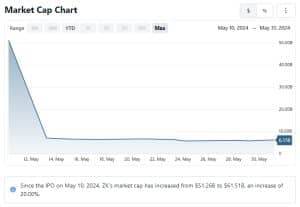

On May 10, Zeekr’s shares soared almost 35% above their initial public offering price, marking a robust debut for the electric vehicle (EV) manufacturer. This is the first significant U.S. market debut by a China-based company since 2021. Zeekr’s successful U.S. flotation aims to distinguish it from the competition of Chinese EV makers vying for a larger European market share.

Zeekr, a high-end EV brand under Geely, the parent company of Volvo and Lotus, has been gaining attention for its luxury electric sedans and SUVs. The company’s flagship model, the Zeekr 001, boasts features like rapid acceleration, advanced driving assistance systems, and a fast-charging battery, making it a strong contender in the premium segment.

High Stakes: Chinese EV Giants Eye Premium Market to Navigate US Tariffs

US Tariffs and Market Strategy

In the past year, Chinese electric car manufacturers have shifted their focus from producing small, inexpensive vehicles to targeting the premium market. This transition coincides with a new 100% import duty imposed by the US on Chinese EVs, posing a significant challenge as these companies begin their global expansion with high-end cars.

Zeekr’s debut comes as the Biden administration plans to increase tariffs on Chinese vehicle imports.

ZEEKR’s CEO, Conghui “Andy” An, has said that,

“ZEEKR plans to enter six European countries in 2024, including Germany, Sweden, and the Netherlands, and is targeting another 38 markets across Southeast Asia and the Middle East.”

Consequently, some companies might halt US expansion plans due to increased costs, while others may establish production facilities in Mexico to bypass tariffs.

Zeekr’s Strategic Leap: Strong IPO and Global Ambitions Amid EV Competition

CATL Partnership

A key factor behind Zeekr’s appeal is its cutting-edge technology. The company benefits from a close relationship with CATL, China’s largest battery manufacturer, providing early access to the latest battery advancements. This partnership ensures that Zeekr vehicles have a competitive range and performance, crucial for success in the high-end market.

Expansion Plans Beyond China

Zeekr was established to meet the growing demand for premium models in China. While the high-end EV brand has seen strong sales growth at home, the company now aims to expand internationally. The US debut marks a key step in Zeekr’s strategy to capture a share of the lucrative North American EV market. This entry coincides with rising consumer demand for electric vehicles, driven by growing environmental awareness and supportive government policies.

Intense competition in China among domestic EV makers and with Tesla has squeezed profits, pushing companies to explore international markets.

As highlighted by Zeekr, the IPO debut achieved a fully diluted valuation of $6.8 billion, about half of the $13 billion valuation from a funding round last year.

In the competitive market, Chinese automakers like BYD, SAIC, and Great Wall Motor are also targeting Europe. They are launching electric models to compete with established European manufacturers. This is why Chinese EV sales in Europe have grown significantly in recent years.

source: Stock analysis

Zeekr’s Stock Soars: Stellar Market Performance Amidst EV Boom

Latest market reports state that Zeekr’s shares peaked at $29.36 after opening at $26, well above the IPO price of $21, closing at $28.26, up 34.6%.

In 2023, Zeekr Intelligent Technology Holding achieved impressive financial results. Here are the key highlights:

Annual Revenue:

Zeekr’s annual revenue in 2023 reached $7.29 billion.

This represents a remarkable 59.24% growth compared to the previous year.

source: Stock Analysis

Quarterly Performance:

For the quarter ending December 31, 2023, Zeekr reported revenue of $2.31 billion.

The year-over-year growth rate for this quarter was an impressive 75.69%.

EV Sales:

Zeekrs is renowned for focusing on electric mobility. By the end of 2023, Zeekr had delivered over 100,000 electric vehicles. The brand unveiled its third model, the Zeekr X, and began delivering vehicles to users in Europe.

Significantly, this year Zeekr aims to 2x its annual sales with a target of over 200,000 units.

Zeekr has outpaced its competitors in deliveries since the beginning of the year. By April 30, Zeekr delivered 49,148 vehicles, surpassing Xpeng’s 31,214 units and Nio’s 45,673 cars during the same period.

The company’s IPO comes amid rising geopolitical tensions between the U.S. and China, involving trade, intellectual property, Taiwan, and China’s stance on the Russia-Ukraine war.

In April Zeekr witnessed a remarkable achievement by surpassing Tesla in car sales.

This strongly indicated potential competition for the American EV giant. The achievement further highlights Zeekr’s strong domestic presence and its ability to challenge established industry leaders.

On this stellar performance, Zeekr CEO Andy An commented:

“Our sales gap with Tesla keeps on narrowing,”

Despite the impressive sales performance, Zeekr faces fierce competition from Tesla and others in the EV market, amid geopolitical tensions and trade uncertainties. Yet, its focus on luxury features, innovative tech, and a successful IPO signals optimism and strong investor interest amidst broader market losses.

The company said in its SEC filing:

“Through developing and offering next-generation premium BEVs and technology-driven solutions, we aspire to lead the electrification, intelligentization, and innovation of the automobile industry.”

Looking forward, Zeekr’s ~ 35% surge in its US market debut marks a promising start for the Chinese EV maker. Zeekr is committed to delivering high-quality, technologically advanced EVs as it navigates the competitive landscape and expands its international footprint Investors and consumers alike will be watching closely to see how Zeekr leverages this momentum in the coming months.

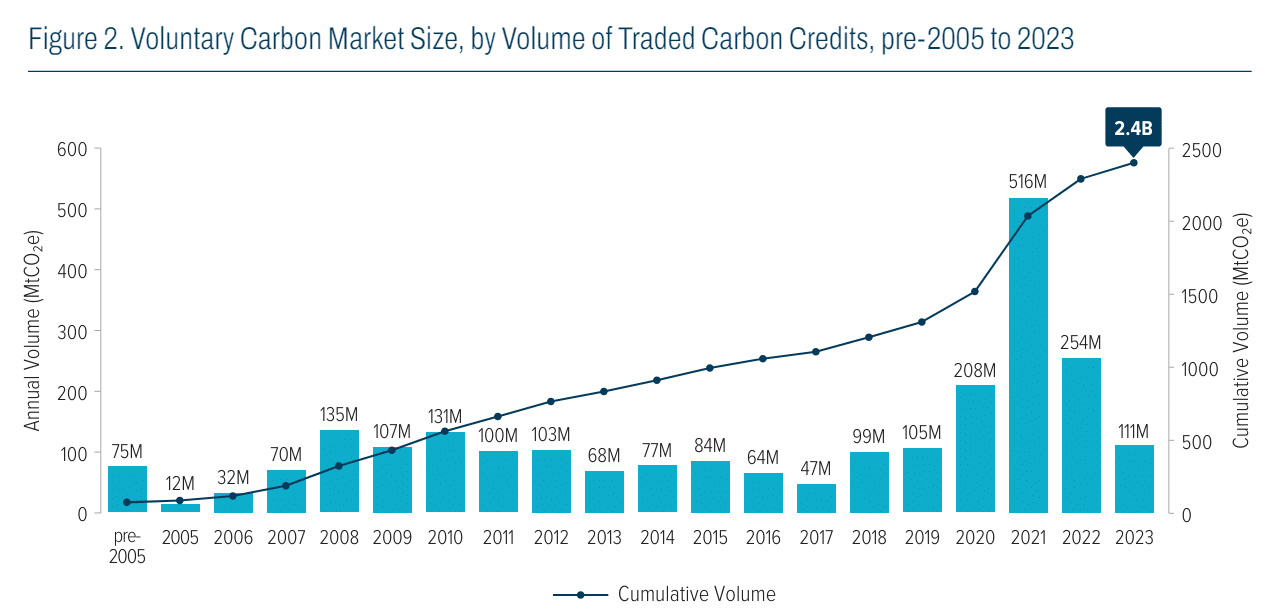

Ecosystem Marketplace (EM) releases the 2023 State of the Voluntary Carbon Market (SOVCM) report, thoroughly analyzing global voluntary carbon credit supply and demand. The report combines interviews and disclosures from key market players with registry data from major carbon credit standards. While retrospective, the report also provides insights into future market trends.

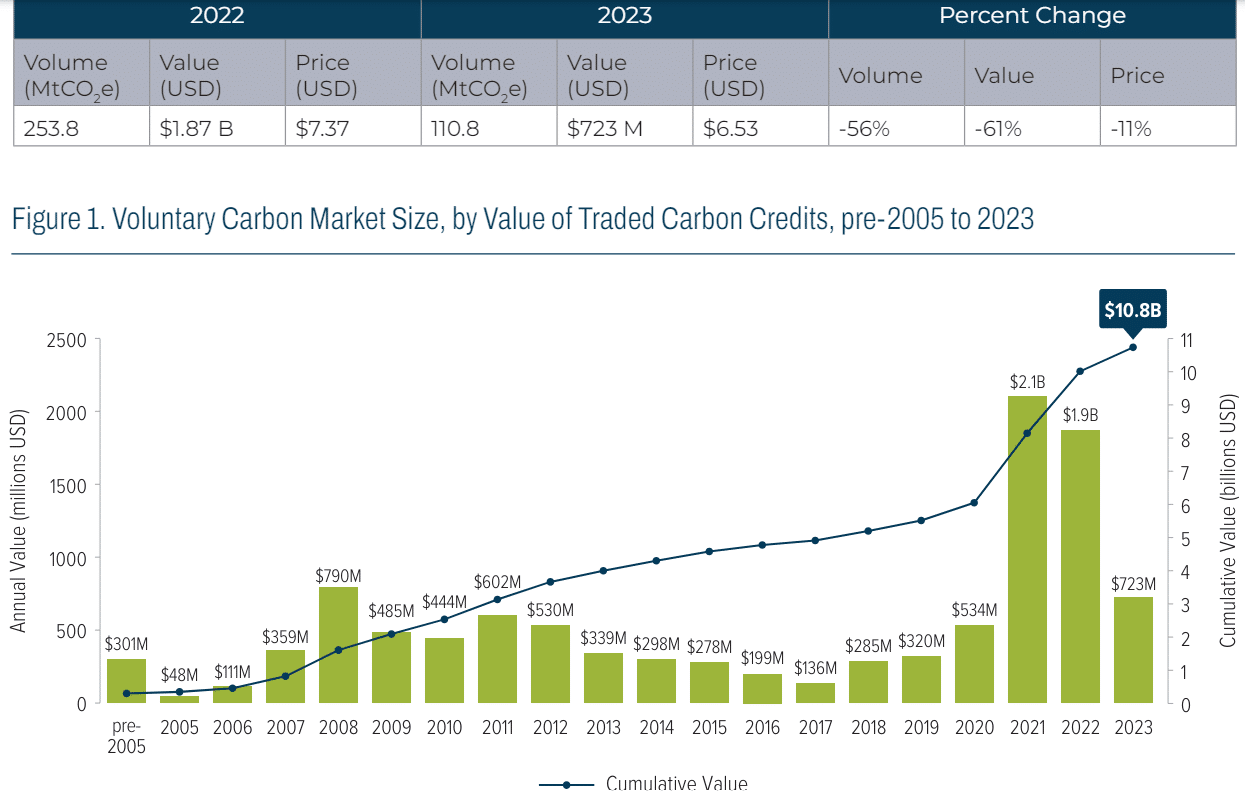

2023 marked a significant year for the market, characterized by more scrutiny due to media coverage of unethical carbon projects. Despite this, the market’s value rose for the fourth consecutive year since 2020, reaching $723 million in 2023. This trend, which began in 2020 and peaked in 2021 with over $2 billion in carbon credits traded, has partially offset declining transaction volumes.

Overall, 49% of the total VCM value reported to EM since 2005 occurred between 2020 and 2023, signaling significant market growth and resilience. We crunch the EM report, with the following highlights.

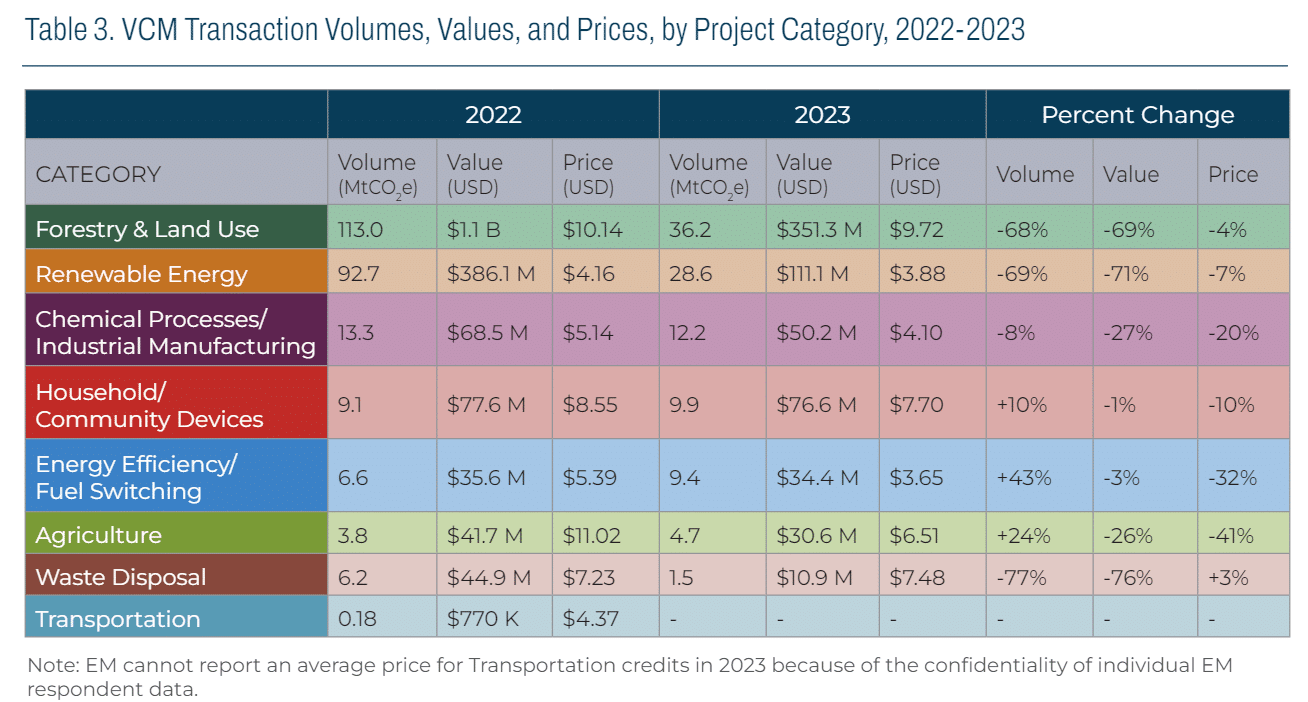

The Big Picture: Volume, Value, and Price Dynamics

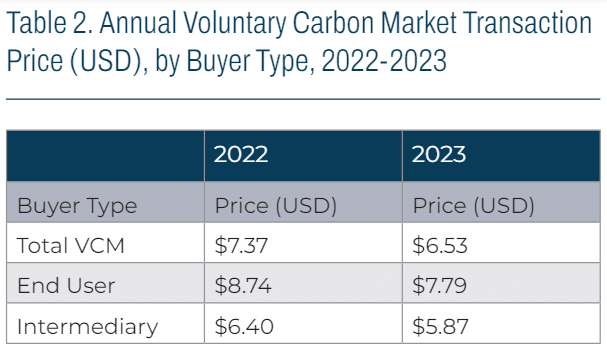

In 2023, the voluntary carbon market (VCM) experienced a significant downturn, with total transactions plummeting by 56% to 111 million tons CO2e compared to the previous year. Despite this steep decline in volume, the average price per ton of CO2e only saw a moderate decrease of 11%, reaching $6.53.

Consequently, the total market value also took a hit, dropping by 61% year-over-year to $723 million. This decline in market activity was primarily attributed to both a reduction in volume and a retreat from the peak carbon prices observed in 2022.

The decrease in the number of market respondents further contributed to the downturn, with some entities merging and others temporarily halting credit sales as they awaited the establishment of stronger integrity and quality norms within the VCM. As a result, the number of respondents providing transaction data decreased from the previous year.

Qualitative feedback from market participants revealed divergent trends among different segments of the market. Remarkably, there was a notable preference among buyers for credits sourced from nature-based and community-focused projects, which offer additional environmental and social co-benefits alongside emissions reductions.

This shift in preference away from carbon removal projects contributed to the decline in overall market volume. However, the impact on market value was less pronounced.

Buyer Behavior: Premiums and Preferences

The EM report further highlighted notable variations in credit prices depending on the buyer type. End users, who directly use carbon credits for emission reduction purposes, paid a premium of 33% over intermediaries, consistent with the previous year. This premium reflects the value end users place on credits for achieving their sustainability goals.

Notably, transactions involving Energy Efficiency/Fuel Switching and Renewable Energy credits saw the largest premium for end users. This indicates a reliance on intermediaries for project quality assessment.

Among different credit standards, Gold Standard credits commanded the highest premium for end-user sales, amounting to 140%, up from 83% in 2022. This suggests a growing preference among buyers for trusted intermediaries to vet project quality.

Similarly, Clean Development Mechanism (CDM) and Verified Carbon Standard (VCS) credits also saw substantial increases in premiums for end-user sales. The shift towards intermediaries for project quality assessment is particularly pronounced in CDM transactions, with 73% of sales going to intermediaries in 2023.

These trends may reflect market uncertainty surrounding the transition of CDM projects to future mechanisms under the Paris Agreement. This prompted buyers to rely more on intermediaries for quality assurance.

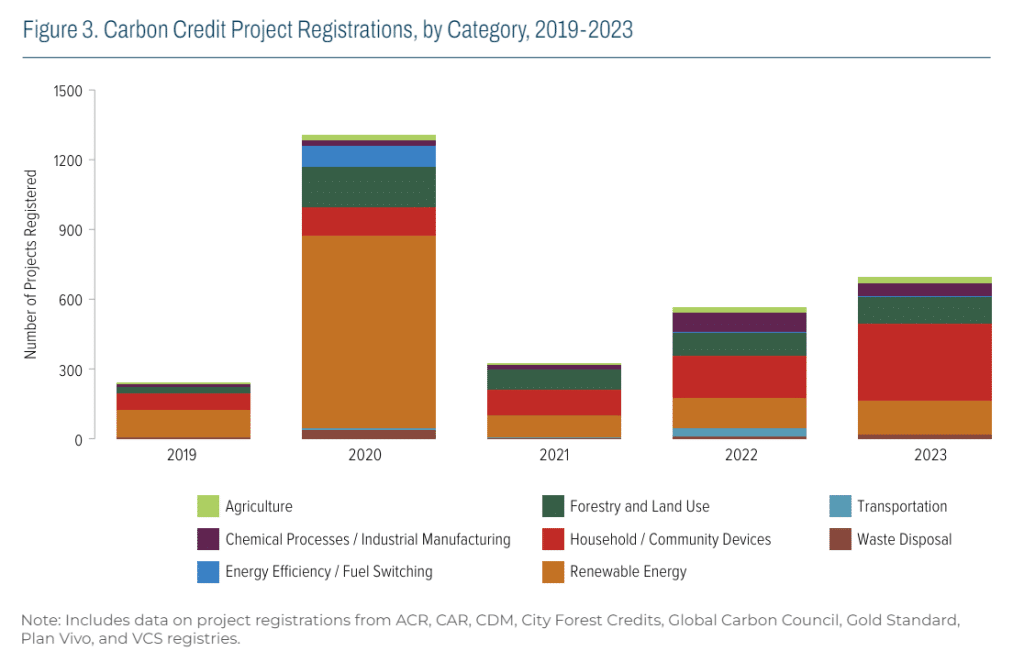

Registry Round-Up: Project Registrations and Trends

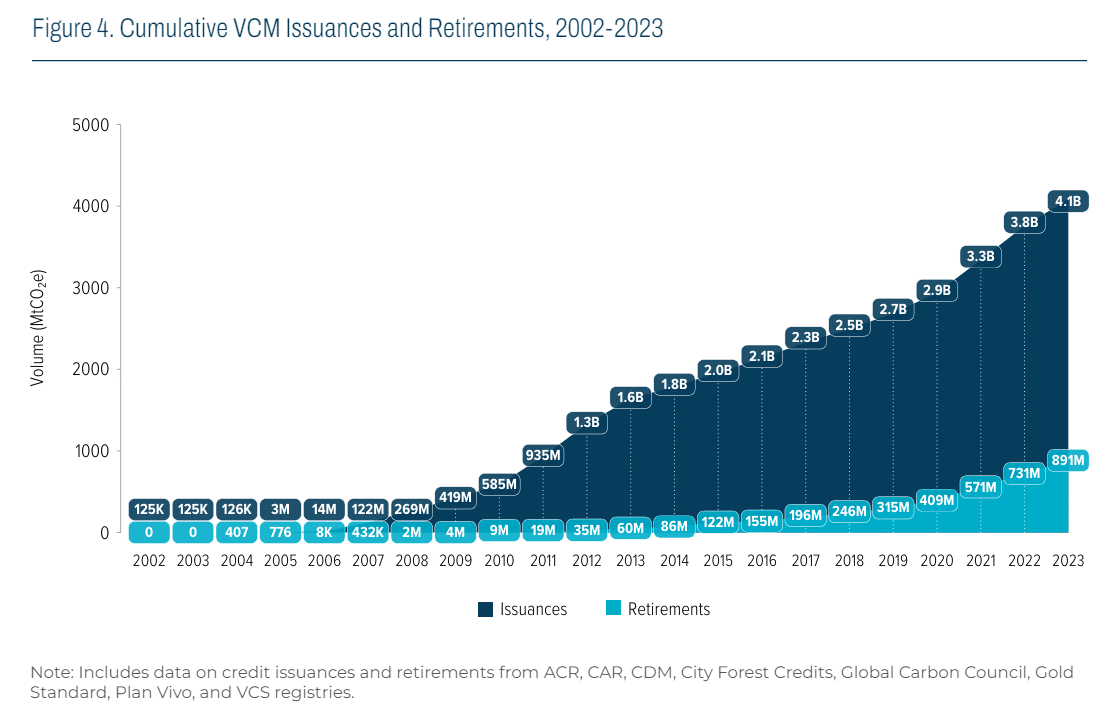

Analysis of registry data from credit standard registries provides insights into the dynamics of project registrations, issuances, and retirements in the VCM.

Despite challenges, the total number of newly registered projects increased to 694 in 2023, with Household/Community Devices projects leading the growth. Registrations in Forestry and Land Use, Renewable Energy, Agriculture, and Waste Disposal categories also saw year-on-year increases.

In terms of credit issuances, it decreased by 93 MtCO2 e in 2023 compared to 2022. Meanwhile, retirements increased by 2.6 MtCO2 e, indicating a tightening surplus supply of carbon credits.

Declines in issuances were observed in Chemical Processes/Industrial Manufacturing and Energy Efficiency/Fuel Switching categories, while Household/Community Devices and Transportation projects experienced increases.

Forestry and Land Use, and Chemical Processes/Industrial Manufacturing categories saw the greatest growth in retirements, suggesting a preference for projects with clear carbon removals and emissions reductions. Conversely, retirements of Renewable Energy, Waste Disposal, and Transportation credits decreased.

Total annual credit retirements have remained around 170 MtCO2 e for the past three years, indicating steady fundamental demand. However, there’s potential for increased retirements if corporate buyers can claim credits as offsets against their Scope 3 emissions targets. These trends reflect shifting preferences towards projects with stronger additionality and clear carbon impact within the VCM.

Evolving Project Preferences

The decline in total market value for all categories of VCM credits in 2023 was accompanied by various factors affecting each category. While some categories experienced increases in volume and/or average transaction price, others faced declines.

Energy Efficiency/Fuel Switching, Agriculture, and Household/Community Devices categories saw volume growth, indicating increased activity. However, Forestry and Land Use and Renewable Energy credits witnessed the largest declines in volume, despite being popular project types.

However, Blue Carbon credit volume plummeted, with prices driven down, particularly for Wetland Restoration/Management projects without ARR activities.

Notably, North American industrial process efficiency credits were transacted at lower prices, contributing to the price decline in the Chemical Processes/Industrial Manufacturing category. These trends illustrate shifting dynamics within different segments of the VCM, reflecting evolving market preferences and supply factors.

Carbon Streaming Corporation has announced pivotal changes to its leadership and board composition in a strategic move to enhance its governance and operational agility.

Former Equinox Gold CEO Christian Milau steps in as the interim CEO, with Olivier Garret appointed as the new Chair of the Board. These appointments come on the heels of the resignation of Justin Cochrane and Maurice Swan from their director roles.

The stock was up as much as 135% in early trading on significant volume compared to its average.

New Appointments and Market Impact

This leadership overhaul follows a series of constructive dialogues between the board and influential shareholders, spearheaded by Marin Katusa. The changes aim to steer the company towards more robust growth and operational efficiency amidst the fluctuating dynamics of the carbon credit market. The company has also welcomed Marcel de Groot to the board, with additional responsibilities as the Chair of the Audit Committee.

Amidst these changes, Carbon Streaming has successfully acquired Blue Dot Carbon Corp. for a purchase price of $2.5 million, payable in Carbon Streaming shares.

This acquisition is a strategic expansion move, bringing in new assets and expertise to bolster Carbon Streaming’s portfolio in the carbon finance sector whose interests are aligned with shareholders. The transaction was unanimously approved by the Board upon the recommendation of the Special Independent Committee.

Sources indicate Marin Katusa negotiated and facilitated the transaction with Christian Milau, the CEO of Blue Dot.

The newly formed board has embarked on a mission to navigate Carbon Streaming through a critical phase. They aim to reposition the company as a leader in the carbon finance sector, focusing on high-integrity carbon credit projects that align with global climate action goals.

This involves a meticulous strategy to enhance cash flows, recover shareholder value, and ensure sustainable project delivery.

In his role as interim CEO, Christian Milau articulated his commitment to driving the company towards achieving positive operating cash flows and executing a robust project pipeline. In addition, there’s no change of control pay outs for the new management. The previous management’s change of control provisions was also canceled.

Milau’s extensive experience in managing large-scale projects across diverse geographies will play a crucial role in Carbon Streaming’s strategic realignment. His immediate focus is on leveraging the company’s strengths to improve financial performance and stakeholder returns.

Additionally, the company is set to enhance its governance framework and operational transparency. This includes a comprehensive review of existing investments and the strategic pipeline under the new leadership. The board is committed to maintaining high standards of corporate governance and stakeholder communication. This is to ensure that Carbon Streaming remains a trustworthy and effective participant in the carbon markets.

In addition, to support the new management and board of directors, Marin Katusa will be a special advisor on technical and financial matters to the board of directors. Katusa waived all fee’s to further advance the interests of the shareholders, of which he is the largest individual investor.

New Key People Onboard:

Olivier P. Garret

Mr. Garret is a successful business executive and turnaround agent with experience working across a dozen different industries. In his capacity as CEO or Chief Restructuring Officer, he has led the growth and restructuring of companies in the financial industry, defense industry, as well as a variety of manufacturing and service businesses.

For the past 16 years, Mr. Garret has successfully launched and led the growth of five financial research and publishing companies, one gold bullion company, four resource funds, and two real-estate funds. Mr. Garret earned an MBA from the Amos Tuck School at Dartmouth in 1989 and a Masters in Business Management from the University of Paris-IX in 1983.

Christian Milau

Mr. Milau is CEO of Blue Dot, a private carbon credit financing company. He has also led a number of gold and copper mining companies through growth from single asset to large multi-national, multi-billion dollar NYSE-listed groups with the highest standards of environment, social and governance implementation.

Companies Mr. Milau has led, or for which he has been part of the senior management team, include Equinox Gold, True Gold Mining, Endeavour Mining and New Gold. He is currently a non-executive director of two junior energy metals exploration companies, Arras Minerals and Copper Standard Resources.

Mr. Milau holds a Bachelor of Commerce degree from the University of British Columbia and is a Chartered Professional Accountant.

Marcel de Groot

Mr. de Groot is a co-founder and the President of Pathway Capital Ltd. Pathway Capital partners with successful mining entrepreneurs to launch new ventures. Examples of such ventures include Peru Copper (acquired by Chinalco), Equinox Gold, and Solaris Resources. He has over 25 years of experience in providing strategic support to both private and public companies within the resource industry. Mr. de Groot is currently a director of Sandbox Royalties and Copper Standard Resources.

Mr. de Groot holds a Bachelor of Commerce degree from the University of British Columbia and is a Chartered Professional Accountant.

McKinsey & Company released its 2023 ESG Report titled “Accelerating sustainable and inclusive growth for all,” detailing its global efforts to promote sustainability and inclusivity. The report highlights McKinsey’s partnerships with clients, colleagues, and communities to foster societal progress.

Here are the key takeaways from McKinsey’s 2023 progress, focusing on their decarbonization efforts.

The net zero transition is transforming the global economy, creating new markets and threatening others. Leaders must reduce emissions, ensure affordable energy and materials, provide reliable energy systems, and enhance competitiveness.

McKinsey has prioritized sustainability, working with clients for over a decade to decarbonize and build climate resilience. The firm is committed to helping all industries reach net zero by 2050 and meet the Paris Agreement goals. McKinsey uses proprietary tools, thought leadership, talent, and cross-sector collaborations to drive innovation and growth.

The firm partners with entrepreneurs and start-ups to scale technological innovations rapidly. It also works with banks and investors to decarbonize portfolios, and engages with high-emission sectors to reduce emissions and costs. By scaling green ventures and expediting decarbonization, organizations can achieve climate commitments quickly, measuring progress in months rather than decades.

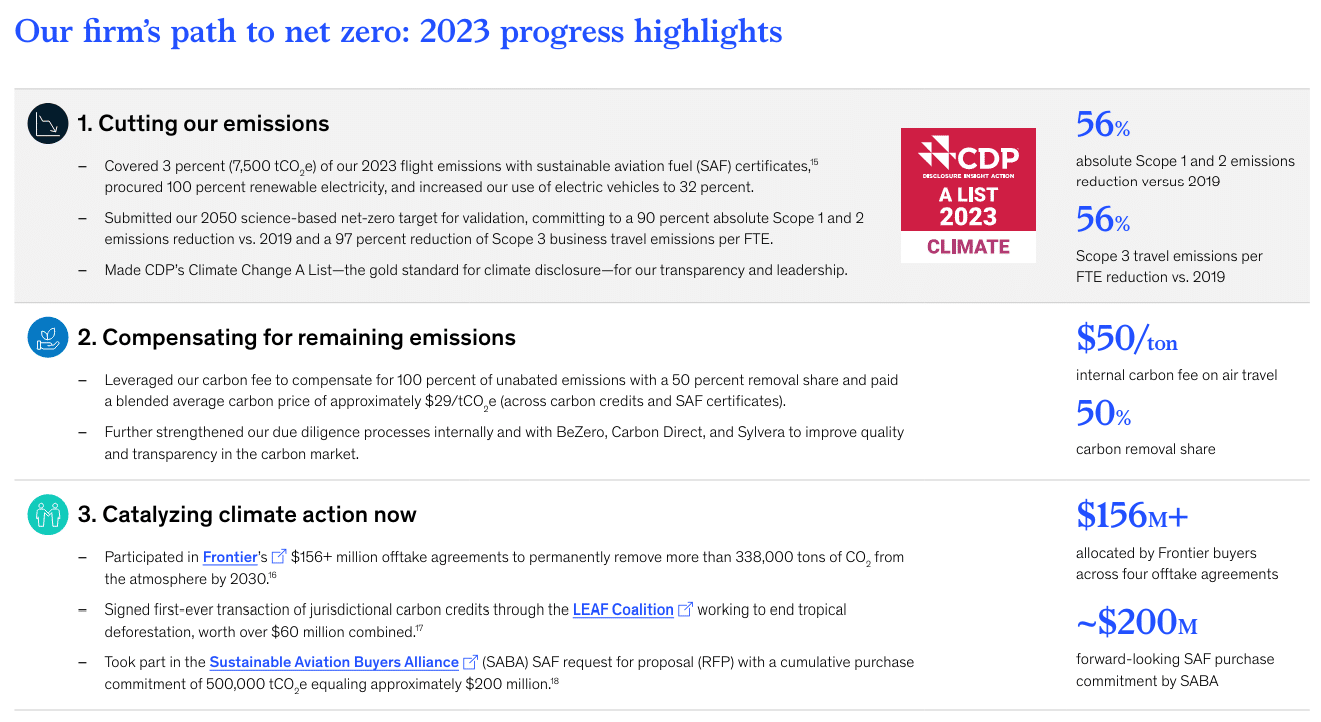

McKinsey faces the climate crisis heads-on by charting its path towards net zero with the following progress at a glance:

McKinsey’s Progress Toward Net Zero

Slashing Scope 1 and 2 Emissions

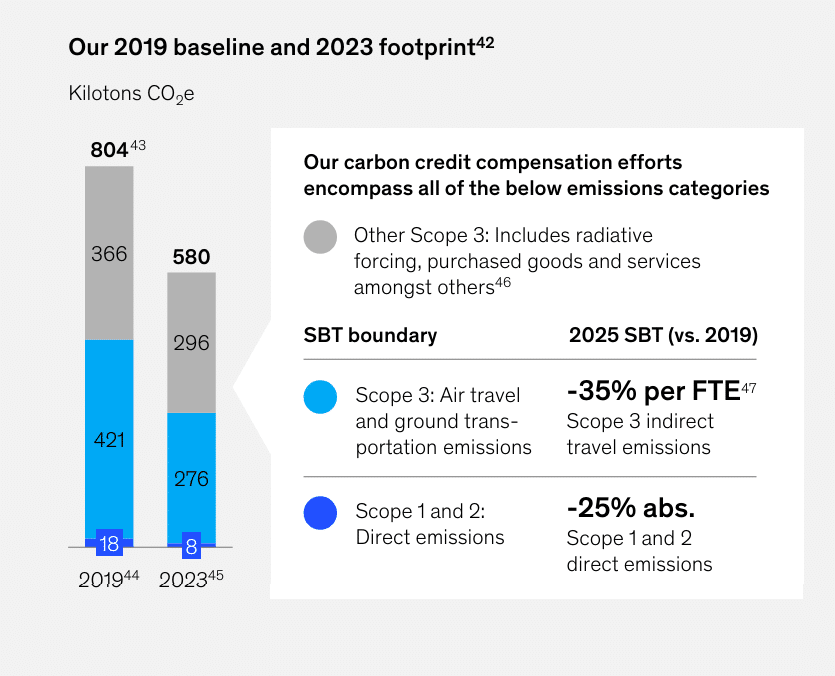

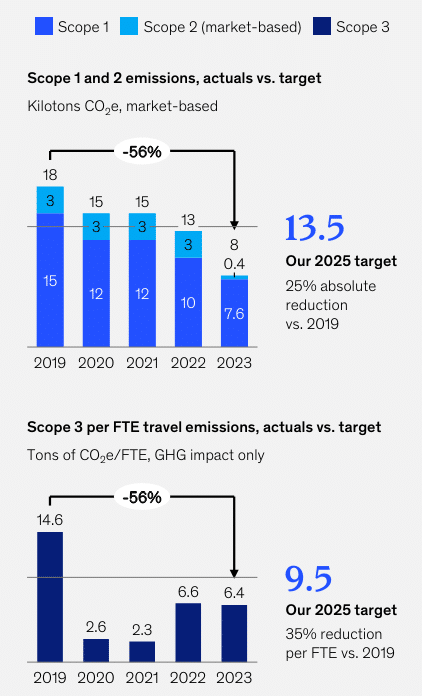

McKinsey has made significant progress towards achieving net zero emissions by addressing Scope 1 and 2 emissions, which account for 2% of their 2019 baseline. In 2023, they reduced absolute Scope 1 and 2 emissions by 56%.

The consulting firm also focused on electrifying their fleet of vehicles, with a remarkable increase in the global use of electric vehicles from 4% in 2019 to 32% by the end of 2023.

The company’s commitment to sustainability extends to making office spaces more sustainable, with 64% of global office space being LEED-certified and 55% being LEED Gold or Platinum certified. Transitioning to renewable electricity has been successful, as McKinsey achieved the goal of sourcing 100% renewable electricity two years ahead of schedule, with 98% procurement aligned with RE100 criteria.

Moreover, McKinsey has conducted comprehensive assessments of water, waste, and biodiversity, taking proactive measures to minimize water consumption and reduce single-use plastics.

Additionally, the firm drives change through local initiatives involving over 1,100 Green Team members. They contribute to reducing the firm’s environmental footprint through various activities like achieving office environmental management system certification, eliminating single-use plastics, and promoting vegetarian options in office cafeterias.

In summary, cutting Scope 1 and 2 emissions results in these major progress:

Electrifying firm-controlled vehicles: 32% share of EVs

Making office space more sustainable: 64% LEED‑certifed

buildings

Transitioning to renewable electricity: 100% renewable

Driving change through local initiatives: 1,100+ Green Team members

Cutting Scope 3 Emissions

Scope 3 emissions primarily originate from air travel, hotels, and ground transportation. In 2023, Scope 3 business travel emissions were down by 56% per FTE against the 2019 baseline. Efforts are underway to partner with suppliers to further reduce Scope 3 emissions.

Putting a price on emissions:

As of January 1, 2023, McKinsey introduced a global internal carbon fee of $50 per tCO2e on all air travel. The fee is calculated based on flight emissions and will expand to cover all emission categories in 2024.

This fee supports carbon-related procurement, including carbon removals and sustainable aviation fuel (SAF), while also raising colleague awareness of environmental footprints.

Fostering sustainability in aviation:

Collaborative efforts with airlines, fuel producers, and aviation stakeholders aim to make air travel more sustainable. SAF is deemed crucial, with procurement efforts aimed at building the market and learning from experiences.

Initiatives include participation in SAF RFPs and bilateral SAF certificate purchases, resulting in significant emission reductions. A total of 7,500tCO2e was abated through four SAF offtakes, equivalent to 3% of GHG fight emissions.

With all the decarbonization efforts done and progress achieved by McKinsey, the company managed to reduce its emissions vis-a-vis targets as shown below.

Tackling Residual Emissions with Carbon Credits

Compensating for residual emissions remains a key focus for the multinational consulting company through carbon credits.

Since 2018, they’ve invested in carbon avoidance and removal projects certified by international standards like the Gold Standard and Verified Carbon Standard, alongside Climate, Community & Biodiversity Standards (VCS+CCBS), to offset emissions they can’t yet eliminate.

McKinsey continually assesses its carbon credit project portfolio with third-party due diligence to ensure effectiveness.

In 2023, the company enhanced its approach by diversifying supplier base, refining scoring system based on internal quality criteria, and collaborating with external partners like BeZero, Carbon Direct, and Sylvera for additional feedback.

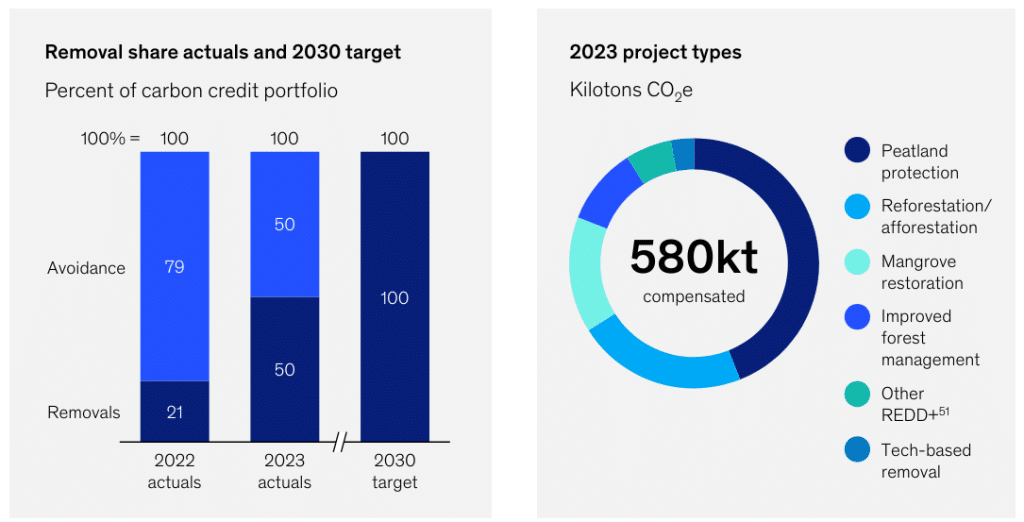

The sustainability champion also increased its share of carbon removal credits to 50%, primarily investing in nature-based solutions to address climate and biodiversity crises. Additionally, the company made its first technology-based removal purchase to scale biochar technologies.

Ultimately, McKinsey aims to transition to removing 100% of its remaining emissions by 2030. They’ll focus on nature-based solutions and a blended carbon price of around $29/ton.

McKinsey & Company’s 2023 ESG Report demonstrates the firm’s commitment to sustainability. With substantial reductions in their carbon footprint, strategic partnerships, and innovative approaches to decarbonization, McKinsey is on a clear path to achieving net zero emissions by 2050.

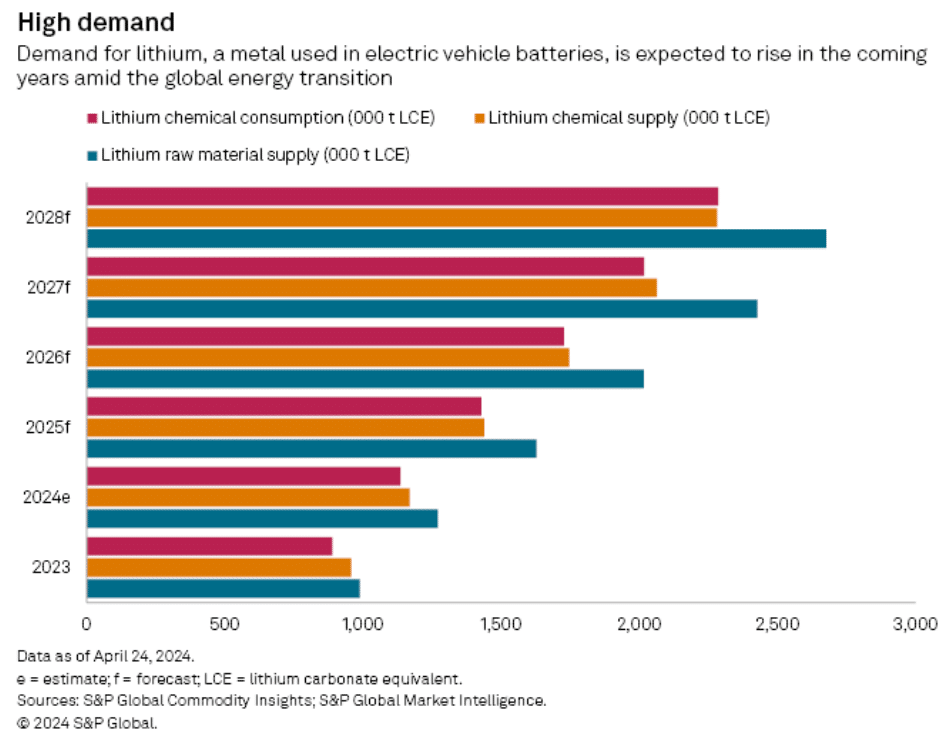

Facing unprecedented demand surges and volatile price swings, the world’s lithium producers are revolutionizing the way the commodity is bought and sold. Miners are using auctions to secure higher prices than those assessed by price reporting agencies (PRAs) as demand for the battery metal increases amid the energy transition.

Traditionally, the lithium market relied on private contracts, but the surge in demand has led to the introduction of public trading platforms. PRAs now provide price assessments, and the London Metal Exchange and Guangzhou Futures Exchange have launched futures market.

However, with a 2024 lithium price slump affecting margins, producers turn to spot auctions that yield better prices than PRA reports.

A Valuable Tool for Lithium Price Discovery

According to S&P Global Commodity Insights, market experts and participants expect auctions to continue, as companies aim to achieve favorable prices despite market downturns.

Albemarle Corp., a major US lithium producer, stated that auctions help in responsible price discovery. This benefits both buyers and sellers and contributes to a more sustainable market.

For Przemek Koralewski, global head of market development at price reporting agency Fastmarkets Global Ltd., auctioning lithium prices serve two things:

“It allows miners to get the price of the day and it means that the contracts on which most material is sold are truly reflective of market dynamics.”

Unlike other commodities with a single benchmark price, lithium prices are typically determined using a range of PRA assessments, incorporating data from various market stakeholders.

In 2022, lithium companies leveraged auctions to secure higher prices despite slowing demand for electric vehicles and rising COVID-19 infections impacting market prices. Alice Yu, an analyst at Commodity Insights’ Metals and Mining Research team, stated that “auction prices provide an extra means of price discovery and add to market transparency.”

The use of auctions decreased as pandemic effects waned and prices surged amid the energy transition. However, a supply glut and global decline in EV sales have caused lithium prices to drop again.

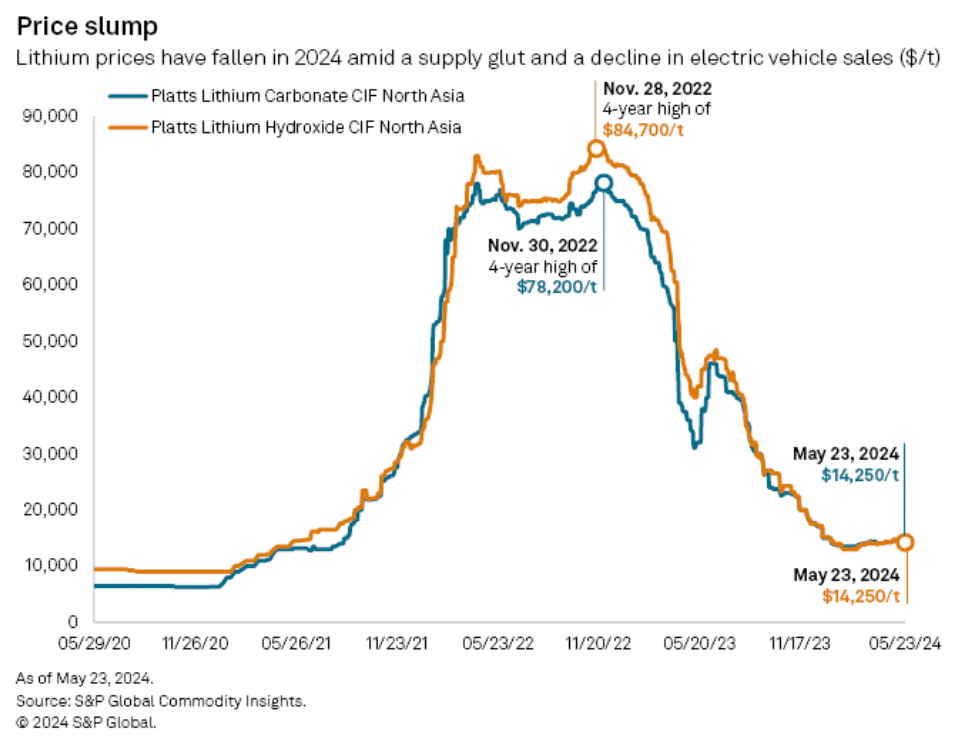

On May 23, Platts reported the lithium carbonate CIF North Asia price at $14,250 per metric ton, down 81.8% from the four-year high of $78,200/t on Nov. 30, 2022. The lithium hydroxide CIF North Asia price also fell 83.2% to $14,250/t from a peak of $84,700/t on Nov. 28, 2022.

Embracing Lithium Auctions for Better Pricing

Several lithium companies are now revisiting auctions, believing that price reporting agencies have overstated the price decline. Auctions have indeed yielded higher prices.

For instance, Albemarle’s two lithium spodumene auctions on March 26 and April 24 increased the spot spodumene price by about 10% each time. Encouraged by these results, Albemarle plans to continue with auctions.

In late March, Australia-based Mineral Resources Ltd. sold lithium spodumene concentrate at $1,300/t through digital auctions. This was 13%-20.4% higher than the Platts lithium spodumene 6% FOB Australia price of $1,080/t to $1,150/t during that period. The company aims to continue using auctions for price transparency.

Joshua Thurlow, CEO of Mineral Resources, highlighted the market’s recognition of future lithium demand for the global energy transition, noting delays or failures in long-awaited supply projects.

Similarly, Brazil-headquartered Sigma Lithium Corp. reported achieving higher prices through an “auction-price discovery process” compared to the traditional PRA approach.

These developments indicate that auctions are becoming a valuable tool for lithium producers to secure favorable prices and enhance market transparency. This is particularly crucial as demand for lithium, a critical element of EV batteries, will rise again amid the energy transition.

A Dynamic Pricing Approach for A Resilient Lithium Market

Lithium prices have experienced a dramatic fall and the market is still adjusting to inflated inventories from the boom period. There’s also a growing divergence between different lithium products as the supply chain matures.

Historically, long-term contracts have been linked to the downstream chemicals market rather than the raw material, spodumene, which has become significant only in the past decade. This has led to a disconnect between the prices of these two materials.

Ana Cabral, CEO of Sigma Lithium Corp., noted that lithium producers are gaining more control over pricing previously influenced by lithium chemicals. She emphasized the need for a risk-reward system aligned with the pricing mechanism, highlighting that those producing the raw concentrate bear most of the risk.

Lithium producers face not only explosive demand growth but also geopolitical and regulatory changes that could create regional market divisions. The West aims to reduce dependence on supply chains involving China, with increasing attention to the carbon footprints of various sources.

Chris Berry, president of House Mountain Partners LLC, likened the current lithium market evolution to that of the iron ore market. He noted that auctions and increasing liquidity in lithium futures are positive developments.

Regular, open spot pricing through bids and offers enables market participants to react swiftly to supply and demand changes, ensuring more efficient market clearing during both boom periods and downturns. This dynamic approach allows the market to adapt more effectively to fluctuating conditions.

Leading universities worldwide are at the forefront of driving innovation to combat climate change and achieve net zero goals. Institutions like Oxford, Cambridge, Imperial College London, the University of Edinburgh, and the University of Aberdeen are pioneering groundbreaking solutions in CCUS technologies, policy frameworks, and integration strategies in the United Kingdom.

Learn how these research initiatives are shaping the future of sustainable energy and environmental stewardship.

Oxford University’s Carbon Management Program

Launched in December 2022, theCarbon Management Program at the Oxford Institute for Energy Studies (OIES) focuses on the in-depth examination of business strategies aimed at implementing groundbreaking low-carbon technologies essential for transitioning to a net zero world. Specifically, these technologies include carbon capture, utilization, and storage (CCUS) as well as carbon dioxide removal (CDR) solutions, spanning both technological and natural approaches.

The program scrutinizes the role of carbon markets, encompassing both voluntary and regulatory compliance mechanisms, in stimulating investments towards these transformative technologies. The Program’s research activities focus on 3 key thematic areas:

Carbon Capture, Utilization and Storage (CCUS):

The research segment examines the feasibility of CCUS in various sectors like oil & gas, steel, cement, and waste-to-energy. It provides insights into the economic, policy, and regulatory aspects of CCUS adoption.

Additionally, it assesses different policy support methods like tax incentives and carbon pricing to promote CCUS deployment. Comparative analyses with alternative decarbonization solutions in sectors like steel production (e.g., hydrogen adoption) and renewables are also conducted.

Carbon Dioxide Removal (CDR):

COP27 emphasized the importance of taking CO2 out of the air to meet the climate goals outlined in the Paris Agreement. Research in this area looks into various ways to do this, known as Carbon Dioxide Removal (CDR) solutions, to help us transition to cleaner energy and reach those targets.

CDR methods cover a wide range of techniques, so this research zeroes in on the most promising ones like direct air capture (DAC), bioenergy with carbon capture and storage (BECCS), and biochar production. It also explores newer solutions to see how practical and scalable they are.

Carbon Markets:

The third research area of the Program focuses on integrating CCUS and CDR solutions into both voluntary and mandatory carbon markets. Specifically, it offers solutions to significant challenges that have slowed down the progress of CCUS and CDR in voluntary carbon markets and emissions trading systems.

These solutions address various issues, including the need for robust carbon accounting frameworks, methods to ensure the permanence of carbon removal and to manage the risk of leakage or reversal, and assessments of the types of claims companies can make by investing in these solutions.

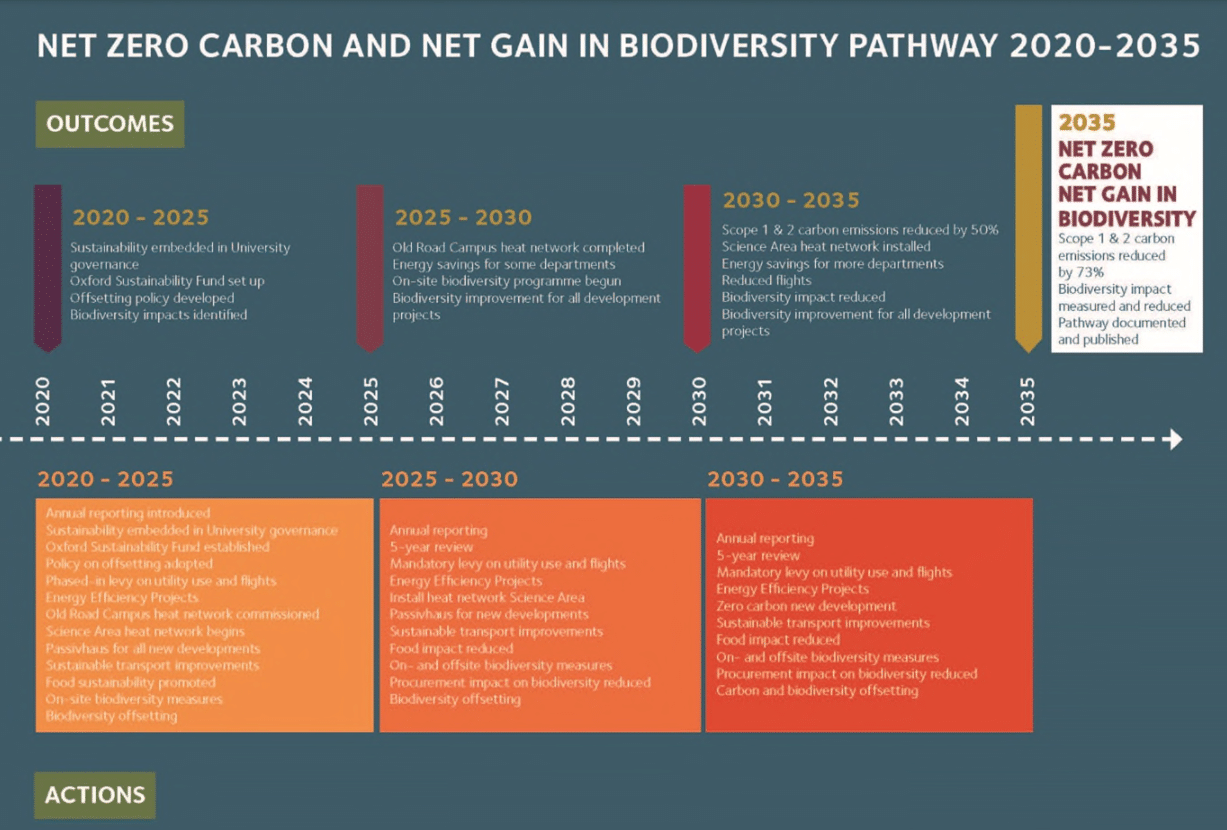

The University aims to achieve its own net zero carbon goal and biodiversity net gain by 2035, with the following pathway:

“Oxford Net Zero” Initiative

Oxford Net Zero is an interdisciplinary research effort drawing on 15 years of climate neutrality research at the University of Oxford. It is dedicated to monitoring progress, establishing standards, and guiding effective solutions across various fields including climate science, law, policy, economics, clean energy, transportation, land use, food systems, and CDR.

Essential climate change questions that Oxford Net Zero addresses include:

How will carbon dioxide be distributed between the atmosphere, oceans, biosphere and lithosphere?

Where will it be stored, in what forms, how stable will these storage pools be, who will own them and be responsible for maintaining them over the short medium and long terms?

How does net zero policy extend to other greenhouse gases?

How will the social license to generate, emit, capture, transport, and store carbon dioxide evolve over the coming century?

University of Cambridge Carbon Capture, Storage And Use Research

TheUniversity of Cambridge’s Carbon Capture, Storage, and Use (CCSU) research is part of the Energy Transitions@Cambridge initiative, an interdisciplinary research center dedicated to addressing current and future energy challenges. With over 250 academics from 30 departments and faculties, the initiative aims to develop solutions for energy transitions.

The CCSU research focuses on understanding and raising awareness of opportunities and risks associated with CCUS. Areas of focus include chemical looping of solid fuels to produce clean CO2, hydrogasification of coal to methane gas, reforming of methane to hydrogen, and seismological observations of active injection sites. On the use side, research covers manufacturing processes of CO2 andcarbonate mineralization.

By bringing together academics and external partners, the university’s research program aims to explore cutting-edge technology themes in carbon capture for large-scale decarbonization.

Cambridge Zero, the University’s ambitious new climate initiative, will generate ideas and innovations to help shape a sustainable future – and equip future generations of leaders with the skills to navigate the global challenges of the coming decades.

The University made history by becoming the first university to adopt a science-based target for emissions reduction, aiming to limit global warming to 1.5 degrees Celsius. It plans to cut greenhouse gas emissions tozero by 2038.

To achieve this, Cambridge is exploring the substitution of gas with alternative heat technologies on a large scale and is progressively transitioning to renewable sources for its power supply. Watch below to learn more about the university’s climate initiative.

University Of Edinburgh CCS Research

The University of Edinburgh’s School of Engineering hosts one of the UK’s largest carbon capture research groups, focusing on carbon dioxide capture through adsorption and membrane separations. This group is part of the Scottish Carbon Capture and Storage (SCCS) Centre, the UK’s largest CCS consortium, which includes over 75 researchers from the University of Edinburgh’s Schools of Geosciences, Engineering, and Chemistry, Heriot-Watt University, and the British Geological Survey.

The Adsorption & Membrane group at the University of Edinburgh specializes in:

Adsorbent Testing and Ranking: Using zero-length column systems to evaluate adsorbents for CO2 capture.

Membrane Testing: Assessing polymers for carbon capture membranes.

Dynamic Process Modelling: Simulating adsorption and membrane-based capture technologies.

Process Integration and Optimization: Enhancing efficiency of capture processes.

Circulating Fluidised Beds: Studying fluid dynamics for improved carbon capture.

Mixed-Matrix Membranes and Carbon Nanotubes: Developing advanced materials for capture applications.

This extensive expertise positions the University of Edinburgh as a leading institution in the research and development of carbon capture technologies.

Zero by 2040

The University has also committed to becoming zero carbon by 2040 as outlined in its Climate Strategy 2016. This strategy employs a comprehensive whole-institution approach to climate change mitigation and adaptation to achieve ambitious targets.

In alignment with the 2016 Paris Agreement, which aims to reduce global greenhouse gas emissions, the University is committed to supporting Scotland’s and the world’s transition to a low-carbon economy.

Key goals include reducing carbon emissions by 50% per £ million turnover from a 2007/08 baseline and achieving net zero carbon status by 2040. The University plans to achieve these objectives through initiatives in research, learning and teaching, operational changes, responsible investment, and exploring renewable energy opportunities.

Furthermore, the University will use its 5 campuses as “living laboratories” to experiment with and demonstrate innovative ideas that can be implemented elsewhere, fostering a culture of sustainability and practical application in the fight against climate change.

This year, the University is undertaking a major project to achieve carbon neutrality, which is considered the largest of its kind in the UK. This multimillion-pound initiative involves planting more than 2 million trees and restoring at least 855 hectares of peatlands. The project is a crucial part of the University’s goal of 2040 net zero.

Initial regeneration efforts will focus on a 431-hectare site overlooking the Ochil Hills in Stirlingshire and 26 hectares at Rullion Green in the Pentland Hills Regional Park near Edinburgh. Over the next 50 years, the project aims to remove 1 million tonnes of carbon dioxide from the atmosphere, equivalent to the emissions from over 9 million car journeys between Edinburgh and London.

Imperial College London – CCS Research Program

Imperial College’s carbon capture and sequestration (CCS) research program is the largest in the UK, involving over 30 professionals across various departments. They focus on engineering, industrial CCS, subsurface CO2 behavior, and legal and regulatory aspects. The university collaborates with the UK CCS Research Centre, CO2 GeoNet, and the European Energy Research Alliance.

The program has refurbished a pilot carbon capture plant to provide hands-on experience for students and professionals. Built to industry standards, it captures flue gas from a power station and supports research conducted by leading industrial organizations.

Imperial College London is also employing various means to directly curb its GHG emissions. The school’s long-term goal is to be a sustainable andnet zero carbon institution by 2040.

ICL’s Transition to Zero Pollution

The Transition to Zero Pollution initiative is structured around 5 focus themes, each addressing a significant challenge that demands exploration, innovation, and interdisciplinary collaboration:

TheUniversity of Aberdeen is at the forefront of carbon capture and utilization research, with experts developing processes and products that not only sequester emissions but also add economic value.

In 2017, the university’s patented CO2 capture and conversion technology led to the establishment of Carbon Capture Machine Ltd (CCM), which became a finalist in the NRG COSIA Carbon XPrize competition, offering a $20 million prize to the winner.

CCM’s technology involves dissolving CO2 flue gas into slightly alkaline water, which is then mixed with a brine source containing dissolved calcium and magnesium ions. This process generates Precipitated Calcium Carbonate (PCC) and Precipitated Magnesium Carbonate (PMC), both of which are nearly insoluble and have various industrial applications.

PCCs are used in industries such as papermaking, plastics, paints, adhesives, and in the development of cement and concrete.

Additionally, sodium chloride (NaCl) is extracted from the final products. These carbon conversion products are carbon negative and in high demand across multiple industries, offering companies opportunities to reduce emissions and create new revenue streams through carbon capture and utilization technology.

Aberdeen’s Net Zero Goal

Same with the other top universities, the University of Aberdeen aims to reachnet zero by 2040.As part of this climate commitment, the university became a member of the Global Climate Letter and the One Planet Pledge.

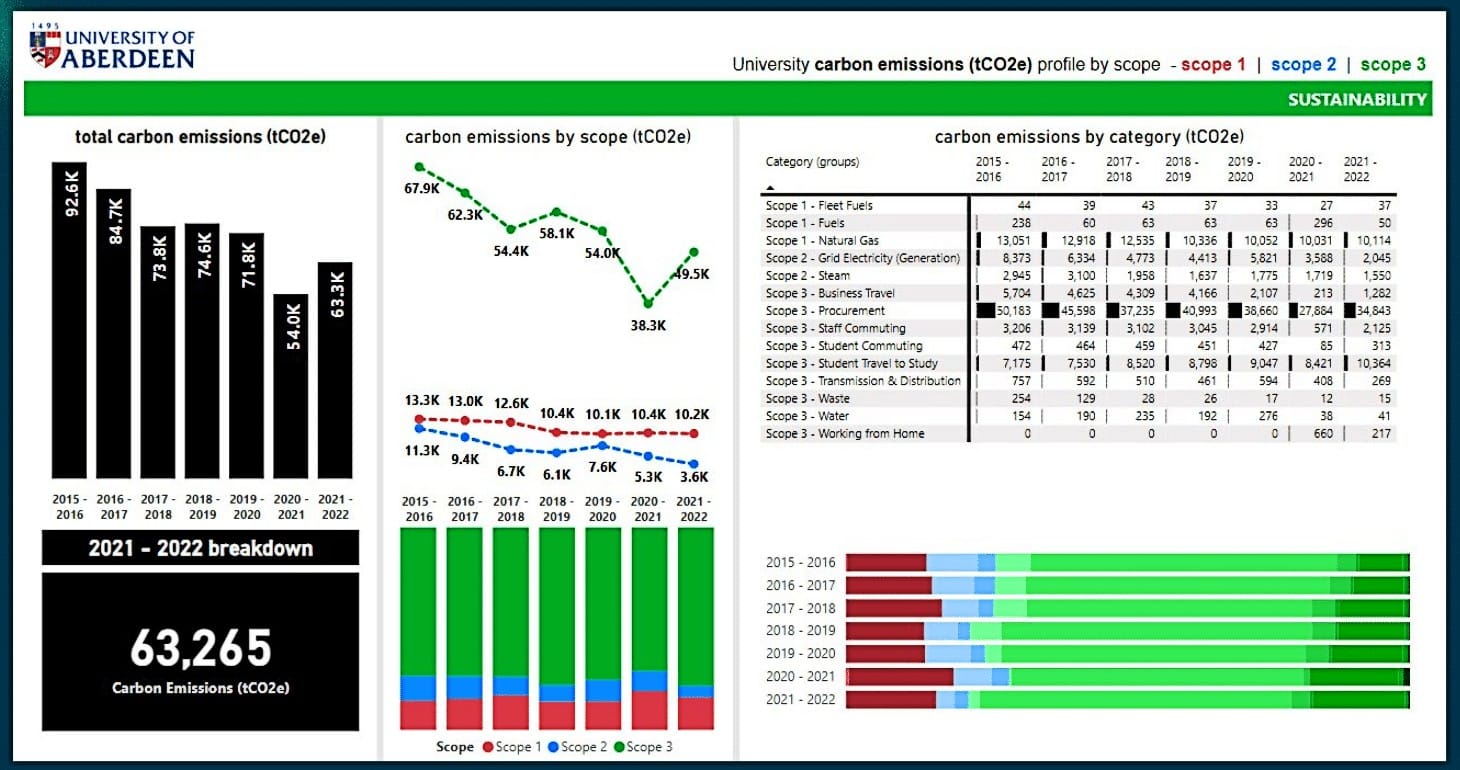

At a glance, here is the university’s carbon emissions, total and by scope, accessible through an online tool.

In addition to enhancing emissions reporting, the university is actively developing a comprehensive net zero strategy. This strategy includes setting targets and exploring pathways across various business functions to achieve carbon neutrality. The publication of this strategy will be available this year.

Conclusion

Leading universities in the UK are advancing carbon capture, utilization, and storage (CCUS) technologies, essential for achieving net zero goals. Oxford, Cambridge, Imperial College London, the University of Edinburgh, and the University of Aberdeen are driving research and implementation strategies that address the technical and economic challenges of CCUS.

Their interdisciplinary programs and climate initiatives integrate these solutions into broader carbon markets and regulatory systems. These universities’ efforts are crucial in transitioning to a sustainable energy future, demonstrating the critical role of academic institutions in global climate action. Through collaboration with industry and government, UK universities are setting the standard for climate action and paving the way for a net zero future.

The potential merger between BHP and Anglo American has been a significant topic in the mining industry, with the possibility of creating the largest base metal company globally. However, the merger has faced multiple rejections and challenges.

Here are the key points of the merger proposal:

Initial and Revised Proposals:

BHP initially proposed a $38.8 billion all-share offer to acquire Anglo American, which included plans to demerge Anglo American’s platinum and iron ore assets in South Africa.

The revised proposal increased the merger exchange ratio by 15%, offering Anglo American shareholders 16.6% ownership in the combined entity, up from 14.8% in the initial proposal.

Rejections and Concerns:

Anglo American’s board has consistently rejected BHP’s proposals, citing that they significantly undervalue the company and involve a highly complex structure with significant execution risks.

The structure requires Anglo American to demerge its holdings in Anglo American Platinum and Kumba Iron Ore, which the board finds unattractive and risky for its shareholders.

Focus on Copper:

Both companies are heavily focused on copper due to its crucial role in the energy transition, with BHP aiming to become the world’s largest copper producer through this merger.

The combined entity would control significant copper assets, including major mines in South America, enhancing BHP’s position in the copper market.

The merger faces potential regulatory scrutiny, particularly concerning market concentration in the copper sector and the impact on South African operations. BHP has proposed several socioeconomic measures to address these concerns, including maintaining employment levels and supporting local procurement in South Africa.

Ultimately, BHP has pulled its bid as of May 29th. With or without the deal, each mining giant has been figuring hard how to deal with their carbon emissions.

BHP’s Carbon Crusade and Net Zero Ambitions

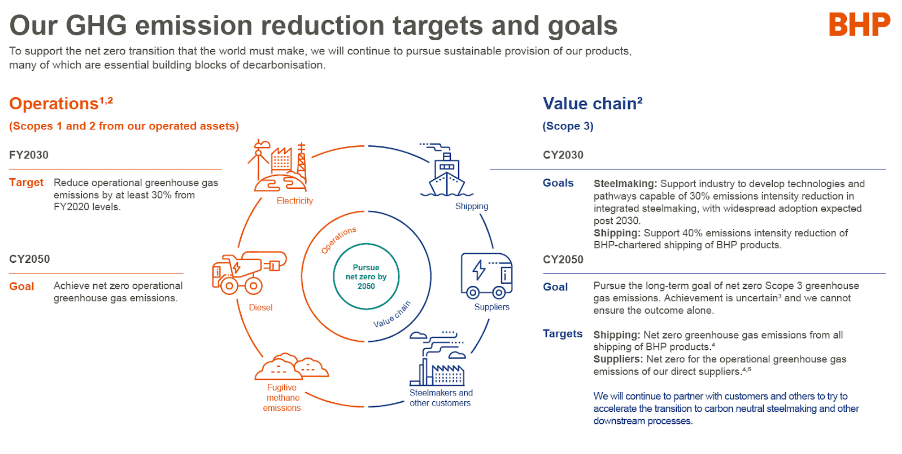

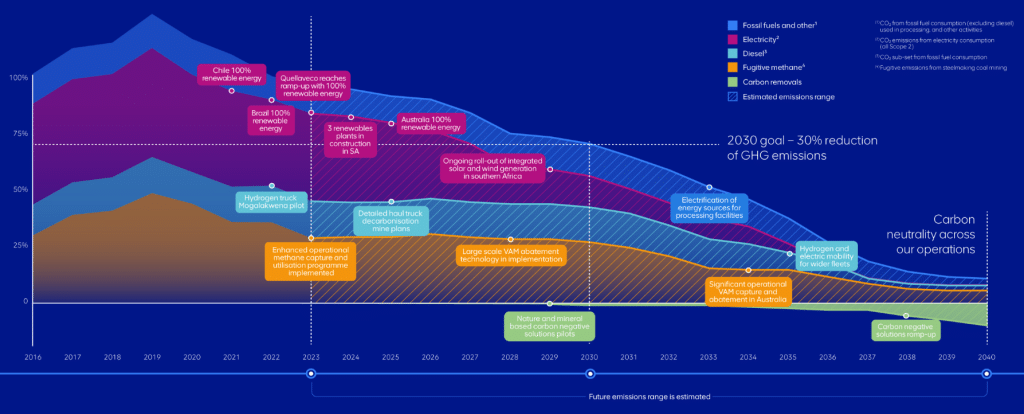

BHP has committed to achieving net zero operational (Scope 1 and 2) emissions by 2050. Their medium-term target is a 30% reduction from adjusted FY2020 levels by FY2030, involving an investment of around $4 billion. Key initiatives include transitioning from diesel to battery-powered haul trucks, which are more efficient, and investing in renewable energy sources to power their operations, especially in Western Australia and Chile.

While BHP prioritizes internal GHG emission reduction, they recognize the temporary role of high-integrity carbon credits. The mining titan doesn’t plan to use carbon credits for operational GHG emission reduction medium-term targets. However, if abatement projects do not achieve the expected GHG reductions, BHP retains the flexibility to use high-integrity carbon credits toward their 2030 climate targets.

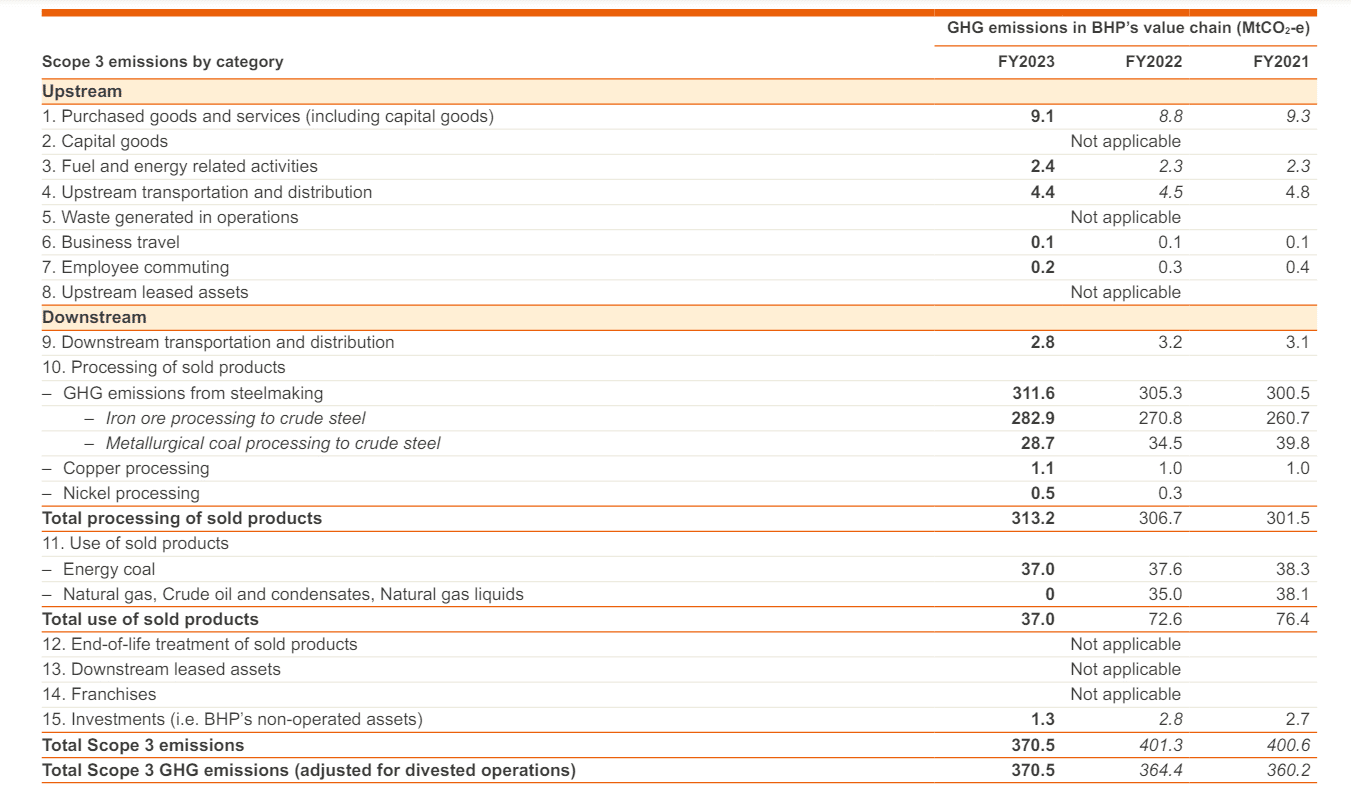

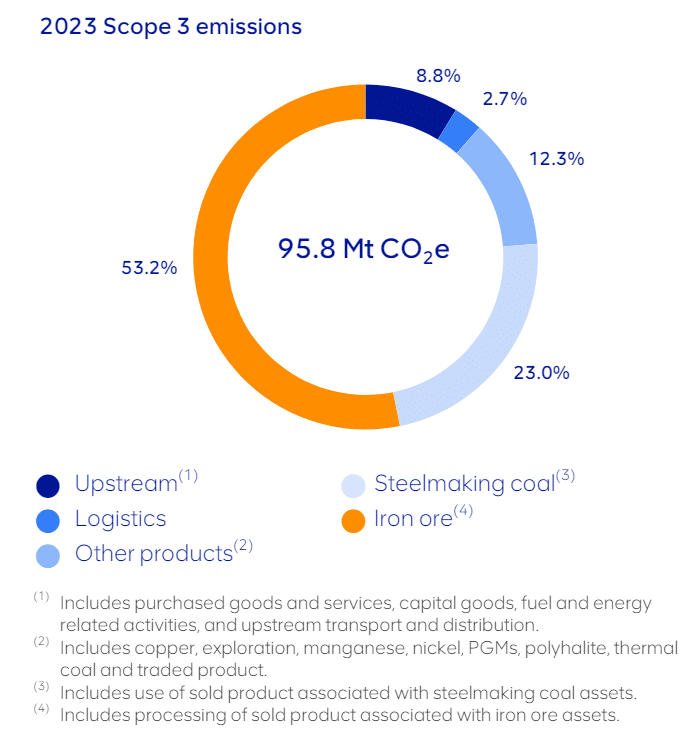

BHP’s Scope 3 emissions, which account for 97% of their total emissions, are predominantly from the use of their products by customers. While BHP aims to achieve net zero Scope 3 emissions by 2050, this remains an aspirational goal rather than a strict target.

They are focusing on developing low-carbon technologies in collaboration with the steelmaking industry, such as hydrogen-based Direct Reduced Iron (DRI) plants. BHP also supports carbon capture and storage (CCS) technologies, although these have faced criticisms for their limited effectiveness and low capture rates.

BHP Carbon Emissions:

Scope 1 emissions (direct emissions from operations) in FY2023: 7.5 million tonnes CO2e

Scope 2 emissions (indirect emissions from purchased electricity/energy) in FY2023: 5.0 million tonnes CO2e

Scope 3 emissions (indirect emissions from value chain) in FY2023: 95.8 million tonnes CO2e

Anglo American’s Eco Revolution: Slashing Emissions in Style

Anglo American aims to achieve carbon neutrality across its operations by 2040. Interim targets include reducing these emissions by 30% by 2030. Their FutureSmart Mining™ program is central to this effort, leveraging technology and digitalization to enhance sustainability.

Notable initiatives include securing 100% renewable electricity for operations in Brazil, Chile, and Peru, and developing hydrogen fuel cell and battery hybrid trucks, which are set to replace diesel trucks across their global fleet from 2024.

Anglo American has set an ambitious target to reduce Scope 3 emissions by 50% by 2040. This will be achieved by working with customers and technology partners to decarbonize the steel industry and by making changes in their product portfolio.

Anglo American Scope 3 emissions

They are also focused on improving efficiencies and controlling emissions within their supply chain and logistics, particularly in shipping.

Anglo American carbon emissions:

Scope 1 emissions in 2023: 7.5 million tonnes CO2e

Scope 2 emissions in 2023: 5.0 million tonnes CO2e

Scope 3 emissions in 2023: 95.8 million tonnes CO2e

The British mining giant is making significant progress in reducing emissions from Scope 3 sources. Processing iron ore remains the largest contributor, with steelmaking accounting for 50.9 Mt CO2e, or 47% of total emissions in 2023. The emissions intensity of the company’s iron ore has decreased by 5% in 2023 compared to the 2020 baseline.

Anglo American plans to reduce its Scope 3 emissions by prioritizing 7 initiatives over four themes, as specified in its Climate Change Report 2023.

Cutting-Edge Clean Energy and Decarbonization Projects

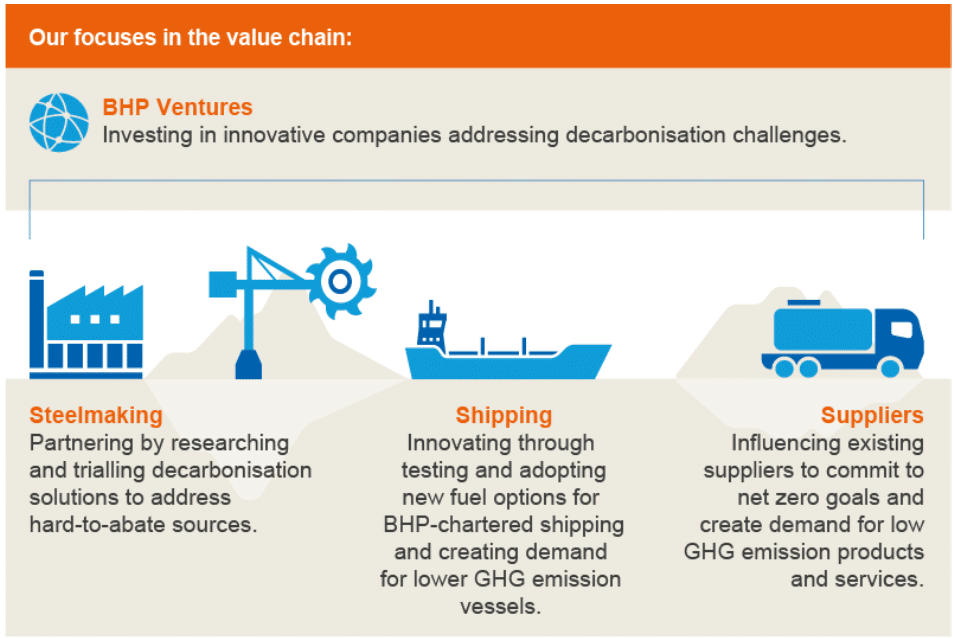

BHP is investing in several clean energy and decarbonization projects. They are trialing “dynamic charging” for electric haul trucks, allowing them to be charged while in operation. In addition, they are developing carbon capture projects with steelmakers and exploring various renewable energy projects to power their operations.

Despite these efforts, BHP has acknowledged that short-term emissions may increase due to production growth before significant reductions are realized.

Similarly, Anglo American is actively engaging in clean energy projects as part of their decarbonization strategy. Their partnership with EDF Renewables aims to ensure that all electricity used by 2030 will come from zero-emission sources.

They have already achieved a 100% renewable electricity supply for their operations in several countries and are developing hydrogen-powered haul trucks to replace diesel ones. These initiatives are expected to significantly reduce their carbon footprint and contribute to their net zero goals.

The potential merger between BHP and Anglo American may have faced significant challenges, but both companies remain steadfast in their commitment to reducing carbon emissions and advancing towards net zero goals. Both miners are leveraging technology and strategic partnerships to drive their decarbonization efforts.

Xpansiv voluntary carbon credit trading data saw a significant divergence in prices for nature-based and technology-based carbon credits. The report is from Xpansiv Data and Analytics, which offers a comprehensive database of spot firm and indicative bids, offers, and transaction data.

Xpansiv delivers extensive market data from CBL, the world’s largest spot environmental commodity exchange. It provides daily and historical data on bids, offers, and transactions for carbon credits, compliance and voluntary renewable energy certificates, and Australian Carbon Credit Units (ACCUs) traded on the CBL platform.

The exchange recently secured a major capital raise from Aramco Ventures to further enhance its environmental markets infrastructure solutions.

The spot data is further enhanced by forward carbon prices from top market intermediaries, along with aggregated registry statistics and ratings from leading providers.

Nature-Based Credits Surge While Energy Sector Prices Drop

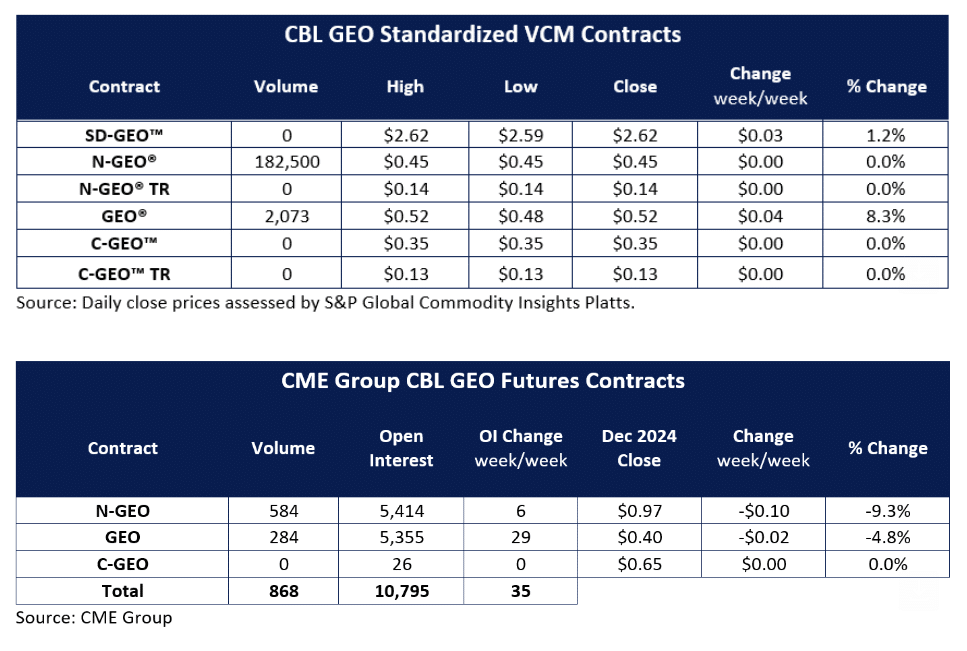

Last week saw large blocks of Verified Carbon Standard (VCS) Nature Group Eligibility (N-GEO)-eligible and Climate Action Reserve (CAR) nature credits driving the 20-day moving average of recent-vintage AFOLU (Agriculture, Forestry, and Other Land Use) credits to $12.05, a 125% week-over-week increase. Conversely, a significant block of Asian renewable credits pushed the energy sector average price down by 60% to $0.76.

These blocks accounted for most of the 316,124 metric tons traded on CBL last week. This is composed of 224,730 nature credits and 91,394 energy credits. CME Group’s emissions futures also reflected this trend, trading 584,000 tons through CBL N-GEO and 284,000 via CBL GEO futures contracts.

Specific credit trades on CBL included vintage 2019:

VCS 1477 Katingan credits at $6.00,

ACR 556 industrial process credits at $2.85,

ACR 658 credits at $2.30, and

Vintage 2020 VCS 1753 Indian solar credits at $1.25.

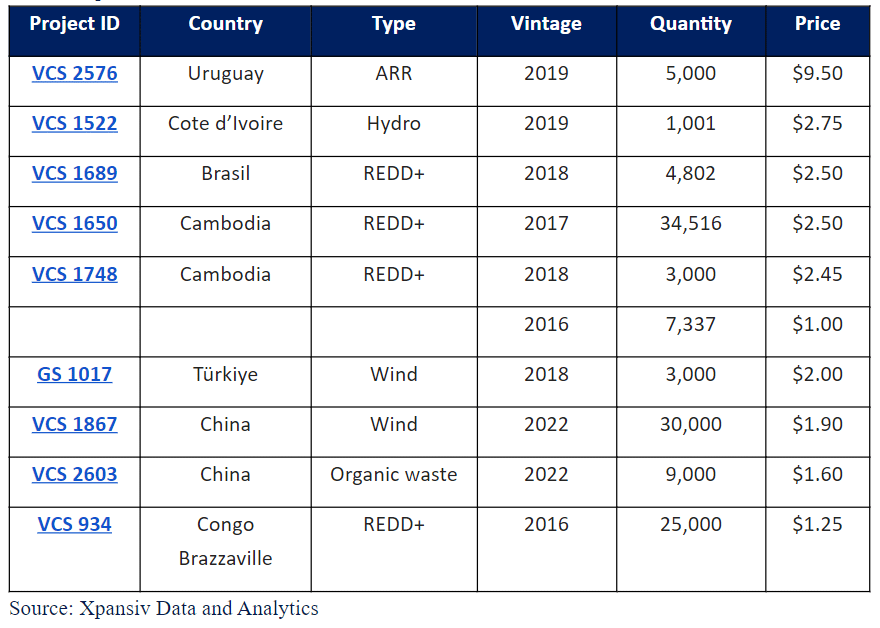

Who Leads the CBL REC Markets?

Last week, a $9.50 offer for 5,000 tons of vintage 2019 VCS Afforestation, Reforestation, and Revegetation (ARR) credits from Uruguay was reposted. New and renewed offers for VCS and Gold Standard renewable energy and REDD+ (Reducing Emissions from Deforestation and Forest Degradation) credits ranged between $1.00 and $2.75.

Project-Specific Credit Offers on CBL

REC trading activity on CBL was light but included larger blocks of bilaterally traded PJM credits settled via the exchange, along with smaller PJM and NEPOOL trades matched on screen.

Virginia Credits: 2024 Virginia credits traded at $0.25, closing the week at $35.25.

New Jersey Solar Credits: Over 1,400 2023 New Jersey solar credits were matched at $207.50, $1.50 higher than the previous week’s close, with an additional 1,500 credits cleared via reported trade.

New Jersey Class 2 Credits: 355 vintage 2024 RECs were matched at $37.50.

NEPOOL Credits: 189 Massachusetts Class 2 non-waste credits were matched at $31.50.

In related news, the White House released new voluntary carbon credit guidelines to promote high-integrity emissions reductions and support nature-based projects and carbon removal technologies.

Xpansiv’s data highlights a stark contrast in the carbon credit market: with nature-based credits experiencing a significant price surge while energy sector credits see a sharp decline. This divergence underscores the growing demand for high-integrity, nature-based solutions in the voluntary carbon market.

As companies strive to meet their net zero targets, understanding these market dynamics will be crucial for making informed investment and sustainability decisions.

Ørsted has announced a significant expansion of its partnership with Microsoft, agreeing to sell an additional 1 MT of carbon removal over 10 years from the Avedøre Power Station. This is part of the bioenergy carbon capture and storage (BECCS) initiative known as the ‘Ørsted Kalundborg CO2 Hub’. This new deal builds on Microsoft’s existing commitment to purchase 2.67 million tonnes of CO2 from the Asnæs Power Station, bringing their total contracted carbon removal to 3.67 MTs.

The Key Highlights of the Ørsted-Microsoft Deal

1. Carbon Capture Implementation

As part of the ‘Ørsted Kalundborg CO2 Hub’, Ørsted will install carbon capture technology at the wood chip-fired Asnæs Power Station in Kalundborg, western Zealand, and the straw-fired boiler at Avedøre Power Station in Greater Copenhagen. The combined heat and power plants will capture 430,000 tonnes of biogenic CO2 annually, which will then be transported to a storage reservoir in the Norwegian North Sea for permanent storage. The hub is expected to be operational by early 2026.

2. Microsoft’s Carbon Removal Commitment

Starting in 2026, Microsoft will receive one million tons of carbon removal from the straw-fired unit at Avedøre Power Station. This plant uses locally sourced straw, an agricultural by-product, to generate electricity and district heating. By capturing and storing biogenic carbon from these biomass-fired plants, the process not only reduces CO2 emissions but also removes carbon from the atmosphere, creating negative emissions. This is because biogenic carbon from sustainable biomass is part of a natural cycle.

3. Supporting Sustainable Development

The collaboration between Ørsted and Microsoft is crucial for advancing the ‘Ørsted Kalundborg CO2 Hub’, especially since bioenergy-based carbon capture and storage technology is still emerging. The project, which received a subsidy from the Danish Energy Agency, included anticipated revenue from carbon removal certificates in its investment decision. This competitive pricing was a key factor in the subsidy award.

4. Importance of BECCS for Climate Goals

The UN’s Intergovernmental Panel on Climate Change (IPCC) has highlighted the importance of carbon removal technologies like BECCS for limiting global warming. Projects such as the ‘Ørsted Kalundborg CO2 Hub’ are essential for helping companies like Microsoft achieve their sustainability targets and contribute to global climate goals.

Is Microsoft Leading the Charge Toward a Carbon-Neutral Future?

Decoding its carbon emissions and net-zero plans

In 2023, Microsoft expanded its renewable energy assets to over 19.8 gigawatts (GW), incorporating projects across 21 countries. Additionally, last year the company secured contracts for 5,015,019 MTs of carbon removal to be retired over the next 15 years. Its net-zero plans focus on three primary areas:

Reducing carbon emissions

Increasing the use of carbon-free electricity

Removing carbon

The company’s latest ESG report suggests that the pathway to becoming carbon-negative has the following milestones:

Reducing Scope 1 and Scope 2 Emissions

Microsoft aims to nearly eliminate its Scope 1 and 2 emissions by increasing energy efficiency, decarbonizing its operations, and achieving 100% renewable energy by 2025. It achieved a 6% reduction in its Scope 1 and 2 emissions from the 2020 base year by advancing clean energy procurement, implementing green tariff programs, and using unbundled renewable energy certificates

Reducing Scope 3 Emissions

Microsoft’s Scope 3 emissions account for more than 96% of its total emissions. Most of these emissions come from purchased goods and services, capital goods, downstream, and the use of sold products downstream. By 2030, Microsoft aims to cut its Scope 3 emissions by 50% from the 2020 baseline.

Although Scope 3 emissions have surged by 30.9% since 2020, Microsoft remains committed to expanding clean energy purchases across its supply chain. It aims to invest in the decarbonization of hard-to-abate industries like steel, concrete, and other materials used in its data centers.

Tracking progress toward carbon negative by 2030

Microsoft’s overall emissions increased by 29.1% in FY23 from the base year. Additionally, it retired 605,354 MTs of carbon removal as part of its net zero goals.

Can Ørsted’s Bold Strategies Propel U.S. to a Carbon-Free Future? Find Out…

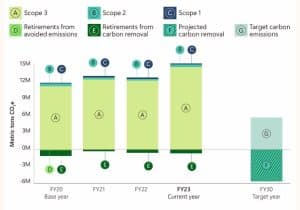

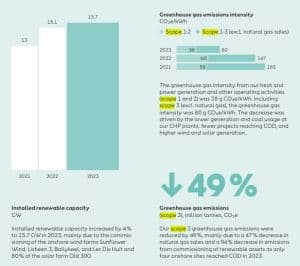

Ørsted has committed to achieving net-zero emissions across its value chain by 2040, aiming to reduce emissions through various initiatives, including renewable energy projects, energy efficiency measures, and engaging stakeholders in sustainable practices.

The company reports its greenhouse gas emissions under three categories: Scope 1, Scope 2, and Scope 3, as defined by the Greenhouse Gas (GHG) Protocol.

ReducingScope 1 and Scope 2 Emissions

Ørsted significantly reduced its Scope 1 emissions by transitioning from fossil fuels to renewable energy sources like wind and biomass. For Scope 2 emissions, Ørsted focused on increasing energy efficiency and sourcing renewable energy to reduce the emissions from purchased electricity and heat.

Scope 1 and 2 emissions: FY2023 was 38g CO2e/kWh

Reducing Scope 3 Emissions

To address Scope 3 emissions, Ørsted engages with suppliers, optimizes logistics, and promotes sustainable practices across its value chain, targeting emissions from fuel production and transportation, manufacturing of wind turbine components, business travel, and the use of sold products.

Scope 3 emissions: FY2023 was 80g CO2e/kW

The image depicting Ørsted’s installed renewable capacity and GHG emissions intensity

source: Ørsted

Key sustainability targets

Scope 1-2 emissions intensity: 98 % reduction by 2025 and 99 % reduction by 2030 (from 2006)

Scope 1-3 emissions intensity (excl. natural gas sales): 77 % reduction by 2030, and 99 % reduction by 2040 (from 2018)

Scope 3 emissions (from natural gas sales): 67 % reduction by 2030, and 90 % reduction by 2040 (from 2018)

Top Clean Energy and Decarbonization Projects

Microsoft:

The company invests in renewable energy sources such as wind, solar, and hydroelectric power, and implements energy efficiency measures across its operations. Like its partnership with Ørsted, and other CDR projects alike to offset emissions and remove CO2 from the atmosphere. Through these efforts, Microsoft aims to become carbon-negative by 2030, addressing both its direct emissions and those across its entire value chain.

Some remarkable decarbonization achievements of Microsoft include:

Ørsted is leading the way in clean energy and decarbonization. It is transitioning from fossil fuels to renewable energy sources such as wind, solar, and biomass. The company majorly focuses on:

Large-scale offshore wind farms

Onshore wind energy

Bioenergy carbon capture and storage projects.

Solar power and grid stabilization

These initiatives aim to reduce and remove CO2 emissions, contributing to Ørsted’s goal of achieving net-zero emissions across its value chain by 2040. Thus, Ørsted is making significant strides in combating climate change and promoting sustainable energy solutions through these projects.

Ørsted’s Global Footprint

source: Ørsted

Notably, Ole Thomsen, Senior Vice President and Head of Ørsted’s Bioenergy business has commented:

“This expanded collaboration with Microsoft is a testament to our shared vision for a sustainable future. By combining Ørsted’s expertise in bioenergy carbon capture and storage with Microsoft’s commitment to reducing its carbon footprint, we’re showcasing how strategic relations can accelerate the transition to a greener economy.”

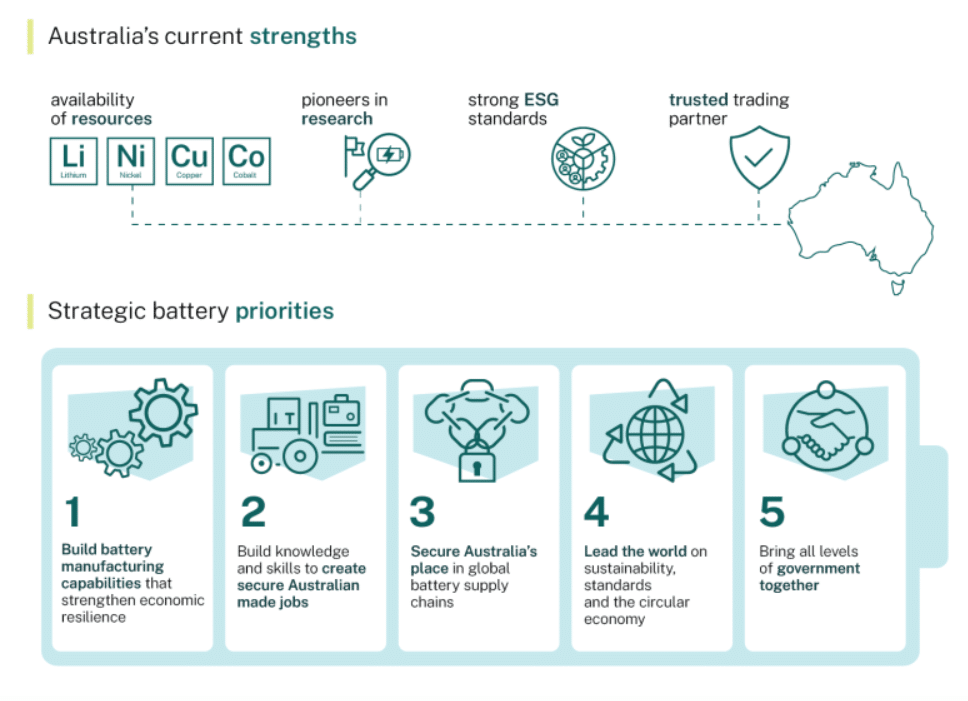

The Australian government unveiled the country’s first National Battery Strategy, detailing plans to establish a domestic battery industry. The strategy aims to develop processing capacity for upgrading raw minerals into processed battery components. This will enable Australia to supply battery-active materials globally, as stated by Prime Minister Anthony Albanese’s government.

Key elements of the strategy include building energy storage systems to bolster renewable power generation in the national grid and leveraging industry expertise to develop safer, more secure batteries for grid connection. Additionally, Australia plans to create batteries for its transport manufacturing sector, including heavy vehicle production.

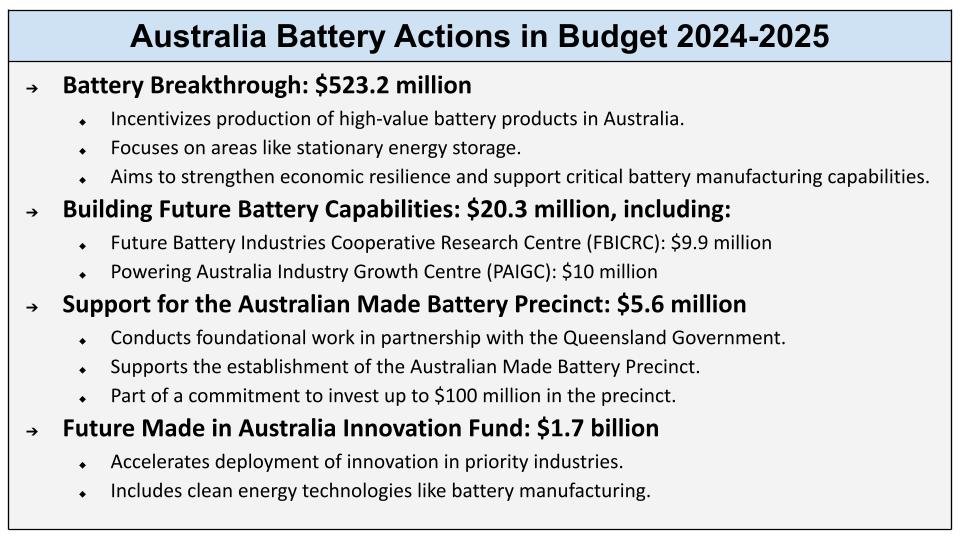

Federal Budget Boosts Battery Breakthrough

The strategy is funded by Australia’s 2024–2025 federal budget, which allocates A$523.2 million for the Battery Breakthrough Initiative. The initiative offers production incentives to enhance battery manufacturing capabilities. Furthermore, the Building Future Battery Capabilities plan provides A$20.3 million to support battery research.

Prime Minister Albanese emphasized the importance of this initiative, saying that:

“We want to make more things here and with global demand for batteries set to quadruple by 2030, Australia must be a player in this field. Batteries are a critical ingredient in Australia’s clean energy mix. Together with renewable energy, green hydrogen, and critical minerals, we will meet Australia’s emission reduction targets and create a strong clean energy manufacturing industry.”

Australia aims to transition its electricity grid to 82% renewable energy by 2030, supporting the country’s commitment to reduce emissions by 43% within the same period.

The federal government has also announced an A$7 billion tax incentive for critical mineral producers. It aimed at bolstering domestic supply chains for raw materials essential to the energy transition.

Unveiled as part of the 2024–2025 federal budget, the Critical Minerals Production Tax Incentive will cover 10% of relevant processing and refining costs for 31 critical minerals. This incentive will apply to minerals processed and refined between 2027-2028 and 2039-2040, extending up to 10 years per project.

Future Made in Australia: Jobs, Innovation, and Sustainability

This initiative is a key component of the government’s A$22.7 billion Future Made in Australia package. It is designed to create jobs and strengthen the economy while striving for net zero greenhouse gas emissions by 2050. The government sees it crucial in helping the country meet its 82% renewable energy target and cement its position in global battery supply chains.

Prime Minister Albanese and Treasurer Chalmers highlighted that the plan aims to maximize economic and industrial benefits from the global shift to net zero, securing Australia’s position in the evolving economic and strategic landscape.

Additionally, the government will allocate A$14.3 million to enhance trade competitiveness in critical minerals and A$10.2 million for prefeasibility studies of common-use infrastructure to support the sector.

Australia’s critical minerals list includes lithium, nickel, cobalt, vanadium, graphite, and rare earths.

The country is a leading global producer of lithium, iron ore, and bauxite, and boasts the largest reserves of lithium, iron ore, zinc, and vanadium, according to S&P Global Market Intelligence and federal government data.

The Prime Minister emphasized the need for Australia to enhance its competitiveness in the global metals and battery investments market, particularly in response to the US Inflation Reduction Act and other international incentives promoting domestic supply chains.

Albanese noted that “Australia cannot compete dollar-for-dollar with the US Inflation Reduction Act, but this is a competition, not an auction.” He acknowledged the global competition, noting initiatives in the US, EU, Japan, Korea, and Canada aimed at strengthening their industrial and manufacturing bases.

Below is the country’s battery actions identified in the federal budget 2024-2025. Amounts are in Australian dollars.

Industry Praise and Economic Resilience

The Association of Mining and Exploration Companies (AMEC), which includes over 500 members such as Fortescue Ltd. and Albemarle Lithium Pty. Ltd., praised the tax incentive.

AMEC’s chief executive, Warren Pearce, stated that the incentive would spur new projects and industries, driving economic growth and job creation, while maintaining Australia’s high standard of living. He emphasized that this proven mechanism would reward those taking risks in new and costly industries, promising significant returns on investment.

AMEC advocates for a 10% federal production tax credit for downstream materials producers to mitigate Australia’s production cost disadvantages compared to countries like the US. Pearce believes the proposed legislation could be a “game-changer” for clean manufacturing and critical minerals investment.

Amanda McKenzie, CEO of the Climate Council, also expressed support. She remarked that the legislation could catalyze immediate investments in clean energy sectors.

Indeed, Australia’s National Battery Strategy marks a significant step toward a sustainable energy future, backed by substantial federal investment. By enhancing battery production and innovation, the strategy aims to strengthen the nation’s position in the global market, create jobs, and support the transition to renewable energy.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy policy

source: Stock analysis

source: Stock analysis source: Stock Analysis

source: Stock Analysis

")

Specific credit trades on CBL included vintage 2019:

Specific credit trades on CBL included vintage 2019:

source:

source:  source:

source: