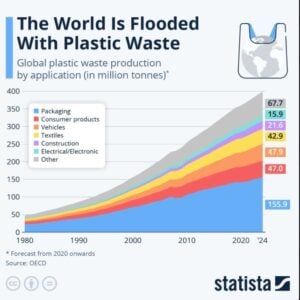

Plastic pollution is one of the greatest environmental challenges facing the world today. As per Verra, every year, more than 430 million tons of plastic are produced, and nearly two-thirds of this ends up as waste—dumped, burned, or abandoned in open spaces, rivers, and oceans.

Without significant intervention, global plastic waste is projected to triple by 2060, threatening ecosystems, economies, and communities alike. Thus, plastic credits are becoming essential tools in sustainable development strategies, particularly in emerging markets.

What Are Plastic Credits and How Do They Work?

Plastic credits are a way to tackle plastic pollution through the market. Individuals and organisations can buy these credits to balance out the amount of plastic they use. The money from these purchases helps fund projects that collect, recycle, or reuse plastic waste—keeping it out of oceans, landfills, and the environment.

This system encourages people and businesses to cut back on plastic use while supporting waste recovery efforts both locally and globally.

This video further explains plastic credits:

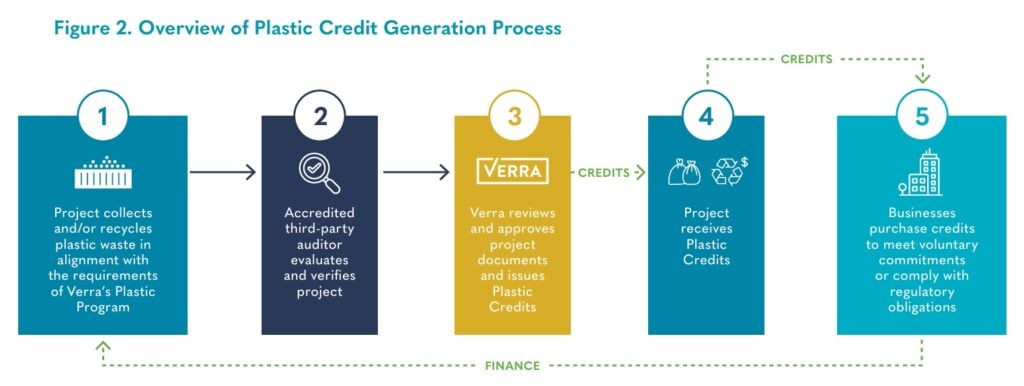

How Are Plastic Credits Created?

Plastic credits are only given for plastic waste that would have harmed the environment if it hadn’t been collected. Projects working with credit organizations gather plastic waste and recycle or process it using methods like:

-

Mechanical recycling

-

Advanced recycling

-

Reprocessing

-

Co-processing

For every extra kilogram of plastic that is recycled or recovered, a certified plastic credit is issued. These credits are checked through records and audits to make sure the plastic waste would have otherwise ended up in the environment without the project’s help.

Moving on to Verra, its globally recognized standards-setting organization ensures credibility, transparency, and impact of plastic credit programs.

This article explores how Verra’s Plastic Waste Reduction Program is transforming waste management, strengthening Extended Producer Responsibility (EPR) systems, and helping countries and businesses alike combat plastic pollution through verified, high-integrity plastic credits.

- ALSO READ: From Plants to Plastics and Carbon Credits

Why Verra’s Work Is Key to Ending the Global Plastic Problem

Plastic pollution has long been a global concern, but its impact is particularly acute in emerging markets and developing economies (EMDEs). These regions face critical gaps in waste management infrastructure, financing, and regulation, which hinder their ability to collect and effectively recycle plastic waste.

Some key challenges include:

-

Lack of collection and recycling infrastructure

-

Funding shortages and limited private investment

-

Weak legal and regulatory frameworks

-

Underrepresentation of informal waste workers

-

Reliance on open dumping and burning of waste

These challenges make it difficult to reduce plastic pollution without external support, technological innovation, and robust governance frameworks.

And in the plastic sector, Verra is leading by creating a global framework for plastic credits that drives waste reduction, community support, and sustainable growth. Its results-based financing channels investments into projects with proven impact, building a cycle of trust and long-term environmental solutions.

Unlocking Verra’s Plastic Waste Reduction Standard

Verra’s EPR Discussion Paper states that its Plastic Waste Reduction Standard is the key to its plastic credit program. It offers a transparent, science-based methodology for tracking and certifying plastic waste recovery, ensuring that projects create real, measurable impact.

The standard is built on four foundational pillars:

1. Measurability and Transparency

Verra’s methodology makes projects document every step of waste collection and recycling. Projects track waste sources, volumes, and weights. They record management practices and verify the chain of custody from collection to recycling.

All data is accessible and traceable. This helps governments, funders, and consumers confidently assess project performance.

2. Impact Verification

Verra requires third-party auditors to validate the waste collection and recycling claims made by projects. These audits confirm that plastic waste would otherwise have been lost to the environment and that the recovery efforts are additional, meaning they would not have occurred without the project’s intervention.

The verification process safeguards against inflated reporting and helps maintain trust in the plastic credit system.

3. Social and Environmental Safeguards

Plastic waste projects often involve communities that rely on informal waste collection for their livelihoods. Verra integrates safeguards to ensure that projects:

-

Uphold human rights and provide fair compensation

-

Offer safe working conditions

-

Respect local environmental and social concerns

By aligning sustainability goals with community development, Verra ensures that projects generate benefits beyond just waste reduction.

4. Market Access and Financing

Verra’s certification enables projects to access both voluntary and regulatory markets. This creates investment opportunities for businesses aiming to offset their plastic footprint while supporting high-impact waste management efforts globally.

How Verra Supports Extended Producer Responsibility (EPR) Systems

Extended Producer Responsibility (EPR) is a policy tool that shifts the financial and environmental responsibility for plastic waste from governments to producers. Effective EPR frameworks incentivize companies to design recyclable products, invest in waste management infrastructure, and reduce their overall plastic consumption.

However, developing EPR systems is challenging, especially in countries with limited resources. Verra helps strengthen EPR systems across three phases:

Phase I – Initiation

During this phase, governments explore EPR as a policy tool and begin building legal frameworks. Verra’s methodologies help producers understand the measurable impacts of waste management, providing data that informs policymaking.

Phase II – Transition

This phase focuses on implementing enforceable regulations and aligning stakeholders. Verra’s third-party audits and reporting tools ensure that data collection is transparent, helping build trust in the early stages of regulation.

Phase III – Maturity

In mature systems, EPR frameworks are fully operational, with clearly defined regulations and robust monitoring mechanisms. Verra’s certifications support scaling waste management solutions by providing financing options and ensuring compliance with international standards.

By integrating plastic credits into EPR systems, Verra helps governments and companies build resilient waste management infrastructures while promoting accountability and innovation.

Making Every Ton Count: Financing Change with Plastic Credits

Plastic credits are only as effective as the financing structures behind them. Verra’s program helps mobilize investments from both public and private sectors, ensuring that projects receive the support they need to scale operations.

Key ways Verra enables financing include:

Bridging Funding Gaps

Plastic credit markets channel investments into waste collection and recycling projects that would otherwise lack access to funding. This is especially important in regions where waste management is underfunded and informal labor plays a significant role.

Results-Based Incentives

By issuing credits only after verified waste recovery, Verra ensures that funds are aligned with real-world impact. Investors and governments alike can be confident that their contributions lead to measurable improvements.

Promoting Innovation

Verra’s framework encourages the development of new recycling technologies, supply chain management tools, and data tracking solutions, helping to modernize waste management practices across sectors.

Encouraging Circular Economy Models

With verified credits, recycled plastic becomes a more valuable commodity, attracting demand and promoting the reuse of materials within production cycles. This supports long-term sustainability and reduces reliance on virgin plastics.

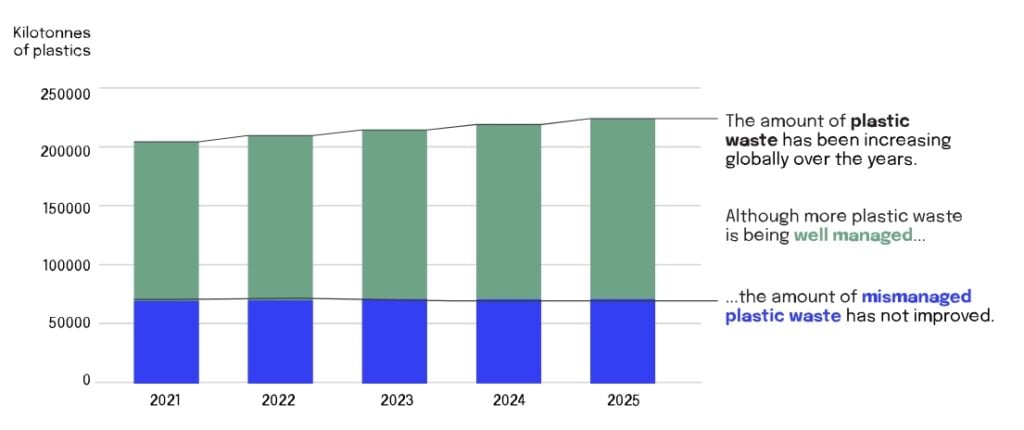

Verra’s Impact Across the Globe

Challenges and the Way Forward

While Verra’s plastic credit program offers promising solutions, challenges remain:

-

Data Quality: Accurate measurement and reporting remain difficult, especially in regions lacking infrastructure.

-

Risk of Misuse: Without strict regulation, companies might offset plastic usage without reducing consumption.

-

Funding Constraints: Infrastructure development requires significant capital, particularly in developing regions.

-

Inclusion of Informal Workers: Waste collection often depends on informal labor sectors, which require support and integration into formal systems.

As read and studied, Verra’s Plastic Waste Reduction Program plays a pivotal role in ensuring that these efforts are credible, verifiable, and impactful. Last but not least, as plastic pollution worsens, Verra leads with accountability and innovation, turning waste into opportunity and responsibility into lasting action.

Partners with American Forest Foundation on Carbon Credits: A Step Toward Its Net-Zero Goal")

Posts Strong Passenger Growth Ahead of Holiday Travel, Bets Big on SAF Future")