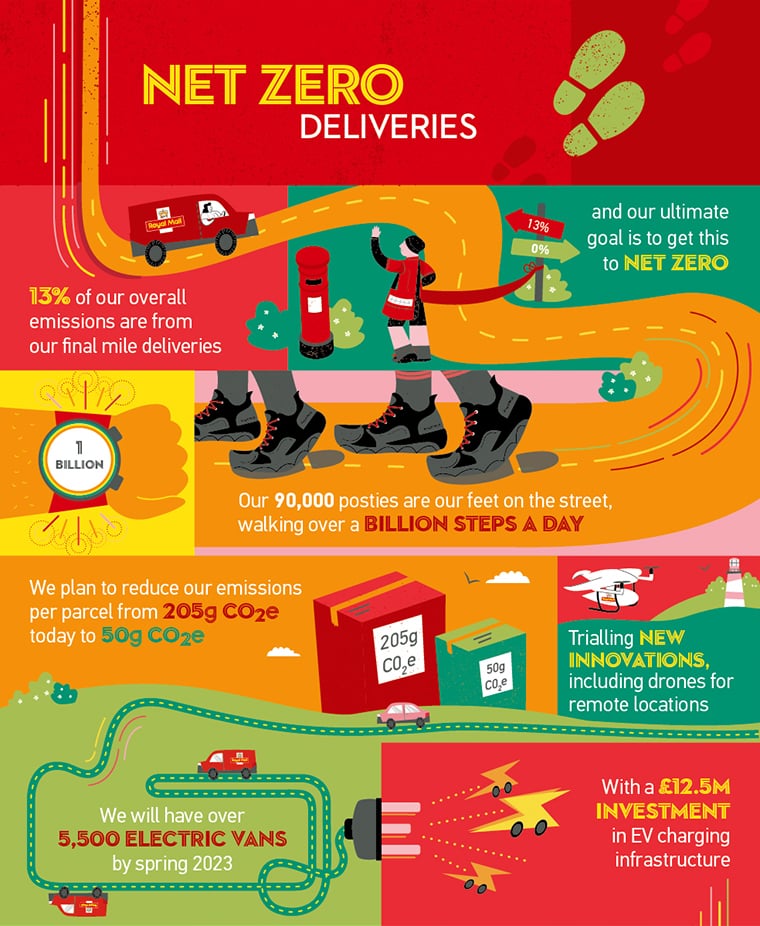

The UK’s Royal Mail revealed an ambitious net zero carbon emissions target by 2040 through its new four-pillar ‘Steps to Zero’ plan.

The British postal service and courier company outlined its plans to reduce emissions from deliveries, operations, and the supply chain. In particular, its net zero plan includes a long-term goal to cut down its carbon emissions per parcel it delivers in the UK from 205gCO2e today to 50gCO2e.

The company’s 90,000 posties are walking over a billion steps daily to deliver parcels to 31 million addresses. These ‘feet on the street’ make the company a green option for delivering parcels.

Yet, its 4-pillar Steps to Zero plan goes further, embracing the urgency of tackling climate change.

Per Simon Thompson, Royal Mail’s CEO:

“A seven-day parcel service, to and from the customer’s door, delivered by a postie you trust and with the lowest emissions is the winning proposition.“

He also added that the environment is the next battleground for businesses. And setting an ambitious target to cut parcel emissions to 50 gCO2e shows the firm’s commitment to minimizing its impact on the environment.

Royal Mail’s Net Zero Emissions Plan

For 2020-21, Royal Mail posted a 5.8%increase in its total carbon footprint which is due to an increased volume of parcels. But it also posted a 6.9% reduction in carbon intensity when intensity is measured per £1m of revenues.

The company seeks to reach its net zero targets by 2040, 10 years earlier than the world’s goal by 2050. It pledged to reduce Scope 1 (direct) and 2 (power-related) emissions by 25% by 2025/26.

At the same time, its target for Scope 3 emissions is a 25% reduction between 2020/21 and 2030.

Such targets are in line with 1.5C from the Science Based Targets initiative (SBTi).

The “Steps to Zero”

Royal Mail’s net zero emissions plan is a four-pillar strategy to address the climate crisis; each pillar consists of specific net zero emissions targets.

Here are the four pillars and their corresponding targets and measures.

1. Net Zero deliveries: fleet electrification

13% of Royal Mail’s total emissions are from final mile deliveries. And so the firm seeks to reduce this to zero by:

Growing electric vans (EVs) to 5,500 by Spring 2023

Investing £12.5m in charging infrastructure across the country in 2022/23

Trying new innovations like drones for remote locations

2. Net Zero operations: 100% renewable electricity

49% of Royal Mail’s emissions are from domestic operations, including transport networks and buildings. Measures to reduce them include:

Moving to 100% renewable electricity across the business from 2022

Royal Mail’s largest solar panel installation will go live at the new Midlands Parcel Hub in 2023.

3. Making circular happen: circularity via reuse and reduce

Royal Mail’s 3rd pillar for net zero emissions involves transforming its operations and behaviors toward circularity.

In particular, it will apply reuse models and reduce single-use items, targeting to achieve:

25% reduction in waste by 2030

Increase recycled content of plastic delivery bags

Elimination of cable ties in mail bags

Help customers embrace their own circular journey via its Parcel Collect service

4. Collaborating for action: drive net zero in the industry

The final pillar of Royal Mail’s ‘Steps to Zero’ plan is all about collaboration with other businesses across the UK’s postal system to standardize reporting on CO2e per parcel. This is to help customers make an informed decision about their delivery/courier needs.

Also under this pillar, Royal Mail emphasized its intention to collaborate with other fleet operators to speed up the decarbonization of transport via rolling out of EVs and low emission vehicles.

The company will also look at all commercial vehicles and new fuel types not just electric.

Royal Mail is a member of The Climate Group’s EV100 initiative. The group sought to make EVs “the new normal” by 2030.

According to Royal Mail’s CEO, pulling forward its net zero emissions target by 10 years to 2040 means the company has to:

“… transform the way we collect, process, and deliver the 10 billion letters and parcels we handle each year.”

The company will report its ‘Steps to Zero’ progress annually and later in June through its ESG report.

DeepMarkit responded to the current industry dialogue on tokenizing retired, expired, and low-quality carbon credits, also known as “zombie credits”.

The company is motivated by recent discourse and remarks by leading registries, Verra and Gold Standard, pertaining to the tokenization of active and validated credits only.

Their statements marked a positive development in the industry and its stakeholders as they have a crucial role in keeping the integrity of the carbon credit market.

Through its MintCarbon.io platform, DeepMarkit believes that the blockchain continues to have a vital role in providing more transparency, utility, and liquidity in the market. The platform is designed to ensure the quality and legitimacy of all minted credits.

DeepMarkit’s interim CEO stated that their regulated public company is deeply aware of the challenges and issues facing the new ‘crypto-carbon’ space and that he’s proud of their team’s efforts to identify friction points early in their development cycle.

The company also reaffirmed that it solely tokenizes (ERC-1155) tokens based on active, verified, and high-quality carbon credits that allow buyers to fund legitimate carbon projects.

DeepMarkit looks forward to continuing to respond to the industry’s dialogue about this matter.

Canadian Environment Minister Steven Guilbeault proposed regulations to create Canada’s first carbon offset market to help big industries cut their greenhouse gas emissions.

Same with the general standard, one credit is equal to each tonne of emissions reduced, according to the regulation.

Canada’s First Carbon Offset Credit Market

Carbon offset credits will be created when an entity like a municipality, a company, or a farmer reduces its own emissions more than they have to.

But those credits need to be registered and independently verified first before an entity can sell them.

There are several standards that use different methods to measure and verify emission reduction. These standards provide a robust verification process to ensure the credibility of emission reduction projects. The most widely used ones are Verra, Gold Standard, and American Carbon Registry.

Businesses that pay the federal carbon price can buy carbon offset credits to lessen the cost they have to pay.

Right now, big industrial emitters can buy and sell carbon credits created by other companies under the federal carbon pricing system. But the carbon offset markets will expand this system beyond those firms covered by the regulated pricing mechanism.

Under the carbon offset market, prices tend to be cheaper as demand is created by various buyers and not by regulated mandates. Different factors also impact carbon prices like project type, size, location, and co-benefits.

Companies that are unable to achieve their emission targets can get carbon offset credits by investing in projects that cut carbon emissions. These projects vary from deforestation to industrial gas capture.

The first Canadian carbon offset market is for credits produced by municipalities that capture methane from their landfills.

While future markets will be up for cutting emissions from farmland and forests, as well as reducing or eliminating fluorinated refrigerants in advanced refrigeration systems.

Once this carbon offset market operates, Canada can expect to see more emissions reduction schemes to help entities offset their carbon footprint.

The federal government released Canada’s 2030 Emissions Reduction Plan last March. It’s the first plan describing the nation’s pledge to reduce its GHG emissions outlining measures Canada needs to achieve its 2030 target and 2050 net-zero emissions.

Ernst & Young (EY) Net Zero Centre analysis revealed that achieving net zero emissions means carbon credits volume will grow by 40x and price be at $150 per ton by 2035.

The pressures to decarbonize are mounting. Over a hundred countries committed to the Paris Agreement and set ambitious climate goals.

Also, the number of organizations and businesses disclosing net zero pledges tripled in 2021. What’s more, investors and consumers are favoring climate action with their money.

All signs are pointing in one direction. Yet, meeting the world’s net zero pledges can be challenging and costly for businesses.

But entities have to find essential and cost-effective emissions reduction and carbon credits can provide that.

As for the EY Net Zero Centre, 50-80% of decarbonization costs in line with the Paris Agreement can be achieved through carbon credit offsets.

Why Carbon Credits Volume Will Balloon by 30x to 40x

The EY’s report provided the outlook for carbon credits and offsets volume between now and 2050. The analysis aims to help companies make clear pathways to net zero emissions by 2050 and manage the uncertainties involved.

Carbon credits are an essential part of the business toolbox. They support earlier and more ambitious net zero commitments of companies.

But hitting net zero emissions can take time and may involve uncertainties. Still, by using carbon credit offsets to reduce emissions, businesses can be profitable in the short run while they’re moving towards net zero in the long run.

Here’s how emissions offsetting works using carbon credits:

Carbon credits volume is expected to balloon by 30x to 40x their current levels if the world is to meet the Paris climate goals.

That’s because competition for carbon credits will heat up, emissions reductions will scale up, and regulations will ramp up.

While it’s certain that the voluntary carbon market poses to explode, how the market develops remains uncertain.

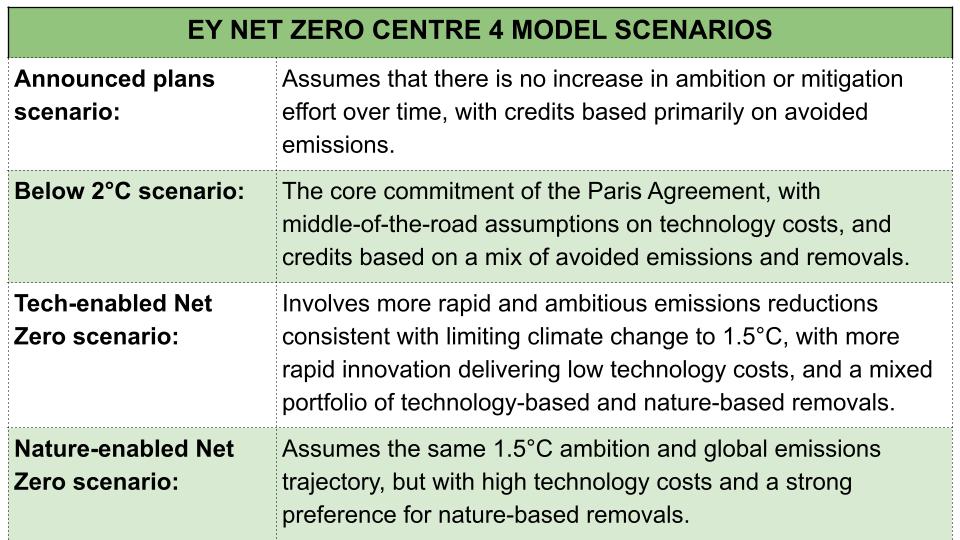

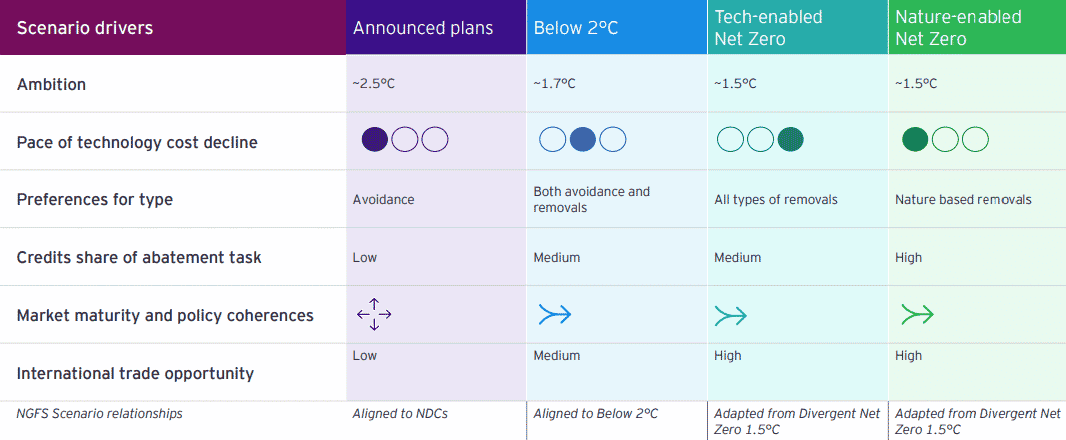

So, to explore the possible carbon credit market role and outlook, the EY Net Zero Centre developed four future scenario models.

The four scenarios consider different combinations of climate, technology, and institutional drivers which are:

Across all four outlooks, the analysis reveals these major findings:

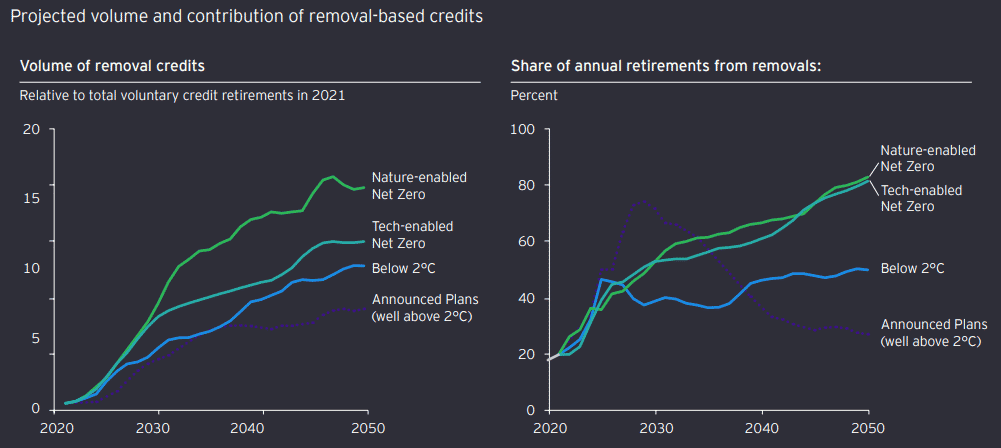

Carbon credit volume will increase to 30-40x current supply by 2035

Rising demand makes the volume and price of carbon credits grow rapidly to 2035. After that, the volume of credits grows more slowly across all the four outlooks analyzed.

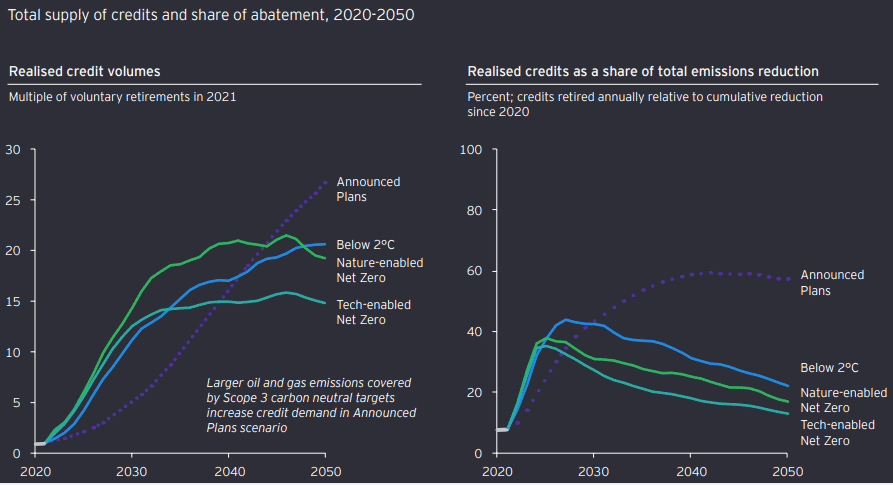

The projections for carbon credit supply volumes are shown for four scenarios in the chart below.

The left chart plots the increase in credit volumes needed to meet the emissions reduction commitments by 2050. While the right one shows the share of total reductions met using carbon credits (includes both avoidance-based and removals-based credits).

The volumes rise rapidly in Paris-consistent scenarios. And that’s despite credits having a decreasing share of emissions reductions.

The projections assume that 100% of carbon offsets and credits are high integrity across all scenarios. Also, all credits have additional permanent reductions in emissions.

In other words, there’s no greenwashing. Greenwashing is conveying a false or a misleading claim to make the public believe that a company is reducing its emissions even if it’s not.

Rising demand, race to quality, and climbing unit supply costs = carbon credits become scarce and expensive across all four outlooks

EY’s analysis finds that scaling up carbon credit volumes will deplete available low-cost supply fast. As a result, there’ll be rapid increases in credit prices to 2035 across all four model scenarios.

In a typical market, growing demand for a good/service will not result in higher prices over the long term if supply is elastic.

But the case for the supply of high-quality carbon credits is different. It’s subject to some constraints such as:

geopolitics of climate commitments (ex. the notion of common but differentiated responsibilities)

the increasing importance of more costly removals-based credits.

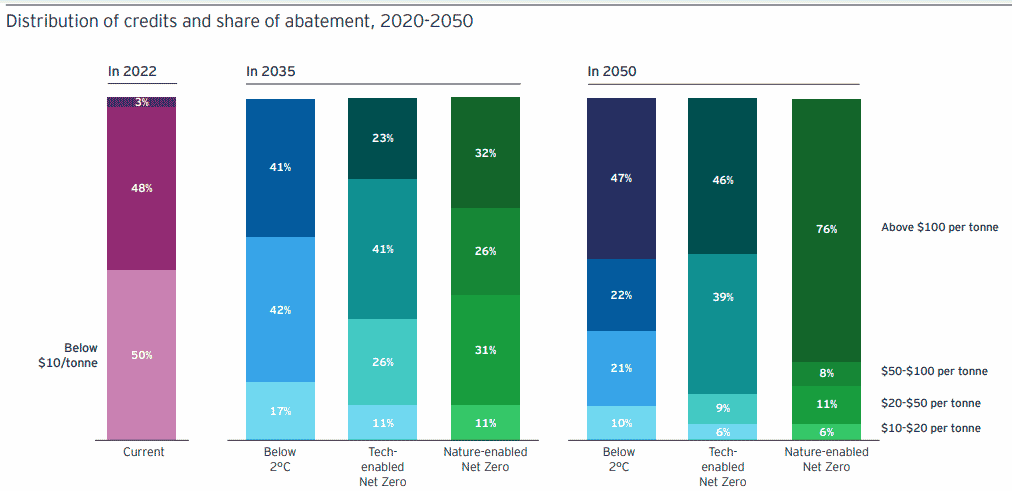

Average costs of high-quality carbon credits supply will rise as volume increases.

About 40-60% of credits will cost over US$50 per tonne by 2035 as the figure shows.

The price increases will continue after 2035 in most scenarios. This is due to an incremental increase in emissions reductions among businesses.

This scenario will boost competition for avoidance-based credits and raise the need for removals-based credits.

But price increases for the Tech-enabled scenario will moderate after 2030 or 2035. This reflects the common assumption for faster and bigger reductions in technology costs.

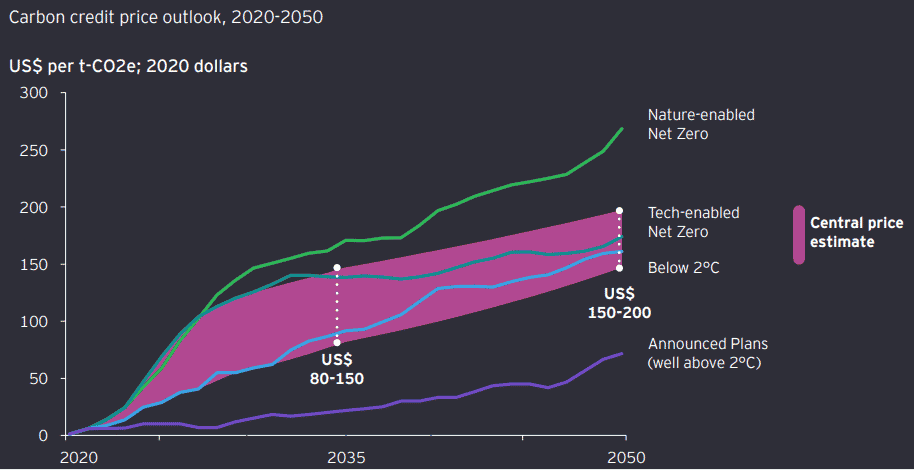

Credit Prices Will Rise to US$80-150/Ton by 2035

EY Net Zero Centre’s central estimate deems that countries and companies move quickly to execute actions and policies that are consistent with the Paris accord.

The projection further assumes that costs of abatement and supply of credits will be in the middle or lower end of the range explored.

The graph below reveals the results of these price assumptions.

The analysis suggests credit prices can rise from under $25/tCO2e today to $80-150/tCO2e in 2035. And they’ll continue to rise to $150-$200/tCOe in 2050 (in real 2020 dollars).

Another key analysis by EY is that tightening emissions budgets will affect the mix of carbon credits demanded and how they are used.

Tighter Emissions Budgets Drive Removals-based Credits Up

Changes in technology costs and policy context will shift baselines for carbon credit offset projects. These will make it harder to create credits based on avoided emissions while sboosting the role of removals-based credits.

And so, removal credits become essential in net zero scenarios.

This forecast is very crucial to note as avoidance-based credits dominate the current global use and volume of carbon credits. They account for ~80% of all credits issued and ~90% of all credits used (or retired) in 2020 across the largest voluntary registries.

Thus, technologies that remove carbon from the air will be a vital part of reducing emissions to limit the harsh effects of climate change.

Moreover, stricter government regulations will drive several changes in carbon credit markets.

However, this is unlikely to prevent strong growth in the demand for carbon credits as net zero emissions targets still need offsets.

What’s more significant is that tightening regulation will blur the distinction between voluntary and compliance markets for carbon credits.

This will increase the need for companies to use the supply of high-quality carbon credits, especially beyond 2035.

Lastly, market fundamentals will drive the emergence of large and efficient carbon exchanges. This will enable the trading of a high volume of carbon credits through top carbon exchanges linked to various carbon registries.

All these market trends amplify the risks and opportunities created by the need to reach climate goals. For business leaders, this means the need to engage and act urgently.

And every leader needs to have a clear net zero strategy embracing the role of carbon credit to create new value in a rapidly changing industry.

Everland unveiled “The Forest Plan” to end deforestation by developing up to 75 forest conservation (REDD+) projects around the world.

Everland represents the world’s largest portfolio of high-impact forest conservation (REDD+) projects. They’re particularly found in Southeast Asia, Africa, and Latin America.

It brings forest communities and corporations together for a common cause:

to protect the world’s most important and vulnerable forests.

It’s a time-bound action plan that marks Everland’s commitment to ending deforestation, the leading cause of climate change, by 2030.

The company will scale the resources available to conserve forests through the plan.

Everland’s Forest Plan: The Data-Driven Solution to Deforestation

The Forest Plan is the largest single voluntary carbon finance initiative to date. It has over $2 billion for 10-year commitments to REDD+ projects and communities.

A Community Relations Officer from the Kasigau Corridor REDD+ Project in Kenya noted during the plan’s launch:

“Without a doubt, the REDD+ mechanism has brought sustainable livelihoods into our communities where there are now jobs, opportunities for building sustainable community-based enterprises, and funding for schools and healthcare facilities.”

The plan is a science- and experience-based approach focusing on tackling the root cause of deforestation.

It seeks to use data to form an effective response to two urgent planetary challenges: the climate crisis and the loss of biodiversity. Everland forest plan will do so with speed and scale.

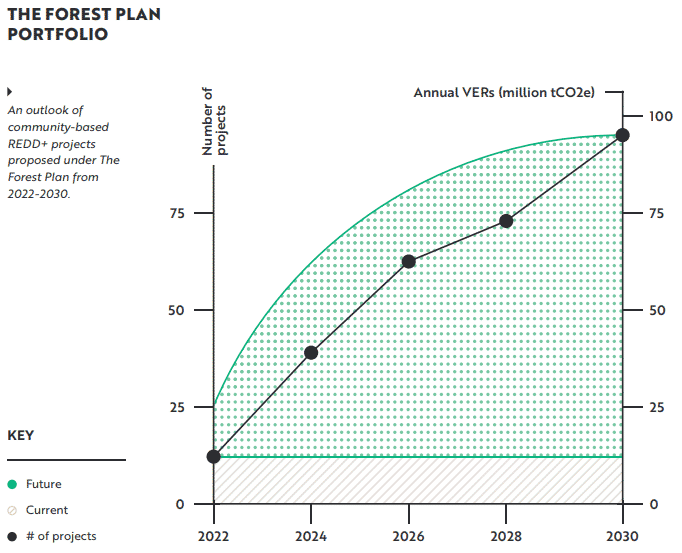

The plan has been shaped by respected experts and community leaders from around the world. In particular, it will help the development and long-term financing for up to 75 REDD+ projects in threatened forests.

Here’s the plan’s outlook for REDD+ projects from 2022 to 2030.

The Everland’s Forest Plan serves as a call to action across four areas:

Expanding high-impact, community-based REDD+ to its full potential.

Enabling national and jurisdictional REDD+ programs to achieve effective results.

Prioritizing rights of Indigenous Peoples and Local Communities (IPLCs).

Empowering supply chain-based initiatives to end deforestation to achieve effective results.

It will further scale REDD+ financing beyond this initiative with more projects by other Everland partners.

Carbon Credits of the Plan

Under the plan, project developers, communities, and governments leading the work will generate 90 million tons of verified carbon creditseach year. In total, that would be over 800 million tons by 2030.

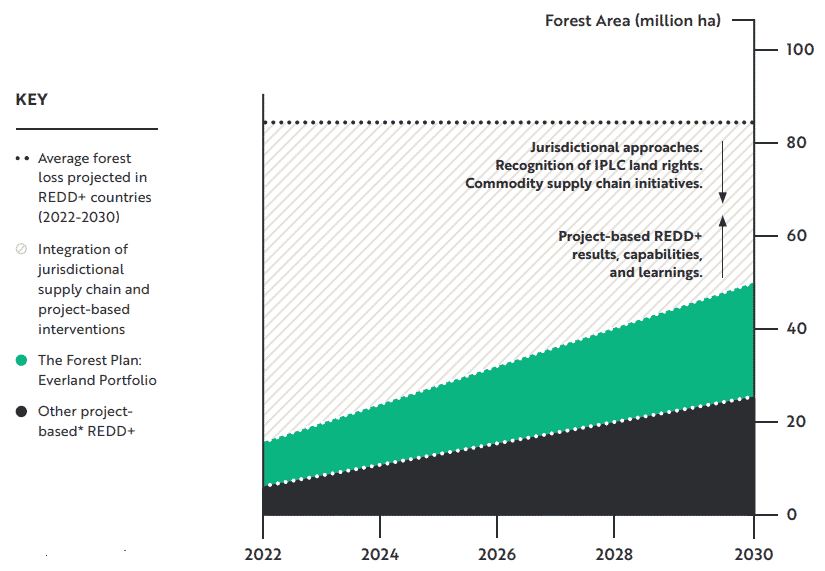

The community-based forest projects by Everland, plus other REDD+ projects, can protect a total of about 50.5 million hectares. This equals 17% of the projected deforestation in 15 critical forest nations.

The forest projects represented by Everland cover 23 million hectares.

The chart shows the forest area covered under The Forest Plan portfolio projects.

As per Josh Tosteson, Everland President:

“Preserving forests is central to the climate fight, yet failures on past pledges have brought us to where we are today… Perhaps more than anything else, the goal of The Forest Plan is to show that there is a legitimate, data-driven basis for hope. Through aligned, dedicated collective action and collaboration, we can, in fact, end deforestation.”

He further said that carbon emissions from tropical deforestation are far higher than expected. And with forest loss rates doubling in two decades, there’s indeed an urgency to act now.

Hence, the Forest Plan by Everland came about to quicken the actions needed to stop deforestation by the end of this decade.

For instance, it will support forest nations to achieve their Nationally Determined Contributions (NDCs) under the Paris Agreement goals.

It will also provide access to private sector resources to finance these projects in those countries.

More remarkable is the key role that businesses play in ensuring the achievement of the forest plan’s goals. They can do so by investing in the projects as part of their emission reduction targets to offset their unavoidable emissions.

Many large companies have been directing their funds to REDD+ projects that the Forest Plan supports.

But how exactly will the plan operate?

How Forest Plan Will Work

People often decide to exploit the forest or convert it for commodity crops or other uses because few alternatives are available.

This is where the REDD+ projects come in to help. Their main goal is to resolve deforestation by delivering financial proceeds to forest stakeholders for their conservation efforts.

By doing so, buyers and financiers drive resources directly to the ground level by purchasing Verified Emission Reductions (carbon credits) from the project. These carbon credits are 3rd party verified to high-quality standards.

The REDD+ projects will then deliver transformative impacts on communities and governance. And with these impacts, forest stakeholders will realize the new value that gives them incentives to protect the forests.

And so, project by project, landscape by landscape, Everland’s Forest Plan seeks to bring this model to its full potential as fast as possible. This is the plan’s core.

Everland will keep track of the progress of The Forest Plan’s portfolio against key performance indicators or KPIs targets. It will look deeply into each project’s impacts and results on communities, biodiversity, and the climate.

The Forest Plan’s aims may be lofty but they’re a part of a bigger, collective effort to end deforestation. And Everland plans to achieve it by 2030 through carbon credits generation.

The Carbon Credit Quality Initiative (CCQI) launched a new online scoring tool to assess the quality of three types of carbon credits.

The CCQI is led by Environmental Defense Fund, World Wildlife Fund (WWF-US), and Oeko-Institut. It offers free online resources that include its robust assessment method and interactive scoring tool.

The free online CCQI Scoring Tool allows buyers to evaluate the quality of carbon credits. This will help them to make more informed decisions in the booming carbon credit market when buying credits.

Ultimately, the initiative aims to improve the quality of carbon credits transacted in the market. It does so by showing which ones provide the greatest climate impact.

CCQI Online Scoring Tool for Carbon Credits Quality

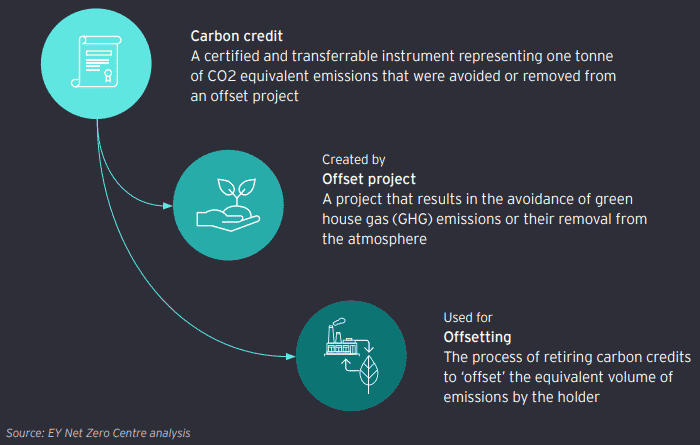

Carbon credits are tradeable permits allowing polluters to offset carbon emissions or prevent them. Typically, one carbon credit equals one ton of carbon or other greenhouse gases.

The CCQI online tool gives scores for the quality of three commonly used projects that generate carbon credits. These are:

The voluntary carbon market has grown so fast in recent years. More and more entities have set net zero emissions goals and use carbon credits to offset part of their emissions or to finance climate measures.

But the quality of carbon credits available varies to date. And the results of CCQI’s first round of scorings confirm this. It reveals that carbon credits perform great in some criteria but poorly in others.

For instance, efficient cookstove projects have drawbacks in quantifying emission reductions and addressing non-permanence. Yet, most often they generate high environmental and social benefits.

As per the Senior Director of Climate at Environmental Defense Fund Pedro Martins Barata:

“CCQI’s first round of scoring confirmed that there is both wheat and chaff in the carbon credit market. The important thing, however, is that the consumer can tell the difference.”

He added that CCQI’s free and transparent online scoring tool can move the market toward quality by helping users understand what quality means for carbon credits.

CCQI methodology’s quality criteria for carbon credits

Under the CCQI’s methodology, a carbon credit is scored on an interval scale of 1 through 5 against several quality objectives. This enables buyers to understand the nuances and trade-offs in the quality of carbon credits to make an informed decision.

Lambert Schneider from the Oeko-Institut remarked that:

“What makes a high-quality carbon credit is a complex question… We designed our Scoring Tool so that users could have a nuanced 360-degree view of different quality features of carbon credits. The scorings show a mixed performance of carbon credit programs.”

In particular, the CCQI scores show notable differences between carbon crediting programs.

For instance, the scoring results reveal that Clean Development Mechanism has the best third-party auditing rules. While the Climate Action Reserve performed best in its approach to compensating for potential non-permanence.

Likewise, the Gold Standard has the most comprehensive environmental and social safeguards. Whereas the Verified Carbon Standard or Verra performed high in its governance, transparency, and approaches for reducing non-permanence risks.

According to Brad Schallert, WWF’s director of carbon market governance and aviation:

“When buyers come to the carbon credit market, they are sometimes surprised that detailed guidance on how to evaluate credits is not publicly available… CCQI hopes to fill this information gap by offering our scoring tool.”

Using CCQI’s online tool is one of several steps a buyer can take when performing due diligence on how carbon credits differ in quality.

CCQI’s 7 Quality Objectives

What makes a high-quality carbon credit is not a simple question. It depends on many different factors.

The CCQI tool uses 19 quality criteria assessed based on their importance and the context in which the carbon credit is generated and used.

For example, some criteria may not be relevant for all types of climate mitigation activities. This is particularly the case with measures that address the risk of non-permanence.

These criteria are then organized under CCQI’s seven “Quality Objectives”. The table below identifies and explains each quality criterion.

CCQI will expand its free online Scoring Tool to assess more carbon credits. This is to let users know how other project types and programs perform on quality as well as cover a bigger part of the market.

CCQI’s next round of scores will be up for release later by the end of this year.

The Paris Agreement created different ways to fight climate change and the EU’s Carbon Border Adjustment Mechanism (CBAM) is one of them.

Several efforts were made to limit GHG emissions globally. All these measures seek to influence the carbon price tied to producing goods or services that emit CO2.

The main purpose of carbon prices is to reduce carbon emissions, particularly in high emitting sectors. At the same time, revenues fromcarbon pricing present opportunities for governments and businesses to support the shift to a sustainable economy.

But latest events in the carbon market urged regulators to review their climate policies. And the EU has been very active in this case as it aims to be the kingmaker in the sector.

This guide will explain one of the EU’s latest policy proposals on carbon pricing: the Carbon Border Adjustment Mechanism (CBAM).

But before we discuss the details of the EU’s CBAM, let’s explain first the general term it falls under – the Border Carbon Adjustment or BCA.

The BCA Approach to Carbon Pricing

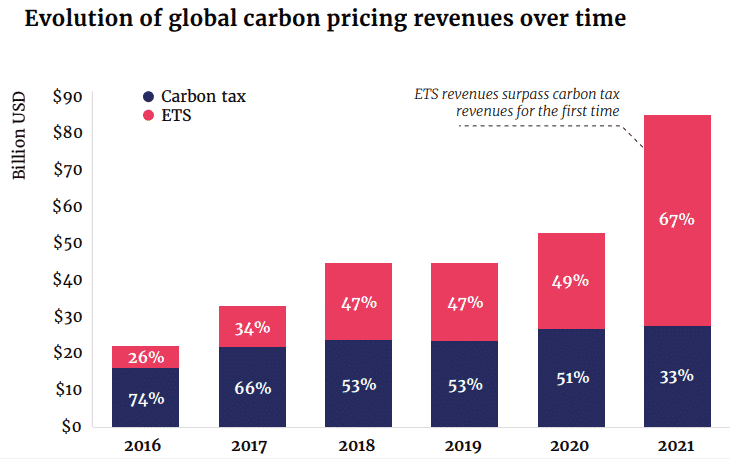

Among the different types of carbon pricing, carbon taxes used to be the highest generating revenue instrument.

But that was before 2021 when revenues from Emissions Trading Systems (ETS) exceeded carbon taxes revenues for the first time. The chart below shows that.

Source: World Bank Report

ETS refers to the compliance carbon market where carbon prices are driven by government policy. They’re also called the cap-and-trade emissions system.

Government policies usually inform the maximum emission limits (cap) which are also known as allowances or credits that an entity can emit.

Carbon polluters can buy or sell carbon credits based on emissions they produce in relation to their allowance limits.

If they are below their cap, they can sell their excess allowances. But if they are over their limit, they can buy to cover the shortfall.

And one of them is carbon leakage which is a big concern for industry stakeholders and politicians alike.

Carbon leakage refers to the risk where emissions reduced in one country are offset by increased emissions in another country.

It can reduce the efficiency of climate policies by shifting emissions to laxer countries. This can lead to an increase in global carbon emissions.

And so, cross-border approaches to carbon pricing come into play to address the issue of carbon leakage. They’re increasingly recognized by countries and a Border Carbon Adjustment or BCA is one of those approaches.

BCA is an environmental trade policy that applies domestic carbon pricing to imported goods. This carbon pricing mechanism reflects the regulatory costs born by domestically produced carbon-intensive products but not by the same, foreign-produced products.

It’s a policy option that exists in the absence of a global, unified carbon pricing policy or an international agreement on how to deal with it.

Even if BCA is a very recent policy for carbon pricing, some countries are citing it as a means to adopt a direct carbon price. These nations include Ukraine, Uruguay, and Taiwan.

But the EU’s approach would be by far the biggest one – its CBAM.

What is the EU CBAM?

The EU’s CBAM is one form of BCA mechanism for carbon pricing. Its ultimate goals are twofold:

To avoid trade advantages and disadvantages as countries have different climate policies’ ambition

CBAM creates a level playing field by making foreign importers face the same costs and incentives that domestic producers experience.

In essence, it protects the climate ambition and the domestic industry of the country enacting it.

In July 2021, the European Commission (EC) presented the “Fit for 55” legislative package. It contained 13 policy measures to reduce the EU’s GHG emissions by 55% in 2030 from their 1990 levels. It has a main goal to reach climate neutrality or net zero emissions by 2050.

That package includes the CBAM, which will introduce a carbon price on certain products imported into the EU. The EU Council and the European Parliament are responsible for enacting the EU CBAM proposal.

On March 15, 2022, the Council reached an agreement on the CBAM regulation.

As per Bruno Le Maire, French Minister for Economic Affairs, Finance and Recovery:

“The agreement in the Council on the CBAM is a victory for European climate policy. It will give us a tool to speed up the decarbonisation of our industry while protecting it from companies from countries with less ambitious climate goals.”

He added that it will also incentivize other countries to become more sustainable and emit less.

Another main aim of EU CBAM is to avoid carbon leakage. It can happen when production relocates to other countries with weaker climate policies (lower carbon prices).

If that occurs, it can lead to a loss of revenues in countries with ambitious climate goals like the EU.

CBAM will also encourage trading partners to establish their own carbon pricing policies.

How Does the EU CBAM Work

EU’s CBAM is designed to function in parallel with the EU’s Emissions Trading System (EU ETS). In particular, it will gradually replace the free allocation of EU ETS allowances.

EU ETS is the European carbon credit contract that is exchange-traded. It is by far the biggest regulated carbon market trading carbon credits or the EU allowance (EUA).

When an entity buys a carbon allowance from the EU ETS, they gain permission to generate one ton of CO2 emissions. Carbon revenues then flow vertically from companies to regulators.

Under the voluntary carbon market (without government regulation), companies can also buy carbon credits generated by various projects around the world. They range from nature-based projects like reforestation and technology-based carbon removal projects.

The idea is pretty much the same: one carbon credit = one ton of carbon emissions offset or avoided. Firms can also buy credits from different carbon exchanges to voluntarily offset their emissions.

On the other hand, the EU’s CBAM involves applying a carbon price to imports of certain goods to the EU. This price is proportionate to the goods’ “embodied emissions”, referring to the emissions generated during their production. They don’t mean the carbon that the goods physically contain.

Under the CBAM, EU importers must buy CBAM certificates in relation to the goods’ embodied emissions. Just like the current EU allowance,each CBAM certificate equals one ton of emissions.

Essentially, the number of CBAM certificates must be equal to the total embodied emissions of the imported goods.

And the price of CBAM certificates should reflect that of the EU ETS allowances in the week before the import of goods.

Once a carbon price has been paid in the country of origin of the imported goods, the required CBAM certificates can be reduced by such paid amount (e.g. the origin country’s own ETS or carbon tax).

CBAM certificates will be valid for two years from the date of purchase.

CBAM’s Application

The EU CBAM applies to the import of electricity and certain goods including:

steel,

iron,

cement,

fertilizer, and

aluminum sectors

Initially, it will apply only to Scope 1 emissions or direct emissions. But importers need to report on embodied Scope 2 indirect emissions from electricity consumption as well.

Determining embodied emissions can be done in two ways:

Actual emissions: recorded at production installation level (at country of origin) and verified by accredited verifiers.

Default values: applied where importers cannot show actual emissions generated by the goods. It refers to the average emissions in the country of export, plus a mark-up.

For electricity, calculations will rely on third-country default values. But electricity imports from countries whose markets integrate with that of the EU would be an exception.

The CBAM will enter into force as early as 2023 in a transitional way, and it is likely to fully apply from 2026. During its transitional period (2023-2025), EU importers must meet reporting requirements. But they don’t need to buy CBAM certificates yet.

Once the carbon policy is fully in force in 2026, importers have to pay for CBAM certificates to import CBAM goods.

CBAM Carbon Pricing Impact on Non-EU Countries

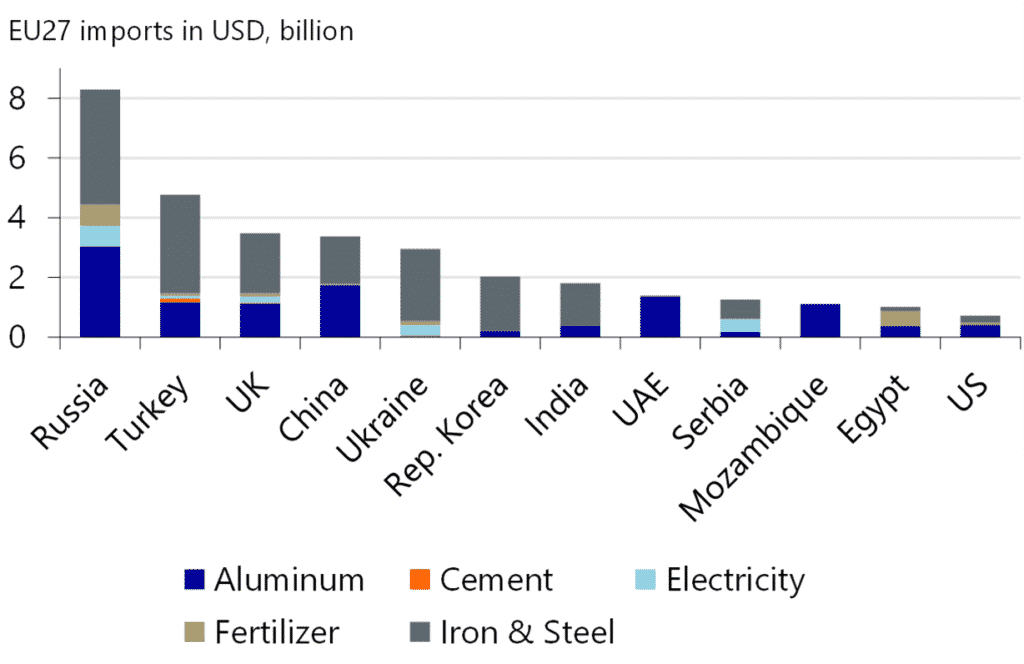

To know which non-EU countries are most likely impacted by the CBAM, studies look at the exports of CBAM products.

Obviously, Russia is the biggest provider of CBAM products to the EU. It is then followed by Turkey, the UK, and China as shown in the graph below.

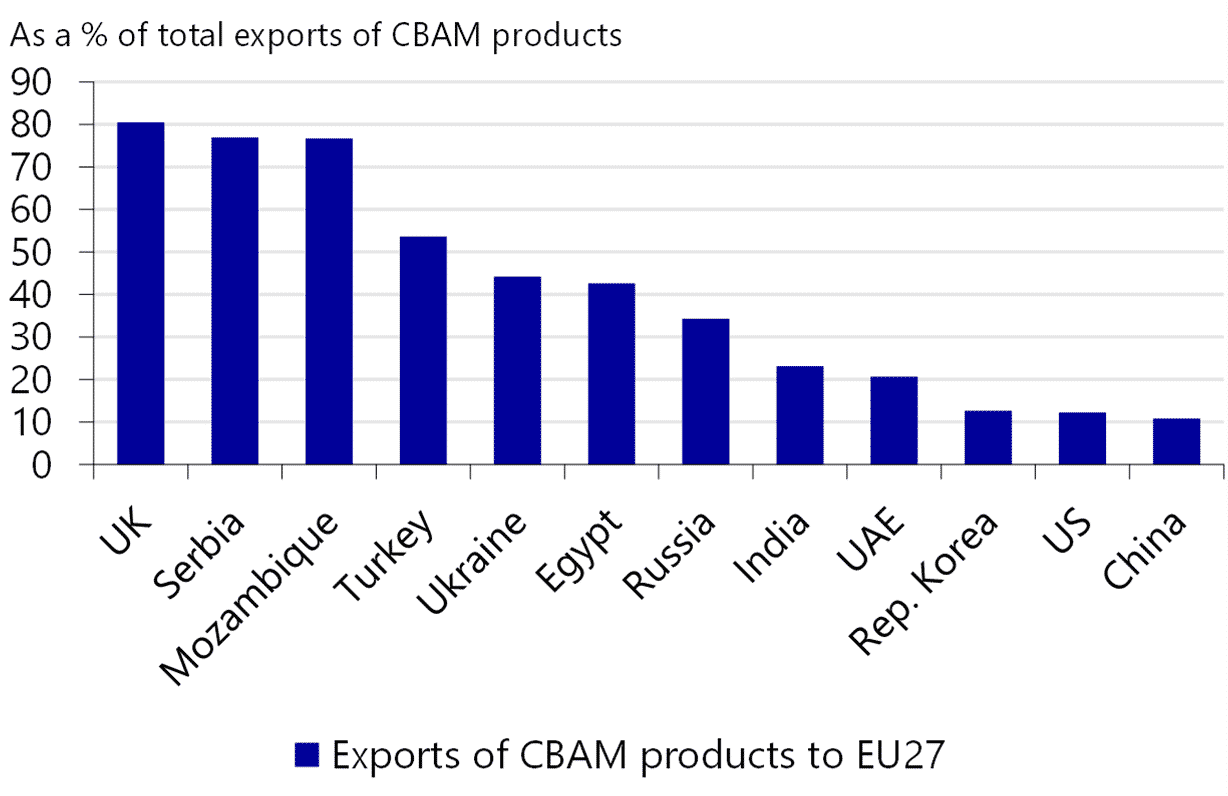

Meanwhile, the most affected non-EU states under CBAM would be the UK, Serbia, and Mozambique as shown in the chart in terms of export percentage. Around 80% of their CBAM exports go to the EU.

It’s important to note that based on the current ETS systems in major trading partners with existing carbon pricing, there’ll be some exceptions in EU CBAM.

For instance, CBAM products from the UK are an exception due to the country’s own emissions system. While imports from South Korea will also have lower CBAM prices than other jurisdictions because of its own carbon pricing.

CBAM Effects on the EU Member States

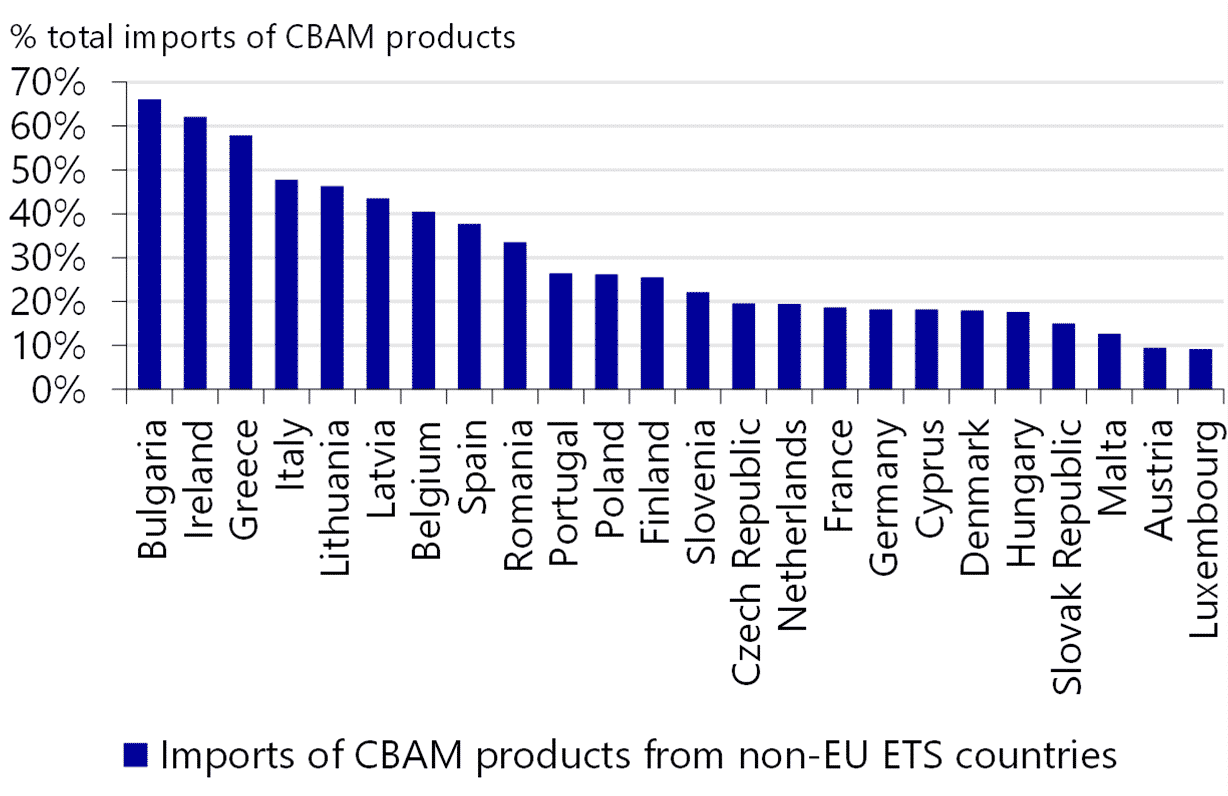

Not only non-EU nations but also the EU member states themselves could be hurt by the CBAM as they may face higher import costs.

In particular, Bulgaria would be the most at risk of having imports taxed by the CBAM. This is because it has a high reliance on CBAM imports from other countries outside the EU.

The chart below shows other EU member states affected by the CBAM carbon pricing mechanism.

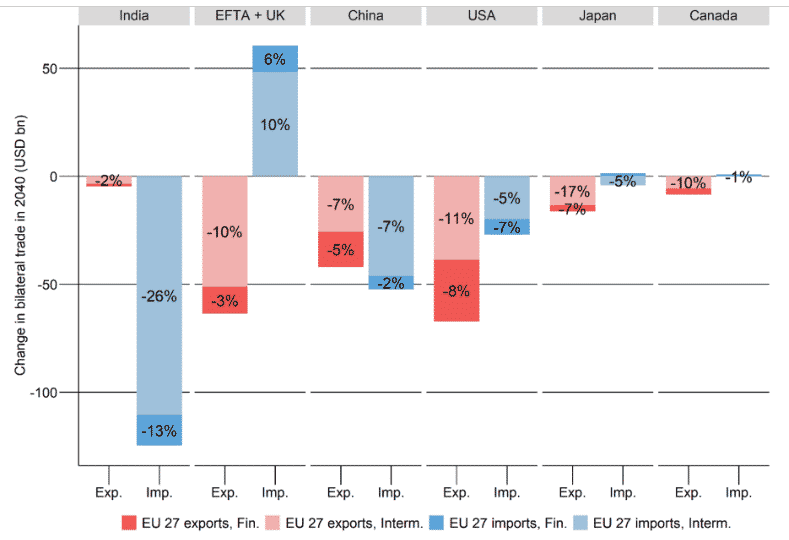

Another possible impact of the CBAM is on the bilateral exports of the main European trading partners of carbon-intensive products.

The figure below shows the impact on EU bilateral exports to (in red) and imports from (in blue) selected countries in 2040. A darker shade refers to the final products exported.

Source: CEPII Working Paper No. 2022-01

Interestingly, there are trade imbalances favoring Canada, Japan, and the US. The UK and European Free Trade Association (EFTA) are extreme cases. They benefit from low-carbon compensation and so increase their exports.

On the other hand, the CBAM deeply affects India, with a -26% drop in its exports to the EU as projected.

EU CBAM Drawbacks and What it Means for Businesses

The proposal for the CBAM is now under review by the European Parliament and the European Council. Some amendments proposed include making the transitional period shorter and sooner. This is to rid of the EU ETS free allocation much more rapidly.

While the CBAM holds promising changes in carbon pricing in the EU ETS, some find it so complicated. Others said that this BCA policy involves a very complex administrative process.

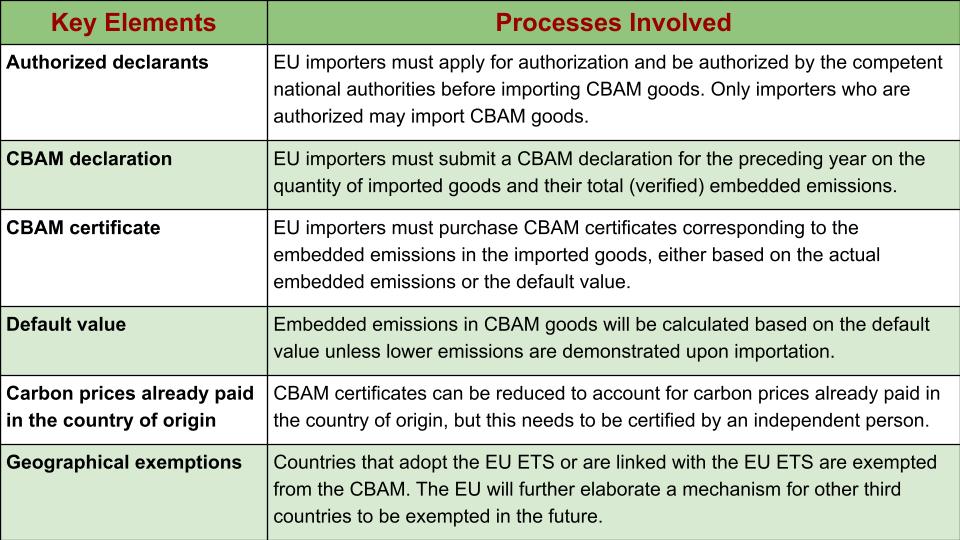

The following are the key elements of the CBAM administration process:

Even if the CBAM still needs approval to become a policy, some proactive steps can help businesses prepare in advance to avoid high administrative burdens.

For instance, companies may:

Evaluate potential CBAM impact on their operations: purchase data, bill of material, etc.

Quantify CBAM exposure: value and number of transactions of goods to import/export

Review global value chain and footprint: ex. determine strategies for investing in manufacturing facilities to reduce emissions

Identify alternative sources available: goods with lower to no CBAM impact

The EU CBAM and other BCA mechanisms are gradually taking shape. They will make a significant impact on reducing carbon footprint and reaching net zero emissions.

The impact is not only in the EU region but also across the global sourcing and distribution footprint of the businesses covered by the CBAM.

The CBAM carbon pricing may give companies more work to do when it comes to accounting and administration. But it also presents a great opportunity to meet their Environmental, Social, and Governance (ESG) criteria. ESG is one of the criteria that investors look into when making their investments.

You can check out our news page to stay on top of the recent events in the EU carbon market. You can also monitor carbon prices here to help guide your investment decision.

Direct Air Capture (DAC) is one of the key technologies that governments and businesses use in fighting climate change.

The latest IPCC report on climate change says that apart from carbon emissions efforts, limiting global warming to the critical 1.5⁰C will depend on DAC technology.

So how does it work, what are the top 3 Direct Air Capture companies, and what’s the role of DAC in reducing emissions?

This guide will help you know how direct air capture works. It will also explain the four important things to know about DAC in the fight for climate change.

DAC: A Carbon Dioxide Removal Technology

You can think about the CO2 in the Earth’s atmosphere like a bucket and that bucket is now almost full. To prevent that bucket from overflowing (or staying below the global warming limit), we have to cut back our GHG emissions.

For many climate activists, carbon dioxide removal (CDR) seems to be the last hope to keep the CO2 bucket full. This, along with huge emissions reduction efforts, will help materialize the Paris Agreement.

Carbon removal pathways particularly include the development of direct air capture technology. Though DAC won’t keep the world below the 1.5⁰C limit alone, it can help drain out some of the emissions dumped in the air.

This CDR technology is gaining traction and receiving the spotlight as this decade is the key to reaching net zero emissions. So, you’re more likely hearing DAC most often and wondering how it functions and what it’s all about.

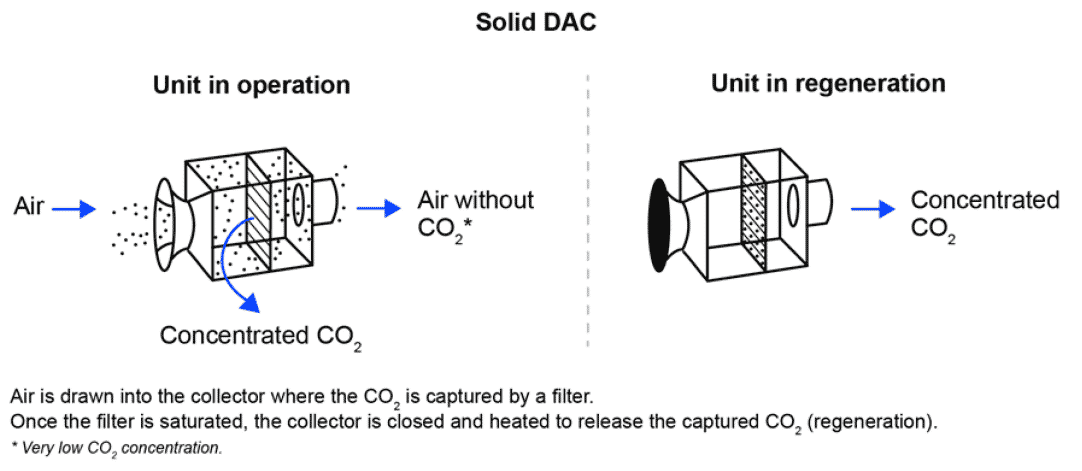

How Direct Air Capture Works (Solid vs. Liquid DAC)

Simply put, direct air capture technology sucks in air through a fan. It is then passed through a material that absorbs the carbon dioxide from the air.

There are two technology approaches that are currently used to capture CO2 from the air: solid and liquid DAC. Climeworks, the largest DAC operating company so far, uses a solid filter.

Solid DAC technology (S-DAC) uses solid sorbent filters that bind with CO2. When these filters are full of air, the units that house the fans are closed and then heated. Once heated, the filters release the concentrated CO2 which can be captured for storage or use.

An S-DAC plant comes in modular design and may include as many units as needed. For instance, the biggest operating S-DAC plant captures 4,000 tons of CO2 a year. The image below shows how the solid direct air capture process works.

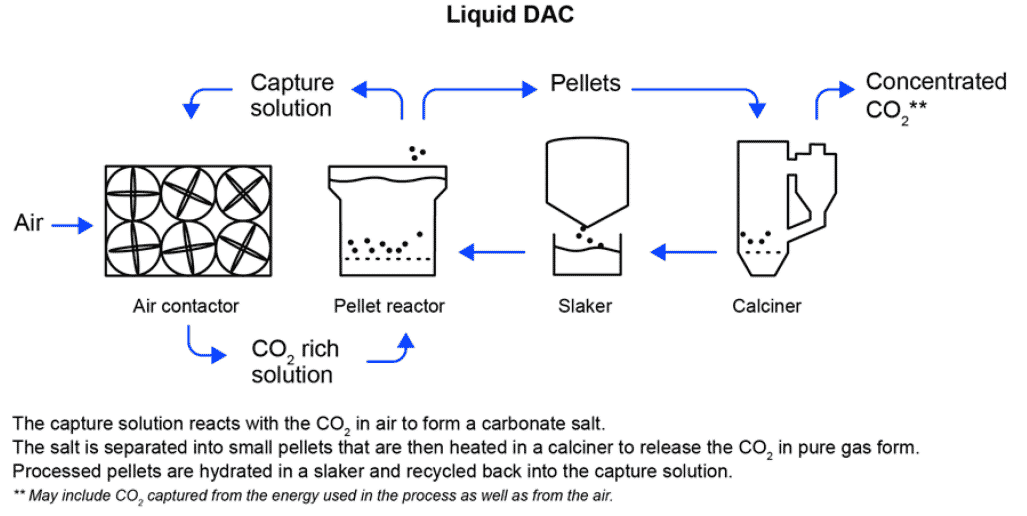

On the other hand, liquid DAC technology (L-DAC) uses a chemical solution like potassium hydroxide to draw in CO2. L-DAC is based on two closed chemical loops.

The first loop occurs in the contactor unit which brings the air into contact with potassium hydroxide. The second loop releases the captured CO2 from the solution in a series of units operating at high temperatures (300°C – 900°C).

The following picture illustrates how L-DAC technology operates.

An L-DAC plant can capture around 1 MtCO2 a year. Carbon Engineering is using this kind of direct air capture process.

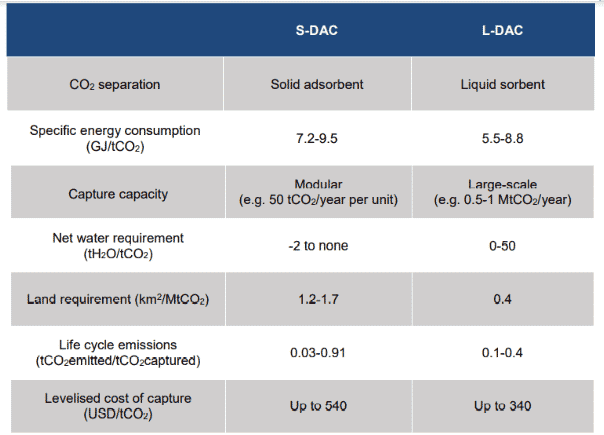

While each DAC technology has its distinct features, both have the potential to remove CO2 from the air. The captured CO2 can be stored permanently or can be a raw material for carbon neutral products.

Moreover, both DAC options don’t need vast land to operate and they work at different temperatures. They’re fit for large-scale operations (L-DAC), as well as small-scale but modular and scalable operations (S-DAC).

The table distinguishes the key features between the two DAC technology approaches.

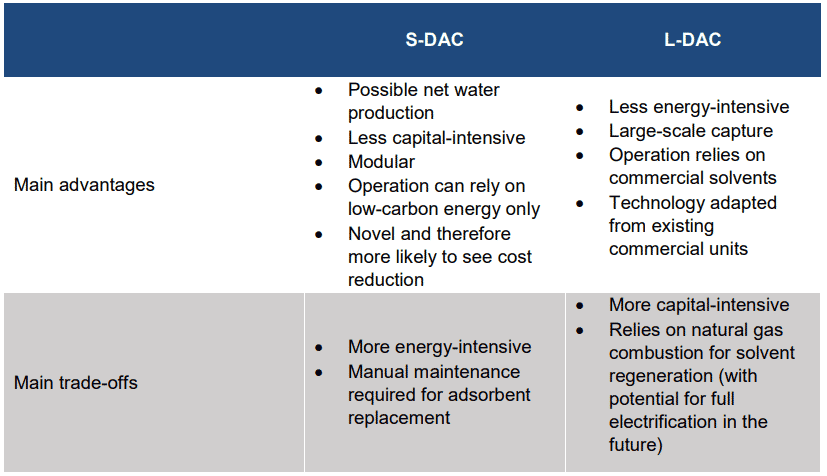

While the table below compares the major advantages and trade-offs of using these DAC technologies.

4 Essential Things to Know About DAC

With the expected rise in carbon dioxide removal schemes, more and more people are also asking for other important things about DAC.

For instance, how expensive is direct air capture? What are the leading direct air capture companies? What’s the role of DAC in meeting net zero emissions goals and who is investing in DAC?

Let’s address each question one by one.

Direct Air Capture Cost

Capturing CO2 from the air costs more than capturing it from a point source.

This is because the atmospheric CO2 is much more dilute than the flue gas of a power station, for instance. This results in the higher energy need and cost of DAC relative to other CDR technologies.

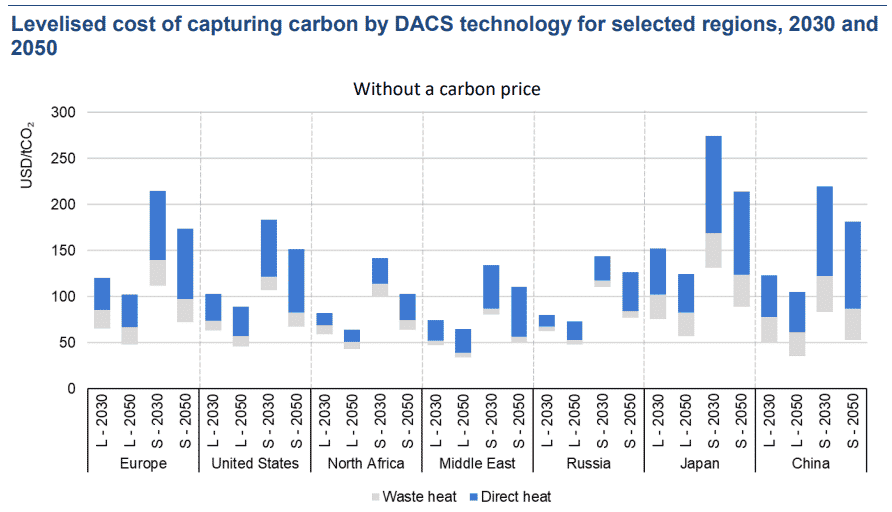

Here’s the direct air capture cost in USD for every ton of CO2, as per CO2 concentrations.

Source: IEA, 2022

As DAC technology has yet to be demonstrated on a large scale, its costs are uncertain. Capture cost estimates range anywhere from $200/t – $700/t.

While cost estimates from the top DAC technology companies varies: $95 to $230/tCO2 for L-DAC and $100 to $600/tCO2 for S-DAC. The actual DAC cost depends on a couple of things such as:

Technology choice,

CAPEX (capital expense) for DAC plant

Energy source,

Carbon price, and

Scale of DAC deployment

All these factors affect the regional cost of carbon removal via direct air capture.

On a regional level, CAPEX is likely to be lower in China, the Middle East, Russia, and North Africa than in Europe and the US. This is because of the cheaper materials and lower gas prices in those parts of the world.

Whereas CO2 prices will be higher in Europe, the US, and Japan (up to $250/tCO2) than in other regions.

But DAC costs will likely drop by 31-43% during 2020-2030 and by 10-24% during 2030-2050 as shown in the graphs. This is due to the considerable cost reduction potential of DAC.

In particular, its potential for performance improvement is also high. Plus, there’ll be massive DAC deployment as a policy response to the climate crisis.

Source: IEA, 2022

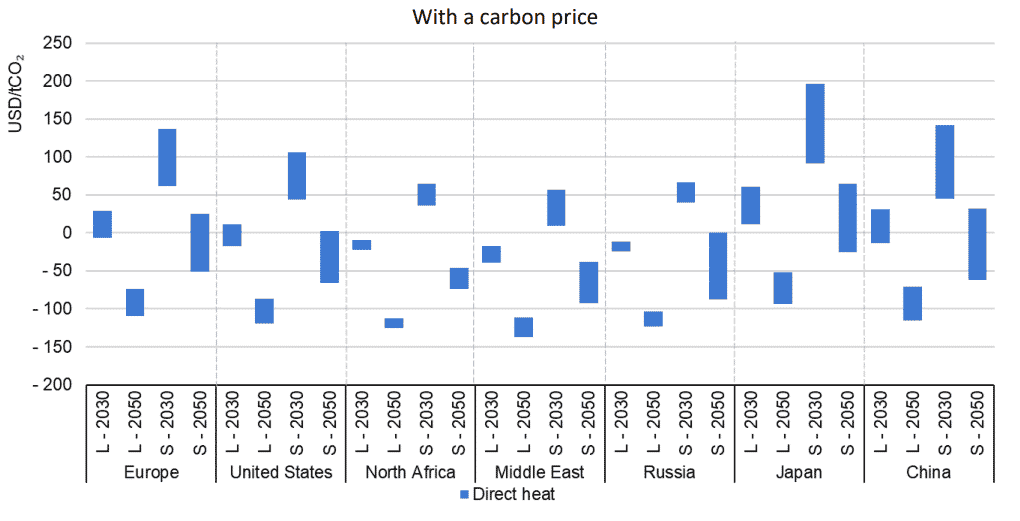

Without a carbon price like a tax, all the regions can capture CO2 directly from the air for less than $100/tCO2. Not surprisingly, the Middle East can enjoy a DAC cost below $50/tCO2. Thanks to its low CAPEX, low natural gas prices, and low electricity prices.

Meanwhile, a carbon price of USD 250/tCO2 in 2050 allows DAC to be profitable in all regions. That’s when a DAC plant sources power from heat and renewable energy (solar PV, or onshore and offshore wind).

In a global DAC scale deployment, the CAPEX cost in line with the Net Zero scenario can decrease a lot, up to 49-65% lower in 2030 and 65-80% lower in 2050.

So, high renewable energy sources and the best DAC technologies for electricity and heat can reduce total direct air capture costs.

Top 3 Direct Air Capture Companies

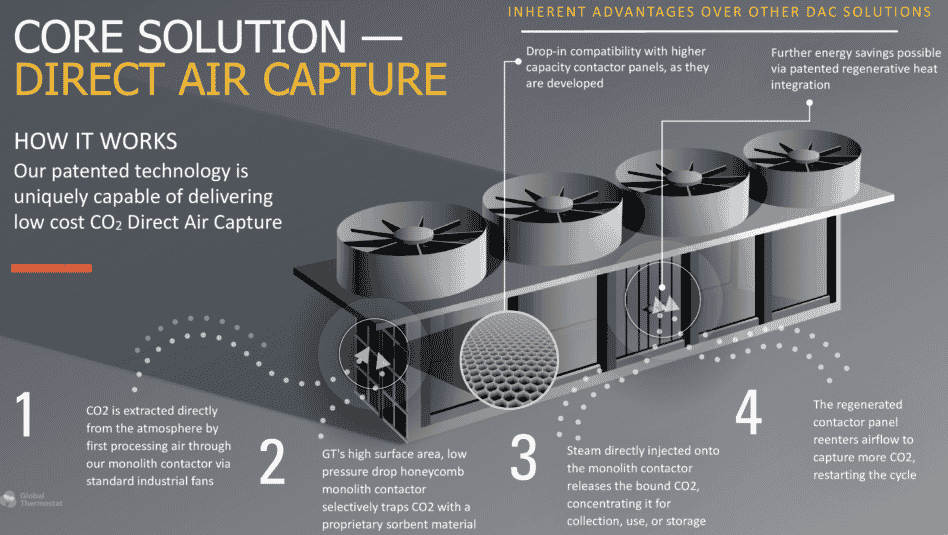

The top 3 in the sector are Climeworks, Carbon Engineering, and Global Thermostat.

Climeworks:

Zurich-based Climeworks is a DAC company founded in 2009 as a spin-off of the research university ETH Zurich.

As mentioned, Climeworks uses S-DAC with a solid filter that absorbs CO2. The image below shows how Climeworks’ direct air capture technology works.

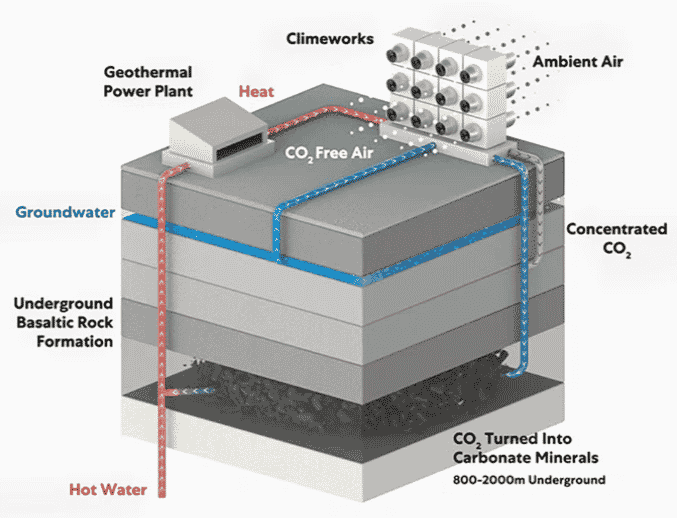

To date, it has constructed a total of 15 DAC plants worldwide. It built the $15 million Orca DAC plant in Iceland that sucks CO2 out of the air and pumped it deep underground for permanent storage.

Orca is the first industrial-scale direct air capture and storage plant, capturing about 4,000 tons of CO2 a year. This corresponds to a yearly emission of about 600 people residing in Europe.

Climeworks’ Orca is built next to a geothermal plant, a ready-made source of renewable energy to heat the CO2. While its other DAC plants get energy solely from renewable sources or from burning waste.

About 10 tons of CO2 are emitted for every 100 tons sequestered by DAC.

Right now, Climeworks continues to scale up. It was a Venture Kick winner in 2010, a Venture Leader in 2017, and one of the TOP 100 Swiss Startups from 2011 to 2014.

Carbon Engineering:

Vancouver-based Carbon Engineering Ltd. has a direct air capture pilot plant in British Columbia. It was also founded in 2009 from academic work on carbon management technologies at the University of Calgary and Carnegie Mellon University.

Carbon Engineering (CE) licensed its technology to 1PointFive (a joint venture between Oxy Low Carbon Ventures and Rusheen Capital Management). It aims to build a DAC plant capable of capturing 1 million tons of CO2 a year in 2024.

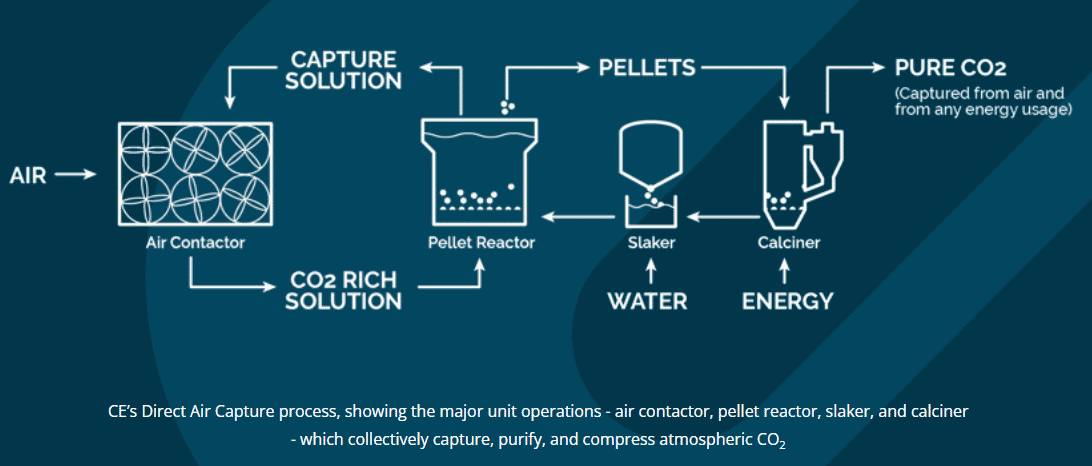

CE’s DAC technology sucks in atmospheric air with a fan. It uses potassium hydroxide solution (L-DAC) to bind the captured CO2 molecules. Then it extracts pure CO2 in gas form through a series of chemical reactions while returning the rest of the air back to the environment.

Here’s how CE’s liquid direct air capture process works:

CE started its pre-FEED (front-end engineering and design) with Pale Blue Dot Energy on the development of a DAC plant in Scotland, U.K.

This DAC company also recently started engineering an air-to-fuel plant that will be operational in Canada in 2026.

Global Thermostat:

This DAC company is founded in the United States in 2010 by two academics from Columbia University.

Same as Climeworks, Global Thermostat (GT) is also using its patented solid sorbent material that captures CO2. The image below demonstrates how GT direct air capture technology functions.

GT has so far commissioned two DAC pilot plants. It’s currently collaborating with ExxonMobil to advance and scale up its DAC technology.

It has also supplied its DAC equipment to the Haru Oni eFuels pilot plant in Chile. This DAC plant will use captured CO2 blended with hydrogen to produce synthetic gasoline.

The project will capture up to 250 kg of CO2 per hour, which is equal to around 2,000 tCO2/year.

It’s essential to note that DAC contributes to one of the very few solutions available to reduce emissions in the aviation sector. It remains one of the most challenging energy sectors to decarbonize. Using captured CO2 enables synthetic fuels (used by airlines) to be carbon neutral over their life cycle.

Other smaller direct air capture companies include:

Heirloom: proposes a hybrid DAC approach based on carbon mineralization

Hydrocell: captures CO2 and recovers heat from exhaust air

Infinitree: provides CO2 enrichment solutions for enclosed agricultural applications

Skytree: focuses on air quality management for electric vehicles

Soletair Power: combines ventilation with CO2 capture for buildings

Direct Air Capture’s Role in Meeting Net Zero Emissions

DAC plays an important role in meeting net zero emissions targets. And that’s by being a key CDR approach and a source of captured CO2 needed to produce carbon neutral products.

Net zero emissions mean reaching a point where CO2 emitted into the air by human activities is balanced by the amount of CO2 removed from the atmosphere.

There is a range of CDR approaches available for use today. These include nature-based solutions (reforestation/afforestation), enhanced natural processes, and technology-based approaches. DAC is a technology-based CDR approach that’s getting much attention and growing interest right now.

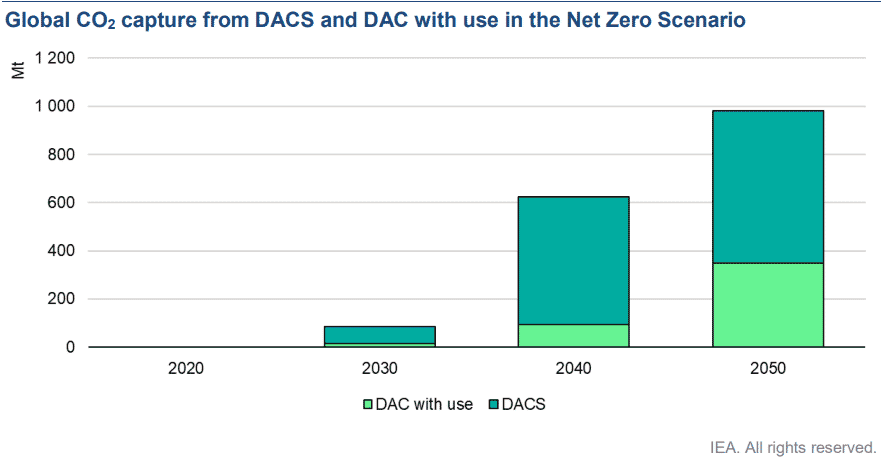

In fact, the world needs DAC to steer the global energy system to net zero emissions by 2050. The projections in the graph below show the potential of DAC in reaching net zero emissions by 2050.

Estimations by the International Energy Agency showed that DAC can capture over 85 million tons of CO2 in 2030 and 980 million in 2050. But that needs a lot of work to do to help scale up CDR and DAC technologies to unlock such potential.

The good news is that the global trend today indicates high regard for more investments in DAC both from the public and private sectors. And through emissions reduction strategies like DAC, businesses can meet or even exceed their net zero targets.

Investments in DAC Technology

Growing recognition of DAC technologies as a CDR approach to cut down emissions is translating to more policy support and investment.

Since the start of 2020, almost $4 billion in public funding has been invested for DAC research, development, and deployment (RD&D). Likewise, leading direct air capture companies have raised more than one billion investments for scaling up their CO2 capture technologies.

The private-sector support for and investment in DAC has also expanded in recent years. Major organizations like Breakthrough Energy Ventures, Prelude, and Lower Carbon Capital are investing in DAC companies.

Fortune 500 companies are also putting their money to help ramp up DAC technologies.

In April this year, five of the world’s biggest companies committed to invest $925 million in CDR technologies. Stripe, Alphabet, Shopify, Meta, and McKinsey provide the funding for it. Shopify is also supporting DAC through its Sustainability Fund.

So far, Climeworks raised $650 million in equity funding to scale up its DAC technology. It’s the biggest amount ever raised by a carbon removal company.

Further support for DAC comes from programs like the XPRIZE (offering up to $100 million for innovative carbon removal projects including DAC). Also, the Breakthrough Energy’s Catalyst Program raises money from various sources to invest in CDR technologies like DAC.

Investors have one common goal in putting their money into scaling up CDR and DAC approaches: to reduce or offset their emissions.

Most carbon offsets offer credits for claiming to prevent a new emission elsewhere. Carbon credits work like permits for entities or companies to emit CO2. One credit equals one ton of CO2 emission.

Along with the rising interest in DAC, investing through carbon credits is also getting traction right now. Countries and businesses are in an urgent state to cut down emissions as early as 2030 and as late as 2050.

Carbon credits are one of those market tools that help individuals and organizations alike to reduce their emissions. When combined with direct emission reductions, carbon credits generated by DAC programs can tackle organizations’ unavoidable emissions, making net zero achievable.

Together, they also offer a mechanism to address emissions from the past. Hence, they provide a chance to achieve not just net zero, but also eventually help reverse climate change effects.

You can learn more about how this scheme works through our several guides. It helps to start by knowing the difference between carbon offsets and carbon credits here.

You can also check out our in-depth articles on carbon credits and carbon offsets for a closer look at how they work in helping companies reach net zero carbon emissions.

DeepMarkit welcomes added validation of its business model as venture capital firms led a US$70 million investment in the recent funding raised by Flowcarbon.

Flowcarbon is a carbon credit start-up co-founded by former WeWork CEO Adam Neumann. It operates in the voluntary carbon market with Web3 which focuses on influencing the blockchain to scale climate change solutions.

The financing boosted the emerging industry that brings carbon credits on-chain, as well as DeepMarkit’s credibility planning to increase the transparency of the market.

The company has been pursuing the tokenization of carbon credits through its wholly-owned subsidiary, First Carbon Corp. with a primary asset MintCarbon.io platform.

Economies worldwide believe that voluntary carbon credit markets are one of the best solutions to cut emissions. Investors are also immensely interested in putting their money in the market, potentially adding to the industry growth.

With that, DeepMarkit focuses on decentralizing the fight against climate change and democratizing access to the voluntary carbon market by minting credits into NFTs.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy

")

")

")