The global race to build artificial intelligence (AI) infrastructure is accelerating at a historic pace. Bank of America (BofA) now estimates the AI data center systems market could hit about $1.7 trillion by 2030. This is a big jump from earlier predictions.

The updated outlook shows a rising need for AI computing power, cloud infrastructure, advanced semiconductors, and electrical systems. These are essential for large-scale AI deployment.

At the center of this expansion are hyperscale data centers. These facilities train and run advanced AI models that power chatbots, enterprise tools, automation systems, and cloud services.

However, the rapid buildout also raises concerns about electricity demand, carbon emissions, water use, and strain on existing power grids. The result is a growing tension between digital expansion and environmental sustainability.

BofA Sees a Trillion-Dollar AI Buildout Ahead

Bank of America increased its forecast for the AI data center systems market to about $1.7 trillion by 2030. This is up from earlier estimates of around $1.2 trillion and later $1.4 trillion. The bank expects the market to grow at a compound annual rate of roughly 38% to 45%, depending on the segment analyzed.

The bank also sharply increased its semiconductor outlook. In April 2026, BofA analyst Vivek Arya increased the global semiconductor revenue forecast for 2026 to $1.3 trillion. This was $300 billion more than the estimates from just four months prior.

BofA projects the broader chip market could reach $2 trillion by the end of the decade. Several parts of the AI hardware market are expanding rapidly:

- AI accelerator forecasts increased to around $1.2 trillion.

- AI networking projections rose to roughly $316 billion.

- Data center server CPU forecasts increased to around $110 billion.

BofA also expects AI infrastructure spending to remain strong for years. The bank describes 2026 as roughly the midpoint of an eight-to-ten-year AI expansion cycle.

Big Tech and Governments Drive Spending Surge

Other major technology firms and national AI strategies further fuel the AI expansion.

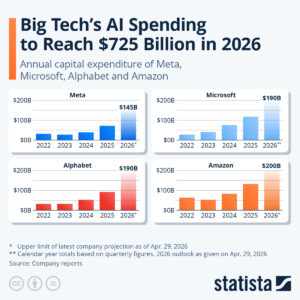

The BofA report states that Microsoft, Amazon, Meta, and Alphabet plan to spend over $670 billion on data center development in 2026. Some estimates, like that by Statista, say combined spending is around $725 billion. This shows the fierce competition for AI computing capacity.

At the same time, sovereign AI programs are becoming a major source of demand. Governments now see AI infrastructure as a key part of national resources. It’s like energy systems or telecom networks. This is pushing countries to build domestic computing capacity rather than rely entirely on foreign cloud providers.

The market is also expanding beyond semiconductors and servers. BofA introduced a ranking of 67 electrical infrastructure companies expected to benefit from data center construction. The list includes firms involved in transformers, power systems, cooling equipment, and grid connectivity.

BofA says that electrical infrastructure is a major bottleneck for AI growth. Many power systems aren’t built to handle the rapid increase from data centers.

Grid Strain and Electricity Demand Become Central Challenges

The AI boom is increasing pressure on electricity systems worldwide.

BofA estimates that U.S. electricity demand could grow at a 2.5% annual rate through 2035, compared with only 0.5% growth during the previous decade. Data centers are expected to be one of the main drivers of this increase.

The bank stated that about 67% of U.S. utility spending in 2024, roughly $63 billion, will go to replacing and upgrading old systems instead of building new capacity. This creates concerns about whether grids can expand fast enough to support AI growth.

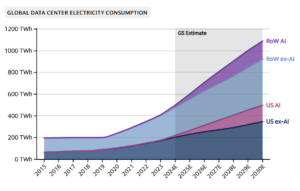

Other forecasts show even steeper increases. Goldman Sachs estimates that global data center electricity use may rise by over 220% by 2030. This could hit about 1,350 terawatt-hours each year.

In the United States alone, data centers could account for nearly 11% of national electricity demand by 2030, almost double current levels.

Research also suggests that AI infrastructure is becoming concentrated in a few regions. North America, Western Europe, and the Asia-Pacific are expected to account for more than 90% of projected AI compute capacity by 2030.

Some areas, like parts of Virginia, Oregon, and Ireland, might experience rising grid stress. This stress comes as data center demand outpaces local energy infrastructure.

AI’s Climate Footprint Is Expanding Fast

The environmental impact of AI infrastructure goes far beyond energy consumption.

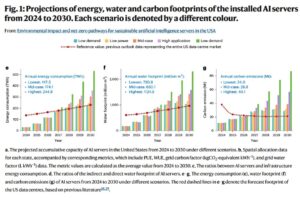

A study suggests that by 2030, AI data centers in the United States alone are projected to generate an additional 24 to 44 million metric tons of carbon dioxide annually. That is roughly equal to adding 5 to 10 million cars to American roads.

One reason is that data centers often rely on electricity sources with higher carbon intensity than the national average. Data centers currently use electricity that is 48% more carbon-intensive than the average U.S. grid mix. This is mainly because operators still rely on fossil-fuel baseload power.

Even under aggressive renewable energy scenarios, analysts estimate that around 11 million tons of residual emissions could remain by 2030. Reaching net-zero emissions would require roughly:

- 28 gigawatts of wind capacity, or

- 43 gigawatts of solar capacity.

Water use is also emerging as a major concern. AI data centers could consume between 731 million and 1.125 billion cubic meters of water annually by 2030. A large hyperscale AI facility may use 3 to 7 million gallons of water per day for cooling systems. Some facilities reportedly source up to 57% of cooling water from potable drinking supplies.

These pressures are especially important in regions already facing water scarcity or drought conditions.

Semiconductor Production Adds Another Layer of Emissions

The environmental footprint of AI infrastructure also includes semiconductor manufacturing.

Global chip manufacturing already generates roughly 50 megatons of CO₂ emissions each year. Semiconductor facilities use highly energy-intensive processes and rely on specialized gases with extremely high warming potential.

Nitrogen trifluoride (NF₃) is one example. This gas is used in chip production. Its global warming potential is about 17,000 times that of carbon dioxide. If current trends continue, analysts say semiconductor manufacturing could make up about 3% of global emissions by 2040.

At the same time, AI chip demand continues to surge. TSMC recently estimated that the global semiconductor market might surpass $1.5 trillion by 2030. This growth is mainly fueled by demand for AI and high-performance computing. The company expects AI accelerator wafer demand to increase 11-fold between 2022 and 2026.

AI Infrastructure Growth Brings Economic Opportunity and Environmental Pressure

The rapid expansion of AI infrastructure is reshaping global technology investment. Bank of America’s new $1.7 trillion forecast reflects how central data centers, semiconductors, networking systems, and electrical infrastructure have become to the next phase of economic growth.

However, the buildout carries major environmental costs. Rising electricity demand, higher emissions, growing water consumption, and grid strain are becoming structural challenges tied to AI expansion.

The industry now faces a difficult balance. Companies and governments want faster AI growth, but they also face increasing pressure to meet climate targets and strengthen energy systems.

As AI infrastructure spending rises, the ability to align digital growth with sustainable energy development may become one of the sector’s defining challenges.