A new regulatory filing in the European Union shows that several major carmakers will not join the 2026 carbon credit pool led by Tesla. The filing lists Stellantis, Toyota Motor Corporation, and Subaru Corporation as absent from the Tesla-led alliance for the coming compliance year.

The change highlights an important shift in the European auto market. Carbon credit trading has become a major financial lever for electric vehicle makers, especially Tesla. At the same time, legacy automakers are investing heavily in electric and hybrid vehicles to reduce their dependence on regulatory credits.

EU Filing Reveals Breakup in Tesla’s Carbon Credit Alliance

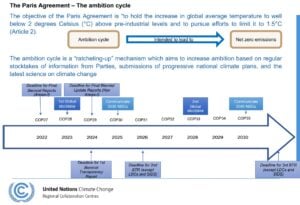

The European Union allows automakers to join “emissions pools” to meet strict fleet-wide carbon targets, as shown below. In these alliances, companies combine their fleets when regulators calculate average CO₂ emissions.

Carmakers with high emissions can offset them by joining a pool led by a low-emission manufacturer such as Tesla.

According to an EU filing dated February 27, 2026, Tesla is recreating its carbon credit pool for the year. However, Stellantis, Toyota, and Subaru are not currently listed as members.

The absence marks a change from 2025. That year, the Tesla pool included a large group of automakers: Tesla, Stellantis, Toyota, Subaru, Ford, Honda, Mazda, Suzuki, and Leapmotor. These partnerships helped companies comply with EU emissions targets while their EV production ramped up.

For 2026, the pool appears smaller. Current participants include Tesla alongside Ford Motor Company, Honda Motor Company, Mazda Motor Corporation, and Suzuki Motor Corporation.

However, companies can still join later. Automakers are allowed to enter pooling agreements until December 2026, leaving the door open for changes during the year.

How Tesla Turns Carbon Credits Into Billions in Revenue

Tesla’s role in carbon pools comes from its all-electric lineup. Since the company sells only zero-emission vehicles, its fleet emissions are far below EU regulatory limits. This creates excess regulatory credits. Tesla can sell those credits to other automakers that struggle to meet the limits.

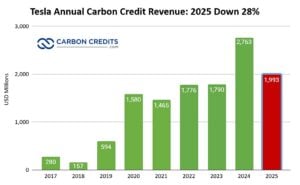

Globally, Tesla has earned nearly $2 billion in 2025 from emissions credits, according to its report filings. The EV maker has earned a total of around $12.4 billion since 2017.

These revenues have historically played an important role in Tesla’s profitability. In several earlier years, regulatory credits accounted for a large share of the company’s net income.

In Europe alone, analysts previously estimated that Tesla’s pooling arrangements could generate more than €1 billion in annual credit revenue. For traditional automakers, buying credits is often cheaper than paying regulatory fines.

Under EU rules, companies that fail to meet emissions targets face penalties of €95 per gram of CO₂ above the limit for every car sold. This can add up quickly for large manufacturers selling millions of vehicles each year.

Carbon credit pooling, therefore, acts as a compliance bridge while companies transition their fleets to electric vehicles.

Why Some Automakers Are Leaving the Pool

The absence of Stellantis, Toyota, and Subaru from the 2026 pool may reflect several strategic changes across the industry.

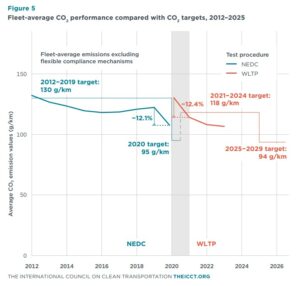

First, the European Commission adjusted the compliance timeline. Instead of assessing emissions strictly for 2025, regulators now allow compliance based on the average emissions between 2025 and 2027.

This change gives automakers more flexibility. Companies that expect their emissions to fall in the next two years may decide they no longer need to buy credits immediately.

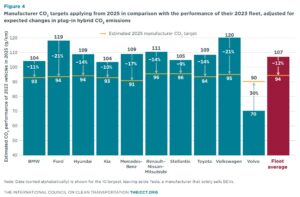

Second, many legacy manufacturers have expanded their production of hybrid and electric vehicles. For example:

- Toyota has one of the world’s largest hybrid fleets.

- Stellantis has expanded its EV lineup across brands such as Peugeot, Opel, Fiat, and Jeep.

- Subaru sells hybrid vehicles and is developing more EV models with Toyota.

These changes could reduce their reliance on Tesla’s credits in the short term. There are also corporate partnerships reshaping the market. Stellantis has a joint venture with Leapmotor, which sells EVs in Europe and could help offset emissions within the group.

Europe’s Strict Climate Rules Are Reshaping the Auto Market

The EU has some of the world’s strictest vehicle climate rules. Under the bloc’s current standards, automakers must steadily cut average fleet emissions. These targets support the EU’s broader climate goal of reducing greenhouse gas emissions 55% by 2030 compared with 1990 levels.

The long-term objective is even more ambitious. The EU plans to phase out sales of new gasoline and diesel cars by 2035, effectively shifting the market toward zero-emission vehicles.

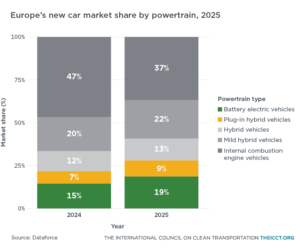

As a result, the European EV market has grown rapidly. Battery-electric vehicles (BEVs) accounted for 15% in 2024. In 2025, this share rose to 19%, reflecting continued EV market growth amid stricter emissions rules.

Hybrid vehicles also play a large role in the transition. Many manufacturers use hybrids to reduce fleet emissions while EV adoption grows.

Tesla’s EV Dominance Still Anchors the Carbon Credit Market

Despite changes in the credit market, Tesla remains one of the most influential players in the global EV industry. The company delivered about 1.81 million vehicles in 2024, making it one of the largest electric car producers worldwide. However, deliveries dropped to 1.6 million in 2025.

- Tesla’s main models include: Model 3, Model Y, Model S, and Model X.

The carmaker also continues to expand its production footprint. Major factories operate in the United States, China, and Germany. The company’s Gigafactory Berlin-Brandenburg plays a key role in supplying EVs to the European market.

However, BYD has overtaken Tesla in EV sales in 2025, both in the EU market and globally.

As EV adoption rises, the role of regulatory credits may gradually shrink. More automakers will meet emissions targets using their own electric vehicles rather than buying credits. Yet, credits still provide a useful financial buffer for Tesla during the transition period.

Are Carbon Pools a Temporary Bridge for the Auto Industry?

Carbon credit pooling reflects the uneven pace of the automotive transition. Some companies, like Tesla, moved early into fully electric vehicles. Others are still shifting large gasoline and diesel fleets toward cleaner technology.

Pooling allows the industry to comply with regulations while maintaining vehicle supply and avoiding sudden price increases.

Yet, the system may evolve. As more automakers scale EV production, fewer companies will need to buy credits. This could gradually reduce the value of Tesla’s carbon credit business, as the 2025 sales drop shows.

At the same time, tightening climate policies and rising EV demand could create new market dynamics.

For now, Tesla remains at the center of the regulatory credit ecosystem. The 2026 EU filing shows that alliances are shifting, but the underlying system still plays an important role in the global transition to low-carbon transportation.

The coming years will reveal whether carbon pools remain a major financial tool or become a temporary bridge as the auto industry moves toward fully electric fleets.