Deputy Prime Minister and Finance Minister Chrystia Freeland announced that the Canada Carbon Rebate for small businesses will not be taxed.

Freeland clarified this in a statement on X, following concerns from the Canadian Federation of Independent Business (CFIB) that the rebate would be considered a taxable benefit.

Freeland’s post reaffirmed the government’s commitment to providing financial relief for small businesses without adding tax burdens.

The CFIB posted on X that the government will tax the long-awaited $2.5 billion carbon tax rebate for small businesses when it’s issued in December.

CFIB President Dan Kelly criticized the move, comparing it to taxing a tax refund. He stated that this undermines claims of the carbon tax being revenue-neutral, as the government will collect significant corporate tax revenue from the rebate.

The Canada Revenue Agency initially assured CFIB that the rebate would be tax-free, similar to the Canada Carbon Rebate for individuals.

However, the Department of Finance later declared the small business rebate as taxable, considering it “government assistance.” Kelly argued that calling the rebate government assistance is absurd since it merely returns a portion of the taxes small businesses have paid.

CFIB’s Campaign Pays Off

The carbon tax system has long been criticized for its unfairness to small businesses. After initially promising 10% of total carbon tax revenue as rebates in 2019, the government delayed issuing the funds for five years.

The rebate only materialized after persistent lobbying by CFIB and widespread support from business owners, opposition leaders, and provincial premiers.

Adding to the frustration, the carbon tax will increase again on April 1, 2025. Meanwhile, future rebates for small businesses will be slashed from 9% to 5% of total revenue.

In response, CFIB has sent an open letter to Finance Minister Chrystia Freeland, urging the government to reverse course. Kelly noted that:

“It’s clear why 83% of small business owners now oppose the carbon tax. Delaying, taxing, and reducing promised rebates make it evident that the carbon tax should be scrapped entirely.”

Business owners can estimate their rebates and sign CFIB’s petition to abolish the tax using the CFIB’s online calculator.

The Carbon Tax Controversy Continues

The Canada Carbon Rebate (CCR), formerly the Climate Action Incentive Payment (CAIP), is a tax-free payment that helps individuals and families offset the federal carbon price. It includes a base amount, with an extra supplement for those in small or rural communities.

The rebate amount varies by province and is calculated annually based on projected carbon pricing revenue in each province.

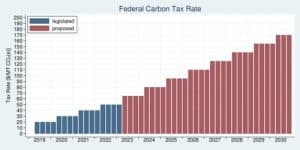

The federal carbon price currently increases gasoline costs by about 17.6 cents per liter, but quarterly rebates help Canadians manage these expenses. The chart below outlines the government’s planned annual carbon price hikes, implemented every April 1st.

Canada’s carbon price is currently set at C$65 per tonne and will rise to C$80 per tonne on April 1. After that, it will increase by C$15 annually, reaching C$170 per tonne by 2030. These incremental hikes aim to reduce emissions while generating revenue to support climate initiatives.

The tax-free Canada Carbon Rebate offers some relief for small businesses facing rising carbon costs. However, with future rebates set to decline and carbon taxes increasing, the debate over the system’s fairness and effectiveness remains heated.

GenZero, a decarbonization-focused investment platform owned by Temasek, and global commodities trader Trafigura have committed over $100 million to Brújula Verde, Colombia’s largest nature-based carbon removal project. Located in the Orinoco River Basin, this project aims to restore land degraded by agriculture and wildfires while generating high-integrity carbon removal credits.

Bringing Degraded Lands Back to Life

The planet is losing about 10 million hectares of forest worldwide every single year. The primary reason is to clear land for agriculture and materials like paper. This deforestation, largely concentrated in tropical forests (96%), contributes to 16% of total tree cover loss.

Notably, deforestation releases nearly 5 billion tons of carbon dioxide annually, accounting for about 10% of global human-made emissions. This is why most nature-based projects are focusing on restoring degraded forests.

Source: World Resources Institute

In Colombia, 79,256 hectares were deforested in 2023. The South American nation is covered by over 60 million hectares of forests, with 405,000 hectares of planted forests.

The Brújula Verde project focuses on afforestation and reforestation across 30,000 hectares of degraded land, particularly areas previously used for cattle grazing. The initiative will plant 24 million mixed-species trees, with no plans for commercial harvesting.

By restoring the land, the project could sequester over 20 million tonnes of carbon throughout its lifetime.

The project uses advanced technologies such as high-resolution sensors for accurate carbon monitoring and eDNA sampling to track biodiversity. It also assesses the health of local ecosystems, including their biodiversity, water systems, and social impacts.

Expanding the Project’s Scope

Trafigura initially invested in Brújula Verde in 2023, funding the first phase, which reforested 10,000 hectares. This latest investment, supported by GenZero, will double the project’s size and help it issue its first carbon credits by 2025.

Matthew Nelson, Head of Carbon Investments at Trafigura, highlighted the project’s potential to attract institutional investors and deliver environmental and social benefits. He stated that:

“GenZero’s partnership will enhance the scope and impact of Brújula Verde, bringing local employment alongside environmental and biodiversity benefits to the region, whilst producing high integrity nature-based carbon removal credits.”

Trafigura is a leading global commodity trading firm, specializing in the trading of oil, refined products, metals, and minerals. The company plays a vital role in connecting producers with consumers through efficient supply chains. In 2023, Trafigura reported revenues exceeding $315 billion, underscoring its significance in global markets.

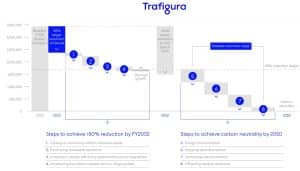

The global commodity trading giant is actively pursuing ambitious carbon reduction initiatives, aiming to align with global net-zero targets. It targets a 50% reduction in Scope 1 and 2 emissions by 2032 and operational carbon neutrality by 2050.

Trafigura Net Zero Pathway. Source: Trafigura website

The company’s emissions reduction strategy also includes reducing its Scope 3 emissions intensity. These targets are complemented by investments in renewable energy projects, such as solar and wind. The company also invests in the development of low-carbon fuels, including green hydrogen and ammonia.

In 2023, Trafigura launched a $2 billion fund to support its energy transition projects. The company is also advancing its emissions trading activities, helping clients offset their carbon footprints by sourcing high-quality carbon credits. Trafigura’s climate action plan underscores its commitment to decarbonizing its supply chain and supporting global sustainability goals.

The $100 million investment in Colombia’s Brújula Verde project for nature-based carbon removals is the company’s most recent initiative.

Building High-Quality Carbon Markets

The project aims to contribute to the development of robust carbon markets by delivering high-quality, verifiable carbon removal credits. According to Hoon Ling Min, Director of Investments at GenZero, the project’s focus on soil restoration and native species reintegration ensures the production of top-tier carbon credits. He further noted that:

“The Brújula Verde project marks an important effort in restoring one of Colombia’s most biologically diverse areas. It is a unique project which adopts a restoration bridge concept by reconditioning soil health through reforestation, which enables the reintegration of native species gradually.”

GenZero, a wholly-owned subsidiary of Temasek, is committed to accelerating global decarbonization. The platform invests across three key areas:

technology-based solutions,

nature-based projects, and

carbon ecosystem enablers.

GenZero has already deployed capital in impactful initiatives, including investments in Carbon Capture, Utilization, and Storage (CCUS) and nature-based solutions like sustainable forestry.

The company’s key achievements include reducing carbon emissions through clean cookstove projects in Southeast Asia and supporting the New Forests Tropical Asia Forest Fund 2. Together, these efforts contribute to advancing decarbonization by 2030, aligning with global net-zero goals.

The Brújula Verde project represents a significant step toward addressing climate change by restoring ecosystems and generating carbon credits. With GenZero and Trafigura’s combined investment, the project will deliver environmental, social, and economic benefits to the Orinoco River Basin while advancing the global carbon market.

Disseminated on behalf of Alaska Energy Metals Corporation (AEMC)

As reported by Bloomberg, Russia’s largest mining company, Nornickel is negotiating to establish a major copper smelting facility in Fangchenggang, a port city in China’s Guangxi region. The proposed plant will use raw copper concentrate transported from Russia and will have the capacity to refine up to 500,000 tons of copper annually. This project aims to bring the final processing a step closer to China’s vast metal market.

Nornickel’s Push for Joint Ventures in China Amid Western Sanctions

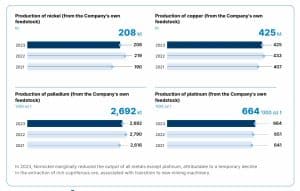

Nornickel is Russia’s leading metals and mining company and the world’s largest high-grade nickel and palladium producer. President, Vladimir Potanin said that the company has been exploring options in copper for joint projects in China since earlier this year.

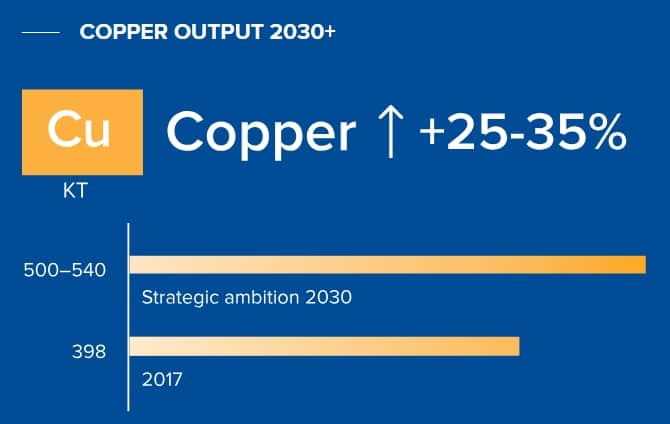

Strategic ambitions for 2030+ metal production

Source: Nornickel

Lately,Western sanctions on Russian commodities have made global trade more difficult. These restrictions limit where and how Russian goods, like metals (aluminum, copper, and nickel) and energy resources, can be sold. As a result, Nornickel has been seeking joint ventures in China since earlier this yeareven though it is not directly sanctioned by the West.

The mining giant has not disclosed the name of the Chinese partner they are in talks with but they hint at constructing a greenfield plant at the mentioned location.

The smelter project represents a strategic shift for Nornickel, which previously explored partnerships with established Chinese smelters to process Russian concentrate. However, those plans were abandoned in favor of a new, purpose-built facility.

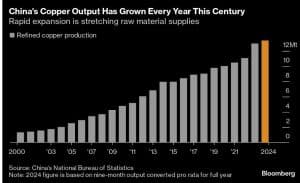

China’s Copper Dominance: Too Much of a Good Thing?

Demand for copper is going high due to renewables, electric vehicles, and grid infrastructure. According to Bloomberg, China’s refined copper output rose by over 5% in 2024 despite certain production curbs. Furthermore, in recent years, the country has rapidly constructed smelters which has led to an increase in its global share for copper.

This burst in capacity is certainly not favorable for the Chinese copper market. Rather it has put tremendous pressure on domestic smelters to slow expansion. This is the outcome of the fierce competition and limited raw materials which have shrunk the profits of the copper industry.

Source: Bloomberg

Grant Sporre, head of metals and mining research at Bloomberg Intelligence had cautioned that China’s excesses threaten the future of copper refining beyond its borders and operations from Chile to Europe and India could be at risk.

The above analysis is based on the fact that ore supply has intensified as new smelters open in India and Indonesia. India is rapidly building plants to cut down on copper imports and strengthen domestic production. Meanwhile, Indonesia has taken steps to keep its ore resources within the country by curbing exports on which many smelters in Asia rely. This shift forces copper smelters in Asia to secure new sources or risk production slowdowns, further straining the already tight market.

However, interestingly some analysts suggested that state-owned Chinese smelters may handle the market downturn better than global competitors. This is simply because of the cost advantages and more modern facilities the country is equipped with.

Is Nornickel’s Entry A Threat to China’s Copper Giants?

Fangchenggang, where the plant would be built, already has a large smelter with a 600,000-ton capacity and is operated by China’s state-owned Jinchuan Group. On top, this project comes at a time when the country is dealing with an oversupply of copper refining capacity.

As a consequence, Nornickel’s project has met substantial resistance from Chinese copper producers, who feel the extra capacity could harm their domestic output.

China’s refined copper imports from Russia have declined by over one-third year-on-year, totaling about 165,000 tons in the first nine months of 2024. The new smelter, if finalized, would help stabilize the flow of Russian copper into China and offer Nornickel an opportunity to circumvent Western trade restrictions while accessing the world’s largest copper market.

Operational performance

Source: Nornickel Sustainability Report

Thus, it’s too early to comment on whether Nornickel’s entry will be a boon or a bane for China’s copper market. The study is speculative and the picture will be clear eventually as the mining company reveals more details of their expansion plans.

Expanding on Critical Resources: Alaska’s Role in U.S. Energy Independence

The challenges Nornickel faces in China underscore the broader global race to secure critical mineral resources, especially as countries like the U.S. strive for energy independence. Alaska, a state rich in mineral deposits, is at the center of efforts to boost domestic production of essential metals. Canadian mining company Alaska Energy Metals Corporation (AEMC) is one such player making strides by exploring Alaska’s underground deposits of nickel, a metal critical for energy transition technologies, particularly electric vehicle batteries.

AEMC President Greg Beischer has highlighted the importance of building a sustainable, domestic supply chain for nickel and other key minerals. With AEMC’s flagship project, the 23,000-acre Nikolai deposit, the company aims to help reduce the U.S.’s reliance on imports and support a shift towards a low-carbon economy. The Nikolai deposit holds substantial nickel reserves and also contains copper, cobalt, platinum, and palladium—metals deemed critical by the U.S. Department of Energy.

AEMC’s activities in Alaska mirror Nornickel’s efforts in Fangchenggang. Both companies recognize the growing need to secure a stable supply of strategic minerals, given geopolitical pressures and the global focus on energy security. For AEMC, overcoming challenges posed by fluctuating nickel prices and securing project funding are priorities to advance the Nikolai project, which they aim to assess economically by 2025. This project also aligns with U.S. initiatives to establish local sources for critical minerals, a strategy that could mitigate reliance on overseas production.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: AEMC.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

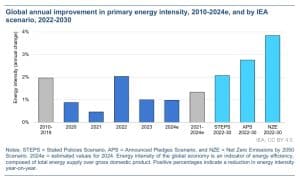

IEA defines energy intensity as the amount of primary energy used to produce a given amount of economic output. It is the key global indicator to track energy efficiency- which is technically the rate of change in primary energy intensity.

At COP28, at least 200 countries pledged to double energy efficiency improvements by 2030. This is because this factor drives the world’s climate goals. Recently, IEA has rolled out its 2024 Energy Efficiency Report which has decoded the significance of energy efficiency with rising energy demands.

Let’s deep dive into this…

Energy Demand Surges with Electrification

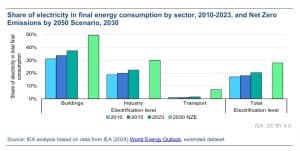

A transition to electrification has gained ample significance with electricity’s share in total energy demand rising faster than in previous years. Electrification means shifting from fossil-fuel-powered systems to efficient electric alternatives. And this stands out as a positive force in an otherwise slow year for global energy efficiency.

The demand is further spurred by increased EV sales, industrial growth, and cooling needs, particularly in warmer regions. On the contrary, the demand for gasoline is slowing down in many regions due to the same reasons.

In 2024, the share of electricity in overall energy demand is expected to grow by nearly 2%, double the 1% average growth seen from 2010 to 2019.

Talking about EVs, the market continues to expand. IEA predicts, in 2024 EV sales can reach 17 million if one in five cars is sold worldwide. China remains a dominant player, accounting for about 60% of global EV sales last year. Overall, the EV boom is an example of electrification’s role in improving energy intensity even if overall efficiency progress remains modest.

However, reaching the net zero target by 2050 will require faster and sustained progress.

The Missing Piece in Achieving Net Zero Emissions

Energy efficiency is essential for reducing fossil fuel reliance and cutting emissions. In the IEA’s net zero pathway, ramping up energy efficiency could account for over 70% of the anticipated drop in oil demand and 50% of the reduction in gas demand by 2030. Thus, this energy efficiency is like the missing block that needs to be placed to bridge the net zero pathway.

However, the global efforts to reduce energy intensity are yet to reach targeted levels. In 2024, global energy efficiency progress is projected to improve by just 1%, the same rate as 2023, despite energy demand expected to rise by 2%.

Despite the historic pledge, a significant increase in policy action is necessary to accelerate the process of energy efficiency.

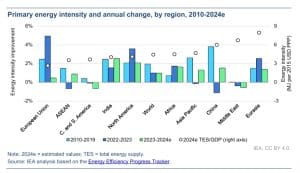

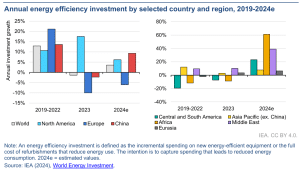

Energy Efficiency: Advanced Economies Slow in, Emerging Markets Pick Up

Last year advanced economies like the European Union and the United States showed strong improvements in energy intensity. In contrast, China, a long-time leader in energy efficiency gains, saw its energy intensity sharply decline from its decade-long average of 3.8% annual improvements. India’s progress also slowed, posting just 1.5% improvement.

However, in 2024, the momentum has shifted. Advanced economies are seeing slower energy efficiency progress, with the EU expected to improve by only 0.5% and the U.S. by 2.5%.

Meanwhile, emerging markets and developing economies (EMDEs) are starting to pick up the pace. China’s energy intensity is projected to improve by 1.5%, bouncing back from 2023’s decline, while India’s progress has accelerated to around 2.5%. Similar gains are anticipated in Southeast Asia, where energy efficiency initiatives are gaining traction.

As energy demand rises, maintaining efficiency improvements is becoming more challenging. Advanced economies are slowing, while EMDEs are showing modest progress. This shift highlights the need for tailored policies to drive efficiency across diverse regions and economic stages, especially when the world has already set an ambitious energy target.

Flexibility: Eases Grid Strain and Boosts Affordability

Another system-wide theme highlighted by IEA is flexibility across the grid. As renewable energy grows globally, the need for flexibility to balance grids is rising. Traditionally, grids relied on thermal and hydropower for flexibility. But now, demand-side management—such as smart appliances and battery storage, is emerging to provide this flexibility.

Following record growth in renewables in 2023, when nearly 565 GW was added, scaling up flexible, efficient solutions is crucial to manage demand and stabilize prices.

Government Strategies

Governments worldwide are responding. For example, the UK plans to release its Flexibility Markets Strategy by the end of 2024. It will focus on building a flexible market that contracted 4 GW last year. Australia’s New South Wales initiative is adding 1 GW of grid stability projects, and the Netherlands is committing $108 million to support battery storage integration.

Consumer Level Shift

The shift is not just confined to government policies but is also happening at the consumer level. In the UK, the Demand Flexibility Service trial involved 2.6 million households and 8,000 businesses, shifting demand and saving over 3.7 GWh during winter 2023-2024.

In the US and California, several federal initiatives are directed at improving grid flexibility and the growth of EVs. They are looking ahead to achieve this with support for smart heat pumps, dynamic-rate pilot programs, and funding for community-based grid innovation.

Digitization

Digitization plays a vital role in unlocking flexibility. New data-sharing platforms and dynamic tariffs, like Octopus Energy’s real-time rate and EDF’s EV charging scheme, incentivize users to adapt their energy consumption to grid needs. This will ease pressure on the grid and improve affordability. These efforts also highlight the growing integration of renewables, flexibility, and consumer-driven innovations.

In conclusion, IEA predicts that accelerating energy efficiency could cut over a third of global CO2 emissions by 2030, helping achieve net zero by 2050. However, as said before this calls for faster electrification, improvement in technical efficiency, and setting up robust policies.

COP29, held in Baku, Azerbaijan, made a major breakthrough in global climate action during its opening day. Nearly 200 governments agreed on a framework under Article 6.4 of the Paris Agreement. This deal sets up a UN-led global carbon market, allowing countries and companies to trade carbon credits more efficiently. The goal is to create a stronger demand for carbon credits, especially to fund climate projects in developing nations.

COP29 President Mukhtar Babayev called the agreement a “game-changing tool” to support climate action in less wealthy countries. He also urged all nations to continue working together to make more progress during the summit, noting that:

“By matching buyers and sellers efficiently, such markets could reduce the cost of implementing NDCs [Nationally Determined Contributions] by 250 billion dollars a year.”

A New Era for Carbon Trading

Article 6 of the Paris Agreement outlines how countries can work together to reduce greenhouse gas emissions. Article 6.4 introduces a global carbon trading system, managed by a UN body. This system will let countries and companies trade emissions reduction credits generated from projects worldwide.

The new system replaces the older Clean Development Mechanism (CDM) from the Kyoto Protocol. It aims to be more transparent and effective, ensuring that carbon credits are credible and valuable.

In October 2024, Article 6.4 Supervisory Body finalized rules for how projects will work under this system. These include standards for carbon removal projects and emissions reduction methods. The system will let companies in one country earn credits for reducing emissions and sell them to companies in another country, fostering global cooperation.

Challenges and Pushback

Despite the breakthrough, reaching an agreement wasn’t easy. Some countries and groups raised concerns about how decisions were made. The Coalition for Rainforest Nations (CfRN), representing several developing countries, argued that Article 6.4 Supervisory Body bypassed proper procedures.

Kevin Conrad, CfRN’s Executive Director, said the body adopted rules without first getting approval from the Conference of the Parties (CMA), which oversees the Paris Agreement. As a compromise, the final text used softer language, like “take note,” to acknowledge the rules without fully endorsing them. This wording sends a message that future decisions must follow proper processes.

Despite these issues, Babayev assured participants that more discussions on Article 6.4 would continue. Negotiations will also focus on Article 6.2, which deals with how countries trade carbon credits directly.

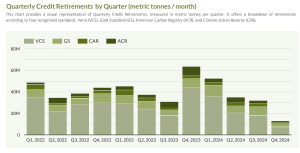

The new global carbon market aims to solve problems that have plagued carbon trading in the past. Older systems often faced criticism for lacking transparency and effectiveness, which led to low demand and falling prices for carbon credits.

The chart below shows the quarterly credit retirements, which represent demand, falling and are lower this year than prior years.

Chart from Viridios AI report

With clear rules and a centralized structure, Article 6.4 hopes to restore confidence in carbon markets. Sebastien Cross, Chief Innovation Officer at BeZero Carbon, called the agreement a major win for COP29. “This framework provides the tools we need to make carbon markets work better,” he said.

The carbon finance sector is optimistic that this move will help revitalize trading.

The agreement also benefits project developers by giving them clear guidelines to follow. Countries can align their climate policies with international standards, making it easier to meet their emission reduction goals.

Economic and Environmental Benefits

A global carbon market could bring significant economic and environmental gains. For one, it will provide new funding opportunities for climate projects, especially in developing countries that need financial support.

By creating a market-driven system, Article 6.4 encourages businesses to reduce emissions in cost-effective ways. Companies that reduce more emissions than required can sell their extra credits for profit. Meanwhile, those struggling to meet their targets can buy carbon credits to make up the difference.

This system not only helps cut global emissions but also supports sustainable development in poorer regions. It also allows countries struggling to meet their target by purchasing carbon credits.

What’s Next?

The Article 6.4 framework is just the beginning. The next steps include registering project methodologies and establishing operational guidelines, expected to be in place by mid-2025. During this period, the Supervisory Body will focus on finalizing details to ensure the system operates smoothly.

However, significant work remains to address concerns about market integrity and inclusivity. Some stakeholders worry that a centralized system could disadvantage smaller or less-developed markets. Policymakers must ensure the system is fair and accessible to all participants.

While there are still challenges ahead, this agreement sets the stage for stronger international cooperation. By establishing a UN-backed carbon market, the deal promises to boost demand for carbon credits and direct funding to critical climate projects.

As COP29 continues, leaders will work to refine this system and tackle other important climate issues.

Oklo, the California-based nuclear technology company recently announced that it has received clearance from the U.S. Department of Energy (DOE) and Idaho National Laboratory (INL) to proceed with site characterization for its first commercial fission power plant in Idaho.

The completion of the environmental compliance process is a significant milestone for Oklo as it can now initiate work for its fission power plant.

Jacob DeWitte, CEO and Co-Founder of Oklo noted,

“These approvals represent pivotal steps forward as we advance toward deploying the first commercial advanced fission plant. With this process complete, we can begin site characterization. Our unique business model of selling power directly to customers rather than power plants, combined with our early mover advantage, positions us to respond to a growing order book effectively and meet diverse energy needs across data centers, industrial processes, defense, and off-grid communities.”

Oklo Signed MOA with DOE for its Advanced Fission Power Plant

Oklo is dedicated to delivering clean, reliable, and affordable energy at a large scale. The company secured a site use permit in September through a Memorandum of Agreement with the DOE. This paved the way for its first commercial advanced fission power plant in Idaho, U.S. Interestingly, it’s the only advanced commercial fission company in the U.S. with a DOE site use permit.

The MOA will enable Oklo to conduct key site evaluations, including geotechnical studies, environmental surveys, and infrastructure planning. Additionally, it will also help maintain a schedule, manage costs, and support timely deployment.

On October 15, the company’s press release explained that they had also received DOE approval for its Conceptual Safety Design Report for the Aurora Fuel Fabrication Facility, which will recycle nuclear fuel material at Idaho National Laboratory (INL).

Subsequently, the Aurora Fuel Fabrication Facility will produce fuel for Oklo’s Aurora power plant at the Idaho National Laboratory (INL). It will essentially deploy high assay low enriched uranium recovered from spent Experimental Breeder Reactor-II fuel.

With a secured fuel supply, site use permit, and strong regulatory progress, Oklo is ready to launch its Aurora reactor. Its developed supply chain will further support the first deployment.

Now that the final clearance is approved by both the DOE and INL, CEO Jacob DeWitte is confident in the collaboration. He expects to bring Oklo’s first commercial nuclear fission plant online within the next few years.

From Waste to Power: Oklo’s Aurora Reactor Sets New Standards in Clean Energy

We discovered from World Nuclear News some unique features of the Aurora powerhouse, which are illustrated below:

It is a fast neutron reactor that generates electricity by moving heat from its core to a supercritical carbon dioxide power conversion system.

Designed to run on either fresh HALEU or recycled nuclear fuel, Oklo’s reactors can transform used nuclear fuel into clean energy.

It can generate 15 MWe, scale up to 50 MWe, and operate for over a decade before needing refueling.

The fission pioneer also explained that they use advanced recycling techniques to keep transuranic materials together as fuel. This avoids the need to create pure material streams, which is a unique feature of fast reactors.

Uranium Royalty Corp.: Powering Decarbonization with Nuclear Efficiency

The only pure-play uranium royalty company is focused on capturing value from uranium price shifts through strategic investments. These include royalties, streams, debt, equity in uranium companies, and even physical uranium holdings. Notably, the company is growing with the rising demand for uranium.

IEA revealed that in the U.S. alone, nuclear energy supplied roughly 19% of total electricity in 2022 and accounted for 55% of the nation’s carbon-free electricity.

This nuclear output mitigated around 482 MMT of CO₂ emissions, which is equivalent to taking 107 million gasoline-powered vehicles off the roads.

More Power per Punch: Nuclear Energy Outshines Fossil Fuels

Why Oklo’s Advanced Nuclear Fission is Just One of A Kind

Oklo’s advanced fission powerhouse has unique advantages over traditional power generation technologies. In short clean, resilient, reliable, and affordable are the four features that truly make it one of a kind.

The reactors produce zero carbon emissions which makes them an environmentally friendly option. Oklo has stressed the fact that the energy density of nuclear fuel is a million times more than fossil fuels, hence it requires less land for mining. This attribute is significant for environmental preservation.

Moreover, unlike coal and gas plants that require frequent refueling, Oklo’s reactors can run for decades on a single load. This is how the nuclear company ensures long-term fuel reliability and independence.

Check out the landscape view of Oklo’s preferred site in Idaho

Image Source: Oklo Inc

Talking about the cost-effective factor, the immense energy density of its fuel makes it an economical alternative to fossil fuels. Also, nuclear fuel has fewer resource requirements and lower operational costs.

Most importantly Oklo’s reactors deliver consistent, clean energy, and heat with minimal refueling—sometimes as infrequently as every 20 years. This long-term reliability supports steady power output that’s ideal for critical energy needs.

Thus, starting with Aurora, Oklo is developing unique kinds of next-generation reactors. Furthermore, with the collaboration with DOE and INL, the company is just on the right path to establishing nuclear fission as an abundant, affordable, and clean energy source across the world.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: UROY.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

China and Indonesia partnered for a series of business agreements worth $10 billion during the Indonesia-China Business Forum in Beijing on Sunday. This high-level forum followed a Saturday meeting between China’s President Xi Jinping and Indonesia’s President Prabowo Subianto. Reuters revealed that the leaders expressed their plans for strategic economic growth across sectors like food, clean tech, biotechnology, and pressing issues related to water conservation, maritime resources, and mining, particularly nickel.

Notably President Prabowo Subianto said,

“We must give an example that in this modern age, collaboration — not confrontation — is the way for peace and prosperity.”

The joint statement further explained their plans to expand cooperation across new energy vehicles, lithium batteries, photovoltaic projects, and the digital economy. They also committed to advancing the global energy transition, securing mineral resources, and stabilizing supply chains.

Indonesia’s Nickel Surge: Fresh Billion-Dollar Deals from China

Indonesia’s nickel industry was a significant topic of discussion during the meeting. The country, which leads global nickel production always has been a major investment hub for Chinese firms.

In this regard, the latest news is that Chinese battery materials producer GEM Co., Ltdstriking a groundbreaking deal with Indonesia’s PT Vale to build a high-pressure acid leaching (HPAL) plant in Central Sulawesi. The agreement with a deal value of $1.42 billion, will ensure the nickel plant maintains nickel supplies which is crucial for battery-grade materials.

Moving on, Tsingshan Holding Group and Zhejiang Huayou Cobalt, the two major Chinese companies, continue to dominate Indonesia’s nickel industry. Their investments reflect faith in Indonesia as a prominent supplier of raw materials for EVs, lithium-ion batteries, and other green technologies.

Elaborating this further, Bloomberg reported that Zhejiang Huayou Cobalt Co. is pursuing $2.7 billion in financing for its battery-nickel plant in Indonesia. The financing deal, backed by Ford Motor Co., is being coordinated by HSBC Holdings Plc and Standard Chartered Plc, who are inviting additional banks to participate.

The Pomalaa plant, located in Southeast Sulawesi, will use high-pressure acid leaching (HPAL) technology to produce battery-grade nickel for electric vehicles. Notably, it will have a capacity of 120,000 tons of nickel annually, making it one of Indonesia’s largest HPAL projects.

Both nations consider the timing of these deals a boon to the slump nickel market. Currently, nickel prices are weak due to low demand in the stainless-steel market and slow growth of the EV sector.

The Ever-Expanding Indonesian Nickel Industry

Indonesia has always attracted foreign investment to boost its domestic nickel production. The country sees this as essential for boosting and adding value to its vast natural resources. Despite these market pressures, Indonesia and China remain committed to their long-term goals, with Indonesia flagging its nickel industry as an integral part of its economic strategy.

As one of the top producers of metallic commodities—including gold, copper, cobalt, and especially nickel—Indonesia produced over half of the world’s mined nickel in 2023. Indonesia’s cost-effective nickel industry spurred major shifts in the nickel market. While nickel prices have dropped since last year, the country has still maintained a resilient and steady production.

China and Indonesia are not limiting their partnerships to the resources sector. Credible media agencies reported that GoTo Gojek Tokopedia, a prominent Indonesian technology company, signed agreements with China’s Tencent and Alibaba to bolster Indonesia’s digital infrastructure.

These partnerships can advance cloud services and foster local digital talent. It also signals a long-term investment in Indonesia’s digital economy and improving digital literacy and infrastructure at large.

Notably, President Subianto envisions transforming Indonesia’s tech landscape with investments in the most advanced sectors like AI and cloud computing.

Reuters reported, in addition to high-level industry deals, China and Indonesia agreed to streamline travel and visa policies, introducing measures like multi-entry long-term visas. This will enable more bilateral exchanges, business trips, and tourism.

Furthermore, the nations also agreed to deepen trade in agricultural products, including fresh coconuts. Interestingly, President Subianto also secured export agreements during his visit. This expansion of agricultural exports creates new opportunities for Indonesian farmers while fulfilling China’s demand for tropical produce.

Overall, it is evident that President Subianto’s decision to choose China as its first state visit shows the nation’s strong intention to deepen ties with Beijing.

As the world gears up for the upcoming UN climate summit, COP29, in Baku, Azerbaijan, the G-20 governments face the challenge of crafting more ambitious climate plans. These plans must balance bold climate commitments with economic realities like budget constraints, a cost-of-living crisis, and the push for energy independence. The situation is further complicated by recent election outcomes.

However, not all G-20 countries are moving at the same pace. The latest Climate Policy Factbook by BloombergNEF, commissioned by Bloomberg Philanthropies, evaluates G-20 progress in three crucial policy areas:

Fossil-fuel subsidies,

Carbon pricing, and

Climate-risk policies.

Here’s our key takeaways from the report.

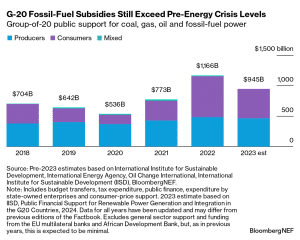

Fossil-Fuel Subsidies Surge Despite Climate Goals

In 2022, G-20 countries provided a staggering $1.1 trillion in fossil-fuel support, the highest in over a decade. This spike was driven by the global energy crisis, as governments aimed to shield consumers from soaring energy costs.

However, $500 billion of this went to producers and utilities, some of which reported record profits.

Despite global climate goals, the G-20 is expanding its coal power capacity. From 2019 to 2023, coal-fired capacity grew by 3%, adding up to 2 terawatts (TW) of operational capacity, with another 0.6 TW in development. Coal remains the largest contributor to climate change.

The distribution of fossil-fuel support by type has remained largely unchanged in recent years. Although coal represents a small portion, its share is significant due to the high overall fossil-fuel support in 2022. G-20 governments allocated $49 billion to coal, the most emissions-intensive fuel.

Remarkably, OECD members reduced coal capacity by 22% since 2019. Conversely, non-OECD economies increased their coal capacity by 6%.

Country Progress

Australia is showing improvement by reducing coal-fired capacity and lowering fossil-fuel support in 2022. Meanwhile, China and Japan are labeled as making insufficient progress while Canada and the UK were downgraded to “mixed progress.”

Preliminary 2023 data suggests fossil-fuel subsidies fell to $945 billion, a 19% decrease from 2022 but still above pre-crisis levels. Reforming these subsidies is politically sensitive, as it could raise consumer prices.

Canada offers a potential pathway by defining and eliminating inefficient fossil-fuel subsidies.

Carbon Pricing Gains Traction, But Is It Enough?

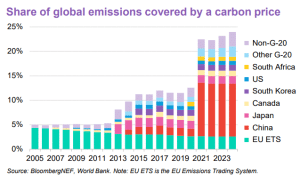

Carbon pricing is becoming more widespread across the bloc. It now account for about 25% of global greenhouse gas emissions and 29% of G-20 emissions through taxes or trading schemes, per BNEF analysis. This share is expected to grow as more programs roll out.

Currently, 14 G-20 economies, including the EU, have economy-wide carbon pricing mechanisms. Russia and the US have subnational schemes, while South Africa remains the only African Union member with a carbon tax in place.

While some G-20 countries, like Australia, China, and South Africa, have seen rising carbon prices, others, particularly in Europe, experienced declines. Only the EU’s Emission Trading Scheme (ETS) currently operates within the price range necessary to limit global warming to 2°C by 2030.

Expanding Carbon Markets

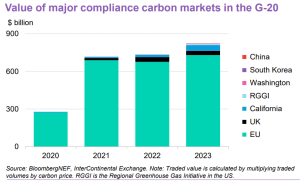

Canada, France, Germany, and Mexico lead the pack with multiple national-level carbon taxes or markets.

Brazil, India, and Turkey are designing compliance carbon markets while Indonesia and Japan are considering additional carbon pricing programs. And all EU members will see another carbon market with the 2027 launch of the road transport and buildings ETS.

Notably, China’s carbon market, the largest globally by covered emissions, is set to expand to aluminum, steel, and cement sectors. The EU ETS leads in traded value, driven by higher prices and trading volumes, whereas Canada and California are on track to meet their targets by the end of the decade.

The combined value of G-20 compliance carbon markets exceeded $800 billion in 2023, BNEF Factbook shows. Price increases across these markets stemmed from policy reforms aligning with climate goals, though trading volumes dipped in some due to economic impacts from Russia’s invasion of Ukraine.

As G-20 members strengthen their carbon markets, they create powerful incentives for emission reductions and sector-specific adaptation. As such, they can contribute significantly to the transition toward a low-carbon global economy.

Climate-Risk Policy: Who’s Leading and Who’s Lagging

G-20 members are at varying stages of implementing climate-risk regulations. Some, like the EU, Brazil, and the UK, lead the charge with comprehensive frameworks.

However, others, including Argentina, Saudi Arabia, and Russia, lag behind, lacking even basic regulations. Other remarkable recent developments in this area include:

Turkey and the US made notable strides in climate-risk policy.

Nine G-20 countries have adopted or are developing regulations aligned with the International Sustainability Standards Board (ISSB).

The ISSB framework promotes consistency in climate-risk reporting. However, its effectiveness could be undermined by local variations and relatively low stringency.

What COP29 Means for G-20 Climate Action

The G-20’s progress is uneven, with some countries advancing robust policies while others remain stuck in outdated systems. COP29 presents a crucial opportunity for world leaders to reassess their commitments and bridge these gaps.

Based on BNEF’s Climate Policy Factbook data, to accelerate the transition to a low-carbon economy, countries must:

Phase out fossil-fuel subsidies, starting with inefficient ones.

Implement stringent climate-risk policies to build a more resilient economy.

Ultimately, meaningful climate action requires global cooperation and bold leadership, particularly from the G-20, which holds the key to the planet’s future.

Most industrial greenhouse gas (GHG) emissions come from energy use. By improving energy efficiency, the world can cut energy consumption, lower emissions, and save on costs. It’s a smart and cost-effective first step toward decarbonization and businesses are continuing to pour funds into energy efficiency initiatives and technologies worldwide as the International Energy Agency (IEA) reported.

The IEA’s Energy Efficiency 2024 highlights key trends in energy intensity, demand, prices, and policies. It also offers insights into system-wide themes including investment, which this article will delve into in detail.

Driving Change: What Leads the Energy Revolution?

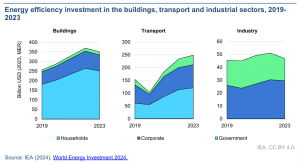

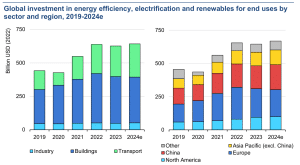

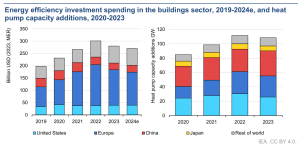

The report shows that energy efficiency investments could remain resilient in 2024, with total spending projected to reach around $660 billion. This level matches the record set in 2022 and highlights the steady commitment to sustainable energy use. These investments span sectors like transport, buildings, and industry, driven by the need to reduce emissions and enhance energy efficiency amid fluctuating economic conditions.

Since 2019, global energy efficiency investments have surged by 45%, fueled by the energy crisis and significant government spending post-Covid-19. The transport sector has seen the highest growth, with a 77% rise, followed by buildings at 34% and industry at 13%.

Source: IEA 2024 Report

However, from 2022 to 2024, the trend shifted. Investments in buildings dropped by 7%, while transport saw a 14% rise, and industry remained steady.

A key driver for the trend is the push for efficient electrification, especially in the electric vehicle (EV) sector across China, Europe, and North America. EV sales, particularly in emerging markets, have supported this trend.

However, as energy prices stabilize and government stimulus wanes, overall global investment has plateaued. Rising inflation and interest rates also pose challenges for financing efficiency upgrades.

Emerging Markets Take the Spotlight in Efficiency Investments

The growth of efficiency-related investments in 2024 is uneven across regions. Emerging markets and developing economies (EMDEs) are expected to lead.

Africa is projected to see a 60% rise, the Middle East 40%, and Central and South America over 20%. China will also witness nearly 10% growth.

Conversely, advanced economies are stabilizing after years of crisis-driven spending. Europe is set for a slight decline, while North America will see a modest 5% increase.

Despite slower growth in these regions, they still account for the bulk of global energy efficiency investments—95% of total spending occurs in Europe, Asia Pacific, and North America, regions responsible for about 75% of global energy demand.

Transport Electrification: A Surge in EV Sales

Globally, the electrification of transport has gained momentum. By 2024, around one in five new cars sold will be electric.

EV sales reached 14 million in 2023, making up 18% of total car sales, and this figure is expected to grow to 17 million in 2024. The bulk of these sales occurred in China, Europe, and North America, which accounted for 95% of global EV sales.

In EMDEs, the focus remains on two- and three-wheelers. These vehicles dominate markets in regions like Southeast Asia and Latin America. China leads in two-wheeler sales, though global sales in this category dropped 18% in 2023 due to supply chain disruptions.

India, however, saw a 40% increase in electric two-wheeler sales and continued growth in three-wheelers, spurred by government initiatives like the Electric Mobility Promotion Scheme.

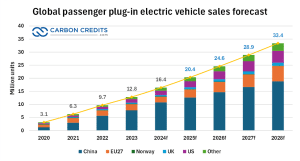

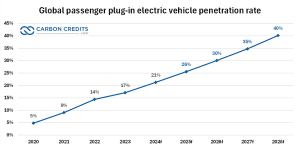

According to S&P Global data represented by the chart above, global passenger plug-in EV sales could reach over 33 million units by 2028. That’s almost a 104% increase in EV units sold. China is set to take the biggest growth in sales.

The number of people projected to use EVs for the same period (penetration rate) will also double by 2028 compared to 2024.

Source: S&P Global

Building Smarter: A Post-Crisis Slowdown

Investment in energy-efficient buildings boomed during the energy crisis, driven by technologies like heat pumps. In 2022, heat pump sales peaked, particularly in Europe, where they are central to long-term climate goals.

However, this momentum slowed in 2023 due to high electricity prices and reduced government support. For instance, Italy’s Superbonus program, which heavily subsidized energy-saving renovations, was phased out in 2024. This program alone accounted for more than half of Italy’s building sector investments in 2023.

Meanwhile, heat pump deployment in China has seen modest growth. These trends highlight the critical role of government policies in sustaining investment in building efficiency.

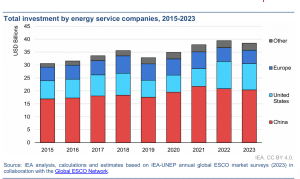

ESCOs and the Power Players Behind the Efficiency Boom

The energy service company (ESCO) market experienced a slight decline in 2023, dropping by 2.2%. Despite this, the market size remains robust at over $35 billion, supported by strong policies in regions like the U.S.

Federal programs, such as the Federal Energy Management Program, have bolstered ESCO activities, which grew by 54% between 2021 and 2023 in the U.S.

China leads the global ESCO market, with investments exceeding $20 billion in 2023, accounting for half the global total. The majority of ESCO investments target the buildings sector, followed by industrial applications and energy storage.

Among the major players in the ESCO market, some of the interesting companies making waves in the sector include:

Johnson Controls is a global leader in smart building solutions, offering advanced technologies and services to enhance building performance and sustainability. In energy efficiency, Johnson Controls has made significant progress by implementing high-capacity heat pumps and optimizing energy use in various industries. They have contributed to over $6 billion in customer projects worldwide, driving sustainability and reducing carbon footprints.

Ameresco is a leading cleantech integrator that specializes in energy efficiency, renewable energy, and infrastructure modernization. In 2023, its renewable energy projects and assets helped avoid around 16 million metric tons of CO₂ emissions, contributing to over 110 million metric tons of cumulative carbon reductions since 2010. Ameresco has received numerous awards for its sustainability efforts and continues to drive innovation in clean energy.

Trane Technologies, through its flagship brand Trane, provides innovative HVAC solutions designed for energy efficiency and sustainability. The company delivers services such as Energy Savings Performance Contracting (ESPC) to optimize energy consumption and reduce operational costs for buildings. Trane emphasizes sustainability, helping clients meet carbon reduction goals through electrification, energy monitoring, and renewable energy integration.

NORESCOis specializing in energy and infrastructure solutions for government, institutional, and commercial clients. The company has a strong track record in improving energy efficiency, managing over $2.75 billion in federal energy projects. It helps clients achieve sustainability goals through advanced technologies like microgrids, battery storage, and renewable energy systems.

Scaling Up: What’s Needed for 2030?

To meet net-zero targets, energy efficiency investments must triple by 2030, reaching $1.9 trillion annually, per the report. The IEA’s NZE Scenario underscores the importance of a comprehensive strategy tailored to each country’s needs.

In emerging economies, efforts focus on improving building performance and electrifying transport. In sub-Saharan Africa, the transition to clean cooking fuels is a top priority. Advanced economies, meanwhile, focus on retrofitting older infrastructure, deploying heat pumps, and scaling up EV infrastructure.

Ultimately, energy efficiency investment is vital for meeting global climate goals and expanding investment to underrepresented regions will be key to accelerating progress.

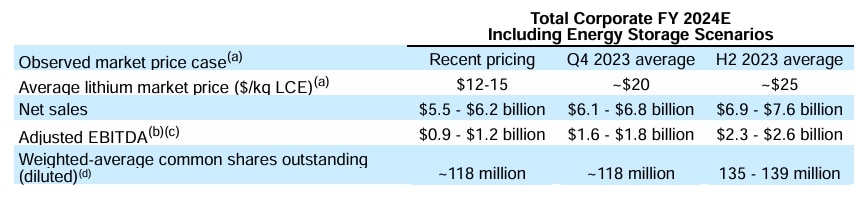

From the latest news from CarbonCredits, you can see that the lithium market has entered a period of price decline. This is mainly because of weaker demand conditions and an oversupply of lithium carbonate in key regions. However, this trend doesn’t favor the top lithium miners and producers across the globe. Recently Albemarle and Pilbara have taken some drastic steps to counter the lithium market lows.

Let’s see how they are navigating the challenges…

Albemarle’s Strategy for Surviving the Lithium Market Slump

As a consequence of dropping lithium prices, Albemarle Corporation is set to reduce its global workforce by between 6% and 7%, which will save around $300 million to $400 million annually.

Despite being the world’s largest lithium producer, the company reported a net loss of $1.07 billion for the third quarter. The company released its earnings report on November 6.

Kent Masters, Albemarle’s president and CEO expressed himself by saying,

“Right now we’re focused on making sure that we put the cost structure in place to compete through the bottom of the cycle. We’re trying to create the flexibility to pivot up if the market returns.”

The New Approach

The earning report revealed how the company is planning to streamline its organization by adopting a more integrated and functional model. In purview, it will reduce its 2025 capital expenditures by about 50% compared to 2024 to bring spending down to between $800 million and $900 million.

The company noted that this quarter’s results sharply contrast with the $302 million net income earned in the same period last year.

CEO Kent Masters emphasized that China has scaled back high-cost lepidolite production, while Australian miners have reduced output and laid off employees in response to market conditions. Still, these trimming measures are insufficient to stabilize lithium prices.

According to him, the surprising factor is that “African supply has filled Chinese cuts.”

On the demand side, CFO Neal Sheorey highlighted a 36% increase in demand for lithium in grid storage this year, driven by U.S. and Chinese projects, along with a 23% rise in global electric vehicle registrations.

Albemarle estimates that around 25% of the lithium industry is currently operating at a loss. The reason is again the oversupplied market. However, the top lithium producer wants to stay competitive over the long term. This is why they have conducted a thorough review of their costs and operating structure.

Broadly speaking, they revealed their potential future actions to address ongoing market challenges. Masters said that, while rising demand could help restore balance further production cuts will be essential to stabilize prices effectively. In response to the lingering low lithium prices, the company plans to adopt a conservative growth strategy to ensure long-term reliance.

Notably, In July, Albemarle halted expansion plans at its Kemerton lithium hydroxide refinery in Australia to manage costs more effectively.

Li-FT Power Ltd.(TSXV: LIFT) recently announced its first-ever National Instrument 43-101 (NI 43-101) compliant mineral resource estimate (MRE) for the Yellowknife Lithium Project (YLP), located in the Northwest Territories, Canada.

An Initial Mineral Resource of 50.4 Million Tonnes at Yellowknife.

This maiden estimate is a major milestone for the company and marks a significant step forward in the project’s development. Li-FT Power’s upcoming mineral resource is expected to further solidify Yellowknife as one of North America’s largest hardrock lithium resources.

Pilbara’s Strategic Move to Overcome Lithium Price Dip

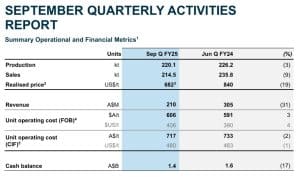

On October 30, Pilbara Minerals announced its decision to pause construction of their Mid-Stream Demonstration Plant Pilgangoora lithium mine in Western Australia citing weak lithium prices as the main reason. The project is a JV with environmental technology company Calix Ltd formed in November 2022.

The smaller Ngungaju plant will be placed on temporary care and maintenance from December 1 which will allow the company to manage current price pressures more efficiently.

Pilbara Minerals highlighted that spodumene concentrate prices, ranging from US$750 to $800 per ton, remain below the sustainable industry benchmark of US$1,400 per ton.

In the September quarter, the company sold lithium at an average of US$682 per ton, a decrease from US$840 per tonne in the previous quarter.

The demonstration plant at Pilgangoora that would produce lithium salts using Calix’s advanced calcination technology was 60% completed by the end of September this year. Pilbara anticipates these measures will contribute about A$200 million in cash flow improvements for fiscal 2025.

Cutting Capital Expenditure

MINING.com reported: Pilbara Minerals also revised its production guidance for fiscal 2025 to a range of 700,000 to 740,000 dry metric tonnes (dmt). It’s down from an earlier target of 800,000 to 840,000 dmt.

Meanwhile, it has cut its capital expenditure forecast to between A$565 million and A$610 million, down from a previous estimate of A$615 million to A$685 million.

Managing Director and CEO Dale Henderson said,

“Given current lithium price environment, this pause enables the joint venture to time expenditure with improved market conditions. We remain fully supportive of the midstream strategy and our joint venture, recognising the Project’s potential to transform the lithium supply chain through lower emissions and value-added processing. Our commitment to our joint venture with Calix remains. We will assess with Calix resuming the Project as market conditions improve or further government support is received.”

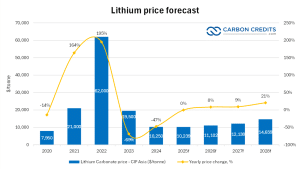

Lithium Glut Lingers, Even as Demand Surges

Data Source: S&P Global

Analyzing the market condition further, the lithium scenario is quite vivid. This rapidly growing demand has attracted new lithium players, but major producers are yet to make significant production cuts.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.