The demand for quality carbon offsets is at an all-time high due to the strong eagerness of businesses to act on climate change. This leads to the fast and high growth of the carbon offset market.

For only a period of 2 years (2019 to 2021), it grew by 3x and reached $1 billion market value.

In fact, the Paris Agreement set up a fund of $100 billion to help finance projects that remove or reduce carbon footprint.

But apart from the demand alone, what could be the other reasons that drive such immense market growth?

If you’re asking the same question yourself, this article will give you the most comprehensive answer. It will identify the key drivers that promote the growth of the voluntary carbon offset market.

It will also discuss the other important factors that help grow the market and will continue to shape its development.

What are Carbon Offsets?

Carbon offsets are assets used to compensate for an entity’s carbon emissions. The offsets are from activities or projects that suck in carbon from the air. They’re also from initiatives that reduce future emissions.

As such, the credits produced by the projects represent the amount of carbon offsets that they deliver. They allow individuals, firms, and countries to offset their emissions.

- One carbon offset represents one carbon credit. And in turn, one credit equals one ton of carbon removed or prevented from entering the atmosphere.

When can you use carbon offset credits?

Carbon offset credits are best to use when emissions reduction solutions are not enough. In other words, they’re perfect for a “last-case scenario”.

Emitters can also use them as a short-term measure ahead of bigger emissions reduction plans. High-emitting sectors can use them to address their hard-to-abate emissions.

Large firms that are required by the government to account for and reduce their carbon footprint often use carbon credits as offsets. This refers to the compliance market where firms must meet the limit to their footprint.

But many big companies are also willing to invest their funds in projects that create carbon offset. They do this in the voluntary carbon market (VCM) often via carbon trading houses or exchanges.

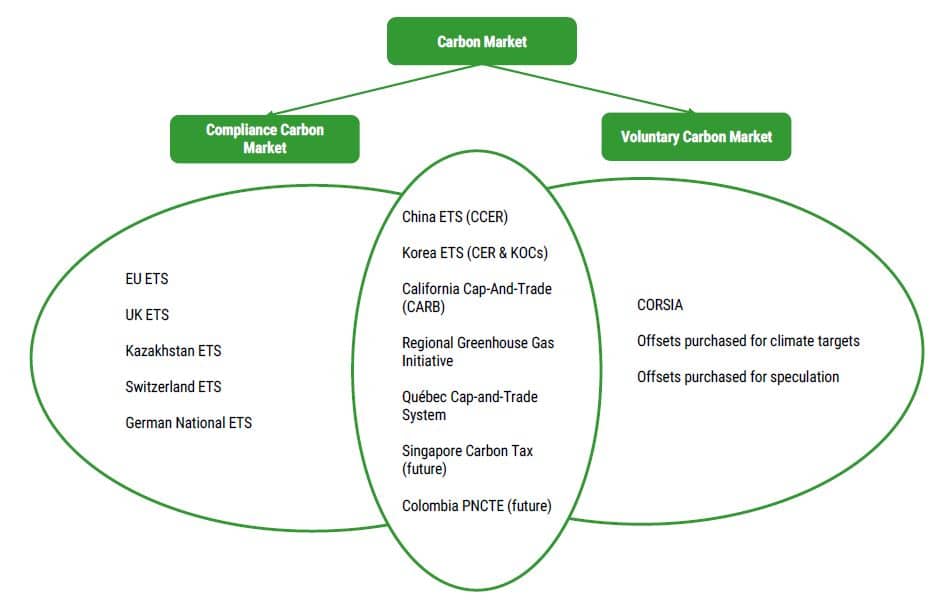

Broadly speaking, the compliance carbon market and the VCM are two separate carbon markets. Yet, there are instances where they overlap as the image below shows.

For example, the China Emissions Trading System (ETS) allows emitters to use carbon offset credits (CCER) to meet up to 5% of allowances or credits they need to account for in their report.

On the other hand, the EU ETS and the UK ETS don’t allow such use of carbon offsets.

Though the carbon offsets market is still in its infancy, its future holds a lot of promise for growth.

The increase in its market size from $306mn in 2020 to $1b in 2021 is solid proof of its rapid growth.

- In fact, analysts expect that the voluntary carbon offset market can reach a value of ~$35bn by 2030.

That’s under the net zero scenario where ~1Gt of carbon emissions must be offset by the end of the decade. The three key participants in the market are:

- corporations or business companies,

- institutional investors, and

- governments.

Here are the major factors that are responsible for promoting such growth in the carbon offset market.

3 Key Factors Driving Carbon Offset Market Growth

We’re highlighting the three key drivers of carbon offset market growth, followed by other minor factors.

#1. Rising Climate Targets

As mentioned earlier, there are three market players – corporate firms, governments, and institutional investors. Each of them contributes to the growing climate ambitions.

Corporate net zero pledges:

The whole world is seeing a rapid increase in offsetting demand from businesses. This is mainly because of the growing pressure on their responsibility to commit to their climate goals.

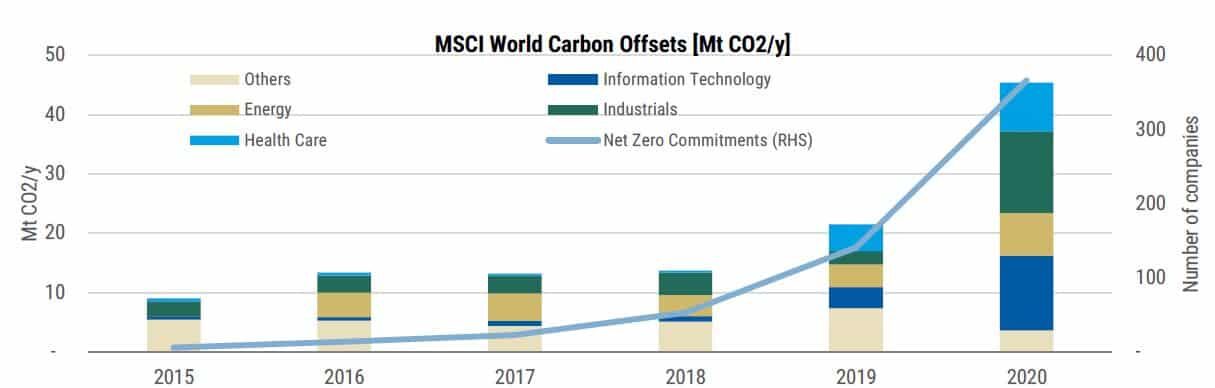

In fact, the net zero pledges from corporations continue to further rise. The graph below illustrates a specific case of the growth in carbon offset market by MSCI World. Its purchases rose in line with the rising number of net zero commitments.

The recent report on corporate net zero pledges for 2022 by Net Zero Tracker revealed that 702 companies on the Forbes Global 2000 have net zero targets. The number was up from 417 in 2020.

Carbon offsetting or buying carbon credits for emissions was found dominant among corporate net zero strategies. Yet, the net zero targets remain to be unacceptably low if the planet has to reach net zero emissions by 2050 according to the analysts.

Some firms will buy carbon offsets today to offset their current emissions. While others may do so to hold and retire them against future emissions to reach future targets.

Either way, we can expect that as companies near their key climate goal dates (as early as 2030), there’ll be more demand for carbon offsets.

Governments:

Same with corporate climate pledges, governments and nations were also eager to decarbonize. Countries that joined the Paris Agreement have set and submitted their plans for cutting their carbon footprint. They reflect these in their net zero goals via Nationally Determined Contributions or NDCs.

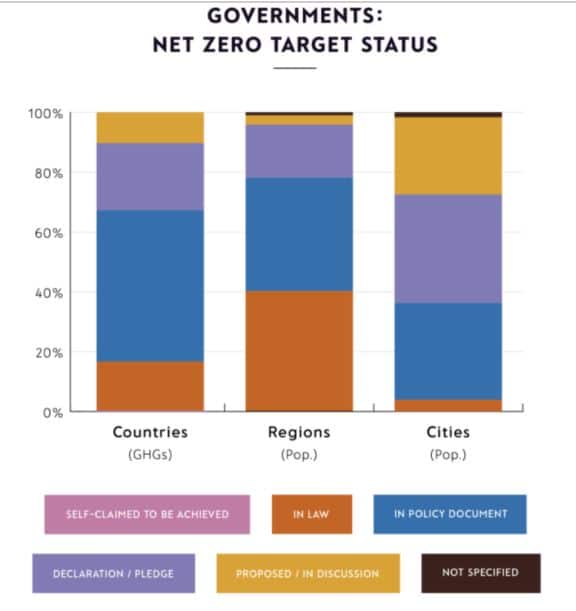

In fact, 18 out of 20 top emitters have declared their carbon neutrality or net zero pledges. There’s also a big increase in the number of national policies governing net zero targets. It went up from only 10% of national carbon emissions in 2020 to 65% in June 2022.

Plus, the count of large cities with a climate goal doubled, from 115 in 2020 to 235 this year. The chart below shows the current status of governmental net zero targets per level.

Though many are already in the law, most of them are also in policy documents waiting for approval.

To achieve their climate goals, countries use different means to cut their emissions. The common ones include carbon pricing mechanisms such as the ETS and carbon taxes. The most recent system introduced in the CBAM – carbon border adjustment mechanism.

For most of their unavoidable emissions, governments are turning to carbon offsets to address them. The Article 6 of the Paris accord allows nations to sell or buy carbon credits to count toward their NDCs.

But only one of the two participating countries can account for the emission reductions in its NDC. That’s to avoid the risk of double counting the offsets.

Institutional Investors:

Carbon emissions linked to the operations of the asset management industry are small. Yet, there’s a growing focus on how asset managers or institutional investors contribute to climate change. That’s through the allocation of capital to carbon intensive issuers.

For instance, the Net Zero Asset Managers (NZAM) Initiative now has 273 signatories that represent ~$60 trillion in assets under management (AUM). All participating firms commit to support investing aligned with net zero emissions by 2050 or sooner.

Signatories to the group agree to deliver some major commitments including:

- Setting interim targets for 2030 for the proportion of AUM in line with achieving net zero emissions

- Reviewing goals every 5 years to ensure that AUM covered by net zero commitment grows up to 100%

- Working in partnership with asset owner clients on their decarbonization goals

Across all key net zero strategies that investors can make, it’s not likely that they’ll see zero emissions across all portfolios. This means carbon offsets can also play an important role in executing their strategies.

But that’s best done if the offsets are for long-term carbon removal or would be the last resort only. There are no other viable options to consider to reduce emissions.

#2. Growing regulatory (compliance) and industry association requirements

If all participants in the compliance markets identified earlier were to use all their regulatory emission allowances with carbon offsets, it would total to 275 Mt CO2e. This is almost equal to the same size of the entire VCM today, which is 298 Mt CO2e.

When it comes to the growth of the carbon offset market due to the compliance market, there are 2 major things involved.

- Rising number of markets permitting the partial use of carbon offsets

- Increasing number of sectors joining the carbon markets

Though carbon offset credits used to be common in the VCM, we’re now seeing a rising trend of their inclusion in the compliance markets.

The China ETS is one example given earlier. Other examples are the case with Singapore and California.

The former expressed intention to include high quality carbon offset credits in its market mechanism. In the same way, California’s compliance market also plans to change carbon offsets from 4% this year to 6% in 2026.

Notably, the EU ETS remains strong in its stance to ban the use of carbon offsets and credits in its low carbon transition this decade.

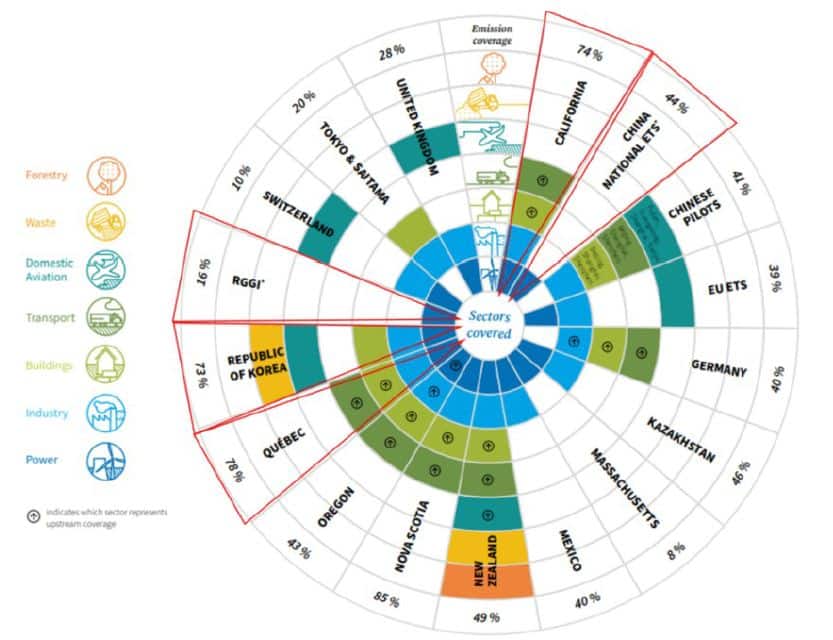

Moreover, forecasts show that many compliance markets will cover new sectors in the long run to reach net zero emissions. In effect, the emissions covered will also grow and so is the need for carbon offsets.

As the image below suggests, many compliance carbon markets still have a long way to go for growth when it comes to adding new sectors.

Take for instance the case of China ETS. It only includes the power sector in its regulatory emissions requirements. It’s the same for the Regional Greenhouse Gas Initiative (RRGI).

While for both the UK and EU ETS, they cover only 3 sectors right now out of the 7 major ones. These include the power, industry, and aviation sectors.

Also, many of those market mechanisms included the sectors that are easiest to decarbonize. So as new sectors that have less readily available decarbonization means will join the race to net zero, we can expect to see a higher reliance on carbon offsets.

#3. Increasing participation in the speculation market

Lastly, more and more buyers of carbon offset credits are using them to get exposure to the market. They’re buying the offsets to retire them in exchange for environmental impact later on.

This is where the carbon offset futures come in. For the direct exposure to the VCM, buying the futures can be a viable option as a retail investor. Market participants with this purpose continue to grow as forecasts see the carbon offsets price to rise over time.

As a result, they want more exposure and new investors keep on adding with the goal of selling the futures at a higher price later. Though the market is not yet liquid, estimates for carbon offsets demand are very promising.

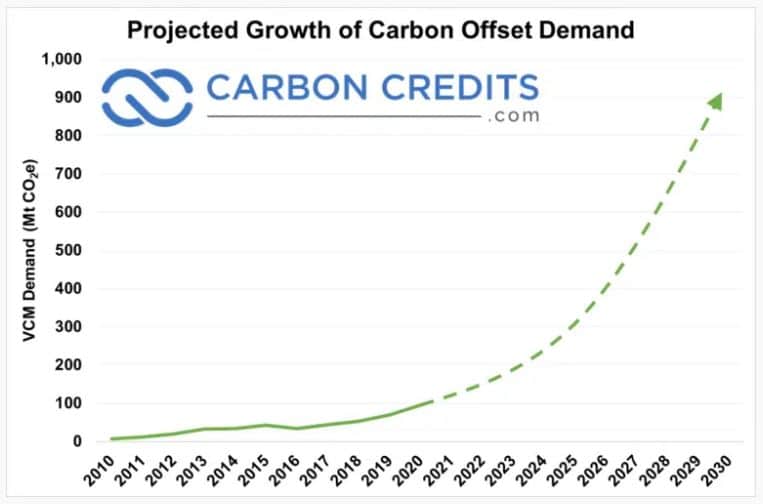

For instance, the Taskforce for Scaling Voluntary Carbon Markets (TSVCM) survey suggested that market size in 2030 can be between $5 billion and $30 billion. It can even grow into ~$50 billion at the high end of projection.

That means something between 20x and 200x growth for the carbon offset market within a decade. The chart below plots this high growth.

Other Drivers of VCM Growth

CORSIA:

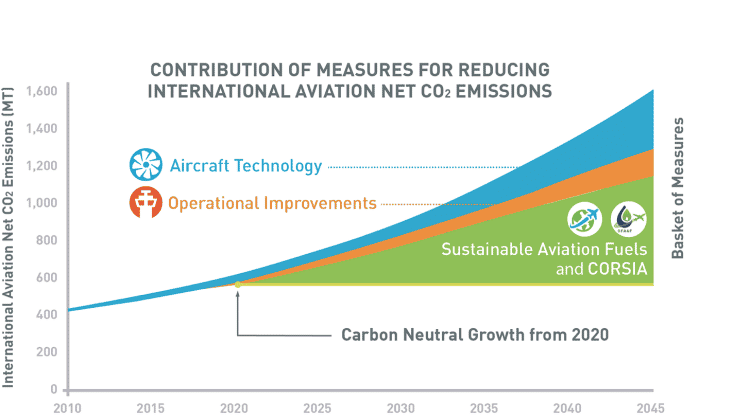

CORSIA is a market-based mechanism developed by the International Civil Aviation Organization or ICAO. It stands for Carbon Offsetting and Reduction Scheme for International Aviation.

It will drive further growth of the carbon offset demand as ICAO aims to bring the global aviation industry into carbon neutral level from 2020. This industry accounts for about 2% of global emissions but traffic is growing so fast.

Airlines can offset their emissions that go beyond the 2020 levels by buying CORSIA eligible offsets. CORSIA is one of the market-based measures that ICAO is using to achieve its climate goals. These measures take the largest contribution in reducing the aviation carbon emissions.

ICAO projects that, between 2021 and 2035, the CORSIA system will offset ~165MT of CO2e/year. This figure represents ~1.8x the size of the voluntary offset market in 2021.

With that said, major American airlines are already in the market buying carbon credits to offset their CO2 footprint.

The Carbon Crypto Movement:

Another recent driver of the VCM growth is the carbon crypto movement. Crypto currencies have been getting much media attention and investor interest. But as the crypto industry matures, developers started to apply blockchain to one of the other hot markets: carbon offset credits.

However, it’s also common knowledge that crypto mining uses very high energy. In fact, Bitcoin’s energy consumption equals the total electricity generated by the Netherlands. As such, many crypto mining companies committed to either preferring renewable sources or buying carbon offsets.

Plus, tokenization of carbon offsets is taking the market by storm by showing potential in resolving issues like verification and transparency.

Non-fungible tokens (NFTs) allow crypto carbon projects to issue NFTs for certain projects or particular pieces of offset projects. Though most of these carbon crypto initiatives are in their early stages, their ability to link carbon offsets to a blockchain avoids the issue of double-counting of carbon credits.

These unique features of the carbon crypto will drive NFT carbon offsets to grow even more. In effect, they will also bring more growth to the entire carbon offset market.

Top technologies improving the quality of the offset market

As more money pumped in the VCM continues to increase, the market is facing more criticism over time. For example, carbon leakage and permanence of the credits receives more scrutiny.

Luckily, recent advances in technological solutions emerge to help address those problems and improve the quality of the offsets. Here are the top 3 technologies that provide market solutions.

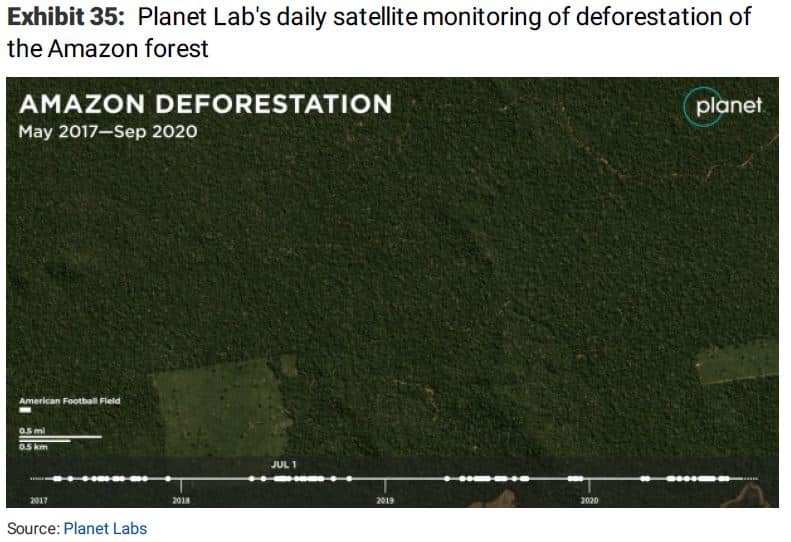

- Satellite Data/Imagery

Satellite monitoring provides critical environmental data from space. The major satellite remote sensing technologies offer plenty of environmental applications that can help farmers improve yields and reduce fertilizer use.

They are also useful in monitoring and verifying carbon offsets. They do this by providing insights into the use of land areas creating carbon credits.

For instance, satellite images can confirm the existence of a forest and track illegal deforestation activities. This can help tackle the permanence concerns with the forestry offsets by providing proof.

The image below shows an example of satellite monitoring of deforestation of the Amazon forest.

- Drones

Drones are unmanned aerial vehicles that can support data gathering activities. They also work alongside onboard sensors and global positioning systems (GPS).

Drones are very useful for many environmental purposes like reforestation and seeding projects. They can help speed up the process of surveying land areas, gathering topography information, and more. These are important for measuring carbon performance of a project.

Plus, drones can also be used to track deforestation but this can be quite costly right now.

- Machine Learning/AI

AI can help analyze data from satellites and sensors to boost transparency in using carbon offsets. It’s useful in analyzing a large amount of data that satellite imagery and sensors provide.

Machine learning can help in measuring carbon sequestered in trees, crops, and soil. This enhances the quality of carbon data for offset projects while also improving their verification.

The case of Pachama is a perfect example for the valuable use of this technology. The firm’s AI gives high assurance to buyers of carbon credits to reach their net zero goals.

With all these drivers combined, one can see why the growth of the carbon offset market is set to be exponential.

If by chance you’re in the market looking for the best offset programs to consider, read our top guide here. Or in case you want to know about the governance of this market, we also got you covered in this comprehensive article.