The European Commission (EC) recently proposed a bold climate target: reduce net greenhouse gas emissions by 90% by 2040 compared to 1990 levels. For the first time, the plan allows up to 3% of this reduction to come from international carbon credits. This marks a major shift in EU climate strategy—blending domestic action with global cooperation.

Ambitious Goal with New Flexibility: A Shift in the EU’s Climate Strategy

Under the EU’s original plans, all emission cuts had to occur within its borders. Now, the EU will permit a limited share of high-quality international carbon credits, starting in 2036, and no more than 3% of the total 90% target by 2040. This allows the bloc to maintain ambition while offering economic and technical ease for industries under stress.

In announcing the proposal, European Commission President Ursula von der Leyen called it “a clear, pragmatic and realistic” step. Officials say that allowing member states some flexibility sends a good message. This approach benefits both local industries and global climate partners.

The Commission states that with the new proposed target, the EU is:

“…sending a signal to the global community: it will stay the course on climate change, deliver the Paris Agreement and continue engaging with partner countries to reduce global emissions.”

How the New Framework Works

The new EU climate plan aims to cut net greenhouse gas emissions by 90% by 2040, based on 1990 levels. This target includes direct emission cuts, domestic carbon removals, and the use of carbon credits. However, the plan strictly limits the role of international carbon credits.

Starting in 2036, the EU will allow up to 3% of the 90% reduction goal to be met using carbon credits from outside the EU. These credits must meet high-quality standards and undergo transparent monitoring.

SEE MORE: International Carbon Credits Back on the Table? EU’s Climate Goal Gets a Twist

Most emissions reductions need to happen in Europe. This can be done by:

- Improving energy efficiency,

- Expanding clean energy,

- Capturing and storing carbon, and

- Using sustainable land management practices.

Carbon removal methods—whether through planting trees, improving soil health, or using new technologies—will also play a role. These efforts are already being tracked through the EU Emissions Trading System (ETS). It will also govern how domestic carbon removals are counted.

The framework focuses on internal solutions first. It looks at international carbon offsets only after. This way, the EU aims to cut emissions at home before using credits from other countries.

Why Include Carbon Credits?

Ministers from Germany and Poland said the 90% target could hurt the manufacturing, transport, and heating sectors. A 3% international offset helps ease this pressure. It allows the EU to buy emission reductions from projects in developing countries. These projects include forest conservation and cleaner cookstoves.

Supporters see this as a win-win, mixing ambition with resilience. But, scientific advisers warn that these credits might slow down home-grown clean energy efforts. They cautioned: it “might divert resources” if misused.

The Credit Tug-of-War: Flexibility vs. Integrity

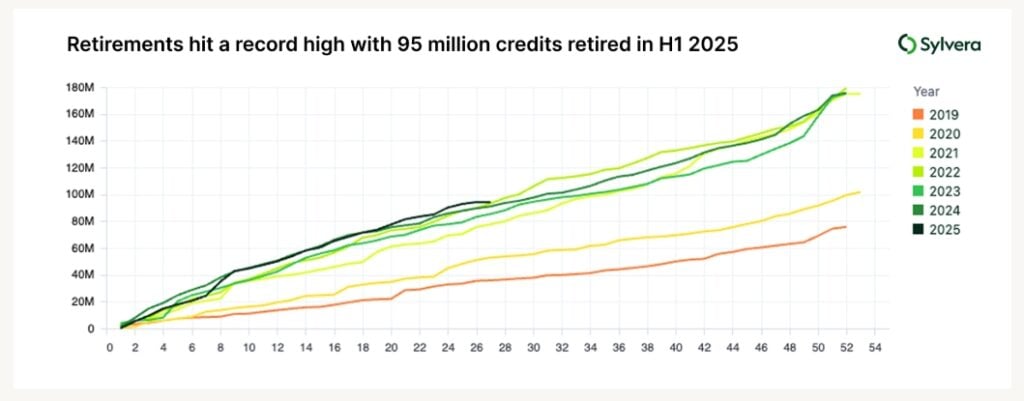

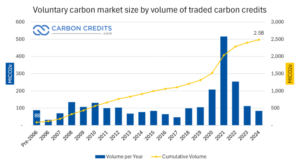

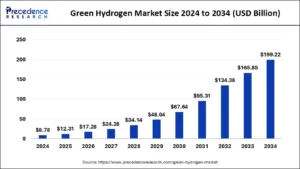

The shift has sparked a heated debate. Supporters say carbon credits offer economic flexibility for EU industries. This helps them manage costs and still meet climate goals. The chart below shows the traded volume of voluntary credits that entities used in offsetting emissions.

Moreover, the credits can provide important funding for emission-reduction projects in developing countries. This helps build global cooperation and solidarity in the fight against climate change.

However, critics warn that past reliance on carbon credits has not always resulted in real emissions cuts. Some projects have been poorly monitored, or overestimated their climate benefits.

They worry that if the EU relies too much on credits, it could slow down important actions at home. This includes growing renewable energy and updating infrastructure.

Scientists and environmental groups stress the need for strict rules. They warn that low-quality or unverified credits can harm public trust. This, in turn, can slow real climate progress.

Colin Roche, from the Friends of the Earth Europe, remarked:

“The European Commission will try to portray this as an ambitious step forward, but the reality is we are fast running out of room to achieve the Paris agreement. This target is in line neither with climate science nor with climate justice.”

To address these concerns, the European Commission plans to introduce a set of EU-wide rules in 2026. These rules will aim to ensure that carbon credits are transparent, traceable to their origin, and meet strong integrity standards. This step helps stop greenwashing. It also ensures that using credits really supports the EU’s climate goals, not just in theory, but in real life.

To prevent abuse, the Commission plans to propose EU-wide rules in 2026, ensuring transparency, clear origins, and high integrity.

What This Means for EU Policy and Global Climate Action

These reforms set the stage for mid-term climate planning ahead of the EU’s 2035 submission under the Paris Agreement, which is due by September.

By promoting a 90% target with a 2036–2040 credit window, the EU signals both ambition and realism. Yet it also underscores that pure domestic reductions remain unpopular among some Member States. Denmark’s climate minister urged not to “stall the green transition” despite pressures for flexibility.

This shift may also impact the EU’s global image. Compared with slower-moving nations, the EU positions itself as a climate leader. However, critics worry that lean credit use could be seen as avoiding internal responsibilities.

For international carbon markets, the EU’s plan is a major boost, potentially adding 140 million tonnes worth of demand by 2040. But sluggish rollout and tight standards may limit near-term impact.

Eyes on 2026: Rules, Votes, and What to Watch

Looking forward, here are some major things to watch as the region continues with this new proposal:

- Approval Process: The proposal needs approval from the European Parliament and all 27 EU Member States.

- Credit Rules by 2026: Watch for legislation defining which offset projects meet EU standards—no shortcuts.

- Member State Limits: Key actions may focus on how countries use credits, for example, in transport versus energy.

- Future Targets: The 2040 rule will guide the EU’s 2035 climate pledge and set the course toward net-zero by 2050.

- Industry Response: Some businesses may welcome flexibility with stricter emissions. Others might push for deeper cuts at home.

The EU’s new law is a compromise that balances ambition with adaptability: maintaining momentum while giving industries breathing room. Critics caution that credits must not replace hard-fought investment in domestic clean infrastructure. Ensuring strong governance and transparent carbon credit standards will be key to aligning the EU’s high-level goals with on-the-ground climate action.

As the EU prepares to finalize the law and set its 2035 target, one message is clear: global cooperation will count—but so will cutting emissions at home.

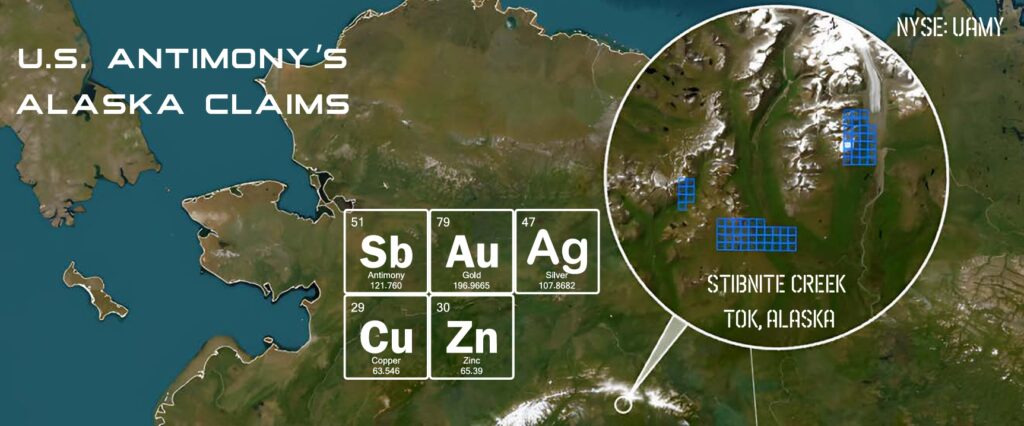

Ramps Up Domestic Mining to Strengthen America’s Supply Chain")

Is a Long-Term Winner in Clean Energy and EV Markets?")