Verra, a leading non-profit VCM registry in the US has recently released its Verified Carbon Standard (VCS) modular methodology VM0049 for carbon capture and storage (CCS). Carbon dioxide removals play a crucial role in corporate net-zero strategies. Thus, VM0049 is a global framework for tech-based CCS activities that generate carbon dioxide removals (CDRs) and emission reductions.

Unlocking the Future of Carbon Capture: VM0049’s Modular Approach

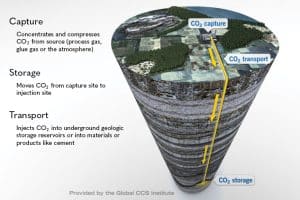

CCS involves CO2 capture directly from the atmosphere or from high-emission industrial sources. It is then transported or permanently stored underground. CCS is a highly efficient technique to combat CO2 emissions in tough sectors like industrial manufacturing (e.g., cement), oil and natural gas, and power generation.

VM0049 underscores the key requirements essential for CCS projects. Verra’s press release describes that these projects can choose from various modules for CO2 capture, transport, and storage activities to quantify their CDRs and emission reductions. Furthermore, the modules are customizable to fit a project’s design and technological needs. The unique modular format adapts to project expansions, shared infrastructure development, and future innovations.

Verra is set to launch the initial modules in the upcoming months, encompassing the following activities:

Direct air capture

CO2 transportation

CO2 storage in saline aquifers and depleted oil and gas reservoirs

At present, multiple additional modules are under development to encompass a wide range of activities supported by VM0049.

Image: An overview of Verra’s CCS and Transport Model

Pre-requisites for Carbon Capture from Ambient Air

This module governs projects that capture CO2 from ambient air using the latest VM00XX Methodology for Carbon Capture and Storage. Verra’s draft highlights that these projects must meet the following conditions:

Capture activities must extract atmospheric CO2, potentially alongside CO2 from on-site point sources such as oxy-fuel combustion. Methods may include chemical or physical absorption/adsorption with solvents or sorbents (e.g., amines), membrane processes, electrochemical processes, or cryogenic processes.

The primary capture fluid or media must be regenerated to prevent one-time use. It should yield a concentrated CO2 stream available for subsequent transport and storage.

Capture facilities must either be new, expand existing ones, or refurbish those that would otherwise be decommissioned at the project’s start.

Both existing and new capture facilities can share auxiliary equipment like utilities.

Notably, this framework ensures that CO2 capture from ambient air meets rigorous standards, facilitating effective carbon storage and utilization. The draft is yet to be finalized.

The methodology is evolving in stages using a modular approach. The initial phase will emphasize storing carbon in saline aquifers and depleted oil and natural gas reservoirs. Later phases will focus on using captured carbon, storing it, and carbon mineralization in geological formations. Each type of GCS project (CCS, GCM, or CCUS) will have specific requirements. Verra has outlined all the rules applicable to GCS projects under the VCS Program.

Verra examines two approaches to managing risks in GCS projects. Regulatory measures establish eligibility criteria, operational requirements, and closure obligations outlined in the VCS Standard and GCS Requirements. The Geologic Carbon Storage Non-Permanence Risk Tool assesses project risks. It allocates funds to the GCS pooled buffer account to protect the validity of all issued Verified Carbon Units (VCUs) from possible reversals.

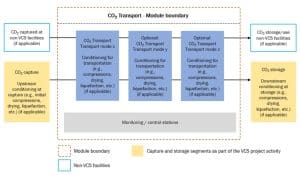

CO2 Transport Module Boundary

The CO2 transport module covers all processes in the CO2 transport value chain. Key processes include CO2 conditioning (like dehydration and cooling), compression, and loading/unloading from ships, trains, and trucks. It also provides for the propulsion of these transport modes, maintaining CO2 conditions in pressure vessels, and reconditioning CO2 for different transport modes or delivery conditions.

Verra signifies defining module and segment boundaries crucial for projects with diverse ownership. For now, the activities are divided into intermediate storage sites and transport segments within the transport module. Intermediate storage sites handle temporary CO2 storage during transfer, while transport segments involve equipment and processes for moving CO2 through a consistent transportation system. All documents are currently in their draft stage.

Figure: Verra’s Module boundary for CO2 transport (for public consultation)

source: Verra

Overall, Verra’s framework supports various capture, transport, and storage technologies. They ensure real, additional, and high-integrity emission reductions and removals (ERRs) globally. Deploying CCS and engineered CDR technologies is crucial to limit global warming to 1.5℃. These technologies complement emission reduction efforts, offset residual emissions, and provide a net negative CO2 option.

H&M (Hennes & Mauritz) Group is partnering with Rondo Energy to explore heat storage technologies to decarbonize its textile supply chain. The global fashion retailer, a sensation among all age groups for its chic, street style, and edgy designs, believes in sustainability. They are committed to making fashion and design eco-friendly. Will this partnership help H&M take bigger strides to achieve net zero?

Let’s discover how this partnership can transform their textile operations.

The Partnership is Weaving Sustainability into Style!

According to the press release rolled out on June 19, H&M is joining Rondo’s Strategic Investor Advisory Board (SIAB). The former would invest to support the expansion of Rondo’s operations and storage projects. Furthermore, the collaboration aims to replace fossil fuels with Rondo’s Heat Batteries. These energy-efficient batteries can transform renewable electricity into continuous, high-temperature heat and power essential for large-scale textile production.

In May, Rondo and SCG Cleanergy launched Southeast Asia’s first heat battery and the world’s first heat battery for a cement plant. They have established large-scale production in Thailand and plan to scale up to 90 GWh annually.

Notably, Southeast Asia is a global textile industry hub, where companies like H&M Group strive to impact people, economies, and our planet positively. Rondo, with its growing presence and expertise in the region, is well-positioned to support H&M Group’s efforts.

Eric Trusiewicz, CEO of Rondo Energy, said

“Rondo is thrilled to be working in partnership with H&M Group to explore how our technology can be of use in their supply chain, and to have H&M as an investor and member of our Strategic Investor Advisory Board.”

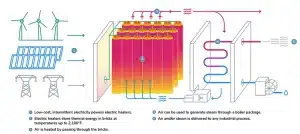

Rondo’s Heat Battery- the “Brave Little Toaster” Revolutionizing Textile Decarbonization

The Rondo Heat Battery is described as a “brave little toaster”. Essentially the battery is a pile of bricks with insane power to decarbonize the expansive textile sector. It is an innovative fusion of age-old techniques and modern automation to convert renewable energy into power. This approach can drastically reduce the carbon footprint of fabric production by offering a clean alternative to fossil fuels. H&M Group’s involvement in Rondo’s advisory board aligns them with other global titans like Rio Tinto, Aramco Ventures, SABIC, SCG, TITAN, and SEEIT, committed to low-cost, zero-carbon energy solutions.

Here’s the image of the battery:

source: Rondo Energy

Can this Innovative Battery Slash Global CO2 Emissions by 15%?

The answer is yes! Rondo Energy, the California-based renewable energy semiconductor manufacturing firm claims to eliminate 15% of global CO2 emissions in the next 15 years. The Rondo Heat Battery offers the lowest-cost energy storage and reduces energy price volatility. It provides 24/7 zero-carbon heat and eliminates scope 1 and 2 emissions. The battery ensures sustainability by nullifying NOx, SOx, and other particulate matter.

Additionally, its modular and scalable design allows easy integration as a drop-in replacement. The battery has proven highly profitable for consumers.

John O’Donnell, Founder & Chief Innovation Officer of Rondo Energy has further made an assertive statement, noting:

“Producing and finishing fabrics requires large amounts of low-cost energy, which makes our brick batteries a perfect fit. Today, coal delivers most of the heat and most of the carbon pollution making fabrics, because it’s always been cheap and simple to burn. But the world is changing. Region by region around the world, wind and solar power are becoming cheaper than fossil fuels. At Rondo, we’ve created a simple, practical tool to harness these new energy sources.”

H&M, Designing its Sustainable Path to Net Zero

Laura Coppen, Sustainability Investments at H&M Group Ventures has expressed her thoughts on this deal. She said,

“Rondo is H&M Group Venure’s first investment in decarbonization technology. The company’s thermal battery energy storage has the potential to help factories electrify, which is key to achieving our climate targets. We look forward to working closely with Rondo and the broader ecosystem in scaling decarb tech.”

The fashion industry faces challenges in decarbonization due to its reliance on low-cost energy. Currently, clothing production contributes approximately 5% of global GHG emissions, with annual increases.

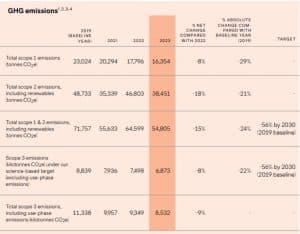

Image: H&M GHG emissions

source: H&M

H&M aims to achieve net-zero emissions by 2024. For this, the company has strategically planned to reduce its GHG emissions by at least 90%. They also promise to offset residual emissions with permanent CO2 removal technology.

Their climate transition plan, as defined in their latest sustainability report primarily outlines strategies to achieve these targets. It focuses on:

Energy efficiency, reducing energy use across their operations, logistics, and supply chain.

Sourcing 100% renewable electricity and engaging partners and suppliers to increase its renewable energy usage.

Scaling up circular systems to reduce dependency on virgin materials and decouple revenue from resource use.

Overall, the partnership between H&M and Rondo Energy shows promise in tackling the challenges of decarbonizing the textile industry. Their collaboration can make significant strides towards sustainability in fashion.

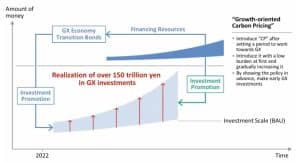

The press release from Japan Climate Transition Bonds Framework under the Ministry of Finance (MoF) states that on July 2, 2024, Japan will launch its inaugural JPY1.6 trillion (USD 11 billion) Climate Transition Bond, dedicated to funding the nation’s extensive Green Transformation (GX) program.

The GX Plan aims to mobilize JPY150 trillion (USD 1 trillion) in public and private investments over the next decade, targeting cutting-edge, sustainable technologies to mitigate domestic emissions. This initiative aligns with Japan’s commitment to achieving its 46% greenhouse gas (GHG) reduction targets by 2030 and becoming carbon neutral by 2050.

Key Initiatives in Japan’s GX Promotion Strategy

As per the Climate Transition Bond Framework, In FY 2021, Japan’s energy self-sufficiency rate was 13.3%. It has been heavily reliant on imported oil, coal, and liquefied natural gas since the Great East Japan Earthquake occurred in 2011.

Achieving Green Transformation (GX) necessitates addressing high-emission sectors.

Emission reduction efforts are crucial for energy transformation in the following sectors:

Heavy industries like steel and chemicals, significantly contribute to emissions after distribution.

Everyday life sectors include households, transportation, commercial, and educational facilities.

Priority will be given to technologies that efficiently and effectively reduce emissions in each sector. The prime focus will be on those that forge industrial competitiveness and drive economic growth.

Japan’s GX promotion strategy establishes two key initiatives to meet international commitments, ensure a stable energy supply, and realize economic growth.

1. Stable Energy Supply and Decarbonization:

Promote energy conservation measures.

Transition power sources to improve energy self-sufficiency, focusing on renewable energy and nuclear power.

2. Growth-Oriented Carbon Pricing Concept:

Implement and execute bold upfront investment support using instruments such as GX Economy Transition Bonds.

Provide incentives for GX investment through carbon pricing.

Utilize new financial mechanisms to support the transition.

These initiatives ensure a stable energy supply while advancing toward decarbonization and economic growth.

Japan’s Climate Transition Bonds Set New Standards in Sustainable Finance

The press release discreetly mentions that Japan’s Climate Transition Bonds are certified under the Climate Bonds Standard. It assures investors’ adherence to global best practices in environmental objectives.

Sean Kidney, CEO, of Climate Bonds Initiative, said:

“Transition is the theme for the year: corporates, cities and countries need to do transition plans in line with global emission reduction targets; under the Paris Climate Agreement countries are working on ambitious new Nationally Determined Contributions (NDCs) – transition plans – to be tabled at next year’s COP. “This bond shows clearly how governments, and others, can raise funds to invest in that transition. It marks a significant milestone in transition finance.”

The First 55.5% Share

A substantial 55.5% of the bond’s proceeds will fund R&D initiatives. It would focus on renewable energy and hydrogen utilization in steelmaking, to help limit global temperature increases to 1.5°C.

The Second 44.5% Share

The remaining 44.5% will support subsidies for activities like manufacturing electricity storage batteries and implementing energy-efficiency measures in buildings. Notably, the bond explicitly excludes funding for gas-fired power generation or ammonia co-firing in coal-fired plants.

The independent verification report, prepared by the Japan Credit Rating Agency (JCRA), a Climate Bonds Approved Verifier, reinforces the bond’s credibility.

Atsuko Kajiwara, Managing Executive Officer and head of the Sustainable Finance Evaluation Group at JCRA, said:

“Since 2020, JCR has been contributing to the government’s efforts to develop Japan’s transition pathway toward net zero by 2050 and alignment with the Paris Agreement. JCRA hopes the government’s strong initiative will help various Japanese corporates that struggle to find a way to attain both carbon neutrality and business expansion in the coming decades.”

We shall elaborate on the history and additional details of this bond in the next paragraphs.

The development of Climate Transition Bonds (JCTBs) in Japan, IEA Reports

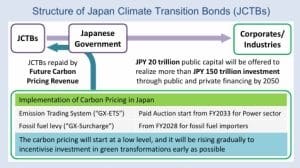

In February 2024, Japan made history by issuing the world’s first sovereign transition bonds—Japan Climate Transition Bonds (JCTBs). The issuance included two tranches of JPY 800 billion (USD 5 billion) each, with tenors of 5 and 10 years. Certified by the Climate Bonds Initiative, these bonds are grounded in Japan’s national transition strategy.

source: IEA Report 2024

Unlocking the Key Features of JCTBs

Investment Plan

Japan’s Basic Policy for the Realization of Green Transformation, published in February 2023, outlines a detailed investment plan for 22 industrial sectors to achieve carbon neutrality by 2050.

Envisions JPY 20 trillion (USD 130 billion) of public capital

Aims to generate over JPY 150 trillion (USD 1 trillion) in investment through public and private financing by 2050

Includes sector-specific transition roadmaps developed by expert committees

Focus on Nascent Technologies

Over half of the proceeds from JCTBs will be allocated to emerging technologies crucial for the transition.

Innovative Carbon Pricing Approach:

Utilizes future carbon pricing revenue for immediate bond repayment

Allows for immediate deployment of capital based on assumed future revenue from carbon taxes

Potential for Emerging Markets and Developing Economies (EMDE):

Credit Intermediary Role: The government acts as a credit intermediary, enhancing the creditworthiness of corporates and simplifying financing for small-scale projects.

Credit Enhancements: For countries with sub-investment-grade credit ratings, additional credit enhancements such as guarantees from Development Finance Institutions (DFIs) may facilitate access to international capital markets.

Japan’s climate transition bonds set a new standard for sovereign transition bonds. This model can guide other nations, especially in emerging markets. Consequently leveraging future carbon pricing revenues and attract significant investment for green transformations.

Lithium, hailed as the ‘white gold‘ of modern times, is reshaping battery technology. Known for its lightweight nature, unparalleled electrochemical potential, and high energy density, lithium stands at the forefront of energy storage, driving the global transition to renewable energy. Its journey from a basic mineral to a crucial battery component highlights its pivotal role in technological advancement and sustainable energy solutions.

Amid the push for net zero emissions by 2050, lithium assumes paramount importance. The soaring demand necessitates ramped-up production, urging advancements in mining, refining, and sustainable extraction and processing technologies.

As nations and industries align towards a greener future, lithium emerges as a linchpin in driving technical innovation and sustainability efforts. But before lithium turns out to be this important, it’s interesting that this unique element has a fascinating origin story.

Humanity’s interaction with lithium spans just over 200 years. In the 1790s, Brazilian scientist José Bonefácio de Andrada e Silva discovered two new minerals, petalite and spodumene, on the Swedish island of Utö.

Later, in 1817, Swedish scientist Johan August Arfwedson identified a new element in these minerals. Working in the lab of chemist Baron Jöns Jacob Berzelius, Arfwedson isolated a sulfate that did not contain any known alkali or alkaline earth metals. He named this new element lithium, derived from the Greek word “lithos,” meaning stone, due to its grey, stone-like appearance.

Where Does Lithium Come From?

Some of the lithium found in the rechargeable batteries of our smartphones, laptops, and EVs dates back almost 14 billion years ago.

The lithium cycle begins with magma that contains lithium rising to the Earth’s crust during volcanic activity. This magma cools and crystallizes into rocks such as granites or pegmatites. Over thousands of years, weathering breaks down these rocks, releasing lithium salts that flow into rivers. Most of this dissolved lithium ends up in the oceans.

However, in some high mountainous regions like the South American Andes, rivers terminate in closed basins. Here, water evaporation leaves behind lithium-enriched brine in salt flats, known as salars.

Besides these natural deposits, lithium can also be sourced from oilfield brines, geothermal brines, and clays. Although lithium is not rare, it is highly reactive and never found in its pure form in nature. It ranks as the 33rd most abundant element in the Earth’s crust, with an estimated 98 million tonnes.

What Are The Applications and Uses of Lithium?

Lithium stands out for its extraordinary properties. It is the lightest and least dense solid element on the periodic table, with a standard atomic weight of 6.94. Highly reactive, lithium metal ignites on contact with water, a familiar demonstration in chemistry labs.

Consequently, it is only found in mineral or salt forms in nature. In its metallic form, lithium is a soft, silvery-grey metal with excellent heat and electric conductivity, making it ideal for storing and transmitting energy.

Lithium is so soft it can be cut with a knife and has one of the lowest melting points (180.5 °C) and boiling points (1,347°C) among metals. Its high electrode potential and low atomic mass provide a high charge and power-to-weight ratio, which makes lithium especially suitable for use in rechargeable batteries.

Lithium Batteries: Powering the Future

A critical element in the production of rechargeable batteries, lithium is vital for electric vehicles (EVs), hybrids, laptops, and mobile phones. Lithium-ion batteries are favored by car manufacturers for their ability to store significant energy in compact spaces and quick recharge capabilities.

Notably, lithium iron phosphate batteries are esteemed for their safety and durability, making them ideal for stationary storage and secure EV applications.

In the realm of EVs and lithium-ion batteries, two primary types of lithium, lithium carbonate, and lithium hydroxide, dominate. Major lithium producers often supply both variants to meet the demands of EV manufacturers, alongside catering to other industries requiring diverse lithium applications.

Conversely, smaller lithium companies typically specialize in the production of a single lithium type.

Diverse Applications Beyond Batteries

The versatility of lithium goes beyond battery technology, impacting various sectors that leverage its unique properties. In aerospace, lithium’s lightweight yet robust characteristics enhance fuel efficiency and performance in aircraft and spacecraft.

Incorporating lithium into glass and ceramics yields stronger, more durable products with enhanced thermal resistance, ideal for sturdier and more efficient cookware, tiles, and household items.

Furthermore, lithium compounds serve as high-temperature lubricants, enduring extreme conditions to ensure smooth operation for heavy machinery and vehicles under intense stress and temperature. This wide array of applications underscores lithium’s pivotal role, not only in driving cleaner energy solutions like electric vehicles but also in propelling manufacturing processes and product functionalities across diverse industries.

The breadth of its applications underscores global dependence on lithium for technological advancements and sustainability initiatives. But how exactly is lithium produced or mined?

How is Lithium Mined?

Various ways are available to extract lithium, but two major ones exist to produce industrial lithium.

Conventional Lithium Brine Extraction

The majority of commercial lithium production today comes from extracting lithium from underground brine reservoirs, primarily located in the Lithium Triangle of the Andes (Bolivia, Argentina, and Chile) and in China.

Lithium brine recovery is a straightforward but time-consuming process. Salt-rich water is pumped to the surface and into evaporation ponds. Over months, water evaporates, precipitating various salts and increasing lithium concentration in the remaining brine.

During evaporation, hydrated lime (Ca(OH)2) is added to remove unwanted elements like magnesium and boron. Once lithium concentration is sufficient, the brine is pumped to a recovery facility where the following steps occur:

Brine purification to remove contaminants.

Chemical treatment to precipitate desirable products and byproducts.

Filtration to remove solids.

Treatment with soda ash (Na2CO3) to precipitate lithium carbonate (Li2CO3).

Washing and drying of lithium carbonate to produce the final product.

2. Hard Rock Mining

Hard rock mining, more complex and energy-intensive than brine extraction, involves extracting lithium from minerals such as spodumene, lepidolite, petalite, amblygonite, and eucryptite. Spodumene is the most abundant, providing most of the world’s mineral-derived lithium.

Australia leads in spodumene production, with operations also in Brazil, Portugal, southern Africa, and China. New mines are expected in North America and Finland by 2025. The process involves:

Mining and crushing the ore.

Roasting at 2012°F (1100°C), cooling to 140°F (65°C), milling, and roasting again with sulfuric acid at 482°F (250°C) (acid leaching).

During acid leaching, lithium ions replace hydrogen in the acid, forming lithium sulfate and insoluble residue.

Adding lime to remove magnesium.

Using soda ash to precipitate lithium carbonate.

Lime slurry may adjust pH to neutralize excess acid.

3. New Lithium Production Methods

In the US, commercial-scale lithium production mainly comes from a brine operation in Nevada. However, there’s growing pressure to increase domestic production to secure lithium supplies.

Opportunities for new methods include:

Direct lithium extraction from geothermal brines (e.g., Salton Sea, CA) and produced water from shale gas fracking (Texas).

Extraction from lithium-bearing clays in Nevada.

Various production methods are being tested, including:

Acid leaching with sulfuric and hydrochloric acid.

Using hydrated lime to remove impurities and neutralize waste before returning it to the environment.

These innovations aim to enhance domestic lithium production and ensure a stable supply of this critical metal.

What is The Current State of the Lithium Market?

In the rapidly evolving landscape of the lithium market, competition is fierce and dynamics are swiftly changing. With the price of lithium batteries constituting 40% of an electric vehicle’s production costs, major EV manufacturers like Tesla, Ford, and BYD are actively seeking cost-effective alternatives.

As global aspirations for emission-free transportation by 2050 intensify, about 30 nations have committed to phasing out the sale of new fuel-engine cars, driving demand for critical EV minerals.

China currently leads the lithium battery production market, but the United States and latecomer South Korea are aiming to challenge its dominance. Amid this dynamic environment, understanding the nuances of lithium is crucial. The next sections explore market and price dynamics, the key players, and the outlook associated with the burgeoning lithium industry.

Asia-Pacific’s Dominance and Its Global Impact

The global lithium market has been significantly shaped by the commanding influence of the Asia-Pacific region, spearheaded by economic powerhouses such as China, Japan, and Korea. Recognizing the transformative potential of lithium, especially in battery technology, these nations swiftly invested in the industry, initially targeting consumer electronics and later expanding into EVs.

Their strategic vision included not only production and processing but also the entire lithium supply chain, from extraction to advanced battery manufacturing. This comprehensive approach has granted them considerable leverage over global battery technology trends and pricing dynamics.

In contrast, North America has struggled to keep pace with this rapid progress. Hindered by a fragmented approach and a lack of cohesive strategy and investment, the region’s lithium industry lags behind its Asia-Pacific counterparts.

This disparity has hindered the development of a robust domestic lithium market in North America. This leaves the region vulnerable to supply fluctuations and pricing determinations driven by Asia-Pacific leaders.

China’s stronghold extends beyond LFP batteries, encompassing lithium-ion battery, cathode, and anode production, as well as lithium, cobalt, and graphite processing and refining.

Despite efforts by governments in Europe, the United States, and South Korea to develop domestic battery supply chains, the majority of the EV battery supply chain is expected to remain concentrated in China for the foreseeable future, maintaining its lead in global battery production capacity until 2030, as projected by the International Energy Agency (IEA).

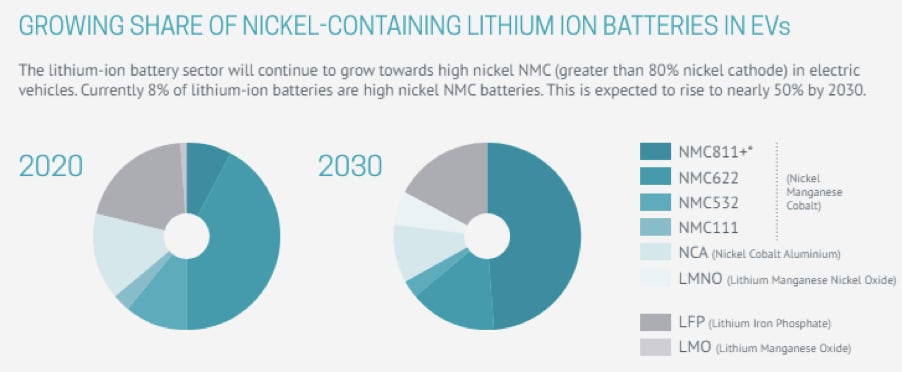

The Shifting Trend in Lithium Batteries

Tesla and Ford Motor, along with other major automakers, have embraced lithium iron phosphate (LFP) batteries as a cost-effective alternative for some of their EVs, moving away from cobalt-based and nickel-based lithium-ion batteries prevalent in Europe and the US. LFP batteries, identified as the most economical lithium-ion battery type in 2022, now constitute around 40% of global EV production. Demand for this battery is projected to rise substantially in the coming years.

Tesla’s shift to LFP batteries at its Shanghai plant since October 2022 signals a broader industry trend. Its peers like Mercedes-Benz Group AG, Volkswagen AG, and Rivian Automotive Inc. also commit to integrating LFPs into their vehicles.

This shift is largely facilitated by Chinese manufacturers like Contemporary Amperex Technology (CATL) and BYD, which dominate the LFP market, accounting for 99% of global LFP battery production. CATL, in particular, stands as the world’s largest EV battery maker, supplying batteries to Tesla and various other automakers.

Understanding Lithium Prices: Key Factors and Trends

The global appetite for lithium has surged, propelled by the burgeoning battery industry and the widespread adoption of lithium-ion batteries in electric vehicles (EVs). This surge in demand casts a glaring spotlight on the current state of lithium supply, underscoring the escalating consumption rates worldwide.

In this segment, we delve into the intricate dynamics of various factors driving the market, examining how the industry is responding to this mounting need. Key factors such as supply and demand dynamics, mining capacities, geopolitical influences, and technological advancements play pivotal roles in shaping the delicate balance between supply and demand.

Understanding these factors is crucial for stakeholders in the lithium industry, from miners to battery manufacturers and investors. Here are the primary elements that impact lithium prices:

Navigating the Supply-Demand Dynamics

The lithium market exhibits characteristics of an immature market. The supply swings between deficit and surplus due to strong growth and infrastructure development challenges.

With rechargeable batteries constituting around 85% of global demand, the surge in EV uptake has led to soaring demand.

However, the slow pace of infrastructure development has hindered supply growth, resulting in price spikes in 2022. As EV subsidies decrease and prices normalize, we anticipate a controlled decline, settling around $20,000 per tonne by the decade’s end.

Therefore, any imbalance in the supply and demand equation directly affects prices. Any oversupply can depress prices until demand catches up.

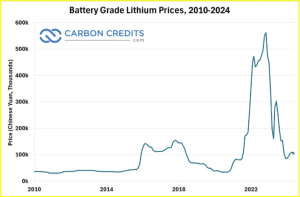

Conversely, a surge in demand, driven by the EV boom, can outpace supply, pushing prices up. This is exactly what happened in November 2022 when a record-breaking lithium price rally happened, reaching over a fivefold increase.

Today, lithium spot prices see an even greater increase of 191%+ from July 2025. It jumped from $8,259 per tonne to a whopping $24,086 per tonne in February 2026.

Unraveling Geopolitical Influences

Geopolitical factors significantly influence the lithium market due to the concentration of lithium reserves in specific regions. Countries like Australia, Chile, and Argentina hold substantial lithium reserves and are major players in the global supply chain. Political stability in these countries is crucial. Any political unrest or policy changes can disrupt supply and affect global prices.

Moreover, government policies regarding mining operations, environmental standards, and export regulations can also impact lithium production and prices. Favorable policies can boost production, while restrictive regulations can hinder it.

International trade policies, including tariffs and trade agreements, further influence the flow of lithium across borders. For example, trade tensions between major economies can lead to tariffs on lithium products, affecting global supply chains and prices.

This is what happened recently with the United States announcing its plan to increase tariffs on Chinese imports, including EVs, batteries, and solar cells.

Advancements in technology have a dual impact on lithium prices by affecting both demand and supply.

Battery Technology: Breakthroughs in battery technology can significantly influence lithium demand. The development of alternative battery chemistries, such as solid-state batteries or sodium-ion batteries, could reduce reliance on lithium, potentially decreasing its demand and price. On the other hand, innovations that enhance lithium-ion battery performance can boost demand.

Extraction and Processing Technologies: Technological improvements in lithium extraction and processing can increase supply efficiency and reduce production costs. For example, advancements in direct lithium extraction (DLE) techniques can make it easier and more cost-effective to extract lithium from brine resources, positively impacting prices.

Disentangling Environmental Regulations

Environmental considerations are increasingly shaping the lithium market today.

Stricter environmental regulations on mining practices can limit lithium supply and drive up prices. Mining operations must comply with environmental standards to mitigate their impact on ecosystems and water resources, which can increase operational costs.

Furthermore, the growing emphasis on reducing the environmental footprint of lithium extraction is prompting the industry to adopt greener practices. These sustainable techniques, such as using renewable energy in mining operations and recycling water, may initially increase costs. However, they are expected to lead to long-term sustainability and potentially stabilize prices.

There is also rising pressure from consumers and investors for companies to adhere to environmental, social, and governance (ESG) criteria. Companies that prioritize sustainable and ethical practices may gain a competitive edge, influencing market dynamics and prices.

Quality Challenges in Battery-Grade Lithium Production

As lithium increasingly powers rechargeable batteries, ensuring high-quality lithium products for battery use becomes paramount. Producing battery-grade lithium involves intricate refining processes to meet stringent quality and purity standards.

New refineries typically start with lower-quality technical-grade lithium, necessitating refining improvements to achieve battery-grade purity. Consequently, despite an overall supply surplus, the battery-grade lithium market may face short-term constraints until refining operations are optimized.

What are the Top Lithium Producing Countries?

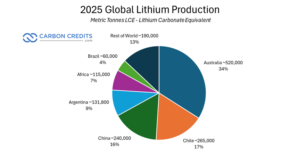

In 2025, three countries – Australia, Chile, and China – dominated global lithium production, collectively accounting for 67% of the total output.

Australia: Leading the Charge

Australia stands as the world’s top lithium producer, sourcing the mineral directly from hard-rock mines, particularly spodumene. Over the past decade, Australia witnessed a remarkable surge in production. In 2013, output stood at 13,000 metric tons, soaring to an impressive 520,000 metric tons by 2025.

Chile: Brine Extraction Expert

Chile follows closely behind Australia in lithium production, albeit with more modest growth. The South American nation primarily extracts lithium from brine sources, with production climbing from 13,500 tonnes in 2013 to 265,000 metric tons in 2025.

China: Closing the Gap

China, also harnessing lithium from brine, has been steadily approaching Chile’s production levels. From a modest 4,000 metric tons in 2013, China ramped up domestic production to 240,000 metric tons in 2025.

Additionally, Chinese companies have expanded their influence in the global lithium market, with three of them ranking among the top lithium mining entities. Tianqi Lithium, the largest among them, holds a significant stake in Greenbushes, the world’s largest hard-rock lithium mine in Australia.

Argentina: A Rising Contender

Argentina emerges as the fourth-largest lithium producer, tripling its output over the past decade. With increased investments from international players, Argentina aims to further enhance its lithium production capacity.

With major producers scaling up to meet the surging demand, particularly from the clean energy sector, like electric vehicle batteries, the lithium market recently experienced a surplus. This oversupply led to a significant price collapse of over 80% from the record highs witnessed in late 2022.

How to Invest in Lithium? Stocks, ETFs, and Derivatives

Due to the nascent stage of the lithium market, the range of investment products available is relatively limited compared to other commodities. Nevertheless, investors can still tap into this dynamic market through two primary avenues: lithium stocks and lithium ETFs.

Lithium Stocks:

Investing in individual stocks remains one of the most direct ways to gain exposure to the lithium industry. However, it’s crucial to recognize that stocks serve as proxies for the market’s performance.

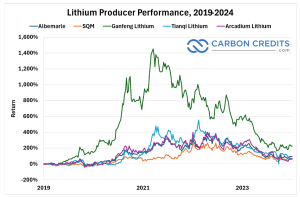

The soaring costs of lithium don’t always translate into corresponding increases in lithium stock prices. Establishing new mining operations can be capital-intensive, and ultimately, a stock’s valuation hinges on the company’s financial health. Despite this caveat, lithium stocks have demonstrated robust performance over the past five years.

Investing in lithium stocks offers several benefits. Firstly, individual lithium stocks provide significant earning potential if the company performs well. Additionally, many lithium stocks pay dividends, offering investors regular income that can be reinvested to bolster portfolio growth.

Moreover, some lithium producers have alternative revenue streams, which can help mitigate the volatility associated with lithium prices. However, investing in lithium stocks also entails certain risks. For instance, putting all investments into one or two lithium stocks can result in a lack of diversification in the portfolio.

Furthermore, the return on lithium stocks is heavily dependent on the financial health of the company, necessitating regular updates on the company’s fundamentals and thorough research.

Lithium ETFs

For investors seeking exposure to the lithium market without the time-intensive task of researching individual stocks, lithium exchange-traded funds (ETFs) offer a convenient option. These ETFs track an index composed of a diversified collection of lithium stocks, providing you with instant access to a broad portfolio that includes both lithium producers and manufacturers.

Here are two prominent lithium ETFs:

Global X Lithium & Battery Tech ETF (LIT): LIT comprises 39 different lithium and battery stocks. With $4.5 billion in assets under management, this ETF charges an annual fee of 0.75%.

Amplify Lithium & Battery Technology ETF (BATT): BATT is solely focused on lithium battery providers. Holding $194 million in assets, this ETF charges an annual fee of 0.59%.

Investing in lithium ETFs presents its own set of benefits. ETFs provide instant diversification across a broad range of lithium-focused stocks, thereby reducing the risk associated with individual stock selection. Also, ETFs spread investment risk across a large portfolio of stocks, making them less risky than individual stocks.

Furthermore, similar to individual stocks, some lithium ETFs offer dividend schemes, providing investors with the opportunity for positive cash flow. Nevertheless, there are risks associated with investing in lithium ETFs as well.

For example, during upward trends in the lithium market, returns from ETFs may not be as substantial as those from individual stocks. And take note, ETFs are not free products; providers charge investors a percentage fee for operating and maintaining the ETF.

Direct Investment Through the Commodities Market

For those interested in direct investment, lithium can be traded in the commodities market through futures and options. These derivatives allow you to buy and sell access to lithium as a material, though they come with significant risk and volatility, making them unsuitable for inexperienced investors.

Futures Contracts

A futures contract is an agreement to buy or sell a commodity at a future date for a specified price. There are two types:

Standard Futures Contracts: You commit to buying the actual commodity. If you hold the contract until expiration, you must purchase the physical lithium.

Cash Settlement Futures Contracts: Instead of exchanging the physical commodity, the parties settle the contract’s value in cash.

Options Contracts

Options contracts allow you to trade the value of an asset, with the added flexibility of choosing whether to execute the contract at expiration. This differs from futures contracts, which must be executed regardless of market conditions. When buying an options contract, you pay an upfront fee known as a “premium.”

Investing in lithium offers several pathways, including stocks of lithium producers or users, funds that aggregate lithium-related equities, and direct commodity trading through futures and options. Each method carries different levels of risk and complexity, catering to various investor preferences and experience levels.

Who are the Major Lithium Companies?

1. ALBEMARLE: Market cap: US$14 billion

Albemarle, based in North Carolina, stands as the largest lithium company by market cap and the world’s leading lithium producer, boasting over 7,000 global employees. Following a 2022 realignment, Albemarle now operates two primary business units, with a particular focus on lithium-ion battery and energy transition markets under its Albemarle Energy Storage unit. This division oversees lithium carbonate, hydroxide, and metal production.

With operations spanning Chile, Australia, and the US, Albemarle holds a diverse portfolio of lithium mines and facilities. In Chile, the company produces lithium carbonate at its La Negra conversion plants, leveraging brine from the Salar de Atacama.

In the US, Albemarle aims to bolster domestic production in line with the Inflation Reduction Act. It owns the Silver Peak lithium brine operations in Nevada’s Clayton Valley, set to double lithium production by 2025. Albemarle received a $90 million critical materials award from the US Department of Defense in September 2023 to enhance domestic lithium production and support the EV battery supply chain.

Additionally, the company plans to revive the Kings Mountain lithium mine in North Carolina, backed by US government funding. Albemarle also plans to develop the Albemarle Technology Park in North Carolina for advanced R&D in lithium innovation.

2. SQM: Market cap: US$12.07 billion

SQM, a chemicals giant, operates in over 20 countries, serving customers across 110 nations. The company’s diverse business areas span lithium, potassium, and specialty plant nutrition.

Primarily operating in Chile, SQM extracts brine from the Salar de Atacama and processes lithium chloride into lithium carbonate and hydroxide at its Salar del Carmen lithium plants near Antofagasta. The company is expanding production at Salar del Carmen from 180,000 MT to 210,000 MT, initiating this year.

To mitigate environmental impact, SQM announced a $1.5 billion investment in the Salar Futuro project, focusing on advanced evaporation technologies, direct lithium extraction, and a seawater desalination plant.

Despite uncertainty stemming from Chile’s National Lithium Strategy, SQM’s existing contracts, extending through 2030, are expected to be respected by the government. In early 2024, a partnership was formed between SQM and state-owned mining company CODELCO, with CODELCO holding a majority control stake.

In Australia, SQM is developing the Mount Holland lithium project, recognized as one of the world’s largest hard-rock deposits, in partnership with Wesfarmers. Anticipating lithium hydroxide production to commence by H1 2025, SQM’s lithium carbonate capacity was projected to reach 210,000 tons by the beginning of 2024.

3. Tianqi Lithium: Market cap: US$10.43 billion

Tianqi Lithium is a subsidiary of Chengdu Tianqi Industry Group based in China. As the world’s largest hard-rock lithium producer, Tianqi Lithium operates assets in Australia, Chile, and China. The company holds a notable stake in SQM, having acquired a 2.1% share in 2016, later increasing it to 23.77%.

In Australia, Tianqi owns the Greenbushes mine, acquired in 2012 through the purchase of Talison Lithium. The company also developed a lithium hydroxide plant in Western Australia’s Kwinana Industrial Area, commencing production in Q3 2019. Subsequent output began in mid-2021.

Rising lithium prices and its Hong Kong listing in 2022, which raised approximately US$1.7 billion, contributed to Tianqi’s buoyancy. Commercial production at Kwinana’s Train 1 commenced in December 2022, with Train 2 anticipated to start in 2024. Once operational, the hydroxide plant is projected to produce 48,000 MT per year, utilizing lithium from Greenbushes.

In February of the current year, Tianqi Lithium updated its total mineral reserves at Greenbushes to 447 million tonnes, with an average lithium oxide grade of 1.5%, equivalent to about 16 million tonnes of lithium carbonate.

What is In Store for Lithium?

Forecasting lithium supply beyond the end of the decade presents challenges due to limited visibility into existing, planned, and potential projects. While projections until 2030 can be reasonably accurate, the landscape becomes murkier.

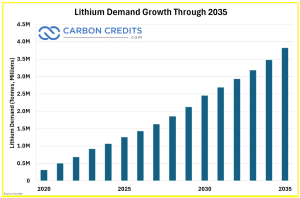

On the demand side, projections suggest that it will increase to almost 4 million tonnes, as shown below. But of course, as discussed earlier, various trends impact this demand trajectory.

Incentive pricing becomes a critical factor in determining the attractiveness of new projects. With an estimated 1.5 million tonnes of supply, the fully allocated cost of lithium would be around $15,000 per tonne, suggesting market pricing would exceed this threshold.

Navigating the Immaturity of the Lithium Market

Forecasting the future of the lithium market is hindered by its relative immaturity. Lack of globally accepted specifications and pricing anchors complicates pricing dynamics.

Lithium products, akin to specialty chemicals, require precise specifications, yet the industry’s growth trajectory impedes standardization efforts. While greater standardization is anticipated in the future, it will evolve gradually.

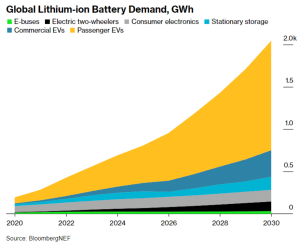

According to Bloomberg estimates, demand for lithium-ion batteries will increase tenfold over the next decade. This surge in demand is largely driven by the global commitment of over 100 countries to achieve net zero emissions within the coming decades.

As part of this commitment, many nations are turning to the electrification of transportation as a crucial solution to reduce GHG emissions and combat climate change. This shift towards electrification underscores the growing importance of lithium-ion batteries in powering EVs and other clean energy technologies.

The Role of Partnerships in Shaping the Lithium Industry

In 2022, a significant portion of the lithium supply was dominated by a handful of companies. However, future industry dynamics are expected to witness a decline in their market share, as smaller firms expand and new ventures emerge.

While horizontal integration may not be a prevailing trend, vertical integration is poised to play a pivotal role. Partnerships between miners and refiners offer mutual benefits, enabling risk-sharing and capital investment in new projects.

Collaborative efforts between upstream and downstream operations enhance expertise, improve margins, and capture a larger market share. Such partnerships, exemplified by ventures like Pilbara Minerals and POSCO in South Korea and SQM and Wesfarmers in Western Australia, are anticipated to become increasingly common in the industry’s future landscape.

Conclusion

The evolution of lithium, from its discovery over two centuries ago to its pivotal role in powering modern technology, underscores its significance in shaping our present and future. As the world accelerates towards a sustainable energy paradigm, lithium emerges as the linchpin of this transition, fueling advancements in battery technology and driving the proliferation of electric vehicles and renewable energy storage solutions.

Neustark, the Swizz-based carbon removal solution provider, has raised US$69 M from Decarbonization Partners BlackRock and Temasek. The company intends to use the funds to expand its portfolio of global CDR projects and the overall growth of its team.

Let’s deep dive into the deal in the upcoming content.

Decarbonization Partners: The Investment Catalyst for Neustark

Decarbonization Partners, a collaboration between Singapore-based Temasek and the world’s largest asset manager company BlackRock was launched in 2022. They focus on late-stage venture capital and early-growth private equity. They invest in companies developing technologies to accelerate the global transition to a net zero economy by 2050. Sectors like Carbon Capture, Bio Products, Energy Innovation, Mobility, and Digital Transformation are their major investment partners.

Their press release from April revealed.

“The final closure of $1.40B for its inaugural late-stage venture capital and growth private equity investment fund. The Decarbonization Partners Fund I, surpassed its $1 billion fundraising target.”

Noteworthy, Decarbonization Partners led Neustark’s growth equity round, with participation from climate tech investor Blume Equity. Subsequently, new investors joined Neustark’s existing chain of investors. For instance, UBS, Holcim, Siemens, Verve Ventures, and ACE Ventures are continuing their support.

Meghan Sharp, Global Head & Chief Investment Officer of Decarbonization Partners, said:

“With carbon capture, utilization, and storage being one of our key investment focuses, we believe that we have found a perfect partner to help scale the industry – and ultimately its decarbonization impact – in the years to come. Neustark not only helps organizations integrate carbon removal to address their hard-to-abate emissions, but their solution also contributes to decarbonizing the construction industry.”

Neustark is a pioneer in the carbon removal industry. It offers unique solutions to permanently store CO₂ in recycled mineral waste, such as demolished concrete.

IP-protected Carbon Removal Technology

Scientifically speaking, their IP-protected technology captures biogenic CO2 primarily from biogas plants. It is then liquified and transported to recycling sites for construction waste. There, CO2 is injected into concrete granulates or other mineral waste. Consequently, it triggers the mineralization process that permanently binds CO2 to the surfaces and pores of the granules. The carbonated aggregate can then be used for road construction or to produce recycled building materials. This mineralization process securely stores CO2 for hundreds of thousands of years, with minimal risk of reversal.

Moving on, the company is already capturing and storing tons of CO₂ daily with its initial deployments in Switzerland and Europe. Now, the company is ramping up its operations globally.

The funding from BlackRock and Temasek fuels its ambitious plans of permanently removing 1MT of CO₂ by 2030 and soaring higher.

Notably, Neustark currently has 40 plants under construction across Europe and has already sold nearly 120,000 tons of carbon removal to date. Their key clients include Microsoft, UBS, and NextGen. All projects receive certification under the Gold Standard, ensuring credible third-party assessment and transparency in performance.

Johannes Tiefenthaler, Co-CEO and Founder at Neustark said:

“We turn the world’s largest waste stream – demolition concrete – into a carbon sink. In the last year, we have already deployed our unique solution at 19 sites. This growth investment will take us into the next exciting phase of our mission, helping us to further scale our impact across Europe, enter new markets in North America and Asia Pacific, and develop new solutions to store even more CO2 in mineral waste streams.”

Neustark stores around 10kg of CO₂ per ton of demolished concrete. They claim, “One site can do in one hour what 50 trees do in one year.” This is how they make negative emissions.

An example of a remarkable achievement is the large-scale storage plant constructed at a demolition site in Biberist, Switzerland. It’s a collaboration with Alluvia and Vigier Beton Seeland Jura. This plant, with a yearly storage capacity of 1000T of CO₂, has been operational since May 2023.

Financial and Sustainability Highlights of BlackRock and Temasek

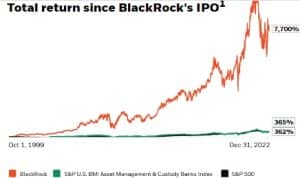

BlackRock proudly attributes its success to the trust of its clients and the strong partnerships forged with them.

source: BlackRock

It pursues a sustainability strategy to reduce GHG emissions from its facilities, data centers, and upstream value chains. In 2023, BlackRock made progress by:

Employing energy efficiency strategies

Achieving 100% renewable electricity match

Enhancing SAF and carbon credit procurement processes

Establishing a Supplier Sustainability Program

BlackRock’s emissions reduction goals (relative to 2019 baseline):

67% reduction of Scope 1 and 2 emissions by 2030

40% reduction in Scope 3 business travel emissions by 2030

Engaging suppliers representing 67% of emissions to set science-aligned goals by 2025

On the other side, Temasek’s S$382b portfolio, as of 31 March 2023, is primarily concentrated in Singapore and the broader Asia region. It spans diverse industries including financial services, transportation & industrials, telecommunications, media & technology, consumer & real estate, and life sciences & agri-food.

It has implemented an internal carbon price of US$50 per tonne of carbon dioxide equivalent (tCO2e), with plans to increase this to $100 tCO2e by 2030. This initiative aims to deepen climate considerations in investment evaluations.

source: Temasek

Apart from BlackRock, Temasek has also partnered with GenZero, Climate Impact X, Pentagreen Capital, etc. It has formed a dedicated investment platform with an initial capital commitment of S$5 billion. This platform is designed to accelerate and expand global decarbonization solutions.

Overall, we can infer that with support from BlackRock and Temasek, Neustark can make significant strides in carbon removal through innovative solutions.

Carbon Credits are an allowance for a company holding the credits to emit carbon emissions or greenhouse gases. A single credit equals one ton of carbon dioxide to be emitted or the mass equivalent to carbon dioxide for other gases. Companies hold many credits, as many as they wish to purchase to balance out their emissions.

Carbon Markets 101

A carbon market allows investors and corporations to trade both carbon credits and carbon offsets simultaneously. This mitigates the environmental crisis, while also creating new market opportunities.

New challenges nearly always produce new markets, and the ongoing climate crisis and rising global emissions are no exception.

The renewed interest in carbon markets is relatively new. International carbon trading markets have been around since the 1997 Kyoto Protocols, but the emergence of new regional markets has prompted a surge in investment.

In the United States, while no federal carbon market exists yet, multiple states now operate carbon pricing initiatives.

California continues to lead with its cap-and-trade program, while the Regional Greenhouse Gas Initiative (RGGI) includes 11 northeastern states.

Washington State launched its cap-and-invest program in 2023, and Oregon’s program began in 2022, marking a significant expansion of state-level carbon markets.

The advent of new mandatory emissions trading programs and growing consumer pressure have driven companies to turn to the voluntary market for carbon offsets. Changing public attitudes on climate change and carbon emissions has added a public policy incentive. Despite an ever-shifting background of state, federal, and international regulations, there’s more need than ever for companies and investors to understand carbon credits.

This guide will introduce you to carbon credits and outline the current state of the market. It will also explain how credits and offsets work in currently existing frameworks and highlight the potential for growth.

1. Carbon Credits, Offsets and Markets – An Introduction

The Kyoto Protocol of 1997 and the Paris Agreement of 2015 were international accords that laid out international CO2 emissions goals. With the latter ratified by all but six countries, they have given rise to national emissions targets and the regulations to back them.

With these new regulations in force, the pressure on businesses to find ways to reduce their carbon footprint is growing. Most of today’s interim solutions involve the use of the carbon markets.

What the carbon markets do is turn CO2 emissions into a commodity by giving it a price.

These emissions fall into one of two categories: Carbon credits or carbon offsets, and they can both be bought and sold on a carbon market. It’s a simple idea that provides a market-based solution to a thorny problem.

2. Carbon Credits vs. Carbon Offsets?

The terms are frequently used interchangeably, but carbon credits and carbon offsets operate on different mechanisms.

Carbon credits, also known as carbon allowances, work like permission slips for emissions. When a company buys a carbon credit, usually from the government, it gains permission to generate one ton of CO2 emissions. With carbon credits, carbon revenue flows vertically from companies to regulators, though companies that end up with excess credits can sell them to other companies.

Offsets flow horizontally, trading carbon revenue between companies. When one company removes a unit of carbon from the atmosphere as part of its normal business activity, it can generate a carbon offset. Other companies can then purchase that carbon offset to reduce their own carbon footprint.

Note that the two terms are sometimes used interchangeably, and carbon offsets are often referred to as “offset credits”. Still, this distinction between regulatory compliance credits and voluntary offsets should be kept in mind.

3. How Are Carbon Credits and Offsets Created?

Credits and offsets form two slightly different markets, although the basic unit traded is the same – the equivalent of one ton of carbon emissions, also known as CO2e.

It’s worth noting that a ton of CO2 refers to a literal measurement of weight. Just how much CO2 is in a ton?

The average American generates 16 tons of CO2e a year through driving, shopping, using electricity and gas at home, and generally going through the motions of everyday life.

To further put that emission in perspective, you would generate one ton of CO2e by driving your average 22 mpg car from New York to Las Vegas.

Carbon credits are issued by national or international governmental organizations. We’ve already mentioned the Kyoto and Paris agreements, which created the first international carbon markets.

In the U.S., California operates its own carbon market and issues credits to residents for gas and electricity consumption.

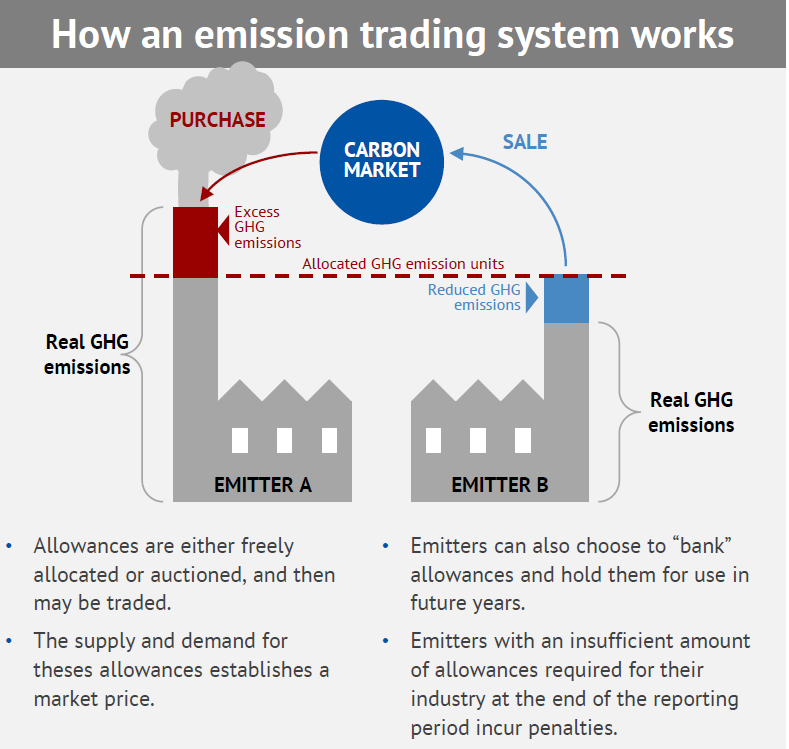

The number of credits issued each year is typically based on emissions targets. Credits are frequently issued under what’s known as a “cap-and-trade” program. Regulators set a limit on carbon emissions – the cap. That cap slowly decreases over time, making it harder and harder for businesses to stay within that cap.

You can think of carbon credits as a “permission slip” for a company to emit up to a certain set amount of CO2e that year.

Around the world, cap-and-trade programs exist in some form in many countries, including Canada, the EU, the UK, China, New Zealand, Japan, and South Korea, with many more jurisdictions considering implementation.

As of 2024, carbon pricing initiatives operate in 46 national jurisdictions and 37 subnational jurisdictions. Recent additions include Indonesia’s carbon trading scheme launched in late 2023, Vietnam’s pilot program initiated in 2024, and Malaysia’s emissions trading system planned for early 2025. Together, these markets cover approximately 23% of global greenhouse gas emissions.

Companies are thus incentivized to reduce the emissions their business operations produce to stay under their caps.

In essence, a cap-and-trade program lessens the burden for companies trying to meet emissions targets in the short term and adds market incentives to reduce carbon emissions faster.

Carbon offsets work slightly differently…

Organizations with operations that reduce the amount of carbon already in the atmosphere, say by planting more trees or investing in renewable energy, have the ability to issue carbon offsets. The purchase of these offsets is voluntary, which is why carbon offsets form what’s known as the “Voluntary Carbon Market”. However, by buying these carbon offsets, companies can measurably decrease the amount of CO2e they emit even further.

4. What is the Carbon Marketplace?

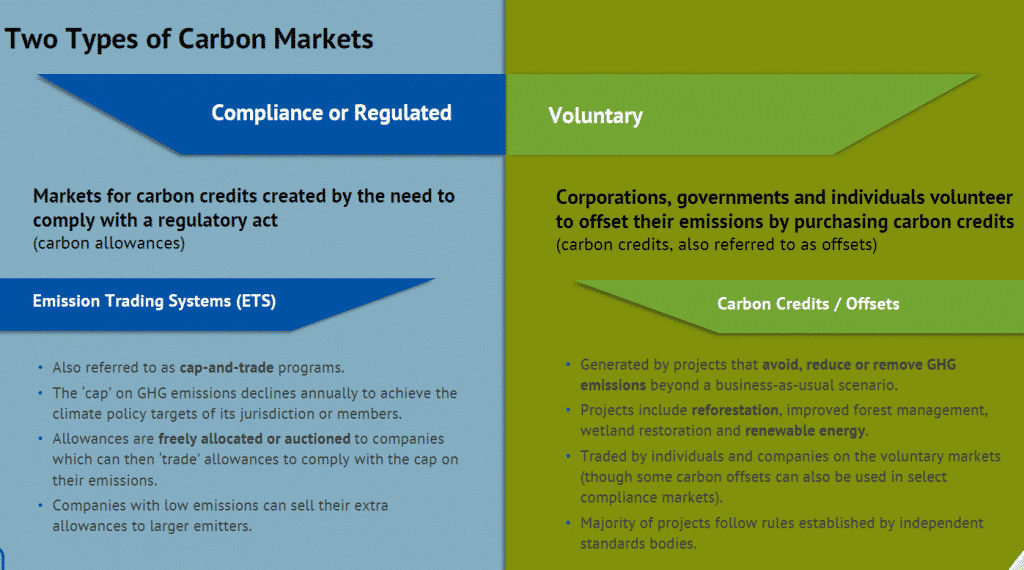

When it comes to the sale of carbon credits within the carbon marketplace, there are two significant, separate markets to choose from.

One is a regulated market, set by “cap-and-trade” regulations at the regional and state levels.

The other is a voluntary market where businesses and individuals buy credits (of their own accord) to offset their carbon emissions.

Think of it this way: the regulatory market is mandated, while the voluntary market is optional.

When it comes to the regulatory market, each company operating under a cap-and-trade program is issued a certain number of carbon credits each year. Some of these companies produce fewer emissions than the number of credits they’re allotted, giving them a surplus of carbon credits.

On the flip side, some companies (particularly those with older and less efficient operations) produce more emissions than the number of credits they receive each year can cover. These businesses are looking to purchase carbon credits to offset their emissions because they must.

Most major companies are doing their part and/or have announced a blueprint to minimize their carbon footprint. However, the amount of carbon credits allocated to them each year (which is based on each business’s size and the efficiency of their operations relative to industry benchmarks) may not be enough to cover their needs.

Regardless of technological advances, some companies are years away from reducing their emissions substantially. Yet, they still have to keep providing goods and services in order to generate the cash they need to improve the carbon footprint of their operations.

As such, they need to find a way to offset the amount of carbon they’re already emitting.

So, when companies meet their emissions “cap,” they look towards the regulatory market to “trade” so that they can stay under that cap.

Here’s an example:

Let’s say two companies, Company 1 and Company 2, are only allowed to emit 300 tons of carbon.

However, Company 1 is on track to emit 400 tons of carbon this year, while Company 2 will only be emitting 200 tons.

To avoid a penalty comprised of fines and extra taxes, Company 1 can make up for emitting 100 extra tons of CO2e by purchasing credits from Company 2, which has extra emissions room to spare due to producing 100 tons less carbon this year than they were allowed to.

The Difference between the Voluntary and Compliance Markets

The voluntary market works a bit differently. Companies in this marketplace have the opportunity to work with businesses and individuals who are environmentally conscious and are choosing to offset their carbon emissions because they want to. There is nothing mandated here.

It might be an environmentally conscious company that wants to demonstrate that it’s doing its part to protect the environment. Or it can be an environmentally conscious person who wants to offset the amount of carbon they’re putting into the air when they travel.

For example, in 2021, the oil giant Shell announced that the company aims to offset 120 million tonnes of emissions by 2030

Regardless of their reasoning, companies are looking for ways to participate – and the voluntary carbon market is a way for them to do just that.

Both the regulatory and voluntary marketplaces complement one another in the professional (and the personal) world. They also make the pool of buyers more accessible to farmers, ranchers, and landowners – those whose operations can often generate carbon offsets for sale.

4.1 Top Carbon Companies (Stocks, ETFs)

As the world transitions to a low-carbon economy, carbon companies are gaining momentum among investors. The stocks they represent are leading the charge in reducing or offsetting emissions. With growing global support for climate goals, these businesses are delivering environmental benefits and financial returns, making them an attractive investment opportunity.

Top Carbon Stocks

We list the top 5 carbon companies of 2025 to watch in this article. These are arguably the best carbon stocks with world-class assets or management teams. Take a quick peek at each of these carbon stocks to have a general understanding of what they do:

Brookfield Renewable Partners (BEP) is a standout in renewable energy. Its 35,000-megawatt portfolio includes hydroelectric plants, wind farms, and solar power. In 2024, BEP reported a solid 11% growth in Funds From Operations (FFO). With plans to add 11,000 megawatts of capacity, BEP is well-positioned to meet surging global demand for clean energy.

Aker Carbon Capture ASA (AKCCF) is revolutionizing industrial emissions reduction with scalable carbon capture solutions. Its “Just Catch” technology serves industries like cement and biomass. The company is involved in notable projects, including capturing 400,000 tonnes of CO₂ annually at Norcem in Norway. With NOK 4.5 billion in cash, Aker is primed for expansion.

LanzaTech Global (LNZA) specializes in converting waste emissions into useful products like ethanol and sustainable aviation fuel. Despite a dip in revenue, LanzaTech is advancing key projects, including Project Drake, a 30-million-gallon SAF initiative. Its innovative technology is driving progress in carbon recycling and biofuel production.

Occidental Petroleum (OXY) is leading the way in carbon capture and storage (CCS) through its subsidiary, 1PointFive. The company is developing the world’s largest Direct Air Capture (DAC) facility, aiming to remove up to 500,000 tonnes of CO₂ annually. With strong government backing and corporate partnerships, Occidental is positioning itself as a major player in the carbon removal industry.

Equinor ASA (EQNR) is a global energy company investing heavily in carbon capture and storage (CCS) and offshore wind. Its Northern Lights project, developed with Shell and TotalEnergies, will store 1.5 million tonnes of CO₂ annually. Equinor is also expanding renewable energy production, ensuring a balanced approach between fossil fuels and clean energy.

From renewable energy to carbon capture and recycling, these companies are leading the way in tackling climate challenges. With robust financials and ambitious strategies, they offer investors a unique opportunity to align profits with sustainability.

Top Carbon ETFs

Like stocks, investors can buy and sell Exchange-Traded Funds (ETFs) whenever the market is open. Often, investing in carbon credits through ETFs offers a simple and diverse way to enter this expanding market.

Here are the top ETFs for 2025 in the carbon credit market and how they are supporting sustainable investments.

The iShares Global Clean Energy ETF (ICLN), managed by BlackRock, invests in renewable energy companies like solar and wind while excluding coal and oil sands. It holds $5-6 billion in assets, with projections to reach $8-10 billion by 2025. Top holdings include First Solar, Iberdrola, Enphase Energy, Vestas Wind Systems, and Ørsted. These companies drive ICLN’s diversified, growth-focused portfolio.

Invesco Solar ETF (TAN) manages $3–4 billion in assets and aims to reach $6–8 billion by 2025. It focuses on solar companies, including manufacturers, installers, and tech providers. TAN follows the MAC Global Solar Energy Index and invests 90% in listed securities, ADRs, and GDRs. Its top holdings include Enphase Energy, First Solar, Sunrun, and Nextracker.

First Trust Global Wind Energy ETF (FAN) manages $2–3 billion in assets, with projections to reach $5–7 billion by 2025. It focuses on wind energy firms, including wind farm operators, power producers, and equipment manufacturers. FAN’s portfolio includes 52 companies, with 60% weight on “Pure Play” and 40% on “Diversified” firms. Top holdings include Orsted, Vestas, Siemens Energy, and GE Vernova, benefiting from global wind power growth.

SPDR S&P Kensho Clean Power ETF (CNRG), managed by State Street, holds $1–2 billion in assets and could grow to $4–6 billion by 2025. It tracks the AI-driven S&P Kensho Clean Power Index, featuring companies in solar, wind, geothermal, hydroelectric power, and energy storage. Key holdings include Plug Power, Shoals Technologies, and Bloom Energy, showcasing its focus on innovation.

The Global X Lithium & Battery Tech ETF (LIT) invests in the growing lithium and battery technology sector. With $4–5 billion in assets, it’s projected to reach $8–10 billion by 2025. LIT tracks the Solactive Global Lithium Index, focusing on lithium mining and battery production. Its top holdings include Albemarle, Tesla, CATL, and Ganfeng Lithium.

ETFs offer a cost-effective, low-risk way to diversify investments, providing stability and reduced volatility. They simplify access to the carbon market, saving investors time and money. For a balanced, hassle-free approach, ETFs are a smart choice over individual stocks.

The voluntary carbon market is difficult to measure. The cost of carbon credits varies, particularly for carbon offsets, since the value is linked closely to the perceived quality of the issuing company. Third-party validators add a level of control to the process, guaranteeing that each carbon offset actually results from real-world emissions reductions, but even so, there are often disparities between different types of carbon offsets.

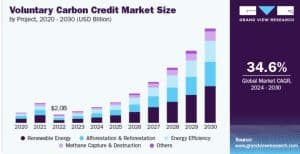

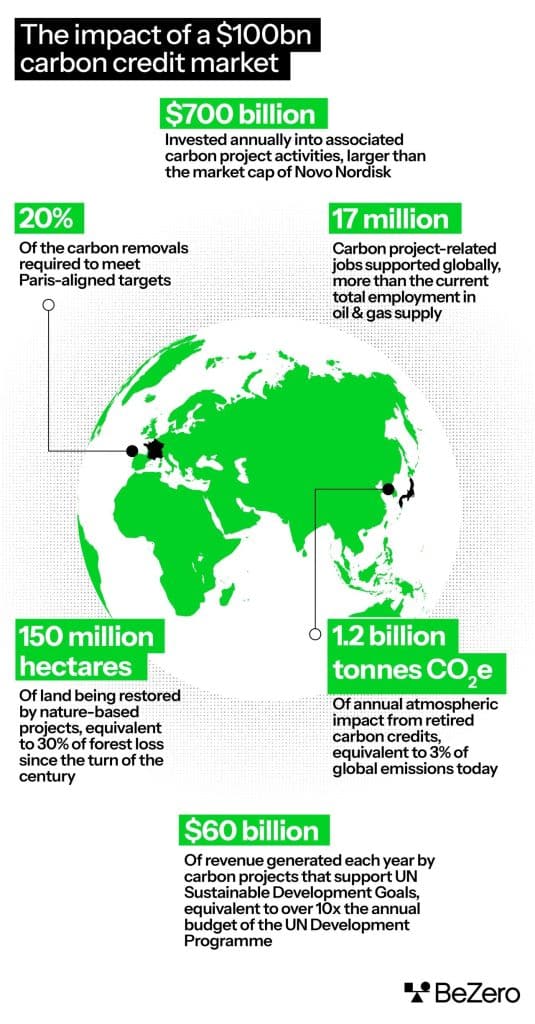

The voluntary carbon market reached a value of $2.52 billion in 2025 and is projected to grow to $100-250 billion by 2030, according to recent analyses.

This remarkable growth reflects increased corporate commitments to net-zero targets and growing investor interest in carbon markets. The market saw over 300 million carbon credits retired in 2024 (up significantly from 250 million traded in 2023). Preliminary 2025 data showing 280-350 million amid quality-driven demand surges.

Despite the difficulties, analysts agree that participation in the voluntary carbon market is growing rapidly. Even at the rate of growth depicted above, the VCM would still fall significantly short of the amount of investment required for the world to fully meet the targets set out by the Paris Agreement.

6. How to Produce Carbon Credits

Many different types of businesses can create and sell carbon credits by reducing, capturing, and storing emissions through different processes.

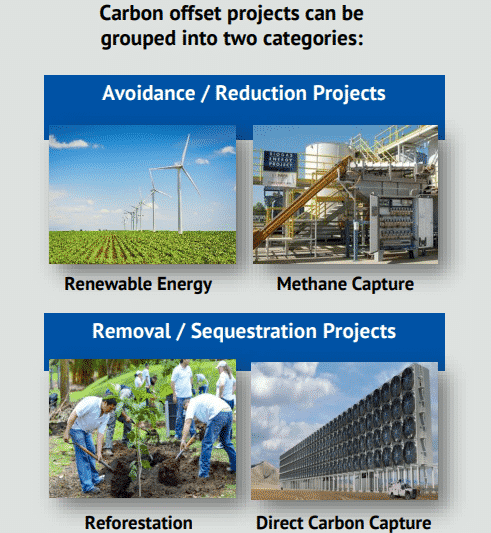

Some of the most popular types of carbon offsetting projects include:

Renewable energy projects,

Improving energy efficiency,

Carbon and methane capture and sequestration

Land use and reforestation.

Renewable energy projects have already existed long before carbon credit markets came into vogue. Many countries in the world are blessed with a natural wealth of renewable energy resources. Countries such as Brazil or Canada that have many lakes and rivers, or nations like Denmark and Germany with lots of windy regions. For countries like these, renewable energy was already an attractive and low-cost source of power generation, and they now provide the added benefit of carbon offset creation.

Energy efficiency improvements complement renewable energy projects by reducing the energy demands of current buildings and infrastructure. Even simple everyday changes like swapping your household lights from incandescent bulbs to LED ones can benefit the environment by reducing power consumption. On a larger scale, this can involve things like renovating buildings, optimizing industrial processes to make them more efficient, or distributing more efficient appliances to the needy.

Carbon and methane capture involves implementing practices that remove CO2 and methane (which is over 20 times more harmful to the environment than CO2) from the atmosphere.

Methane is simpler to deal with, as it can simply be burned off to create CO2. While this sounds counterproductive at first, since methane is over 20 times more harmful to the atmosphere than CO2, converting one molecule of methane to one molecule of CO2 through combustion still reduces net emissions by more than 95%.

For carbon, capture often happens directly at the source, such as from chemical plants or power plants. While the injection of this captured carbon underground has been used for various purposes like enhanced oil recovery for decades already, the idea of storing this carbon long-term, treating it much like nuclear waste, is a newer concept.

Land use and reforestation projects use Mother Nature’s carbon sinks, the trees and soil, to absorb carbon from the atmosphere. This includes protecting and restoring old forests, creating new forests, and soil management.

Plants convert CO2 from the atmosphere into organic matter through photosynthesis, which eventually ends up in the ground as dead plant matter. Once absorbed, the CO2-enriched soil helps restore the soil’s natural qualities – enhancing crop production while reducing pollution.

The carbon credit verification landscape has evolved with new standards emerging. Beyond established verifiers like Verra and Gold Standard, the Integrity Council for the Voluntary Carbon Market (IC-VCM) launched its Core Carbon Principles in 2024, setting new global threshold standards for high-quality carbon credits.

Likewise, the Science Based Targets initiative (SBTi) has also introduced enhanced verification protocols for corporate net-zero claims.

7. How Companies Can Offset Carbon Emissions

There are countless ways for companies to offset carbon emissions.

Though not a comprehensive list, here are some popular practices that typically qualify as offset projects:

Investing in renewable energy by funding wind, hydro, geothermal, and solar power generation projects, or switching to such power sources wherever possible.

Improving energy efficiency across the world, for instance, by providing more efficient cookstoves to those living in rural or more impoverished regions.

Capturing carbon from the atmosphere and using it to create biofuel makes it a carbon-neutral fuel source.

Returning biomass to the soil as mulch after harvest instead of removing or burning. This practice reduces evaporation from the soil surface, which helps to preserve water. The biomass also helps feed soil microbes and earthworms, allowing nutrients to cycle and strengthen soil structure.

Promoting forest regrowth through tree-planting and reforestation projects.

Switching to alternate fuel types, such as lower-carbon biofuels like corn and biomass-derived ethanol and biodiesel.

If you’re wondering how carbon offset and allotment levels are valued and determined through these processes, take a deep breath. Monitoring emissions and reductions can be a challenge for even the most experienced professional.

Know that when it comes to the regulated and voluntary markets, there are third-party auditors who verify, collect, and analyze data to confirm the validity of each offset project.

However, be careful when shopping online or directly from other businesses – not all offset projects are certified by appropriate third parties, and those that aren’t generally tend to be of dubious quality.

8. Voluntary vs Compulsory: The Biggest Difference Between Credits and Offsets

Participation in a cap-and-trade scheme typically isn’t voluntary. Your company either needs to abide by carbon credit limits set by regulators, or no such limits exist. As more and more countries adopt cap-and-trade programs, companies increasingly need to participate in carbon credit programs.

Carbon credits intentionally add an extra onus to businesses. In return, the best cap-and-trade programs provide a clear framework for reducing carbon emissions. Not all programs are created equal, of course, but at their best, carbon credits have a clear impact on total carbon emissions.

In contrast, carbon offsets are a voluntary market. No regulation mandates companies to purchase carbon offsets. Doing so is going above and beyond, particularly for companies operating where cap-and-trade programs don’t exist yet. Precisely for that reason, offsets provide a few advantages that credits simply don’t.

9. The Two Types of Global Carbon Markets: Voluntary and Compliance

There’s one more important distinction between carbon credits and carbon offsets:

Carbon credits are generally transacted in the carbon compliance market.

Carbon offsets are generally transacted in the voluntary carbon market.

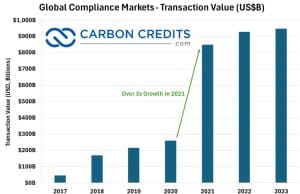

Global Compliance Market

The global compliance market for carbon credits is massive. According to Refinitiv, the market has grown substantially, reaching a trading value of approximately $1.5 trillion in 2024, up from $950 billion in 2023. This represents about 15.7Gt CO2 equivalent traded across various compliance markets worldwide.

The European Union Emissions Trading System (EU ETS) remains the largest market, followed by China’s national ETS.

Source: Katusa Research, Refinitiv, LSEG