As the new year ushered, Microsoft revealed its boldest plan of investing $80 billion in artificial intelligence. This funding will be used to develop cutting-edge data centers worldwide to power AI models and cloud-based applications. The company further revealed that more than 50% of this investment will take place in the United States. This huge decision bolsters its confidence in the American economy and dedication to technological leadership.

Brad Smith, Microsoft’s president and vice chairman, outlined this bold vision in the blog post noting,

“The country has a unique opportunity to pursue this vision and build on the foundational ideas set for AI policy during President Trump’s first term. Achieving this vision will require a partnership that unites leaders from government, the private sector, and the country’s educational and non-profit institutions. At Microsoft, we are excited to take part in this journey.”

This Year, Microsoft Takes the AI Lead

AI relies heavily on advanced computing power that requires specialized data centers equipped with thousands of interconnected chips. Microsoft’s substantial investment will enable the expansion of these facilities and expand AI innovation on a global scale. Smith highlighted that this effort would not only support AI model training but also drive the deployment of AI-enabled applications worldwide.

The initiative further strengthens Microsoft’s partnership with OpenAI. Since ChatGPT’s launch in 2022, the demand for AI integration has surged across industries and corporate sectors. These AI endeavors also got some fresh boost when Sam Altman recently penned down in his blog,

“We are now confident we know how to build AGI as we have traditionally understood it. We believe that, in 2025, we may see the first AI agents “join the workforce” and materially change the output of companies. We continue to believe that iteratively putting great tools in the hands of people leads to great, broadly-distributed outcomes.”

Now coming to AI’s impact in general, Smith added,

“Each of these eras was marked by what economists call a General-Purpose Technology, or GPT. In contrast to single-purpose products, GPTs boost innovation and productivity across the economy. Ironworking, electricity, machine tooling, computer chips, and software all rank among history’s most impactful GPTs.”

Thus, the $80 billion investment plan can in every way push the tech giant ahead in the AI race and challenge its competitors like Google, Meta, and xAI directly.

Education, Innovation, Collaboration: America’s AI Advantages

However, the efforts will not be confined solely to Microsoft. The tech giant is envisioning to work closely across the private sector, government, educational institutions, and non-profits to achieve these goals. The approach will be that – the private sector’s innovation, supported by government policies can drive AI advancements to the next level. Basic research at universities and funding for private enterprises will also be vital to this effort.

Moreover, America has a strong educational system that will spread AI skills across diverse sectors. Technology platforms and non-profits can also provide tools for individuals to integrate AI into their careers.

Smith also added more clarity to the company’s plans noting,

“Our success, however, depends on a broad and competitive technology ecosystem, much of which is based on open-source development. This includes our longstanding competitors, chip suppliers, applications companies, systems integrators, service providers, and the millions of software developers who use our products to create customized solutions working for our customers.”

Fortunately, the U.S. has several other advantages apart from its robust educational system. American companies lead in advanced technology- from chips and AI models to software applications. They are also building AI systems that prioritize trust, security, and responsible use.

Microsoft, for instance, designs AI that protects privacy, cybersecurity, and digital safety. These technologies are deployed globally through highly secure data centers that meet stringent U.S. standards.

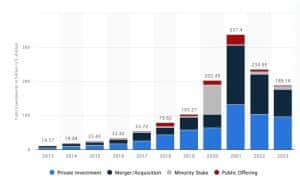

Global corporate investment in artificial intelligence (AI) worldwide from 2013 to 2023, by investment activity (in billion U.S. dollars) Source: Statista

Source: Statista

Promoting Domestic AI Exports: A Key Priority for 2025

One of the top priorities for 2025 and the key motive behind this massive investment is promoting American AI exports. The post highlighted President Trump’s executive order in 2019 stressing the need to open global markets for American AI while safeguarding critical technologies from competitors.

Since then, generative AI has spread its wings. Yet again the rapid growth of China’s AI industry has intensified competition as both nations vie to be international leaders. The blog post revealed another scenario of Chinese dominance exemplifying the telecom industry.

Lessons from the Telecom Industry

The past two decades of telecommunications exports provide valuable insights. Initially, companies like Lucent, Alcatel, Ericsson, and Nokia set standards for innovative products. However, Huawei, backed by subsidies from the Chinese government, quickly gained ground.

By offering affordable products to developing countries, Huawei’s technology became the backbone of many nations’ telecom networks. This dominance later raised concerns about cybersecurity, which became a major issue for the U.S. in 2020.

Today, China appears to be replicating this strategy with AI. The Chinese government is offering subsidized access to scarce chips and building local AI data centers in developing nations. Their goal is clear: countries that adopt China’s AI platforms early will likely remain reliant on them not just now but also in the future.

A Winning Strategy for the U.S.

While the U.S. government has concentrated on securing sensitive AI components through export controls, a bigger challenge lies ahead. The real competition will be about which country can spread its AI technology globally the fastest. And Smith believes America can inevitably win this race by developing a smart, international strategy to promote its AI solutions worldwide.

Elaborating further, the U.S. will need to swiftly position American AI as the preferred choice. This will require collaboration with allies and a unified effort to promote U.S. technology globally. In this perspective, the U.S. is supported by growing international regulatory cooperation among North America, Europe, and the Asia-Pacific. Thus, by continuing to lead initiatives like G7 AI diplomacy, the U.S. can showcase its AI leadership globally.

Additionally, Google, Amazon, and many more private companies are also investing heavily to power up America’s AI, computing, and data center space. This commitment and sincere efforts are also fuelling America’s dream to win the AI race.

Microsoft’s Investment Plans Fuel America’s AI Future

On an optimistic note, Smith once again voiced himself confidently that the United States is well-positioned to outpace China in the global AI competition. Well, American products are more trusted than Chinese counterparts, globally. Moreover, exceptional private-sector investment and balanced export control policies further give the U.S. an international edge.

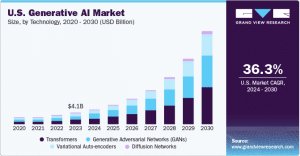

According to Grand View Research Market Insights,

- The U.S. generative AI market size was estimated at USD 4.06 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 36.3% from 2024 to 2030.

Microsoft’s investments in the past and plans for the future are the right kind of testament to American optimism for the AI race. Last year, the company announced plans to invest over $35 billion in 14 countries within three years to build secure and reliable AI and cloud data center infrastructure. This plan will broadly span across 40 countries, including some regions of the Global South, where China has heavily invested.

Secondly, Microsoft is partnering with the UAE’s sovereign AI company, G42, to develop AI infrastructure in Kenya. Additionally, the company is teaming up with BlackRock and MGX to create a global investment fund to raise a whopping $100 billion. This fund will support AI infrastructure projects to boost the global AI supply chain.

In conclusion, we can envision that Microsoft’s $80 billion investment is a huge leap for the U.S. AI industry. By focusing on infrastructure, workforce empowerment, and global partnerships, the company is helping the nation stay at the forefront of AI technology.

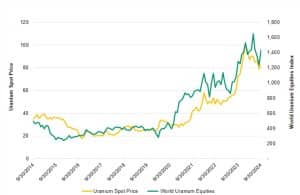

Source: Sprott (Bloomberg and TradeTech LLC. Data from 9/30/2014 to 9/30/2024)

Source: Sprott (Bloomberg and TradeTech LLC. Data from 9/30/2014 to 9/30/2024)

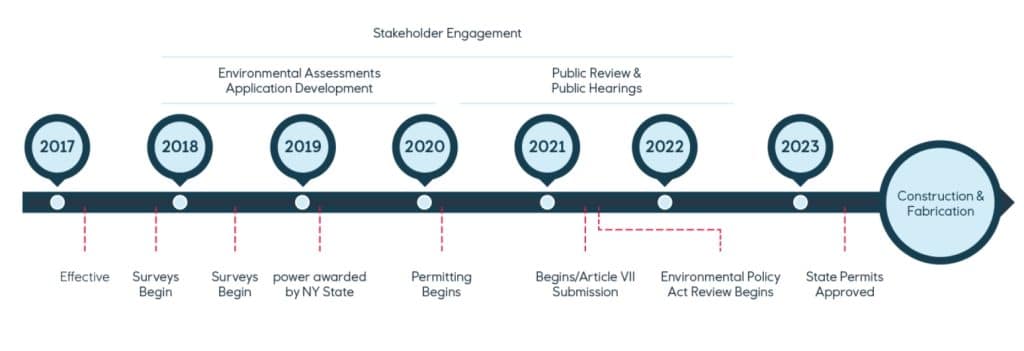

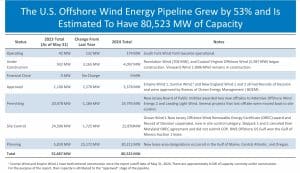

Source: National Renewable Energy Laboratory Offshore Wind Market Report

Source: National Renewable Energy Laboratory Offshore Wind Market Report

Source: LanzaTech

Source: LanzaTech Source: Technip Energies

Source: Technip Energies