The United Nations (UN) has achieved a significant milestone by unanimously approving the Biodiversity Beyond National Jurisdiction Treaty (BBNJ), commonly known as the High Seas Treaty.

About 2/3 of the planet’s oceans lie beyond national boundaries in an area called the high seas. But only about 1% of this unexplored expanse has been protected. And so, the BBNJ came about.

The groundbreaking international agreement marks the first-ever legally binding framework governing activities on the high seas. The ultimate goal is to protect the environment and prevent disputes over natural resources and shipping.

Here are 7 key takeaways from the High Seas Treaty announcement:

High Seas Treaty: The UN member states have adopted the BBNJ Treaty. It establishes rules to safeguard the environment and address critical issues in areas beyond national jurisdiction.

Protection of Biodiversity: The treaty promotes the establishment of Marine Protected Areas (MPAs) in the high seas to counteract biodiversity loss caused by climate change impacts, overfishing, pollution, and other harmful activities.

Regulation of High Seas Activities: The treaty sets standards and guidelines to assess the environmental impact of high seas activities. These particularly include deep-sea mining, ensuring the preservation of marine life and ecosystems.

Compliance and Enforcement: The treaty creates a Conference of Parties (COP) responsible for monitoring and enforcing compliance with its terms. Additionally, a scientific advisory board will provide guidance based on scientific research.

Technology Transfer and Resource Sharing: The treaty incorporates a mechanism to facilitate the transfer of marine technology to developing countries. This is to ensure equitable sharing of benefits and resources from the high seas. This includes groundbreaking advancements in medical and nutrition science.

Implications for Climate Change: The high seas play a crucial role in regulating the climate by absorbing carbon dioxide and excess heat from the atmosphere, as well as driving global weather patterns. Protecting the high seas contributes to mitigating climate change impacts.

Ratification Process: The treaty requires individual ratification by at least 60 UN member nations before it can enter into force. The aim is to achieve this by the next UN Ocean Conference in June 2025 in Nice, France.

The UN’s adoption of the High Seas Treaty represents a significant step towards protecting the environment and ensuring sustainable management of the high seas.

The groundbreaking agreement establishes guidelines for the preservation of biodiversity, regulation of high seas activities, and equitable sharing of resources.

As the world continues to experience out-of-this-world disasters, polluters are under more fire to help clean up the planet-warming carbon they dump into the air. As they do that, more people are asking what carbon credits are, how they work, and what role they’ve got in fighting the climate crisis.

Many believe that they are instrumental in promoting both corporate sustainability and global sustainable development.

Others think that carbon credits can help companies meet their climate goals by reducing emissions and advancing sustainable business practices.

Yet, some consider them as a greenwashing tool for some reason…

…But many more find them an essential market mechanism to help reverse the effects of climate change.

Regardless of the different views on carbon credits, getting them explained in this article will help clarify things and answer your most pertinent questions about them.

What are Carbon Credits?

The idea behind carbon credits is to put a price on carbon emissions. The goal? To incentivize emitters to pollute less, ideally.

In essence, carbon credits serve as permits to emit a certain amount of carbon. These permits are tradable in carbon markets. These markets turn CO2 emissions into a commodity by giving them a price.

International carbon trading markets have been around since the 1997 Kyoto Protocols. But the new regional markets have prompted a surge of investment.

The world has seen billions of metric tons (Mt) of CO2 pumped into the air every year. In 2022, around 41 billion Mt of greenhouse gasses were emitted, up from 36 billion Mt in 2016. These gasses are the ones to blame for the earth’s rising temperatures.

So, if we want to stop the planet from heating up more, we need some solutions up our sleeves. And yes, carbon credits are one of them. But how do they work in fighting climate change?

How Do Carbon Credits Work?

One carbon credit represents one tonne of CO2 or its equivalent (CO2e) gas that an organization can emit.

It’s important at this point to say that carbon credits are often referred to as carbon offsets. While they’re very similar, they’re not the same.

Carbon credits, also known as carbon allowances, work like permission slips for emissions. You can think of them as a unit of measurement for CO2e emissions that have a tradable element.

The number of credits issued to a company corresponds to its emissions limit or “cap” set by a regulatory body. So, they’re also called a “cap and trade” system.

If that company doesn’t go above its cap, then it will have excess carbon credits which they can sell in the compliance carbon market regulated by the government. But if the company goes beyond the limit, it can turn to the carbon market to buy the required carbon credits.

In short, the governing organization creates carbon credits and allocates them to individual companies within that jurisdiction. Over-emitters buy carbon credits from under-emitters.

On the other hand, carbon offsets (also called carbon offset credits) are from projects or initiatives that reduce or remove carbon emissions.

Carbon reduction projects generally fall into two types: nature-based and technology-based.

Nature-based solutions usually include reforestation and wetland restoration projects. They naturally sequester carbon in the environment.

Technology-based projects often involve investments in new technologies that increase efficiencies or reduce emissions like renewable energy projects.

Once an offset is generated, the organization that develops or completes the project can retain the offsets or trade them on a voluntary carbon market (VCM).

Other companies can then buy the offsets to compensate for their own carbon footprint.

To fully distinguish the two terms, keep these keywords in mind – compliance for carbon credits and voluntary for carbon offsets.

In a compliance market, companies regulated by the government must abide by their limits or cap. Within the voluntary market, the idea is just the same. It’s just that companies do the offsetting voluntarily, either as part of their ESG goals or because of shareholders’ pressure

Who Are The Biggest Buyers Of Carbon Credits?

Carbon-intensive sectors such as energy face a harder quest to net zero emissions than others. That’s no surprise because companies in this sector simply can’t just instantly reduce their reliance on fossil fuels.

This is why the biggest buyers of carbon credits were from the energy sector, as well as from the finance, technology and consumer goods sectors. The Ecosystem Marketplace (EM) keeps track of these companies and how much credits they’re buying.

In another analysis, researchers found that at least 36% of large companies buy carbon credits voluntarily to offset their footprint. The analyzed companies include the world’s biggest and top S&P 500 businesses.

The findings revealed that Microsoft, Salesforce, Goldman Sachs, Disney, and Nike, among others are the top buyers.

The projects that those companies bought credits mainly generated in the global south. These projects often involved:

Forestry projects,

Renewable energy,

Household and community projects

In a broader analysis by EM, which included carbon project developers and investors, they found that the most popular projects producing carbon offsets are forest and renewable energy initiatives.

In separate Bloomberg analysis of data from Verra, the largest buyers of voluntary carbon credits are cryptos, airlines, and carmakers. The analysis covers only about 50% of the global carbon market in 2021 as data is voluntarily disclosed.

On the sellers’ side, in case you don’t know it yet, Tesla is the largest seller of carbon credits under the California cap-and-trade system. The company had earned billions of dollars from it.

Last year, Tesla’s total carbon credit sales reached a record $1.78 billion. All thanks to the carmaker’s hundreds of thousands of sold EVs.

Same with other commodities, there’s no single price for a carbon credit.

The cost varies. A lot. Even so in the VCM.

The cost of carbon offsets depends on various things, including project quality, issuance year, verifiability, additional benefits created and so on. For live VCM carbon pricing, please go here.

Let’s consider the project type. Common carbon offsetting projects are forestry and nature conservation, waste-to-energy, and renewable energy. Some of these projects can be worth below $1 per tonne of carbon offset, while others can cost over $40.

For a clearer explanation, take for example you opt to have a forest tree planting initiative.

If a tree can store about 5 tonnes of carbon and each tonne of carbon removed is valued at $15, you’ll generate $75/tree. Assuming the cost of carbon increases, then your revenue goes up, too.

Sounds pretty good in theory, right? But in real life, that could even be better, especially the figures.

Several farmers have been receiving over $100,000 in yearly income by letting their lands sequester over 7,000 tonnes of CO2. Boston-based Indigo Ag has been paying their partner farmers that amount and more, depending on how much carbon their farms remove.

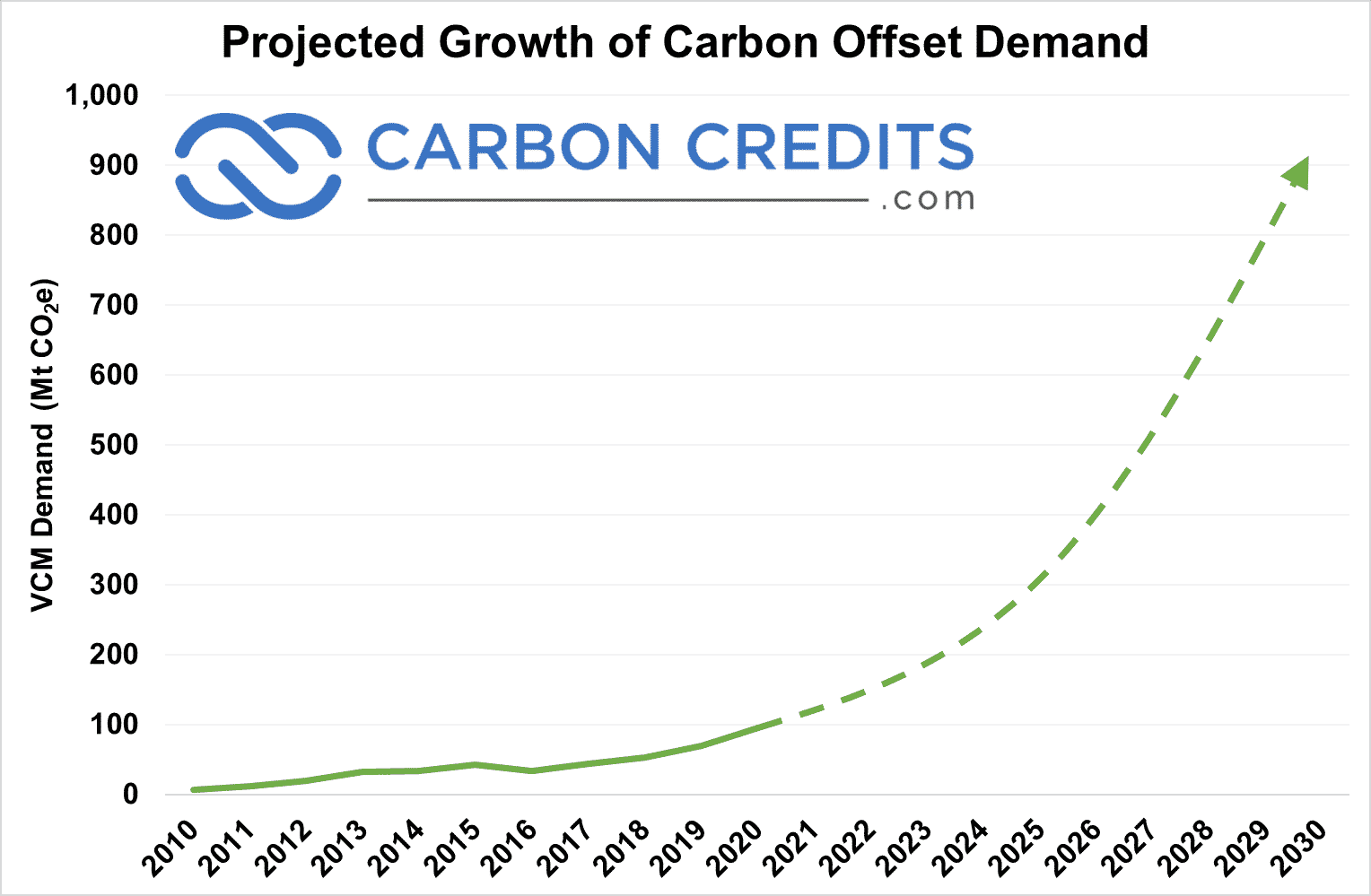

Looking at the entire market, the VCM was valued at $2 billion in 2022 alone. It may be quite huge for some market outsiders, but for insiders that’s rather not surprising.

That’s because more and more companies and organizations are expected to reveal their net zero pledges. And as mentioned earlier, over a third of the large businesses are using carbon credits as offsets.

For a better picture of how huge the market could get, take a look at the projection below.

That estimation is conventional and other market analysts predict even higher demand growth.

So how could you leverage this exponential carbon market growth? You might be asking how you can invest in carbon credits, earn profits, or simply help in the climate change fight.

We’ll explain the steps involved in the next sections. Let’s first help you out on how to buy carbon credits step-by-step.

How To Buy Carbon Credits

Buying carbon credits may not be as simple as selling them. But after you’ve known the criteria for a successful purchase, the following steps won’t be hard.

#1. Buy directly from project developers

This is the most direct way to get the credits you need – at the source. That’s from the project developers themselves. Here are the top five options that have the highest ranks.

You can either directly invest in the project as it’s being developed (lowest cost but longest time to wait until delivery) or you can contract for delivery (lower than market price but still have to wait for some time).

#2. Buy from a broker

If you want to skip all the work needed when contracting with the developer, look for a broker. Yes, carbon credits have brokers, too.

They make it easier for you and other buyers to find the credits you need. Plus, the best ones can give you an analysis of the project where those credits are from.

This is perhaps the most practical way to buy carbon credits, more so if you need a lot of them. The purchasing process doesn’t include long contracts but, of course, you guess it right – it comes with a price. So, you may have to pay more for the broker’s services.

#3. Purchase from a retailer

If you’re still wondering how to buy carbon credits if you only need a smaller volume, then going for a retailer might help. In fact, this option may also be the fastest way to get the credits.

Most often, retailers have an account on a carbon registry, allowing them to retire the credits on your behalf. But ensure that after paying the retailer, you get the rights to the credits.

#4. Purchase from an exchange

Finally, you can buy carbon offset credits from a carbon exchange. Doing so will also allow you to earn profits from trading them.

Sourcing the credits from an exchange can be quick and easy. But it may also be more difficult to access enough information about the credits’ quality.

So, there you have it. You’ve got four ways on how to buy carbon credits. Here’s a much more comprehensive guide on how to do that. And here’s the checklist you should keep in mind as a buyer.

Now, if you’re more into selling the credits or planning to sell them and get paid, here are the ways to do that.

How To Sell and Get Paid for Carbon Credits

The fastest way to sell these credits is through an online carbon exchange. There are many within the U.S. and globally that allow sellers to get paid for their offsets.

Carbon exchanges are pretty much similar as to how various regular stock exchanges operate. Selling or trading through them follows this general rule: buy low, sell high.

One quick tip though – quality carbon credits sell higher. So, it’s best if the offset credits you sell follow the standards set by the top carbon registries.

Next, if you’re a land owner or farmer, you need to secure the documents showing that you own the land, along with all the details describing your land. You must also have the papers documenting the land management practices you perform. This is crucial for the buyers and as proof that your land captures the amount of carbon you declare.

But before you sign any contract with the buyer or look for one, do your research first. Knowledge will help you be confident that the amount you’ve sold or get paid for is enough and not too low than you deserve.

As mentioned earlier, you may also opt to enlist the help of a broker. But be prepared to share the payment with one.

But if you want to take home all the money, then by all means, just find the right buyer yourself.

How To Earn Carbon Credits?

Before you can sell the credits, you have to earn them first. How do you do that?

If your business activity or project reduces, avoids, or removes CO2 from the atmosphere.

For every metric ton of reduction or removal, you earn one carbon credit for it.

So if you have a huge project or a couple of them, you can earn even more credits to sell. But what are the major factors you need to consider to earn high-quality credits? Remember, quality credits sell higher.

Let’s give a specific example for a better understanding – a farmer or rancher.

Here are the things farmers should be aware of to earn more through carbon credits.

Right carbon program.

The right carbon credit program prompts farmers to apply sustainable practices designed to improve soil health, reduce carbon emissions, and enhance soil carbon sequestration. The approach should take into consideration that each farm is unique and so needs a customized guideline.

Right carbon farming plan.

Having a custom carbon farming practice plan means basing it on your baseline assessment and goals. The experts will guide you on how to implement carbon farming practices to generate the credits. Common examples are reduced tillage, improved residue management, cover corps, to name a few.

Right implementation.

This stage requires proper data-keeping and monitoring. Remember your goal is to generate credits by implementing the changes in your farming methods. Availability of data will help you guide what to improve in your practices.

Verification.

Verifying your data and results can be done by the carbon program you partner with or an independent body. Verification means determining if the amount of carbon removals or reductions your farm delivers is correct.

Only with all those things in place that you can be issued with carbon credits and earn them.

Carbon Credits Explained: Key Takeaway

To wrap it all up, can you make money from carbon credits? Yes, you can. Either by selling them or trading them as an asset.

Either way, you are not only earning cash but you are also contributing to winning over the climate change fight.

After all, carbon credits were designed to encourage us to reduce our planet-damaging footprint before it’s too late.

Lithium is the new oil, at least for electric vehicles (EVs), and the global race is on to secure this valuable resource.

The rising demand for lithium-ion batteries in the United States reached a record high in the first quarter this year, showing powerful interests on EVs and the clean energy transition.

This data highlights the urgent need to ramp up domestic production capabilities to meet the soaring demand.

Unfortunately, the U.S. doesn’t produce enough of the silvery metal it will need as it only has one source of domestic lithium production. For Tesla and other EV manufacturers, this can be a problem down the road.

More importantly, the country won’t be able to reach its Net Zero goal without increasing its own lithium capabilities.

This is where American Lithium Corp. (AMLI) comes to the rescue, playing a major role in filling the supply gap. The company manages two of the biggest lithium deposits in the Americas.

Tesla Needs $374B to Invest in Lithium

In 2021, Tesla said that it would use lithium-based cathodes for its batteries, which the company had already been doing at its Shanghai factory at that time.

Two months ago, the carmaker revealed that it will use the same for its short-range heavy electric trucks (semi-light). The leading EV company is also planning to use lithium-ion batteries for its mid-sized vehicles.

The carmaker’s goal is to produce 20 million EVs each year by 2030. It delivered just above one million units in 2022 but used around 42,000 tons of lithium in 2021. That’s more than 5x the combined lithium consumed by Ford and GM, according to BNEF data calculations.

To meet its ambitious goal, Tesla would need a huge volume of lithium to make the required batteries. Earlier this year, it broke ground in Texas for its lithium refinery plant worth $1 billion.

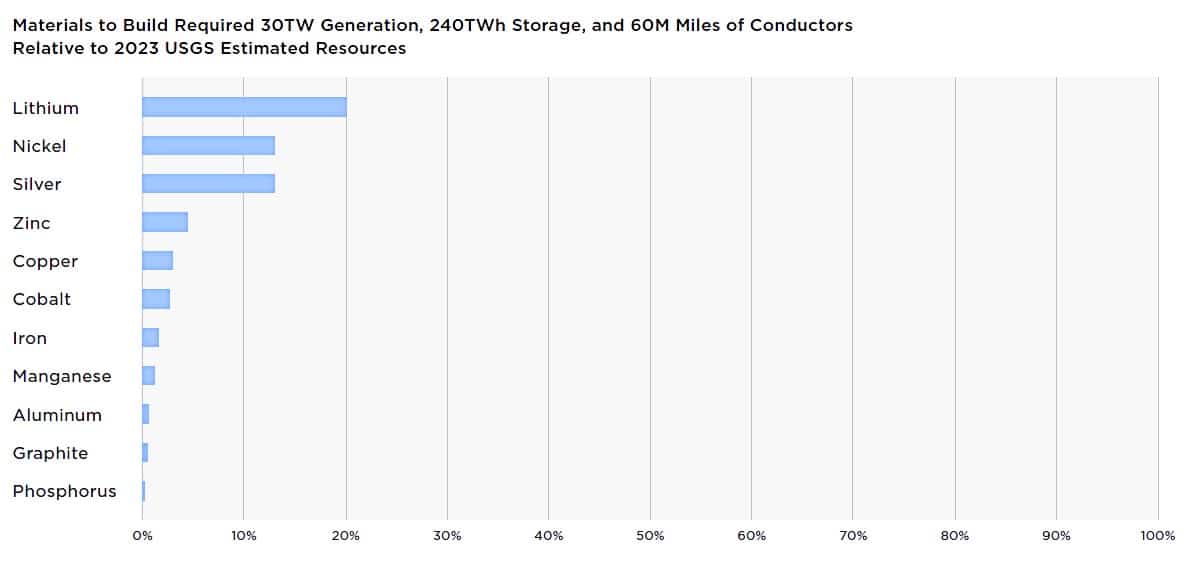

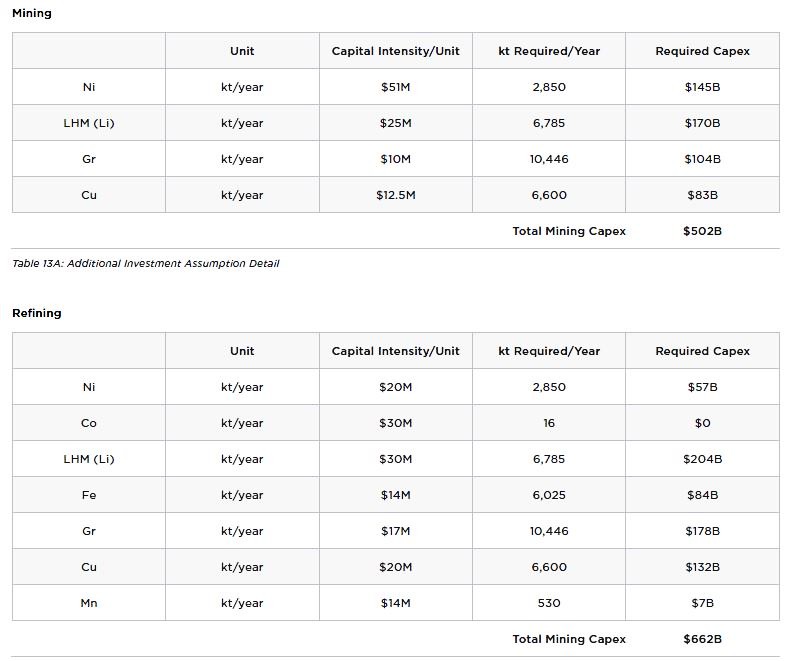

In its recent Master Plan report, Tesla analyzed that lithium is responsible for about 20% of the materials needed to deliver the energy storage in batteries for EVs relative to 2023 USGS data.

With that data, the giant EV maker estimated that it needed a total of $374 billion to invest in mining ($170B) and refining ($204B) lithium (Li).

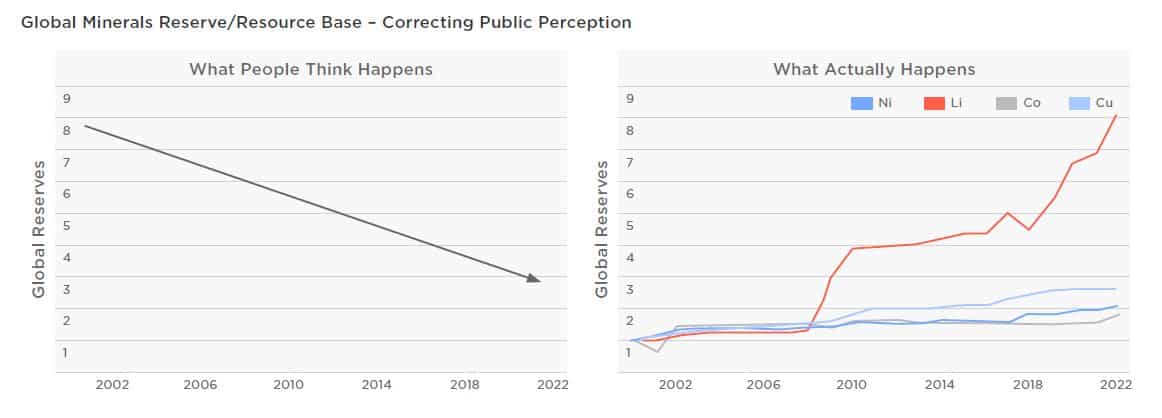

What’s more interesting is Tesla’s analysis of the actual global mineral reserves, including lithium (in red). It’s far way different from what people think. Lithium reserves started to skyrocket in 2008, meaning more lithium deposits were being discovered. And it continues to soar higher…

Global lithium production was at 100,000 tons or 90+ million kg in 2022. The International Energy Agency said that the world needs up to 6x more of that by 2030.

That’s a big opportunity for companies like American Lithium to serve with their large lithium reserves in highly attractive jurisdictions.

The Silicon Valley of Lithium

Nevada is home to the only lithium mine in the US – the Silver Peak mine. The operation is run by Albemarle Corp base in California. But more projects are in the pipeline, alongside American Lithium’s TLC.

Nevada is also dubbed as the “Silver State” whose silvery metal reserves are vital for both the state’s and the country’s economy. Strong government support had made undergoing projects possible, attracting massive investments.

For instance, Ford Motor inked a deal last year to source 7,000 metric tons of lithium from an Australian-owned Rhyolite project. General Motors also invested $650 million in the state’s largest claystone deposit near the TLC project of American Lithium.

Similar deals also abound, with major battery manufacturers signing supply deals with proposed lithium projects in Nevada.

And at Reno’s event last March, the Department of Energy announced a conditional $2 billion loan guarantee for a Nevada-based battery recycling firm. Energy Secretary Jennifer Granholm pointed out that the state is flush with more projects that are all part of a rising lithium battery supply chain.

The entire process, from mining to recycling of the critical mineral – otherwise known as lithium “loop”, is possible within state lines, which is unheard of domestically.

Industry estimates say the lithium-ion battery market will reach over $100 billion by 2030. And Nevada is the only state that allows for each phase of the lithium lifecycle.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: .

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Climate talks in Bonn, Germany kicked off this month where diplomats around the globe meet to agree on a common agenda for the next big UN climate summit, COP28, taking place in Dubai in November.

However, negotiators parted ways with some decarbonization issues left hanging. These particularly include climate finance and how quick emissions cuts must be done formally known as the Global Stocktake.

Global Stocktake provides a picture of where the world is in addressing climate change, where it needs to go, and how to get there.

The Bonn delegates have the huge task to lay the groundwork for the Global Stocktake before its finalization at COP28. But early in the two-long-week talks, tensions were high as negotiators couldn’t agree on the agenda.

This prompted the climate conference’s co-chair Nabeel Munir to call the diplomats “a class of primary school”.

Here are the key issues that caused agenda woes and disputes among delegates.

Where Are We Right Now in Cutting Emissions?

The Global Stocktake is a key element of the Paris Agreement that will inform the next round of climate pledges by countries. It’s a critical turning point when it comes to national efforts in reducing carbon emissions to tackle climate change.

In other words, it’s a defining moment to take a deeper look at the state of the Earth and chart a better course ahead. It will help nations bolster their ambition as necessary to avoid more global warming.

The first talks on Global Stocktake also happened in Bonn in June last year. The second one took place at COP27 in Egypt, while this is the third one it’s discussed for COP28.

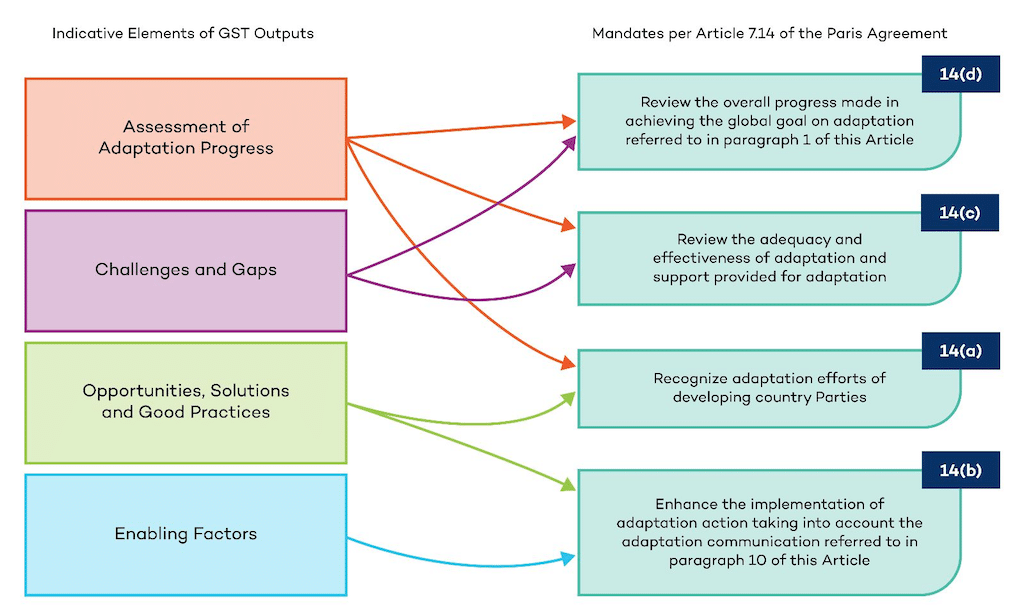

To have the final output of the Global Stocktake (GST), here’s how it will go for the participating parties:

Mapping of the indicative elements of Global Stocktake (GST) outputs with Paris Agreement Article 7.14 mandates (Source: NAP Global Network)

There’s a common understanding that countries aren’t on track to achieve their climate goals. These targets even fall short to meet the 1.5°C warming threshold. And so, the Global Stocktake was designed to bring countries back on the right course in addressing the climate crisis.

But there were significant disagreements on some points discussed within Global Stocktake (third section) among delegates. And one of them is on climate finance.

Climate Finance: The Most Disputed Agenda

Since the Paris Accord in 2015, the Dubai COP28 will see the UN publish the Global Stocktake for the first time. But disputes arise on how to incorporate finance and support.

In the words of a delegate from a global nonprofit organization, “Progress was underwhelming on nearly every front, with one main culprit: money.”

While climate finance isn’t directly part of the agenda, it casts a shadow over the talks.

During the conference, low-income nations expressed frustrations on the funds promised by rich countries that didn’t come. The $100 billion 2020 pledge by wealthy developed nations to finance developing countries’ climate actions remains unmet.

Meanwhile, there’s a new post-2025 climate finance target to help developing nations cut their carbon emissions and improve climate resilience. They call it the “new collective quantified goal” (NCQG) that’s the agenda for COP29 in 2024.

Yet, discussions for this new climate finance goal in Bonn were so technical.

The general sense is that rich nations, particularly the U.S. and the EU, are trying to avoid specific talks on climate finance.

For instance, the US wants to make developing nations also rely on private financing and suggest including wealthy developing nations in the list of climate finance donors. These include China and the Gulf states, in particular.

For Tom Evans of E3G, developed countries are using that as a shield to block talks on climate finance at Bonn. He remarked that they’re bothered that “the more we talk about financial flows, we’re literally talking about ending fossil fuel investment.”

Commenting on this issue, Harjeet Singh from Climate Action Network tweeted that wealthy nations showed indifference toward developing countries. She further asserted that:

“Let’s be clear: without honouring their financial pledges—directly tied to their historical role in driving the climate crisis—these affluent nations lack the moral authority to exert pressure on poorer countries.”

That climate money is not only due to developing nations; it’s also critical to ensure a transition to a renewable energy system for all.

The COP for Global Stocktake

Looking forward to COP28, many believe it would be a big fight between the rich and the poor countries over climate finance.

Others dub this year’s climate summit as “Global Stocktake COP”.

After Bonn climate talks, there will be a summary report on the 3rd meeting of the Global Stocktake’s technical dialogue by August. Then a synthesis report ensues by September that brings together all the assessments of the entire 3rd Global Stocktake dialogue. All these in preparation for COP28 final talk.

In his closing speech, the UN Climate Change secretary Simon Stiell noted that pledges and implementation are far from enough. Thus, “the response to the Global Stocktake will determine the success of COP28 and, far more importantly, success in stabilizing our climate”, he adds.

A study by scientists at Lawrence Berkeley National Laboratory (Berkeley Lab) and the University of Zurich found that the decomposition of organic matters responsible for carbon sequestration in deep soil is significantly accelerated by global warming.

The alarming results have serious impacts on carbon projects that rely on forests and soil as nature-based solutions to mitigate climate change.

What is Soil Carbon Sequestration?

Soils are the largest natural sink for carbon. Soil carbon is a key component of the planet’s carbon cycle that maintains soil health and productivity. It comes in many forms such as decomposing organic matters.

Soil carbon sequestration is a process by which carbon dioxide is removed from the atmosphere and stored in the soil. It involves the conversion of CO2 into organic matter that stays in the soil for decades or even centuries, which is crucial to mitigate climate change.

During photosynthesis, plants store carbon in their cell walls and the soil, notably contributing to carbon sequestration. About 25% of the global carbon emissions are captured by forests, grasslands, and pasture land.

This natural carbon sequestration has been going around for decades. So the amount of carbon in the soil may now have doubled. 50% of this soil carbon content resides at the deeper layer in subsoils – over 8 inches or 20 cm deep.

But because of human activities such as deforestation and agriculture, global temperatures are heating up. CO2 emissions from these activities are increasing and account for about a fifth of global GHG emissions.

In effect, even the deeper layers of soil are now warming up, too. The researchers confirmed this. Their finding shows that climate change will impact all areas of soil carbon and nutrient cycling.

Margaret Torn, the study’s senior author and a senior scientist in Berkeley Lab pointed out that:

“It also shows that in terms of carbon sequestration, there’s no silver bullet. If we want soil to sustain carbon sequestration in a warming world, we will need better soil management practices, which can mean minimal disturbance of soils during forest management and agriculture.”

The Alarming Finding: Major Loss of Carbon Sinks

In a previous study in 2021, Torn and her team discovered that warmer temperatures result in a huge drop in carbon stocks stored in deep soils. Their results show a 33% loss over 5 years.

In this present study, researchers provided more evidence that higher temperatures cause a major drop in the soil organic carbon compounds produced by photosynthesis in plants.

The team at the University of California’s Blodgett Forest Research Station did an experiment in Sierra Nevada mountains. They used vertical heating rods to warm one-meter-deep plots of soil by 4°C (7°F). This is the projected warming level by year 2100 under a high GHG emissions scenario.

The scientists found that only 4.5 years of warming at this temperature resulted in major changes in carbon stocks at over 30 cm depth (12 inches) below the ground.

The researchers also did a spectroscopic analysis at the University of Zurich to know which organic compounds are affected. Here are their shocking findings:

17% loss in lignin – a compound that gives plants their rigid structure

About 30% loss in cutin and suberin – waxy compounds in leaves, stems, and roots of the plants

Lastly, the team surprisingly found that there’s also a significant change in the amount of “pyrogenic carbon” in soil samples. This is one type of soil carbon from charred vegetation and other organic matters left by wildfires.

Pyrogenic carbon is the most stable form of sequestered carbon in soils. It can remain in the soil for up to centuries. And the researchers found much less of it in the artificially heated deep soils.

More remarkably, their results suggested that pyrogenic carbon can decompose as fast as other materials because of warming soil. This means that “when you put material deep into soil where it’s in contact with minerals and microbes, those natural systems will decompose the material over time,” Torn highlighted.

What All These Mean for Soil Carbon and Nature-Based Climate Solutions?

While further research is necessary to solidify the findings of the study, they do have significant implications in using soil carbon sequestration to tackle climate change.

Large companies and governments are investing heavily in this kind of natural carbon sequestration projects.

Given the findings, initiatives involving forests and soil carbon capture may have to reconsider how they approach these mitigation efforts. More sustainable farming and soil management practices like cover cropping would be critical.

Even the UN group tasked to finalize the international carbon trading systems may find the results relevant. They tend to consider nature-based solutions more reliable than technology in capturing CO2.

The researchers plan to resample the studied soil to know how nine years of heating affect the soil. They’ll be having a grassland warming experiment in Northern California and the whole-soil or deep-soil warming experiments for more knowledge.

If you’ve been keeping up with the net zero trend, then you’ve probably heard the terms Carbon Dioxide Removal (CDR) and Carbon Capture and Storage (CCS) thrown around before.

Both are important tools in the ongoing fight against climate change. What you might not know, however, is that they actually refer to two different processes.

Generally speaking, CDR refers to processes and technologies that remove carbon dioxide from the atmosphere. Some examples of this include afforestation and reforestation.

On the other hand, CCS differentiates itself from CDR with the term “capture”. This refers to the fact that CCS methods generally capture CO2 from specific points of emission, also known as “point sources”. An example of CCS would be capturing the carbon dioxide emitted by a specific industrial factory.

With that said, CDR and CCS are two sides of the same coin – they simply differ in where they remove the CO2 from. For both processes, the end goal is the same: to remove carbon dioxide that would otherwise end up in the environment, and to get rid of it by storing or using it up.

Various Types of CDR and CCS

Both CDR and CCS are expected to scale up significantly from where they are now in the IEA’s Net Zero Emissions by 2050 Scenario.

There are already a number of differing options for both. And we’ll go over some of the major ones in detail below.

For CDR, one of the most common types of projects is planting trees, which falls under either afforestation (planting trees where there weren’t trees before) or reforestation (planting trees where there used to be trees).

Trees and other types of vegetation store carbon through photosynthesis as they grow, making them fantastic natural carbon sinks.

Many of these forestation type projects qualify under the UNFCCC’s REDD+ framework. If you haven’t heard the acronym before, REDD+ stands for “Reducing Emissions from Deforestation and forest Degradation in developing countries”. The “+” includes activities that don’t directly involve planting trees such as forest management.

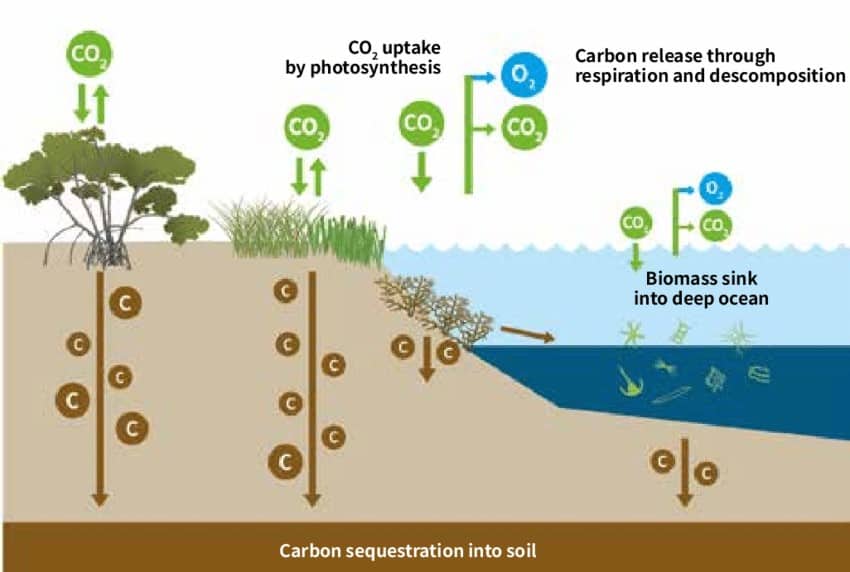

In a similar vein, some projects also aim to store carbon in the soil through special farming practices, or in certain types of ecosystems that work as excellent carbon sinks. Coastal wetlands and peat marshes are examples of such ecosystems that are particularly suited to sequestering carbon. As such, conserving and restoring these kinds of ecosystems also serves as a method of CDR.

Another offshoot of this type of CDR is blue carbon projects, named so for how they focus on ocean-based ecosystems. Coastal biomes such as tidal marshes and mangroves are thought to be more effective at removing carbon when compared to a forest of similar size on land.

Blue carbon ecosystems aren’t as well understood as traditional land-based ones though. But this is an exciting CDR field with lots of ongoing research.

Storing carbon in the above manner is collectively known as “biological sequestration”, where the carbon is stored in natural ecosystems.

Geological Carbon Sequestration

On the flip side of biological sequestration, we have “geological sequestration”, where the carbon is stored in deep rock formations. Much like how oil and gas deposits are usually found deep underground, trapped between layers of impermeable rock, carbon can be stored the same way.

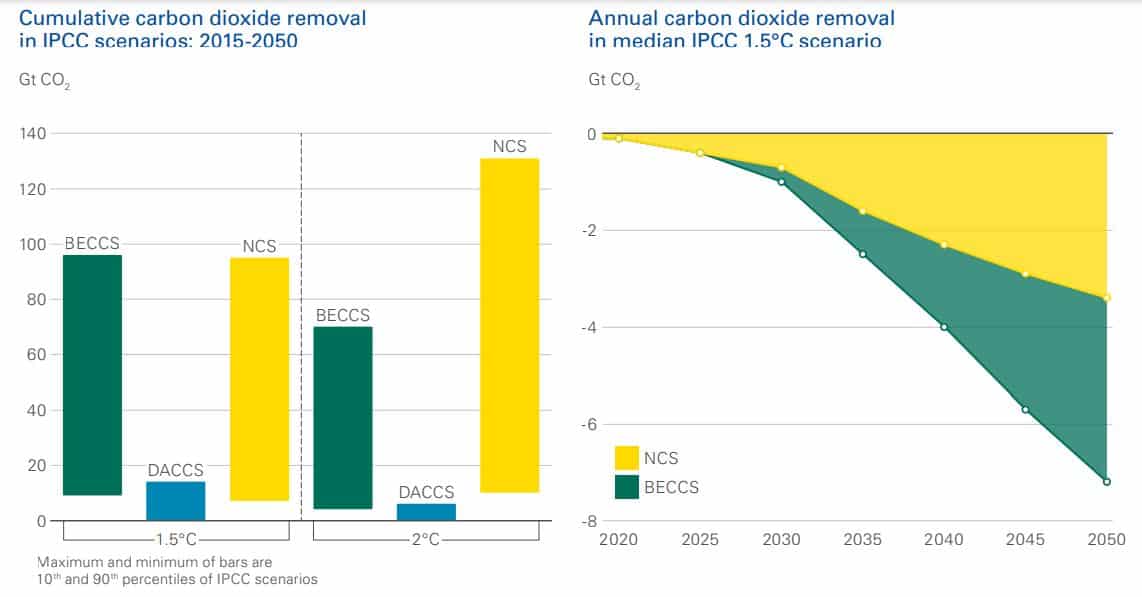

Types of CDR that allow for geological sequestration include technology-based solutions like Direct Air Capture (DAC) and Bioenergy with Carbon Capture and Storage (BECCS).

DAC involves directly removing CO2 from the air. BECCS involves capturing the carbon emissions from biological sources such as bioethanol or pulp and paper production. Both are critical to achieve the IPCC’s 1.5C °C scenario as shown above.

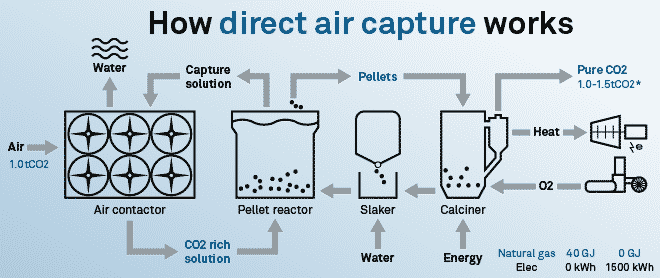

To date, over 50 DAC plants are operational, expected to reach ~93 plants capturing 6.4–11.4 Mt CO₂/yr by 2030.

Example of DAC process by Climeworks

While BECCS technically involves removing carbon from a point source and has CCS in its name, it blurs the line between CDR and CCS. The biomass used in BECCS processes absorbed CO2 from the atmosphere while it grew. In effect, BECCS technically removes carbon from the atmosphere as a net result.

For instance, the process of fermenting corn to turn it into bioethanol releases carbon dioxide as a by-product. However, that corn also absorbed CO2 from the atmosphere as it was growing.

As a result, any CO2 captured from the fermentation process was actually effectively removed from the atmosphere.

On the subject of CCS and net zero, the technologies involved are much more straightforward than with CDR.

As mentioned, CCS is mostly often performed on point sources as that’s where it’s most easy and cost-effective to do. Large industrial plants, fossil-fuel-based energy plants, and other such facilities with significant carbon emissions are all viable targets for CCS.

The different types of CCS technologies differ in exactly how they capture carbon from emissions streams. Examples include absorption through carbon dioxide scrubbers, chemical looping combustion, and oxyfuel combustion, to name a few.

The Role of CDR and CCS in the Push to Net Zero

Though the world continues on the path to net zero, the transition will take time – decades worth of it.

In the meantime, there will continue to be plenty of ongoing essential processes worldwide that are difficult to make net-zero with current technology. Steelmaking and cement manufacturing are two such examples of industrial processes that are hard to completely eliminate carbon emissions from.

For these industries, CCS will serve as a perfect solution for abatement.

On top of this, CDR will help to reduce carbon either already in the atmosphere, or already emitted by sources that are difficult to capture emissions from.

CDR and CCS are both key parts of our efforts to mitigate climate change. But they can’t fully replace the net-zero transition.

Geological analysis has estimated that the global potential for geological storage is in the range of 8,000–55,000 GtCO₂, though only a fraction is technically or commercially viable. This reinforces why both CDR and CCS remain vital, especially given the difficulty of decarbonizing heavy industries like steel and cement.

And the fact that there exist industries where it’s difficult to completely eliminate carbon emissions, as previously discussed, means that it’s even more important to remove other sources of carbon dioxide wherever possible.

Still, both CDR and CCS will play major roles globally as we continue on our 2050 net-zero pathway. Expect to see heightened focus on both in the years to come as the fight against climate change progresses.

In a strategic shift that startled the energy sector, Royal Dutch Shell PLC announced plans to maintain its current level of oil production until the end of the decade. It’s a major shift from its previous commitment to reduce oil production by 1-2% annually until 2030.

The announcement came as part of a larger suite of decisions aimed at increasing investor confidence, making the business more efficient, and aligning operations with Shell’s long-term carbon reduction goals.

Shell’s new CEO, Wael Sawan, justified this unexpected change by pointing to the company’s significant reduction in oil production over the past three years.

In a rapid operational pivot, Shell managed to reduce oil production from 1.9 million barrels per day in 2019 to 1.5 million in 2022. This achievement effectively met its 2030 reduction target eight years ahead of schedule.

This impressive reduction was due to selling oil fields to others who continue to extract fossil fuels from these sites.

Despite the shift, Sawan has taken steps to reassure investors about the financial health and growth potential of the company. Shell plans to reduce capital spending in 2024 and 2025 to $22-$25 billion a year. It’s down from a planned $23bn-$27bn in 2023.

Additionally, the company intends to cut group-wide annual operating costs by $2bn-$3bn by the end of 2025. These cuts come as part of a larger plan to simplify operations and close the valuation gap that separates Shell from its US rivals.

Shell Investor Appetite and Satisfaction: Dividend Hike

Investors, it seems, have more than just cost reductions to look forward to.

The company has announced a 15% rise in its dividend per share from the second quarter of 2023. Dividends are set to increase to 30-40% of cash flow from operations. Moreover, the company also plans to return at least $5bn to shareholders by buying back their shares in the second half of this year.

This announcement comes on the heels of Shell’s nearly $1.7bn profit increase in 2022, driven by rising energy prices.

Net Zero Goals Remain Firm

Despite the move to maintain oil production levels, Shell maintains a firm commitment to its net zero emissions target. The energy giant intends to grow its gas business and allocate about 20% of its group spending toward clean energy technologies, including hydrogen, biofuels, and vehicle charging.

Sawan emphasized the need to develop scalable and profitable models that can drive the decarbonization of the global energy system.

In its 2023 press release, Shell clarified that its operating plans, which are updated yearly, currently reflect a 10-year forecast. These plans take into account the current economic environment and reasonable projections for the next decade.

However, they do not yet incorporate the company’s 2050 net zero emissions target and 2035 Net Carbon Intensity (NCI) target. That’s because these goals are outside of the current planning period. Shell expressed a readiness to adapt its operating plans as society moves towards net zero emissions. At the same time, acknowledges the significant risk if society fails to achieve net zero emissions by 2050.

Shell’s strategy of balancing carbon reduction, production goals, and shareholder satisfaction marks an important turning point in the company’s approach to navigating the energy transition.

Despite the unexpected change in its oil production strategy, Shell has shown that it remains committed to addressing climate change while simultaneously maintaining investor confidence. By prioritizing both environmental responsibility and shareholder value, Shell is setting a precedent for the energy industry.

The strategic shift emphasizes that the transition to a low-carbon future need not come at the expense of investor confidence.

Leading by Example

Wael Sawan, in his statement, expressed Shell’s commitment to the energy transition, saying,

“We are investing to provide the secure energy customers need today and for a long time to come, while transforming Shell to win in a low-carbon future“.

He further emphasized the need for “performance, discipline, and simplification” as the guiding principles for Shell’s capital allocation strategies.

Shell’s ambitious plans include continued investment in profitable business models, including carbon reductions, that are scalable to impact energy decarbonization. This strategic approach showcases the company’s commitment to taking part in the global transition to sustainable and environmentally responsible energy sources.

The energy giant’s ability to balance investor interests with environmental commitments could serve as a template for the industry. Its recent strategy to commit both to sustainability and shareholders signals a possible path forward for the energy sector.

A consortium of global experts, Coal to Clean Credit Initiative (CCCI), is developing a world-first “coal-to-clean” carbon credit program that incentivizes the transition away from coal-fired power plants to renewable energy in emerging economies.

The group includes the Rockefeller Foundation, Global Energy Alliance for People and Planet (GEAPP), with support from South Pole, Climate Policy Initiative (CPI), and Rocky Mountain Institute (RMI).

The new carbon credits under development will be called coal-to-clean credits.

What are Coal-to-Clean Credits?

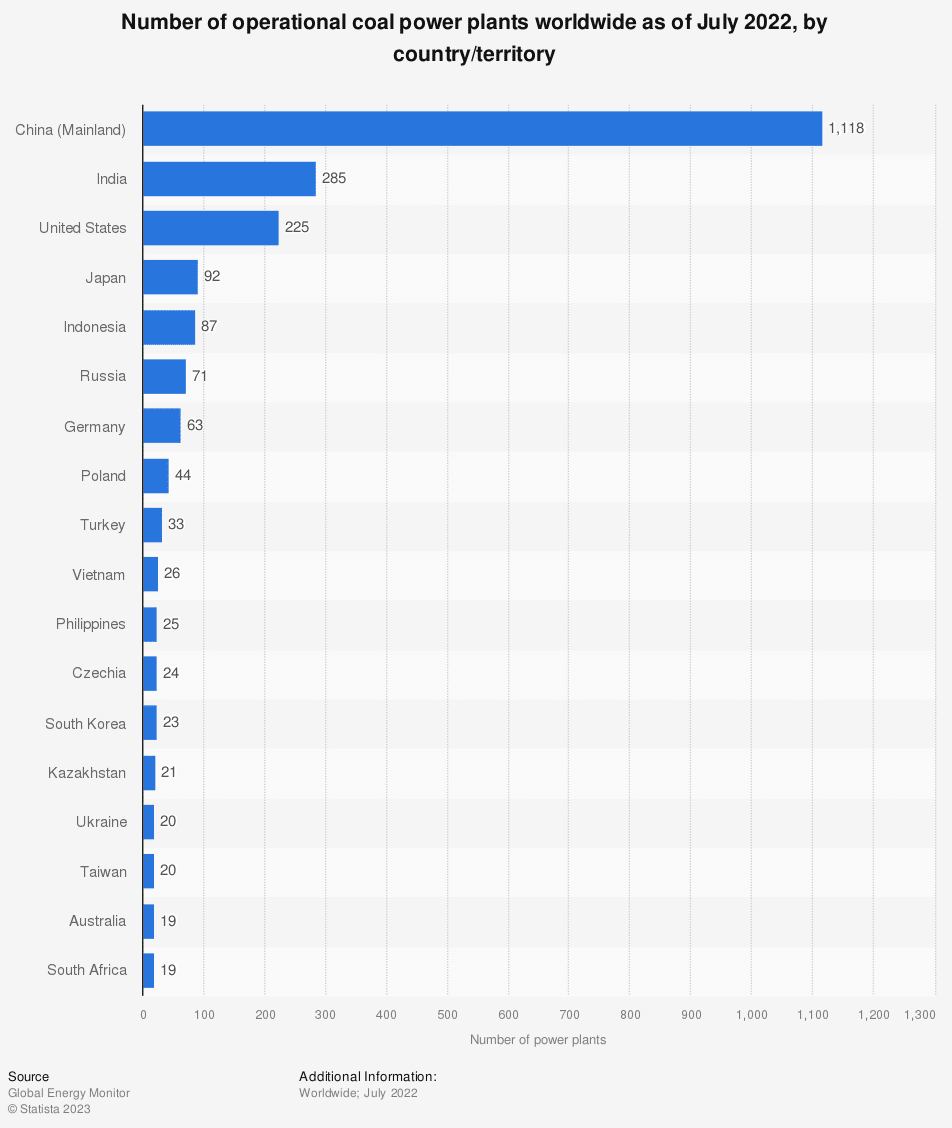

As of July 2022, the total number of coal power plants operating globally is around 2,195, according to Statista. They accounted for over a third of total electricity generation.

China, which accounts for over 50% of global coal electricity generation, has the most coal-fired power stations worldwide – 1,118. That number is about 4x the total power plants in India, which came second in ranking.

Many of those plants have no financial incentives to retire early, allowing them to emit more CO2. In fact, coal-fired power generation reached an all-time high in 2021, also pushing emissions to record levels.

Power stations in China alone reached a record high of 8 billion metric tons of CO2 in the same year. These trends don’t align with the Net Zero Emissions by 2050 scenario shown below. It calls for about 9% annual reduction in unabated coal-fired generation between 2022 and 2030.

Annual change in CO2 emissions and generation from unabated coal-fired power plants in the Net Zero Scenario, 2015-2030

Source: International Energy Agency website

Unfortunately, more than 90% of the coal power plants today are protected from competition either because of regulation or long-term contracts. Also, 40 countries pledged to phase out their coal-fired power plants during the climate conference, COP26, in 2021.

But the 3 giant economies owning the most operational stations didn’t agree to the terms of phase-out.

To address these concerns, the CCCI is working on a methodology to develop a world-first approach to speed up the phase-out of coal power plants. The goal is also to provide financial incentives for the owners to partially or fully replace those with clean power.

The revenue from selling the CCCI’s “coal-to-clean” carbon credits will incentivize plant owners to invest in renewable energy. The funds will also help the affected workers and communities during the transition.

The consortium devised a detailed concept for its new carbon credits. They sought technical input from industry experts and identified real-world examples most suited for generating the credits.

The ultimate goal of creating the coal-to-clean credits is to avoid tens of millions of tons of CO2 emissions from coal.

And that’s possible for just one plant if it’s “retired and replaced by cleaner power decades ahead of its planned closure”, says Joseph Curtin, Managing Director at The Rockefeller Foundation. He further points out that:

‘’If we are to avoid the threat of over 2 degrees Celsius of global warming, we must provide a credible pathway for coal plants in emerging economies to transition sooner.”

CCCI’s Approach to Coal Phase-out

The CCCI’s approach to early coal phase-out follows a just transition as it will be in partnership with local communities for every project. The initiative will ensure that affected communities have a crucial role to play during the transition.

The aim is that CCCI will set a new benchmark for carbon-financed projects while ramping up the global coal-to-clean transition. To do that, the group will provide a nearer-term opportunity at the project level while aligning with jurisdictional methods and systems of decarbonization.

The team is aware that coal plants are national assets integrated within a country’s power system. So, retiring them earlier than planned needs careful consideration and talks with the authorities.

In this case, CCCI explores a unique way in mobilizing finance via carbon credits to achieve its goal. The alliance will also consider integration of their credits with existing and future compliance and voluntary carbon markets.

Doing so allows them to complement other carbon market and climate finance initiatives. They also support broader carbon market improvement by growing the supply of high-integrity carbon credits with clear standards for buyers.

Who Leads the CCCI?

The Global Energy Alliance for People and Planet (GEAPP) leads the CCCI. GEAPP is an alliance of philanthropy, governments in emerging and developed economies, and technology, policy, and financing partners. Their mission is to enable emerging economies to shift to clean energy.

The Rockefeller Foundation, which also focuses on scaling renewable energy for all, joins GEAPP, along with their implementing partner South Pole. The group is further supported by technical experts from CPI and RMI.

Altogether, the team ensures that CCCI’s methodology meets the highest level of environmental integrity and technical best practice.

Currently, they’re able to close a high-level deal with the government of Indonesia and have started scoping work in Vietnam and South Africa. In these regions, the cost of renewable power undercutting fossil fuels in 2030 will bring over 20 million jobs.

The CCCI will start its consultative process to develop its coal-to-clean carbon credit methodology this month. In the coming months, the group will continue to work with industry experts in developing its unique approach to coal-to-renewable projects.

Carbon standards, international finance institutions, and other organizations dealing with financial mechanisms are welcome to engage with the team.

The CCCI aims to start making deals earliest in 2024 and use the program for many plants this decade. The team will present its program at this year’s United Nations Climate Change Conference (COP28) in Dubai in November.

Xpansiv, the largest spot exchange for environmental commodities, revealed that it will spin out its finance data subsidiary, Fiutur, to deal with specific challenges and give better services to its energy transition participants.

Xpansiv runs the market infrastructure to rapidly scale the global energy transition. The environmental commodities it trades include carbon credits, renewable energy credits, and digital fuels.

The company’s CEO, John Melby, asserted the role of environmental markets in the transition, saying that:

“Environmental markets are a critical tool in accelerating the global energy transition and Xpansiv is focused on providing and operating the core registry and market infrastructure for these global markets to evolve.”

The New Fiutur

Xpansiv’s decision will allow its capital markets participants like banks as well as data providers to include environmental markets for more integrity across the capital lifecycle.

The newly formed company, Fiutur, is a powerful financial data platform. It will have its own governance and capitalization, separate from Xpansiv and will run with more independence over time.

Fiutur will have the following board of directors and executives:

Directors: Jamila Piracci, Tom Lewis, and Roseann Palmieri

Executive Chair – Will Stewart

CEO – Joe Madden

COO – Sam Teplitsky

The key reason that prompted the spin off of Fiutur is to help Xpansiv’s stakeholders to face specific challenges related to energy transition finance.

The decision comes after Xpansiv’s move to license its global environmental numeric reference system called the Universal Project Numbers (UPN). This system has been tracking millions of environmental assets, together with its digital dMRV (measurement, reporting, and verification) technology.

The referencing system links environmental market and sustainable finance data. It was licensed by T-REX, a financial infrastructure provider for fixed income investments, in April this year.

Fiùtur will further take advantage of Xpansiv’s UPN by incorporating roles-based data governance and ownership across multiple parties. This will result in certain and conclusive outcomes in finance, markets, and insurance.

As the world transitions to clean energy in the coming years, trillions of dollars are necessary to fund it.

In effect, market participants are requesting scalable solutions to emerging risks and opportunities. And so, the new company “is purpose built to help them do that”, says Fiutur CEO.

California-based EV startup Rivian hoped to earn carbon credits for the chargers powering its electric trucks and SUVs, including those found in the homes of its customers, which raised questions about who should own the credits.

The popular EV maker claiming carbon credits for home chargers received big disagreements from market experts, MIT reports. It particularly raises concerns on who has the right to claim the climate impact of using clean technologies like EVs. Should it be the manufacturing company or the buyer?

Speeding Up the Move to Carbon-Free Transport

Rivian has received outstanding reviews both from customers and automotive critics for its high-end electric pickups (R1T) and SUVs (R1S). They’re praising the EV’s power, design, and luxury features.

Last year, Rivian applied to Verra to earn carbon credits for the carbon emission reductions through the use of its chargers. The EV startup stated that it “retains all environmental attributes” (or carbon credits) from the use of its EV chargers. These credits are tradable in carbon markets and bought by entities looking to offset their own carbon footprint.

Rivian’s project proposal with Verra specifically includes these items:

Adventure Networks

Waypoint chargers (bought by 3rd-party site hosts)

Residential or home chargers located in the U.S.

The EV carmaker clearly said in the documents that they have the “sole and exclusive” rights to the carbon credits generated by their charging network. That means they have absolute discretion to transfer, sell, or hold those credits as they see fit.

Rivian’s electric cars come with portable wall chargers that are compatible with standard outlets. By displacing fossil fueled vehicles, the company’s charging network can cut carbon emissions.

They said that their charging infrastructure can cut CO2 emissions by 200,000 tonnes yearly all throughout the project’s 7-year period. Each tonne of reduced emission produces one carbon credit.

Andrew Peterman, Rivian’s director of renewable energy, noted that this program is crucial in transitioning to clean transportation, saying that:

“Alternative revenue sources from programs like this not only make the scaled transition to clean electric transportation possible (and at the necessary speed) but enable companies like Rivian to do so while generating a greater positive impact for communities, conservation, and the climate.”

In a separate study, researchers found that charging 1 million EVs at an optimized time delivers carbon emissions savings equal to taking up to 80,000 fossil fuel-powered vehicles off the road.

However, Rivian’s claim was met with critics – especially on “additionality” concerns.

Meeting the Criteria for Reliable Carbon Credits

Not all carbon credits are made equal. The best and credible carbon credits must meet a set of criteria and one of them is additionality.

A carbon credit becomes additional if it delivers climate impact that wouldn’t happen without the revenue from selling the credit. But if the carbon reductions are going to happen anyway, even without the revenue from the credits, then they’re not additional.

Now, applying that additionality to Rivian’s EV charging network, do they deserve to earn carbon credits for it?

Some say they don’t because of the factors that are driving the growth of EVs and their charging infrastructure. In particular, these include more policy support and the current rising trends for EVs.

As per market estimates, EVs will make up over 50% of new passenger car sales in the US by 2030. And it’s not just in the US because historic EV sales are also soaring globally as shown in the chart below.

Others are also skeptical of Rivian’s claim to cover residential chargers in their Verra carbon credit proposal.

In that case, the company is assuming that the EV chargers won’t be installed without the funds from carbon credits. Not to mention the fact that it’s the customers who pay for the chargers themselves and they can decide to either charge at their homes or not, regardless of the credit revenue.

So for critics, it seems not right that Rivian takes ownership of the credits that customers can independently produce. As one skeptic puts it, customers buy the EV, pay for the charger, and pay for the power to charge it. But then others take the credits?

Commenting on these questions, Peterman said that the additional revenues from selling carbon credits will help speed up the deployment of clean renewable EV charging solutions. He further added that the extra funds also help promote more access to and more affordable home charging solutions. And that’s even more important in states or locations where there are limited utility incentives.

Peterman also stressed that Rivian is not using carbon offset credits to meet its own climate goals.

According to 3Degrees, the climate firm that made Rivian’s proposal to Verra, the additional revenue will enable the carmaker to pass on cost reductions to EV owners through lower costs of EV chargers. The climate solution provider also said that “successful project validation and verification is not guaranteed” so the critics come too early.

Rivian’s Carbon Credits from EV Chargers Under Review

Verra, the world’s largest carbon credits certifier and issuer, is still in the process of reviewing Rivian’s project proposal. So there are no carbon credits issued or sold yet.

In 2018, Verra published a methodology on how entities become eligible to generate carbon credits for reducing emissions through EV charging systems. Since then, the nonprofit organization has approved projects and issued the corresponding credits. But some proposals remain under review, including Rivian’s.

Verra emphasized that for a project to be approved, it has to meet safeguards to be additional, including:

Below 5% of the maximum adoption potential for EV charging system’s penetration level

Expansion of EV chargers is not mandated by government regulations

With that, Rivian’s proposal does not cover EV chargers in states where existing government crediting programs are in place. So the EV maker didn’t include Oregon and California, for instance.

From the point of view of a Rivian SUV owner, the issuance of carbon credits seems to be questionable if it doesn’t incentivize people (to use EVs and install home chargers). He said that he will charge his car at home, whether or not he buys a charger from Rivian.

But he also stressed that EVs are a good alternative to gas-powered cars. They emit less pollution and cost much less to drive – $30 for electric power vs. $100 for gas. So, he is for carbon credits that make the shift to electric cars more possible.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")

and Carbon Capture and Storage (CCS): A Primer")