A pioneering climate tech company, Greenlines Technology, announced the approval of the world’s first carbon credit generation process patent awarded by the United States Patent and Trademark Office (USPTO).

Greenlines Technology empowers and rewards sustainable behaviour in the mobility and e-commerce industries to make a positive environmental impact through its advanced digital measurement, reporting, and verification (dMRV) technology.

The Vancouver-based climate tech startup is the first to coin the term ‘Human-based Solutions’ (HbS) in carbon markets, which refers to contributions by individuals and their behavior in reducing carbon emissions.

Greenlines: Pioneer Carbon Credit Patent in Transportation

The first-of-its-kind patent, Mobility Carbon Engine (MCE™), represents a significant advancement in global carbon markets, providing novel intellectual property rights. Titled “Methods and Systems for Conversion of Physical Movements to Carbon Units”, it has Patent Number US 11,774,255 B2.

Greenlines’ landmark patent enables mobility app owners to measure and monetize emission reductions facilitated by users. The groundbreaking technology can accurately calculate and monetize those reductions, setting a precedent for quantifying sustainable transportation impacts.

The newly patented technology has been around since 2019 in 60+ cities across Canada and the U.S.

Highlighting the importance of this technology in reducing emissions and promoting sustainability in mobility, CEO and co-founder David Oliver noted:

“By providing a systematic approach to accurately quantify and recognize emission reductions resulting from individuals’ use of low-carbon land, water, and air-based transportation modes, the MCETM creates a comprehensive framework that rewards individuals and organizations for choosing sustainable alternatives.”

As per the Environmental Protection Agency’s latest data, greenhouse gas (GHG) emissions from transportation account for about 29% of total U.S. emissions, making it the biggest contributor of the country’s pollution.

With over a third of Americans commuting to work on an average of 44 km or 27 miles, the annual CO2 emissions per commuter stands at about 4.6 tons.

According to Oliver, if 10% of these commuters use their MCE, it can potentially slash their emissions by around 20%. That’s equivalent to a total of 24 million tons of CO2 emission reductions each year in the US transport sector.

The MCE is powered by Greenlines proprietary Modal Shift Optimization GHG Quantification Methodology developed according to ISO 14064-2. This guarantees that the carbon credits generated through the app meet the highest standards and trades at a premium price.

The technology uses advanced algorithms to measure the emission reductions from each trip, avoiding reversal and ensuring offsets are permanent. It is simple to use and has a user-friendly interface, thus it is highly accessible to everyone.

To meet the criterion on additionality, the MCE creates a custom baseline for each user and use it as reference for getting the emission reductions. The reduction is the difference between the baseline and the actual carbon pollution emitted by each trip. The data is crucial to ensure that the reductions are additional compared to the emissions without the offset project.

In establishing the baseline, Greenlines uses regional project and baseline emissions for various transportation modes – land, water, and air. These include taxis, public transit, ride-hailing, e-scooters, and pedal bikes.

The innovative technology employs a robust monitoring system to track and verify the emission reductions. Verification is through independent, third-party verifier. And these verified emission reductions (VERs) have been successfully sold as carbon credits to voluntary buyers in the carbon market.

Greenlines’ carbon offset project is transparent with publicly accessible information, including the amount of CO2 reduced, the MRV process, and offset revenue use.

Meeting all these criteria – additional, permanent, real, verifiable, and transparent – makes the carbon credits or offsets generated of high-quality. Each credit represents a tonne of reduced CO2 emissions.

Greenlines’ technology offers a potential to revolutionize the mobility sector while providing a strong incentive for individuals to choose low-carbon trips. It empowers mobility aggregators, including transit agencies, trip planning apps, and private mobility providers to promote sustainable transportation practices.

Incentivizing Sustainable Behavior with Carbon Credits

The patent doesn’t only track and monetize emissions from personal trips but also from food and package deliveries, Oliver said.

That’s through their upcoming E-commerce Carbon Engine (ECE), which is currently in its pilot phase. Same as MCE, ECE will also generate carbon credits from low-carbon items bought in e-commerce or online trading platforms.

ECE uses Greenlines’ proprietary algorithms to get the CO2 footprint of each product, allowing consumers to choose low-carbon purchases. Thus, it also has the potential to slash emissions of online shopping.

Greenlines had already implemented the MCE technology across various North American cities. But it also plans to expand its reach globally by initiating patent applications in other jurisdictions such as the EU.

Their goal is to incentivize and drive sustainable practices worldwide through carbon credits generated by their patented technology.

By combining innovative technology with sustainability, Greenlines revolutionizes carbon markets while giving commuters the opportunity to identify, quantify, and monetize their carbon emissions reductions.

The single largest driver of climate change, industry, accounts for about ⅓ of global carbon emissions. But a Bill Gates-backed startup, Antora Energy Inc., offers a potential solution to eliminate over 50% of industrial emissions with its unique approach to decarbonizing the sector – thermal energy storage via solid carbon blocks.

Industry has been considered a hard-to-abate sector due to the very nature of their energy-hungry and heat-intensive processes. This is what the startup Antora Energy, a company supported by billionaire Bill Gates’ Breakthrough Energy Ventures, tries to address.

Antora has launched its groundbreaking commercial-scale thermal battery system in Fresno, California, with a slated technology delivery target of 2025.

What is Thermal Energy Storage?

Almost every industrial facility needs heat to do its daily grind: to melt, cure, dry, cook, treat, calcine, among others. This heat accounts for ⅔ of all industrial energy use and the bulk of the sector’s emissions.

In the United States, the industry accounts for about ¼ of the country’s total greenhouse gas emissions in 2021.

Energy experts believe that if the world can solve the challenge of clean energy for heavy-emitting industries, it would pave the way for rapid industrial decarbonization.

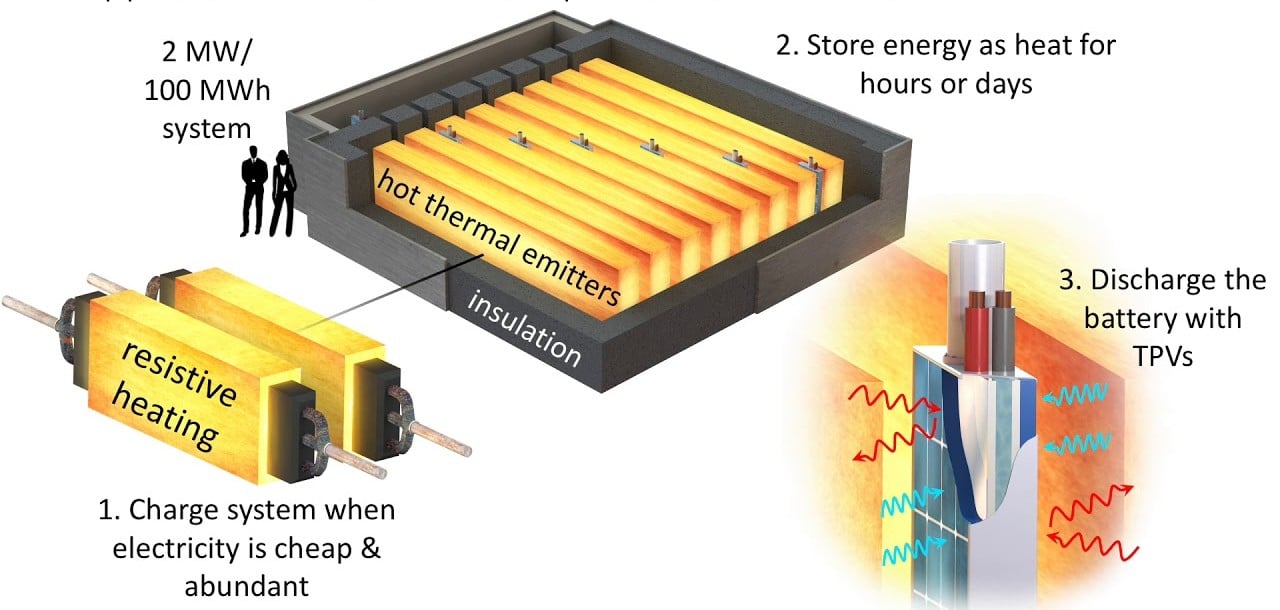

Enter thermal energy storage or TES. Powered by renewable energy, TES can help decarbonize industrial heat in significant amounts.

Thermal energy storage enables companies to store heat using low-cost, scalable, and ample materials. It allows for the use of renewable energy when it’s cheapest, meaning when the wind blows or the sun shines. The solar or wind energy heats up a thermal battery, which is then stored for hours or days.

Image from https://reimaginingenergy.afwerx.com/

Thermal batteries are cheap to assemble, easy to maintain, and work for decades. Moreover, they don’t use expensive and limited materials, but abundant and cheap materials like carbon and concrete. They could provide the much-needed storage that can make renewable power available year-round.

The International Renewable Energy Agency (IRENA) estimates that TES would facilitate increased use of renewables in energy systems. With it, operators can effectively match energy demand and supply, making the system more efficient, flexible, and cheap.

Solid carbon, in particular, is available cheaply and comes with a vast supply chain of >30 million tons annually. Plus, it can store and emit huge amounts of heat at very high temperatures. This is what Antora Energy’s storage system is using.

Antora Energy’s Innovative Thermal Energy Storage

Co-founded by an MIT alumnus, David Bierman, Antora Energy leverages the power of nature, sun and wind, to provide low-cost and highly-efficient energy storage. Their thermal energy system stores electricity as heat to enable manufacturers and energy-intensive industrial processes to stop fossil fuel consumption. According to Bierman,

“The economic opportunity has grown, but more importantly the awareness from industries that they need to decarbonize is totally different. Antora can help with that, so we’re scaling up as rapidly as possible to meet the demand we see in the market.”

Different from traditional lithium-ion batteries, Antora’s thermal battery stores energy as heat within solid carbon blocks. It offers an eco-friendly solution for industries like cement and steel manufacturing that heavily rely on fossil fuels.

The company’s TES stores energy as heat in the blocks at extremely high temperatures, exceeding 1,800°C! It can then be used directly as heat or converted back to electricity via thermophotovoltaic (TPV) cells, similar to solar cells.

The building blocks can be configured to meet any load and their compact footprint enables seamless site integration.

Antora’s modular thermal energy storage turns solar and wind energy into dispatchable, zero-emissions heat and power. This can help companies operating in the industry to reduce their Scope 1 and 2 emissions.

While Antora forges ahead with this innovative approach, other startups are also making strides in the battery sector. Their approaches may differ but they all aim to eliminate or lessen the environmental impact of batteries while providing eco-friendly energy storage.

In fact, in the recent surge of venture capital, battery startups are making waves and attracting significant investments. One area of investor’s focus is optimizing renewable energy’s grid storage, which Antora Energy seeks to deliver.

Antora’s upcoming battery production site in the Bay Area, set to be completed by 2024, presents economic challenges more than technological ones; the venture requires significant capital. Overcoming these obstacles could pave the way for a transformative shift in the energy sector.

A Shift Towards Zero-Carbon Solutions

Antora’s thermal energy storage aims to provide an end result of a zero-carbon, flexible heat and power system for industry.

The company’s unique dual function of providing heat and electricity without carbon emissions presents a vital alternative for industries currently reliant on non-continuous renewable sources, essential for meeting decarbonization goals.

The energy storage company targets sectors relying on consistent heat and power for their plants, eyeing a substantial share of the $60 billion U.S. market. Market segments include cement, steel, chemicals, oil, and gas refining.

The company is targeting clients in windy and sunny states where renewable energy is abundant and cheap. With that, Antora aims to eventually outcompete fossil fuels on cost, potentially revolutionizing the energy industry. This innovation promises a significant step forward in the battle against climate change in carbon-intensive industries.

The British Columbia film industry, a key production hub for Hollywood entertainment, is under pressure to shift away from diesel generators to power film and food trucks on local sets.

According to reports, the use of diesel generators is a main source of carbon emissions. This makes Vancouver’s film sets a significant contributor to air pollution.

Suggestions for a change include using mobile power alternatives such as sourcing energy directly from the local grid. This works both for film and TV sets in British Columbia for producing original content for large studios and streamers.

Carbon Footprint of the Entertainment Industry

Sustainability is crucial to every industry and the film industry is no exception, facing growing scrutiny for its environmental impact.

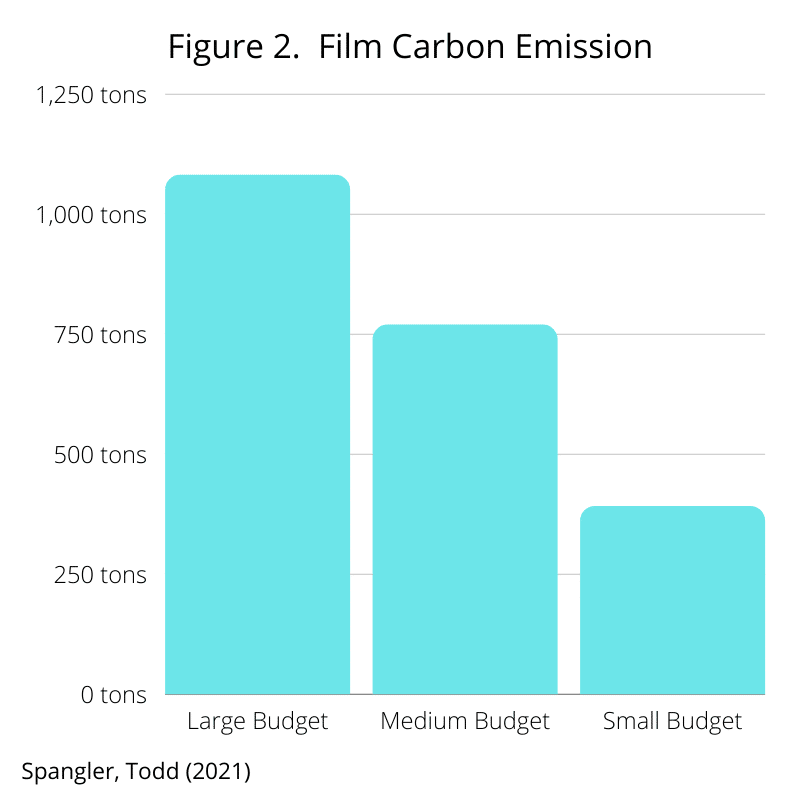

According to the Sustainable Production Alliance (SPA), each film production emits around 3,370 metric tons (Mt) of CO2 or about 33 Mt for each shooting day. This figure is equivalent to over 7 million miles driven by a car. That applies to production with an average budget of $70 million, while smaller films emit about 400 Mt.

SPA is a group of film, TV and streaming companies committed to making the entertainment industry more sustainable. The consortium members include Amazon Studios, Disney, Fox Corp., NBCUniversal, Netflix, Sony Pictures, and WarnerMedia.

The group’s report considers various factors contributing to the production’s carbon emissions, including flights, housing, fuel and utilities. The largest contributor for all film sizes is fuel used by vehicles and power generators.

Their data covers industry wide production carbon emissions averages for the SPA member companies over three years. A more recent report included a May 2023 report on Clean Power Alternatives for the Film Industry for Metro Vancouver.

Source: Variety

For a TV series, a 1-hour scripted dramas emitted 77 Mt of CO2 per episode while a half-hour scripted single-camera show released 26 Mt. Unscripted series generated a smaller CO2 footprint per episode, 13 Mt.

The SPA’s recent report in July 2022 covered more than 300 films and TV productions in the U.S. and over 60 productions in Canada.

As per the report, the 6 largest films shot in Vancouver produced over 1,400 Mt of CO2. Over in Atlanta, medium-sized movies emitted a little above 970 Mt of CO2.

Cleaner Energy Options for Lower Emissions

The difference in total carbon emissions between the two locations is the energy used in Georgia, which comes from dirtier sources (e.g. coal and natural gas).

In Vancouver, producers can reduce their pollution by tapping into cleaner energy sources for local films and TV shows. These include the use of zero-emission battery power and local electricity grids.

However, compared to other North American filming locations, fuel use in British Columbia remains proportionally higher. That’s primarily because of the big sizes and number of power generators used in sets as well as at soundstages.

Apart from spewing air pollutants, diesel generators also pose health risks, prompting calls for more sustainable and planet-friendly practices.

Some productions turned to using solar energy to power generators and banning single-use plastics on sets. Other film and TV studios are adopting other ways to reduce their emissions and the entire industry’s carbon footprint.

A Call for a More Sustainable Filming

In the B.C. film industry, major studios and streamers are encouraged to ramp up transition to cleaner energy sources. Similar trends are seen in Ontario where Hollywood post-strikes called for sustainable film productions as default on sets and soundstages.

Hollywood and other producers are also pushing for a more sustainable entertainment industry.

For instance, the streaming giant, Netflix, pledged to reduce carbon emissions by 45% below 2019 levels by 2030. The company’s approach to net zero involves three R’s: Reduce, Retain and Remove.

Disney aims for a net zero emissions for its direct operations by 2030 which involves investing in natural climate solutions.

On the other hand, Sony committed to eliminate its environmental footprint by 2050 while NBCUniversal aims to achieve carbon neutrality by 2035.

As for individual initiatives in greening the industry, producers and streamers use fully recyclable sets using waste materials. This helps avoid traditional materials (timber, plywood, fiberboards, etc.) from going to landfills.

Other large studios partner with green organizations such as Earth Angel and The Green Production Guide. These organizations helped studios learn and adopt sustainable filming practices. Example of these sustainability efforts from various movie productions include the following:

Image borrowed from Georgia Calawerts at https://amt-lab.org/

By transitioning away from diesel generators and embracing cleaner energy options, the entertainment industry is demonstrating a commitment to reducing its carbon footprint and promoting sustainable filming practices. With a concerted effort from major studios, streamers, and industry organizations, the move towards sustainability in film production sets a precedent for the industry as a whole.

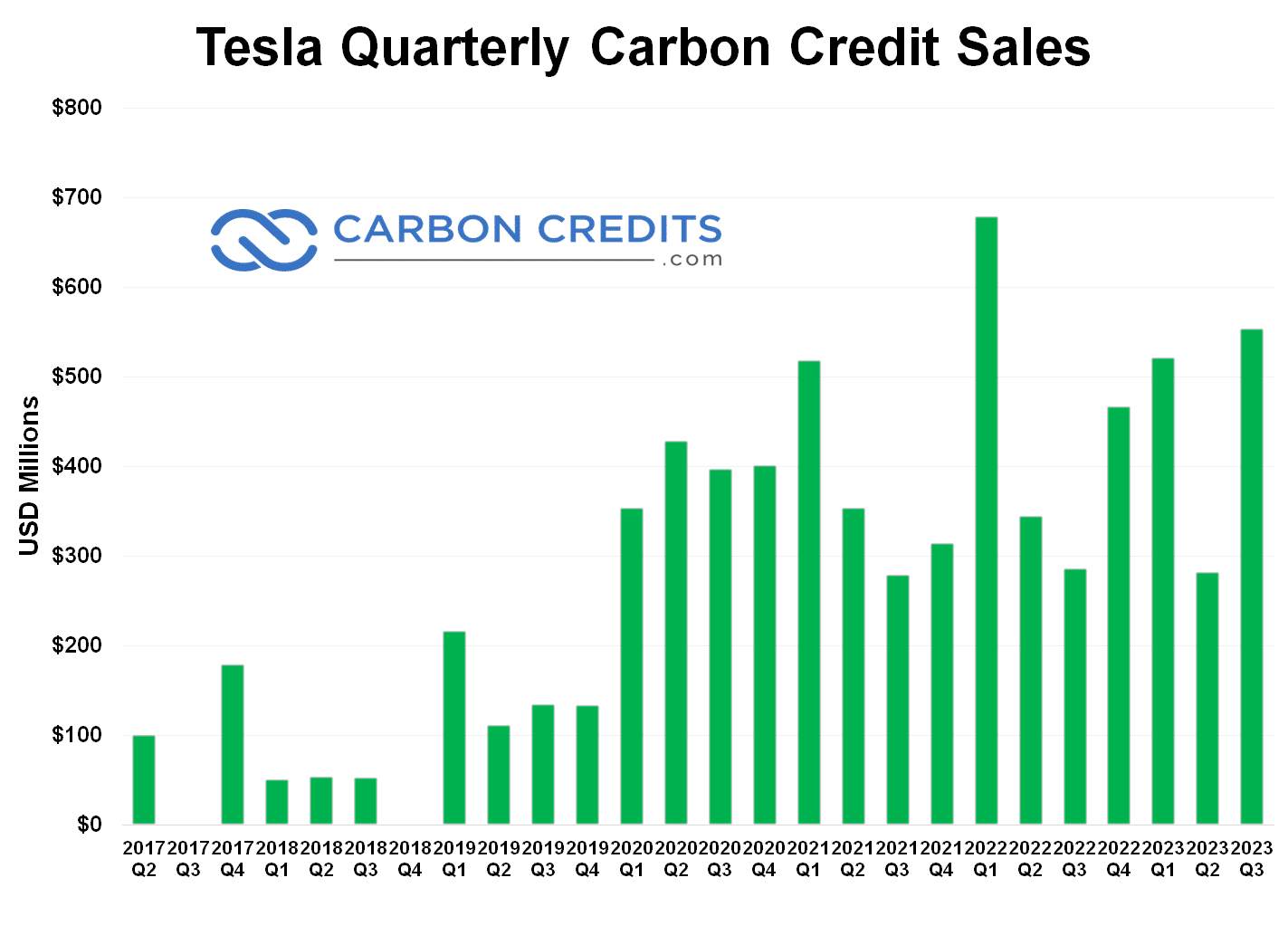

While Tesla has missed this year’s third quarter on both earnings and revenue expectations since its Q2 2019 report, the EV leader reported record-breaking carbon credit sales, which the company referred to as regulatory credits.

For over 4 years, the EV maker has been drawing attention by reporting record-breaking income from selling carbon credits. The automaker reported a revenue of $554 million from the Q3 2023 sale of carbon credits, significantly contributing to its profits.

This record sales also represented a huge portion of Tesla’s net income in Q3 2023 ($1,878 million) – 29%. Most notably, its quarter three carbon credit revenue increased 94% year-over-year, marking the value of Tesla’s EV production.

Tesla Carbon Credit Revenues Are Soaring

Tesla has been earning revenues from the sale of carbon credits since 2017. These credits, otherwise called carbon offset credits or carbon allowances, give companies a way to offset their carbon emissions by investing in projects that reduce planet-warming emissions.

Despite Elon Musk’s “paranoia” over the global economy’s instability due to ongoing wars, its soaring carbon credit income steadily contributes to its overall profits.

A 29% revenue-to-net income ratio is hard to ignore and speaks highly of the value of the credits for Tesla.

Compared to the previous quarter’s revenue ($282 million), this quarter saw a whopping 96% increase in sales at $554 million. By far, it’s the highest among Q3 revenues and is the second largest among Tesla’s quarterly credit sales.

First quarter 2022 has seen the highest income at $679 million, while the company also earned a total of $1.78 billion for that year alone.

It’s not clear who exactly bought the credits and for how much, but most likely they’re sold to other car companies that miss out on emissions standards of the California Air Resources Board (CARB).

Previous buyers include Tesla’s peers, General Motors and Chrysler, but this year’s purchasers were not disclosed.

The revenue generated from credit sales supports Tesla’s mission to accelerate the transition to cleaner energy and sustainable transportation. By incentivizing the adoption of EVs by other carmakers, carbon credits contribute to reducing carbon emissions in the sector.

Ramping Up Clean Energy Solutions

Producing and delivering more EVs is just one part of Tesla’s commitment to clean and sustainable energy transition. A consistently growing business segment of the carmaker is its lithium-based energy storage solution.

Though this segment is much smaller than its automotive business, it has expanded rapidly.

In its current quarter financial report, the company’s energy generation and storage revenue was also up about 40% year-over-year. The segment raked in $1,559 million in Q3 2023 revenue compared to $1,117 million in the same quarter last year.

Tesla also reported that its energy storage deployments hit a new record, up by 90% YoY to 4.0 GWh, the highest quarterly deployment ever.

The growth was mainly driven by the company’s ongoing ramping up of its Megafactory in California. Tesla aims to produce 10,000 Megapacks (energy storage for large-scale commercial and utilities projects) each year in this factory.

Other energy storage systems include Powerwall for residential and Powerpack for businesses, which all use lithium-ion batteries.

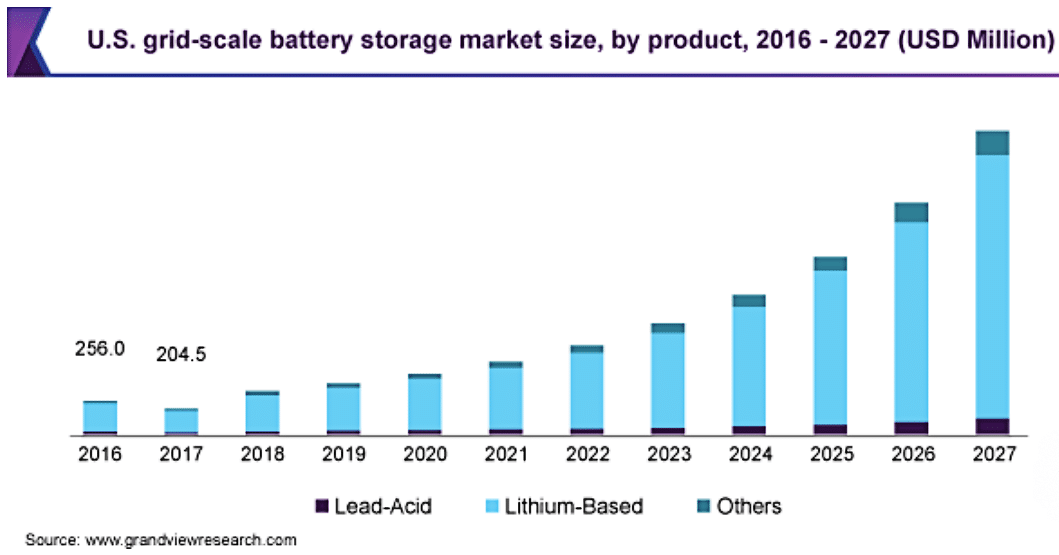

The growing demand for Tesla’s Megapacks signals that there’s a huge market for grid-scale battery energy storage solutions. Estimates project that this market will achieve over 24% growth rate through 2027 to more than $15 billion.

For Tesla Energy, that growth means its battery energy storage solutions like Megapack could see a significant market share. Musk even said that their battery storage segment is becoming one of Tesla’s most profitable divisions.

This growing business, along with its solar deployments, is a key part of the EV maker’s journey to sustainability.

More than Just a Carbon Credit Winner

Manufacturing EVs, deploying battery energy storage and solar panels all generate carbon credits by avoiding carbon emissions. The revenues that these credits bring are undeniably huge, giving Tesla billions of dollars in income.

But more than the cash, the increasing sales highlights the role of Tesla’s clean energy and sustainable solutions in reaching net zero targets.

Achieving a sustainable global economy entails curbing greenhouse gas emissions, which requires addressing both energy generation and use. Both areas are what the transportation and energy sectors are tackling to reduce harmful emissions.

Tesla is in an advantaged position to take charge in this quest by designing and implementing clean transportation and sustainable energy solutions.

The carmaker has been enhancing its manufacturing capabilities and employing advanced technologies to continuously improve its clean energy operations. The automotive giant is also working to slash its own carbon footprint as outlined in its sustainability paper.

Tesla’s remarkable success in carbon credit sales not only bolsters its financial standing but also underscores the significance of clean energy solutions in combating climate change. As the company advances its sustainable practices, it continues to pave the way toward net zero emissions.

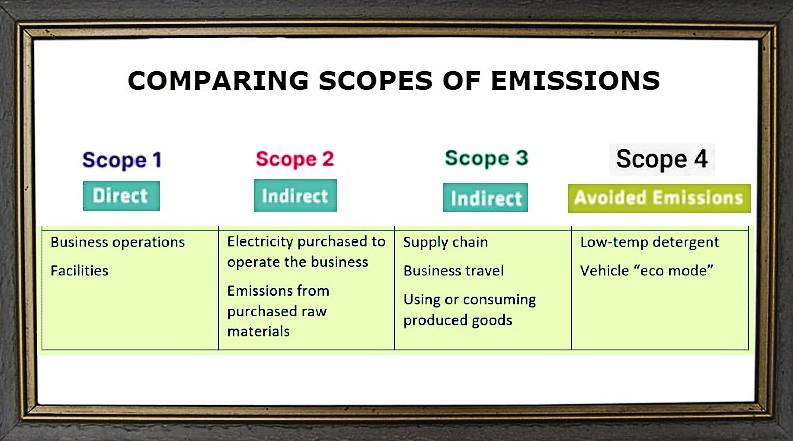

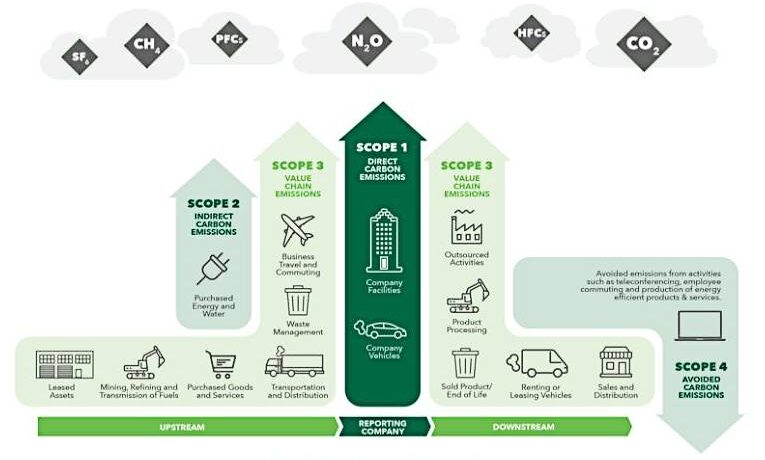

If you’re into carbon accounting, you probably have encountered scopes 1, 2, and 3 emissions used to determine a company’s carbon footprint and guide reductions efforts… but have you heard of Scope 4 emissions?

Most likely, not yet. That’s because Scope 4 emissions are an addition to emissions that companies need to keep track of.

While the concept is quite new, understanding it and knowing how to account for it is useful for companies and organizations wanting to curb their emissions and meet their climate goals.

So, we’re going to explain what Scope 4 emissions are, how they differ from the other scopes, why they’re important and beneficial for companies to measure and report, alongside the major challenges in calculating them.

What Are Scope 4 Emissions? How Do They Differ From Other Scopes?

To understand Scope 4 (S4) emissions, we need to differentiate them from its peers. Scope 1, Scope 2, and Scope 3 emissions refer to direct, indirect, and other indirect emissions, respectively.

Scope 1 emissions are from direct sources such as fuels burned to heat products or run a machine.

Scope 2 emissions are indirect footprint resulting from purchased energy used by the company such as electricity.

Scope 3 emissions refer to all other indirect emissions, such as embodied carbon of building materials and supply chain.

In other words, they’re what a company emits through their operations and other business activities.

Companies have full control over their Scope 1 and 2 emissions whereas Scope 3 emissions are generated by activities that the company can’t control.

Scope 4 emissions, on the other hand, refers to the AVOIDED emissions or carbon pollution that happen OUTSIDE of a product’s value chain. They’re a result of using that product or the saved emissions due to its performance.

Theoretically, S4 emissions provide companies a way to report on the avoided emissions by opting for more efficient products, either a product or a service.

For instance, telecommuting or carpooling to work saves on the carbon footprint of working. Likewise, decreasing energy consumption by using energy efficient equipment or appliances also cuts down carbon emissions.

At a glance, here’s how these different scope emissions differ from each other:

There are two main types of S4 emissions:

Product or service that replaces a more carbon-intensive product: e.g. tele-conferencing services that reduces the emissions of traveling to office.

Product or service that reduces emissions elsewhere: e.g. a low-temperature detergent that uses less energy.

Scope 4 emissions also cover work-from-home scenarios as they avoided using transport fuel and energy use in office work.

S4 emissions can be quite challenging to measure and report, but it’s becoming increasingly important for companies to do so. By fully understanding their Scope 4 emissions, businesses can identify areas where they can reduce their planet-warming emissions and contribute positively to climate change.

Why Should Companies Report Scope 4?

Most companies would like to account and report on their S4 emissions to gauge their efforts in helping their respective industry slash emissions.

In fact, 75% of the surveyed companies by the Carbon Disclosure Project (CDP) are offering products and services that help others reduce emissions. The caveat, however, is that without enough data to back up their claims, they remain unsubstantiated.

In other words, to validate their claim on reductions of a product/service, rigorous testing, predictions, and reporting is key. It also calls for scientific estimations or calculations on how consumers use a company’s product.

In principle, calculating avoided emissions needs extensive research and product development or improvement. In practice, though, it’s so much more difficult to make accurate calculations and substantiate claims.

That’s why accounting for S4 emissions right from the very beginning of making a product/service is crucial. It also sets a baseline from which to measure the avoided emissions.

Source: ESG Professionals Network

On the contrary, failing to consider these emissions may result in serious consequences for a company. Apart from a potential fine if a certain regulation is not met, the business may report its total emissions incorrectly.

More remarkably, incorporating avoided emissions the soonest time possible puts a company at an advantage compared to its peers. Currently, it’s not mandated to report on these emissions, but as governments started to become more stringent in regulating climate disclosures, companies who have their feet on this front will find it easier later on.

Existing Guidance or Framework for Reporting S4

Tracking and disclosing emissions under S4 can be tricky and there’s no standards available yet today. But if your company attempts to do it, there are some frameworks that can guide you.

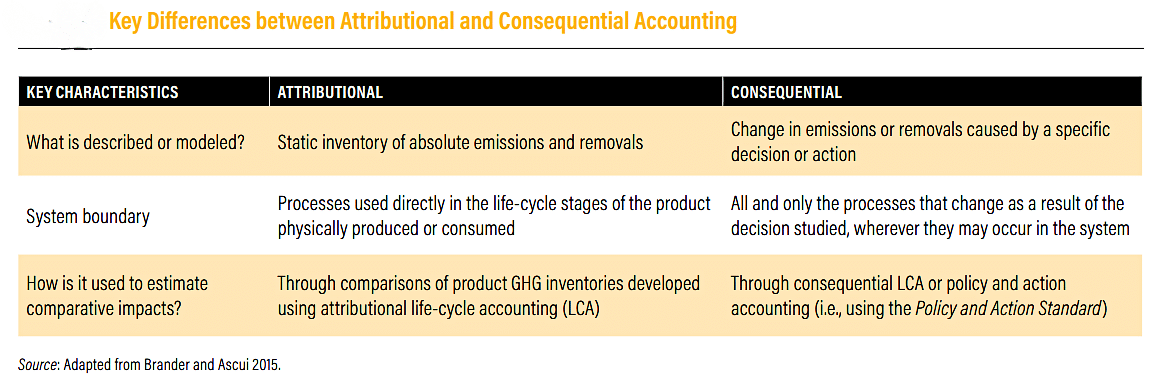

A good starting point is the World Resources Institute’s guideline entitled “Estimating and Reporting the Comparative Emissions Impacts of Products”. It may not be the most comprehensive framework but it helps in learning how to collect credible data for S4. It’s a sector-specific guidance for industry associations.

As the paper suggests, it’s a framework for estimating and disclosing the full impact of products. It includes guidance for accounting for a product’s negative and positive impact on emissions. This S4 accounting comes in two different approaches defined and compared in the table:

The framework also offers recommendations on how companies can improve the credibility and consistency of their claims. Companies can consider three common avoided emissions claims that the WRI specified:

Claims that compare avoided emissions of a product to its previous version,

Claims applying the benefits of a product’s S4 emissions to the whole market to measure emissions, and

Claims resulting from comparing emissions of various products.

One of the recommendations of WRI in using their guidelines is for companies to measure emissions from every stage of the product’s life cycle for correct representation of how it compares to the previous product.

Another supplemental guideline is the GHG Protocol’s Policy and Action Standard. The GHG Protocol is also developed by the WRI. Though the standard seems to be more general, it suggests that reporting companies consider how their products will change emissions.

By using these frameworks and approaches, you can more effectively measure and reduce your company’s Scope 4 emissions.

However, given that S4 emissions are outside of your company’s value chain, capturing it comes with some hurdles.

Key Challenges and Limitations in Disclosing Scope 4

Reporting on S4 emissions entails overthrowing some roadblocks along the way. Let’s enumerate and explain the main challenges you may encounter along the way.

Difficulties in Measuring S4

To measure scope 4 emissions accurately, companies must validate that their offerings really do avoid emissions. This entails a lot of resources from start to end of the validation process. The most difficult part is estimating on how customers use and dispose of the product.

Not to mention that it may involve complicated assumptions and calculations, calling for extra market research.

For instance, the company has to know how many consumers were using the older product and whether they’ll replace it with the new version. Incorrect data collected would be very bad if used as a basis for decision making related to the product.

Quantifying Avoidance is Complicated

Measurement is one thing and quantifying avoidance is another thing. But they’re both hard to come by accurately. Take for example the case of selling second hand items like bags or shoes. The seller can assume that their second hand products can avoid buying new items.

But what this assumption may use to consider is that consumers may buy more than one of their items. That’s simply because they’re cheaper to buy, so they can buy more. The seller has to factor all these things when quantifying for the product’s avoided emissions.

Quantifying Avoidance is Complicated

As mentioned earlier, researching, developing and testing new products needs plenty of resources. In other words, companies may have to invest big for the upfront costs. But this should not discourage them to make new and innovative products that can actually reduce emissions.

No Widely Accepted Standard

While there are some guidelines available relating to Scope 4 or avoided emissions, there’s still no widely accepted standard. This lack of standardization further makes it more challenging what to follow when measuring and reporting S4. But the WRI framework would be a good way to start on this climate disclosure quest.

Accusation for False Claims

All the previous hurdles above boil down to one thing that companies all fear to face – greenwashing. Inaccurate data or overestimations of avoided emissions will likely put the company in the spotlight for scrutiny.

Climate activists are even more vigilant today as planet-warming emissions continue to cause disasters and damages worldwide. Being subject to greenwashing accusations would damage the stakeholder’s trust, including customers and investors.

Now, we’ve come to the last question you may have – how to calculate and report S4? That depends on the specific industry you’re in. Let’s take a look at some examples.

How Can Industries Calculate and Report S4?

Companies operating in the real estate industry can measure their S4 by measuring tenant commuting footprint. They can do that either by sourcing data from transportation apps or directly asking or surveying their tenants. They may also factor in waste diversion rates to account for avoided emissions.

If you’re into a retail business, you can calculate the environmental footprint of your products using life cycle assessments. This approach takes into account avoided emissions in the supply chain.

It’s different if you have a manufacturing company. You can measure Scope 4 emissions through energy efficiency initiatives and process improvements.

Specifically, if a company is manufacturing capital goods, they can follow the example of French multinational company Schneider Electric. Schneider specializes in digital automation and energy management, making it easier for them to provide examples of calculation of avoided emissions via their variable speed drives, which generate savings on energy consumed by using their VSD.

For instance, in one of Schneider’s reports, it showed that its EcoStruxure Industrial Internet of Things platform enabled customers to save a whopping 134 million metric tonnes of CO2 since 2018. That avoided emissions equal to the footprint of over 28 million gas-powered passenger cars driven for a year.

If you’re running a business in the hospitality industry, you can consider transportation emissions, such as shuttle services. You can also convince guests to reduce their own footprint while using your facilities and amenities.

Here’s a sample calculation of various emissions, including scope 4 by the Thunder Said Energy.

After getting all the Scope 1, 2, and 3 emissions, they deduct the S4 emissions that are avoided by using the energy product compared with the most likely counterpart.

Why Get Started With Scope 4?

Disclosing S4 emissions is voluntary; it doesn’t count towards a company’s total emissions reductions. It remains a theoretical estimation using a reference scenario.

Avoided emissions also is in its nascent stage but improving transparency and standardizing measurement methods will drive value to investors.

The calculation of this metric enables companies to determine how capable their product is in helping decarbonize their business. Taking into account Scope 4 disclosures makes sense from a decarbonization perspective. It can also provide financial insight as it reveals the real added value a business is making toward its sustainability agenda.

Ultimately, while carbon accounting including all scopes of emissions won’t be an easy task, it’s essential to guide companies, their investors, and other stakeholders to better understand how they are progressing towards their climate and corporate sustainability goals.

Partanna Global has built the world’s first climate-resilient, carbon-negative ‘Home for the World’ in the Bahamas, marking a new breakthrough in sustainable housing.

Partanna is a sustainable building materials startup founded by NBA Lakers legend and actor Rick Fox in 2021, together with Sam Marshall.

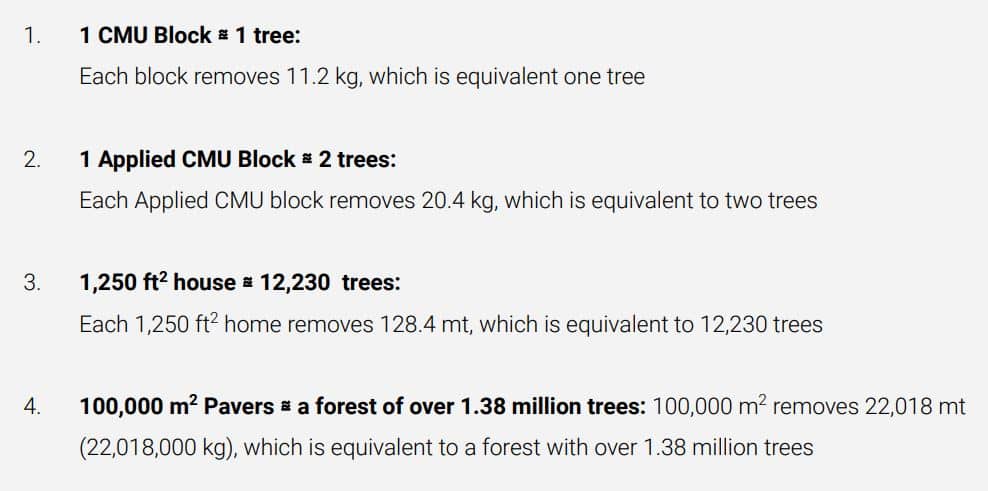

The groundbreaking 1,250 square-foot house in the Bahamas actively eliminates and prevents 182.6 metric tons of CO2. That amount is equivalent to the annual carbon intake of 5,200 mature trees, contrasting sharply with the 70.2 tons of CO2 emitted by a typical concrete-built home during production.

Partanna’s ‘Home for the World’

The built environment is responsible for around 40% of the world’s annual greenhouse gas emissions significantly contributing to climate change. And concrete happens to be the major choice of today’s modern homes.

The main culprit is cement, a main ingredient in concrete mix that’s responsible for over 8% of CO2 emissions globally. Thus, various initiatives have been introduced to make alternative sustainable building materials to traditional concrete.

Apart from Partanna, other startups are also working to suck in carbon from the air and lock it in concrete. For example, a California-based company C-Crete is making a cement-free, carbon-negative concrete.

But what makes Partanna’s technology unique is the fact that they’re using slag and brine instead of cement. They are waste materials the company takes from energy-intensive steel and desalination facilities.

Moreover, the company said that their concrete mix cures at ambient temperatures, further lowering energy use. That makes Partanna’s building material production capable of reducing both energy costs and carbon emissions.

Plus, the material’s curing process called ‘carbonation’ further removes carbon from the air just like a tree does. When standing in a house or any building, the material continues to draw in carbon from the air.

The company said that a 1,250 sq. ft. home can remove 130 Mt of CO2 and avoid another 54 Mt. Therefore, the total avoided and removed CO2 per house stands at around 184 Mt.

Partanna’s standard concrete masonry unit, CMU, block is 25% stronger than traditional CMU.

Most remarkably, their binder ingredient makes the concrete even stronger when exposed to seawater – exactly what houses in the low-lying islands in the Bahamas need to weather the storms and sea level rise.

The carbon negative ‘Home for the World’ in Nassau is designed and built to do just that.

Changing the Way the World Builds

Partanna’s prototype home is the first of 1,000 planned homes announced in partnership with the Bahamian government last year. Their deal came after hurricane Dorian devastated Fox’s home country in 2020, severely impacting 29,500 people.

After their agreement’s announcement, Richard Branson’s Caribbean Climate-Smart Accelerator (CCSA) also partnered with Partanna in February this year to develop the world’s first carbon negative housing community.

CCSA’s goal is to build resilient nations, cities, and industries across the Caribbean, and create the world’s first climate-smart zone.

The billionaire’s non-profit finds Partanna’s innovation a sustainable housing solution in a country at the frontline of the climate crisis. The CCSA will help the Bahamian startup realize its mission by identifying public and private collaborations in the region.

Remarking on their first build, Fox noted that the need to disentangle development from pollution has never been more urgent. He also said that:

“The world is forecast to build an area equivalent to the size of The Bahamas every three years… Our ‘Home for the World’ is the answer to this challenge, and The Bahamas is the symbolic birthplace for our movement to change the way the world builds – for good.”

Resilience in the Face of Climate Change

Prime Minister and Minister of Finance of The Bahamas, Hon. Philip Davis praised Partanna’s innovative approach to the climate crisis. He highlighted the essential role of climate-resilient solutions for the disaster-stricken nation and in fighting global warming.

Nobody lives in their prototype carbon-negative home yet, but the next houses will be livable for first-time homeowners. Their initiative aims to build 29 more homes by 2024. Details on this development will be early next year.

Bringing a sustainable housing solution is a part of Partanna Global’s mission. But apart from that, the company is also complying with the global standards for construction material by securing prestigious certifications.

Not to mention that its carbon-negative concrete boats excellent strength, exceeding its traditional peers. If their pilot construction in the Bahamas turns out a success, they’re planning to expand production into the United States.

Their goal is to make their climate-friendly concrete a mainstream material that can address both the global housing demand and carbon emission reductions goals. They’re continuing the hunt for strategic partners to revolutionize large-scale developments worldwide.

The world’s largest carbon crediting program, Verra, approved Partanna and its carbon removal to be listed on its VCS registry.

Partanna’s carbon reduction or avoidance are the first verified carbon-absorbing building materials to generate carbon credits. Each credit represents a metric ton of avoided or removed CO2.

Given the escalating impact of extreme weather events and rising sea levels, Partanna’s unique construction material, fortified by brine, offers a sturdy and sustainable alternative, particularly beneficial for regions, like the Caribbean, vulnerable to climate-related hazards.

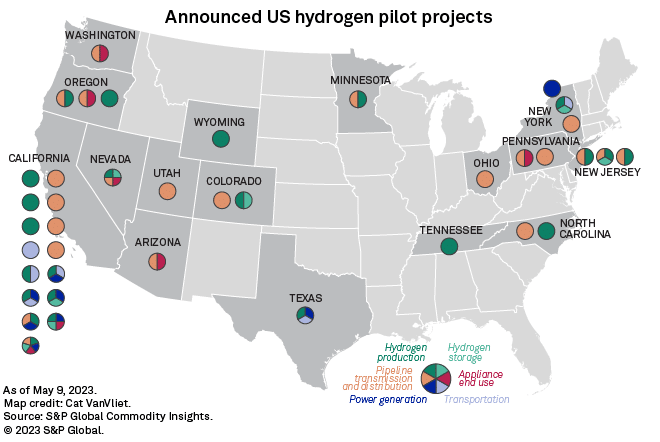

First Hydrogen Corp. (TSXV: FHYD) (OTC: FHYDF) (FSE: FIT) announced that it will be hosting its first ever track day for major UK fleet managers to demonstrate its unique hydrogen fuel cell vehicles (FCEV).

The event, which will take place at the end of October, will also be a test drive for the First Hydrogen’s FCEVs on the track at HORIBA MIRA, UK. All attendees will get hands-on access to the first-of-their-kind 3.5-tonne FCEV and the chance to drive them. They will also gain knowledge on how practical it would be to introduce the FCEV into their own fleets.

This invitation-only event targets major UK LCV fleet operators including members of the UK Aggregated Hydrogen Freight Consortium (AHFC) that promotes ramping up commercialization of FCEVs and hydrogen refueling infrastructure.

First Hydrogen’s FCEV has already been trialed by SSE and Rivus, with over 15 others on the waiting list to test the vehicle in their fleets. The inaugural track allows the company to showcase its FCEV’s unmatched capabilities to several organizations in a day.

That includes an impressive range of over 630km on a single refueling, ease of driving, and carrying huge payloads without trading off performance.

First Hydrogen Automotive CEO, Steve Gill, remarked that their goal for the event is for “attending fleet managers and operational specialists to leave with a clearer view on the capabilities of First Hydrogen’s FCEVs which will inform decision making on the purchase of zero emissions fleets”.

If the event turns out a success, First Hydrogen aims to take their FCEV into Europe and North America in similar track events.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: FHYD.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

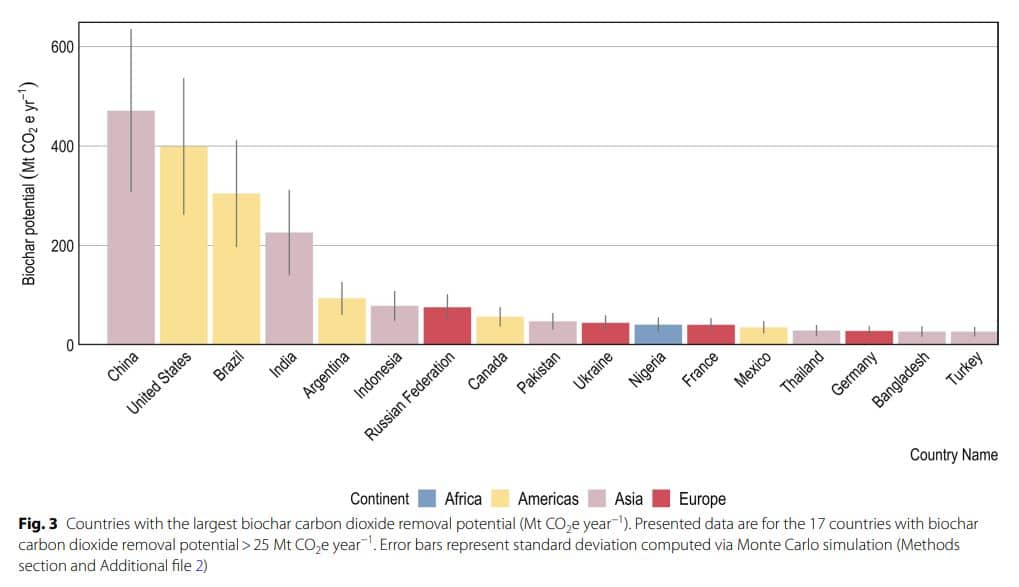

Groundbreaking research highlights the potential of biochar as a solution for scaling carbon removal, benefiting both the environment and people. Biochar has the capacity to remove a significant portion of global emissions, providing a win-win solution for addressing climate change.

Developed thousands of years ago, biochar is a material made by heating organic matter like crop residues that would otherwise emit greenhouse gasses when decaying. By turning these organic materials into biochar, carbon gets trapped for hundreds to thousands of years.

Biochar does not only mitigate climate change but also enhances soil health, water retention, and nutrient levels, helping communities adapt to climate change’s effects.

Biochar’s Topnotch Removal Ability

Hailed as “nature’s black gold”, biochar has been building momentum yet growth is slow due to lacking attention and investment. But a new research reiterates the importance of this ancient farming practice in offering an accelerated pathway toward global decarbonization.

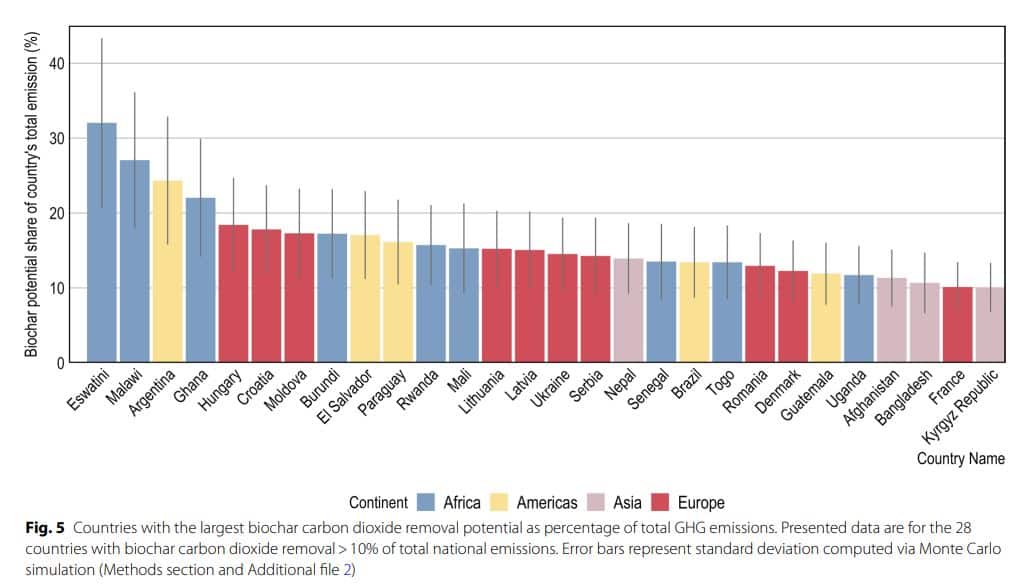

According to the peer-reviewed study, biochar has the potential to remove up to 6% of global emissions each year. This equates to about 3 billion tonnes of CO2, equivalent to the emissions of 803 coal-fired power plants a year.

Moreover, biochar offers a minimum removal potential of 10% in 25+ countries, primarily in Africa, South America, and Eastern Europe. Notably, it can cut down CO2 emissions by >30% in Eswatini and >20% in Malawi, Argentina, and Ghana. This potential is relative to the country’s total emissions as represented in the chart.

The world’s major emitters, including China, the United States, Brazil, and India, have the largest potential to lead the way in sustainable emissions reductions using biochar. Other countries with high biochar removal potential are shown below.

Quantifying Biochar’s Role in Climate Action

The study, published in the peer-reviewed journal Biochar and commissioned by the International Biochar Initiative (IBI), quantifies biochar’s carbon removal potential across 155 countries.

The results highlight biochar as an affordable, scalable, and readily available solution that also provides environmental and social co-benefits. Improved soil health and increased crop yields are among the various benefits of using biochar as a soil amendment.

Remarking on this breakthrough discovery, Dr. Thomas Trabold, co-author and research professor at the Rochester Institute of Technology said that:

“This is the first research to quantify the significant role biochar can play in worldwide climate action and carbon removal strategies… To scale biochar to its full potential, we now have a starting point of what is possible at the country level.”

The study findings also showed biochar’s relevance to small-emitting countries, which is particularly significant. It offers a sustainable approach to their climate change mitigation efforts.

While these countries are the least responsible for climate change, they’re disproportionately experiencing the impacts, from extreme drought to floods. Through biochar, they can maximize carbon removal while increasing national and local revenues, promoting sustainable agriculture, and providing employment opportunities.

For farmers encountering climate change issues, biochar would be particularly a game-changing solution.

Despite being referred to as “nature’s black gold,” biochar has faced historical challenges in terms of attention and investment. Addressing these bottlenecks requires collaboration at all levels to accelerate investment and amplify demand for biochar on a global scale.

A Call to Action

Recent developments in the industry are showing a promising outlook for this technology.

For instance, a leading carbon rating agency, BeZero Carbon, has given its first Biochar project the rare “A” rating. That means the project has a high likelihood of avoiding or removing 1 tonne of CO2.

This development signifies the maturation of carbon removal and particularly biochar, which accounts for >90% of all removal deliveries.

Moreover, a Canadian biochar producer has raised $38 million to expand production of this carbon removal technology. The company plans to produce biochar from compost or residual matters from municipalities.

With the upcoming international climate change conference, COP28, this scientific study serves as a compelling call to action for world leaders to consider biochar in their decarbonization strategies.

Biochar’s ability to sequester carbon while providing other benefits makes it a critical component of the climate change toolbox. It could be the time to accelerate its use to stay on a 1.5°C pathway.

Contrary to the instant fun it provides, the gaming industry has been slow to acknowledge that developing and playing video games uses a lot of energy and generates emissions responsible for climate change. A researcher revealed the gaming industry’s carbon footprint, standing at over 81 million tonnes of emissions in 2022.

Dr. Benjamin Abraham, a digital games researcher and founder of AfterClimate, closely evaluates how the gaming industry tackles climate change. He publishes an annual progress report on the industry’s net zero ambitions in his ‘Net Zero Snapshot 2023’.

The Gaming Industry’s Carbon Footprint

Abraham estimates that the $180+ billion video game industry consumes energy and produces carbon emissions comparable to the global film industry.

His conservative estimates revealed that the gaming industry’s carbon footprint stands at 81 million tonnes of CO2, but it doesn’t specifically break down how much is emitted by video gaming alone. The estimation shows how much video games and the big tech companies emitted last year, which is even larger than what many small countries emit.

The data included 35+ global games and tech companies, with around $1.2 trillion in revenues in 2022. Tencent, Microsoft, Apple, Sony, and Google account for the majority of the total emissions.

Taking those 5 big tech companies out of the equation, the other companies reported >7 million tonnes in 2022. Including the absolute minimum of the total emissions of companies that didn’t disclose data, the researcher estimated >14 million tonnes of CO2.

Thus, video game companies alone were responsible for these carbon emissions, about 14 Mt CO2. That amount is about the same as what the country of Estonia emitted in 2021.

The analysis didn’t even account for other sources of emissions, particularly falling under Scope 3 emissions. These include activities outside the video game companies’ or developers’ control, such as manufacturing consoles and computer hardware, powering servers, and flying developers or executives for meetings and conferences.

One of the most notable findings in Abraham’s 2023 report is that the gaming industry’s carbon emissions were up globally. Out of the 34 largest game companies, only 3 were able to reduce their carbon footprint in 2022.

Tencent – 13.73% down

Apple – 11% down

Nintendo – 2.95% down

What Video Game Companies Are Missing Out

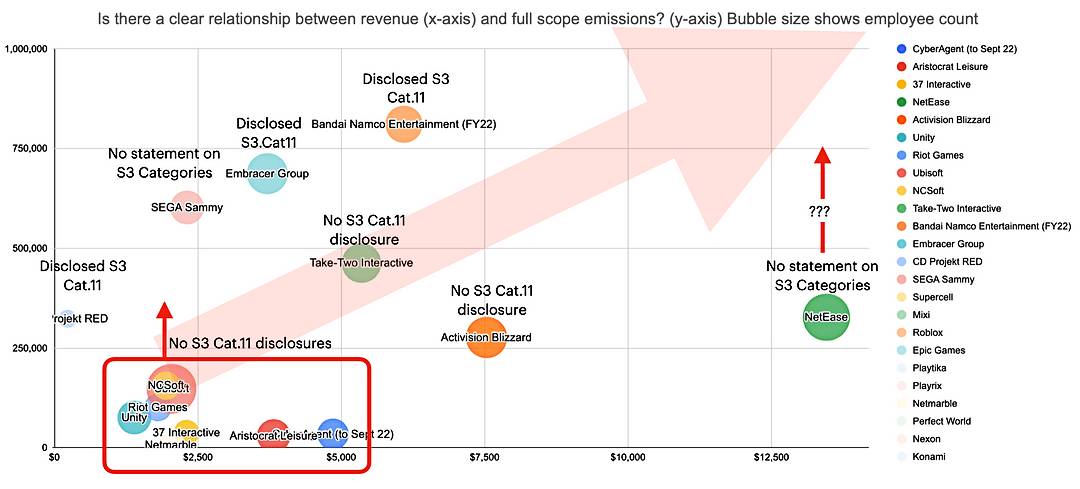

The report also highlighted a more secretive issue in the industry – most companies aren’t diligent at disclosing Scope 3 emissions. “Use of sold products” emissions, which fall under Category 11 of the GHG Protocol, is specifically missing. That includes energy from the use of a gaming device, such as Xbox or PlayStation, or a computer or smartphone.

Gamers generate Scope 3 emissions, which account for about 10-90% of the total Scope 3. Let’s take the example of Ubisoft, one of the world’s largest game studios. Of the company’s total annual CO2 emissions, only as much as 10% is from their direct operations. The remaining footprint breaks down to 10-15% for game distribution, 40% for game device production, and 40% for gamers.

Microsoft estimates that the average gamer using a high-performance gaming device emits 72 kilograms of CO2 per year. In the United States, gamers emit 24 million tons of CO2 each year, data according to Project Drawdown. Globally, 3+ billion people, or 40% of the world’s population, are playing video games.

For other companies, Scope 3 is most often not included in disclosures as they’re not mandatory, only optional, for now.

The extent of Scope 3 disclosures. Source: AfterClimate Game Industry Net Zero 2023 Snapshot

The 2023 snapshot suggests that video game companies are still not up to the standards of disclosing their emissions data as shown above. However, there has been a significant shift in the industry’s approach to the climate crisis in the recent years.

What Sustainable Game Leaders Are Doing

Reports show a growing number of video game developers who take into account the climate impact of their games. Indie video game developers, in particular, are taking the matter into their own hands. They advocate for a more sustainable game development that reduces their impact on the planet.

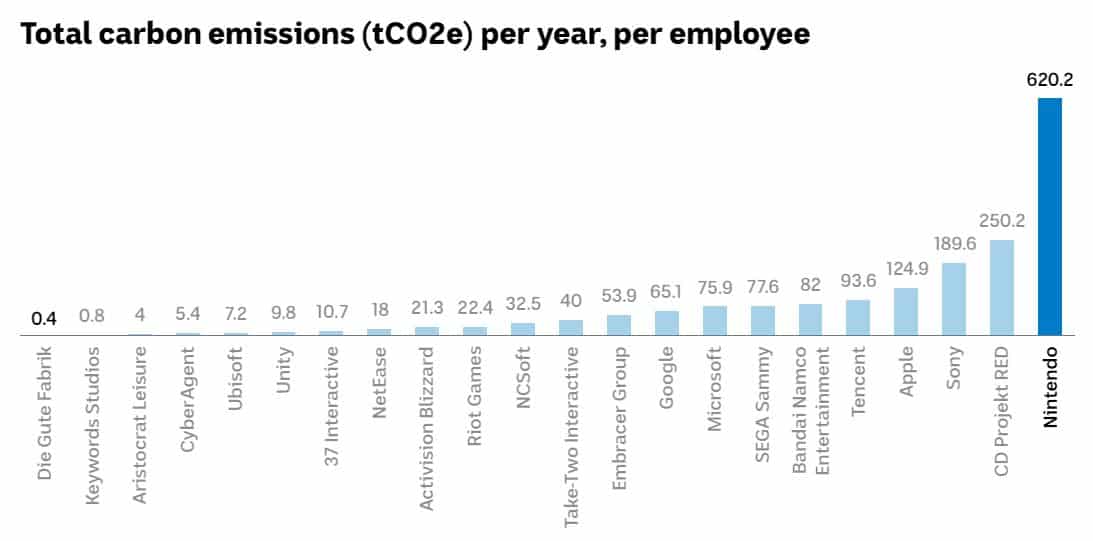

For instance, indie game developers like Hannah Nicklin of Die Gute Fabrik studio, are proactively accounting for their carbon footprint. By doing so, the developer is providing the gaming community some ways to tackle their carbon footprint, which is crucial to bringing the industry to net zero, Dr. Abraham said. He particularly noted that:

“As more and more businesses start to do this, it starts to have this amplification effect on the whole industry where we just set this expectation that, yes, we’re going to pay attention to our emissions.”

Nicklin’s indie gaming studio emitted only about 47 tonnes of CO2 per year per employee. This figure represents only 0.000058% of the total emissions of the largest game companies worldwide.

Each of those big companies have set their own net zero emissions targets, employing different strategies. Some are opting for offsetting or buying clean energy credits to negate their fossil fuel consumption. Microsoft and Apple, in particular, are investing significantly in carbon removals to offset their emissions.

But they’re also proactively innovating how they can reduce their gaming emissions directly.

For example, Microsoft developed the Xbox Developer Sustainability Toolkit that guides developers to clean up the game’s performance and look for areas for energy savings. Decreasing resolution and frames-per-second in pause screens or menus could save up up to 55% of energy use.

Other gaming companies like Nintendo and Sony had also expressed intent to reduce their carbon emissions. But their sustainability and net zero pledges lack specific strategies on how they’re going to address video game related footprint.

Despite the gaming industry’s significant carbon emissions, recent initiatives by independent developers and major companies signal a promising shift towards more sustainable practices. This development underscores the need for greater transparency and concerted action to address the industry’s environmental impact.

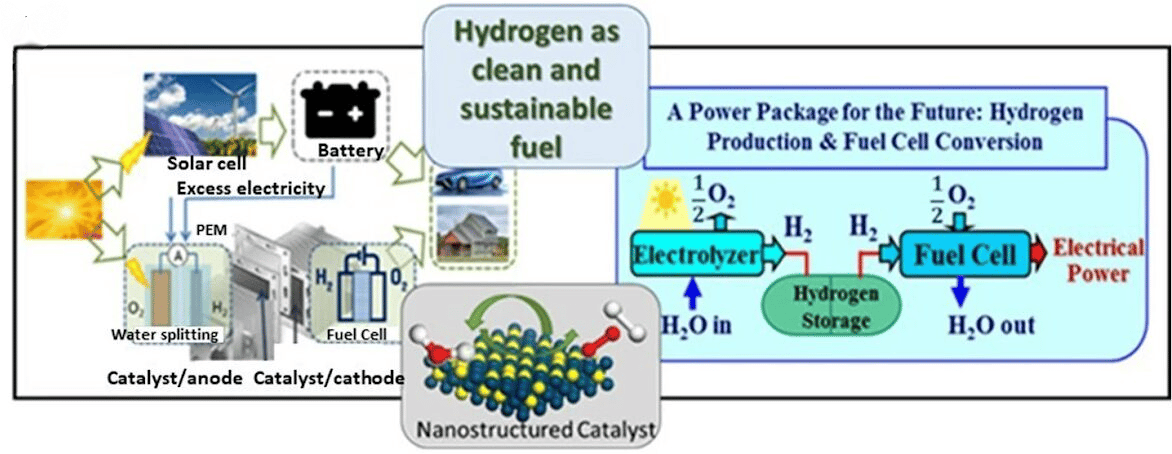

In the race toward a sustainable future, hydrogen has emerged as a star player in the global clean energy transition. Among the companies embracing this transformative shift are NiSource Inc. and Sempra Energy, which are taking proactive steps to harness the potential of hydrogen as a key driver of a greener energy landscape.

NiSource just launched a multi-phase hydrogen blending project; it’s a pioneering project in the U.S. to use a blending skid in a controlled environment to combine natural gas and hydrogen at precise levels. The goal is to find out the best blend percentages and their benefits for consumers and the planet.

Taking the same direction, San Diego-based Sempra Energy, will also test electrolytic hydrogen blending into existing natural gas infrastructure. The energy giant is also working on what could be the nation’s largest green hydrogen energy infrastructure system.

NiSource Hydrogen and Natural Gas Blending

NiSource envisions the potential for substantial investments in hydrogen production, transportation, and storage. It comes following the conclusion of its current five-year $15 billion capital plan in 2027.

To make that vision a reality, NiSource is developing its capacity to handle hydrogen safely and efficiently. It also seeks to show to policymakers that low-carbon hydrogen can effectively decarbonize gas utility services.

Several hydrogen projects have been announced in the U.S., encompassing different areas of application.

NiSource pilot project, led by its subsidiary Columbia Gas of Pennsylvania Inc., will test a 20% hydrogen blend in natural gas distribution infrastructure. It facilitates the regulated blending of hydrogen into Safety Town’s natural gas system at varying concentrations.

The results of this project to be tested in Monaca, Pennsylvania will be key to demonstrate that hydrogen blending is feasible. The project is a collaboration between NiSource’s Columbia Gas and EN Engineering.

Together, they’ll create a blending skid that will inject hydrogen into the gas stream at different percentages, from 2% – 20%.

The project will also assess the impact of various blending concentrations on different gas appliances through a model home. The goal is to ensure the proper functioning of equipment and to know if any adjustments on processes are necessary.

NiSource prioritizes safety and regulatory compliance in hydrogen blending. They will share data with the US Pipeline and Hazardous Materials Safety Administration for monitoring hydrogen-gas blends and their impact on pipeline materials.

Moreover, its other subsidiary, Northern Indiana Public Service Co. LLC (NIPSCO), plans to use a blend of gas and hydrogen to repower one of its turbines.

An Alternative to Electrification

In all these innovations, CEO Lloyd Yates emphasizes the importance of policies in incentivizing efforts driving the hydrogen transition.

He specified some federal tax credits and initiatives such as the Appalachian Regional Clean Hydrogen Hub (ARCH2). NiSource backed this application to secure a subsidy from the Energy Department’s funding program on setting up regional hydrogen hubs.

The Indiana-based utility aims to achieve net zero Scope 1 and 2 emissions by 2040. Hydrogen blending can further help the company tackle its elusive Scope 3 emissions, which are linked to customer’s gas use. Burning hydrogen as a fuel emits only water vapor, no greenhouse gasses given that it uses renewable sources.

NiSource said its hydrogen and natural gas blending strategy is part of their “Future of Energy” program. It particularly includes renewable energy and electrification strategies as well as renewable natural gas pathways.

Yates further noted that the project seeks to make hydrogen an alternative to electrification for customers facing financial challenges. It will allow them to reduce their carbon emissions without buying new appliances, thus making it a viable option.

Along with NiSource, other utilities like Sempra Energy are also exploring hydrogen projects to meet the nation’s clean energy goals.

With a strong focus on sustainability, Sempra pursues >20 hydrogen R&D projects to enhance grid resilience and promote decarbonization. It works with strategic research partners while providing funding worth $140 million in the last 2 years.

In particular, Sempra’s subsidiary Southern California Gas Co. (SoCalGas) partners with the University of California, Irvine on a demonstration project. They aim to show how electrolytic hydrogen can be safely mixed into the campus’ existing natural gas pipeline. Testing for this hydrogen-natural gas blending may start next year once approved.

The joint initiative aims to better understand how hydrogen could be delivered at scale through California’s existing natural gas system. It can either be for existing customers tapping at the grid or to produce clean electricity in zero-emissions fuel cells.

The testing project will use an electrolyzer to convert water into hydrogen for blending into the UCI campus gas grid. It will involve powering residential and light commercial equipment such as ovens, boilers, furnaces, and water heaters.

Water Electrolysis Method

Initially, SoCalGas will use 5% hydrogen in the mix, aiming for up to 20%, the same as NiSource’s blending project. The ultimate goal is to also significantly reduce customer’s emissions from gas use.

The Missing Link in the Clean Energy Equation

SoCalGas announced its goal to reach net zero greenhouse gas emissions by 2045. That makes it the first large natural gas utility in the country to do so. Its parent company, Sempra, pledged to achieve net zero emissions 5 years later, by 2050.

The energy firm also proposed the Angeles Link, which could be the country’s largest green hydrogen energy infrastructure system. They refer to it as the missing link in the clean energy equation.

The initiative can potentially deliver cleaner energy to hard-to-electrify sectors such as heavy-duty transportation and industrial processes.

By replacing fossil fuel-powered trucks with hydrogen fuel cell trucks, Sempra Energy aims to eliminate up to 3 million gallons of diesel a day. This would result in displacing about 25,000 tons of carbon emissions each year.

First Hydrogen(TSXV: FHYD), a Vancouver and London-based company, specializes in zero-emission hydrogen fuel cell vehicles (FCEV) and green hydrogen production. Its innovation is a testament that FCEV works, with trial results beating test expectations.

NiSource and Sempra Energy’s initiatives in hydrogen blending exemplify their commitment to a sustainable energy future, reducing emissions while ensuring affordable and accessible solutions for consumers. If their efforts turn out successfully, they can show the significance of hydrogen in the clean energy transition.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: FHYD.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.