Gevo, a developer of net-zero hydrocarbon fuels, has inked a deal to acquire Red Trail Energy’s ethanol production plant and carbon capture and sequestration (CCS) assets for $210 million. This strategic purchase aligns with Gevo’s mission to expand its sustainable fuel production capabilities. The move could play a crucial role in making the company’s earnings to be positive by 2025 and produce more renewable fuels.

Strengthening the Path to Net Zero

Gevo seeks to transform renewable energy and biogenic carbon into sustainable fuels and chemicals with a net-zero carbon footprint. Its technology produces various products, including sustainable aviation fuel (SAF), motor fuels, chemicals, and other materials.

SAF refers to various biofuels and synthetic fuels proposed as jet fuel alternatives. While SAF still produces tailpipe emissions, these are offset by a carbon-negative production process.

The Colorado-based company currently operates one of the largest dairy-based renewable natural gas (RNG) facilities in the U.S. and owns the world’s first alcohol-to-jet (ATJ) fuels and chemicals production facility. Through its Verity subsidiary, Gevo tracks and verifies the carbon footprint of its operations to ensure sustainability.

The acquisition includes Red Trail Energy’s ethanol production and CCS assets, which, when combined with Gevo’s renewable natural gas (RNG) business and other ventures like Verity, are projected to turn Gevo’s earnings positive in 2025.

Gevo CEO Patrick Gruber remarked on this achievement, saying that:

“This acquisition of Red Trail puts on the path of profitability, we believe, in advance of our Net-Zero 1 project’s commercial operation.”

This purchase marks a significant step for Gevo in boosting its revenue streams and enhancing shareholder value. The integration of carbon abatement with advanced liquid fuel production could strengthen Gevo’s market position in the renewable energy sector.

Expanding Sustainable Aviation Fuel (SAF) Production

Gevo aims to leverage this acquisition to support its Net-Zero 1 SAF project in Lake Preston, South Dakota. The Red Trail Energy facility offers a “Net-Zero” site that will facilitate future production of sustainable aviation fuel (SAF) with a low-carbon footprint.

The site is strategically located to serve both the U.S. and Canadian markets. It provides Gevo with a wholly-owned CCS asset and additional supply of low-carbon intensity (CI) ethanol.

Gevo plans to use the site’s existing infrastructure to expand into alcohol-to-jet (ATJ) SAF production, capitalizing on the available low-carbon ethanol and defossilized energy. The ethanol plant has a production capacity of 65 million gallons per year. Thus, it strengthens Gevo’s supply chain, enabling the company to meet growing demands for renewable fuels.

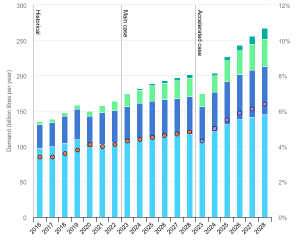

According to the International Energy Agency, renewable or biofuel demand will grow by 38 billion liters from 2023 to 2028. That’s almost a 30% increase from the previous five years.

Global biofuel demand, historical, main and accelerated case, 2016-2028

By 2028, total biofuel demand will reach 200 billion liters. Renewable diesel and ethanol will drive ⅔ of this growth, while biodiesel and biojet fuel account for the rest.

CCS Site: A Game-Changer for Gevo’s Carbon Strategy

One of Gevo acquisition’s key features is the Red Trail Energy’s CCS site. It has been operational since 2022 and currently captures 160,000 metric tons of carbon annually.

The site has the potential to sequester up to 1 million metric tons per year, offering considerable expansion opportunities for Gevo’s future net zero projects. The CCS facility generates monetizable tax credits under Section 45Q of the tax code, contributing additional revenue streams for Gevo. Currently, the plant uses less than 20% of its capacity, allowing room for future projects.

Gevo has also enlisted Summit Carbon Solutions to transport CO2 from the Lake Preston plant to another storage site in North Dakota. However, Summit faces challenges in obtaining state permits for its carbon capture and storage hub, which involves multiple biofuel plants across five Midwestern states.

Many carbon capture projects have been stuck for years in the U.S. Environmental Protection Agency’s permitting queue for Class VI wells, used to inject CO2 underground. However, the process is faster in North Dakota, one of only three states authorized by the EPA to manage carbon storage independently.

Situated on 5,800 acres in the Broom Creek formation, the Red Trail Energy site provides ample pore space for long-term carbon storage. This large capacity allows Gevo to produce defossilized energy and steam, essential components for net-zero fuels and chemicals.

The ethanol producer not only sells low-carbon fuel but also generates carbon offsets by growing corn to capture CO2 and then capturing and burying emissions from the refining process.

Clearing the Path to Completion

Gevo expects the acquisition to close by the first quarter of 2025, subject to regulatory approvals and approval from Red Trail Energy’s equity holders. To finance the transaction, the company plans to use a mix of asset-level debt and cash from its balance sheet.

Most recently, the American renewables company announced that the U.S. Patent and Trademark Office has granted a patent for its ethanol-to-olefins (ETO) process. This patent strengthens Gevo’s position as a leader in intellectual property for bio-based renewable fuel and chemical production from alcohols.

This milestone is vital for the company’s mission to make the transition from fossil-based to renewable fuels and chemicals practical. The ETO process technology covered by this patent represents a significant improvement in capital cost and energy efficiency for producing biofuels like SAF.

- FURTHER READING: Google Signs Up Shell’s SAF Program to Cut Business Travel Emissions

Acquiring Red Trail Energy is a critical step in Gevo’s strategy to expand its renewable fuel portfolio, providing both immediate financial benefits and long-term growth potential in the low-carbon energy market.