A U.S. federal judge has dismissed a proposed class-action lawsuit accusing Apple of misleading consumers with “carbon neutral” marketing for several Apple Watch models. The case targeted the Apple Watch Series 9, Apple Watch SE, and Apple Watch Ultra 2. Plaintiffs said the company exaggerated the environmental benefits of the watches. They claimed Apple relied on carbon offset projects that did not truly cancel the products’ emissions.

Seven buyers filed the lawsuit in February 2025 in federal court in California. They argued they would not have bought the watches, or would have paid less, if they knew the details of Apple’s carbon accounting.

In February 2026, U.S. District Judge Noël Wise dismissed the case. The court ruled the complaint lacked strong evidence showing Apple’s carbon-neutral claims were false or misleading. Wise said:

“At this juncture, the court has a narrow question to consider: have plaintiffs plausibly alleged that Apple’s claims of carbon neutrality are false? Because the court finds that the answer to that question is no, Apple’s motion to dismiss is granted.”

The ruling gives Apple an early legal win. But it also highlights growing scrutiny of corporate climate marketing.

How Apple Calculates a “Zero-Emission” Watch

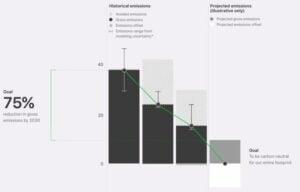

Apple launched its first carbon-neutral devices in September 2023. The company said the Apple Watch models achieved neutrality through a mix of emissions reductions and carbon offsets.

For example, Apple estimates the lifecycle carbon footprint of a carbon-neutral watch model at about 8.1 kg of CO₂-equivalent emissions per device before offsets. After applying carbon credits, Apple says the net footprint becomes 0 kg CO₂e.

The tech giant says it lowers emissions by:

using recycled materials,

increasing renewable electricity in manufacturing,

improving product efficiency, and

reducing shipping emissions.

Any remaining emissions are offset through environmental projects.

The lawsuit challenged two offset projects tied to Apple’s claims. One project protects forests in Kenya’s Chyulu Hills, while another supports reforestation efforts in China. Critics argued such projects may not always deliver additional carbon reductions.

The court did not rule on the scientific debate over offsets. Instead, it said the plaintiffs failed to show Apple’s claims were clearly deceptive.

The Tech Giant’s 2030 Net-Zero Roadmap

Apple’s carbon-neutral watches are part of a larger climate plan known as “Apple 2030.” The company aims to make its entire business, supply chain, and product lifecycle carbon neutral by 2030.

Source: Apple

The iPhone maker has made progress toward that goal. The company says its global greenhouse gas emissions have fallen by more than 60% compared with 2015 levels.

In 2024, Apple reported a total carbon footprint of about 16.5 million metric tons of CO₂-equivalent emissions across its operations and supply chain. That figure represented a decline from the previous year.

Source: Apple

Most of Apple’s emissions come from Scope 3 sources, including manufacturing and product use. To address that, it works closely with suppliers. The company reports that 17.8 gigawatts of renewable electricity are now operating in its global supply chain. Those projects helped avoid about 21.8 million metric tons of greenhouse gas emissions in 2024 alone.

Apple has also increased recycled materials in its products. About 24% of the materials used in Apple devices in 2024 came from recycled or renewable sources. These efforts are central to the company’s climate strategy.

Greenwashing on Trial: Climate Claims Face Legal Tests

Even though Apple won the U.S. case, climate lawsuits are rising worldwide. Greenwashing claims typically challenge marketing statements such as:

“carbon neutral”

“net zero”

“climate friendly”

These terms can involve complex carbon accounting that consumers may not fully understand.

Apple has faced legal pressure outside the United States as well. A court in Frankfurt, Germany ruled in 2025 that Apple could not advertise the Apple Watch as “CO₂-neutral” in Germany. The court said the claim could mislead consumers under local competition law.

European regulators are also tightening rules on environmental claims. New EU consumer protection rules will restrict vague labels like “carbon neutral” in advertising beginning in 2026. These legal developments could reshape how companies communicate climate progress.

Big Tech Emissions: Clean Energy vs. Rising Power Demand

The Apple case reflects a larger trend in the technology sector. Tech companies are under growing pressure to cut emissions as demand for digital services rises.

Data centers, cloud computing, and artificial intelligence require massive amounts of electricity. As a result, technology firms are investing heavily in renewable energy and carbon removal projects.

Apple’s progress contrasts with some peers whose emissions have risen due to expanding AI infrastructure. Apple still emitted about 15.3 million metric tons of CO₂ in 2024, but that figure is far below its 2015 baseline of 38.4 million tons.

At the same time, clean energy adoption is growing globally. The rapid expansion of renewable power also supports other low-carbon industries, including electric vehicles.

Companies such as Tesla rely heavily on the decarbonization of electricity systems. The climate benefit of electric cars increases when power grids shift toward renewable energy.

Global electric vehicle adoption is rising quickly. According to the International Energy Agency, EVs represented about 20% of global car sales in 2024, compared with 18% in 2023 and just 4% in 2020. That growth is expected to continue as governments strengthen climate policies and consumers adopt cleaner transportation.

Technology companies and automakers both depend on credible climate strategies to maintain investor confidence.

The Role of Carbon Credits in Corporate Climate Plans

Carbon credits remain a key tool for many companies pursuing net-zero goals. Apple increased its use of carbon credits in 2024, retiring about 737,100 tons of CO₂-equivalent offsets—its highest level to date.

However, the quality of carbon credits has become a major issue in climate policy.

Some researchers argue that certain nature-based credits may overestimate their climate impact. Others say these projects are essential for protecting ecosystems and funding conservation. The debate is likely to intensify as more corporations adopt net-zero targets.

A Legal Win, but Climate Claims Under the Microscope

Apple’s victory in the U.S. greenwashing lawsuit marks an important moment in the evolving field of climate litigation. The court ruled that the plaintiffs did not present enough evidence to prove the tech giant’s carbon-neutral claims were misleading.

However, the case also shows how closely corporate climate messaging is now examined. Companies across technology, energy, and transportation sectors face growing pressure to show real emissions reductions and transparent reporting.

As the clean-energy transition accelerates, and industries from consumer electronics to electric vehicles expand, clear standards for climate claims will become increasingly important.

For Apple and other global companies, the challenge is not only reducing emissions but also proving those reductions in ways that stand up to scientific, legal, and public scrutiny.

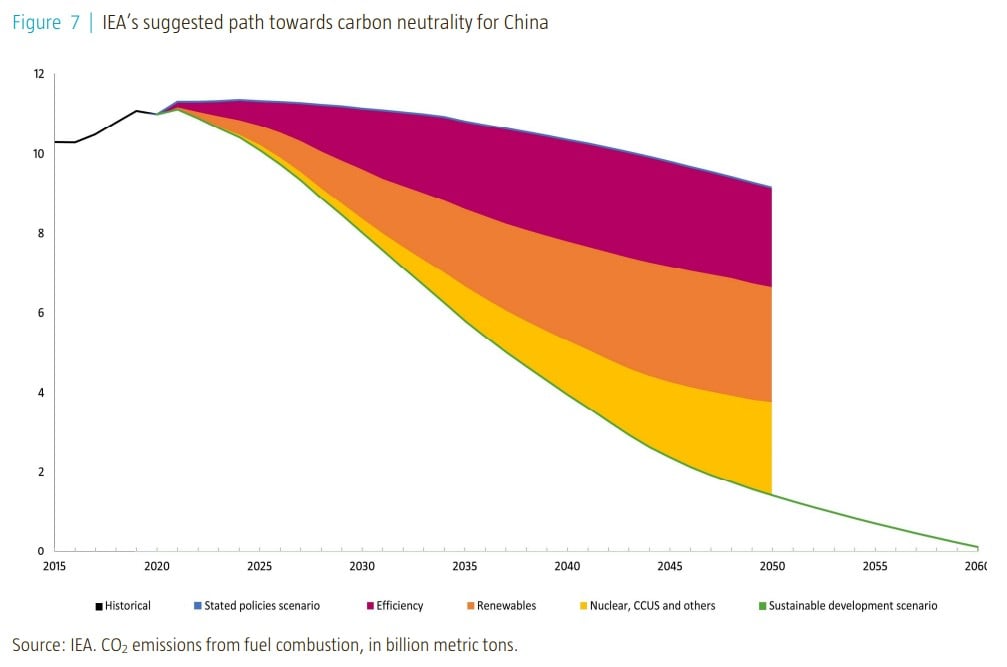

China has released updated climate goals for the period leading to 2030, framed as part of its 15th Five‑Year Plan (2026–2030). These goals focus mainly on improving carbon efficiency, that is, lowering emissions relative to economic output, rather than capping total emissions.

Under the new plan, China aims to reduce carbon dioxide (CO₂) emissions per unit of gross domestic product (GDP) by 17% between 2026 and 2030. The immediate 2026 target is to cut carbon intensity by about 3.8% from the prior year.

The world’s largest emitter has not announced a new absolute cap on total CO₂ emissions for 2030. This means emissions could still rise in total even as the economy becomes more efficient. That cautious tone has drawn attention from analysts.

Norah Zhang, China country lead for Climate Action Tracker, remarked:

“In 2025, renewable electricity generation in China grew faster than overall electricity demand, which helped reduce coal-fired power generation and lowered CO₂ emissions in the power sector. However, the new five-year plan does not update the 2030 target for newly-installed solar and wind capacity, which China already achieved in 2024. By not updating these targets, the new plan misses an opportunity to create additional momentum through more ambitious goal setting for 2030 and beyond.”

What the New Targets Mean in Practice

China has long said it will peak carbon emissions before 2030 and achieve carbon neutrality by 2060 — often called its “dual‑carbon” goals under the Paris Agreement. However, the new 2030 plan places greater emphasis on intensity improvements rather than absolute reductions.

China’s updated climate strategy reflects a balance between economic growth and emissions control. The plan includes a GDP growth target of 4.5–5% for 2026, suggesting the government expects continued industrial expansion. But this raises the possibility that total CO₂ emissions could climb even as carbon intensity improves.

The new plan also prioritizes energy transition actions, such as:

Replacing ~30 million tonnes of coal per year with renewables

Setting up a low‑carbon transition fund and energy storage build‑outs

However, the absence of an absolute emissions cap means China’s total carbon output may still grow if economic expansion is strong.

China’s Global Emissions Weight: Why It Matters

China is the world’s largest emitter of greenhouse gases, accounting for roughly 30% of global CO₂ emissions. Most studies suggest that the country’s emissions will peak between 2027 and 2030 with a peak between 11.6 and 13.2 gigatonnes of CO₂ equivalent (GtCO₂e) under current policy trajectories.

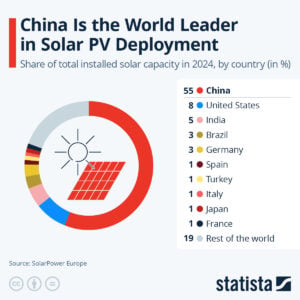

China’s transition has been supported by rapid renewable energy growth. China accounts for more than half of global solar panel production and is a global leader in wind and solar deployment.

Growth in clean energy helped fossil fuel use fall by an estimated 2% in 2025, and renewable sources met about 84% of electricity demand growth, according to independent analysis. This trend is expected to make global fossil fuel demand begin to decline by 2030 if current energy shifts hold.

China is also the world’s largest electric vehicle (EV) market. The country plays a major role in EV adoption, and its policies can shape global trends, including demand for vehicles from companies like Tesla.

The Asian nation’s 2030 goals indirectly influence EV demand. Strong efficiency and clean energy targets can make EVs more attractive versus traditional combustion cars by lowering emissions from electricity generation. EVs reduce local pollution and align with both national and global climate ambitions.

Tesla has been expanding in China, including with the Gigafactory Shanghai that supplies vehicles domestically and for export. China’s EV market is projected to grow further, supported by urban electrification policies and consumer incentives.

However, policies that rely mainly on carbon intensity reductions — as opposed to absolute emissions limits — may slow the pace of structural changes needed to fully decarbonize transport and power sectors. Still, China’s rising clean electricity share helps strengthen the climate case for EV adoption by lowering the lifecycle emissions of electric vehicles.

Broader Market Trends, Forecasts, and Investment Signals

China’s cautious climate plan comes amid shifting global policy dynamics. While many countries are enhancing climate targets, some have pulled back from earlier commitments. For example, changes to U.S. federal climate policy have created uncertainty in long‑term emissions strategies.

As of late 2025, around 145 countries had announced or were considering net‑zero targets, covering about 77% of global greenhouse gas emissions. China remains a key driver in this global push.

Source: Climate Action Tracker

In carbon markets, China has also taken steps to expand its emissions trading system (ETS). Recent policy outlines suggest broader coverage of sectors and possibly higher stringency in future phases. This could help drive cleaner investments and offer market signals to investors and companies.

Renewable energy and clean tech markets may benefit from China’s cautious but steady approach. The country’s demand for solar panels, batteries, and wind equipment can sustain supply chains and keep manufacturing costs down globally — benefiting EV makers and green tech firms alike.

Ambition vs. Reality: Tracking China’s Climate Trajectory

Despite progress in clean energy, challenges remain. China has not set a firm limit on total emissions through 2030, and coal consumption continues to play a major role in power generation. The reliance on carbon intensity targets means that total emissions may grow if GDP expands faster than emissions decline per unit of output.

To stay aligned with Paris Agreement goals, many analysts believe stronger absolute cuts are needed. Independent research suggests that China could reduce emissions by up to 30% by 2035 relative to current levels with more ambitious policy action.

However, the current 2030 plan keeps a cautious balance between economic growth and climate policy. The country aims to improve carbon efficiency and expand clean energy, but stops short of committing to cuts in total emissions. These targets are part of its long‑term plan to peak emissions before 2030 and achieve carbon neutrality by 2060.

For markets and companies like Tesla, China’s climate strategy will continue to matter. As the largest EV market and a leader in clean energy production, China’s demand trends and policy frameworks shape global investment and manufacturing patterns.

The cautious tone of China’s new climate goals shows a complex trade‑off between growth and climate action. Whether China will accelerate its ambition before 2030 remains a key question for global decarbonization and the broader energy transition.

Cameco has signed a major long-term uranium supply agreement with India. The Canadian uranium giant will deliver nearly 22 million pounds of uranium ore concentrate (U3O8) to India over nine years. The contract is valued at about $2.6 billion.

Deliveries will begin in 2027 and continue through 2035. The uranium will power India’s growing fleet of nuclear reactors. The agreement strengthens energy ties between Canada and India at a time when nuclear power is gaining fresh momentum worldwide.

A Strategic Boost for India–Canada Relations

The agreement was celebrated in New Delhi in the presence of Narendra Modi, Mark Carney, and Saskatchewan Premier Scott Moe. Carney’s 2026 visit marked a reset in India–Canada relations.

As we have read and heard earlier, diplomatic ties have been strained in recent years. However, both leaders described this visit as the start of a “new era of partnership.”

The uranium deal was one of the key outcomes of the visit. In addition, both countries renewed efforts to finalize a Comprehensive Economic Partnership Agreement (CEPA) by the end of 2026.

India and Canada also set a bold trade target. They aim to increase bilateral trade to $50 billion by 2030, up from nearly $9 billion in 2024–25.

Both sides agreed to deepen cooperation in:

Critical minerals

Renewable energy

Energy security

Advanced nuclear technologies, including SMRs

This uranium agreement fits directly into that broader economic and strategic framework.

India’s Nuclear Ambitions and Uranium Demand

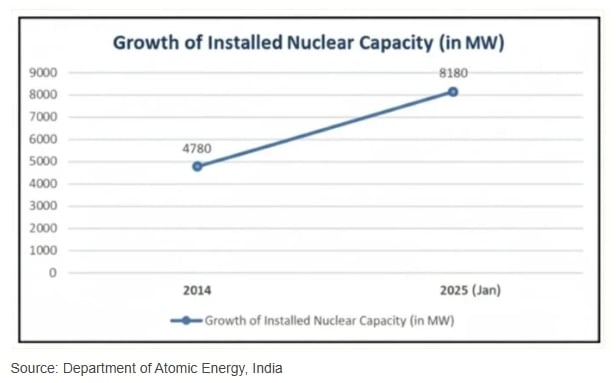

India currently operates 24 nuclear reactors. However, the country has much larger plans. Under its long-term energy roadmap, India aims to reach 100 gigawatts (GW) of nuclear capacity by 2047.

The Union Budget 2025–26 placed nuclear energy at the center of this strategy. The government launched the Nuclear Energy Mission for Viksit Bharat. This mission focuses on expanding nuclear capacity, cutting fossil fuel use, and boosting energy security.

A key part of the plan is the development of small modular reactors (SMRs) that are smaller, more flexible, and easier to deploy. They can power remote regions and replace retiring coal plants.

The government has allocated $2.4 billion to build at least five indigenously designed SMRs by 2033. This move signals strong policy backing for advanced nuclear technology.

As electricity demand rises due to industrial growth and data centers, nuclear power offers a stable, round-the-clock, low-carbon energy source. Therefore, securing a long-term uranium supply is critical for India’s expansion goals.

For Cameco, the deal aligns perfectly with its disciplined contracting model. The company avoids chasing short-term spot fces. Instead, it focuses on securing long-term contracts with reliable customers.

By the end of 2025, Cameco had about 230 million pounds of uranium under long-term contracts. This provides strong revenue visibility for years.

The new India agreement was already included in the company’s disclosed long-term contracting volumes and price sensitivity analysis. The estimated $2.6 billion value is based on a uranium price of $86.95 per pound, reflecting late February 2026 spot price averages.

Uranium: The Backbone of Cameco’s Business

In 2025, the company reported strong financial results. Earnings before income tax in the uranium segment rose by $50 million year over year. Adjusted EBITDA increased by $76 million.

Source: Cameco

Although fourth-quarter earnings dipped slightly due to sales timing, underlying pricing remained strong. But operationally, Cameco delivered solid production results:

At Cigar Lake, production reached 19.1 million pounds (100% basis), exceeding annual expectations.

At McArthur River/Key Lake, production totaled 15.1 million pounds, meeting revised guidance.

Average realized uranium prices improved as market-linked and escalated contracts reflected higher pricing.

Source: Cameco

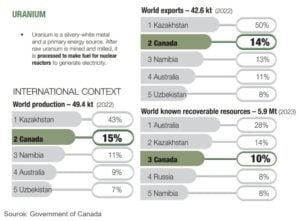

Canada’s Expanding Uranium Role

Canada is one of the world’s leading uranium producers. Saskatchewan hosts some of the richest uranium deposits globally. Major mines such as Cigar Lake, McClean Lake, and Rabbit Lake have supplied uranium for decades. Recently, Canada approved its first large-scale uranium mine in over 20 years.

The federal and provincial governments cleared the Phoenix In Situ Recovery (ISR) uranium project. This project is part of Denison Mines’ Wheeler River development in Saskatchewan. Approval allows the construction of both the mine and its processing facilities.

This decision signals Canada’s commitment to supporting global nuclear growth. As more countries expand nuclear capacity, demand for a secure uranium supply continues to rise.

A Deal With Long-Term Impact

Around the world, nuclear energy is regaining policy support. Countries are seeking reliable, low-carbon power to meet climate targets and rising electricity demand. India stands out as one of the fastest-growing nuclear markets. Its target of 100 GW by 2047 represents a massive expansion from current levels.

To reach that goal, India will need a steady uranium supply, new reactor builds, and strong international partnerships. The Cameco deal addresses one key piece of that puzzle: fuel security.

Overall, this agreement goes beyond a simple supply contract. It reflects deeper economic and strategic alignment between the two major democracies. While India secures uranium to power its future reactors, Canada strengthens its role in the global nuclear fuel market. Meanwhile, bilateral trade and diplomatic ties gain fresh momentum.

As nuclear energy returns to the global spotlight, long-term fuel partnerships will become even more important. In that context, Cameco’s $2.6 billion agreement with India marks a decisive step toward a more secure and low-carbon energy future for both nations.

Google has announced a new climate finance commitment. The company pledged $50 million by 2030 to fund projects that aim to eliminate superpollutants. These are greenhouse gases (GHGs) that heat the atmosphere much faster than carbon dioxide (CO₂) .

Google said it will work alongside other corporations in a collective effort called the Superpollutant Action Initiative. In total, participating companies have committed $100 million to this cause.

Short-lived GHGs include methane, fluorinated gases like hydrofluorocarbons (HFCs), and black carbon. These gases trap heat in the atmosphere far more effectively than CO₂ in the short term, making them a key target for near-term climate action.

“As we continue to support superpollutant elimination projects, we’ll ensure our impact is catalytic and accurately measured and pave the way for additional companies and governments to follow. Since common superpollutants like methane are shorter lived than CO2, taking action against them helps address near-term rather than long-term warming, complementing our ongoing carbon removal efforts.”

What Are Superpollutants and Why They Matter

Superpollutants are greenhouse gases with high global warming potential (GWP). This means that each ton of these gases can trap much more heat in the atmosphere than a ton of CO₂.

Methane (CH₄), for example, warms the planet about 80 times more than CO₂ over a 20-year period. Other short-lived GHGs, such as HFCs used in refrigeration, can be thousands of times more potent per ton than CO₂.

Unlike CO₂, which can stay in the atmosphere for centuries, many short-lived GHGs break down much faster. Reducing them can deliver significant cooling benefits in the near term due to their high potency and short lifespan.

Scientists say that superpollutants, like methane and black carbon, cause almost half of all global warming observed so far.

Source: IPCC

How Google’s Bold Pledge Fits Into Broader Climate Goals

Google will spend $50 million to fund projects that remove short-lived GHGs worldwide by 2030. The company plans to back initiatives that make a real difference for the climate. It also aims to help more companies and governments take similar steps.

The pledge focuses on both methane and fluorinated gases, which come from sources such as:

landfills and waste operations

refrigeration and air-conditioning systems

industrial leaks and fuel systems

This funding boosts the tech giant’s climate work. It includes buying carbon removal and investing in clean energy.

Source: Google

The company aims to reach net‑zero emissions across all operations and its supply chain by 2030. This includes running on carbon‑free energy 24/7 and cutting emissions from data centers, offices, and supply chains.

By 2024, Google’s data centers ran on an average of 64% carbon‑free energy, even as electricity use grew 27% due to AI and other services. The company has also avoided 44 million tonnes of CO₂-equivalent emissions since 2011 through renewable energy and efficiency measures.

Source: Google

In 2024, Google added 2.5 GW of clean energy from new projects and signed contracts for 8 GW more, the largest annual total in its history. These projects include geothermal and nuclear SMRs in Asia and the U.S.

The $50 million superpollutant pledge complements these efforts. Reducing superpollutants gives fast climate benefits while Google continues long-term CO₂ reductions and clean energy expansion.

Partnership Power: Corporates Team Up for Global Impact

Google is not acting alone. A group of top global companies, including Amazon, Salesforce, Autodesk, Figma, JPMorgan Chase, and Workday, launched the Superpollutant Action Initiative with Google. They will invest $100 million through 2030 to reduce superpollutants.

The initiative will fund high-impact projects worldwide that cut these short-lived but potent pollutants. The goal is to deliver climate, health, and economic benefits while accelerating progress where it’s most needed.

The tech giant has also signed partnerships with third‑party organizations that focus on reducing these planet-warming GHGs.

In 2025, Google teamed up with Recoolit and Cool Effect. Their goal is to cut over 25,000 tons of superpollutants by 2030. These partnerships focus on capturing and destroying harmful gases. This includes HFCs from cooling systems in Indonesia and methane from landfills in Brazil.

Recoolit, an Indonesian company, has partnered with Google. They will sell 250,000 carbon credits. These credits come from destroying refrigerant gases found in HVAC systems.

Moreover, Google and its partners backed a project with Vaulted Deep. This project aims to permanently remove 50,000 tonnes of CO₂ and methane emissions. They use technology that injects organic waste underground for storage.

The tech giant’s partnerships aim to reduce superpollutants. They also strengthen the science behind measuring and certifying these efforts.

Near‑Term Impact, Long‑Term Strategy

Climate scientists emphasize that reducing the pollutants can produce rapid climate benefits. Because these gases are potent but short‑lived, cutting them can slow warming quickly, within years rather than decades.

Analysts and climate assessments show that cutting methane quickly can slow warming. Some studies suggest that strong reductions could lower global temperature rise by about 0.4–0.5 °C by 2050. This is compared to a scenario without these cuts.

Source: Global Methane Initiative

A peer-reviewed study found that cutting global methane by 40% by 2050 could lower warming by about 0.4 °C by mid-century. Bigger reductions might push this down to 0.5 °C during that time.

Superpollutant mitigation also has public health benefits. Methane and black carbon contribute to ground‑level ozone and air pollution, which can cause respiratory and cardiovascular issues. Cutting them can improve local air quality while also addressing climate change.

Google and its partners plan to track and report the impact of funded projects regularly. The Superpollutant Action Initiative will work with scientists and research groups. They aim to create global plans to boost action.

Markets and Money: Carbon Credits Meet Corporate Action

Google’s pledge comes at a time of rising corporate climate commitments worldwide. Many companies are boosting their spending on carbon credits. They are also investing in carbon removal technologies and emissions measurement tools.

Many corporate climate efforts aim to cut CO₂ emissions. However, superpollutants are now in the spotlight. Reducing them can quickly improve the climate, while also supporting long-term CO₂ strategies.

Compliance systems like emissions trading schemes now also recognize the role of powerful greenhouse gases beyond carbon dioxide.

Google teaming up with big companies shows that corporate collaboration on climate issues is increasing. This group aims to scale funding and knowledge sharing on superpollutants at a global level.

A Tactical Move for Near‑Term Climate Impact

Google’s $50 million pledge to reduce the GHGs through 2030 highlights a growing focus on near-term climate action.

Superpollutants, though short-lived, have outsized warming effects that make them a critical target for climate mitigation. Google and its partners fund elimination projects and work with experts and non-profits. They aim to speed up progress on global warming beyond what CO₂ reductions can achieve alone.

This initiative also reflects corporate climate strategy trends. As markets for carbon credits and climate solutions expand, companies are committing capital and resources beyond traditional carbon focus areas. In doing so, they aim to bring scalable, measurable progress in areas that can deliver both immediate and long-lasting climate benefits.

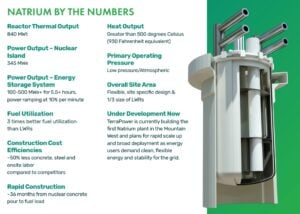

The United States took a major step toward the next generation of nuclear energy after the U.S. Nuclear Regulatory Commission approved a construction permit for TerraPower’s first Natrium reactor.

The permit allows the company to begin building Kemmerer Unit 1, a commercial-scale advanced nuclear power plant in Wyoming. Notably, this is the first advanced reactor project in the U.S. to receive such approval, marking an important milestone for the future of clean energy and nuclear innovation.

Developed by TerraPower in partnership with GE Vernova Hitachi Nuclear Energy, the Natrium system combines a 345-megawatt sodium-cooled fast reactor with a molten salt energy storage system. The project is also supported through the U.S. Department of Energy Advanced Reactor Demonstration Program.

With regulatory approval secured, TerraPower plans to begin construction within weeks and aims to complete the plant by 2030.

A Long Regulatory Journey Reaches a Breakthrough

Securing approval for a new nuclear design is a rigorous and lengthy process. TerraPower spent more than four years working closely with regulators to reach this stage.

The company first engaged with the NRC through extensive pre-application consultations. These discussions helped refine the reactor’s design and ensured regulators fully understood the new technology. TerraPower then submitted its official construction permit application in March 2024, and the NRC formally accepted the filing in May 2024.

Initially, the regulator expected the review process to take 27 months. However, the timeline moved faster than anticipated.

Several factors helped accelerate the review:

TerraPower submitted a comprehensive technical application.

The company responded quickly to regulator questions.

NRC staff prioritized the project’s review.

Federal policies encouraged faster licensing of advanced reactors.

As a result, the approval process finished in 18 months, making it one of the fastest regulatory reviews for a new nuclear technology in the United States.

This milestone positions TerraPower as a first mover in the advanced reactor market, which many experts see as essential for meeting future energy demand while reducing emissions.

Natrium: A New Kind of Nuclear Reactor

Unlike traditional nuclear plants, the Natrium system uses sodium instead of water as its coolant. This design change brings several operational advantages.

Source: TerraPower

Most existing nuclear facilities rely on light water reactors, which operate under high pressure. In contrast, the Natrium reactor runs at low pressure and high temperatures, reaching more than 350°C (662°F) while remaining far below sodium’s boiling point.

Because of this design, the reactor can rely on natural forces such as gravity and thermal convection for cooling. This passive safety approach reduces the need for complex emergency systems and lowers construction costs.

Another key innovation is the plant’s integrated energy storage system.

The reactor continuously produces 345 megawatts of electricity, ensuring stable baseload power. Meanwhile, molten salt storage can hold excess heat and release it later to boost output to 500 megawatts during periods of high demand.

Instead of running at a constant power level like traditional nuclear plants, the system can adjust electricity production based on grid needs. That flexibility allows it to complement renewable energy sources such as wind and solar.

Thus, this capability makes the Natrium plant unique among advanced reactor designs.

In addition, the design separates the nuclear reactor from the energy storage and power generation systems. This “decoupling” means non-nuclear teams can operate components such as steam turbines and salt tanks outside the nuclear island, improving safety while reducing operational costs.

Supporting Decarbonization Beyond Electricity

The Natrium plant is designed to deliver more than just electricity.

Because the reactor produces high-temperature heat, it can also supply industrial steam and thermal energy. This opens opportunities to decarbonize sectors that are traditionally difficult to electrify, including heavy industry and manufacturing.

The technology can therefore support multiple applications:

With an expected operational life of up to 80 years, the Natrium system could provide reliable low-carbon energy for decades.

Nuclear Power’s Role in America’s Energy Strategy

The approval of TerraPower’s Natrium project comes as the United States seeks to significantly expand its nuclear power capacity.

The U.S. already leads the world in nuclear generation, producing roughly 30% of global nuclear electricity. According to the Energy Department, the country has about 100 gigawatts of nuclear capacity today.

However, the government aims to quadruple that capacity to 400 gigawatts by 2050 to meet growing electricity demand and climate targets.

Federal policies are increasingly focused on rebuilding the nuclear supply chain and accelerating the deployment of new reactors.

Recent initiatives include:

$2.7 billion investment in uranium enrichment was announced in January 2026 to strengthen the domestic nuclear fuel supply.

$800 million in funding for small modular reactors was awarded in December 2025 to support projects led by utilities and developers.

A $1 billion loan to restart the Crane Clean Energy Center nuclear plant in Pennsylvania.

These measures reflect a broader push to ensure the United States maintains leadership in advanced nuclear technology.

Several companies are already developing next-generation reactors, including Oklo, Kairos Power, and X-energy. However, many of those projects are expected to deploy in the mid-2030s.

That timeline makes TerraPower’s Natrium project one of the earliest large-scale demonstrations of advanced reactor technology in the United States.

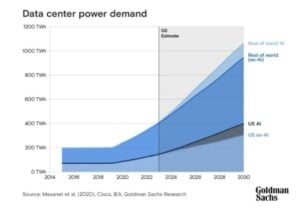

Rising Power Demand From AI and Data Centers

Another factor driving interest in nuclear energy is the rapid growth of data centers and artificial intelligence infrastructure.

Large technology companies, or the hyperscalers, are building massive data centers to support AI systems and cloud computing. These facilities consume enormous amounts of electricity and require reliable, constant power. As demand grows, many tech companies are exploring nuclear energy to secure their own supply rather than relying solely on public grids.

This trend could reshape the energy landscape. Governments must balance the needs of fast-growing digital industries with the need to keep electricity affordable for households and businesses.

The outcome may also influence the global AI competition between the United States and China, where access to reliable power could become a strategic advantage.

Nuclear Generation Remains Strong in the U.S.

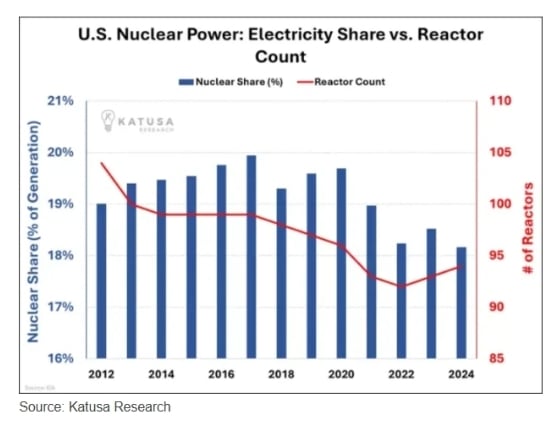

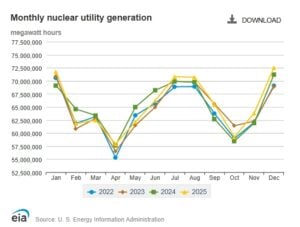

Despite maintenance cycles, nuclear power continued to provide stable and high levels of electricity in 2025. According to the Energy Information Administration (EIA), U.S. nuclear generation stayed consistently strong throughout the year. Output typically dipped during scheduled maintenance periods but rebounded quickly afterward.

The year ended on a particularly strong note. December 2025 recorded about 72–73 million megawatt-hours of nuclear generation, one of the highest monthly totals of the year.

This reliability is one reason policymakers continue to support nuclear energy as a key component of the country’s low-carbon power system.

In conclusion, the construction permit for the Natrium plant signals that advanced reactors are moving from concept to reality. And for TerraPower, the next step is clear: begin construction and prove that advanced nuclear technology can deliver reliable, carbon-free power at commercial scale.

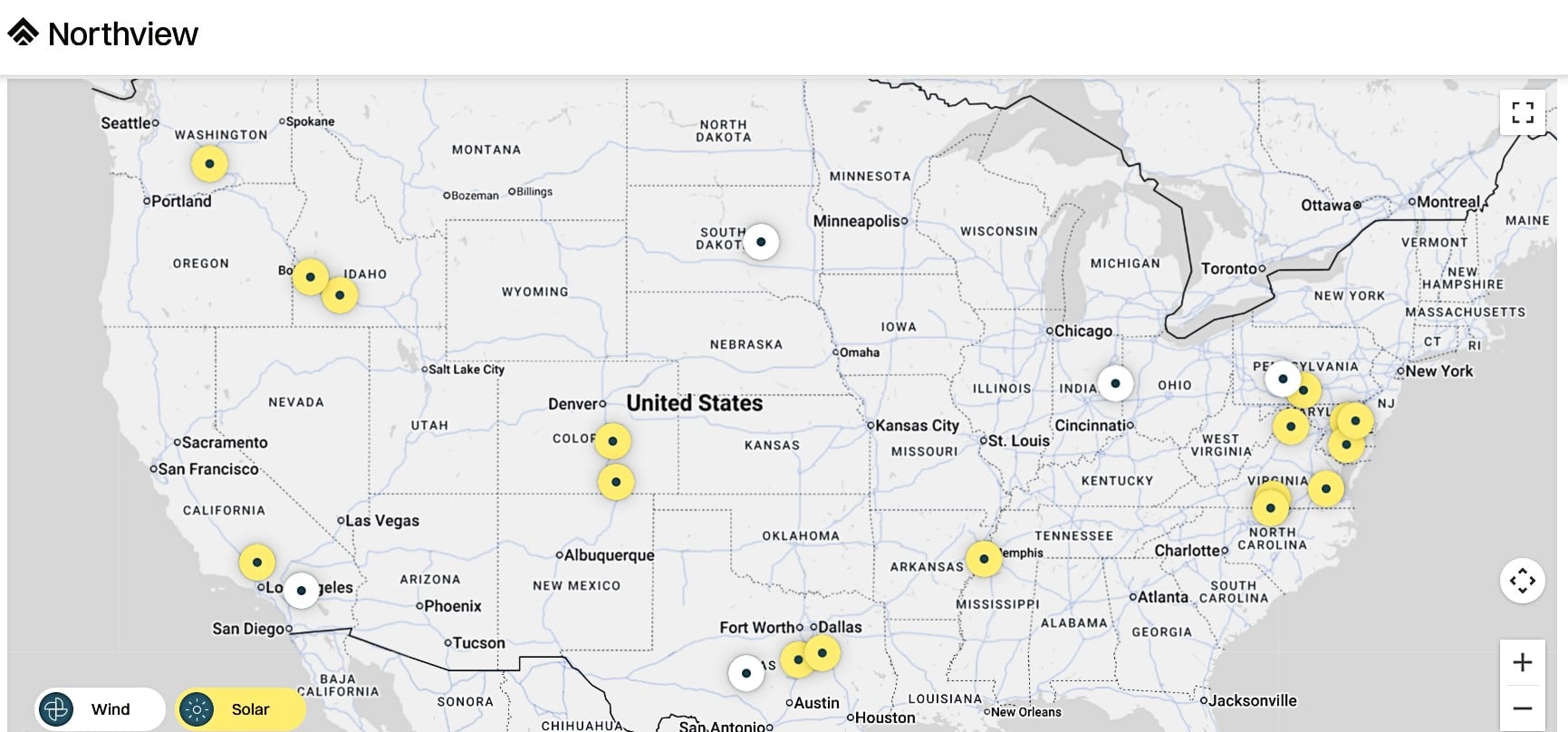

Three major global investors have joined forces to build a new renewable energy platform in North America. Brookfield Asset Management, Norges Bank Investment Management (NBIM), and British Columbia Investment Management Corporation (BCI) have launched a new company, Northview Energy.

Jehangir Vevaina, Chief Investment Officer for Brookfield’s Renewable Power & Transition group, remarked:

“This partnership marks the creation of a scalable platform for Brookfield and our partners. Northview Energy will be an owner of high-quality operating assets that deliver affordable and clean power to the grid, and the framework for future acquisitions provides a clear growth pathway for the vehicle to add de-risked, high-quality, cash-yielding assets delivering strong returns.”

Norway’s $2 Trillion Sovereign Fund Enters North American Renewables

The Northview Energy platform will own and acquire renewable energy infrastructure across the United States and Canada. It begins with a large portfolio of operating solar and wind projects.

The initial portfolio includes 22 utility-scale renewable assets with a total operating capacity of about 2.3 gigawatts (GW). The projects include 17 solar plants and five onshore wind farms.

These assets are spread across 11 U.S. states and six regional power markets. The projects are already operational and supply electricity to the grid.

Source: Northview Energy

The portfolio has an estimated enterprise value of about $2.6 billion. Each of the three partners will hold an equal 33.3% ownership stake in the new platform.

The launch of Northview Energy also marks an important step for NBIM. The firm manages Norway’s sovereign wealth fund, officially known as the Government Pension Fund Global. It is the largest sovereign wealth fund in the world, with assets of about $2 trillion.

NBIM will invest about $425 million to acquire its one-third stake in the renewable portfolio. This deal represents NBIM’s first renewable infrastructure investment in North America.

The partnership allows the fund to expand its real asset portfolio while supporting the growth of clean energy. Renewable infrastructure investments can generate stable income and help diversify long-term portfolios.

Institutional investors, such as pension funds and sovereign wealth funds, are putting more money into renewable energy. This trend has grown in recent years. These assets often offer predictable cash flows through long-term electricity contracts.

A Portfolio Built on Long-Term Power Contracts

The Northview platform focuses on operating renewable assets with contracted revenue. This model reduces investment risk. All projects in the initial portfolio have long-term power purchase agreements (PPAs) with strong buyers. These contracts have a weighted average remaining term of about 16 years.

PPAs allow companies to sell electricity at pre-agreed prices for many years. Utilities, corporations, and data centers often sign these contracts to secure a stable power supply.

For investors, long-term contracts create predictable revenue streams. This helps protect returns from energy price volatility.

Brookfield managed renewable companies that developed the projects. These include Deriva Energy, Scout Clean Energy, and Urban Grid. These developers built the wind and solar assets before transferring them to the new platform.

The partners plan to expand the platform beyond the initial portfolio.

Northview Energy has already signed a framework agreement to pursue future renewable acquisitions. The partners may deploy up to $1.5 billion in additional equity capital for new investments.

Future acquisitions will focus on operating renewable assets across North America. These may include:

The platform structure allows investors to buy multiple projects through a single vehicle. This approach can improve efficiency in operations, financing, and asset management.

The new platform will have a management team. They will oversee operations and future acquisitions. Subject to regulatory approvals, Northview Energy is expected to launch formally in the second quarter of 2026.

Strong Demand for Renewable Power in North America

North America remains one of the world’s most active markets for renewable energy investment. Demand for electricity is rising as industries electrify and digital infrastructure expands.

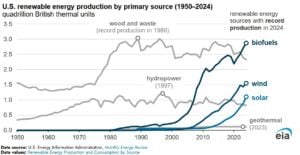

In 2024, renewable sources provided around 24.2% of total electricity in the U.S. This is an increase from 23.2% in 2023, as reported by the U.S. Energy Information Administration (EIA).

Source: EIA

Growth is expected to continue. By 2025, renewable energy accounted for nearly 26% of U.S. electricity generation and more than 36% of installed power capacity.

Wind and solar power are the main drivers of this growth. In 2024, the United States generated about 756,621 gigawatt-hours (GWh) of electricity from wind and solar combined. Wind produced 453,454 GWh, while solar generated 303,167 GWh.

Most new power plants are now renewable. Renewable energy made up over 90% of all new electricity capacity added in the U.S. in 2024, according to the Federal Energy Regulatory Commission (FERC). Solar alone represented over 81% of the new capacity added that year.

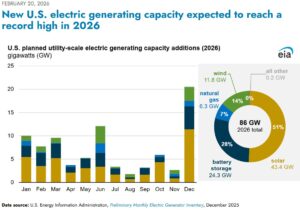

In 2026, US clean energy additions, led by solar and batteries, will shatter records with over 90% of new capacity from renewables. Despite challenges like grid limits, growth surges toward decarbonization goals.

Source: EIA

Corporate demand for clean electricity is also growing rapidly. North America now leads the global corporate renewable procurement market. The region accounts for about 40% of global PPA activity, supported by strong demand from technology firms, manufacturers, and data-center operators.

These trends make operating renewable energy projects especially attractive to investors. Wind and solar assets can produce electricity immediately and generate stable revenue through long-term power contracts.

Large institutional investors, like Brookfield, BCI, and NBIM, use platforms like Northview Energy. These platforms give them access to a fast-growing market for clean electricity infrastructure in North America.

Institutional Investors are Driving the Energy Transition

The launch of Northview Energy highlights a broader trend in global infrastructure investment. Big pension funds, sovereign wealth funds, and asset managers are putting billions into renewable energy. They are also investing in clean infrastructure.

These investors typically seek assets with stable cash flows and long operating lives. Renewable energy projects often meet these criteria because they generate electricity for decades.

The partnership between Brookfield, BCI, and NBIM brings together three large pools of capital:

Brookfield manages more than $1 trillion in assets globally, including about $247 billion in infrastructure.

BCI manages approximately C$295 billion in assets for public-sector clients in Canada.

NBIM oversees Norway’s sovereign wealth fund, valued at roughly $2 trillion.

The three investors can team up to build bigger renewable portfolios and enter new markets.

Platforms like Northview Energy also allow investors to scale investments quickly. Once the platform is established, it can acquire additional projects and grow its generation capacity over time.

A Long-Term Bet on Clean Power Infrastructure

Northview Energy is designed as a long-term infrastructure investment vehicle. With 2.3 GW of renewable capacity already in operation, the company starts with a significant footprint in the U.S. power market. The partners are also able to add more projects through the planned $1.5 billion equity investment pipeline.

If it succeeds, the platform could grow into more regions and technologies. This could happen as the North American energy shift speeds up.

For institutional investors, the model offers a way to deploy large amounts of capital into clean energy infrastructure while generating predictable returns. And for the broader energy system, investments like this help expand the supply of renewable electricity needed to meet future demand.

The European Union (EU) is considering a new policy that could allow the use of international carbon credits to help meet its ambitious 2040 climate target. If implemented carefully, the plan could unlock significant climate finance for projects in developing countries, particularly initiatives that expand access to clean cooking technologies.

At a recent clean cooking summit hosted by the International Energy Agency (IEA), France’s climate ambassador Benoît Faraco suggested that the EU could become a major investor in carbon credit projects. These investments could help accelerate efforts to replace polluting wood and biomass stoves with cleaner alternatives across Africa and other regions.

However, the proposal has also revived a long-standing debate in climate policy. Supporters argue that carbon credits can finance climate solutions globally, while critics warn that poorly designed projects can exaggerate emissions reductions and undermine climate integrity.

As global demand for carbon credits grows, the EU’s upcoming rules could shape the future of the voluntary carbon market.

EU’s 2040 Climate Target and the Role of Carbon Credits

The European Union plans to cut greenhouse gas emissions by 90% from 1990 levels by 2040, making it one of the most ambitious climate targets globally. To support this goal, policymakers are exploring allowing a limited share of emissions reductions to come from high-quality international carbon credits.

Under the emerging framework, these credits could account for up to about 5% of the emissions reductions needed to meet the 2040 goal. The mechanism would likely begin in 2036 and would include strict safeguards designed to ensure environmental integrity.

EU officials believe this approach could ease pressure on domestic industries while still maintaining the bloc’s overall climate ambition. At the same time, it could channel new climate finance into developing countries where emissions reductions can often be achieved at lower costs.

However, the European Commission has not yet finalized the rules governing which projects would qualify or how these credits would be sourced and verified.

Clean Cooking Projects Could Benefit

One area that could receive significant investment is clean cooking technology. During the IEA summit, Benoît Faraco suggested that EU participation in carbon markets could help scale up efforts to replace traditional cooking methods with cleaner alternatives such as liquefied petroleum gas (LPG).

Across many developing countries, households still rely heavily on wood, charcoal, or biomass for cooking. These fuels create severe indoor air pollution and contribute to deforestation and greenhouse gas emissions.

Globally, the challenge remains enormous:

More than two billion people still lack access to clean cooking

Indoor air pollution linked to traditional cooking contributes to millions of deaths every year

Most of those without access live in rural areas where energy infrastructure remains limited.

Expanding access to modern cooking technologies requires large investments in equipment, fuel distribution systems, and consumer financing. Carbon credit funding could help close these financial gaps.

Private companies are already experimenting with this approach. TotalEnergies, for example, has invested in LPG infrastructure aimed at expanding clean cooking access across Africa and India.

One notable initiative involves a cookstove project in Rwanda developed with the organization DelAgua. The program aims to distribute 200,000 high-performance cookstoves to rural households.

Within a year, the project is expected to benefit more than 800,000 people living in rural communities. Compared with traditional open fires, the improved cookstoves significantly reduce pollution and fuel consumption.

The new stoves cut harmful smoke emissions by about 81% and reduce wood use by roughly 71%. Over ten years, the initiative could prevent more than 2.5 million tonnes of carbon dioxide equivalent emissions.

These avoided emissions generate carbon credits that companies can purchase as part of their climate strategies. The program also supports Rwanda’s national goal of providing universal access to clean cooking by 2030.

Global Carbon Markets Are Expanding

Recent developments in international climate policy suggest that clean cooking projects may play a growing role in carbon markets.

In February 2026, a United Nations body approved the first carbon credits to be issued under the global carbon market established by the Paris Agreement. The approved activity focuses on distributing efficient cookstoves in Myanmar.

The project aims to reduce household air pollution and limit pressure on forests by lowering fuelwood consumption. Some of the credits will be used within South Korea’s emissions trading system, while the remaining credits will support Myanmar’s own climate commitments.

UN climate officials highlighted the broader benefits of clean cooking initiatives. These projects not only cut emissions but also improve health, protect forests, and reduce the burden on women and girls who often spend hours collecting firewood.

Meanwhile, data from the voluntary carbon market shows growing activity. A report from SCB Group found that carbon credit issuances increased by 28% quarter-on-quarter in the second quarter of 2025.

During that period, about 68 million credits were issued globally. Cookstove projects accounted for the largest share of these credits, representing roughly 29% of total issuances. Wind projects followed with about 20%, while forest conservation initiatives made up around 13%.

Most cookstove credits were certified under the Verra and Gold Standard programs.

Source: Green.Earth

Concerns About Credit Integrity

Despite their potential benefits, cookstove carbon credits have long been controversial. Some climate experts argue that many projects exaggerate their emissions reductions.

Monitoring real-world stove usage can be difficult. Households may receive improved stoves but continue using traditional cooking methods alongside them. In such cases, the actual emissions reductions may be smaller than estimated.

Environmental organizations have also raised concerns about weak monitoring systems and inconsistent verification standards across carbon markets.

An expert from the Brussels-based NGO Carbon Market Watch warned that relying on credits that have repeatedly failed to meet expectations could pose significant risks for climate policy.

These concerns reflect lessons from earlier offset systems, including the Clean Development Mechanism under the Kyoto Protocol. Several projects approved under that framework later faced criticism for overstating emissions reductions.

Because of this history, regulators are now under pressure to ensure that any new carbon credit systems deliver real and measurable climate benefits.

Strong Standards Will Be Critical

EU policymakers say the success of their carbon credit strategy will depend on strict oversight and transparency.

Future rules are expected to focus on three key principles:

strong monitoring and independent verification

clear safeguards to prevent double-counting of emissions reductions

proof that projects deliver additional climate benefits beyond the host countries’ own targets

If implemented effectively, these standards could strengthen confidence in international carbon markets.

At the same time, critics argue that carbon credits should only play a limited role in meeting climate targets. They warn that over-reliance on external offsets could delay necessary emissions reductions within Europe itself.

A Major Global Challenge Remains

The clean cooking challenge illustrates why new financing mechanisms are urgently needed. IEA estimates that around 300 million people must gain access to clean cooking solutions every year to achieve universal access by 2030.

Sub-Saharan Africa accounts for roughly half of the population still relying on traditional cooking fuels. Many rural communities lack access to modern energy infrastructure and affordable alternatives.

Replicating the progress achieved in countries such as China, India, and Indonesia will require large investments and coordinated policy efforts. Carbon finance could become an important tool to accelerate this transition.

Source: IEA

Overall, the European Union’s potential use of international carbon credits could reshape the global carbon market and unlock new funding for climate solutions in developing countries.

Clean cooking projects represent one of the most visible opportunities. They deliver clear health and environmental benefits while reducing greenhouse gas emissions.

However, the debate over carbon credits highlights a deeper challenge. Policymakers must ensure that these credits represent real, measurable emissions reductions rather than accounting shortcuts.

If the EU succeeds in designing a robust framework with strict quality standards, international carbon markets could channel billions of dollars into projects that improve lives and reduce emissions worldwide.

The carbon removal industry is expanding fast, with new projects moving from the pilot stage to the commercial scale. Companies are racing to build infrastructure that can permanently remove carbon dioxide from the atmosphere. One of them is a Canadian carbon management company, Svante Technologies, which announced that it acquired Carbon Alpha Corporation. This move brings together carbon capture technology with carbon dioxide removal (CDR) project development.

The acquisition strengthens Svante’s role in the carbon capture and storage (CCS) value chain. It also adds Carbon Alpha’s development portfolio to Svante’s operations.

Claude Letourneau, President & CEO of Svante, remarked:

“This project is a game-changer for Svante and a pivotal moment for scaling verifiable, durable engineered carbon removal solutions working in tandem with nature. By integrating Carbon Alpha’s team, we’re accelerating the delivery of high‑integrity CDR credits at commercial scale in partnership with the MLTC leadership, who is closely coordinating with us on the North Star Project.”

The North Star Project: A New Source of Carbon Removal Credits

The key asset in the deal is the North Star Bioenergy Carbon Capture and Storage (BECCS) project in Saskatchewan. The facility will capture carbon dioxide from the Meadow Lake Tribal Council Bioenergy Centre. This is how it works:

This plant produces renewable electricity and heat using forestry waste biomass from nearby sawmills.

Phase one of the project is designed to capture up to 140,000 tonnes of CO₂ per year from biomass combustion emissions.

The captured carbon dioxide will move through a dedicated pipeline to a deep saline aquifer. There, it will be stored permanently underground.

This process removes carbon from the natural cycle because biomass absorbs CO₂ while growing. Capturing and storing that carbon after combustion results in net negative emissions.

The project will generate durable carbon dioxide removal credits. Each credit represents one ton of CO₂ removed. These credits can be sold to companies seeking verified carbon removal to meet climate targets.

Carbon Alpha had already developed the project structure and storage system before the acquisition. Svante now takes over development and integration. The next step will be a front-end engineering design (FEED) study and test-well drilling program. A final investment decision is expected in early 2027.

Industry analysts say deals like this show how the carbon removal sector is shifting from research to deployment. Companies are now building full systems that include capture, transport, and long-term storage.

The acquisition expands Svante’s strategy to build an integrated carbon management company. It develops modular carbon capture systems that use nanoengineered solid sorbent filters to capture CO₂ from industrial emissions.

The technology is designed for industries that are difficult to decarbonize. These include cement, steel, hydrogen production, and power generation.

Before the acquisition, Svante already had expertise in capture technology. Carbon Alpha adds expertise in project development, geological storage, and carbon credit generation. This combination creates a full value chain for CCS in Canada:

Capture CO₂ from industrial sources or biomass energy

Transport the CO₂ through pipelines

Store the carbon permanently underground

Generate verified carbon removal credits

Industry experts say this type of integration is important. Carbon removal projects often fail because separate companies handle capture, storage, and financing.

The strategic acquisition includes Carbon Alpha’s development expertise, North Star Carbon Solutions LP’s ownership structure, and eligibility for Canada’s 50% CCUS investment tax credit, positioning Svante to scale multiple BECCS projects rapidly.

By combining these elements, Svante aims to scale projects faster.

First Nations Partnership Anchors the Project in Saskatchewan

The North Star project is being developed in partnership with the Meadow Lake Tribal Council (MLTC). The organization represents nine First Nations communities in northwest Saskatchewan.

Under the project structure, MLTC will be a co-owner of the BECCS facility alongside Svante. The partnership focuses on three main goals: local economic development, job creation, and long-term environmental leadership.

The bioenergy facility already produces renewable electricity and heat using forestry residues. The carbon capture system adds another layer of value. It turns the facility into a carbon removal hub that can produce verified CDR credits.

The project also includes the development of a regional CO₂ pipeline and storage hub. This infrastructure could support other emitters in the region.

Biogenic carbon sources from forestry, agriculture, or bioenergy plants could connect to the same storage network. This approach could turn the region into a carbon removal cluster.

Global Demand for Carbon Removal Is Rising Fast

The acquisition comes at a time when demand for carbon removal is increasing worldwide. Most countries now include carbon removal in long-term climate plans. Industry groups expect global carbon removal markets to reach hundreds of millions of tonnes of capacity by the 2030s.

Source: McKinsey & Company

Boston Consulting Group (BCG) outlines three demand scenarios for 2030–2040: low (40–80 MtCO₂/year), medium (70–230 MtCO₂/year), and high (200–870 MtCO₂/year). McKinsey also estimates durable CDR demand could hit 100 MtCO₂ by 2030, with announced supply at ~50 MtCO₂, creating a supply-demand gap.

The Intergovernmental Panel on Climate Change says that limiting global warming to 1.5°C will require removing billions of tonnes of CO₂ annually by mid-century. Many climate models further show that 5 to 10 billion tonnes of carbon removal per year may be needed by 2050. That translates to between $6 – $16 trillion of investment by mid-century.

Today, global carbon removal capacity is still very small. Most engineered projects remove only thousands or tens of thousands of tonnes annually.

However, investment is rising quickly. Major corporations such as Microsoft, Stripe, and Alphabet have signed large contracts for high-quality carbon removal credits.

Governments are also supporting the sector. In Canada, carbon capture projects can receive financial support through the CCUS investment tax credit. This covers up to 50% of eligible capture equipment costs, depending on project type. These incentives aim to help scale early infrastructure.

Source: Natural Resources Canada.

At 140,000 tCO₂/year, North Star Phase 1 represents about 35x the capacity of Climeworks‘ Orca plant. It also aligns with Microsoft‘s annual CDR purchasing scale, demonstrating commercial viability for durable removal credits.

Why BECCS Is a Key Carbon Removal Technology

Bioenergy with carbon capture and storage is one of the most widely studied carbon removal technologies. BECCS combines three steps:

Biomass absorbs CO₂ while growing.

The biomass is used to produce energy.

Carbon emissions are captured and stored underground.

This creates net negative emissions. The technology also produces electricity or heat, which can improve project economics. However, large-scale BECCS projects require several conditions, including:

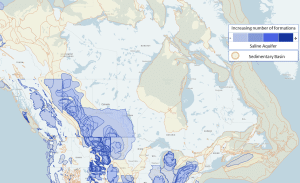

Canada has strong potential for BECCS development because of its forestry resources and suitable geological formations. Western Canada already hosts major CCS infrastructure. For example, large carbon storage reservoirs exist in Alberta and Saskatchewan.

Map of Canada showing saline formations and sedimentary basins

Data source: North American Carbon Storage Atlas. Image from Natural Resources Canada.

This geological capacity could store billions of tonnes of CO₂ over time. Developers say regional storage hubs will be essential for scaling carbon removal.

The Next Phase for Carbon Removal Infrastructure

The acquisition of Carbon Alpha marks an important step in the industrialization of carbon removal. Instead of isolated pilot projects, companies are now building complete carbon management systems.

For Svante, the deal strengthens its ability to build and operate large carbon removal projects. For the broader market, it shows how carbon removal is moving from concept to infrastructure.

As governments and companies push toward net-zero targets, the demand for durable carbon removal credits is expected to keep rising. Projects like North Star may become an important part of the global climate strategy.

A war in the Middle East may increase demand for carbon credits if it continues for a long time. Analysts say energy supply disruptions from the conflict could push some industries back to higher‑emission fuels like coal. This, in turn, could raise emissions and force companies in regulated markets to buy more carbon credits.

The Middle East conflict has already disrupted liquefied natural gas (LNG) supplies. Qatar, a top LNG producer, has halted output at its largest LNG plant. This is due to disruptions in transport routes through the Strait of Hormuz. Qatar supplies about 20% of global LNG output.

LNG provides cleaner fuel for power generation than coal. When gas costs rise sharply or supply is limited, utilities sometimes increase coal use to meet electricity demand. Higher coal use increases carbon emissions. This can lead to higher demand for carbon credits in compliance markets.

Carbon Credits 101: How the Market Responds

A carbon credit represents one tonne of greenhouse gas emissions reduced, avoided, or removed from the atmosphere. Companies must hold carbon credits to meet emissions limits in regulated markets. These markets are part of government climate policy.

Compliance carbon markets, like emissions trading systems (ETS), require companies to lower their emissions. If they can’t, they must buy credits to stay within a limit.

Over 113 carbon pricing systems are in use worldwide. This includes ETS and carbon taxes, which cover about 28% of global greenhouse gas emissions.

In compliance markets, rising emissions usually increase demand for allowances or carbon credits. If companies cannot reduce emissions fast enough, they buy credits to stay compliant. Strong or rising demand can also influence credit prices.

Voluntary carbon markets exist separately from compliance markets. In voluntary markets, companies buy credits to meet internal climate goals, not legal limits.

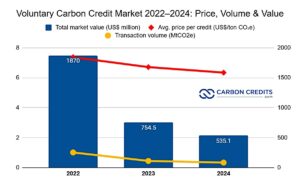

The voluntary market is smaller but growing. The global voluntary carbon credit market is expected to rise from $1.88 billion in 2025 to $2.29 billion in 2026. It could reach $4.92 billion by 2030.

From Gas to Coal: When Utilities Flip the Switch

The Middle East conflict has pushed energy prices higher. Global natural gas and oil prices climbed because of risks to supply routes such as the Strait of Hormuz, a key passage for crude oil and LNG.

Source: TradingView

When gas prices rise, utilities may switch from gas‑fired generation to coal, which is cheaper but emits more CO₂. Analysts observed that fuel switching happened in 2022 after Russia invaded Ukraine. European gas supply was disrupted, so utilities turned to burning more coal.

Coal prices have also risen in response to supply pressures. Some markets saw thermal coal prices climb about 26%, reaching highs not seen in more than two years.

Source: Trading Economics

Such shifts can put pressure on emissions limits in regulated markets. Higher emissions would require companies to buy more compliance credits to avoid penalties. This dynamic is central to why analysts say carbon credit demand could rise if disruptions persist.

Compliance Markets Under Pressure, So Who Pays the Price?

Compliance carbon markets form the largest portion of carbon credit demand. These include emissions trading systems in Europe, China, and the U.S., and expanding carbon pricing schemes globally. The Middle East conflict could affect these markets, which shows how energy security and climate policy are connected.

Demand for carbon credits depends on how countries and companies aim to meet climate goals, like those in the Paris Agreement. This agreement aims to limit global warming to below 2°C. Compliance markets set legal limits, and voluntary markets support corporate climate goals.

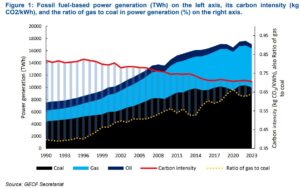

If more companies switch to coal, emissions per unit of energy could go up, and compliance markets might see a higher demand for allowances or credits. This happens as companies try to stay within legal limits. This could result in higher carbon prices and tighter markets, depending on how regulators respond.

Source: GECF

Here is a sample scenario for better understanding:

Coal’s higher emissions factor (~0.35 tCO2/MWh vs. gas’s ~0.20 tCO2/MWh, per IPCC data) means switching boosts shortfalls against free allocations (often benchmarked low, e.g., 0.3 tCO2/MWh). Using this estimation, a firm generating 1 million MWh yearly will have this result:

This scenario creates ~46,000 extra allowances demanded firm-wide, scaling market-wide with multiple switchers.

In the European Union Emissions Trading System (EU ETS), companies must hold allowances equal to their emissions, or face fines. The EU is considering reforms to improve market stability and balance supply and demand for allowances. This scheme has been a key tool for reducing emissions in Europe since 2005.

In addition, more sectors are entering compliance markets. For example, China’s national ETS covers key industrial sources. It accounts for a big part of emissions from the world’s largest emitter.

Any rise in emissions from fuel switching could increase demand in these established markets. However, the exact impact will depend on how long energy disruptions continue and whether regulators adjust compliance caps or other rules.

Voluntary Market Volatility: Green Goals on Hold?

Global carbon pricing revenues topped over $100 billion in 2023 and in 2024. The World Bank reports that around $69 billion came from emissions trading systems and $33 billion from carbon taxes. This amount covers nearly 24% of global greenhouse gas emissions, which reflects the growing scale of these markets.

While compliance demand may rise if emissions increase, the outlook for the voluntary market could differ.

According to analysts, an energy crisis may temporarily constrain corporate spending on voluntary credits. High energy prices raise operating costs. This may lead companies to delay voluntary purchases as they will focus more on their core operations instead.

High-integrity voluntary markets have grown recently. This growth is driven by corporate net-zero commitments and new standards. Companies increasingly seek credits that meet quality criteria such as compliance eligibility, durability, and third‑party verification.

Sudden economic strains or changes in energy costs could quickly change how companies buy.

The Ripple Effect: Energy Security Meets Climate Action

A prolonged Middle East conflict could have ripple effects beyond energy prices. Disruptions to LNG supply may push some utilities toward higher‑emission fuels, raising emissions levels. That could drive demand for carbon credits in regulated markets where companies must meet emissions limits.

At the same time, short‑term pressures from high energy costs could slow voluntary demand as companies focus on operational priorities. The overall direction of carbon credit demand will depend on the duration of energy supply disruptions, policy responses by regulators, and the pace of the global energy transition.

Carbon markets are an evolving part of climate policy, linking energy markets and climate goals. As energy security concerns grow, the role of carbon credits in balancing compliance and emissions reductions may attract more attention from policymakers, investors, and companies in the coming years.

Disseminated on behalf of Alaska Energy Metals Corporation.

nickel Price Analysis Today

Nickel prices advanced 1.39% today, trading at $17,313.86 per ton globally and ¥119,578 in China. This upward momentum is primarily driven by fresh supply-side shocks, as the Indonesian government just approved a new export tax on outbound nickel shipments, stoking fears of tighter availability and raising costs. Additionally, broader risk sentiment improved following US proposals for a Middle East ceasefire, while tighter Indonesian production quotas continue establishing a robust price floor.

The global nickel market enters 2026 after a bruising and uneven year. In 2025, macroeconomic stress, trade disruptions, and deep supply imbalances reshaped pricing and sentiment. Although short-term rallies have returned, the underlying structure of the market remains fragile. As a result, 2026 is shaping up to be a year defined by volatility rather than a sustained recovery.

A Challenging Backdrop from 2025

To understand where nickel is headed, it helps to revisit the environment it emerged from. In 2025, global trade flows came under pressure after the US implemented new tariff policies. These measures disrupted supply chains and dampened confidence across industrial commodities. At the same time, global manufacturing growth slowed, weighing heavily on the broader nonferrous metals complex.

SMM reported highlighted some significant points. Adding to the uncertainty, the US Federal Reserve sent mixed signals throughout the year. Expectations around interest rate cuts shifted repeatedly. Each change altered risk appetite and triggered sharp moves across commodity markets. Nickel, already vulnerable due to oversupply, struggled to attract sustained buying interest.

China attempted to offset some of these pressures. Policymakers rolled out proactive fiscal measures and maintained a moderately accommodative monetary policy. They also focused on boosting domestic demand and diversifying export routes to reduce exposure to trade frictions. In July, China introduced its “anti-involution” policy, aimed at curbing destructive price competition across industries.

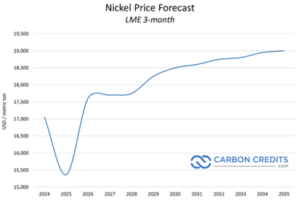

Even so, nickel underperformed. While other nonferrous metals showed mixed results, nickel remained constrained by a clear mismatch between supply and demand. Prices trended lower for most of the year. LME nickel opened near $15,365 per tonne and slid to lows around $13,865 per tonne, marking a sharp reset in the price center.

2026 Nickel Price Outlook: A Volatile Start to the New Cycle

Momentum shifted suddenly toward the end of the year. From mid-December, nickel prices began climbing rapidly.

By early January, LME prices had surged past $18,000 per tonne, the first time in more than a year. In just 12 trading sessions, prices jumped nearly 20%, catching many traders off guard.

Several factors fueled this rebound. Demand signals from China improved modestly, particularly from stainless steel mills and EV battery producers. At the same time, speculative positioning adjusted as supply risks from Indonesia returned to the spotlight.

Trading Economics analysis stated that Indonesia, the world’s largest nickel producer, hinted at a potential 34% reduction in output for this year. Meanwhile, Vale temporarily halted operations at its Pomalaa and Bahodopi mines while waiting for regulatory approvals. Although its flagship Sorowako mine continued operating, these pauses added to market caution.

Still, the rally faced clear limits. Inventory levels remained elevated. Combined LME registered and off-warrant stocks jumped nearly 58% last year, reaching more than 367,000 tonnes. In addition, large shadow inventories in Singapore and Kaohsiung continued to hang over the market. As a result, every price spike met resistance.

Price Expectations Remain Capped

Most analysts expect nickel prices to settle into a narrow band rather than trend sharply higher. Forecasts largely cluster between $15,000 and $16,000 per tonne. Several major institutions attribute the restrained outlook to ongoing surpluses.

Trading Economics data indicated that nickel futures moved back up to nearly $17,800 per tonne, reversing last week’s steep decline as buyers stepped back into the market.

Analysts consider that the differences in price forecasts primarily reflect contrasting views on how strictly Indonesia will enforce production limits and how quickly global manufacturing activity is expected to recover.

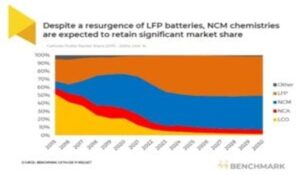

Stainless steel: remains the dominant driver, accounting for about 70% of total demand. Consumption may rise to roughly 2.45 to 2.5 million tonnes. China’s production recovery offers support, while infrastructure projects in emerging markets add incremental demand. Still, no major surge is expected.

Battery and EV application: They make up roughly 13% to 15% of demand. Nickel use in this segment could reach up to 500,000 tonnes. High-nickel cathodes continue to support premium EV models.

According to Benchmark Mineral Intelligence, demand for battery-grade nickel is expected to surge, tripling by 2030. This growth will largely be due to mid- and high-performance EVs in Western markets.

Other uses, including alloying, plating, aerospace, and electronics, provide steady but smaller contributions. A broader manufacturing recovery and net-zero investments could lift demand slightly, while faster EV adoption remains the main upside risk.

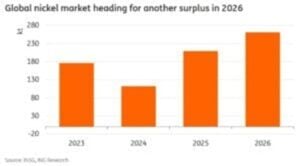

According to SMM, the nickel market will remain oversupplied through the year, remaining between 120,000 and 275,000 tonnes. While short-term rallies may continue, oversupply will remain the dominant force.

On the supply side, Indonesia’s refined nickel output stays high, supported by sunk investments and low operating costs. On the demand side, growth remains steady but unspectacular.

Source: AEMC

Ewa Manthey, a commodities strategist at London-Based ING Group, explained that the global nickel market is still set to remain oversupplied, with a projected surplus of about 261,000 metric tonnes. As a result, any production cuts would need to be deep and sustained to meaningfully shift market fundamentals.

China’s real estate support policies may provide limited relief for stainless steel consumption. However, a strong housing rebound appears unlikely, and any improvement is expected to be gradual. Similarly, demand from ternary batteries faces structural headwinds. Solid-state batteries remain years away from large-scale commercial use, and near-term battery chemistry trends do not favor a sharp jump in nickel intensity.

As a result, the average price level may drift lower over time. Tightening ore supply could briefly push prices above $16,000 per tonne. However, high inventories and excess capacity will take longer to absorb.

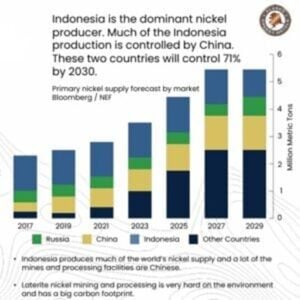

Why Nickel Matters for US Critical Mineral Independence?

Nickel plays a critical role in military-grade alloys, advanced weapons systems, electric vehicle batteries, grid-scale energy storage, and broader clean energy infrastructure. Despite its importance, the United States remains almost entirely dependent on imports for nickel, while China controls much of the global processing and supply chain. This reliance has become a clear strategic risk, one that domestic resources need more exploration.

And this is the reason America’s push to secure its critical mineral supply is gaining real momentum.

Spotlight: Alaska Energy Metals – America’s Nickel Backbone

At the center of this shift is Alaska Energy Metals Corporation (TSX-V: AEMC, OTCQB: AKEMF) and its Eureka deposit, the largest documented nickel resource in the United States. As Washington intensifies efforts to reshore critical supply chains for national security and clean energy goals, AEMC’s Nikolai Project in Alaska is steadily gaining recognition as a strategic domestic asset.

At the same time, the project aligns closely with the Trump administration’s executive orders focused on critical minerals and Alaska resource development. Those directives sought to speed up domestic production, curb reliance on foreign suppliers, and reinforce US security interests.

Against this backdrop, Nikolai stands out as a fully US-based “Sulphide nickel and battery metal project” to meet the country’s metal needs for the energy transition. Significantly, it has two claim blocks: Eureka and Canwell.

Source: AEMC

Eureka: The Largest Known Nickel Resource in the US

The Eureka deposit is not just large—it is nationally strategic. It hosts nickel alongside copper, cobalt, chromium, iron, and platinum group metals, including platinum and palladium. This metal mix makes Eureka highly relevant for both defense systems and the expanding clean energy economy.

According to the 2025 Mineral Resource Estimate, Eureka contains: