Investment giant BlackRock has released a new report outlining key developments expected to impact low-carbon transition-related investment opportunities and risks in 2024.

BlackRock singles out low-carbon transition as a major investment driver while emphasizing specific areas, including clean energy, electrification, and climate resilience.

The report anticipates a significant reallocation of capital towards rewiring energy systems and investing in climate resilience to mitigate risks.

In the outlook for 2024, BlackRock identified three key areas that stand out as potentially shaping the market significantly.

Electrifying Expectations: Battery Prices and Market Dynamics

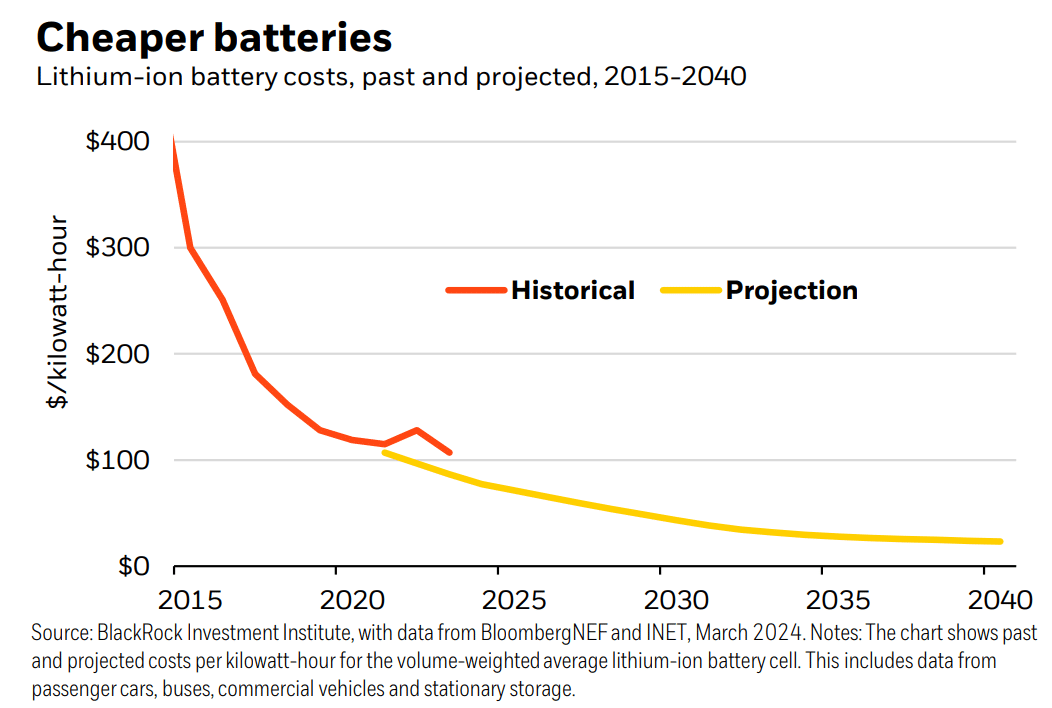

Firstly, the downward trend in battery prices has the potential to drive increased demand for energy storage solutions in power grid infrastructure and the adoption of electric and hybrid vehicles.

Battery prices makes up a significant portion, often a third or more, of the production expenses for various clean technologies. These include energy storage systems for power grids and electric and hybrid vehicles (EVs).

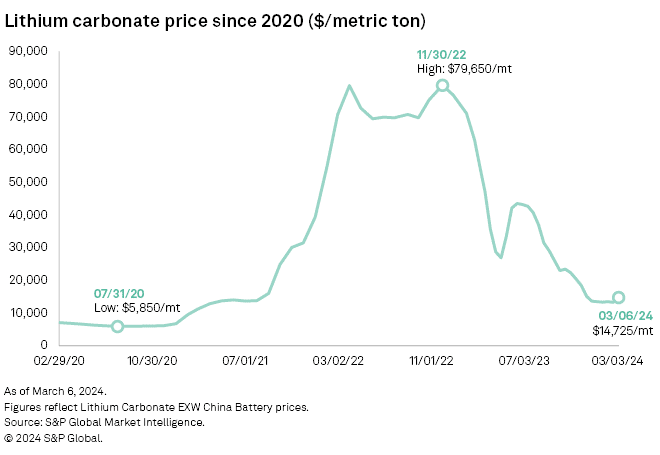

Over the past decade, there has been a notable decline in battery prices, as shown in the chart below.

While there was a slight uptick in 2022, recent signals from battery producers suggest the potential for substantial price reductions in the coming year. This downward trajectory can be primarily due to an 80% drop in lithium prices, a crucial component, driven by increased supply.

Intense market competition and rapid technological advancements also contribute to lowering prices. Some companies are leveraging artificial intelligence, another influential force, to explore novel battery materials, further driving down future costs.

The key question remains whether this continued decline in battery prices will translate into reduced final purchase prices. In turn, this can potentially spur greater demand for energy storage systems, EVs, and hybrid vehicles.

Given their lower operational costs compared to traditional internal combustion vehicles, such a trend could have significant implications for the broader automotive industry and energy sector.

Political Power Plays

Secondly, upcoming elections worldwide could significantly impact future energy and industrial policies, influencing the direction of transition efforts, per BlackRock report.

The year 2024 sees a multitude of elections across significant regions like the European Union, the United States, and India.

Governments worldwide are grappling with the delicate balancing act of pursuing decarbonization while ensuring energy security and affordability. The outcomes of these elections could profoundly influence how this balance is achieved and consequently impact the trajectory of the low-carbon transition and adoption of clean technology globally.

Many governments are actively subsidizing their energy and clean technology sectors, creating pricing and margin pressures for non-subsidized competitors.

Moreover, election results may prompt changes in transition-related policies, potentially either accelerating or slowing down the transition in different regions. For instance, in India, continuity in policy post-election could speed up decarbonization efforts and bolster the country’s position as a leading clean technology production hub.

Similarly, the outcome of the U.S. election could have implications for existing legislation, such as the Inflation Reduction Act of 2022, which has catalyzed significant investments in energy infrastructure and technology.

Possible changes range from repeal or delays to complementary policies aimed at enhancing its effectiveness, such as land permitting reform.

Weathering the Storm

Lastly, another crucial focus in 2024 revolves around the impact of climate change-induced extreme weather events, prompted by 2023 as the hottest year on record by the World Meteorological Organization. This trend is expected to continue this year, further highlighting the urgent need for climate resilience measures.

Investors are beginning to show greater interest in companies and technologies that contribute to climate resilience. This includes innovations such as early monitoring systems for floods, air conditioning solutions to combat heatwaves, and building retrofitting for enhanced resilience against extreme weather events.

Despite this growing interest, markets may still underestimate the potential for firms specializing in resilience-boosting products and services.

Overall, BlackRock anticipates that falling battery prices could stimulate growth in the EV and energy storage industries in 2024. However, the direction of the global transition policy post-election will heavily influence investment opportunities and risks. As physical climate risks mount, the report suggests that climate resilience could emerge as a prominent investment theme this year.

Apart from the transition to a low-carbon economy, BlackRock also tracks these four other mega forces:

- Demographic divergence

- Digital disruption and artificial intelligence (AI)

- Geopolitical fragmentation and economic competition

- Future of finance

BlackRock’s report underscores the dynamic landscape of low-carbon investments in 2024, driven by evolving market dynamics, political shifts, and climate resilience imperatives. As battery prices decline and election outcomes unfold, investors face both opportunities and risks in navigating the transition to a sustainable future.

RELATED:

RELATED: