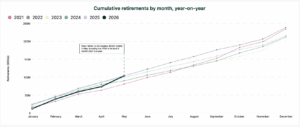

After several years of scrutiny, the voluntary carbon market (VCM) is showing signs of renewed strength. According to the latest H1 2026 report from AlliedOffsets, carbon credit retirements reached their strongest January-to-May performance on record.

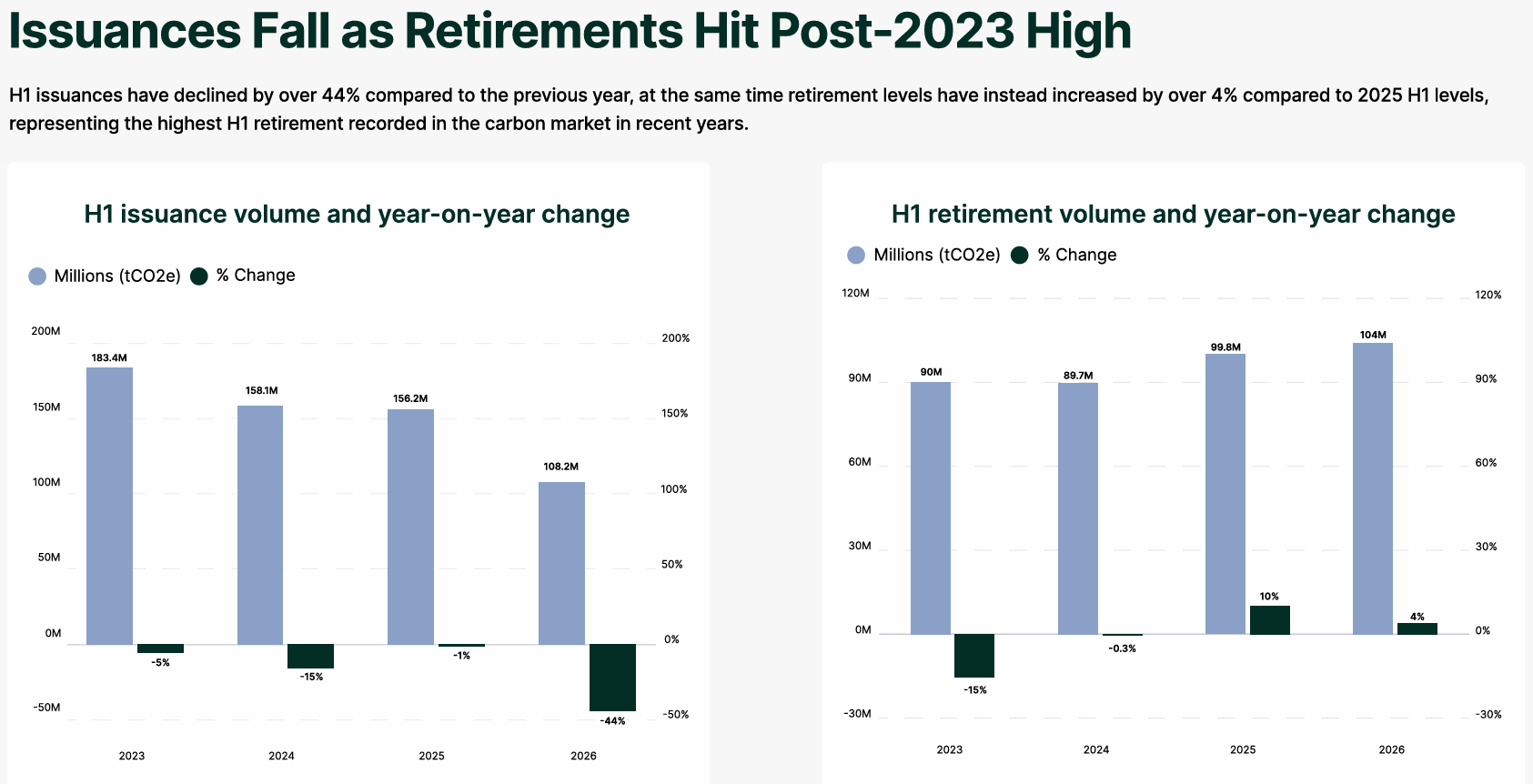

The numbers are notable because they come during a period of lower credit supply. In the first half of 2026, carbon credit issuances fell 44% year over year, but retirements went up 4%. This is the highest first-half retirement volume since AlliedOffsets started tracking the market.

A Rare Market Shift: Demand Is Rising While Supply Shrinks

The milestone shows the highest five-month start for the voluntary carbon market, which means buyers still use carbon credits. They do this even with ongoing debates about quality, regulation, and climate claims.

A major driver came in May, when Hess retired 12.5 million Guyana REDD+ credits. This helps push cumulative retirements to an all-time high for the January-May period.

The trend matters because retirements are widely viewed as one of the clearest indicators of real market demand. When companies retire credits, they permanently remove them from circulation and use them toward climate commitments. Unlike project announcements or future purchase agreements, retirements represent actual carbon market activity.

One of the most important findings from the report is that demand appears to be holding up despite a decline in new supply.

Global issuances dropped from 156.2 million credits in H1 2025 to 108.2 million in H1 2026. At the same time, retirements increased from 99.8 million to 104 million credits. This creates a very different market dynamic from previous years.

For much of the last decade, the carbon market struggled with excess supply. Large inventories often pushed prices lower and raised concerns about credit quality. Today, fewer new credits are entering the market while more credits are being retired.

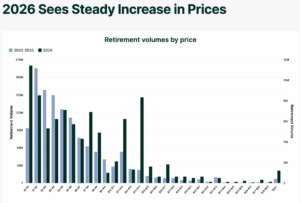

The carbon pricing data reflects that shift.

Buyers Are Paying More for Higher-Quality Credits

AlliedOffsets found that retirement volumes are increasingly occurring at higher price points. In 2026, buyers are more open to purchasing expensive credits. This is a change from past years when most retirements focused on cheaper credits.

That trend suggests a growing demand for higher-quality carbon projects rather than a race to secure the lowest-cost credits. Many companies now focus on stronger environmental integrity instead of just low-cost offsets. They want better verification and greater confidence in their climate impact.

This trend could help support pricing across the voluntary carbon market as demand increasingly favors quality over quantity.

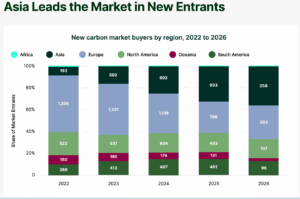

New Buyers Are Entering the Market

The market is also becoming more diverse. Active buyer participation in 2026 has already exceeded previous years, says AlliedOffsets. However, overall transaction volumes are still below the record levels of 2025.

Asia has emerged as the fastest-growing source of new entrants.

The report shows that more companies entered the carbon market from Asia than from any other region in 2026. This growth has been supported by initiatives such as Singapore’s Action for a Resilient Climate (ARC) Coalition, which aims to procure at least 10 million tonnes of carbon credits by 2030.

The trend reflects broader changes in global climate policy.

Many Asian economies have strengthened emissions targets, launched carbon pricing systems, and increased participation in Article 6 carbon market mechanisms under the Paris Agreement. As a result, carbon market demand is becoming less concentrated in North America and Europe.

Carbon Removal Is Scaling—But Supply Still Can’t Keep Up

The carbon dioxide removal (CDR) market is also evolving, although growth remains uneven.

AlliedOffsets reports that cumulative CDR offtake agreements have reached approximately 48.5 million tonnes, compared with only about 2.65 million tonnes of issued credits since 2022. This means demand commitments remain roughly 18 times larger than actual delivered supply.

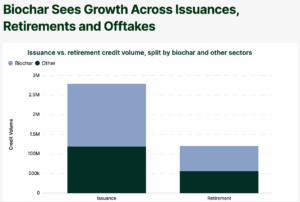

Biochar continues to lead the sector.

The pathway accounts for 57% of all-time CDR issuances and 53% of all retirements. Biochar has generated approximately 1.58 million credits out of 2.75 million total CDR issuances and remains the only removal technology delivering significant volumes across issuances, retirements, and offtake agreements.

Enhanced rock weathering is also gaining momentum. Offtake volumes increased from 10,000 tonnes in 2022 to 470,000 tonnes in 2025, while issuances continue to rise in 2026.

By contrast, direct air capture faces ongoing scale challenges. Although more than 2 million tonnes have been contracted, only about 0.1% has been issued to date. High costs, often ranging from $300 to $1,000 per tonne, remain a major obstacle.

Policy Developments Are Reshaping the Market

Government policies are becoming increasingly important for market growth.

The Paris Agreement Crediting Mechanism (PACM), the successor to the Clean Development Mechanism, now has 22 registered projects and has issued its first credits in 2026.

The inaugural Myanmar cookstove project generated 58,428 credits, roughly 40% below previous CDM estimates. This highlights stricter accounting standards under the new framework.

At the same time, Article 6 markets continue to expand. Countries such as Singapore, South Korea, Vietnam, Chile, India, and Cambodia have strengthened their carbon market infrastructure and international trading frameworks.

The aviation sector is also preparing for greater carbon credit demand. AlliedOffsets estimates that only 37.9 million tonnes of CORSIA Phase 1-eligible supply currently exist. This is far below the projected airline demand of roughly 200 million tonnes.

If those demand projections materialize, high-quality credits could become increasingly valuable over the coming years.

The Market Is Moving From Quantity to Quality

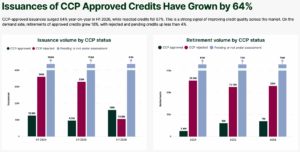

One of the clearest themes emerging from 2026 is the shift toward quality. CCP-approved credit issuances increased 64% year over year in H1 2026, while issuances from rejected projects fell 67%. On the demand side, retirements of CCP-approved credits rose 18%. This suggests that buyers are becoming more selective.

The trend aligns with broader developments across the climate sector. Investors, regulators, and standard setters are placing greater emphasis on transparency, additionality, permanence, and verification.

Recent updates from the Science-Based Targets initiative (SBTi), the growing use of Article 6 mechanisms, and stronger integrity frameworks are all pushing the market toward higher standards.

A New Phase for Carbon Markets

The record retirement volumes seen in early 2026 suggest that the voluntary carbon market may be entering a new phase. Supply is tightening. Prices are rising.

More buyers are entering the market. Carbon removal technologies continue to mature. Governments are building new compliance frameworks. And companies pursuing net-zero goals are increasingly looking for higher-quality credits.

Challenges remain. Issuances have fallen sharply, removal supply remains limited, and policy uncertainty still affects some markets.

Yet, the latest data show that demand has not disappeared. In fact, buyers appear to be becoming more selective and more willing to pay for quality.

That shift could help shape the next chapter of global carbon markets as companies, investors, and governments work toward increasingly ambitious climate goals.

READ MORE: IATA’s New Carbon Credit Alliance: Can Aviation Secure Enough Offsets for Net Zero?