Lithium, a vital elemental metal, also dubbed as “white gold”, has gained significant attention as a sought-after commodity. This is particularly due to its crucial role in battery manufacturing for electric vehicles (EVs).

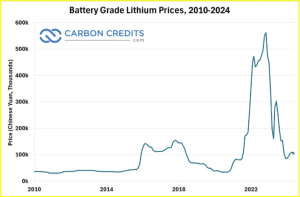

The surge in EV sales has fueled optimism among investors regarding companies involved in lithium production and refinement. Despite being a common substance, lithium prices experienced an astounding 1,000% increase from 2021 to the end of 2022. This exceeds the previous highs set in 2017.

However, the landscape changed in 2023.

An increasing supply of lithium from mines in Africa and Australia is putting downward pressure on prices. Plus, reports of lower consumer demand for EVs in the U.S. and China may further contribute to a decline in lithium prices.

Following the unprecedented boom of 2021/2022, stocks of lithium producers have faced significant declines due to a continued plunge in lithium prices as seen above.

As with all commodity stocks, lithium stocks are intricately tied to supply and demand dynamics in the underlying materials they deal with. The future trajectory of lithium prices and associated stock values will likely be influenced by the continued demand for EVs.

Investing in top lithium stocks follows a similar process to investing in any other type of stock.

Here are our top picks for lithium stocks that are worth each penny of consideration.

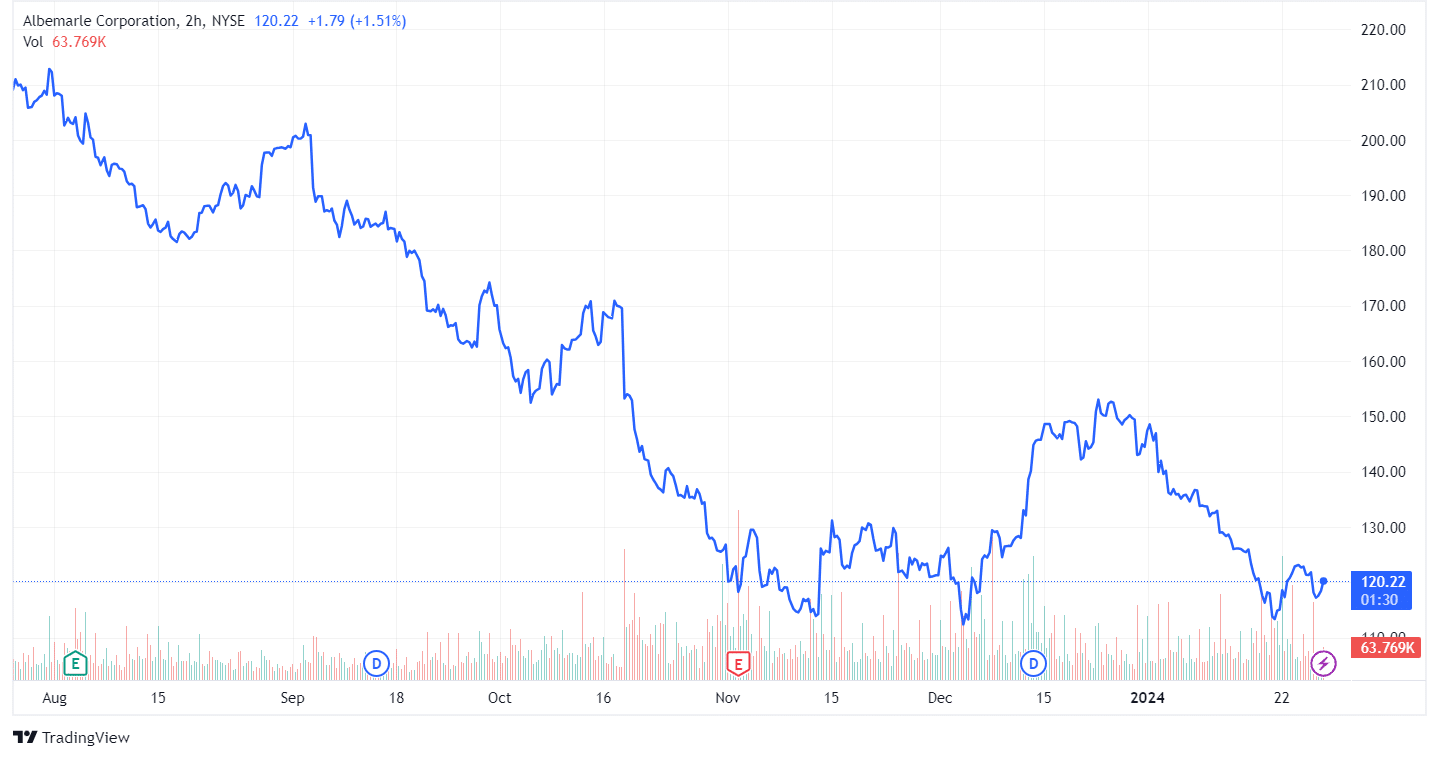

Albemarle Corporation (ALB)

Market cap: US$15.1 billion

Market cap: US$15.1 billion

Enterprise value: US$17.1 billion

Albemarle Corp. stands prominently among the largest lithium stocks and is a key player in lithium mining. With a market value comparable to other major commodities such as Barrick Gold Corporation (GOLD).

The company’s substantial scale and the optimistic long-term forecasts for EV demand position Albemarle as one of the top lithium stocks in the current market. Albemarle has embarked on a significant production expansion initiative in South Carolina, projecting an annual capacity of about 225,000 metric tons of lithium.

-

The American lithium giant anticipates this capacity to triple by the 2030, aligning its growth plans and expectations for the growing EV sector.

But recently, it redirected efforts towards its Kings Mountain lithium-spodumene mine resource in North Carolina, in response to softer market conditions.

Albemarle had warned of potential market share loss to Chinese producers after its unsuccessful takeover bid for Australian lithium producer Liontown Resources. The $4.2 billion merger was abandoned.

The largest producer of lithium for EV batteries has also revised its annual forecast downwards at the end of last year. They further reported a lower-than-expected quarterly profit due to declining prices for lithium.

Still, Albemarle now anticipates a 30% increase in lithium sales volume for the year. But with prices expected to rise only 15%, falling short of market expectations for robust growth.

The reduction in demand from consumers has led major EV manufacturers like Tesla, Ford Motor, General Motors, and Rivian to scale back production. Additionally, Toyota Motor has cut its EV sales forecast by 40% in 2024 due to lower demand in China. This reduced demand is impacting the lithium market and related stocks.

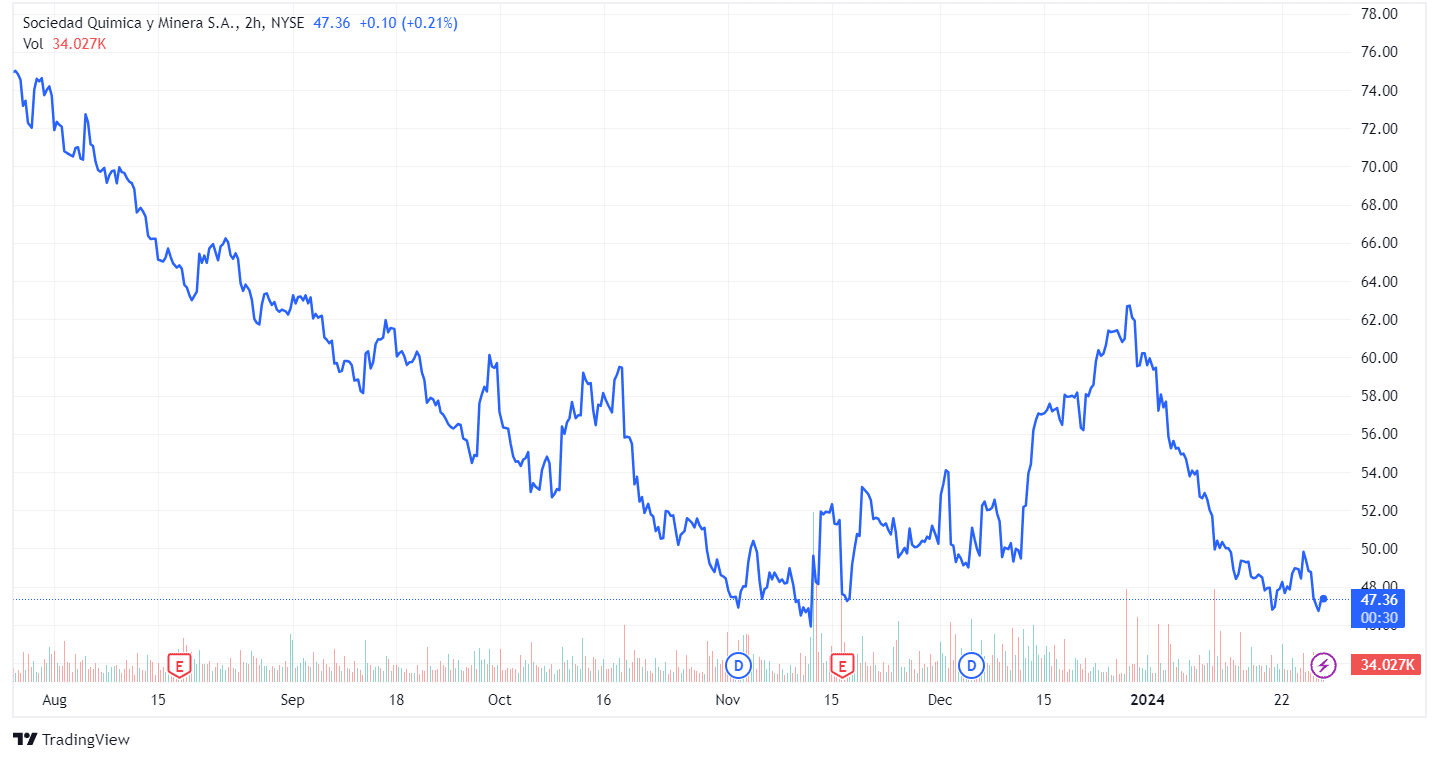

Albemarle’s peers have experienced similar declines. For instance, shares of Sociedad Química y Minera de Chile S.A. are down -39.4% YTD.

Sociedad Química y Minera S.A. (SQM)

Market cap: US$15.1 billion

Enterprise value: US$16.1 billion

Chile, globally recognized for its mineral wealth, features Sociedad Química y Minera de Chile (SQM) at the core of its mining industry. While SQM engages in the production of various minerals, its significance in lithium extraction is paramount.

Alongside diversified mining counterparts like Albemarle and Ganfeng, SQM maintains robust double-digit operating profit margins, substantial cash reserves for expansion, and minimal debt.

In 2022, SQM achieved its highest-ever corporate revenues, surpassing $10.7 billion in sales. A substantial 76% of this revenue was derived from lithium and related products.

SQM’s pivotal role goes beyond its economic contributions, as it stands as the largest taxpayer in Chile. Recent discussions about the government potentially increasing its stake in the company have emerged and raised eyebrows.

Such a move introduces the inherent risks associated with government ownership, including the possibility of political interference. Some investors don’t find it a favorable development.

The trajectory of SQM’s shares showed positive momentum until late 2022, when a decline followed. This is largely due to weakened lithium prices and concerns about the company receiving a fair valuation for the anticipated increased government stake.

The impending nationalization raises uncertainties about state control of lithium. Once this pushes through, it may impact SQM’s profitability.

Looking forward to a long-term demand for lithium to exceed supply, SQM has strategically invested in expanding its production capacity. These developments position the company to augment its market share in the lithium supply chain, particularly for EV batteries.

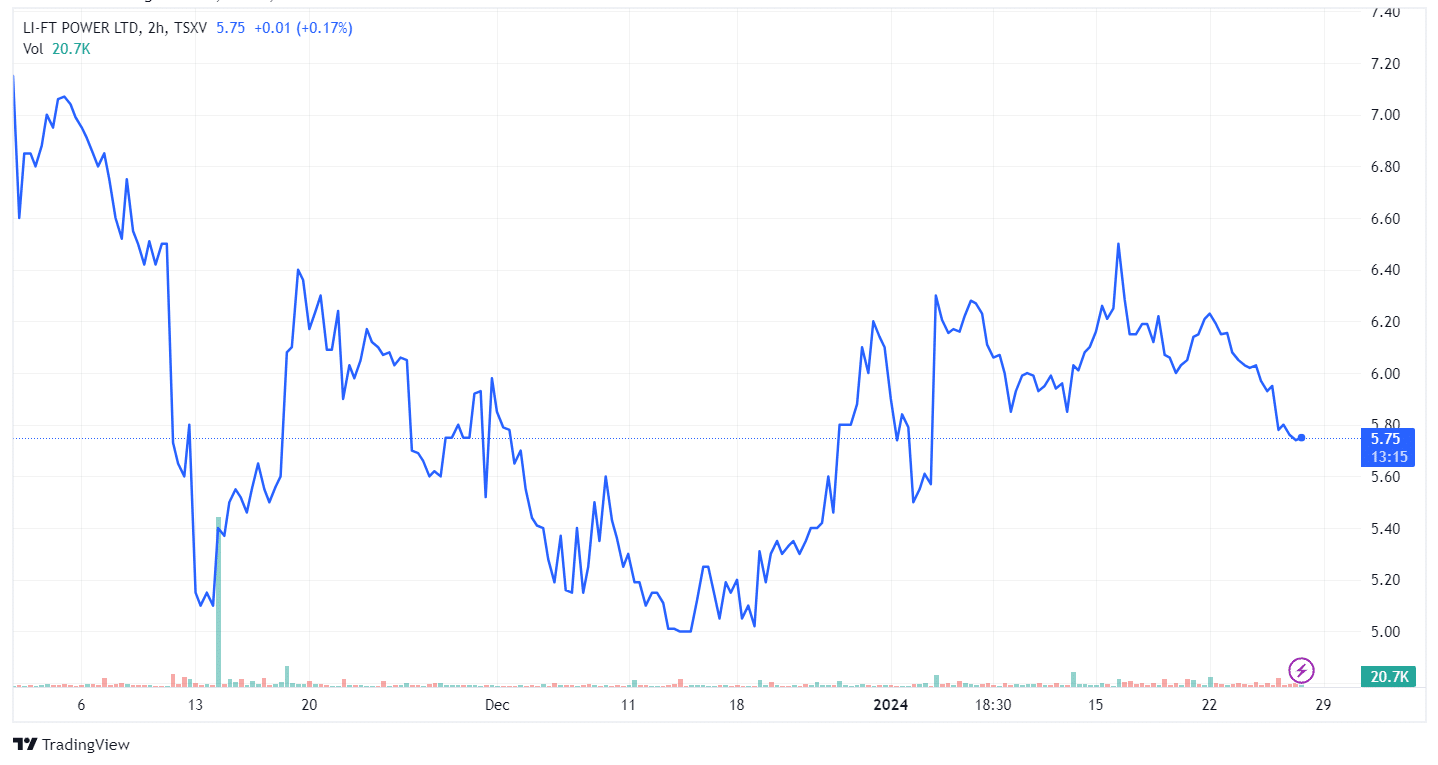

Li-FT Power (LIFT; LIFFF)

Market cap: US$168.5 million

Enterprise value: US$163.4 million

Given the insufficient domestic lithium reserves to meet demand, the U.S. is in a challenging position. With the need for a domestic supply, Canada is positioned to contribute to meeting U.S. lithium requirements. This is where a junior lithium company, Li-FT Power (LIFT: LIFFF), based in Vancouver, British Columbia, perfectly comes into the picture.

Li-FT has acquired promising lithium assets in Canada, starting drilling on their flagship project in June last year. The company’s investment thesis revolves around the aggressive exploration and expansion of high-grade lithium pegmatites to define world-scale resources in a proven mining jurisdiction.

The company’s strategy focuses on consolidating and advancing hard rock lithium pegmatite projects in Canada, particularly in known lithium districts. Li-FT Power aims to apply modern systematic exploration techniques to unveil value in these projects that historical work hasn’t fully realized.

The project portfolio includes assets in the Northwest Territories and Quebec, with flagship projects like the Yellowknife Lithium Project and the Pontax Project, which has revealed an 8km long lithium anomaly.

The company is well-financed to progress its projects, cementing its commitment to advancing the exploration and development of high-quality lithium assets in Canada.

The company is well-financed to progress its projects, cementing its commitment to advancing the exploration and development of high-quality lithium assets in Canada.

LIFT strategically positions itself to take advantage of weak industry sentiment, allowing for the acquisition of shares at discounted valuations.

The Lithium Deficit Looms

While those top lithium stocks are making waves in 2024, projections indicate that lithium prices will further decline due to:

- increasing supplies of the battery metal, and

- subdued demand from China.

In China, lithium carbonate prices have plummeted from an all-time high of $81,360 per tonne in November 2022. This is the lowest level in two years at $20,782 per tonne in the current month. As lithium carbonate prices have fallen by 67% year-on-year, Chinese refining companies are responding by cutting production or suspending operations.

This represents a nearly 75% correction due to a series of negative catalysts that have suppressed lithium prices. The situation is even more challenging for lithium hydroxide markets, primarily due to the sluggish performance of the nickel cobalt manganese battery sector compared to the lithium iron phosphate battery sector.

-

Australia, which contributes 40% of global lithium production, expects a decline in the spot price of spodumene from around $3,840 per tonne in 2022 to $2,200 per tonne in 2025.

Lithium miners are adjusting to the sharp drop in demand for EVs in China by reducing costs and scaling back production expansion plans.

This response aligns with the challenges faced by lithium producers globally as the market grapples with oversupply and weakening demand for EVs.

The inability of China to meet its own demand for lithium, despite being the world’s 3rd-largest producer, has significant implications for other countries that rely on Chinese lithium. This is why the US aims to develop its own lithium supply chain that doesn’t depend on China.

The Inflation Reduction Act, in particular, specifically promotes onshoring of clean energy manufacturing, including EVs, within the U.S. And that also means to reduce or cut off import of lithium from China.

Corinne Blanchard, Deutsche Bank’s director of lithium and clean tech equity research, is among the analysts predicting a future shortage in the lithium industry. Despite forecasting supply growth, she believes that demand will outpace it at a much faster pace.

Blanchard anticipates a “modest deficit” of around 40,000 to 60,000 tonnes of lithium carbonate equivalent by the end of 2025, but she foresees a much larger deficit of 768,000 tonnes by the end of 2030. This forecast aligns with the broader industry expectations of increasing demand for lithium, particularly driven by the growing EV market.

2024 unfolds with challenges for the lithium market, witnessing stock declines post 2023’s meteoric rise. Despite the setback, top players like Albemarle, SQM, and Li-FT Power strategically position themselves. As global trends hint at a Chinese lithium market decline, industry experts see a future lithium deficit, driven by the relentless growth in the EV market.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: LIFFF.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

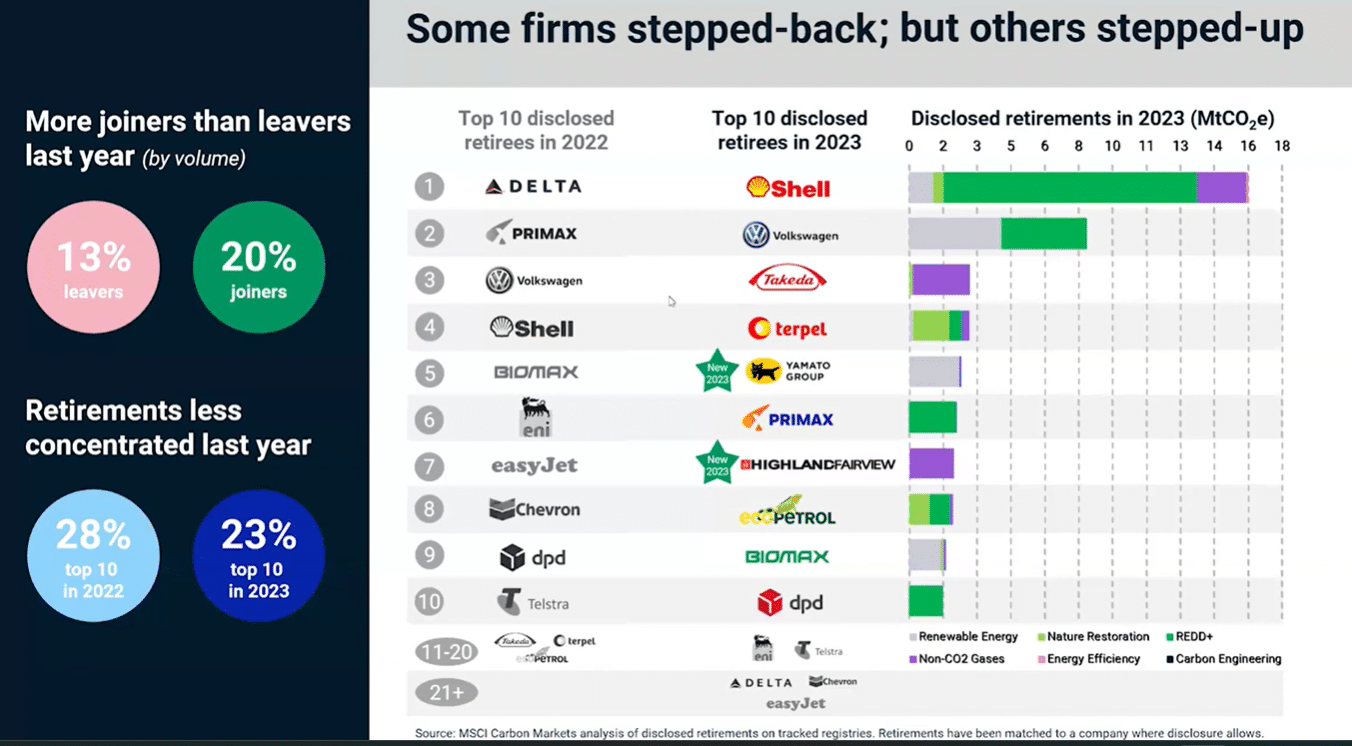

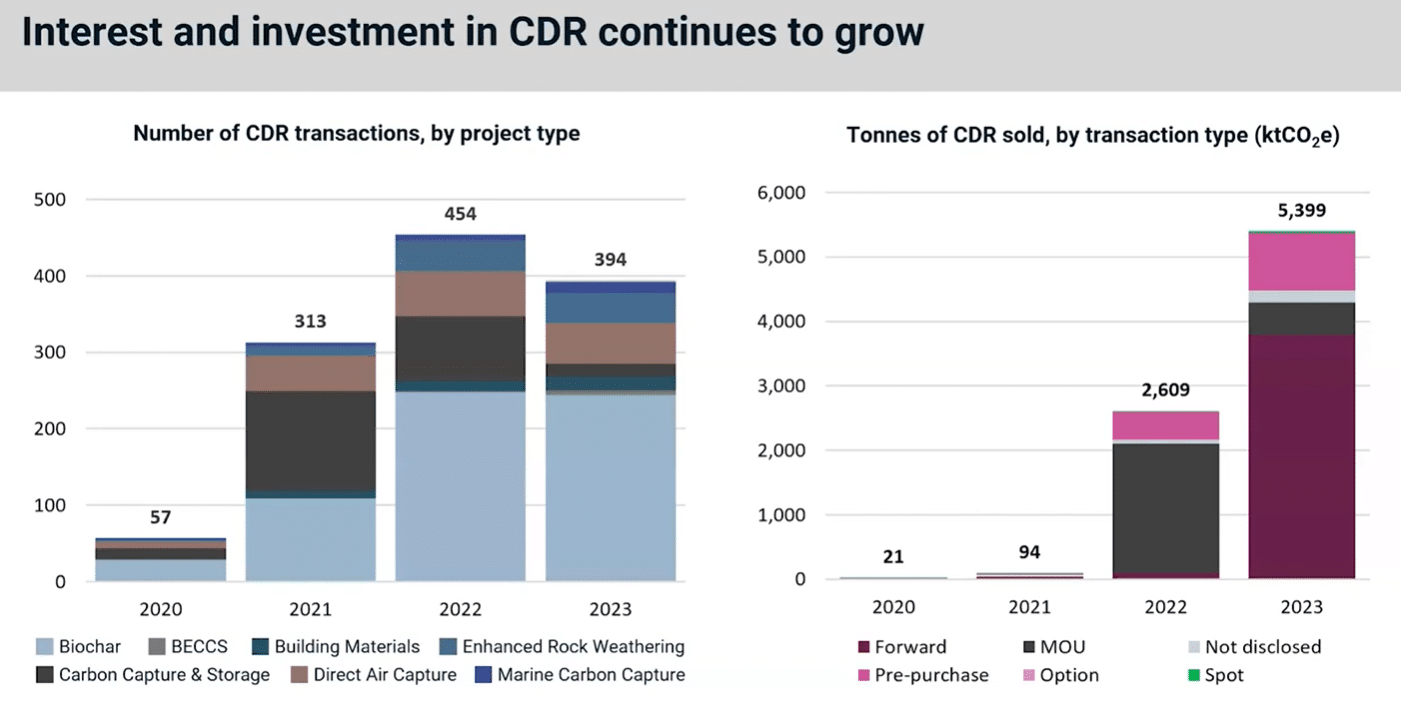

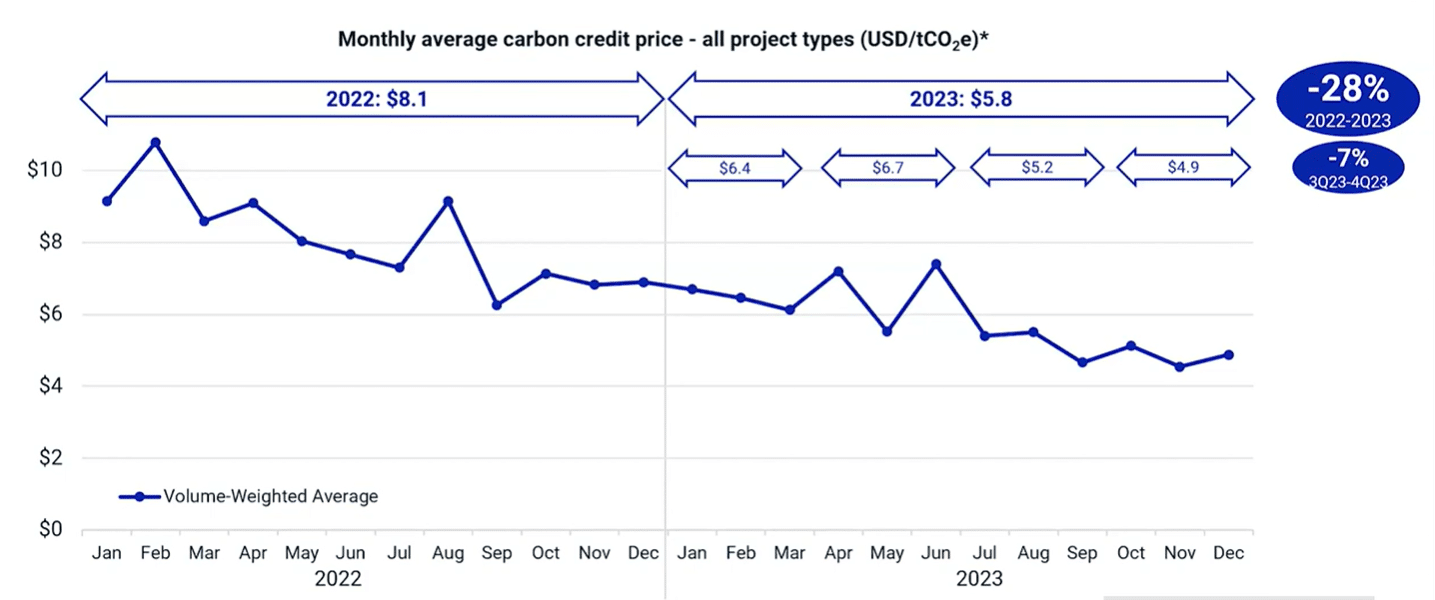

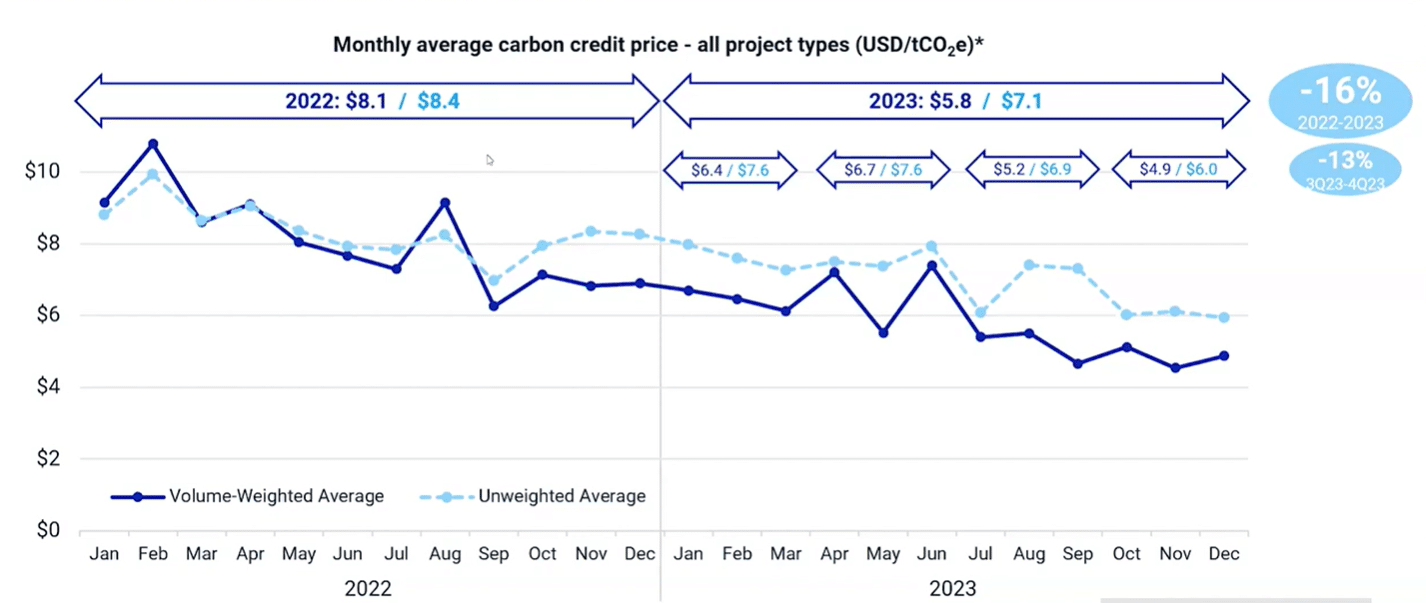

The Top 10 Credit Retirees

The Top 10 Credit Retirees