Industrial heat production makes up a large share of global emissions. About 18% of all greenhouse gas emissions come from heat used in factories, plants, and manufacturing processes. This type of heat is hard to decarbonize because it often requires high temperatures that are still powered by fossil fuels like natural gas.

To tackle this challenge, AstraZeneca, together with Secaro and ERM, launched the Clean Heat Program. The initiative helps companies measure, plan, and reduce industrial heat emissions across their supply chains.

Rob Williams, Senior Director of Sustainable Procurement at AstraZeneca, said:

“It’s clear that a programme like this is the fastest and most effective way to decarbonise heat in our supply chain. We are long-term partners with Secaro and ERM, and now we’re expanding relationships with peers, buyers from other industries and suppliers to plan, fund and launch the projects that will make heat decarbonisation a reality.”

Industrial Heat: The Hidden Carbon Giant

Fossil fuels still supply most industrial heat energy today. Cleaner alternatives like electrification, hydrogen, or biofuels often cost more. They also require new technology and infrastructure.

Despite its importance, industrial heat has received less focus than clean electricity or transport. In many industries, heat drives fundamental operations, from making chemicals to processing food. Because of this, experts say improving how heat is produced is key to cutting industrial emissions.

Clean Heat Program: Turning Plans into Action

In March 2026, AstraZeneca teamed up with ERM and Secaro to launch the Clean Heat Program. This initiative aims to help companies reduce emissions tied to industrial heat across their supply chains.

By combining data tools, technical support, and financing options, the program aims to make it easier for industrial facilities to adopt low-carbon heat solutions and accelerate decarbonization.

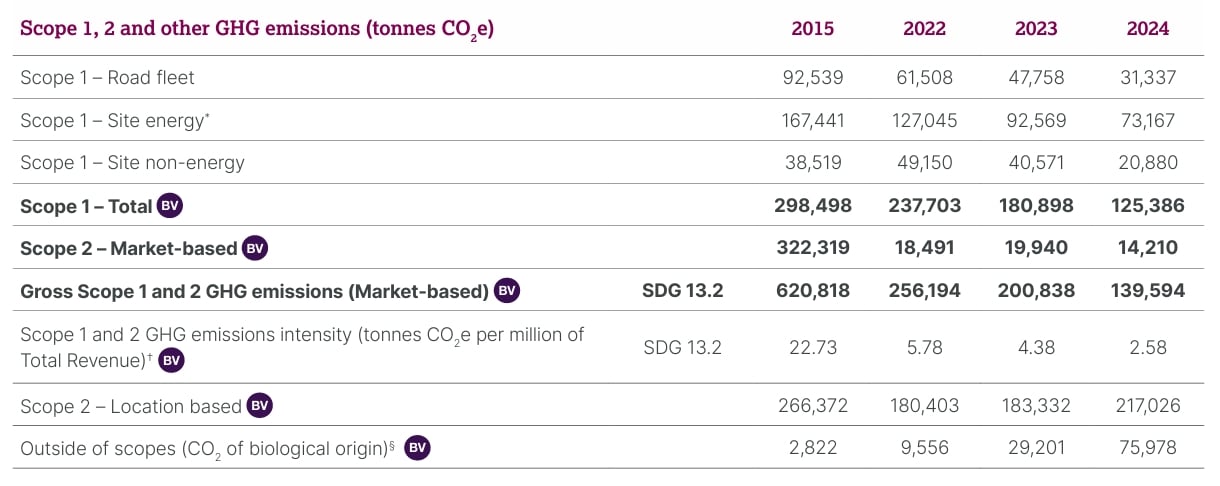

AstraZeneca is joining as a founding partner. The company has its own near‑term climate goals. By 2026, it aims to cut 98% of its Scope 1 and 2 emissions from operations compared to a 2015 baseline.

The pharma giant has already achieved 88.1% reduction by the end of 2025. Its long‑term target is to reach net zero by 2045, including deep cuts in emissions across its suppliers and partners.

The Clean Heat Program is designed to go beyond simple planning. It aims to help companies move from studying options to actually acting on decarbonizing heat.

The program combines:

- Supply chain data tools that show where heat is used and emitted.

- Technical support to find practical ways to reduce emissions.

- Financing options to help companies afford projects that cut heat emissions.

Secaro maps heat emissions across supply chains while ERM designs bankable projects, heat pumps, biomass conversion, and electrification upgrades. Notably, financing leverages EU funds and carbon credit revenue to de-risk upfront costs, moving companies from analysis to implementation.

Unlike many efforts that focus on one plant or site, the program looks at supplier networks. This broader view helps companies pinpoint where changes will have the biggest impact.

Why High-Temperature Heat Is Hard to Replace

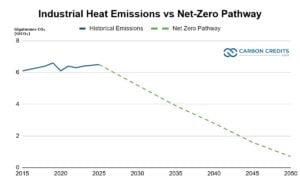

Industrial heat is one of the largest sources of industrial emissions. According to the International Energy Agency, around 70% of industrial energy demand goes to producing heat for processes such as steel, cement, and chemicals.

Estimates from IEA data show that heat-related emissions are about 6.5 gigatonnes of CO₂ each year. This underscores the significant decarbonization needed.

The same analysis suggests that these emissions must drop to less than 1 gigatonne by 2050. This pathway needs quick action from various industries. It also requires strong investment in technology and changes in supply chains to cut emissions in high-temperature processes.

Industrial heat often uses natural gas or other fossil fuels. While electricity can now come from wind or solar, renewable options for high‑temperature heat are still emerging. Solutions such as electrification, biomass fuels, or hydrogen require new equipment and deep planning.

Electrification technologies work for low-temperature heat below 200°C. But industries that need higher heat still rely on fossil fuels. Secaro’s data show that 80% of industrial energy consumption is tied to heat, and 60% of these come from natural gas.

This complexity makes industrial heat one of the hardest parts of decarbonization — even for companies with net‑zero goals. In many cases, heat emissions make up a large share of a company’s direct emissions, known as Scope 1 emissions.

Currently, less than 10% of sites use biofuels or other renewable energy. Industry forecasts suggest that renewable heat may reach only 15% of industrial use by 2028 unless strong action is taken.

Pressure’s On: Regulators, Investors, and Rising Energy Costs

Pressure to cut heat emissions is growing from both regulators and investors. New rules such as the European Union’s Carbon Border Adjustment Mechanism (CBAM) and updated disclosure requirements from the U.S. Securities and Exchange Commission (SEC) require more detailed emissions reporting and climate risk disclosure.

Companies that ignore their emissions might face penalties. They could also lose contracts with buyers who want cleaner supply chains.

Energy price volatility also plays a role. Firms that rely on fossil fuels for heat may face wide swings in energy costs. Decarbonizing heat can help companies stabilize fuel expenses and reduce exposure to price shocks, which investors increasingly watch closely.

Tools and Support for Heat Decarbonization

Secaro’s data platform is central to the program. It now offers heat-specific insights, which show where emissions are highest and highlight chances for change. The platform links buyers, suppliers, and solution providers to highlight high‑impact decarbonization actions.

ERM steps in with its technical expertise. It helps companies assess options and build project plans to attract investment.

These can include:

- Higher energy efficiency

- Switching to low-carbon fuels

- Installing heat recovery systems

- Adopting new technologies, like high-temperature heat pumps

Financing is also part of the program. Many industrial heat projects stall because of upfront costs. The initiative aims to connect companies with financing options, including funds based in the European Union and other mechanisms that help lower financial barriers.

Markets Are Warming Up: Forecasts for Industrial Decarbonization

Efforts like the Clean Heat Program are significant as the market for industrial decarbonization is growing. A recent market outlook projects that global industrial heat decarbonization could grow steadily over the next decade.

From 2025 to 2033, the market is expected to expand at a compound annual growth rate (CAGR) of about 6%, reaching an estimated $380 billion by 2033.

Technologies such as industrial heat pumps are also gaining traction. These devices can reuse waste heat and reduce energy losses. A market forecast shows that the global industrial heat pump market will rise to over 13,150 units by 2035. Revenues may exceed $9.1 billion by that time.

Even though many low‑carbon heat solutions exist, adoption has been slow. For example, only a small share of industrial sites in some sectors currently use renewable heat sources. Without stronger action, forecasts suggest renewable heat may reach only around 15% of industrial heat use by 2028.

A Clear Path for Companies and Supply Chains

The Clean Heat Program offers companies a way to close the gap between their climate goals and the real challenges of industrial heat. It helps companies move beyond early analysis and toward real projects that reduce emissions, improve energy security, and meet investor and regulatory expectations.

For supply chain partners and smaller suppliers, the program can lower barriers to entry. Many small and mid‑tier suppliers struggle to access data, technical support, or financing. This initiative aims to change that by giving a clearer path to decarbonization. If widely adopted, this approach could help reduce significant emissions from industrial heat worldwide and support broader climate goals.