Such initiatives align with broader climate goals, enabling the crypto industry to contribute positively to carbon neutrality. Another emerging trend that could help the industry tackle its environmental impact is Green AI (Artificial Intelligence).

Green AI: Powering Sustainable Blockchain Solutions

The concept of “Green AI” focuses on leveraging artificial intelligence to enhance sustainability and reduce environmental impact, aligning technology with climate action goals. AI can be used to optimize energy usage across various industries, minimizing emissions and maximizing efficiency.

For instance, AI-powered solutions can streamline energy grids, predict resource consumption, and identify areas for improved sustainability. It also supports the development of AI models and algorithms that optimize energy consumption in data centers, making them more energy-efficient.

Green AI includes using AI tools to track carbon emissions, forecast energy usage, and help industries transition toward renewable energy. For example, AI can optimize electricity demand response, helping utilities manage energy more efficiently while reducing carbon footprints.

By integrating AI with sustainability strategies, organizations can achieve measurable reductions in energy consumption, significantly lowering the carbon footprint of industries like manufacturing, transportation, and data management.

AI is also revolutionizing how blockchain networks manage energy. By analyzing real-time data, AI algorithms can predict network congestion, optimize transaction processing, and ensure efficient use of computing resources.

This dynamic allocation of energy minimizes waste and prevents overuse during low-demand periods. For example, predictive models powered by AI can anticipate peak activity times, enabling miners to adjust operations and reduce unnecessary energy expenditure.

AI-Driven Tools to Track and Reduce Crypto Carbon Emissions

AI also plays a critical role in monitoring and mitigating the carbon emissions of blockchain activities. Platforms equipped with AI can measure the carbon output of each transaction, offering insights into the environmental impact of specific operations. These tools provide actionable recommendations for reducing emissions, such as shifting workloads to energy-efficient times or integrating renewable energy sources.

For instance, projects like CryptoCarbonRank leverage AI to provide transparency on carbon emissions across various blockchain networks, empowering users and developers to make greener choices.

Bridging Blockchain and AI for Improved Transparency

Combining blockchain’s transparency with AI’s analytical capabilities has transformed the carbon credit market. Blockchain ensures the integrity of carbon credits by recording transactions in a tamper-proof ledger, while AI automates the verification process. This synergy prevents issues like double counting and fraud, which have historically plagued carbon markets.

AI-driven platforms also facilitate the issuance and trading of tokenized carbon credits. These innovations streamline the offset process, making it accessible to a broader audience while ensuring credibility and trust in global carbon offset initiatives.

Now, let’s consider specifically Bitcoin mining and how current efforts and innovations are helping the network become more sustainable.

The Evolution of Bitcoin Mining: Toward Sustainability

Bitcoin mining has historically depended on fossil fuels, contributing to significant carbon emissions. However, the industry is evolving as miners increasingly adopt renewable energy sources.

For example, China’s 2021 crackdown on crypto mining led many operations to relocate to countries with abundant renewable resources, such as the U.S. and Canada. In Texas, some mining companies use excess wind and solar power, stabilizing the state’s energy grid while reducing reliance on coal and natural gas.

As of 2024, nearly 40% of Bitcoin mining is powered by renewable energy sources, a significant improvement from previous years.

Source: AGU Pub

The shift toward renewables not only lowers carbon emissions but also reduces operational costs. Renewable energy, especially in regions with surplus capacity, is often cheaper than fossil fuels, creating a win-win scenario for miners and the environment.

From Proof-of-Work to Proof-of-Stake: Emerging Energy-Efficient Alternatives

Bitcoin’s PoW mechanism is the main culprit behind its high energy use and carbon pollution. By design, PoW requires miners to solve computational puzzles, consuming vast amounts of electricity. This has led to Bitcoin’s annual energy consumption surpassing that of some mid-sized countries.

Emerging alternatives like Proof-of-Stake are changing the game. PoS eliminates the need for energy-intensive computations, relying instead on validators who are selected based on their stake in the network. Ethereum’s switch to PoS has set a precedent, showcasing that major blockchains can significantly reduce energy consumption without compromising security or decentralization.

Cardano and Solana are among the leading PoS blockchains prioritizing energy efficiency. Cardano consumes only about 6 gigawatt-hours (GWh) annually, a fraction of Bitcoin’s energy use. Solana, known for its high-speed transactions, operates on a hybrid model with minimal energy requirements.

These networks demonstrate that advanced blockchain functionalities, such as smart contracts and decentralized applications (dApps), can be achieved without compromising environmental goals. Their energy efficiency also aligns with growing investor demand for greener technologies.

Crypto Projects for Nature-Based Carbon Solutions

Innovative projects like SavePlanetEarth (SPE) are tackling Bitcoin’s environmental challenges through nature-based solutions. SPE leverages blockchain technology to support reforestation and afforestation initiatives.

By tokenizing carbon credits linked to these projects, SPE provides a transparent and efficient way to offset emissions.

These initiatives not only mitigate the carbon footprint of Bitcoin mining but also contribute to broader environmental goals, such as biodiversity conservation and ecosystem restoration. Such projects demonstrate how blockchain and crypto can play a proactive role in addressing climate change.

Revolutionizing Carbon Markets with Blockchain

Talking about climate, carbon markets offer significant financial instruments that can help fund various emissions reduction initiatives.

However, traditional carbon credit systems often face challenges such as fraud and lack of transparency. Blockchain technology addresses these issues by providing a decentralized and immutable ledger for tracking and verifying carbon credits. Each credit is tokenized, representing a verified reduction or removal of greenhouse gas emissions.

By using blockchain, every transaction is transparent and traceable, ensuring the authenticity of carbon credits. This enhances accountability, especially for organizations looking to meet sustainability targets.

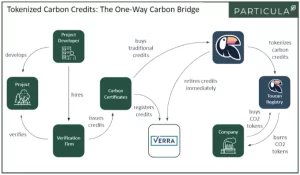

The Toucan Protocol is a prime example of how blockchain enhances trust in carbon markets. The platform tokenizes carbon credits, making them accessible to a broader audience. Each credit is verified and traceable, ensuring its integrity.

Image from Medium

Toucan also allows users to bundle smaller carbon offsets into larger, more marketable assets. This scalability supports global efforts to reduce emissions and makes it easier for companies and individuals to participate in offsetting programs. By combining blockchain’s transparency with innovative tokenization, Toucan is driving progress in carbon markets.

Major carbon standards like Verra and Gold Standard are exploring ways to integrate decentralized systems to improve the verification process.

Blockchain in Renewable Energy Grids

Blockchain is also transforming renewable energy grids by enabling peer-to-peer energy trading. In these systems, households, and businesses with solar panels can sell excess energy directly to others. Blockchain ensures secure and transparent transactions without the need for intermediaries.

Projects such as Power Ledger in Australia and LO3 Energy in the U.S. are leveraging blockchain to create localized energy markets. These initiatives promote renewable energy adoption while increasing grid efficiency and resilience.

The Issues of Double Counting, Scalability, and Trust

One of the most significant challenges in carbon offset markets has been double counting, where the same carbon credit is sold multiple times or claimed by different entities. Blockchain technology provides an effective solution by offering a transparent and tamper-proof record of each carbon credit transaction.

With blockchain, each carbon credit is tokenized, and its transaction history is recorded on a decentralized ledger. This ensures that once a credit is sold or retired, it cannot be reused or misrepresented, drastically reducing the risk of double counting.

Platforms like CarbonX are already implementing blockchain to safeguard the integrity of carbon offset programs. It is a private blockchain ledger designed to capture IoT-based greenhouse gas data for accurate reporting, management, and conversion into carbon commodities.

As Emission Trading Systems (ETS) and Carbon Tax programs continue to roll out globally, blockchain technology is poised to play a crucial role in ensuring compliance with environmental regulations. It also offers new opportunities for carbon asset trading, enhancing transparency and efficiency in the carbon market.

Not only that. Tokenization is a game-changer for carbon credits, making them easier to trade and track across borders.

By converting carbon credits into tokens, blockchain allows for fractional ownership, lower transaction costs, and greater liquidity in carbon markets. This scalability is crucial in meeting the global demand for offsets as businesses and governments strive to achieve their net-zero goals.

As mentioned earlier, the transparency of blockchain ensures that tokenized carbon credits are traceable, improving trust among buyers and sellers.

Blockchain’s Potential for Global Carbon Market Integration

Blockchain has the potential to integrate regional carbon markets into a unified global system, enabling seamless trading of carbon credits across borders. Using blockchain to track credits from multiple countries and regions ensures that the credits are authentic and can be used toward global emissions reduction goals.

This integration not only supports international climate agreements but also fosters collaboration between countries, corporations, and environmental organizations. As such, blockchain could ultimately drive the global carbon market toward greater transparency, efficiency, and scalability. It can then provide a unified approach to tackling climate change.

Final Thoughts

Cryptocurrency and blockchain technology have transformed global finance and data systems, but their environmental impact cannot be ignored. Bitcoin and other crypto networks consume vast amounts of energy, contributing to significant carbon emissions. However, the industry is actively working toward sustainability, with renewable-powered mining, energy-efficient blockchains, and carbon offset initiatives leading the way.

As crypto adoption grows, the balance between innovation and environmental responsibility will be crucial. By embracing greener technologies, the industry can pave the way for a more sustainable digital future.

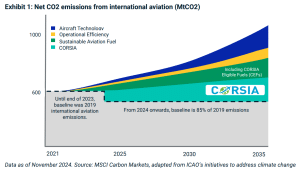

A report analyzing carbon credit demand for over 400 airlines under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) projects significant fluctuations in credit prices and airline costs.

According to modeling by MSCI Carbon Markets, CORSIA-eligible carbon credits could cost between $18-51 per tonne of carbon dioxide equivalent (CO2e) during Phase I, rising to $27-91 in Phase II. If airlines pass these costs on to consumers, international ticket prices could increase by 0.5-1.0% in Phase I.

Alternatively, if airlines absorb the costs, their operating profits could decrease by up to 4%. The impact will vary depending on different demand and supply scenarios.

We crunch the report and here are our key takeaways.

What Are CORSIA Credits? A Flight Plan for Emission Reductions

The aviation sector is one of the fastest-growing contributors to global greenhouse gas (GHG) emissions. As international air travel expands, airlines face increasing pressure to mitigate their environmental impact.

The CORSIA, developed by the International Civil Aviation Organization (ICAO), is designed to limit emissions growth in international aviation. By purchasing carbon offsets known as CORSIA credits, airlines can balance emissions exceeding 2020 levels and invest in sustainability.

CORSIA credits allow airlines to compensate for their emissions by funding projects that reduce or remove CO2. These projects include renewable energy initiatives, reforestation, and carbon capture technologies. Verified under internationally recognized standards such as the Verified Carbon Standard (VCS) and the Gold Standard, these credits ensure that emission reductions are real, additional, and permanent.

CORSIA aims to cap international aviation emissions at 2020 levels. Through its two implementation phases—voluntary (2021–2023) and mandatory (from 2024)—the program encourages investment in global sustainability while aligning the aviation industry with broader climate goals.

Carbon Credit Demand: Will Airlines Keep Up with Rising Costs?

CORSIA’s demand for carbon credits hinges on international aviation growth and decarbonization efforts. Using a bottom-up modeling approach, MSCI Carbon Markets analysts assess individual airline emissions, growth rates, and adoption of sustainable practices to project credit needs.

Demand Scenarios

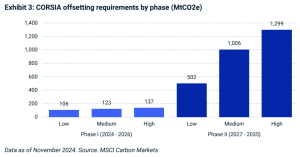

Three scenarios highlight the variability in credit demand:

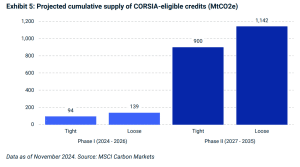

High-Demand Scenario: Strong aviation growth (+4% annually) and slow adoption of sustainable aviation fuels (SAFs) result in higher offsetting needs. Estimated demand reaches 137 million metric tons of CO2 equivalent (MtCO2e) in Phase I (2024–2026) and 1,299 MtCO2e in Phase II (2027–2035).

Medium-Demand Scenario: Moderate aviation growth and increased decarbonization lower credit demand to 123 MtCO2e in Phase I and 1,006 MtCO2e in Phase II.

Low-Demand Scenario: Limited growth and poor adoption of SAFs reduce requirements to 106 MtCO2e in Phase I and 502 MtCO2e in Phase II.

Regional and Airline-Level Insights

Demand will be concentrated among major airlines and regions. For instance, the top 10 airlines are expected to account for 40% of cumulative demand by 2035.

European carriers are likely to lead credit purchases despite regional compliance mechanisms such as the EU Emissions Trading System (ETS). If the ETS is expanded to cover more flights, global demand for CORSIA credits could decrease by 25–50% by 2050.

Supply Struggles: Why CORSIA Credit Availability Could Impact Aviation

The supply of CORSIA-eligible credits faces significant challenges. Credits must meet ICAO criteria, including corresponding adjustments that prevent double counting of emissions reductions under a country’s Nationally Determined Contributions (NDCs). This process requires host countries to authorize projects and align carbon accounting frameworks—a complex and underdeveloped requirement.

As of late 2024, ICAO-approved registries like Verra, Gold Standard, and Climate Action Reserve have expanded the potential credit pool to 230 MtCO2e. However, only 7 MtCO2e of these credits meet Phase I criteria due to limited corresponding adjustments.

Most eligible credits have been issued by a single REDD+ project in Guyana under ART TREES.

A lack of Letters of Authorization (LoAs) from host countries further constrains supply. Of 40 major credit-producing countries assessed, only two are highly prepared to issue LoAs. Without accelerated regulatory progress, substantial credit supply growth is unlikely until the late 2020s.

Projections and Flexibility

Supply projections factor in registry eligibility, crediting timelines, and the readiness of host countries to provide corresponding adjustments. A 30% reduction is applied to projects not yet in the registry pipeline. Despite these hurdles, expanded registry approvals and government action could gradually increase the availability of CORSIA-compliant credits.

Scenarios for Carbon Prices: How High Will CORSIA Credits Soar?

The prices of CORSIA credits will depend on supply-demand dynamics, influenced by credit availability, international aviation growth, and compliance requirements.

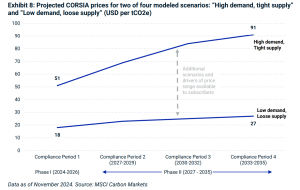

Under high-demand and tight-supply scenarios, Phase I credit prices are expected to range between $18 and $51 per ton of CO2. Prices could climb to $27–$91 per ton during the fourth compliance period (2033–2035) as demand peaks.

Supply-Demand Scenarios

Tight Supply: A potential deficit of 12–43 million tons of CO2 in Phase I could drive prices higher.

Loose Supply: A surplus of 2–33 million tons of CO2 may stabilize prices during Phase I. Airlines also have a grace period until January 2028 to offset emissions, easing initial supply constraints.

In Phase II, higher demand from aviation and other sectors, such as corporate voluntary commitments and sovereign programs, could lead to significant price increases.

Market Value Estimates

The market for CORSIA-eligible credits could reach $2–$8 billion by Phase I and grow to $5–$66 billion by the fourth compliance period. This growth reflects both rising demand and the financial implications of carbon market integration.

Implications for Airlines and Carbon Markets

CORSIA credits are an essential tool for airlines to manage emissions and comply with climate regulations. However, reliance on credits is only a short-term solution.

Long-term strategies include investment in SAFs or Sustainable Aviation Fuel, fleet upgrades, and operational efficiencies. Airlines with slower decarbonization may face higher offsetting costs, incentivizing innovation and sustainable practices.

Geopolitical factors and regulatory developments will heavily influence the carbon market. Expanding participation and ensuring the environmental integrity of credits are critical to maintaining trust and achieving emissions reductions.

CORSIA credits are pivotal to the aviation industry’s efforts to cap emissions and contribute to global climate goals. Although challenges remain in scaling credit supply and ensuring regulatory compliance, CORSIA serves as a transitional mechanism while the sector invests in greener technologies. As demand for high-quality offsets grows, the aviation industry’s collaboration with carbon markets will shape the roadmap of global emissions reductions.

Ever since Trump came to power, there have been serious speculations about America’s future from a climate perspective. We saw clean energy stocks tumble like a pack of cards and Trump’s “drill, baby, drill” policies eventually taking shape.

Well, at this conjecture, Reuters came up with an interesting report explaining that Donald Trump’s energy team is planning an aggressive agenda to reshape U.S. energy policy. He will prioritize expanding liquefied natural gas (LNG) exports, increasing offshore oil drilling, and streamlining permits for federal land projects.

These actions signal a dramatic shift from the Biden administration’s climate-focused pro-renewables policies. Let’sdeep dive into what’s onTrump’s agenda…

Fast-Tracking LNG Exports, Restart Oil and Drilling

The report further highlighted that under the Biden administration, several significant LNG projects were delayed. Venture Global’s CP2, Commonwealth LNG, and Energy Transfer’s Lake Charles facilityall of them are based inLouisiana. Trump wants to de-freeze and approve these projects which would send a strong message of support for the natural gas sector.

Federal records revealed,

“Five U.S. LNG export projects that have been approved by the Federal Energy Regulatory Commission are still awaiting permit approvals at the Department of Energy (DOE).”

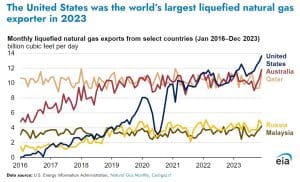

The U.S., as the leading LNG exporter, plays a key role in global energy. With Europe seeking U.S. gas to cut reliance on Russia, Trump aims to seize the opportunity. This means there would be faster approvals, unlocking massive LNG infrastructure investments.

EIA notes, that in 2023 the U.S. LNG exports averaged 11.9 billion cubic feet per day (Bcf/d)—a 12% increase (1.3 Bcf/d) compared with 2022.

Notably,Trump’s team also aims to accelerate oil and gas drilling off the U.S. coast and on federal lands. Federal lands currently account for a quarter of U.S. oil production and 12% of natural gas output.

During his first term, drilling permits took significantly less time to process compared to the Biden administration. This time he plans to reinstate a concrete long-term drilling plan that would expand offshore lease sales and fast-track all permit approvals to increase energy product. His focus will primarily be on regions having rich oil reserves.

Now taking about the stats, Reuters reported,

“According to federal data, oil output on federal lands and waters hit a record in 2023, while gas production reached its highest level since 2016.”

The report also revealed that Trump is most likely to persuade the IEA on pro-oil decisions. However, his advisors have urged him to suppress funding unless the IEA adopts a more pro-oil stance.

Dan Eberhart, CEO of oilfield service firm Canary said,

“I have pushed Trump in person and his team generally on pressuring the IEA to return to its core mission of energy security and to pivot away from greenwashing.”

A symbolic yet bold move would be Trump’s push to approve the Keystone XL pipeline, a project canceled downrightly by Biden. However, reviving the pipeline has challenges, as land easements have been returned and construction would require starting from scratch. Even so, Trump’s endorsement signals a commitment to fossil fuel infrastructure.

Trump’s Stance on Inflation Reduction Act:A “Green Scam”?

Prior to his win, we have read and seen all around how he openly criticized the Inflation Reduction Act (IRA), calling it a “green scam”. He also pledged to repeal it if he returned to power once again.

This bold statement has raised questions about the future of the Biden administration’s $369 billion energy transition agenda. While his rhetoric may signal trouble for renewable energy sectors like electric vehicles (EVs) and wind power, Trump’s track record suggests a more nuanced approach to industrial policy and critical mineral supply chains.

But Critical Minerals are Safe in Trump’s Hands…

The IRA has funneled significant resources into renewable energy, but it also supports rebuilding America’s industrial base. For instance, $75 million was allocated to upgrade Constellium’s aluminum rolling mill in West Virginia. Efforts like these align with Trump’s earlier policies emphasizing industrial revitalization and reduced reliance on foreign nations for critical resources.

In 2020, Trump declared the United States’ dependence on foreign critical minerals a national emergency. A second Trump administration is unlikely to abandon this push for metal self-sufficiency. Instead, he may amplify efforts to boost domestic production of key materials like aluminum, nickel, and lithium.

The good news is cross-party consensus on this issue suggests that funding for industrial projects tied to critical minerals may be safe, even under a Republican administration.

America First: China in Scrutiny

Both the Department of Energy (DOE) and the Department of Defense (DOD) have prioritized investments in rebuilding U.S. metals capacity. While the DOE focuses on EV battery metals like lithium, the DOD has diversified its investments toward antimony to zirconium. All these moves align toward reducing dependency on China for critical minerals.

Projects like Talon Metals’ Tamarack nickel initiative in Minnesota have already received federal funding. However, the nickel market faces significant challenges due to Indonesia’s mining boom, which has driven down prices. Most of Indonesia’s nickel production is controlled by Chinese entities, complicating matters for U.S. companies like Ford, which are sourcing Indonesian nickel for EV batteries.

Trump’s “America First” philosophy highlights his strong opposition to critical metal imports from China. His administration will probably scrutinize even joint ventures like Ford’s collaboration with Indonesia’s Vale and Huayou Cobalt. Even if these ventures technically qualify for IRA subsidies, their ties to Chinese supply chains may face new barriers under his administration.

Can America Be Great Again?

Despite Trump’s bitterness about the IRA, his administration may continue supporting parts of it that align with domestic industrial goals. Consequently building U.S. mineral independence will significantly reduce reliance on China and secure advanced technology materials.

Concisely, this means a second Trump presidency might prioritize America’s self-sufficiency while addressing IRA’s initiatives to fit in his “Make America Great Again” agenda.

This report suggests that Trump’s policies could possibly reinforce a robust U.S. oil, gas, and critical minerals industry. While his decision on renewables like EVs and tariffs on imports are still uncertain, he prioritizes critical minerals which is assuring for national security and economic competitiveness.

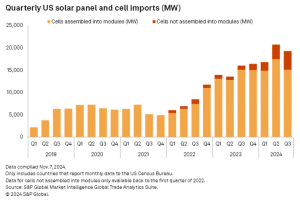

US imports of crystalline-silicon solar cells saw a dramatic increase in the third quarter of 2024, rising more than fourfold compared to the same period in 2023, according to S&P Global Commodity Insights. This surge reflects the growing demand from rapidly expanding domestic solar panel factories, fueled by policy shifts and significant investments in US solar manufacturing.

Solar Power Driving Up the Clean Energy Revolution

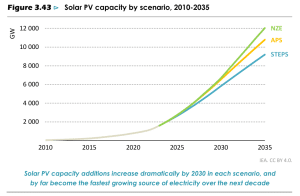

Solar energy is accelerating global energy transitions, driven by affordability and technological advancements. According to the IEA’s World Energy Outlook 2024, solar photovoltaic (PV) systems are a leading force in clean energy deployment.

By 2030, solar could account for over 40% of new power capacity, emphasizing its pivotal role in global decarbonization efforts.

Moreover, renewables’ electricity generation share will climb from 22% to 58% by 2035, driven primarily by solar PV. This growth is supported by record investment and strong policy support in renewables, helping to address energy security concerns and reduce emissions.

The 2022 Inflation Reduction Act (IRA), central to Biden’s clean energy policy, provides up to $1.2 trillion in tax incentives over a decade to drive clean energy growth. Its advanced manufacturing tax credit has spurred over $34 billion in solar investments. This resulted in numerous new or expanded solar module factories across the U.S.

Solar module production capacity in the country has skyrocketed, exceeding 45 GW as of October. At peak production, these solar manufacturing facilities could fulfill most of the U.S. solar demand projected for 2025.

Imports of photovoltaic (PV) cells not yet assembled into panels reached 4,230 MW in Q3. That is a sharp increase from 903 MW in the third quarter of 2023, according to S&P Global Market Intelligence’s Global Trade Analytics Suite.

Over the first nine months of 2024, unassembled PV cell imports totaled 9,454 MW, up nearly 286% from 2,448 MW during the same period in 2023.

This increase follows President Joe Biden’s August decision to raise the annual cap on tariff-free PV cell imports from 5 GW to 12.5 GW. Biden highlighted the solar industry’s “positive adjustment to import competition” and the growth in module production capacity as key reasons for the policy change.

The IRA has played a pivotal role in incentivizing domestic solar panel production through lucrative tax credits. However, despite these gains, a lack of crystalline cell, wafer, and ingot manufacturing capacity in the US leaves panel manufacturers heavily reliant on imported components.

With President-elect Donald Trump promising to introduce new tariffs on foreign-made goods to support US manufacturing, the solar industry is preparing for potential shifts in trade policy that could impact supply chains.

Robust Module Imports

While domestic module production ramps up, imports of fully assembled solar panels remain strong. The US imported 15 GW of modules in Q3 2024, slightly lower than the record 17.4 GW in Q2 but consistent with Q3 2023 levels, per S&P Global report.

For the first nine months of 2024, total panel imports reached 47.3 GW, up from 41 GW in the same period last year. Combined cell and module imports for January–September exceeded 56.7 GW, representing a 31% increase from the 43.4 GW imported during the same period in 2023.

With this robust supply chain, the US solar market could install over 46 GWdc of solar panels in 2024. Plus, an additional 43.3 GWdc in 2025, according to S&P Global Commodity Insights.

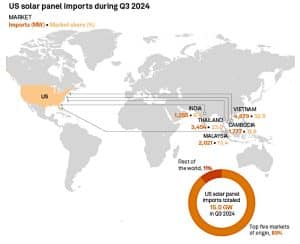

The majority of crystalline solar cell imports in Q3 came from factories in Southeast Asia as shown above. Malaysia led the pack, accounting for 37.3% of U.S. imports, followed by Thailand (27.6%) and South Korea (20%). Vietnam and Laos contributed smaller shares, at 4% and 3.7%, respectively.

Panel imports, including both crystalline and thin-film technologies, were also primarily sourced from Southeast Asia. Vietnam supplied 32.5%, Thailand contributed 23%, and Malaysia accounted for 13.4%. Other key contributors included Cambodia (11.8%) and India (8.4%).

Leading the Solar Revolution: Top Companies Driving Innovation

As solar energy is gaining momentum globally, key players are also making significant strides.

For one, Toronto-based SolarBank Corporation, focusing on utility-scale and community solar projects across North America, just delivered 600 MW of clean energy in the U.S. and Canada. Expanding into new markets like New York, its initiatives offset significant carbon emissions, accelerating the energy transition.