According to a recent report by Abatable, a market intelligence and carbon procurement platform, the voluntary carbon market (VCM) stands at a pivotal moment with flourishing activity in the primary market and notable expansion in issuance and projects among the top 25 developers. The market underwent a period of significant change in 2023, marking a transition towards a new era of growth and investment.

Abatable’s VCM Developer Overview

Abatable’s Voluntary Carbon Market Developer Overview | 2023-2024 report highlights the developers that have leveraged the capital influx of 2024 to expand their portfolios.

The report draws on aggregated data from over 3,000 project developers contributing to the major carbon credit registries. These include Verra’s Verified Carbon Standard (VCS), Gold Standard (GS), Climate Action Reserve (CAR), and American Carbon Registry (ACR).

The report further identifies key market themes to monitor in 2024 and clarifies supply- and demand-side trends. It highlights several crucial factors shaping the market:

- Divergence among developers regarding quality standards,

- Merging of carbon and biodiversity efforts, and

- Heightened collaboration on corresponding adjustments.

These dynamics are poised to exert a substantial influence on the market throughout the year.

Moreover, following the highly anticipated release of the Core Carbon Principles (CCPs) by the Integrity Council for the Voluntary Carbon Market (ICVCM) last year, the report provides the inaugural comprehensive evaluation of potential alignment with this groundbreaking quality standard.

For the first time, it reports on the percentage of issuances by developers currently undergoing ICVCM review for CCP approval.

Commenting on the findings, Maria Eugenia Filmanovic, Co-Founder of Abatable said,

“While we have seen significant growth and interest in carbon credit initiatives and early indications show a move towards greater market integrity, challenges remain as we navigate the implications of the forthcoming Core Carbon Principles. It is essential for stakeholders to stay informed and proactive in addressing these challenges to ensure the continued effectiveness of the VCM.”

Supply, Demand, & Surplus: Analyzing Key Metrics Shaping the VCM

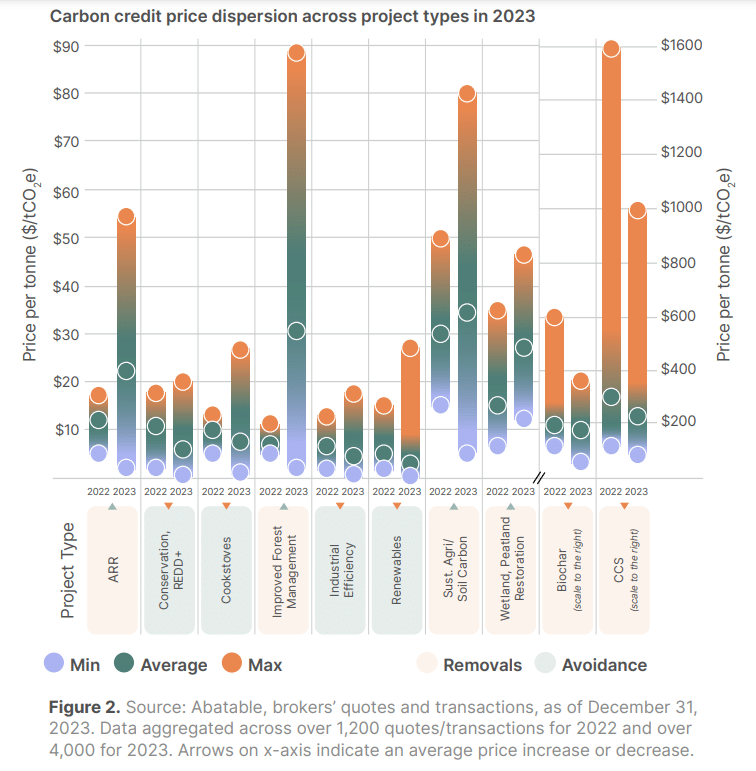

According to the report, the rise in market surplus resulted in price softening and increased price variability, especially among avoidance credits. Conversely, nature-based removal credits experienced a price increase due to limited supply and robust demand.

Despite ongoing challenges in the REDD+ (Reducing Emissions from Deforestation and Forest Degradation) market, the study highlights the continued dominance of REDD+ in the nature-based VCM sector. Seven of the top 10 largest nature-based VCM project developers are actively involved in REDD+ projects.

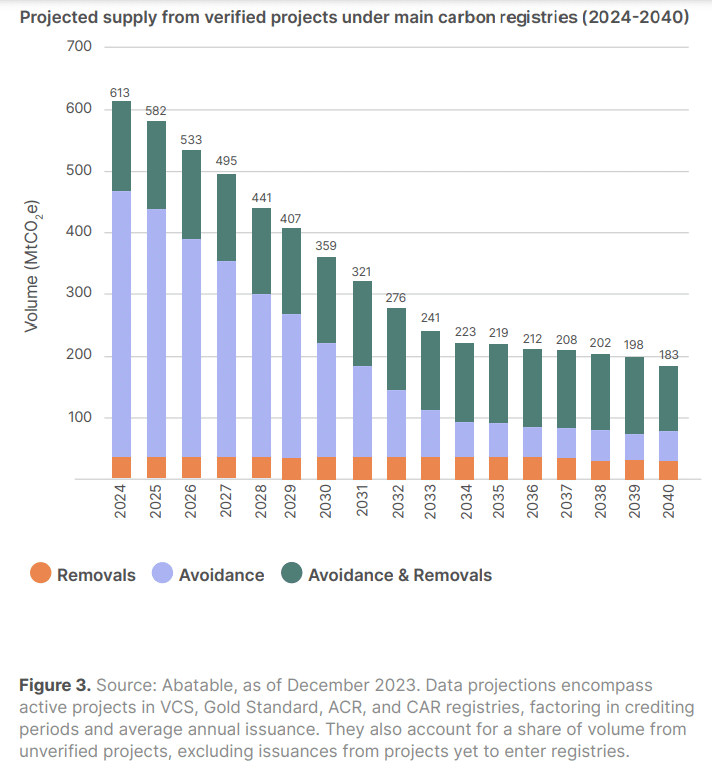

The market would face growing oversupply in the coming years, the report noted. This trend is due to the substantial projected supply from verified projects or those in the verification pipeline. This is also likely to continue to exert downward pressure on prices unless there’s a significant surge in demand.

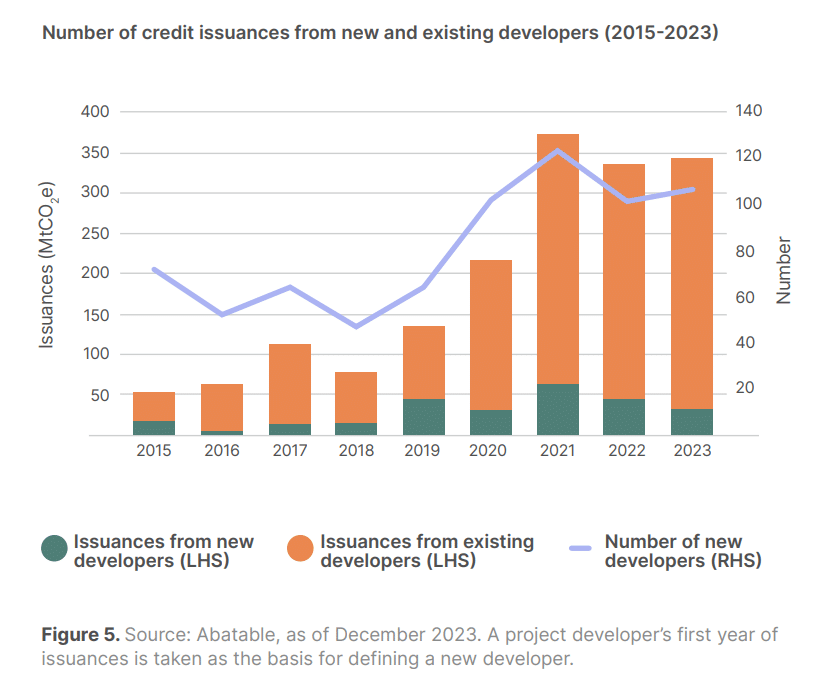

On the supply side, there was a noticeable decrease in the proportion of credits issued by the top 10 developers in terms of issuances, reflecting the entry of new, smaller players into the market.

Additionally, for the 4th consecutive year, over 100 new project developers started issuing credits in 2023. This market development bolsters the existing supply with fresh vintages, as seen below.

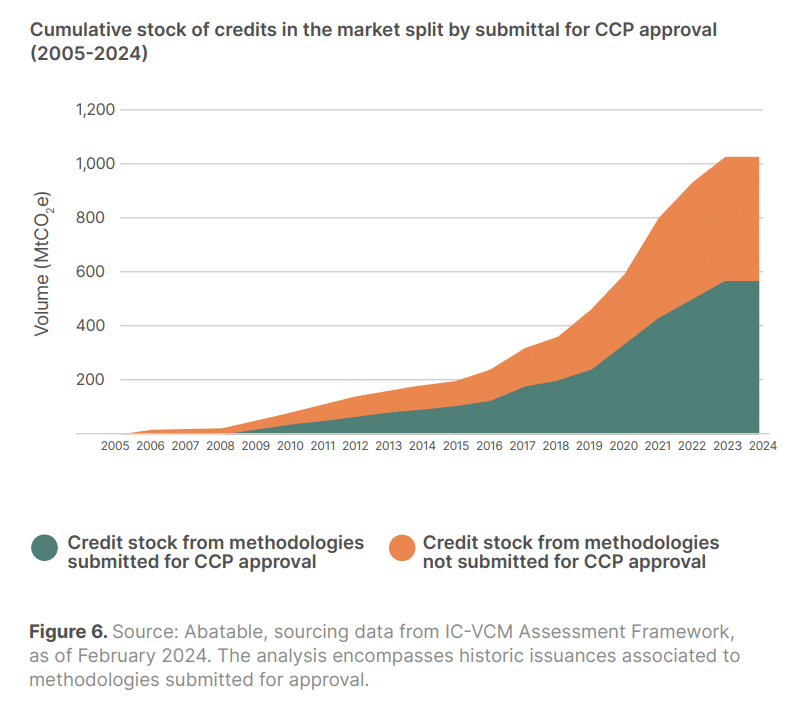

There exists a notable opportunity for developers to pivot towards methodologies undergoing approval under the CCPs. Currently, a significant portion of the market comprises credits that are not eligible under CCP criteria.

About 54% of the market’s surplus credits were issued using methodologies currently under CCP review. However, not all of these methodologies are expected to be approved, which will increase the stock of credits that do not meet the market’s new quality baseline.

Buyer Trends and Market Concentration

The Abatable report also spotlights major trends on the buyer side.

In 2023, a record number of unique buyers entered the market and retired credits for the first time. Meanwhile, newcomers are starting cautiously by retiring smaller batches of credits. This influx of new participants reflects a growing interest and engagement in the carbon credit market.

More notably, increased scrutiny of the market in 2023 prompted more buyers to disclose their credit purchasing activities. This resulted in a reduction in the share of non-disclosing parties, from 56% in 2020 down to 44% in 2023.

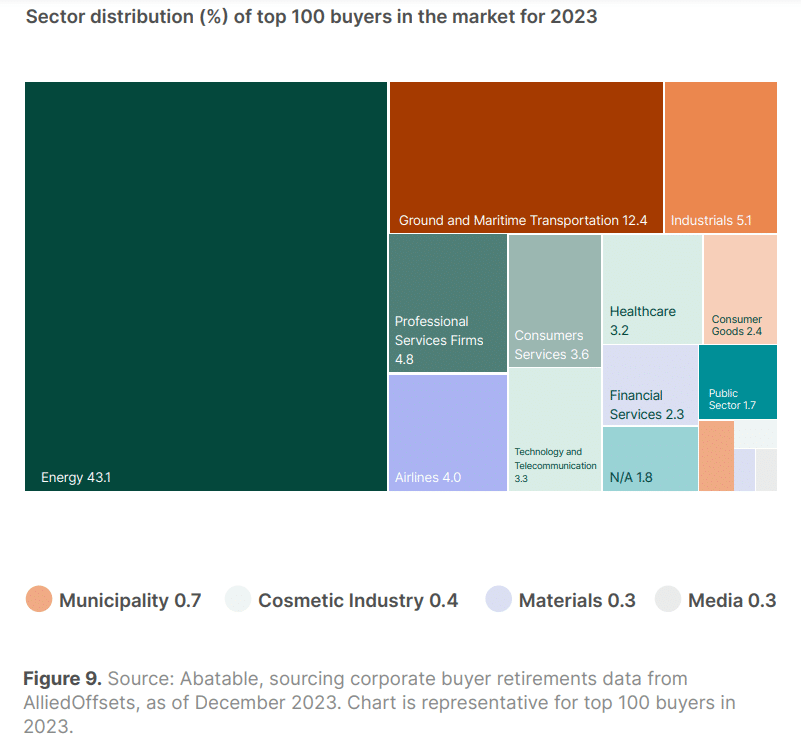

However, the market remains largely concentrated among the top 100 buyers. These top carbon credit buyers in 2023 were primarily (60%) from emission-intensive sectors such as energy, surface transport, and aviation. These companies prioritize the mitigation of their existing and future carbon liabilities, driving their active involvement in the market.

As the voluntary carbon market continues to evolve, stakeholders must remain vigilant in addressing challenges while capitalizing on emerging opportunities. With increased scrutiny and growing interest from diverse sectors, the path towards greater market integrity and sustainability is paved with informed decision-making and proactive engagement.

As the voluntary carbon market continues to evolve, stakeholders must remain vigilant in addressing challenges while capitalizing on emerging opportunities. With increased scrutiny and growing interest from diverse sectors, the path towards greater market integrity and sustainability is paved with informed decision-making and proactive engagement.

")

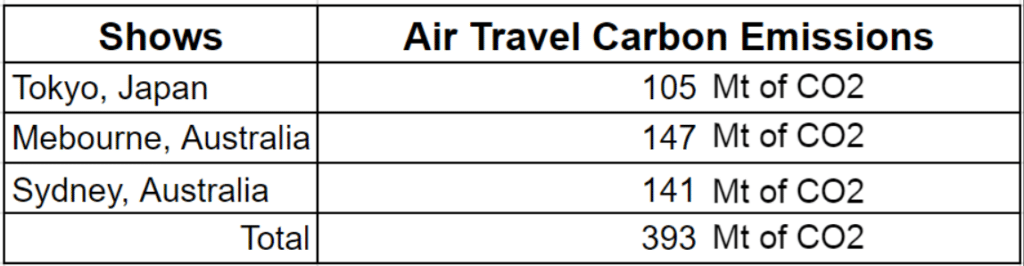

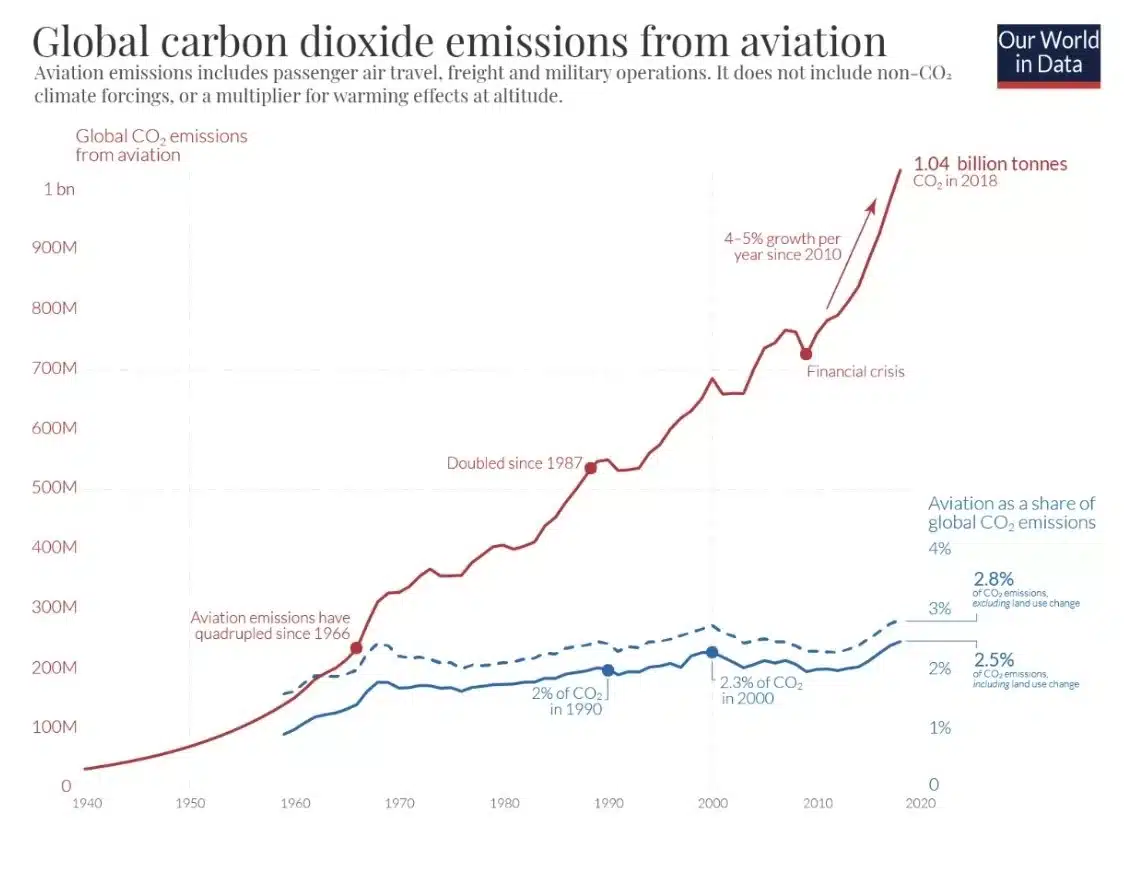

Carbon emissions data for specific flights can vary depending on factors such as route efficiency and passenger load. However, using figures based on estimated emissions data will provide a general idea of the CO2 footprint associated with Swift’s air travel between those cities.

Carbon emissions data for specific flights can vary depending on factors such as route efficiency and passenger load. However, using figures based on estimated emissions data will provide a general idea of the CO2 footprint associated with Swift’s air travel between those cities.