The Cobalt Price is currently trading at $28.15 USD per pound, holding steady with a 0.00% movement over the last seven days. Despite the quiet week, the market remains bullish year-to-date, posting a robust 6.63% gain since the start of 2026. After a volatile opening to the year, prices have entered a consolidation phase as buyers assess the sustainability of the recent rally prompted by supply-side constraints.

Cobalt Price

Unit: USD/lb

---

---

Loading Chart...

Market Drivers: DRC Quotas and Supply Tightness

The primary driver underpinning the current valuation is the continued impact of strict export quotas implemented by the Democratic Republic of Congo (DRC). Following the government’s intervention to cap exports and replace the previous ban with a quota system, global supply chains have tightened significantly. This structural shift has successfully drained excess inventories that plagued the market in previous years, transitioning the sector from oversupply to a delicate balance.

However, the 0.00% movement this week reflects a temporary standoff between buyers and sellers. Industrial consumers, particularly in the EV battery sector, are seemingly hesitant to chase prices higher after the sharp 6.63% YTD surge. Market reports indicate that trading activity slowed this week as major consumers utilized existing stockpiles rather than purchasing at spot rates. This pause allows the market to digest the new pricing reality of roughly $62,000 per tonne, with the DRC’s strategic supply management acting as a firm floor against significant downsides.

Technical Outlook

Technically, the Cobalt Price has established strong support around the $28.00 level. The flat performance this week suggests a consolidation pattern rather than a reversal. Given the YTD momentum and the fundamental supply deficit projected for later this quarter, the outlook remains cautiously optimistic. A breakout above $28.50 could signal the next leg higher, while a dip below $27.50 might trigger short-term profit-taking before the longer-term uptrend resumes.

The Copper Price is trading at $5.95 USD per pound today, marking a -0.71% decline over the last seven days. After a blistering start to 2026 that saw the red metal hit fresh all-time highs above $6.11, the market has entered a consolidation phase. Despite the weekly dip, copper remains up 7.25% over the last 30 days and 4.78% year-to-date, reflecting continued structural strength despite short-term headwinds.

Copper Price

Unit: USD/lb

---

---

Loading Chart...

Market Drivers: Why is Copper Down?

The recent pullback in the Copper Price can be attributed to a cooling of geopolitical risks and shifting supply dynamics that have prompted profit-taking among speculative investors.

Geopolitical Risk Premium Fades: A primary driver of the recent sell-off was the de-escalation of tensions regarding Greenland. Markets breathed a sigh of relief after reports confirmed that the U.S. administration ruled out aggressive measures and retracted threats of tariffs on allied nations opposed to the acquisition. This removed a significant “fear premium” that had inflated commodity prices earlier in the month, leading to a rotation out of hard assets.

Rising Inventories: Easing supply constraints have also weighed on prices. LME copper stocks have risen to their highest levels since May 2025, with significant inflows reported in U.S. warehouses. This inventory build has alleviated immediate concerns of a supply squeeze, narrowing the arbitrage window between Comex and LME contracts and signaling that physical availability is temporarily improving.

Profit Taking Following Record Highs: After surging nearly 40% year-over-year and hitting record peaks in mid-January, the metal was due for a technical correction. Analysts note that the rapid ascent invited profit-taking, particularly as physical buyers in China showed hesitation at these elevated price levels.

Technical Outlook

Technically, copper is testing support near the $5.80-$5.90 region. While the long-term trend remains bullish driven by AI and green energy demand, the short-term momentum indicators suggest a cooling period. A break below $5.80 could open the door for a deeper retracement toward $5.60, while a reclaim of the psychological $6.00 level is needed to reignite the rally toward new highs.

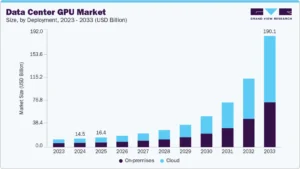

Artificial intelligence (AI) is reshaping technology and energy systems worldwide. As AI grows, it increases the need for powerful hardware, which also puts stress on electricity grids. Two major trends illustrate this change: the fast-growing data center GPU market and rising global power demand to support AI and digital infrastructure. These trends have implications for technology companies, power operators, governments, and energy planners.

GPU Gold Rush: AI Chips Are the New Power Plants

The data center graphics processing unit (GPU) market is expanding quickly due to AI demand. GPUs are specialized chips that speed up AI training and inference tasks. Today’s AI models require thousands of GPU cores working in parallel to process data.

In 2024, the global data center GPU market was estimated at about $14.48 billion. Analysts expect this market to grow rapidly in the coming decade.

One forecast suggests it may hit around $155.2 billion by 2032, about 30.6% increase from 2024. This growth is driven mainly by AI, machine learning, and other high-performance computing workloads.

Source: Grand View Research

Other market research supports rapid growth but shows variation in future values depending on methodology. A different long-term forecast shows that the data center GPU market might grow from about $21.6 billion in 2025 to $265.5 billion by 2035. This means an annual growth rate of 28.5%.

Source: Future Market Insights

These projections show a clear global trend. Demand for GPU-based data center hardware will triple or more in the next decade. This growth comes as AI services spread across various industries.

Hyperscale cloud platforms, enterprises, and government agencies are among the major buyers driving this demand. AI tools, like generative AI and large language models, are booming. This keeps GPU-based computing central to future digital growth.

Global electricity demand is set to rise sharply over the next decade. A recent UN report says demand will rise by over 10,000 terawatt-hours by 2035. This increase is roughly equal to the total electricity consumption of all advanced economies today. Rapid growth in artificial intelligence and digital infrastructure is a major driver of this trend.

Data centers play a central role in this surge. The International Energy Agency (IEA) estimates that data centers consumed ~415 TWh globally in 2024 (1.5% of total electricity). That’s up from ~240 TWh in 2023—a growth of around 73% driven by AI rollout.

This growth shows the quick rollout of AI systems. They depend on power-hungry GPUs and high-density computing gear.

The IEA predicts that by 2030, data centers will make up over 20% of electricity demand growth in advanced economies. In countries with large AI and cloud computing hubs, data centers are becoming one of the fastest-growing sources of new power demand. This shift pressures grids. It also increases the need for new power generation, grid upgrades, and low-carbon sources.

Power demand growth from data centers will also change how grids operate in key economies. In the United States, data centers are projected to account for nearly half of all growth in power demand through 2030. In other advanced economies, data centers could drive more than 20% of electricity demand growth.

Beyond simple demand growth, the global power system must plan for future capacity needs to meet rising consumption. Reports indicate that by 2035, global electricity demand could grow by around 30% compared with today.

AI-driven demand is a central factor behind this increase, along with electrification in transport, industry, and buildings. Renewables, nuclear, and cleaner energy sources will have to expand to meet this growth while reducing emissions.

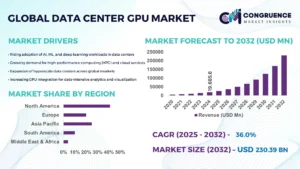

Growth in GPU markets and power demand varies by region. North America leads the data center GPU market, with a large share of sales and installed capacity. This success comes from cloud providers and hyperscale platforms.

Europe and Asia have high demand. Asia-Pacific is growing quickly because of investments in digital services and computing infrastructure.

On the energy side, grids in some regions face more strain than others. Advanced economies with many AI data centers, like the U.S., parts of Europe, and China, must balance current power needs with the fast growth of data center loads. Emerging markets might find it hard to keep up with industrialization and digital growth if they don’t invest in their grid.

Renewable energy plays a growing role in addressing power demands from digital infrastructure. By 2024, renewable energy had grown significantly around the world.

Solar and wind power made up a large part of the new installations. In 2023, solar capacity grew by over 32%. Also, global installed renewable power capacity surpassed 4,400 gigawatts. This expansion helps meet part of the rising demand from data centers and other sectors.

GPUs, Power, and Infrastructure Converge

The growth of AI is changing how investors and companies view computing hardware. GPUs are no longer seen as short-term technology tools. Many investors now treat them as long-term physical infrastructure, similar to power plants or transport assets.

A survey by KPMG and Nuway Capital looked at 120 investors in 10 global markets. It found that almost 80% believe generative AI is the main reason to invest in GPU capacity.

Over 70% of high-net-worth investors see GPUs as a better investment than blockchain and quantum computing. Many also ranked GPUs above renewable energy. This shift reflects stable demand, physical limits, and long asset lifetimes.

Power availability has become a critical constraint. As GPU-dense data centers expand, electricity supply now shapes where and how fast AI infrastructure can grow. In response, major technology firms are securing long-term power sources that can deliver large volumes of reliable, low-carbon electricity, such as nuclear.

Several companies are turning to nuclear energy. Meta has announced deals with Vistra, TerraPower, and Oklo to secure up to 6.6 gigawatts of nuclear capacity by 2035. Microsoft made a 20-year deal with Constellation Energy to restart the Three Mile Island nuclear plant. This effort is backed by a $1 billion loan from the U.S. government.

Amazon also has deals for 1.9 gigawatts of nuclear power from the Susquehanna plant. They also have agreements for small modular reactor projects. Google has signed a deal with Kairos Power for energy from multiple small modular reactors, with up to 500 megawatts expected by 2035.

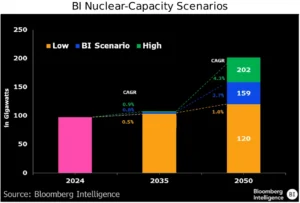

Nuclear to the Rescue: Powering AI 24/7

Industry leaders now describe this link between AI and nuclear power as structural. At a recent International Atomic Energy Agency meeting, officials noted that nuclear energy provides several key benefits. It has low emissions, supplies power around the clock, offers high power density, and is scalable. This makes it a great fit for AI needs.

Globally, 71 nuclear reactors are under construction, adding to 441 operating units, with 10 planned in the United States. Bloomberg Intelligence predicts that U.S. nuclear capacity may grow by 63% by 2050. Most of this increase will happen after 2035, as small modular reactors become commercially viable.

At the same time, supply limits are reinforcing the infrastructure view of GPUs. Constraints in chip manufacturing, power access, land, and grid connections are tightening. Hyperscalers are responding with massive spending.

Major cloud companies are expected to spend over $600 billion on capital expenditures in 2026, a 36% increase from 2025, according to analysts. About $450 billion of that will go to AI infrastructure. NVIDIA leads the market, taking nearly 90% of AI accelerator spending. In early 2025, it reported $35.6 billion in quarterly data center revenue.

Together, these trends show a clear shift. The future of AI will depend not just on software, but on access to GPUs, data centers, and reliable power. For investors, utilities, and policymakers, AI is now an infrastructure challenge as much as a digital one.

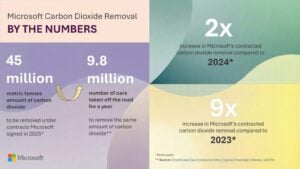

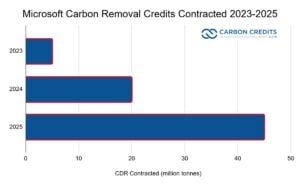

Microsoft sharply expanded its carbon removal activity in 2025. The company announced that it signed agreements covering 45 million metric tonnes of carbon dioxide removal in a single year. This total is more than double the volume the tech giant contracted in 2024 and marks its largest annual increase to date.

The new figure reflects a rapid scale-up in Microsoft’s climate strategy. Since launching its carbon-negative goal, the company has steadily increased its purchases of carbon removal credits.

Microsoft states that these agreements focus on high-quality carbon removal, not avoided emissions. The company prioritizes methods that physically remove carbon dioxide from the atmosphere and store it for long periods.

Phil Goodman, Director of the carbon removal portfolio at Microsoft, remarked:

“With any form of carbon removal, you need someone out there to buy the credits so that the economic model works. By securing that forward demand commitment, suppliers can actually go raise financing, hire staff, and build out their projects. We buy only a fraction of a project’s total credits, and we hope other companies can make faster procurement decisions knowing that projects in our portfolio underwent deep due diligence.”

Mixing Nature and Tech: How Microsoft Removes Carbon

In 2023, Microsoft contracted about 5 million tonnes. In 2024, that number rose to roughly 20 million tonnes. The jump to 45 million tonnes in 2025 signals a shift from pilot-scale deals to long-term market building.

The 45 million tonnes come from a wide range of carbon removal pathways. Microsoft spreads its purchases across both engineered and nature-based solutions. This approach helps reduce risk and supports multiple technologies at once.

Key removal methods in Microsoft’s portfolio include:

Direct Air Capture (DAC), where machines pull CO₂ directly from the air and store it underground

Bioenergy with carbon capture and storage (BECCS), which captures emissions from biomass energy and locks them away

Enhanced weathering, which accelerates natural rock processes that absorb carbon

Afforestation and reforestation, which store carbon in trees and soils

Soil carbon projects, which increase carbon stored in farmland

Microsoft confirmed that a growing share of its 2025 agreements came from durable removals, meaning storage lasting hundreds to thousands of years. This includes DAC, BECCS, and mineralization projects.

Source: Data from Microsoft

The company also works with suppliers across North America, Latin America, Europe, Asia, and Africa. This global spread helps scale carbon removal beyond a few regions. As noted by Microsoft, the goal of all these efforts is to:

“…help restore carbon balance lost through carbon dioxide emissions generated by modern life – from agriculture and construction to chemical and energy production.”

Why Microsoft Is Scaling Carbon Removal So Fast

Microsoft’s emissions have risen in recent years. The company reported that its Scope 1, 2, and 3 emissions were up more than 30% from 2020 levels by the early 2020s. The main driver is rapid growth in data centers, cloud services, and AI computing.

AI systems require large amounts of electricity and hardware. This has made it harder for Microsoft to reduce emissions through efficiency alone. Carbon removal now plays a key role in balancing residual emissions that cannot be eliminated quickly.

Microsoft’s climate targets are clear:

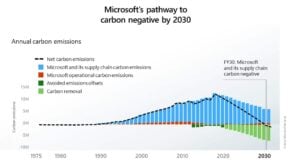

Carbon negative by 2030, removing more CO₂ than it emits each year

The company sees carbon removal as essential to meeting these goals. Microsoft states that emissions reductions remain the priority. Carbon removal comes after efficiency, clean energy, and supply-chain action.

Microsoft leads the carbon removal market, but other large buyers are also active. In the first half of 2025, companies signed at least 61.5 million tonnes of carbon removal offtake agreements worldwide. Microsoft accounted for about 56.3 million tonnes, or roughly 91% of that total. This shows how concentrated demand still is among a few major buyers.

Other tech firms are contributing at smaller scales. Google signed carbon removal agreements totaling about 728,300 tonnes of CO₂ across multiple projects.

Financial institutions such as JPMorgan Chase have also purchased durable removal credits, including BECCS and DAC. In addition, companies including Google and Stripe are part of a coalition that plans to spend $1 billion on carbon removal by 2030.

Nature-based removal also plays a role. Large firms, including Microsoft, Google, Meta, and Salesforce, have committed through joint initiatives to secure up to 20 million tonnes of nature-based carbon removal credits by 2030. These projects focus on forests, soils, and other land-based solutions.

The carbon removal market remains small but is growing fast. In 2024, total carbon removal purchases reached nearly 8 million tonnes, up 78% from 2023. Most purchases still come from repeat buyers with long-term climate targets.

Looking ahead, McKinsey & Company estimates the carbon removal market could reach $40 billion to $80 billion per year by 2030. If the industry scales to meet climate needs, annual revenues could rise to between $300 billion and $1.2 trillion by 2050. These forecasts depend on falling costs, strong standards, and broader corporate participation.

Source: McKinsey & Company

Overall, demand is expanding, but leadership remains concentrated. Microsoft’s scale helps anchor the market, while smaller commitments from other firms show early signs of wider adoption.

Trust in the Numbers: MRV Matters

Microsoft places strong emphasis on Measurement, Reporting, and Verification (MRV). Each project must prove how much carbon it removes and how long it stays stored. The big tech firm works with independent third-party verifiers and recognized carbon standards.

The company also applies internal quality criteria. These include permanence, additionality, and low risk of reversal. Projects that fail to meet these benchmarks do not qualify.

Microsoft states that improving MRV systems remains a priority. Accurate data builds trust and supports long-term market growth. This focus also reflects broader industry concerns about credibility in voluntary carbon markets.

Hurdles Ahead: Costs, Supply, and Permanence

Despite rapid growth, carbon removal faces several hurdles:

High costs: DAC and other engineered methods can cost hundreds of dollars per tonne

Limited supply: Most technologies remain early-stage

Long development timelines: Infrastructure takes years to build

Microsoft acknowledges these limits. The company says large early purchases help push costs down over time through learning and scale. This mirrors how renewable energy prices fell after early corporate and policy support.

The Future of Corporate Carbon Removal

Microsoft plans to continue expanding its carbon removal portfolio beyond 2025. The company expects annual contracting volumes to remain high as AI and cloud growth continue.

Other large firms are following similar paths. Technology companies, airlines, and consumer brands are increasingly signing long-term removal contracts. However, none yet match Microsoft’s scale.

The 45 million tonnes contracted in 2025 mark a turning point. Carbon removal is shifting from niche pilots to a recognized climate tool. Microsoft’s approach shows how corporate demand can help build an entirely new climate industry.

As global emissions remain high, the role of carbon removal is likely to grow. Microsoft’s strategy offers one of the clearest examples to date of how large buyers are shaping this emerging market.

The Middle East and North Africa are no longer on the sidelines of the energy transition. The MENA Energy Outlook 2026 by Dii Desert Energy shows the region has reached a turning point. Renewable capacity jumped 44% in 2025 to about 43.7 GW. Solar PV led the surge, accounting for 34.5 GW.

The growth is unprecedented. MENA took five years to rise from about 14 GW in 2020 to 30 GW in 2024. Then, in just one year, it added nearly 15 GW. This was not gradual progress. It was a rapid scale-up driven by cheap solar power, competitive auctions, and a booming project pipeline.

Falling costs are at the core of this shift. In 2025, solar and wind tenders set new global records. Solar PV prices dropped to around 1.09 US cents per kWh. Wind fell to about 1.33 US cents per kWh. These prices are reshaping expectations for large-scale clean energy worldwide.

Policy, Pipeline, and Project Momentum Poised for Scale

The region’s renewable energy project pipeline has ballooned to ~202 GW — a figure that now nearly matches aggregated national targets out to 2030. That pipeline isn’t theoretical; it includes 38 GW under construction and a deep roster of gigawatt-scale solar programs ready to move into execution.

Under Dii’s updated scenario framework for 2030, three pathways emerge:

A Conservative baseline: 165 GW total renewables.

A Balanced transition: 235 GW, roughly aligned with national ambitions.

A Green Revolution: 290 GW, representing full regional potential.

Even the conservative outlook reflects a dramatic acceleration — the result of policy clarity, cost competitiveness, and private capital intent on capturing the region’s unparalleled solar resource.

Source: MENA Energy Outlook 2026

Saudi & UAE Leading Deployment

Saudi Arabia has emerged as a standout. Operational capacity nearly tripled in one year, reaching around 11.7 GW, and it now stands as a regional leader not only in volume but in setting cost benchmarks.

Meanwhile, the UAE continues to punch above its weight with flagship projects. Masdar and Emirates Water and Electricity Company (EWEC) have begun the construction of a 5.2 GW solar park integrated with 19 GWh of battery storage – one of the largest renewable + storage complexes globally. This project is intended to deliver baseload clean power at scale, significantly reducing reliance on gas-fired generation.

Solar is the centerpiece of the MENA transition — and for good reason.

Market share: Solar PV dominates the region’s current renewable fleet, making up roughly 79% of deployed renewables with 34.5 GW.

Pipeline strength: Of the total 202 GW pipeline, solar accounts for the majority — around 130 GW — leaving wind and storage to complement its growth.

Economics: First-of-their-kind auction prices have pushed levelized costs to historic lows, intensifying private-sector interest and reducing capital-cost risk for long-duration financing.

This solar dominance aligns with broader global forecasts that see solar accounting for most of renewable growth in the decade ahead, especially as project cost declines continue to outpace projections.

The critical driver here is not just sunshine but economics: solar power in MENA is now among the cheapest baseload energy available, challenging even entrenched natural gas generation in many markets.

Source: MENA Energy Outlook 2026

From Panels to AI: MENA’s New Demand Drivers

One of the most interesting insights in the Outlook is the emergence of AI infrastructure as a renewable energy demand driver.

The report highlights that data centers — spurred by the rapid adoption of AI — are becoming “super offtakers” of clean energy. These facilities require long-term, high-capacity power contracts, which in turn improve the bankability of large renewable power purchase agreements (PPAs).

This is a structural shift. Traditionally, renewable PPAs in the corporate sector were dominated by manufacturing and export industries. Now, the AI ecosystem’s appetite for reliable, low-carbon power is helping unlock financing and long-duration contract structures that support gigawatt-scale solar and storage.

In effect, AI is not just a user of clean power — it’s becoming a market catalyst, compressing risk premia and enabling developers to sell projects at scale with predictable cash flows. This is exactly the type of demand signal that carbon markets and corporate net-zero strategists value most: stable, creditworthy offtake linked to decarbonization commitments.

Source: MENA Energy Outlook 2026

Energy Storage: The Key to 24/7 Clean Power

Solar’s growth creates a natural need for storage solutions, and MENA is responding. Battery Energy Storage Systems (BESS) are rising fast — with about 25 GWh operational today and projections showing ~156 GWh by 2030 (a more than six-fold increase).

This shift is pivotal: storage enables firm, dispatchable renewables, bridging gaps between peak solar output and evening demand. It also reduces grid stress and curtails reliance on fossil peaking units — which, in carbon accounting terms, lowers actual emissions and improves marginal grid intensity.

The shift toward BESS over thermal energy storage reflects global trends in cheaper lithium-ion systems and increased merchant storage markets, signaling that long-duration storage will be a defining piece of the region’s decarbonization story.

MENA’s transition — led by solar — has direct implications for carbon reduction pathways:

The region’s power sector emissions are highly carbon-intensive today. Replacing fossil generation with low-carbon solar and storage can materially reduce grid emissions intensity.

Large-scale deployment and low costs improve the economics of displacement, especially for gas. That in turn strengthens the case for deeper cuts aligned with Paris Agreement goals.

However, challenges remain. Natural gas still dominates power generation in many countries and will likely remain part of the mix through 2030. That underscores the importance of carbon pricing, power market reform, and long-term PPAs to accelerate coal-to-solar displacement and enable hydrogen sectors to scale.

MENA: Forecast to 2030 and Beyond

Balanced transition (235 GW): Renewable power capacity grows significantly, narrowing the gap to climate targets and improving energy security.

Green Revolution (290 GW): If finance, supply chains, and permitting keep pace, MENA could exceed current national goals and unlock deeper emissions reductions.

Global modeling from other sources also suggests that solar and wind could respectively represent the majority of electricity growth in the next decade — a pattern that amplifies the MENA trajectory.

MENA has shifted from potential to performance, driven by low-cost solar, strong project pipelines, and rapid growth in energy storage. New demand from AI is adding fresh momentum.

This progress creates fertile ground for carbon markets. Large, contract-backed renewable projects offer credible, long-term emissions reductions. As power markets mature, MENA is emerging as a key player in energy security and global decarbonization.

Mitsui O.S.K. Lines, also known as MOL, one of Japan’s biggest shipping companies, announced its first carbon removal results under its long-term environmental plan. This move marks a real step beyond reducing emissions. MOL aims to reach net-zero greenhouse gas (GHG) emissions by 2050 under its Environmental Vision 2.2.

Shipping emissions are hard to cut, so removal methods help tackle the remaining CO₂. MOL’s actions also reflect the global growth of the carbon removal market. Companies and countries are investing more in solutions that take CO₂ out of the air for long-term storage. This trend is rising as climate targets push industries to go beyond emission cuts.

DAC, Ocean Capture & Rocks: A Trio of MOL’s First Carbon Removal

In fiscal 2024, MOL announced its first verified carbon removal achievements. This progress builds on its Environmental Vision 2.2 strategy. The shipping giant secured measurable removal commitments using several technologies.

In its LinkedIn post, the company notes:

“In FY2024, MOL reported credits equivalent to 2,000 tons of CO₂ emissions- marking the company’s first tangible achievement in CDR… As MOL continues to diversify its CDR portfolio, it remains committed to finding and scaling the most effective solutions- both natural and technological- to advance toward a decarbonized future.”

MOL partnered with Climeworks, a leading Direct Air Capture (DAC) company. Through this partnership, the company agreed to procure 13,400 tonnes of CO₂ removal by 2030 using Climeworks’ DAC systems.

MOL is the first shipping company globally to set up this type of DAC purchase. DAC pulls CO₂ directly from the air and stores it permanently.

MOL also signed an offtake agreement for 30,000 tonnes of carbon removal credits from Captura’s Direct Ocean Capture technology. This method removes CO₂ from seawater, which draws CO₂ from the air over time.

In addition, MOL made a deal with Alt Carbon for 10,000 tonnes of carbon removal credits. These credits come from enhanced rock weathering in India. Enhanced weathering helps pull CO₂ from the air into minerals in soil, a type of removal considered higher quality and more durable. This deal is the first of its kind between a Japanese shipping company and an Indian climate tech firm.

MOL is also buying enhanced rock weathering removal credits through another multiyear offtake. This brings added diversity to its removal portfolio. These deals help the company support different removal paths rather than relying on a single method.

The global shipping industry carries about 90% of traded goods by volume. It also produces roughly 3% of global CO₂ emissions. If trade grows, emissions could rise unless action is taken.

The International Maritime Organization (IMO) aims for shipping emissions to drop. The targets are: 20-30% reduction by 2030, 70-80% by 2040, and net-zero by 2050, all compared to 2008 levels.

Source: IMO

Even with cleaner fuels like ammonia or hydrogen, some emissions will remain hard to avoid. Energy efficiency and fuel switches help, but they cannot remove all CO₂ from long ocean voyages. Carbon removal fills this gap. It helps shipping companies offset their leftover emissions while future fuel solutions scale up.

MOL’s Environmental Vision 2.2 plan aims to remove 2.2 million tonnes of CO₂ by 2030. This goal covers all its removal initiatives. This creates demand for early‑stage removal solutions and helps scale emerging technologies.

Partnerships on the Horizon: Forests, Carbon Credits, and Cross-Industry Moves

MOL’s carbon removal work includes broader moves with partners and industry players. The company is supporting carbon credits to cut emissions and expand negative emissions. All credits are third-party certified and independently verified to ensure quality and impact.

In January 2025, MOL and Marubeni Corporation started Marubeni MOL Forests Co. This joint venture will create, trade, and retire nature‑based carbon credits. Its first project aims to plant around 10,000 hectares of new forest in India. This will generate credits from afforestation and reforestation. These forests will start producing removals around 2028. Nature‑based solutions help store carbon while boosting biodiversity and soil quality.

Also, MOL signed a deal with ITOCHU Corporation. This agreement aims to promote environmental attribute certificates. These certificates help cut Scope 3 emissions in transportation. This work is the first Japanese model linking shipping and aviation in environmental certificate use. Scope 3 emissions come from supply chains and end‑use.

Another related program is the NX‑GREEN Ocean Program by Nippon Express, launched in February 2025. It uses carbon inset certificates tied to low‑carbon shipping by MOL vessels. These certificates help companies reduce their Scope 3 freight emissions. The program shows how removal and decarbonization can work together for supply chains.

Together, these partnerships show MOL’s expanding role. The company is connecting technical and natural removal solutions with marine decarbonization and cross‑industry climate efforts.

Riding the Carbon Market Wave

The global carbon removal market is growing fast. Corporations and governments are investing more in long-lasting removal methods. These include DAC, ocean capture, enhanced weathering, and nature-based solutions. This growth matches scientific calls for big removals to keep warming under 1.5°C.

Source: McKinsey & Company

MOL is helping to expand the removal market by investing in multiple technologies. A joint venture for a NextGen CDR Facility, including MOL and other buyers, aims for over 1 million tonnes of certified removals by 2025. These projects include DAC and biomass removal with long-term storage. Early demand helps drive down costs over time and encourages more technological development.

Shipping companies are also investing in emission reduction technologies. These include more efficient ship designs, alternative fuels, and onboard carbon capture systems.

Global shipping firms continue to align with the IMO’s decarbonization goals through technology upgrades, fuel changes, and climate partnerships. This includes work on hull design, logistics efficiency, and fuel alternatives such as ammonia and hydrogen. Those efforts reduce emissions intensity and support long-term climate targets.

High Costs and Early Stage Technology: Direct Air Capture and ocean capture remain expensive and are still early in deployment, making them less appealing than traditional emission reductions.

Need for Strong MRV and Certification: Measurement, Reporting, and Verification systems must stay robust to ensure credits reflect real and lasting CO₂ removal. Independent certification is critical for market trust.

Nature-Based Risks: Forest and land projects require careful planning. Carbon storage can be reversed if forests burn, degrade, or are mismanaged. High-quality MRV standards help protect long-term carbon value.

Sailing Toward 2050: MOL’s Vision for Net-Zero Maritime

Despite challenges, experts say removals will be necessary for sectors that cannot eliminate emissions by 2050. Shipping, aviation, and heavy industry will likely cut emissions and use durable removals to meet climate goals.

For MOL, investing in removal markets, partnerships, and strong MRV frameworks positions the company as a leader in maritime decarbonization. The first results under Environmental Vision 2.2 show how shipping firms can add new climate solutions to their sustainability plans.

By partnering with DAC, ocean capture, and enhanced weathering technologies, and by investing in nature-based solutions, MOL is expanding its climate action beyond traditional emission cuts.

As shipping and corporate climate planning evolve, carbon removal will remain a key part of long-term strategies. MOL’s progress with Environmental Vision 2.2 shows how companies can blend technology, nature, and market forces to achieve bold climate goals.

Canada’s climate journey is entering a more uncertain phase. Emissions are trending lower, investments continue to flow, and clean technologies remain in play. Yet momentum is clearly weakening. That is the central message of Climate Action 2026: Retreat, Reset or Renew, the third annual report from the RBC Climate Action Institute.

The report paints a nuanced picture. Progress has not stopped. But it has slowed. Policy reversals, economic pressures, and shifting public priorities are weighing on climate ambition at a time when speed matters most.

Canada now faces a defining question: retreat from climate action, reset its approach, or renew its commitment with a sharper focus.

Emissions Are Falling, but Not Fast Enough

Canada’s total greenhouse gas emissions are projected to be 7% lower in 2025 than in 2019, according to RBC’s estimates. That marks real progress, especially after years of volatility during and after the pandemic.

However, this pace remains well short of what Canada needs to hit its longer-term targets. The country has committed to reducing emissions by 40% to 45% below 2005 levels by 2030 and by 45% to 50% by 2035. Current trends suggest those goals will be difficult to reach without stronger policy signals.

Several sectors have reduced emissions intensity:

Electricity: down 27%

Buildings: down 19%

Oil and gas: down 19%

These gains reflect cleaner power generation, improved efficiency, and gradual technology upgrades. Still, absolute emissions reductions remain modest, especially in sectors tied to economic growth and population expansion.

Climate Action Barometer Hits a Turning Point

For the first time since its launch, the Climate Action Barometer declined. This index tracks climate-related activity across policy, capital flows, business action, and consumer behavior.

The drop was broad-based. No single sector drove the decline. Instead, multiple pressures hit at once.

Key factors include:

The removal of the consumer carbon tax

The rollback of electric vehicle incentives

Economic uncertainty and rising trade tensions

Alberta’s restrictions on new renewable energy projects

Together, these shifts weakened confidence. Businesses delayed or canceled projects. Consumers pulled back on major clean-energy purchases. Climate policy slipped down the priority list for governments focused on affordability and job creation.

While climate action remains above pre-2019 levels, the trendline has clearly flattened.

Capital Flows Hold Steady, but Growth Has Stalled

Climate investment in Canada has leveled off at around $20 billion per year. That figure has barely moved in recent years.

Public funding remains a stabilizing force. Nearly $100 billion in incentives for clean technology and climate programs is already budgeted for deployment through 2035 by Ottawa and the largest provincial governments.

However, private capital is showing signs of caution. Investment declined compared to 2024, driven largely by cooling sentiment toward early-stage climate technologies. Policy uncertainty has amplified investor risk concerns, especially in capital-intensive sectors like renewables and clean manufacturing.

Some bright spots remain. Wind projects on Canada’s East Coast have supported investment flows, even as renewable development slowed elsewhere.

Carbon Pricing Changes Ease Pressure

The federal government eliminated the consumer carbon tax in April 2025, refocusing carbon pricing solely on industrial emitters. The change had a limited impact on national emissions coverage, as only around three percent of agricultural emissions were subject to consumer pricing.

For farmers, the move delivered meaningful financial relief. Many agricultural operations rely on propane to dry grain or heat livestock facilities. Few cost-effective, lower-carbon alternatives exist in rural regions, making the tax a direct burden on operating costs. Removing it eased pressure without significantly weakening the overall emissions policy.

Still, the decision lowered Canada’s climate policy score and sent mixed signals to investors and businesses evaluating long-term decarbonization strategies.

Consumer behavior has become a significant hindrance to climate momentum. Electric vehicle adoption slowed sharply in 2025. EVs accounted for just eight percent of total vehicle sales in the first half of the year, down from twelve percent during the same period in 2024. Passenger EVs now make up only about four percent of Canada’s total vehicle stock.

Higher interest rates, the removal of purchase incentives, and uncertainty around future mandates all contributed to the pullback.

The federal government also delayed the Electric Vehicle Availability Standard, which was set to require EVs to represent 20% of new vehicle sales by 2026. That pause further weakened confidence across the market.

At the same time, not all clean technologies lost ground. Heat pump adoption edged higher, supported by new efficiency funding, particularly in Ontario. The province’s $10.9 billion commitment to energy efficiency programs could support further uptake, even as other consumer-facing climate actions slow.

Public priorities have also shifted. Only about a quarter of Canadians now identify climate change as a top national issue. Cost of living pressures, healthcare access, and economic stability dominate public concerns, reshaping how households weigh climate-related decisions.

Source: RBC report

Buildings Sector Becomes the New Battleground

The RBC Institute’s 2026 “Idea of the Year” focuses squarely on Canada’s buildings sector, which has quietly become one of the country’s most challenging emissions sources. Emissions from buildings rose 15% between 1990 and 2023 and now represent a larger share of national emissions than heavy industry.

Today, buildings account for roughly 18% of Canada’s greenhouse gas emissions when electricity-related emissions are included. Progress remains slow. Emissions from the sector are projected to fall by just one percent in 2025, a pace that leaves Canada far from its net-zero target for buildings by 2050.

New construction adds to the risk. If projects continue to follow prevailing building codes, emissions could rise by an additional 18 million tonnes over time, locking in higher emissions for decades.

Source: RBC Report

Responsible Buildings Pact Points to a Reset

Against this backdrop, the Responsible Buildings Pact offers a potential reset. Launched in 2024 under the Climate Smart Buildings Alliance, the initiative aims to accelerate the adoption of low-carbon designs and materials across the construction sector.

The pact focuses on scaling the use of mass timber and low-carbon concrete, steel, and aluminum. These materials can significantly reduce embodied carbon in new buildings while strengthening domestic supply chains. The approach is particularly timely as Canadian producers face constraints from U.S. trade tariffs, limiting access to lower-emissions materials.

If widely adopted, the pact could transform how Canada builds homes, offices, and infrastructure. By embedding emissions reductions into construction decisions today, the sector could deliver long-term climate gains while supporting industrial competitiveness.

Electricity Progress Slows After Early Success

Canada’s electricity sector remains one of its strongest climate performers. Emissions have fallen an estimated 60% since 2005, surpassing Paris Agreement targets. Coal phase-outs continue to drive reductions, with more than six terawatt-hours of coal power expected to be removed from the grid this year.

Still, progress slowed in 2025. Uncertainty surrounding Alberta’s renewable energy policies led to the cancellation of 11 gigawatts of planned capacity, roughly half of the province’s existing generation. At the same time, natural gas use rose sharply, offsetting some of the emissions gains from coal retirements.

Canada now faces a dual challenge: doubling electricity capacity while fully decarbonizing it by 2050. Estimates suggest the required investment could exceed $1 trillion, underscoring the scale of the task ahead.

Source: RBC Report

Climate Action at a Defining Moment

The RBC report makes one point clear. Canada has not abandoned climate action, but it has lost momentum. Emissions are lower, capital remains available, and technology continues to advance. Yet policy clarity has weakened, consumer confidence has faded, and investment growth has stalled.

With just 25 years left to reach net zero, the choices made now will shape Canada’s emissions trajectory for decades. Renewed coordination between governments, businesses, and consumers will be essential, along with policies that balance economic realities without sacrificing long-term climate goals.

Canada still has time to reset and renew. What it cannot afford is continued drift.

Some of the world’s biggest tech companies and space startups are racing to build data centers in space. These orbital data centers are meant to support the massive computing needs of artificial intelligence (AI). Companies see space as a place to get abundant solar energy and natural cooling without the limits of Earth’s power grids. This idea moved from theory to early testing in late 2025–2026 and gained spotlight at the AIAA SciTech Forum 2026 in Orlando, Florida, last week.

Several tech giants, including Google, SpaceX, and Blue Origin, are exploring space‑based computing. At the same time, startups like Starcloud have already launched prototypes with advanced AI hardware into orbit. These efforts reflect growing interest in solving energy, cooling, and infrastructure challenges that terrestrial data centers face.

Why the Tech Giants Look to Space

AI needs more computing power than ever. Traditional data centers on Earth use huge amounts of electricity and water for power and cooling. In the U.S., data centers used over 4% of total electricity in 2024 and could increase to between 6.7% and 12% by 2028 if current trends continue.

At the same time, global data center electricity demand may nearly double by 2030 to about 945–980 terawatt‑hours per year due to AI and cloud services.

Space offers two major advantages: near‑constant solar power and natural cooling.

Solar panels in orbit can be up to 8x more efficient than on Earth because there is no atmosphere to block sunlight. Heat can also be released directly into space by radiation, without the need for water‑based cooling systems.

These factors could lower energy costs and help AI computing scale without straining terrestrial power systems. Companies see space as a place where solar energy is abundant, and energy from the sun is almost always available, especially in certain orbits.

What the Tech Giants Are Doing

Google: Project Suncatcher

Google has announced a research initiative called Project Suncatcher. The project aims to put AI computing hardware into orbit using solar‑powered satellites.

The tech giant plans to launch two prototype satellites equipped with its own AI chips by early 2027 to test whether they can run in space. The goal is to create blueprints for future space‑based data centers.

Google says these satellites will use Tensor Processing Units (TPUs), chips designed for AI tasks, and connect via laser links instead of traditional wires. The company’s CEO said that using solar energy in space could help support the AI industry’s rapidly rising computing needs.

Starcloud, a startup backed by Nvidia and venture capital firms, has achieved an important milestone. In late 2025, the company launched a satellite called Starcloud‑1 carrying an Nvidia H100 GPU. This satellite successfully trained and ran AI models, including a version of Google’s Gemma model, in orbit. This marked the first AI model training in space.

Starcloud aims to expand this capability with future satellites. The company has proposed building a large space data center with about 5 gigawatts (GW) of solar panels spread over several kilometers. The design would deliver more compute power than many terrestrial data centers with efficient energy use.

SpaceX and Blue Origin

Elon Musk‘s SpaceX and Blue Origin are also exploring space data centers. SpaceX plans to use its Starlink satellite network and future satellites that could carry AI compute hardware.

Reports suggest SpaceX may launch upgraded Starlink satellites with terabit‑class capacity starting in 2026. Musk has also talked about using reusable rockets to place larger compute hubs into orbit at scale.

Blue Origin, backed by Jeff Bezos, reportedly has a team working on technology for orbital data centers. The aim is to develop systems that can support AI workloads beyond Earth. These efforts build on Blue Origin’s long history in rocket and space technology.

Global Competition: Startups and Nations Join In

Space data centers are attracting attention beyond the big tech names. Multiple startups and international players are racing to build compute infrastructure in orbit.

Companies like PowerBank Corporation and Orbit AI are planning space‑based nodes or cloud services powered by solar energy. Moreover, Axiom Space has outlined plans for data center modules on its private space station by 2027.

Outside the U.S., China is also advancing space compute projects. The Three‑Body Computing Constellation aims to deploy thousands of satellites equipped with high‑performance GPUs and AI models. The long‑term goal is to provide a combined computing capacity of 1,000 peta‑operations per second (POPS) — a measure of compute power far beyond many ground‑based supercomputers.

This global competition highlights how nations and companies see orbital data centers as strategic infrastructure for AI and other advanced computing tasks.

Challenges and Engineering Hurdles Above the Atmosphere

Building data centers in space is not easy. Engineers must solve many technical problems before full‑scale orbital centers become common.

Radiation: Space radiation can damage GPUs and other chips. Orbital data centers need heavy shielding and backup hardware.

Cooling: Space has no air or water. Systems must use radiative cooling, which is complex but essential.

Debris: Crowded orbits raise collision risks. Large structures could worsen the Kessler syndrome.

Costs: Launching hardware is costly. Firms expect costs to fall to about $200 per kilogram by the mid-2030s, improving feasibility.

Potential Benefits: Solar, Cooling, and Scaling

Despite the challenges, space‑based data centers offer potential benefits that are hard to match on Earth. More remarkably, the market is set for rapid growth as demand for AI compute expands.

Analysts expect the market to rise from about $1.77 billion in 2029 to nearly $39.1 billion by 2035. This shows an annual growth rate of about 67.4%. This surge is driven by rising AI workloads, growing satellite constellations, and the need for more sustainable, high-performance computing beyond Earth-based limits.

Major advantages of orbital data centers include:

Continuous Solar Power

Satellites in certain orbits can receive sunlight almost 24 hours a day. This could allow data centers to run on clean solar energy constantly, without interruptions from night, clouds, or weather. Solar panels in orbit operate at efficiencies up to eight times those on Earth’s surface.

Natural Cooling

The vacuum of space can help with cooling. Heat radiates into cold space at temperatures as low as 4 Kelvin (−269°C). This natural cooling eliminates the need for water‑intensive cooling systems used by terrestrial data centers.

Compute Scaling

As AI models grow larger, so too does their compute demand. Space data centers could provide new capacity that is not limited by Earth’s land, water, or grid constraints. If prototypes prove successful, large orbital systems might be scaled over the next decade.

Future Outlook: Will AI Go Beyond Earth?

Tech companies and startups are actively exploring space‑based data centers to meet the rapidly rising computing requirements of AI. Google’s Project Suncatcher, Starcloud’s prototypes, and efforts by SpaceX and Blue Origin show that orbital compute infrastructure is moving from concept to early reality.

Space offers nearly constant solar energy and natural cooling, which could ease the energy and environmental pressures associated with traditional data centers. Still, radiation, heat management, space debris, and launch costs are major challenges ahead.

The next few years — especially prototype launches around 2027 — will show whether space data centers can become a practical part of the future AI infrastructure landscape.

Lithium battery energy storage systems (BESS) are now an essential part of the world’s energy transition. These systems store electricity from wind, solar, and other clean power and help keep grids stable when demand rises.

In 2025, the BESS market grew at a record pace. China has taken the lead, and global demand for lithium batteries is climbing fast. These trends show how battery storage is reshaping energy systems around the world.

2025: A Record-Breaking Year in BESS Deployments

Lithium‑ion chemistry remains the dominant technology in both large‑scale and behind‑the‑meter storage systems. These batteries help balance power grids. They support renewable energy and allow utilities and businesses to use energy flexibly.

BESS installations are becoming essential for clean energy infrastructure. This is due to more renewables being added and demand for stable power increasing.

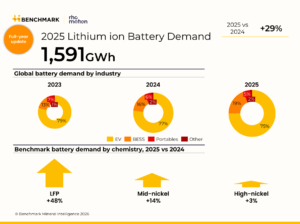

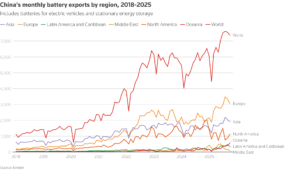

The year 2025 was a landmark year for lithium BESS installations. According to Benchmark Mineral Intelligence, around 315 GWh of battery energy storage capacity was installed worldwide in 2025. This figure represents nearly 50% year‑on‑year growth compared with 2024. China and the United States led global deployments, with China far outpacing all other countries.

A striking sign of China’s dominance came in December 2025. China installed 18 GW (65 GWh) of large‑scale battery storage in that month alone. That amount of capacity was greater than all the battery storage that the United States installed over the entire year. This shows how rapidly China has expanded its energy storage footprint.

Through October 2025, global grid‑scale BESS capacity reached 156 GWh, a 38 % increase from the same period in 2024. China contributed a significant share of this growth, but Europe, North America, and the rest of the world also showed gains in deployment.

Data from Benchmark Mineral Intelligence shows a clear trend: BESS capacity grew in several months of 2025. In October, installations surged by 29% compared to last year. China contributed around 8.8 GWh of new grid-scale capacity that month.

Global Lithium‑Ion Demand Skyrockets

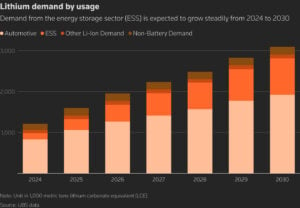

The surge in BESS deployment is part of a larger rise in lithium‑ion battery demand. In 2025, global demand for lithium‑ion batteries grew 29 %, reaching about 1.59 terawatt‑hours (TWh).

Energy storage growth in 2025 outpaced demand in the electric vehicle (EV) market. This increase came from both stationary storage and EVs.

Stationary storage demand in particular jumped by 51 % in 2025, compared with 26 % growth in EV battery demand. This shift signals that storage is becoming a major driver of lithium consumption alongside traditional EV markets.

Researchers highlight that battery chemistries also changed in 2025. Lithium iron phosphate (LFP) batteries grew faster than other cell types, with demand rising 48% year‑on‑year. China’s EV sector remains strong, but LFP’s share outside China also climbed to over 30 % of global battery demand.

Industry analysis shows that global lithium use for energy storage may rise by 45.6% from 2025 to 2030. By 2030, it could reach about 312,934 metric tons. This forecast reflects the growing use of storage systems on power grids and for industrial demand.

Why China Leads the Storage Boom

China’s expansion in the BESS market traces back to sustained support and rapid industrial growth. China’s cumulative battery storage capacity doubled in 2024, reaching roughly 62 GW (141 GWh) by year‑end. Lithium‑ion batteries made up over 96 % of this capacity.

Chinese firms dominate both production and deployment. In 2025, Chinese manufacturers boost global shipments of lithium-ion cells for storage by around 75%. This growth is fueled by demands from power grids, renewable energy, and the expansion of data centers.

Source: Reuters

Chinese exports of battery systems were valued at over $65 billion in the first ten months of 2025, reflecting strong global demand.

China’s leadership also stems from policy reforms that improve storage economics. Changes in market rules have allowed more battery storage to operate profitably. Batteries that can capture price differences throughout the day now have stronger business cases. This shift encourages more installations and higher utilization of grid‑connected storage.

Lithium BESS installations play an important role in supporting the clean energy transition. Storage systems help keep electrical grids stable even when wind or solar power is variable. These systems can store excess renewable electricity during low demand and release it in times of high demand.

This capability helps grids handle peak demand and reduces the need to rely on fossil fuel peaking plants. It also helps spread renewable energy. It smooths out output and offers backup when sunlight or wind decreases. As renewable energy generation expands, storage will remain critical to grid flexibility.

The growth of storage also reflects falling battery costs. Battery pack prices for stationary storage dropped significantly in 2025.

Some industry reports say stationary storage costs dropped to about $70 per kilowatt-hour. This makes it one of the cheapest parts of the battery market. Lower costs help accelerate deployment and make storage investment more attractive for utilities and developers.

Looking Forward: Challenges, Innovation Paths, and Projected Growth

While growth remains strong, the battery storage sector faces some challenges. S&P Global forecasts a small drop in global storage installations in 2026. They predict capacity will fall by about 2.7% by 2025. This expected dip is linked to changes in China’s requirement for pairing storage with new solar projects.

Despite this short‑term dip, long‑term forecasts still point to strong growth through the 2030s as storage becomes central to grid modernization. Battery demand from grid installations is expected to rise even as some geographies adjust policies.

Beyond supply, the industry must also address innovation in long‑duration storage technologies. Lithium-ion systems still lead the market. However, alternatives like flow batteries and sodium-ion cells are starting to emerge. These technologies may help meet storage needs that require longer discharge durations.

Global production capacity for rechargeable lithium‑ion batteries is also growing rapidly. In 2025, total production capacity is set to surpass 2 TWh per year, having doubled from 1 TWh just a few years earlier. This expansion supports both EV demand and energy storage.

As storage continues to scale, its share of overall lithium demand is expected to grow. Some industry estimates suggest that by 2026, energy storage could account for around 31% of total lithium consumption, up from about 23 % in 2025. This shift underscores how storage is gaining ground relative to other uses like EV batteries.

Source: Reuters

China has emerged as the dominant force in both production and deployment. Its policy reforms and manufacturing scale are driving rapid growth. Meanwhile, falling battery costs and strong demand from grids and renewables are pushing stationary storage into the mainstream.

As BESS becomes more important for clean energy and grid reliability, investments, deployments, and innovations in lithium systems are likely to continue rising well into the next decade.

L’Oréal, the global beauty giant, has unveiled its first cohort of startups participating in its new sustainable innovation program, L’AcceleratOR. The program chose 13 startups focused on climate, nature, and circularity. They were selected from nearly 1,000 applicants across 101 countries. It aims to find, pilot, and scale solutions that address key environmental challenges in the beauty industry and beyond.

The initiative is part of L’Oréal’s larger sustainability plan, called “L’Oréal for the Future.” This plan includes bold goals for climate action, resource use, and a shift to a circular economy by 2030 and beyond.

Inside L’AcceleratOR: Funding, Pilots, and Scale

L’AcceleratOR is a €100 million (about US$116 million) sustainable innovation program. The funding will be provided over a five-year period. The program helps startups and small to medium-sized enterprises (SMEs) that create sustainable solutions for L’Oréal and the beauty industry.

L’AcceleratOR is in partnership with the University of Cambridge Institute for Sustainability Leadership (CISL). Selected startups will enter an intensive support phase led by CISL. They will receive funding, expert guidance, and access to L’Oréal’s research and testing capabilities. The aim is to help these companies become pilot-ready and scale their solutions for broader use.

Data intelligence tools to measure and reduce environmental impacts

Startups may run six- to nine-month pilots with L’Oréal and its partners. Successful pilots may be scaled across global operations if they show measurable benefits.

“To accelerate sustainable solutions to market, we are being even more intentional and inclusive in our pursuit of partnerships through “L’AcceleratOR”. We are really energized to be co-designing the future of beauty with the University of Cambridge Institute for Sustainability Leadership, and these 13 change makers.”

The 13 Startups and Their Focus Areas

The selected startups and SMEs represent a range of sustainable innovations across climate, nature, and circularity. They fall into four main categories:

Packaging and materials

Nature-sourced ingredients

Circular solutions

Data intelligence

Source: L’Oréal

These 13 startups use different ways to cut environmental impact. They focus on product design, supply chain management, and manufacturing to promote circularity.

L’AcceleratOR is part of L’Oréal’s broad 10-year sustainability roadmap, “L’Oréal for the Future.” The roadmap covers four main areas: climate, nature, materials circularity, and communities. It includes the 2030 goals that aim to transform operations while driving innovation in sustainable solutions.

Source: L’Oréal

Some of L’Oréal’s key targets under the roadmap include:

Sustainable sourcing of at least 90% bio-based materials in formula and packaging.

100% recycled or reused water for industrial purposes.

Reducing virgin plastic use by 50%.

Sourcing 50% of packaging from recycled or bio-based materials.

Cutting Scope 1 and 2 emissions by 57% and some Scope 3 emissions by 28% against a baseline year.

Source: L’Oréal

The L’AcceleratOR program expands these efforts by tapping external innovation. L’Oréal supports startups to speed up solutions that can cut environmental impacts throughout its value chain.

L’Oréal’s Scope 3 emissions are by far the largest part of its footprint, as seen below. This reflects impacts from sourcing, production inputs, logistics, product use, and end-of-life. In 2024, Scope 1 and 2 fell further to about 227,051 tCO₂e, showing continued reductions in direct and energy-related emissions. Total emissions, though, remained roughly stable at 7.41 million tCO₂e, increased with Scope 3 again the largest component.

Source: L’Oréal

L’Oréal also has other sustainability initiatives. For example, its Fund for Nature Regeneration has invested more than €25 million (about US$29.1 million) in projects like forest, mangrove, and marine ecosystem restoration. This reflects L’Oréal’s commitment to nature and biodiversity alongside climate action.

Water stewardship is another strategic focus. In 2024, 53% of the water used in L’Oréal’s industrial processes came from reused and recycled sources. This was supported through water recycling systems in areas facing water stress.

Implications for the Beauty and Consumer Goods Sector

L’Oréal’s accelerator initiative reflects a larger industry trend. Many global companies are increasingly investing in sustainable technologies through partnerships, incubators, and venture funds. These partnerships aim to speed up climate, nature, and circular solutions. They combine corporate scale with startup agility.

The L’AcceleratOR program connects L’Oréal with companies that use innovation and partnerships to achieve their environmental goals. It also shows that sustainability strategies can go beyond internal changes. They can support the larger ecosystem, too. Helping startups scale can benefit whole industries, not just single companies.

This trend is important in areas like packaging, materials science, green chemistry, and digital climate tools. Packaging waste and carbon emissions from supply chains are major problems for consumer goods. This is especially true in beauty and personal care.

The beauty industry accounts for about 0.5% to 1.5% of global greenhouse gas emissions. Most of these emissions come from the value chain, not from company factories. For many beauty companies, around 90% of total emissions are Scope 3, such as raw materials, packaging, transport, and product use.

Raw material sourcing, including agricultural inputs and plastics, can make up 30% to 50% of industry emissions. Consumer use also adds a large share, especially for products that require water and heat.

The industry produces about 120 billion beauty packaging units each year worldwide. Much of this packaging is single-use and hard to recycle. A typical beauty product can generate several kilograms of CO₂-equivalent over its life cycle, from production to disposal.

Notably, most emissions are in the value chain. So, new solutions in packaging, materials, and data tools are key to cutting the beauty sector’s climate impact. This is what L’Oréal seeks to address. By supporting solutions in these areas, it hopes to change old industry practices.

Early Expectations and Next Steps

The 13 selected startups will now enter the pilot readiness phase of the L’AcceleratOR program. During this phase, the startups will refine their technologies with CISL guidance and L’Oréal support. The goal is to ensure their solutions are ready for real-world testing in commercial environments.

If pilot outcomes are successful, solutions may be scaled beyond initial tests. Some could fit into L’Oréal’s global operations or be used by industry partners. This would speed up sustainable progress.

L’Oréal and CISL plan future cohorts for the L’AcceleratOR program. Future rounds will create chances for more companies. They will also expand the pipeline of sustainable solutions.

By partnering with the University of Cambridge Institute for Sustainability Leadership and supporting startups across packaging, materials, ingredients, circular systems, and data tools, L’Oréal aims to fast-track real solutions that reduce environmental impacts.

The initiative boosts L’Oréal’s sustainability plan, “L’Oréal for the Future.” This plan sets bold goals for 2030, focusing on renewable energy, resource use, cutting emissions, and promoting circularity.

The pilot and scaling opportunities in the program can help new technologies join global supply chains. This support will aid L’Oréal and its partners in tackling climate, nature, and circular economy challenges towards its net-zero goals.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.