Nuclear energy stocks are rising as the U.S. government backs advanced reactors. This supports growing electricity demand and boosts energy security. Companies such as Oklo Inc., NuScale Power, and Centrus Energy are at the center of this shift.

The Trump administration recently approved plans for the U.S. Army to deploy advanced microreactors for defense and research. This move shows stronger support for nuclear innovation. It also reflects a rising interest in compact, reliable power systems for military bases and remote locations.

New U.S. Policies Spark Investor Confidence

The new White House directive speeds up the deployment of small nuclear reactors (SMRs). This change falls under national security rules. These microreactors offer continuous, low-emission power. They work well in areas where grid electricity is unreliable or missing.

Government contracts will likely reach several billion dollars in the next decade. This is because the Department of Defense is testing modular systems for energy resilience.

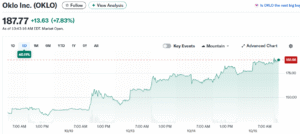

Investor confidence followed immediately. Centrus Energy (LEU) shares have risen sharply this year, supported by strong demand for nuclear fuel. Oklo (OKLO) shares jumped over 700% in the past 12 months, one of the biggest rallies in the clean-tech sector.

NuScale Power (SMR) showed strong financial growth. In Q2 2025, revenue reached USD 8.1 million, up from just $1 million the previous year. They also have nearly $490 million in cash reserves to support future projects.

Market analysts call this a turning point. One industry source told CNBC.

“We’re finally seeing advanced reactors move from prototypes to contracts. That opens the door to real commercial deployment.”

The Janus Program: Power for the Battlefield

The core of this new defense strategy is the U.S. Army’s Janus program. It aims to build and test mobile nuclear microreactors that can generate 1 to 5 megawatts (MW) of power. These small reactors are designed to supply reliable, carbon-free electricity to remote bases and defense sites where fuel delivery is difficult.

Companies like Oklo and Nano Nuclear Energy are developing early designs that can be transported by truck and set up in days. The goal is to reduce diesel use, improve energy security, and keep missions running even if grids fail.

The Army expects to test the first units later this decade. If successful, Janus could change how the military powers its global operations — cleanly and independently.

Why Nuclear Power Is Back in Demand

Global electricity use is climbing fast. The International Energy Agency (IEA) expects global electricity demand to grow three times faster by 2030 than it did in the last decade. Artificial intelligence, data centers, electric vehicles, and electrified industries are driving much of that growth.

Traditional renewables such as wind and solar are vital but intermittent. Nuclear power can run 24 hours a day, providing the steady, carbon-free energy needed to balance modern grids.

The IEA estimates that small modular reactors could have 40 gigawatts (GW) of global capacity by 2050. In a high-investment scenario, this could rise to 120 GW. That’s equivalent to more than 1,000 modern reactors operating around the world.

The Expanding SMR and Microreactor Market

SMRs are smaller, safer, and faster to construct than traditional nuclear plants. They can be built in factories, shipped by truck or rail, and installed near industrial sites or military bases.

Industry estimates value the global SMR market at $7.5 billion in 2025, projected to reach $16.1 billion by 2034, with a compound growth rate near 9%. Other forecasts, like those from BloombergNEF, predict the market could hit $40–50 billion by 2035. This depends on how fast governments make approvals easier.

Investment in SMR and microreactor projects has risen over 65% since 2021, says the Nuclear Energy Institute (NEI).

Microreactors—miniaturized versions producing under 20 MW—are gaining traction for military and research use. Studies show the levelized cost of electricity (LCOE) could be $48–78 per megawatt-hour.

Federal tax credits may reduce costs by up to 25%. They are a good option for remote sites or industrial operations. Diesel generators can be expensive and polluting, so these alternatives become competitive.

Inside the Race: Oklo, NuScale, and Centrus Take the Lead

Oklo Inc. is developing compact fast reactors using advanced fuels. Its first projects aim to deliver reliable power for military and industrial users. Oklo’s model focuses on selling long-term energy contracts rather than just hardware, positioning it for recurring revenue.

NuScale Power is the most advanced among U.S. SMR developers. The 77-megawatt reactor design is certified by the U.S. Nuclear Regulatory Commission (NRC). The company plans to deploy its first commercial modules with utilities and government agencies later this decade.

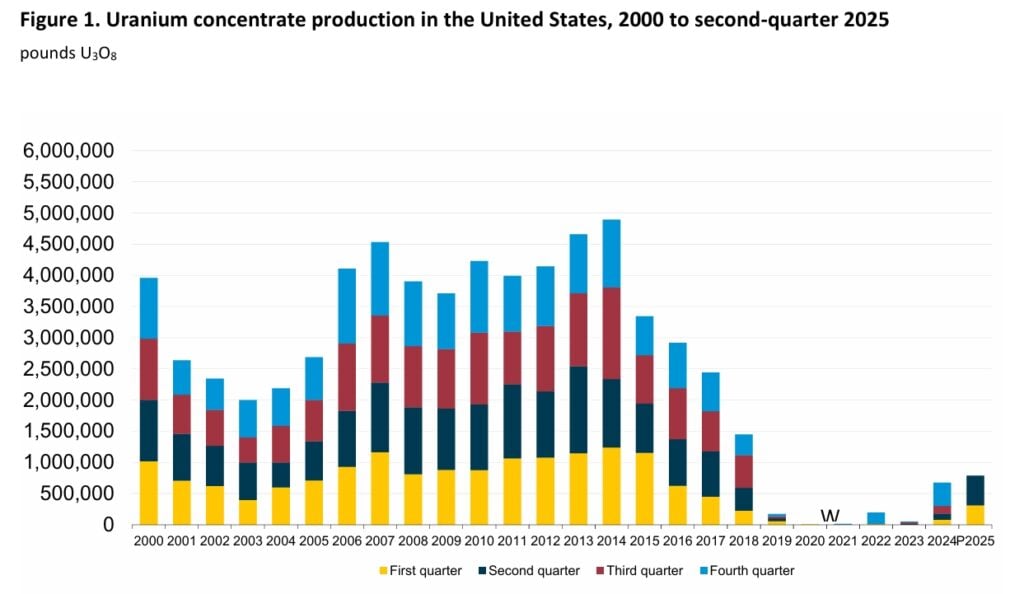

Centrus Energy is the only U.S. producer of high-assay, low-enriched uranium (HALEU). This fuel is essential for next-generation reactors. Its Ohio plant began enrichment in 2024, marking the first domestic production of this type of fuel in over 40 years. As Oklo and NuScale expand, HALEU demand is expected to rise sharply.

Together, these companies represent the full nuclear value chain — from design and deployment to fuel supply — forming the backbone of America’s new nuclear ecosystem.

Industry Tailwinds Point to Long-Term Growth

The IEA says nuclear investment needs to rise from $5 billion today to at least $25 billion each year by 2030. This is crucial to meet climate goals. By 2050, total nuclear investment could reach $670 billion, as new builds replace aging reactors and supply clean electricity to expanding grids.

Nuclear energy currently provides about 9% of global electricity, but that share could rise to 12–14% by 2040 if planned projects succeed. New modular designs could reduce construction time by half. This means faster deployment than traditional plants.

Economic models show that after a company successfully builds its first SMR, it can replicate the process. This can cut costs by 20–30% for each new unit. This follows a “factory learning curve,” much like what we see with solar and wind power.

The main growth drivers are:

- Government policy: Nuclear power is now listed as a critical technology in several national energy strategies.

- Technology improvements: Factory-built reactors reduce costs and risks.

- Rising demand: The surge in AI, EVs, and industrial power needs favors firm, clean energy.

- Fuel security: Domestic HALEU supply reduces reliance on imports.

Challenges include:

- Regulatory hurdles remain high, with licensing often taking 5–10 years.

- Construction delays and cost overruns have hurt investor confidence in past decades.

- Competition from other clean technologies—like hydrogen and long-duration storage—continues to grow.

Analysts caution that while optimism is justified, many small reactor developers will need years before generating revenue. “Policy momentum is there,” said one NEI analyst, “but execution will determine who wins this race.”

Outlook: Nuclear Power’s New Phase

The U.S. Army microreactor initiative underlines a turning point in federal energy planning. Nuclear energy is making a comeback. Both the government and private investors support it. This shift highlights its importance for national security and clean power.

The IEA estimates nuclear generation must expand by roughly 80% by 2050 for the world to stay on track toward net-zero emissions. Achieving this requires faster approvals, predictable regulations, and consistent financing.

For investors, companies like Oklo, NuScale, and Centrus offer exposure to one of the most ambitious technology transitions in the energy sector. Their combined progress will help determine whether the U.S. can build a stable, low-carbon power system for the age of electrification.

Is Still Gaining Ground")