Stock and the Future of Green AI: What Investors Should Know")

As artificial intelligence transforms industries, it also increases energy demands. And NVIDIA (NASDAQ: NVDA) is stepping up in this game. It leads the AI hardware market and is now a key player in energy-efficient computing while making bold sustainability promises.

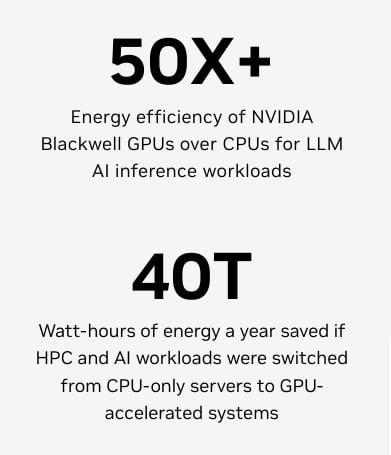

For green-focused investors and corporate leaders, NVIDIA offers a unique opportunity. Its innovative Blackwell GPUs provide up to 50 times more energy efficiency than traditional CPUs for AI tasks. By fiscal 2025, NVIDIA plans to use 100% renewable electricity for all its offices and data centers.

This makes NVDA stock a top tech choice and a solid bet on climate-smart computing. Let’s dive deeper.

How NVDA Stock is Benefiting from AI Growth and Climate Responsibility

NVIDIA’s financial success in 2025 stems from tech strength and climate focus. In fiscal year 2025, NVIDIA reported $130.5 billion in total revenue, a 114% year-over-year increase.

In the first quarter of fiscal 2026 (ending April 27, 2025, earnings hit $44.1 billion, a staggering 154% rise from last year.

This growth didn’t just benefit shareholders; it also funded sustainability efforts worldwide. The chip giant shows that innovation and environmental commitment can co-exist. And is the key to attracting carbon-conscious investors seeking returns and impact.

Micron Boosts NVIDIA Stock

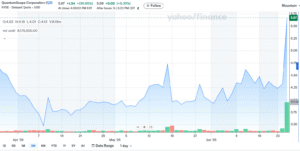

NVIDIA’s solid financial performance strengthens its position in AI hardware and clean computing. Recently, NVIDIA stock (NVDA) rose over 2.6%, reaching a high of $152.97. This reflects investor confidence in its strong standing in AI markets.

A key factor in this rally was anticipation around Micron Technology’s earnings. Micron supplies high-bandwidth memory (HBM) chips, essential for NVIDIA’s advanced AI accelerators. Micron’s report revealed high demand in the AI hardware supply chain. This news raises optimism about NVIDIA’s future.

Blackwell GPUs: Slashing Emissions Through Speed

Now talking about NVIDIA’s green innovation. It centers on its Blackwell GPU architecture. These chips are designed for AI inference tasks and are over 50 times more energy-efficient than older CPUs.

Here’s how they achieve this:

- Acceleration Efficiency: Blackwell GPUs complete complex tasks faster, allowing systems to use less power during idle times.

- Smart Power Controls: Features like power gating turn off unused GPU sections to save energy.

- Advanced Voltage Management: This ensures efficient power delivery without overspending on energy.

- Optical Interconnects: Innovations reduce connection power from 39W to just 9W, saving megawatts in large AI data centers.

According to NVIDIA, the Grace Blackwell Superchip offers 25 times better energy efficiency for large AI model inference compared to its predecessor. Upgrades, like moving from NVL8 at FP8 to NVL72 at FP4, have led to up to 130 times more tokens per megawatt. This means smarter AI at a lower energy cost.

- If widely adopted, Blackwell architecture could save nearly 40 trillion watt-hours annually, enough to power 5 million U.S. homes.

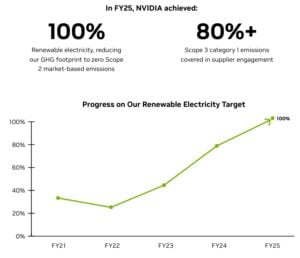

100% Renewable Electricity Milestone Achieved

NVIDIA reached a major sustainability goal in FY25: powering all its global offices and data centers with renewable electricity. This achievement removes Scope 1 and 2 emissions from operations directly under its control.

- In FY2025, total scope 1 and scope 2 emissions totaled 12,952 metric tons of CO₂ equivalent

The company achieved this through:

- On-site solar and wind systems across 22 campuses

- Renewable energy purchase agreements and grid partnerships

- Over 110 renewable projects worldwide

In FY24, it was at 76% renewable electricity. The rapid jump to 100% in just a year shows its commitment to climate leadership. This focus on green energy adoption makes a difference in this high-energy consumption sector.

Tackling Scope 3: Supply Chain Decarbonization

NVIDIA has cut operational emissions, but its Scope 3 emissions are still high. These emissions, mainly from its supply chain, make up 98% of its total footprint. The company is working with suppliers that generate the most emissions.

By FY25, it engaged suppliers covering over 80% of its supply chain emissions, surpassing its target of 67%. The goal is to encourage suppliers to adopt science-based targets for emissions reduction.

- NVIDIA aims to cut supply chain emissions by 30% from 2020 levels by 2030. That’s a significant challenge, but it reflects a strong commitment to sustainability.

Powering Real-World Climate Solutions

NVIDIA’s climate impact extends beyond its internal targets. Its technology enables climate solutions across sectors:

- Climate modeling and forecasting

- Wildfire prediction

- Smart grid management

- Precision agriculture and sustainable land use

Compared to traditional CPU systems, NVIDIA-powered data centers can lower energy costs by up to 42%. This is a strong incentive for businesses balancing AI growth and sustainability goals.

NVIDIA provides great value for eco-friendly, tech-savvy investors. It leads in innovation. It offers energy-efficient AI systems. Also, it’s gaining traction in sustainability.

Green500 Rankings Confirm Energy Efficiency Leadership

Another interesting fact is that real-world results back up NVIDIA’s claims. In November 2024, eight of the top ten Green500 supercomputers, ranked for energy efficiency, used NVIDIA hardware.

The JEDI system in Germany ranked first. It achieved over 1,000 times better energy performance than older systems for AI workloads. These achievements highlight that NVIDIA is leading in energy-efficient high-performance computing (HPC).

NVIDIA’s Carbon Market Readiness and Investor Edge

As carbon pricing grows worldwide, companies with low-emission practices are set for greater success. NVIDIA’s energy-saving tech cuts carbon emissions, which can lead to real value in new carbon markets.

This is especially true for data centers, undergoing a trillion-dollar AI-driven transformation. By offering solutions that cut carbon intensity per computation by up to 40%, NVIDIA becomes more than a chipmaker; it’s a carbon-smart infrastructure provider.

For investors aligning portfolios with climate goals, NVDA stock presents:

- Strong financial performance

- Clear sustainability outcomes

- Regulatory resilience through clean operations

- Leadership in climate-focused tech solutions

Investing in the Green AI Future

This study clearly shows that NVIDIA makes a strong case for investors focused on technology, emissions reduction, and ESG compliance. Its high valuation reflects big expectations. Being a green AI leader can offer significant long-term rewards. This is especially true as governments and markets shift their focus to carbon efficiency.

In short, NVIDIA is not just riding the AI wave; it’s shaping the sustainable future of computing. NVDA stock is worth considering for those seeking growth and green impact.

Stock Surges 35% as EV Battery Technology Drives Carbon Reduction")

Signs $2.6 Million Soil Carbon Credit Deal with Agoro Carbon to Meet its Net-Zero Goals")

: Boosting Carbon Credit Trust with Blockchain & Digital Climate Solutions")

$557M Shanghai Megapack Project: Powering China’s Clean Energy Future")