CATL’s rapid growth across Hungary, Germany, and Spain marks a major shift in how the company operates in Europe. It is no longer only supplying batteries from abroad. Instead, it is becoming deeply involved in Europe’s industrial and workforce ecosystem. Through new factories, training partnerships, and community programs, the company is building a long-term European presence that supports local economies and clean-energy goals.

Hungary: Debrecen Plant Nears Launch and Strengthens the EV Supply Chain

CATL’s new battery cell factory in Debrecen is moving into its final phase before full operation. The greenfield site is set to play a central role in Europe’s EV supply chain. When it opens, it will deliver 40 GWh of annual capacity, all of which is already fully booked by customers. Mass cell production is expected to begin in early 2026.

While the cell lines prepare for launch, module assembly has already been running for more than a year. The plant has produced more than 120,000 battery modules, enough to power over 30,000 electric vehicles across Europe. The number of employees is also rising quickly, and CATL expects the local workforce to reach 1,500 people by Q1 2026.

Matt Shen, Managing Director of CATL Germany and Hungary, said

“Our Debrecen investment is a major step towards strengthening CATL’s European presence. We are planning for the long term, bringing our most advanced and sustainable manufacturing technologies to Hungary.”

A Facility Designed for High Environmental Standards

Environmental protection is central to the Debrecen plant’s design. CATL built the facility to meet Europe’s strictest environmental requirements, along with additional Hungarian regulations. Several achievements highlight this commitment:

Energy use was reduced by almost 30 percent compared with the earlier IPPC permit.

Potable water demand cut to one-third, supported by water-saving cooling technologies.

ISO 14001 certification was achieved in October 2025, confirming strong environmental management.

Greening activities were launched around the site, improving local biodiversity.

CATL already operates ten carbon-neutral plants worldwide. The company expects Debrecen to reach carbon-neutral status within two years of opening, using renewable electricity and installing on-site solar capacity.

Building Local Talent and Creating a Stable Industrial Base

The battery giant has been hiring steadily since 2023. The Debrecen site now employs more than 1,000 people, with two-thirds coming from Debrecen and nearby regions. Recruitment covers a broad range of functions, including production, logistics, quality, finance, IT, and HR.

According to Alexandra Kitta, Head of Recruitment at CATL Debrecen, the company aims to create a modern and stable workplace with strong learning opportunities. CATL offers competitive salaries along with cultural and professional training programs. Employees also gain access to international expertise while building skills in advanced battery technology.

Strengthening Community Connections

Beyond manufacturing, CATL is investing in Debrecen’s cultural and social life. The company supports major local events and brings new traditions to the region, such as the Chinese Lantern Festival and the Mid-Autumn Festival. Community programs focus on children and environmental protection, reflecting its commitment to building long-term relationships with residents.

Germany: Developing Battery Skills Through Training, Industry Links, and the Dual System

Germany plays a major role in CATL’s European strategy. The company is investing heavily in workforce development, technology testing, and partnerships with educational institutions.

New IHK Certificate Course Builds Battery Expertise

At the end of 2025, CATL introduced the IHK-certified course “Basic Battery Technology for Trainees.” This two-week program gives second-year trainees foundational knowledge in areas such as battery safety, sustainability, cell manufacturing, and industry standards.

Nineteen trainees joined the first class. Over time, the course will open to participants from outside the company. Supported through the BatterieMD network, the program includes both hands-on training and digital learning modules that cover the full battery value chain.

This initiative is also an important step toward creating a dedicated battery-technology career path within Germany’s dual vocational system. Despite rising industry demand, Germany still does not have a standardized training track for battery specialists. CATL’s efforts could help shape a modern curriculum that combines theory and practice.

Expanding Testing Capacity in Thuringia

CATL’s training efforts support a growing physical presence in Thuringia. The company began battery cell production in Arnstadt in 2022, its first plant outside China. These cells now power high-performance European vehicles.

Simultaneously, it is also doubling the capacity of its large testing center, which is already certified by Volkswagen for both cell and module testing. The company has invested EUR 1.8 billion in its German operations and employs more than 1,700 people. Training programs focus on chemical processes, Industry 4.0 technologies, and workforce localization.

Deepening Training Partnerships

CATL runs a vocational training center at Erfurter Kreuz and collaborates with key partners, including TÜV Süd, IHK, Debrecen Vocational Training Center, University of Debrecen, and University of Miskolc. Dual study programs and in-house training help build a strong pipeline of skilled workers for Europe’s growing battery sector.

Spain: New 50 GWh LFP Gigafactory with Stellantis

CATL’s expansion reached another milestone with the groundbreaking of a new gigafactory in Zaragoza, Spain. The project is a 50:50 joint venture with Stellantis and will use lithium iron phosphate (LFP) technology. With a capacity of 50 GWh, the plant represents one of Europe’s largest battery investments to date.

Production is expected to begin in late 2026. When fully operational, the factory will supply battery packs for up to one million electric vehicles each year, helping cut more than 30 million tons of CO₂ over their lifetime.

The project includes an investment of up to EUR 4.1 billion and will create more than 4,000 direct jobs. Thousands of indirect jobs are also expected as suppliers and service providers expand around the site.

This gigafactory strengthens Europe’s battery value chain and reflects CATL’s evolution from supplying Europe to operating “in Europe, for Europe.” The Spanish plant will primarily serve Stellantis brands, while the combined Hungary and Spain operations will support a stable European customer base.

Wood Mackenzie expects Europe’s battery storage capacity to climb from about 11 GW in 2024 to 16 GW in 2025, a 45% jump. The firm also projects steady growth through the next decade, with deployments rising at a 9% annual pace and reaching roughly 35 GW by 2034.

Source: Wood Mackenzie

In this space, Germany will remain the largest market, supported by strong utility-scale and commercial demand. But the region also faces grid bottlenecks, more than 500 GW of connection requests, and rising revenue pressure as more projects come online.

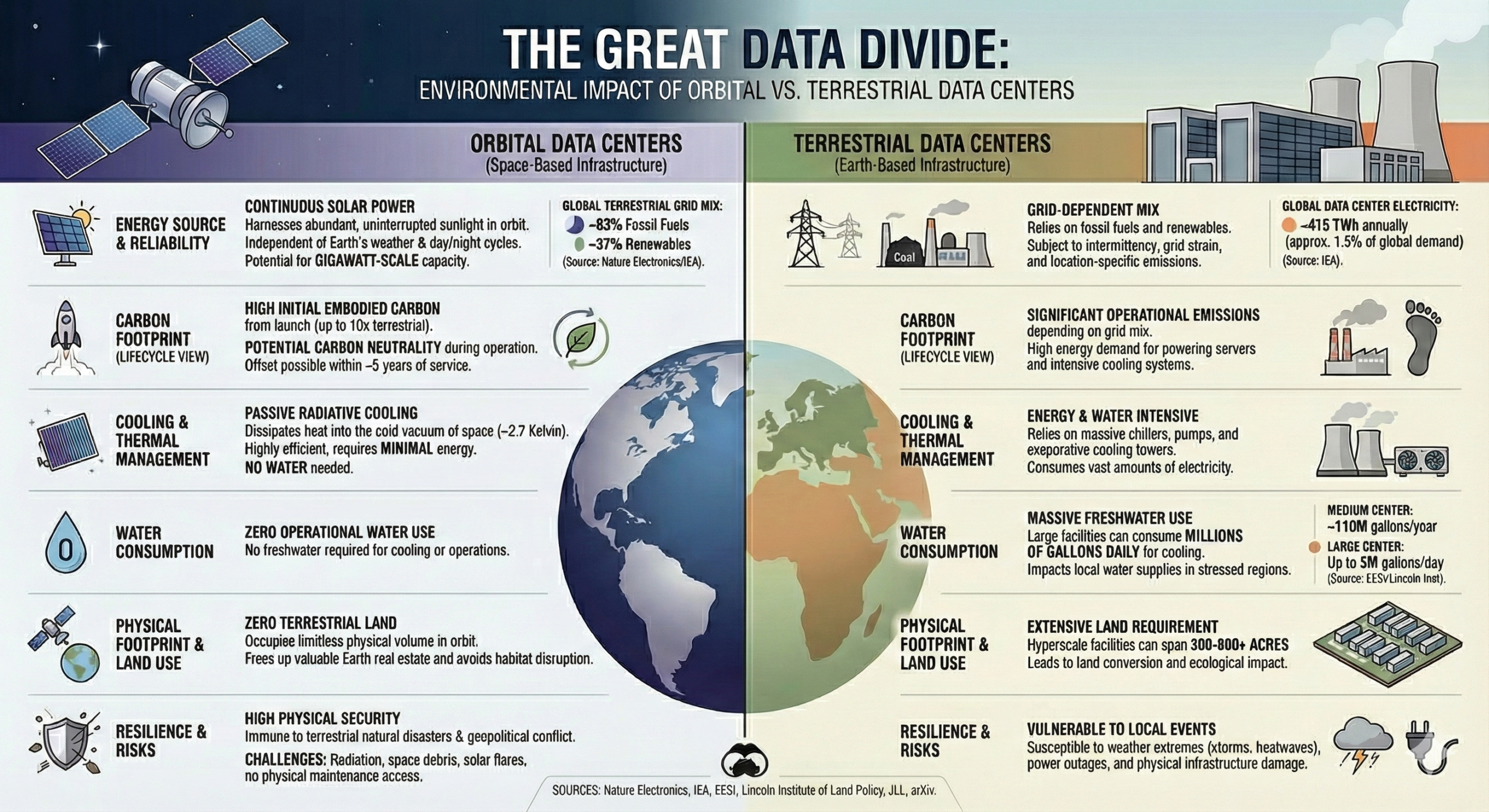

Orbital data centers are a radical rethinking of where and how we process the world’s data. Companies are moving away from building bigger campuses on Earth. Instead, they are designing computing facilities to operate in low Earth orbit and beyond. These systems provide constant solar power and cool naturally to reject heat. Plus, they can process satellite data right on-site. This could tackle some major challenges that terrestrial data centers face today.

The idea has moved quickly from theory to concrete plans. Axiom Space, for example, is planning to deploy orbital data center (ODC) nodes to the International Space Station by 2027. Google has joined the race with Project Suncatcher. This initiative aims to create solar-powered AI data centers in orbit.

Google’s plan includes launching prototype satellites around 2027 equipped with Tensor Processing Units (TPUs). They will run on continuous sunlight and use laser-based communication systems.

The company says orbital solar panels could produce up to 8x more energy than those on Earth. They also believe costs may match those of land-based data centers by the mid-2030s.

Market analysts expect fast growth. The orbital data center market will rise to tens of billions of dollars by 2035. This shows a compound annual growth rate of about 67%. This surge comes from high demand for AI computing, new satellite data, and the push to lower the data center’s environmental impact.

The next sections will explore the technical, environmental, commercial, and geopolitical factors driving this change. They will explain why the decade ahead might determine whether orbital data centers stay niche or become key global infrastructure.

The Rise of Orbital Data Centers

The digital world is expanding at a pace never seen before. Every day, businesses, governments, and individuals generate massive volumes of data. The demand for data processing and storage is skyrocketing. This is driven by AI training models needing a lot of computational power and satellite networks sending terabytes of images back to Earth.

Traditional terrestrial data centers have carried the load so far, but they are reaching their limits. The sheer scale of energy consumption, cooling requirements, and land use is making it harder to sustain growth. This pressure has given rise to a bold alternative: orbital data centers.

The Limits of Earth-Based Data Centers

On Earth, data centers are already among the most energy-intensive types of infrastructure. In the U.S. alone, power demand from these facilities is projected to climb from 17 gigawatts in 2022 to 35 gigawatts by 2030.

The industry could see $2 trillion in global capital spending in the next five years. Half of that will be in the United States. Data centers use more than just electricity. They consume millions of gallons of water each year for cooling. They also take up large areas of land and release a lot of carbon dioxide. This environmental footprint clashes with global climate goals. Many areas are facing water scarcity and grid issues.

The physical expansion of Earth-based data centers also creates tensions with local communities. In parts of the U.S. and Europe, new projects face pushback. This is due to land use issues, water stress, and rising electricity costs tied to large-scale digital infrastructure. As demand continues to rise, these conflicts are expected to grow sharper.

Enter Space-Based Computing

Orbital data centers want to solve these problems by placing processing power in space. These systems use solar energy from space. They don’t rely on power grids on Earth. So, they can work without interruptions from weather or day-night changes.

Orbital centers could cut the environmental impact by eliminating the need for land and water resources. This is a major advantage over Earth-based centers.

The concept is not entirely new. Experiments have already proven that computers can operate reliably in space. Hewlett-Packard Enterprise (HPE) grabbed attention with its Spaceborne Computer project. This project showed that regular hardware can work well on the International Space Station (ISS). This early step showed that data centers could scale to orbital operations. They would need radiation protection, heat dissipation systems, and reliable networking.

Market Potential

What was once science fiction is now a market on the cusp of rapid growth. Analysts expect the orbital data center industry to grow from $1.77 billion in 2029 to $39.09 billion by 2035. This shows a remarkable compound annual growth rate (CAGR) of 67.4%.

Notes: Shows rapid industry expansion with a CAGR of 57.4% driven by AI demands and sustainability

This surge is fueled by multiple drivers:

The insatiable demand for AI and machine learning workloads.

The explosion of satellite constellations is generating enormous amounts of data.

The urgent need for more sustainable, climate-conscious computing.

Advances in reusable rockets and space-based solar power systems are making orbital deployment increasingly feasible.

Cost Comparison

Based on the Lumen Orbit white paper, the cost comparison between orbital and terrestrial data centers is dramatic:

Over a 10‑year span, a 40 MW terrestrial data center would cost about US$167 million, covering energy (~$140 m), cooling ($7 m), water use, backup power ($20 m), etc. Meanwhile, an equivalent orbital setup would cost only ~US$8.2 million, factoring in $5 m for launch, $2 m for a solar array, and $1.2 m for radiation shielding.

This implies space‑based data centers could be roughly 20× cheaper to operate over that timeframe.

Cost Comparison for a 10-year Cycle: Terrestrial vs. Orbital Data Centers

From Vision to Reality

The next few years will be critical in proving the viability of orbital data centers. Companies such as Axiom Space, Google, Starcloud, and China’s ADA Space are already preparing demonstration missions and initial deployments. These projects aim to test hardware. They also show investors and customers that orbital facilities offer real performance benefits.

Axiom Space plans to send an orbital data center module to the ISS by 2027. They aim to grow this with their commercial space station platform. Starcloud plans to launch a GPU-powered satellite in 2025 to test high-performance computing in orbit. ADA Space is launching a bold plan for a 2,800-satellite constellation. This shows how quickly orbital infrastructure can grow.

These efforts mark a shift from theoretical feasibility studies to practical implementation. If they succeed, they could change global digital infrastructure. This would lead to a future where computing isn’t just on Earth, but spread across land and space.

Environmental Promise and Sustainability Benefits

One of the strongest arguments for orbital data centers is their potential to ease the environmental strain created by traditional facilities. Terrestrial data centers use about 1–2% of the world’s electricity. This percentage is rising as more people adopt AI. Cooling systems alone can consume up to 40% of a facility’s power needs.

In addition, many data centers require hundreds of acres of land and millions of gallons of water each year for heat management. These pressures have made the sector a target of regulatory scrutiny and community pushback. Companies think they can greatly reduce these impacts by moving some computing infrastructure into orbit.

Unlimited Access to Solar Power

The most obvious advantage of orbital data centers is access to continuous solar energy. Orbital solar arrays don’t have interruptions from weather or night. Unlike solar farms on Earth, they operate continuously. This means they can deliver a constant and highly efficient power supply. Starcloud and others are planning large solar grids. These grids could stretch up to 2.5 miles and aim to power big orbital data facilities.

For high-performance computing, like AI training, this power source offers faster, cheaper, and more sustainable processing than what we can achieve on Earth.

Cooling in the Vacuum of Space

Cooling is one of the biggest sources of energy waste in terrestrial facilities. Conventional centers use fans, air conditioning, or liquid systems. These can make up almost half of their electricity use.

In orbit, space creates a unique environment. Traditional convection cooling doesn’t work here, so heat must leave through radiation.

Engineers are creating unique radiator panels, heat pipes, and phase-change materials. These tools help control thermal loads in orbital data centers. These systems are complex, but they lack energy-hungry water and air cooling. This could lead to big efficiency gains when scaled up.

Reduced Land and Water Use

Space-based facilities free up land on Earth. This helps avoid conflicts with farming, city growth, or conservation. This is especially important in places like Northern Virginia and Dublin. Data center growth there has led to community pushback about land use and strain on infrastructure.

Orbital centers also sidestep water usage, a growing concern in drought-prone regions such as the American West. By comparison, large data centers use millions of gallons of water each year for cooling. This puts pressure on local water supplies.

Carbon Footprint Reduction

Orbital data centers could reduce dependence on fossil fuel-based electricity by tapping directly into abundant solar power in space. They also eliminate the carbon emissions tied to land clearing and cooling infrastructure.

Research backed by the European Commission shows that orbital data centers may be environmentally friendly. They could offer computing power with a lower carbon footprint than data centers on Earth.

The Trade-Off: Launches and Space Debris

The sustainability equation is not without complications. Rocket launches needed for orbital infrastructure still release a lot of emissions. This includes black carbon particles, which can build up in the upper atmosphere.

Large-scale deployment might increase this footprint. However, reusable launch systems like SpaceX’s Falcon 9 are lowering the cost and emissions for sending hardware to orbit.

Another concern is space debris. With tens of thousands of new satellites projected for launch by 2030, orbital traffic is experiencing significant congestion. Large solar arrays and data hubs represent big targets for collisions with debris traveling at speeds of up to 28,000 kilometers per hour.

Mitigation strategies are key. Debris shields, active cleanup missions, and smart orbital slot management will help. These steps ensure that sustainability gains aren’t lost to new environmental hazards in orbit.

Environmental Impact Comparison: Terrestrial vs. Orbital Data Centers

A Net Positive, if Challenges Are Managed

Taken together, orbital data centers promise major environmental benefits by reducing energy demand, land use, and water consumption on Earth. Launch emissions and orbital debris are concerns, but technology and smart rules can create a positive outcome. If these facilities can scale well, they could be a major innovation in sustainability for digital infrastructure.

Market Landscape and Key Players

The orbital data center market is new, but companies and partnerships are paving the way. These players include space station developers, satellite operators, cloud and hardware firms, and telecom companies. They all compete for a share of a potential multibillion-dollar industry by the mid-2030s.

Their strategies vary, but all aim to address the same challenges while providing real benefits compared to land-based options:

powering,

cooling, and

protecting computing infrastructure in the harsh conditions of space.

Axiom Space: Building the First Orbital Data Hub

Axiom Space is among the most prominent U.S. firms advancing orbital data center capabilities. The company is best known for Axiom Station, which will replace the International Space Station. It also plans to integrate orbital data center (ODC) modules into its future projects. Axiom has received funding to boost its research and development. This includes $5.5 million from the Texas Space Commission.

The company focuses on “Earth independence”, which means data can be stored and processed in orbit. It doesn’t need any ground-based cloud systems.

Axiom teamed up with Kepler Communications and Skyloom Global. Together, they added optical inter-satellite links (OISLs). This upgrade allows fast data transfers between orbit and ground. The first ODC nodes will launch on the ISS by 2027. This will be one of the earliest real-world tests of orbital computing.

Source: Axiom

Starcloud: Scaling Solar-Powered Computing

Another key innovator is Starcloud, which used to be called Lumen Orbit. This startup has raised over $21 million in seed funding: one of the biggest early investment rounds for a Y Combinator graduate. The company’s vision is bold: solar panel grids up to 2.5 miles wide powering megawatt-scale data centers in orbit.

Starcloud’s first demo mission successfully launched in November 2025 on a SpaceX Falcon 9. It carried a 132-pound (60-kilogram) satellite with an NVIDIA data-center-grade GPU. This mission is designed to prove that space can handle demanding computing tasks such as AI inference and training.

Source: Lumin Orbit

If they succeed, the company thinks orbital facilities could be cheaper than Earth-based data centers. This is especially true for processing satellite data and AI tasks that work better near the source.

Google’s Project Suncatcher: Sustainable AI Computing

Google announced this project, which represents the first major move by a global tech giant into orbital computing. The company will launch solar-powered satellites. These satellites have custom TPUs and use laser communication to connect orbital clusters to Earth.

Google’s research shows that solar collection in orbit could be up to eight times more efficient than on Earth. This could provide sustainable AI computing on a large scale. If the prototypes succeed, Google expects to expand toward operational orbital nodes in the early 2030s.

China’s ADA Space: An Ambitious Constellation

China has emerged as a powerful competitor through ADA Space (Guoxing Aerospace). In May 2025, the company launched 12 AI-enabled satellites. This is the first step in a plan for 2,800 satellites. Each satellite has 744 tera operations per second (TOPS) of computing power. They use 8 billion-parameter AI models and feature 100 Gbps laser inter-satellite links.

This project highlights China’s strategic intent to dominate orbital computing. ADA Space processes data in orbit, especially for astronomy and remote sensing. This helps reduce bandwidth issues and speeds up response times. The constellation is more than just a business. It also helps China with its national security and space goals.

PowerBank: A Strategic Contributor

PowerBank Corporation, in partnership with Orbit AI, is developing the Orbital Cloud, a network of AI-enabled orbital data centers. The system combines satellite communication, on-orbit AI computing, and blockchain verification, providing resilient, censorship-resistant services independent of ground networks.

PowerBank supplies advanced solar energy systems, adaptive energy management, and thermal control technologies to power and maintain these orbital compute nodes. The first satellite, DeStarlink Genesis‑1, launched in December 2025, marking the start of the network, with additional nodes planned through 2026 and beyond.

This initiative positions PowerBank at the intersection of renewable energy, AI, and space infrastructure. Analysts estimate the combined market for orbital infrastructure, in-orbit computing, and satellite services could exceed USD 700 billion over the next decade.

OrbitsEdge + HPE: Modular Racks in Orbit

OrbitsEdge has partnered with Hewlett Packard Enterprise (HPE) to design modular, satellite-based data centers. Their SatFrame satellite bus can hold standard 19-inch server racks. It can also scale to support larger hardware.

HPE’s Edgeline Converged Edge Systems show how traditional IT hardware companies are adjusting ground technology for space. This modular approach could allow incremental scaling. This has lower risks compared to large, one-time deployments.

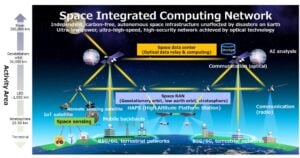

NTT/JSAT Space Compass: Beyond-5G Integration

Japan’s NTT Corporation and Sky Perfect JSAT have teamed up in the Space Compass joint venture. This shows how telecom companies see orbital computing as key to future networks. Their plan connects land, air, and space communication systems. This will support Beyond-5G and 6G connectivity.

Source: NTT

The venture plans to use high-speed optical transmission to connect these layers. This will provide seamless global cloud services. As such, orbital data centers will serve as the backbone for low-latency processing.

European Efforts: Feasibility and Sustainability

Europe is also exploring orbital data centers, though it is earlier in the process. Thales Alenia Space, with help from the European Commission, studied the technology and environmental impact of these systems.

Europe may be behind the U.S. and China in commercial deployments. But its focus on sustainability and regulation might set global standards.

Funding and Strategic Backing

Behind these companies is a growing web of investors and government support. Venture firms like Y Combinator, NFX, FUSE, and Soma Capital are backing startups such as Starcloud. Also, major tech investors like Sequoia and Andreessen Horowitz are interested in orbital computing ventures.

Even the CIA’s venture capital arm, In-Q-Tel, has backed projects in this space. This shows how important orbital data centers are for defense and intelligence.

These investments show confidence that orbital computing will evolve from experimental missions into commercial infrastructure. As demonstration projects show their worth, the sector may attract bigger funding rounds. We could also see more partnerships among aerospace, telecom, and cloud computing giants.

Technical and Operational Challenges

While orbital data centers promise enormous benefits, turning the concept into reality requires solving a set of tough technical and operational problems. Space is a harsh and unforgiving place. Radiation, extreme temperatures, and micrometeoroids constantly threaten electronic systems.

Also, the costs of starting, running, and growing orbital infrastructure create challenges that land-based competitors don’t encounter.

Radiation: The Need for Hardened Components

One of the most critical issues is radiation. Electronic components in space face cosmic rays and charged particles. These can lead to single-event effects (SEEs), memory corruption, and system failures. Commercial off-the-shelf (COTS) hardware, while cheaper and more advanced, is highly vulnerable in orbit.

Radiation-hardened (rad-hard) electronics are tougher. However, they cost more, offer less power, and are often years behind the newest commercial chips.

Google’s Project Suncatcher acknowledges that radiation hardening is key to long-term reliability. This is especially true when using large arrays of TPUs in orbit. The company is testing AI chips that can handle faults. They are also using adaptive software like RedNet AI’s error-correction model, which aims to reduce radiation damage.

Thermal management is equally vital. Google’s research shows that using solar power constantly still faces a big problem. Radiating waste heat in a vacuum is tough to manage. Their proposed solution involves kilometer-scale radiator panels and phase-change systems — technologies also being studied by Starcloud and ADA Space.

Innovative approaches are emerging. Researchers created methods like RedNet. This system is made for deep neural networks. RedNet doesn’t just depend on rad-hard hardware. It also uses the varying sensitivity of AI model layers to manage radiation-induced errors.

Correcting errors in the model’s weak spots leads to nearly zero error rates. This also speeds up inference by 33% compared to traditional methods. Such hybrid strategies could allow orbital data centers to balance cost, reliability, and performance.

Thermal Management in the Vacuum of Space

Cooling is another major hurdle. On Earth, data centers rely on air and liquid cooling systems to dissipate heat. In space, convection does not work in a vacuum — all heat must be radiated away. This is much less efficient and needs special systems, such as large radiator panels, heat pipes, and phase-change materials.

As data centers scale to megawatt power levels, the challenge becomes more extreme. Companies like Starcloud envision orbital facilities with cooling systems stretching kilometers across to shed excess heat.

Designing these systems to run reliably for years without maintenance makes them more complex and expensive. Before orbital data centers can manage workloads like Earth’s biggest facilities, solving thermal management is key.

Space Debris and the Kessler Risk

The growing density of satellites and debris in low Earth orbit (LEO) poses a serious risk. NASA scientist Donald Kessler first described Kessler Syndrome in 1978. It’s a chain reaction in which collisions create more debris, causing even more collisions.

Large orbital data centers, with expansive solar panels and radiator arrays, would be particularly vulnerable. Even tiny fragments, less than a centimeter, can travel up to 28,000 kilometers per hour. They can destroy sensitive equipment.

Operators will need to incorporate shields, redundant systems, and debris-avoidance maneuvers. Still, the risk of serious damage is a big concern for long-term orbital infrastructure.

Launch Economics and In-Space Assembly

Getting heavy, complex systems into orbit is expensive. Current launch costs range from about $7.5 million to $67 million per mission, depending on payload size and orbit. Reusable rockets, like SpaceX’s Falcon 9 and Starship, are cutting costs. However, setting up gigawatt-scale facilities may still need hundreds of tons of hardware.

One solution is in-space assembly and modular construction. Companies could use smaller modules instead of a full facility. They can then piece these modules together in orbit. This incremental approach spreads costs across multiple missions and reduces risk. Longer term, in-space manufacturing could further cut costs by using materials sourced from the Moon or asteroids.

Maintenance Hurdles and Redundancy Needs

Unlike Earth-based facilities, orbital data centers cannot rely on technicians to swap out failing components. Repairs need robotic missions or astronauts. Both options are expensive and complicated. To mitigate this, orbital facilities will need high levels of redundancy and fault tolerance.

This means creating systems that can handle component failures while still operating. This approach adds weight, cost, and complexity. Maintenance challenges will stay a major hurdle for commercial success until autonomous repair systems improve.

Applications and Use Cases

For orbital data centers to thrive, they need to show clear benefits compared to land-based facilities. Building in space has high costs and risks. However, some applications could benefit so much from orbital infrastructure that using it will become necessary. These early use cases, powering artificial intelligence and securing defense systems. show how the market might grow.

AI Training with Continuous Solar Energy

One of the most promising applications is training large AI models, including large language models (LLMs). These workloads need a lot of computing power and constant energy. They often test the limits of Earth’s grids.

Orbital data centers can use constant solar energy in space. They don’t face day-night cycles or weather issues. This enables uninterrupted operations, potentially lowering costs and accelerating model development.

Starcloud’s 2025 mission will test AI training and inference using NVIDIA GPUs in space. This will provide 100 times more computing power than past space demos. In the long run, gigawatt-scale orbital clusters might serve as special platforms for training large AI systems. They could take on the energy-heavy tasks that currently happen on Earth.

Earth Observation and Satellite Data Processing

Today, satellite constellations produce terabytes of data every day. A lot of this data needs to be sent to ground stations for processing. This creates bandwidth bottlenecks and latency issues that limit real-time applications. Orbital data centers solve this problem by processing data in space. They send only useful insights back to Earth.

Research from Tsinghua University shows that using inter-satellite links for data processing can boost system capacity significantly. This is much more effective than traditional downlink methods. This could lead to quicker wildfire detection, better disaster response, and improved environmental monitoring. Plus, it would lower transmission costs.

Defense and National Security

Defense is another high-value use case. Orbital data centers can support missile defense systems, autonomous weapons, and intelligence gathering. Here, even a fraction of a second can make a big difference. Processing data in orbit offers ultra-low latency and global coverage. These benefits aren’t achievable with just terrestrial infrastructure.

Security is also enhanced. Orbital centers are naturally isolated from many physical and cyber threats. Axiom Space has pointed out “Earth independence” as a key feature of its orbital cloud services. This means defense applications stay functional even if ground networks fail.

Disaster Recovery and Data Backup

Orbital and lunar data centers also hold potential for disaster recovery. Lonestar Data Holdings has already shown a lunar payload that can store and retrieve encrypted data. This makes the Moon an ideal backup site. Storing important information in orbit can help protect against natural disasters, political issues, or cyberattacks that could harm data centers on Earth.

This concept echoes the “Library of Alexandria” concern — the idea that without off-world backups, humanity risks losing irreplaceable knowledge in a catastrophe. Orbital data centers may become the ultimate safeguard for digital civilization.

Hybrid Cloud Models

In the near term, orbital facilities are unlikely to replace terrestrial data centers. Instead, they are expected to operate in hybrid systems, where workloads are distributed between Earth and orbit. Advanced optical communication networks will let data flow easily between the two. Placement will be optimized for speed, cost, and security needs.

For instance, AI training could happen in orbit, but customer-facing apps stay on Earth. Satellite data can be processed in orbit. Then, it can be added to cloud platforms on Earth. This hybrid model may prove the most commercially viable, offering the best of both worlds.

Regulatory, Political, and Security Landscape

As orbital data centers move closer to reality, questions of governance, law, and security loom large. Orbital data centers don’t fit neatly under national laws. Instead, they exist in a complex mix of international treaties, national rules, and global competition. Companies venturing into this space must navigate overlapping — and often unclear — legal frameworks.

Data Privacy in Orbit

One of the most pressing issues is data privacy. There is no treaty that specifically governs personal data protection in space. Current laws like the EU’s General Data Protection Regulation (GDPR) apply to any company handling data from EU citizens, no matter where they are located.

U.S. laws also apply to orbital operations. These include HIPAA for health data, the Gramm-Leach-Bliley Act for financial data, and state laws like California’s Consumer Privacy Act (CCPA). Companies must comply with several regulatory rules at the same time, even when in orbit.

Export Controls and Security Restrictions

Orbital data centers must follow rules from the International Traffic in Arms Regulations (ITAR) and the Export Administration Regulations (EAR). Advanced computing systems, radiation-hardened electronics, and satellite technologies are often seen as dual-use or defense-related. This limits international collaboration and may prevent certain partnerships or data-sharing arrangements.

Governments are likely to impose further restrictions as orbital computing becomes strategically significant, particularly for defense and intelligence applications.

Orbital Debris, Licensing, and Traffic Management

The growth of orbital infrastructure adds to existing concerns about space debris. Regulators like the U.S. Federal Communications Commission (FCC) and the International Telecommunication Union (ITU) require companies to develop end-of-life disposal and collision avoidance plans.

Large orbital data centers, with their big solar panels and radiator arrays, will have strict requirements. Licensing rules, debris control, and orbital slot allocation will increase costs and make operations more complex.

Geopolitical Competition

Finally, geopolitics is shaping the orbital data center race. The United States leads in space through companies like Axiom Space, Google, and Starcloud. NASA, the Department of Defense, and venture funding support them.

China, however, is also making big investments in ADA Space’s planned 2,800-satellite constellation. This shows how important orbital computing is for both business and military use.

This rivalry could speed up innovation, but it might also lead to fragmented systems. The U.S. and Chinese orbital clouds may operate side by side.

If governments see orbital computing as a key asset, national security might become more important than working together commercially. This could widen the gap between competitors.

Global Competition Growing: China, Elon Musk, and Amazon Enter the Race

The race to build orbital data centers and AI supercomputers in space is expanding fast. Major tech companies and national programs are now pursuing high-performance computing in orbit.

China is moving quickly. Companies like Zhongke Tiansuan (Comospace) have run space computers on Jilin‑1 satellites for over 1,000 days. Research groups, including the Three-Body Computing Constellation, have launched satellite clusters performing multi-trillion operations per second. The country plans a centralized space data center in dawn-dusk orbit with over one gigawatt of power, rolling out in phases toward a full-scale orbital megacenter by 2035.

Elon Musk’s xAI and SpaceX are exploring AI payloads on Starlink satellites, which could enable distributed orbital computing. Reusable rockets help lower costs and speed deployment. Blue Origin is also developing related technology.

Amazon also aims to extend AWS cloud and AI services into space. Its “Leo” satellite initiative seeks to integrate orbital computing with Earth-based networks, positioning Amazon against both traditional cloud providers and new orbital competitors.

This global competition now includes both state-backed programs and private companies. China’s rapid satellite deployment, Musk’s launch advantages, and Amazon’s cloud ecosystem give each player unique strengths.

As these systems move from prototypes to operational networks, the race will drive innovation, influence regulations, and reshape global computing infrastructure over the next decade. Here is what we can expect in the coming years.

Future Outlook

Orbital data centers are just starting. However, the future looks clearer as technology improves and pilot missions get ready to launch. If costs and risks can be contained, the sector could move from proof-of-concept to mainstream adoption within the next decade.

2025–2030: Demonstrations to Early Operations

The late 2020s will mark a turning point for orbital computing. Axiom’s ISS deployment and Starcloud’s 2025 GPU mission are leading the way. Also, Google’s Project Suncatcher brings strong commercial support. China’s ADA Space constellation is also rolling out in phases, beginning with AI-enabled satellites that can process data directly in space.

Between 2025 and 2030, these demonstrations will test whether AI training and continuous solar power can coexist in orbit. By 2030, the first orbital data centers should be handling some commercial tasks. They will show their worth for AI, Earth observation, and defense uses.

2030–2035: Scaling to Gigawatt-Class Facilities

In the early 2030s, orbital data centers are expected to grow a lot. They’ll shift from small demo payloads to large gigawatt-class clusters. These large facilities will use huge solar arrays that stretch for kilometers. They will also have advanced thermal management systems.

At this stage, orbital computing could play key roles in AI training, global cloud services, and secure government operations. The massive market growth will make orbital infrastructure a key part of the global data economy.

Google’s modeling shows that the cost per kilowatt-year might match Earth-based centers soon. This could be a tipping point for broad adoption. Beyond that, lunar storage projects like Lonestar’s may expand humanity’s computing footprint even further.

Beyond 2035: Lunar Storage and Off-World Infrastructure

After the mid-2030s, orbital data centers may expand to the Moon and deep space. Companies are looking into lunar data centers. They see the Moon as a top choice for storing and backing up digital assets. These lunar outposts could be disaster recovery sites, research hubs, and steps toward interplanetary computing.

As the sector matures, consolidation around successful players is likely. Startups like Starcloud can grow by partnering with or buying established aerospace and cloud computing companies.

Meanwhile, Hybrid Earth-orbit cloud models will likely become the norm. Orbital nodes will work alongside ground data centers. This setup suits energy-heavy or time-sensitive tasks.

The Future of Orbital Computing

Orbital data centers represent one of the boldest ideas in digital infrastructure. By moving computing power into space, they offer solutions to the pressing limitations of terrestrial facilities — from soaring energy consumption and water use to the physical constraints of land and grid capacity.

Orbital data centers could change how and where we process data. They can use continuous solar power, advanced thermal management, and easily integrate with satellites.

If successful, the first orbital data center launch aboard the ISS in 2027 could be remembered as the start of a new era. What once sounded like science fiction is now on the threshold of becoming mainstream — with the potential to transform not only the digital economy but also the environmental footprint of global computing.

Next-generation geothermal energy is moving from the margins to the center of the clean power conversation. Analysts say technology improvements and rising demand for 24/7 clean electricity are opening the door for geothermal to scale in ways that were not possible before. Annick Adjei, senior research analyst for upstream and subsurface carbon management at Wood Mackenzie, summed it up clearly. She said next-gen geothermal was “fundamentally changing the energy landscape” by making a reliable, around-the-clock clean power source available in far more places than before.

That momentum is already showing up in the money. The geothermal sector attracted US$1.7 billion in funding in Q1 2025 alone, a signal of strong confidence from investors looking for firm clean energy solutions. Against this backdrop, Fervo Energy—the leading name in next-generation geothermal—announced the close of its oversubscribed US$462 million Series E round, led by new investor B Capital. The scale of the raise reflects the growing belief that geothermal could play a crucial role in building a fully decarbonized energy grid.

Fervo Gets Funding Boost to Scale the World’s Largest Next-Gen Geothermal Project

The new capital will speed up Fervo’s development plans, especially the buildout of Cape Station in Beaver County, Utah. Cape Station is on track to become the largest next-generation geothermal development in the world. The facility will start delivering 100 megawatts (MW) of firm clean electricity to the grid in 2026. Fervo plans to add another 400 MW by 2028, bringing total capacity to 500 MW.

Construction has been progressing rapidly, driven by significant operational improvements. Drilling times have fallen with every new well, and overall efficiency has climbed. These improvements help bring costs down and reduce development risk, which is critical as utilities and grid operators look for stable sources of clean power.

At the same time, the United States’ power sector is facing a major turning point. Electricity demand is rising rapidly due to electrification, the growth of data centers, and the expansion in advanced manufacturing. Yet supply has not kept pace. This mismatch is creating a once-in-a-generation chance for new energy resources to break in.

Snapshot of Cape Station in Beaver County, Utah

Source: Fervo

Investor Confidence Continues to Rise

Fervo continues to attract top-tier investors who view geothermal as the next scalable zero-carbon resource. The Series E round drew a wide mix of new and returning backers. New investors included AllianceBernstein, Atacama Ventures, Carbon Equity, Climate First, Google, Mitsui & Co., Dr. Kris Singh of Holtec International, and JB Straubel. Returning supporters such as Breakthrough Energy Ventures, CalSTRS, Capricorn Investment Group, CPP Investments, DCVC, Devon Energy, and Mitsubishi Heavy Industries also joined.

Centaurus Capital’s participation was notable. The firm recently made a US$75 million preferred equity commitment to support Cape Station Phase I and also joined the latest round. The ongoing interest highlights how geothermal is increasingly appealing to both climate-focused funds and traditional energy investors.

Geothermal: A Clean Energy Source With Minimal Environmental Footprint

Environmental impacts vary depending on how geothermal energy is used. Direct-use systems and geothermal heat pumps have almost no negative environmental effects and often reduce the need for more polluting energy sources. Even geothermal power plants—which do generate some emissions—produce fewer pollutants compared to fossil fuel plants.

Because geothermal plants don’t burn fuel, emissions are low.

EIA says they release 97% fewer sulfur compounds and around 99% less carbon dioxide than similarly sized coal or gas plants.

Many facilities also use scrubbers to capture hydrogen sulfide from the geothermal reservoir. Most geothermal plants inject used steam and water back underground, which helps renew the resource and keeps surface emissions close to zero.

Fervo Launches a New Standard for Responsible Geothermal Development

As geothermal development accelerates, Fervo is working to ensure that growth happens responsibly. The company introduced the Geothermal Sustainable Development Pact, a new framework outlining best-in-class standards for planning, building, and operating geothermal projects. The Pact includes 37 commitments across six key areas:

Community engagement

Workforce development

Land use

Water conservation and well integrity

Induced seismicity

Emissions

The Pact goes beyond existing regulatory rules and sets a new bar for responsible geothermal scaling. It also builds on the Principles for Responsible Geothermal Development, which Fervo co-developed with the Sierra Club and which has been endorsed by the Sierra Club and the NW Energy Coalition.

Tim Latimer, Fervo’s CEO and Co-Founder, said the Pact came from the belief that the future of energy needs “not just better technology, but better practices.” He emphasized that collaboration with environmental groups will continue as the framework evolves.

Global Capacity and Geothermal’s Path to a Larger U.S. Grid Role

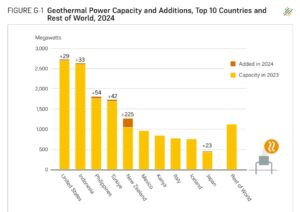

As per REN21’s latest analysis, Global geothermal electricity generation reached 99 terawatt-hours in 2024. During the same year, the world added 400 MW of new capacity, bringing total installed capacity to about 15.1 gigawatts (GW). New Zealand led growth, followed by strong progress in the Philippines, Türkiye, Indonesia, the United States, and Japan.

Source: REN21

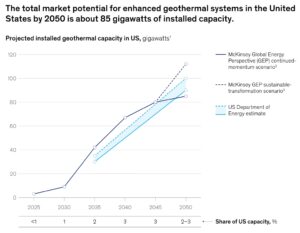

Next-generation geothermal is attracting attention because it addresses one of the biggest barriers facing conventional geothermal: geography. Traditional geothermal depends on rare underground conditions that exist only in certain regions. But improvements in drilling, well design, and subsurface analytics are allowing developers to tap heat resources in many more places.

Moving on, according to McKinsey, falling costs, rapid scaling potential, and strong supply chains could help geothermal become a major part of the U.S. energy mix.

Their analysis suggests next-generation geothermal could supply up to 100 GW of power by 2050, including 40 GW by 2035. That would represent a meaningful share of firm, zero-carbon electricity on the U.S. grid.

Source: McKinsey

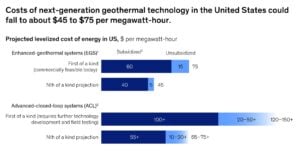

Costs are also expected to drop. Analysts project next-generation geothermal could reach US$45–65 per megawatt-hour for mature, “nth-of-a-kind” facilities within the next decade. While local economic conditions will influence individual project viability, geothermal is expected to outperform other forms of clean, firm power over time.

Source: McKinsey

U.S. Policy, New Wells, and Record Investments Fuel a Geothermal Boom

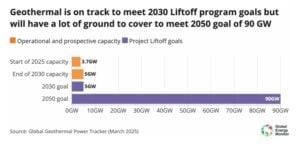

Under the Trump administration, many renewables face challenges, but geothermal could benefit from a “drill, baby, drill” approach, since it shares techniques with oil and gas. With careful policy support, investment in geothermal could grow significantly.

As of 2025, the U.S. holds 23% of global geothermal capacity, leading the world with 3.7 GW in operation. The latest Global Geothermal Power Tracker shows 223 units in development, adding over 15 GW—almost doubling global capacity if completed.

Furthermore, Annick Adjei also highlighted the opportunity: an 80% jump in new wells and nearly US$2 billion in investment show strong confidence in tapping the nation’s vast heat resources. With 500 GW of potential and only 4 GW installed, geothermal could rival traditional oil and gas while delivering always-on, clean power.

To sum up, Fervo Energy, backed by strong investment, is at the forefront of this boom, driving reliable, 24/7 clean energy across the U.S.

More than 230 environmental and public-interest groups asked Congress to halt approvals for and construction of new data centers. They want a temporary national moratorium until federal rules address energy use, water needs, local impacts, and emissions. The request came from Food & Water Watch and was signed by national and local groups across the country.

They said that the fast growth of artificial intelligence (AI) and cloud services is putting big new demands on local grids and water systems. They also said current federal rules do not cover the environmental or social impacts linked to data center growth.

Why the Groups Want a Moratorium

Data centers are using more electricity each year. U.S. data centers consumed an estimated 183 terawatt-hours (TWh) of electricity in 2024. That was about 4% of all U.S. power use. Some national studies project that number could rise to 426 TWh by 2030, which would be about 6.7% to 12% of U.S. electricity, depending on growth rates.

Global data centers used around 415 TWh of electricity in 2024. Analysts expect double-digit annual growth as AI loads increase.

Source: S&P Global

AI-ready data center capacity is projected to grow by about 33% per year from 2023 to 2030 in mid-range market scenarios. Industry groups say global data center capacity could reach over 220 gigawatts (GW) by 2030.

Some groups warn that data center CO₂ emissions might hit 1% of global emissions by 2030. That’s about the same as a mid-size industrial country’s yearly emissions. They say the growth rate is rising faster than the reductions in many other sectors.

An excerpt from their letter reads:

“The rapid expansion of data centers across the United States, driven by the generative artificial intelligence (AI) and crypto boom, presents one of the biggest environmental and social threats of our generation. This expansion is rapidly increasing demand for energy, driving more fossil fuel pollution, straining water resources, and raising electricity prices across the country. All this compounds the significant and concerning impacts AI is having on society, including lost jobs, social instability, and economic concentration.”

When AI Growth Collides With the U.S. Power Grid

Several utilities have linked new power plant plans to data center growth. In Virginia, the largest power company and grid planners see data centers as a key reason for new infrastructure.

In Louisiana, Entergy moved forward with a new gas-plant plan expected to support a large hyperscale data center campus. These cases show how utilities now size new plants with AI-related load in mind.

Some utilities believe these expansions might increase local electricity rates by a few percentage points. This depends on how costs are shared. Regulators in various areas say that extra load can increase distribution and transmission costs. This might lead to higher bills for households.

Several grid operators also report congestion or long waiting lines for new power connections. Northern Virginia, Texas, and parts of the Pacific Northwest now have interconnection queues. In these areas, data center projects make up a large part of the pending requests.

Water demand is another point of conflict. Many large data centers rely on water-cooled systems. A typical water-cooled data center may use around 1.9 liters of water per kWh. More advanced or dry-cooled facilities may use as little as 0.2 liters per kWh, but these designs are not yet common.

One medium-sized data center can use about 110 million gallons of water per year. Large hyperscale sites can use several hundred million gallons annually, and, in some cases, even more. Global estimates suggest data centers could use over 1 trillion liters of water per year by 2030 if growth continues.

Source: Financial Times

These demands have triggered local resistance. In parts of Arizona, California, and Georgia, community groups have raised concerns about water use during drought periods. In some cases, local governments paused or limited data center approvals. A single campus can use more water each year than some small towns.

Trump Plans Executive Order on AI Regulation

While groups push for limits on new data centers, the White House is also preparing an executive order that would reshape AI policy nationwide, as reported by CNN. President Donald Trump has said he plans to issue an order that would block states from creating their own AI rules.

The administration aims to create one national standard for AI. This way, companies won’t have to deal with different state regulations.

Drafts of the plan say the order may tell federal agencies to challenge state AI laws. This could happen through lawsuits or funding limits if the laws clash with federal policy. Supporters say a unified national rule could help U.S. companies compete globally and reduce compliance costs.

State leaders and consumer protection groups argue the opposite. They say states have a legal right to pass their own rules on privacy, safety, and data use. Some governors argue that an executive order cannot override state laws without action by Congress. Minnesota lawmakers, for example, continue to write their own AI bills focused on deepfakes and child-safety concerns.

The debate adds another layer to the data center issue. AI systems require massive computing power. If AI keeps growing quickly, analysts expect even heavier pressure on local grids and water systems. Advocacy groups say that this makes federal regulation more urgent.

Scale of AI and Hyperscale Build-out

The U.S. is in the middle of a major build-out of hyperscale and AI-optimized data centers. Industry trackers report that hundreds of new hyperscale facilities are planned or already under construction through 2030. Many of these campuses are designed specifically for AI training and inference workloads.

Major cloud and social media companies have sharply increased capital spending to support this build-out. Amazon, Google, Microsoft, Meta, and other major platforms, combined spending on AI chips, data centers, and network upgrades reached hundreds of billions of dollars per year in the mid-2020s. These spending levels signal how fast demand is growing.

Some experts track how major technology firms have changed over time. For example, one big cloud provider said its data center electricity use has more than doubled in the last ten years. This increase happened as its global reach grew. This gives a sense of how long-term trends feed current infrastructure pressures.

AI also adds new layers of demand. Training one large AI model can use millions of kilowatt-hours of electricity. Operating a popular chatbot can require many megawatt-hours per day, especially at peak traffic.

Research shows that processing one billion AI queries uses as much electricity as powering tens of thousands of U.S. homes for a day. This varies with the model’s size and efficiency.

Cities and States Move Faster Than Washington

Local governments have acted faster than federal agencies to respond to public concerns. More than 100 counties and cities have passed temporary moratoria, zoning limits, or new environmental rules since 2023. Examples include parts of Georgia, Oregon, Arizona, and Virginia, where communities plan to evaluate energy and water impacts before approving new projects.

Advocacy groups also argue that federal standards have not kept up. The U.S. does not have national energy-efficiency rules for private data centers. It also does not require detailed, mandatory reporting on energy, water, or emissions for the sector. The groups pushing for a moratorium say Congress must update these policies before more sites break ground.

What the Debate Means for 2026 and Beyond

Congress will review the environmental groups’ request in the coming months. Lawmakers are expected to weigh economic benefits against rising tensions around energy, water, and local resources. At the same time, the White House may release its AI executive order, which could shape how states and companies set their own rules.

With rapid AI growth, rising electricity use, and expanding data center construction, both debates are likely to continue through 2026. Many experts say long-term solutions will require national standards, better reporting, and closer coordination between states, utilities, and federal agencies.

ExxonMobil published its updated 2030 Corporate Plan, which keeps the company’s “dual challenge” approach. The oil giant says it will supply reliable energy while cutting emissions. The update raises lower-emission spending, while also forecasting higher oil and gas production to 2030.

Billions in Motion: ExxonMobil’s Financial and Production Targets

ExxonMobil plans about $20 billion of lower-emission capital between 2025 and 2030. It says the $20 billion targets carbon capture and storage (CCS), hydrogen, and lithium projects.

The company projects ~5.5 million oil-equivalent barrels per day (Moebd) of upstream production by 2030. Exxon also forecasts ~$25 billion of earnings growth and ~$35 billion of cash-flow growth by 2030 versus 2024 on a constant price-and-margin basis.

The oil major gives a range for cash capex. It shows $27–29 billion for 2026 and $28–32 billion annually for 2027–2030. The updated plan highlights about $100 billion in major investments planned for 2026–2030. It notes these projects could bring in around $50 billion in total earnings during that time.

Source: ExxonMobil Updated 2030 Plan

Low-Carbon Plan: $20B for CCS, Hydrogen and Lithium

ExxonMobil describes the $20 billion as focused on three business lines:

The company says roughly 60% of the $20 billion will support lower-emissions services to third-party customers. It estimates new low-carbon businesses could deliver ~$13 billion of earnings potential by 2040 if markets and policies develop as expected.

Source: ExxonMobil

Exxon’s updated Corporate 2030 Plan lists current and contracted CCS volumes. The company reports about 9 million tonnes per annum (MTA) of CO₂ capture capacity under contract for its U.S. Gulf Coast network. Key project entries include:

Linde — Beaumont, TX: ~2.2 MTA CO₂, start-up 2026.

Lake Charles Methanol II: ~1.3 MTA, start-up 2030.

Nucor — Convent, LA: ~0.8 MTA, start-up 2026.

The plan also highlights a proposed 1.0 GW low-carbon power/data center project paired with ~3.5 MTA capture, with a planned final investment decision in 2026. Exxon calls its Gulf Coast network an “end-to-end CCS system” and says scale depends on permitting and supportive policy.

Counting Carbon: How Exxon Tracks Methane and Emissions Cuts

ExxonMobil says it is making measurable progress on emissions. The company reports faster-than-expected cuts in several intensity metrics. It states it has already met key 2030 intensity milestones and now expects to meet its methane-intensity target by 2026, four years early.

The company repeats its long-term net-zero framing for operated assets. Exxon’s plan targets Scope 1 and Scope 2 net-zero for its operated assets by 2050. It also sets a nearer target of net-zero Scope 1 and 2 for its operated Permian assets by 2035.

These commitments focus on emissions the company directly controls. They do not include a Scope 3 net-zero pledge for customer use of sold products. Exxon underscores that these goals depend on technology, markets, and supportive policy.

On operational achievements, Exxon highlights large cuts in routine flaring and improved equipment standards. The new plan states that the company reduced corporate flaring intensity by over 60% from 2016 to 2024.

As shown in the chart below, ExxonMobil’s operated-basis greenhouse gas profile shows a clear decline in Scopes 1 and 2 between the 2016 baseline and 2024.

Also, by 2024, Scope 1 emissions dropped to 91 million metric tons CO₂e. Scope 2 emissions (location-based) reached 9 million metric tons CO₂e. Together, this totals 100 million metric tons CO₂e. This is about a 15% reduction from 2016 based on operations.

For the same period, Exxon’s Scope 1+2 emissions intensity dropped from 27.5 to 22.6 metric tons CO₂e per 100 metric tons produced. This shows they are decarbonizing operations, even as production has changed.

The company also hit other flaring and GHG intensity goals ahead of schedule. These outcomes came from replacing old equipment, tightening operations, and limiting routine venting and flaring.

Exxon lists four categories of near-term reduction actions it is scaling up:

Methane control: wider deployment of leak-detection and infrared cameras, more frequent inspections, and accelerated repairs.

Flaring reduction: operational changes and stricter shutdown protocols to cut routine flaring.

Efficiency and asset management: project design improvements, digital optimization, and selective asset sales or retirements to lower average carbon intensity.

CCS and low-carbon services: building capture hubs (about 9 MTA of contracted CO₂ capacity on the U.S. Gulf Coast) and contracting capture services for industrial customers.

The plan also names specific technology and program investments. Exxon highlights advanced sensor networks and real-time emissions monitoring. They also focus on expanding data systems to track and verify reductions. It expects these tools to improve measurement accuracy and speed up corrective action.

Limits and caveats appear repeatedly. Exxon links its long-term net-zero goal to several factors. These include market formation, policy incentives like tax credits and carbon pricing, and permitting timelines. The company warns that total emissions and some asset outcomes will change with production levels and energy demand.

In the near term, key metrics to watch include:

2026 methane-intensity and flaring disclosures.

Volumes of CO₂ captured and stored as Gulf Coast CCS projects launch.

The pace of FID and execution for the 1.0 GW / 3.5 MTA low-carbon power and capture project.

These will show whether Exxon’s claimed progress converts into sustained emissions declines.

Fueling the Future: Rising Oil & Gas Output Through 2030

Exxon projects higher hydrocarbon output even as it invests in low-carbon businesses. The plan targets ~5.5 Moebd by 2030. The company expects ~65% of production to come from advantaged assets such as the Permian Basin, Guyana, and select LNG.

Permian growth is a core part of the supply outlook. Exxon expects roughly 2.5 Moebd from the Permian by 2030, up materially from 2024 levels. Guyana’s Stabroek Block is another major growth driver.

Exxon plans multiple new offshore start-ups in Guyana before 2030. The company argues that these barrels deliver lower operational carbon intensity compared with many older fields.

Critics say rising production risks locking in fossil reliance. Environmental groups, including the Sierra Club, called the plan inconsistent with a 1.5°C pathway. Exxon responds that the world will need oil and gas for decades and that its strategy balances supply security with emissions reduction. Reuters reported split investor and market reactions when the plan surfaced.

Investor Radar: Metrics to Track Exxon’s Low-Carbon Rollout

ExxonMobil links the pace of low-carbon roll-out to policy, permitting, and market formation. Key near-term items to watch include:

Final investment decision and execution of the 1.0 GW / 3.5 MTA project in 2026.

Gulf Coast CCS volumes will actually be placed into service in 2026–2030.

Methane-intensity disclosures in 2026 to confirm earlier achievement claims.

Market analysts noted Exxon’s plan targets improved earnings and cash flow through 2030 while retaining tight capital discipline. Some news channels highlighted that the company raised its earnings and cash-flow outlook to 2030 without raising total capital allocation.

ExxonMobil’s 2030 Corporate Plan balances growth and green ambition. With $20 billion dedicated to CCS, hydrogen, and lithium, the company aims to cut emissions while increasing oil and gas output.

Success will depend on technology, policy support, and timely project execution, making the next few years critical for investors and stakeholders tracking both energy transition and production growth.

Since early 2023, Chinese companies have pledged more than $180 billion for clean energy projects outside China, according to a report by Climate Energy Finance. These firms produce most of the world’s solar panels, batteries, and electric vehicles. They invest in full supply chains, from mining to recycling, helping other countries build green power systems.

China drives this change with large factories, low costs, and strategic planning. Leaders encourage firms to go global, focusing on places with big energy needs and signing agreements to share technology.

The result is a major shift in energy and trade flows. Developing nations in Asia, Africa, Latin America, and the Middle East are becoming key hubs for green industries.

China Leads Global Clean-Tech Production

China dominates new clean energy plants. From 2018 to 2024, it controlled 80% of new solar, wind, battery, and hydrogen facilities worldwide, per the CEF report. Companies such as CATL and BYD set the pace, exporting billions in technology yearly.

Chinese investments cover complete supply chains. Mines, factories, battery plants, recycling centers, and renewable energy projects are all linked. By building such integrated systems, China ensures efficiency, scale, and long-term influence.

Trade agreements and political deals help China expand its reach. Firms get faster approvals, and pacts often include tech-sharing. These moves reshape how energy is produced, consumed, and traded globally.

In a separate report from SNE Research, China controls about 69% of the global electric-vehicle (EV) battery market in 2025. This dominance reflects the country’s strong control over battery supply chains, from material sourcing to manufacturing.

As a result, Chinese firms now significantly influence global battery prices, standards, and EV supply worldwide.

Targeting the Global South: Jobs, Tech, and Energy

Over 75% of China’s projects go to developing nations, and many align with the Belt and Road Initiative. The country selects locations with strict rules, clear policies, and high energy demands.

Source: CEF

Chinese companies often form joint ventures with local partners. This approach shares jobs, skills, and technology. Governments support the investments with loans and incentives. Private companies lead the push, but state backing ensures that projects move quickly.

New investments reduce energy costs and create thousands of jobs. Countries see faster industrial growth and benefit from upgraded grids and green exports. China also adapts to local rules, meeting requirements for local labor, content, or training to secure contracts.

Southeast Asia: Batteries, EVs, and Solar Take Off

The world’s biggest emitter is making major moves in Southeast Asia. In Indonesia, CATL is building a $6 billion battery complex in West Java. The plant produces 6.9 GWh per year using nickel from local mines. Recycling units close the loop, and over 10,000 jobs will be created.

In Malaysia, EVE Energy invests $1.2 billion in energy storage, while BYD plans EV factories for cars and buses. GCL Technology also supports solar farms across the region. With these, trade with China is hitting new highs.

Thailand gets battery production from Sunwoda, a $1 billion plant with training centers. Moreover, Changan adds EV research sites, partnering with local firms. As seen in the chart below, the majority of the global battery manufacturers are Chinese firms.

Chart from CEF

China also uses tax breaks and fast permits to accelerate projects. Local content rules help create steady supply chains. These moves double trade with China and upgrade regional energy grids quickly.

Middle East Goes Green: Solar, Wind, and Hydrogen

China supports Middle Eastern countries in shifting away from fossil fuels. In Saudi Arabia, Shanghai Electric joins a $1.1 billion solar farm, powering 1.5 million homes. ACWA Power trains local staff in China.

Meanwhile, in Morocco, Gotion builds a $5.6 billion battery factory for Europe and local markets. Joint labs create green materials with a 100 GWh yearly capacity.

In Oman, JA Solar’s $564 million plant is producing 6 GW of solar cells. Also, wind turbine projects complement the country’s energy plans. Egypt gets hydrogen projects from LONGi, and Nigeria signs $8.27 billion in clean energy pacts. China brings full technology stacks, turning deserts into power hubs.

These investments lower energy costs, create jobs, and support ambitious national energy plans.

China Expands in Europe

China also targets European energy needs, especially for batteries. Hungary becomes a hub with CATL’s largest European plant in Debrecen. The site aims to produce 100 GWh per year and runs on green power. BMW is a target customer to source from it, and thousands of jobs are expected.

In Spain, CATL and Stellantis are opening a $4.1 billion plant in Zaragoza, producing 50 GWh of batteries starting in 2025. France hosts AESC’s Douai factory, with a target capacity of 40 GWh by 2030. Investments also reach Portugal and Slovakia to avoid EU tariffs.

China brings training programs and research centers, too. Partnerships help local firms gain knowledge and strengthen EV supply chains.

With all these, Europe benefits from faster compliance with car electrification rules by 2035.

In this region, China reshapes Brazil’s auto industry. BYD converts a Ford plant into the region’s largest EV hub, producing 150,000 cars in the first phase. Local steel is used, and later phases add battery production.

Notably, Envision develops a net-zero industrial park, including hydrogen and sustainable aviation fuels.

Wind, solar, and hydro projects expand with Chinese partnerships. China Three Gorges develops hydro plants, while grids are upgraded. As such, energy costs drop by 20%, accelerating green transitions in the region.

A Global Strategy with Local Benefits

China’s clean-tech expansion spreads soft power through technology. Research centers abroad train STEM workers, while new agreements ensure long-term cooperation.

A series of high-level bilateral deals were formed in 2025, linking China to emerging nations in Asia, Africa, Latin America, and the Middle East. Investments grew by 80% in just one year, and local partners led sales and operations, building trust and reducing tensions.

Source: CEF

The Global South, therefore, benefits from cheaper energy, industrial growth, and faster decarbonization with all these projects. Chinese firms remain at the core, guiding global clean-tech supply chains and speeding the transition to net-zero emissions.

China’s Clean-Tech Reach Is Global

China’s $180 billion clean-tech push is reshaping global energy and trade. It creates jobs, reduces energy costs, and spreads green technology. Developing nations gain industrial capacity and know-how while China secures a strong position in global supply chains and expands its influence.

However, careful management is essential. Host nations must enforce local rules, train workers, and build long-term capacity. If done correctly, these investments accelerate global net-zero goals and shift industrial power toward the Global South.

China’s strategy shows that clean energy is not just a domestic goal; it is a global project with wide-reaching economic and environmental impacts.

Silicon Valley startup CarbonZero.Eco reached a major milestone by completing its first commercial biochar facility in Colusa County, California. At the same time, the company signed a landmark carbon credit deal with Climeworks, one of the world’s most trusted carbon removal companies. This deal positions CarbonZero.Eco as a rising player in the fast-growing carbon removal market.

CarbonZero.Eco Teams Up with Climeworks

Climeworks is known globally for its high-quality carbon removals, especially through direct air capture. By partnering with CarbonZero.Eco, Climeworks now adds biochar-based, nature-driven carbon removal to its portfolio. This combination brings together biochar’s natural carbon storage with Climeworks’ tech-based solutions, thereby boosting credibility and offering verified carbon credits to premium buyers.

The deal highlights the strength of CarbonZero.Eco’s technology. While pricing and volumes were not disclosed, the partnership opens doors to high-end buyers and reinforces CarbonZero.Eco’s market reputation.

Climeworks already works with companies like TikTok and NYK. TikTok, for example, is committed to 5,100 tons of carbon removals through 2030, including biochar. Climeworks sees biochar as cost-efficient, scalable, and immediately deployable, with benefits like healthier soil, improved water retention, and lower emissions from agricultural waste.

Why Biochar Matters

Globally, agriculture produces more than 1.5 billion tons of waste every year. Much of it is burned or left to rot, releasing CO₂ and other pollutants. These practices alone contribute about 3% of global greenhouse gas emissions.

Biochar offers a cleaner alternative. Heating agricultural waste in low-oxygen conditions turns it into a stable form of carbon that can last hundreds or even thousands of years. It keeps CO₂ out of the atmosphere and produces a nutrient-rich soil amendment. Over 6,000 studies confirm biochar improves soil fertility, structure, and crop yields.

CarbonZero.Eco is applying biochar in California’s almond industry. Almond shells normally decompose in about two years, releasing carbon. By converting them into biochar instead, the company expects to prevent up to 1.5 million tons of CO₂ emissions.

Scaling Biochar in the Central Valley

The new Colusa County plant is CarbonZero.Eco’s first major production facility. It sits next to almond shell stockpiles, eliminating the need to transport raw material. This lowers emissions and makes the process efficient.

At full capacity, the kilns can produce 30,000 tons of biochar per year, about five times more than most existing technologies. The biochar will be mixed into compost and used by partner farms to enrich soils for future crops.

The facility also helps conserve water. Over 500 aquifers in the Central Valley are drained annually, causing land to sink. Some areas have dropped nearly a foot in a single year. Biochar-amended soils hold 20% more water, reducing irrigation needs and helping stabilize groundwater.

Harper Moss, Founder and CEO of CarbonZero.Eco, said:

“This facility represents a major step toward making carbon-negative agriculture both practical and profitable. By placing our first plant directly where agricultural waste is generated, we’re creating a closed-loop system that benefits farmers, the environment, and the climate. Our mission is to empower American farmers to enhance soil health, improve crop yields, and unlock new revenue streams—while removing atmospheric CO₂ at scale through next-generation biochar production.”

Silicon Valley Backing and Farmer Trust

CarbonZero.Eco emerged from stealth last year with multi-million-dollar backing from leaders at Google, Meta, Amazon, and other tech executives. Since then, it has partnered with hundreds of almond farms across Colusa and Yolo Counties. These farms will divert waste away from landfills and decomposition.

Farmers benefit directly. Biochar stores carbon for centuries, improves water retention, enhances soil health, and boosts crop yields. What used to be waste now becomes both an environmental and financial asset.