Are you looking for high-quality carbon offsets to address your harmful emissions? This guide will help you understand what’s offsetting all about, its benefits, and know what would be the best place to source the offsets.

High quality carbon offsets not only help individuals and businesses reduce their carbon footprint, but they can also have a positive impact on local communities and biodiversity. By supporting projects that focus on renewable energy, reforestation, and sustainable agriculture, carbon offsets can contribute to the development of clean technologies and create employment opportunities.

Additionally, investing in high-quality offsets provides a transparent and credible way to offset emissions, ensuring that the generated funds are effectively used for environmental conservation and social benefits.

Understanding Carbon Offsets

Carbon offsets are a way for your or your company or organization to voluntarily compensate for your carbon emissions. They allow you to invest in projects that reduce or remove an equivalent amount of CO2 from the air.

The main goal of this voluntary carbon market (VCM) mechanism is to balance out the emissions produced in one place by supporting carbon reduction or removal activities somewhere else. They’re often used as complementary strategy to address emissions that are challenging to eliminate completely.

When the reductions are verified, you then receive carbon offset credits. Each credit represents one metric ton of CO2 that has been either avoided or removed from the atmosphere.

By using these offsets, you can essentially cancel out your emissions. The idea is that the positive environmental impact of the offset project counterbalances the negative impact of the entity’s own carbon footprint.

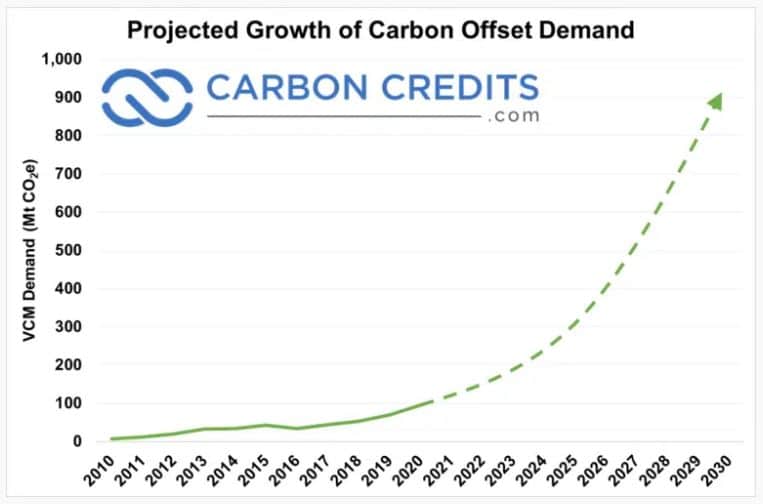

Projections show that the VCM has to increase 15x and reach $50 billion by 2030 to achieve the Paris climate goals.

It’s important to note that while carbon offsets can be a valuable tool in the fight against climate change, they’re not a substitute for directly reducing emissions at the source. The primary goal should always be to minimize carbon footprints through sustainable practices and technologies.

- READ MORE: How Do Carbon Offset Credits Work?

Why Choose High-Quality Carbon Offsets

Choosing high-quality carbon offsets is crucial for several reasons, as it ensures the effectiveness and integrity of offsetting efforts. And as the number of these credits issued to increase massively, you have to be more vigilant about the quality of the offsets you buy.

Choosing reputable projects with rigorous verification processes ensures that the claimed reductions are genuine. The high-quality offsets they produce make sure that the reductions are not counted more than once.

Moreover, the best carbon offsets go beyond just reducing emissions; they also bring about environmental and social benefits.

For example, reforestation projects can enhance biodiversity and provide livelihoods for local communities. Choosing high-quality offsets from these initiatives allows you or your company to contribute to broader sustainability goals beyond just carbon mitigation.

There’s a catch though: you need to assure that the seller or provider of the offsets is credible.

Assessing the Credibility of Carbon Offset Providers

Weighing credibility involves looking at various factors such as the provider’s track record, transparency, adherence to standards, and the quality of their offset projects.

There are various standards and certifications that can guide you to the best place to buy high quality carbon offsets. These primarily include the Gold Standard, the Verified Carbon Standard (VCS) of Verra, American Carbon Registry, Climate Action Reserve, and Plan Vivo.

- Verra’s VCS – focuses on GHG reduction attributes and doesn’t require projects to have additional environmental or social benefits.

- Gold Standard (GS) – created by the WWF, focuses on projects that provide lasting social, economic, and environmental benefits.

- Climate Action Reserve (CAR) – a certification body or registry for the North American carbon credit market.

- American Carbon Registry (ACR) – the regulatory body of the California cap-and-trade offset credit market.

- Plan Vivo – focuses on projects that support local communities and smallholders in developing nations.

Choosing offsets from projects that adhere to these recognized standards provides assurance of their quality.

- READ MORE: Who Certifies Carbon Credits?

Remember that the ultimate goal of carbon offset credits is to reduce the amount of carbon emitted into the atmosphere. Each carbon credit certification gives the owner the right to emit one ton of CO2 or other greenhouse gasses.

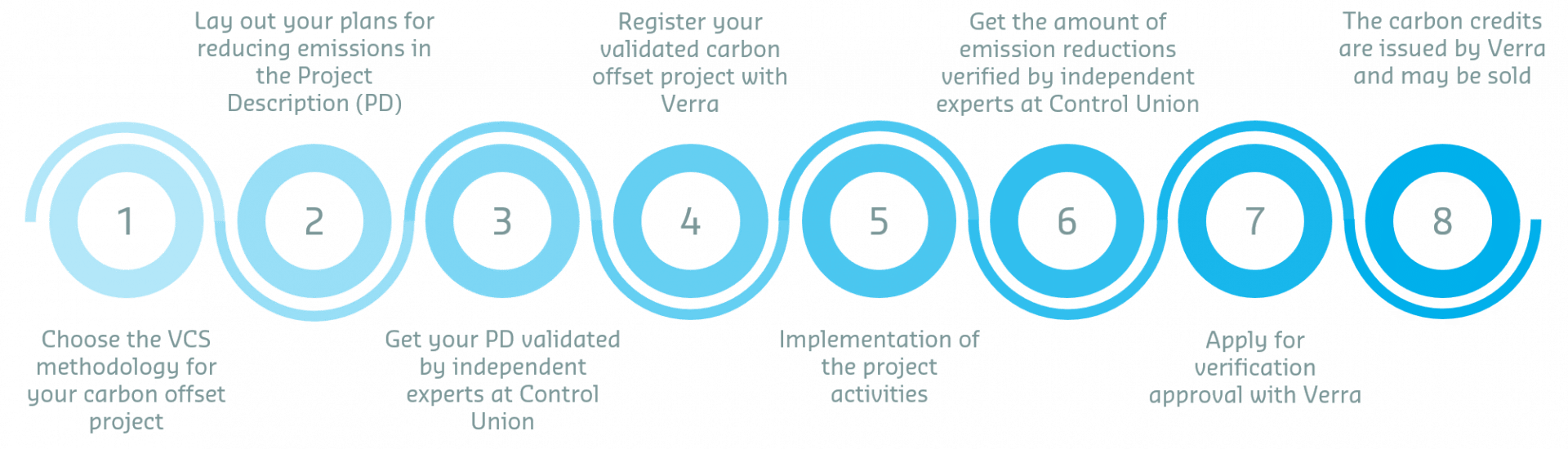

A carbon offset credit becomes certified only by going through the specified processes or procedures set by the certifying standards. This is what separates a high-quality and real carbon credit from other credits swarming the market.

An example of a carbon credit certification process by Verra’s VCS program is shown below.

Another thing to keep in mind is the provider’s project documentation practice. This refers to the detailed information and documentation associated with carbon offset projects. This includes project plans, methodologies, emission reduction calculations, and other relevant documentation.

Transparent and comprehensive project documentation is vital for assessing the integrity of offset projects. It allows you and other stakeholders, including third-party verifiers, to understand how emissions reductions are achieved, measured, and verified.

Reputable carbon offset projects undergo third-party verification by independent organizations. This process adds an extra layer of credibility and transparency, assuring you that the claimed emissions reductions are accurate. It confirms that providers are delivering on their promises to help mitigate climate change.

- RELATED: Who Verifies Carbon Credits?

So always look for projects certified by recognized standards and certification bodies – it’s non-negotiable.

Here are the top carbon offset certification and standard bodies to consider.

Researching Carbon Offset Projects

Finding the right carbon project for your offsetting needs involves a range of factors, including project types, geographic considerations, project longevity, and other relevant aspects. It may not be that easy and quick given the plethora of projects available today. But, here’s how you can find the right offsetting partner.

Different projects may have varying impacts based on their geographic location. For example, reforestation projects in one region may have different ecological and social implications compared to a renewable energy project in another. Considering the geographic context is important for understanding the broader environmental and social implications of offset projects.

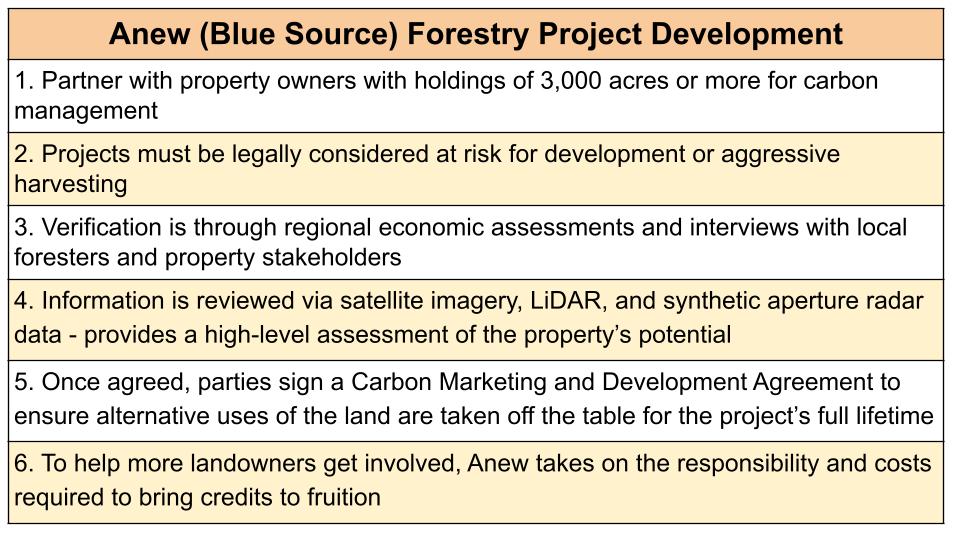

BlueSource, now Anew, is widely known for providing offset credits from improved forest management practices, carbon capture, and other projects. It covers the U.S. Canada and Europe, with an environmental commodities portfolio across five continents.

Under its core project development expertise, forestry, Anew follows these steps for a project to be eligible for offset crediting:

Finite Carbon is another big name in the field of forest improvement projects. With the developer’s wide coverage, their projects cover major forest type from the Appalachians to coastal Alaska.

Finite Carbon is another big name in the field of forest improvement projects. With the developer’s wide coverage, their projects cover major forest type from the Appalachians to coastal Alaska.

Another provider, C-Quest Capital (CQC), creates high impact carbon offsets through three platforms: cleaner cooking, efficient lighting, and sustainable energy. It aims to transform the lives of families in poorer communities worldwide.

You also have to consider project longevity, which refers to the sustainability and durability of carbon offset projects over time. This involves assessing how well a project can maintain its emissions reductions or removals over an extended period.

Longevity is crucial to ensuring that the offsetting efforts have a lasting impact on reducing carbon emissions. Factors such as ongoing maintenance, community engagement, and adaptability to changing conditions contribute to the overall project longevity.

But before you pick a carbon offset provider, there are some things you have to keep in mind first. You need to calculate and verify your carbon footprint and learn the things to avoid so you’ll emerge successfully.

Calculating and Verifying Carbon Footprint

Quantifying your carbon footprint involves assessing emissions from various sources, such as energy consumption, transportation, and manufacturing. The role of the verification process is to ensure the accuracy and reliability of your calculated emissions data.

Measuring emissions is a critical step in calculating your carbon footprint. This involves quantifying the amount of greenhouse gasses such as CO2 released into the atmosphere by certain activities.

Different methodologies and tools are used for measuring emissions from different sources, and accuracy is critical for reliable calculation. This step often involves using emission factors, direct measurements, or modeling techniques.

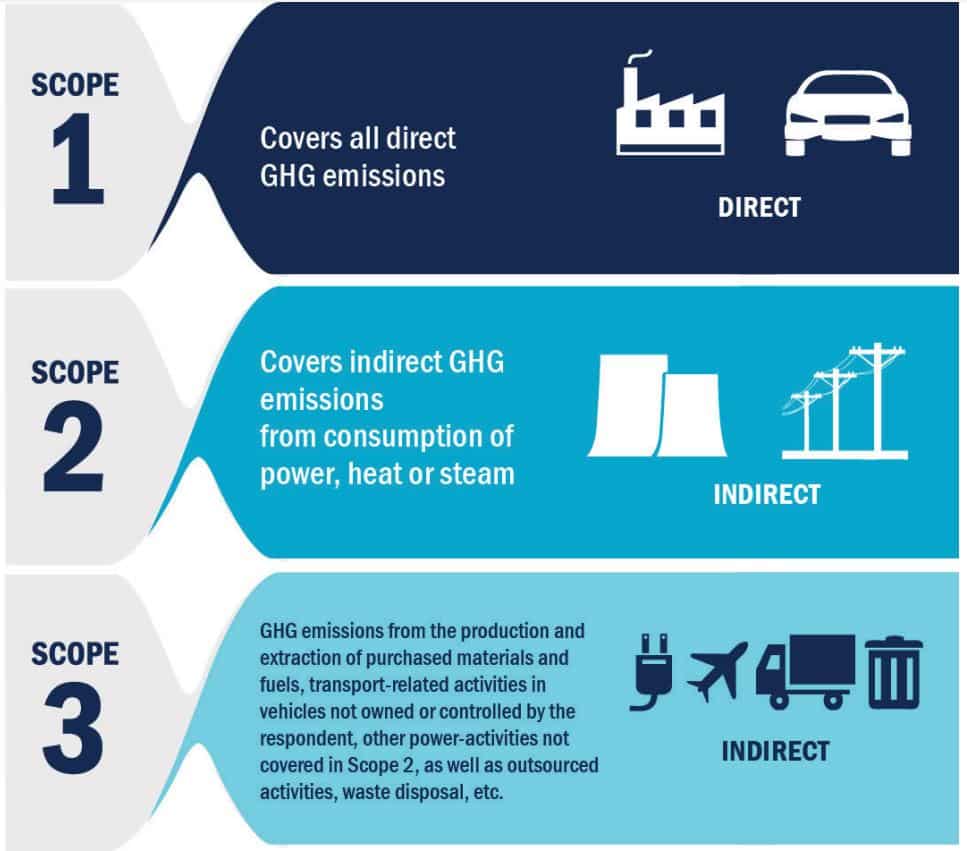

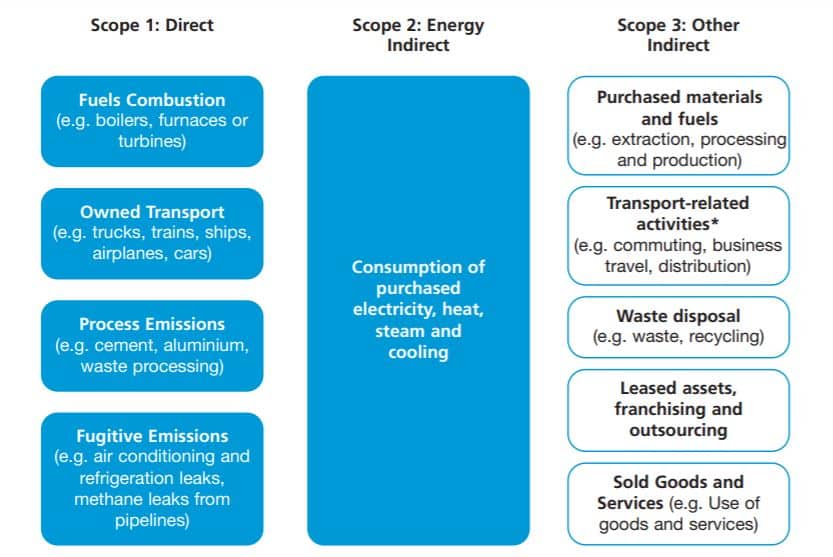

The more complex your organization or company’s activities are, the harder it is to identify the sources of emissions. But most often, it involves the following three emissions scopes.

Here are also the common types of emissions sources under each scope that can help guide you identify them.

After calculating your carbon footprint, the next step is to choose appropriate offsets to compensate for the identified emissions. This is when you can now select carbon offset projects that align with your values and goals.

After calculating your carbon footprint, the next step is to choose appropriate offsets to compensate for the identified emissions. This is when you can now select carbon offset projects that align with your values and goals.

Go here if you want to know more about how to comprehensively calculate your carbon emissions, with specific examples provided.

Apart from considering the major things when assessing providers of high-quality carbon offsets, you also have to watch for the common pitfalls. Identifying and understanding these pitfalls is crucial for making informed decisions and ensuring that your offsetting efforts are effective.

Common Pitfalls to Avoid

First red flag is lack of transparency. It refers to situations where carbon offset projects don’t provide clear and comprehensive information about their activities.

Without sufficient information, it becomes challenging to verify the legitimacy of emissions reductions, project methodologies, and the overall impact of the offsets. Transparency, especially among intermediaries in the VCM, is critical.

Next, pay attention to additionality – it’s a key concept defining a high quality carbon offset. It ensures that the emissions reductions achieved by a project are additional to what would have occurred without the funding.

Concerns about additionality arise when there’s doubt about whether the supported project is genuinely making a positive environmental impact. Forest carbon offsets have been the target of scrutiny over additionality since last year.

Lastly, you should be aware of double counting. It happens when the same emissions reductions are claimed by multiple entities, leading to an overestimation of the overall impact.

This could arise where there’s insufficient oversight in the carbon offset market. For instance, you could have bought high-quality carbon offsets from a reforestation project but the developer sold them to another buyer. Those same offsets are double-counted.

Thus, robust accounting and adherence to established standards are crucial to avoid double counting. Addressing this and the other pitfalls is essential for you to be confident that the carbon offsets you support are of high quality.

Conclusion

In the realm of climate action, the quest for high-quality carbon offsets takes center stage. They offer you and other climate conscious entities a powerful tool to mitigate your carbon footprint. And as the demand for these offsets continues to surge, it becomes important to understand their role in fostering environmental and social benefits.

By choosing reputable projects and assessing the credibility of offset providers through recognized standards, you can ensure the quality of the offset credits. Ultimately, the journey towards high-quality carbon offsets propels us together closer to achieving the ambitious Paris Agreement climate goals.