Carbon credits are becoming a major part of how the world fights climate change. A carbon credit represents the removal or reduction of one ton of carbon dioxide or equivalent greenhouse gas. Companies use these credits to meet emissions targets or to help reach climate goals.

By 2026, analysts predict that carbon markets will be growing quickly. More firms are integrating carbon credit strategies into their business models. Some generate credits directly. Others build markets or invest in credits. This article highlights the top public companies that stand out in the carbon credit space.

Carbon Credit Market: Key Facts and Stats

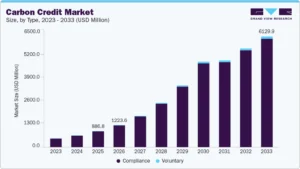

The global carbon credit market is already large, and it is expected to grow quickly in the coming years. In 2025, the total carbon credit market was estimated at around $887 billion.

By 2026, it is projected to reach about $1.22 trillion, driven by stricter rules and corporate demand for offsets. This growth reflects rising demand from companies and governments that want to meet climate targets and comply with emissions rules.

The market includes credits created for reducing emissions and credits created for removing carbon from the atmosphere. Markets fall into two main types: compliance markets and voluntary markets.

- In compliance markets, companies buy credits to meet legal limits.

- In voluntary markets, firms purchase credits to enhance their sustainability and climate goals, but are not required to do so.

Compliance markets currently account for most of the market’s size. Voluntary markets are much smaller, amounting to about ~$2 billion only.

Many countries have set up carbon pricing systems or cap‑and‑trade programs to limit greenhouse gases. Over 70 countries now use some form of carbon pricing or carbon trading, which helps drive demand and creates a large pool of buyers and sellers.

These statistics show that carbon credits are no longer a niche environmental tool. They have become a major global market linked to climate policy and corporate emission reduction strategies.

Here are the top carbon credit innovators to put on your radar this 2026 and even beyond.

Tesla: Leading Carbon Credit Revenue

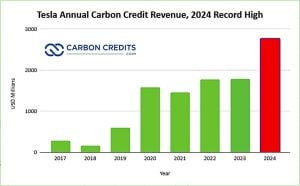

Tesla is known for electric vehicles, but it is also a major player in carbon credit markets. The company earns money by selling regulatory carbon credits to other automakers. These credits help other companies comply with emissions rules in the U.S., Europe, and China.

In 2024, Tesla earned about $2.76 billion from carbon credit sales, up from $1.79 billion in 2023. This marked a 54 % increase in one year and showed strong demand for emissions credits from legacy automakers.

Since 2017, Tesla has earned more than $10.4 billion from selling carbon credits. That revenue stream is crucial for the company’s finances. It matters more as competition in the EV market grows and profit margins shrink.

Tesla’s credits come from producing zero‑emission vehicles that exceed regulatory targets. Companies that cannot meet those targets buy the credits. This dynamic makes Tesla both a leader in EVs and an innovator in carbon compliance markets.

Carbon Streaming Corporation: A New Model for Credits

Carbon Streaming Corporation is a different kind of public company focused on future carbon credits. Rather than building carbon projects itself, it finances project developers around the world and receives rights to future carbon credits in return.

This model works like a royalty or streaming deal. Carbon Streaming pays upfront to help projects get built. In exchange, it receives credits over time. This gives investors exposure to carbon credits without the complexities of running a project.

Carbon Streaming is listed on Canadian and U.S. markets under tickers such as NETZ and OFSTF. As carbon markets grow, the model could expand. More credits might come from forest protection, clean energy, or carbon capture programs. These would then boost its balance sheet.

This approach means Carbon Streaming can benefit from rising carbon prices and volumes in compliance and voluntary markets. Investors looking for direct exposure to carbon credit supply may find its growth model interesting.

Intercontinental Exchange: Exchange Infrastructure for Carbon Markets

Intercontinental Exchange (ICE) is a financial markets company known for running major exchanges. ICE supports carbon markets by providing the infrastructure for trading carbon allowances and credits. This includes platforms for compliance markets like the European Union Emissions Trading System (EU ETS) and other regional cap‑and‑trade programs.

Carbon credits and emissions allowances traded on ICE help companies meet regulated limits. By offering transparent pricing and reliable settlement, ICE reduces barriers for institutional participation. As carbon pricing systems expand globally, the need for strong trading infrastructure grows, too.

ICE is not a carbon credit producer. Instead, it is a market facilitator. Its platforms help buyers and sellers discover prices and exchange credits efficiently. This makes carbon markets more liquid and accessible for corporations and financial investors.

For investors, ICE provides exposure to the growth of carbon markets without tying performance to any single project or credit type.

Xpansiv: Leading Carbon and Environmental Commodities Exchange

Xpansiv is a technology company that operates one of the world’s largest carbon credit exchanges for voluntary environmental commodities. Its platform, the Carbon Business Line (CBL), is used by companies trading voluntary carbon credits and other climate‑linked assets.

Xpansiv’s system has handled more than 250 million metric tons of carbon dioxide equivalent (CO₂e) transactions since 2020. In 2025, weekly trading volumes often exceeded 300,000 tons, with most credits coming from nature‑based projects like forestry and land restoration.

Xpansiv has also expanded its listings to include removal‑only credits and CORSIA‑compliant aviation credits. Its new partnership with the Korea Exchange (KRX) seeks to create a carbon credit trading market in Asia. This will connect KRX to Xpansiv’s global platform. This could increase liquidity and price discovery in new regions.

Xpansiv offers investors a key role in carbon credits. It provides market infrastructure, which is important as trading volume and price visibility increase with rising demand.

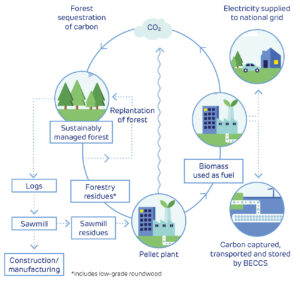

Drax Group: From Power Generation to Carbon Removals

Drax Group plc is a British power generation company listed on the London Stock Exchange. In recent years, Drax has expanded into carbon removal projects, including bioenergy with carbon capture and storage (BECCS).

Drax has a carbon removals deal. They will provide 25,000 metric tons of CO2 removals using BECCS credits. The price starts at $350 per ton. These credits represent permanent carbon storage rather than simple emissions reductions.

Drax’s core power business has used biomass fuel. Now, it is shifting focus to carbon removals. This change places Drax in markets where high-quality credits are in demand. As markets shift toward removal‑based credits, companies with validated removal projects may gain a strategic edge.

Drax gives investors a chance to tap into energy generation and new carbon removal credits. This area could grow as climate goals become more ambitious.

Why These Carbon Credit Innovators Matter

These companies represent different parts of the carbon credit ecosystem:

- Carbon revenue streams: Tesla shows how compliance markets can create meaningful income from emissions‑reducing products.

- Credit financing models: Carbon Streaming provides a way to invest in future carbon credits via streaming agreements.

- Market infrastructure: ICE and Xpansiv build the platforms that make carbon trading efficient and transparent.

- Carbon removal exposure: Drax participates in projects that generate high‑quality removal credits, helping meet tougher climate targets.

Key Carbon Market Trends to Track in 2026 and Beyond

Carbon markets will likely keep growing. This is due to stricter regulations and tougher corporate climate goals.

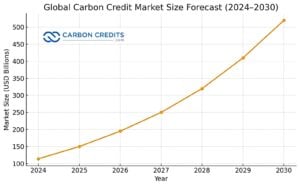

The chart above shows a steady and accelerating rise in the global carbon credit market from 2024 to 2030. Market size grows from just over $110 billion in 2024 to more than $520 billion by 2030, which signals strong and sustained demand.

The upward curve becomes steeper after 2026, suggesting faster growth as climate rules tighten and more countries expand carbon pricing systems. It also reflects rising corporate demand as companies use credits to meet emissions targets.

Overall, the chart supports the view that carbon credits are shifting from a supporting role to a core market tied closely to regulation, compliance, and long-term climate strategy.

Here are key trends that could shape carbon credit investing:

- Expansion of compliance markets: More regions are adopting emissions trading systems and carbon pricing.

- Quality of credits: High‑integrity removal credits are gaining attention from corporations and regulators.

- Voluntary market growth: Companies with net‑zero pledges will continue purchasing credits, especially removal‑based ones.

- Market access: Easier trading through exchanges and platforms will help investors participate.

Carbon credit markets are becoming part of corporate strategy and financial planning. The five companies reflect both business models and market mechanisms that matter for sustainability‑focused investors in 2026 and beyond.