A new peer-reviewed study suggests that most carbon offset programs have failed to deliver real reductions in greenhouse gas emissions. The study in the Annual Review of Environment and Resources (2025) finds that offsets, credits companies buy to offset their emissions, haven’t significantly slowed global warming.

The authors, led by climate scientist Joseph Romm, reviewed over ten years of data. They found that most offsets are tied to projects that would have occurred regardless. This means that many credits do not represent genuine emission reductions.

Carbon offsets are a cornerstone of corporate climate strategies. Despite billions in voluntary carbon markets (VCM), global carbon dioxide levels hit a record 424 parts per million in 2024, says the World Meteorological Organization. The study claims that offset systems, as they are now, provide more accounting ease than real benefits to the atmosphere.

Why Most Carbon Credits Miss the Mark

The paper identifies three main reasons why offsets have underperformed.

First, “additionality” — the idea that a project must only exist because of offset funding — is often not met. Many renewable energy and forest conservation projects would likely move forward without carbon credit revenue.

Another research from 2024 shows that about 87% of VCM offsets likely do not provide real and additional emission reductions. This widespread failure mainly comes from project designs that give too much credit to common renewable energy and forest conservation efforts. Many of these would have happened even without the projects.

Second, measurement and permanence are major issues. Forest-based credits account for about 40% of the voluntary carbon market. They can lose stored carbon due to wildfires, drought, or illegal logging. Studies cited in the review show that over 90% of forestry offsets examined failed to guarantee long-term carbon storage.

Third, double-counting remains common. Some emissions reductions are claimed by both the project developer and the host country, undermining integrity.

Some forest offset projects fail to consider leakage. This means emissions may shift to other places, leading to over-crediting. Similar estimates show that more than half of the offsets in different carbon markets may face double-counting or overstatement.

The result, according to Romm’s team, is that less than 10% of offsets on the market deliver genuine, measurable, and lasting emission cuts.

The Scale of the Problem: Billions in Doubt

The voluntary carbon market was once expected to reach $50 billion by 2030, driven by corporate net-zero pledges. But growth has slowed sharply since 2022, as buyers question credit quality and reputational risk increases.

Market value fell by more than 60% between 2022 and 2024, according to BloombergNEF. Major companies like Nestlé, Gucci, and EasyJet have reduced offset purchases. Instead, they are focusing on funding direct emission cuts in their operations.

Over 1.5 billion carbon credits are still in circulation. This accounts for over a billion tonnes of claimed emission reductions, despite the slowdown. The study warns that if these credits lack real-world carbon removal, they might delay climate action. This is because they create a false sense of progress.

Rebuild or Retreat? How the Carbon Market Fights for Credibility

The study’s findings have triggered strong reactions across the carbon market. Many organizations see the problems. They argue for reform instead of giving up.

The Integrity Council for the Voluntary Carbon Market (ICVCM) is an independent global group. In 2024, it launched its Core Carbon Principles (CCPs). These rules set minimum standards for quality, transparency, and permanence. ICVCM began approving credits that meet its criteria in 2025, with the goal of restoring buyer confidence.

Similarly, major registries like Verra and Gold Standard have updated their methodologies. Verra now requires projects to provide verified, real-time monitoring data. They must also account for climate risks like fire and deforestation.

Gold Standard has shifted its focus from offsets to “climate contributions.” This change pushes companies to invest more in reducing emissions, not just compensating for them.

Industry experts noted that the industry must “shift from quantity to quality.” They emphasized that strong verification systems and independent audits can help rebuild trust.

Even governments are stepping in. At COP30 in Belém, Brazil (2025), negotiators plan to finalize the global rules for carbon trading under Article 6 of the Paris Agreement. These rules will define how international credits can be traded without double-counting.

Examples of New Approaches

Some initiatives are emerging to fix long-standing issues.

- Technology-based removals: Startups like Climeworks and Charm Industrial are producing credits based on direct air capture and bio-oil sequestration. These methods store carbon permanently, though they remain costly — up to $600 per tonne.

- Jurisdictional forest programs: Countries like Indonesia and Gabon are piloting large-scale carbon programs that use satellite monitoring to ensure transparency.

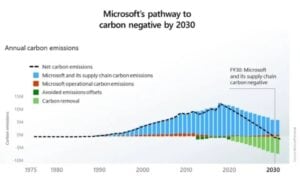

- Corporate reform: Companies like Microsoft and Delta Air Lines will only buy credits from projects that show real, lasting carbon removal. They won’t focus on avoided emissions anymore.

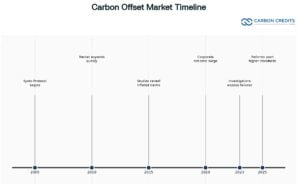

These changes show a shift from offsetting emissions to removing carbon. This aligns better with science-based targets. The timeline below shows major developments in the carbon offset market.

What the Data Really Says About Climate Accounting

The Annual Review study makes a clear recommendation: carbon offsets should no longer be used as a substitute for direct emission cuts. Instead, they can play a role in funding innovation or supporting communities during the transition.

Romm and his team say that governments need to stop using low-quality offsets. They also want strict global oversight. They warn that without reform, carbon markets may face the same credibility issues. This could lead to public backlash like the one seen in 2023 and 2024.

Still, the authors acknowledge that offset mechanisms can evolve. “Offsets could help if they fund projects that remove carbon permanently and are verified transparently,” the paper notes.

Beyond Offsets: Toward a Stronger and More Honest Market

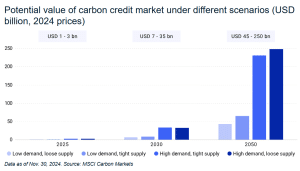

Despite criticism, few expect the voluntary carbon market to disappear. Instead, it is likely to become smaller but more credible. BloombergNEF analysts estimate that a strong market could hit $30 billion each year by 2035. Also, the MSCI forecasts it could reach up to $35 billion in 2030. This growth will come from verified carbon removals and compliance-linked credits.

The broader transition is also creating new demand for accountability. Investors, regulators, and consumers want companies to show how they verify offsets. They also want to see how these offsets fit into long-term plans for reducing carbon emissions.

The Integrity Council’s certification process and the UN’s Article 6 rules are expected to shape the next decade of carbon trading. They could remove low-quality projects and direct funding to real climate solutions.

The study delivers a tough message: the world cannot buy its way out of the climate crisis. Offsets, as they exist today, have not slowed global warming. The new wave of reforms shows that transparency and integrity might make carbon markets part of the solution.

For now, the future of offsets depends on whether companies, investors, and regulators can rebuild trust, shifting from promises on paper to real-world carbon reduction and removal.

Stock Rises on Record Quarter: Growth, Green Goas, and the Road Ahead")